Dale Webster at The Regional has caught CBA out, as despite their promise not to close regional branches while the Senate Inequity is running, they are, by carefully defining down “Regional” to a very narrow definition, conveniently leveraging the ABS definitions, despite elsewhere calling these same regions Regional.

The Senate needs to hold CBA to account here. Write to your Senator, and also CBA management. This is plainly not acceptable nor within the spirit of their earlier statement! Well done Dale!

http://www.martinnorth.com/

Go to the Walk The World Universe at https://walktheworld.com.au/

Digital Finance Analytics (DFA) Blog

CBA Breaks The Pledge To Pause Regional Bank Closures! [Podcast]

Australia’s biggest bank is suggesting people should team up together to buy property to relieve the affordability problem, and they offer a particular structure to do this. However, the risks of this approach are considerable – even worse than using the Bank of Mum and Dad, and their justification is tenuous give the small survey they are basing their releases on. A classic example of buyer should beware.

Housing affordability is a structural issue created by 30 years of bad policy. The approach of encouraging more people to borrow, despite the risks is concerning, and it does nothing to tackle the real underlying issues.

Personally I think it is irresponsible!

Go to the Walk The World Universe at https://walktheworld.com.au/

CBA has partnered with one of the world’s largest regulated crypto exchanges and custodians, Gemini, and leading blockchain analysis firm, Chainalysis. Both partnerships have allowed the bank to design a crypto exchange and custody service that will be offered to customers through a new feature in the app.

The pilot will start in the coming weeks and CBA intends to progressively rollout more features to more customers in 2022. CBA will provide customers with access to up to ten selected crypto assets including Bitcoin, Ethereum, Bitcoin Cash and Litecoin.

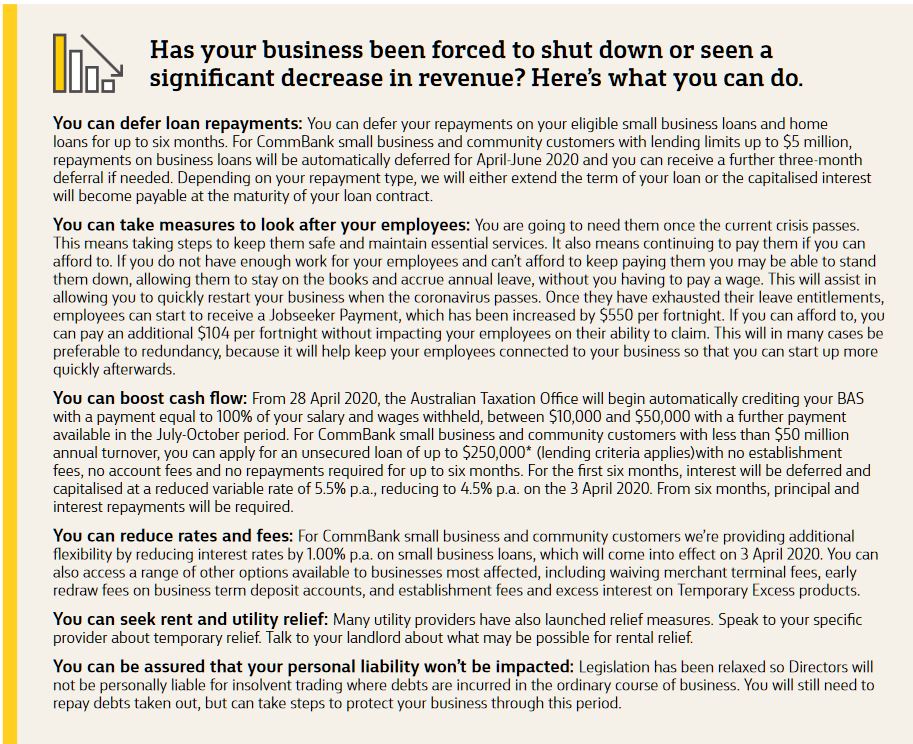

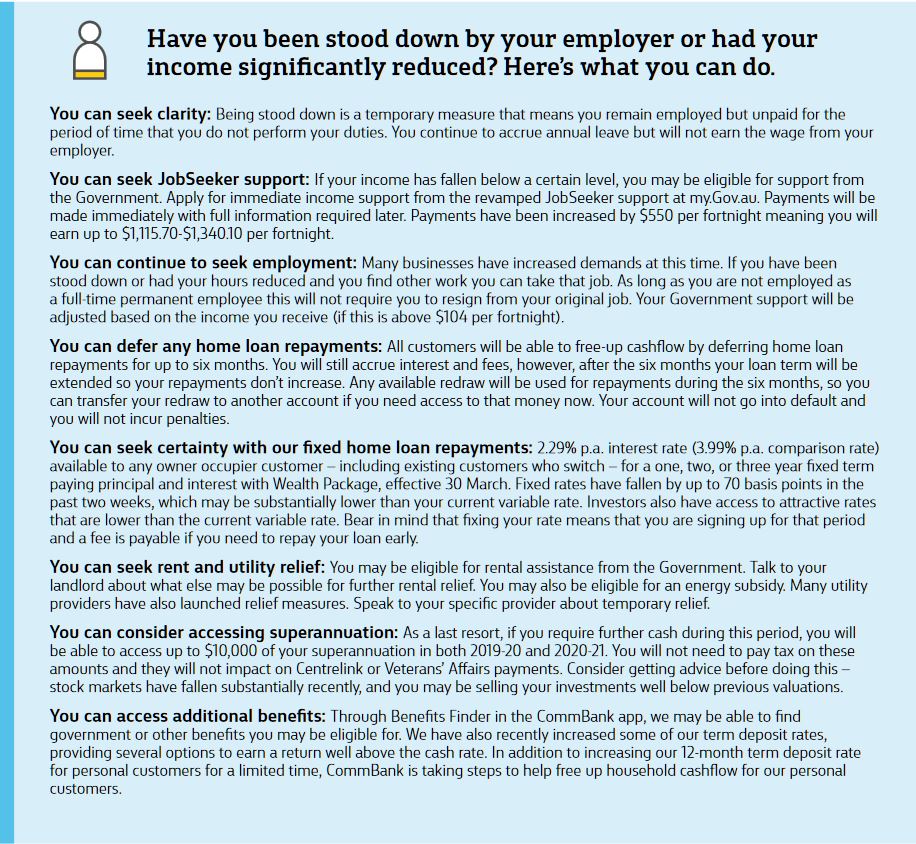

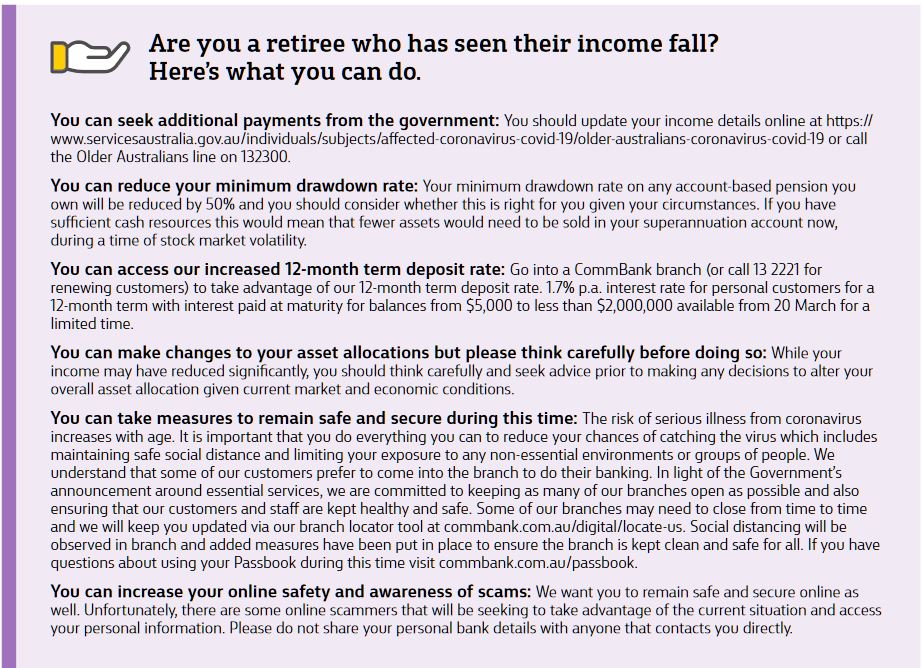

A large scale communication campaign has been launched by CBA to clearly address customers’ most common questions and concerns. It is one of the clearest I have seen yet, and provides some really helpful advice. Kudos to them on their Financial Guide for Customers.

In what is a concerning and confusing time for many Australians, Commonwealth Bank is launching a mass coronavirus communication campaign from today, across all mainstream and social media channels, to help customers access the support and information they need.

CBA’s financial assistance contact centres are currently receiving up to eight times the usual call volumes with a significant number of customers wanting information on how to access support from CBA as well as the recently announced Government assistance measures as they face job loss and business closures.

This new campaign, centred on a detailed Financial Guide for Customers, aims to provide clear, concise, consistent and reliable information to help customers navigate the large volume of recent announcements, as they try to comprehend what support they are eligible for and how to access it quickly.

Customers are also looking for reassurance as well as the tools that will help them regain control of their financial wellbeing.

With the Federal Government designating banking as an essential service, Commonwealth Bank intends to keep as many of its branches open as possible while also encouraging customers to use digital banking for all banking needs other than those for which a visit to a branch is unavoidable. Branches have a range of safe distancing, health and hygiene measures in place.

At such an important time for customers in need, CBA will do whatever it can to help keep as many businesses afloat, as many people in jobs, and as many people in their homes, as possible.

The new Financial Guide will be regularly updated in its easy-to-read format and is available at www.commbank.com.au/coronavirus.

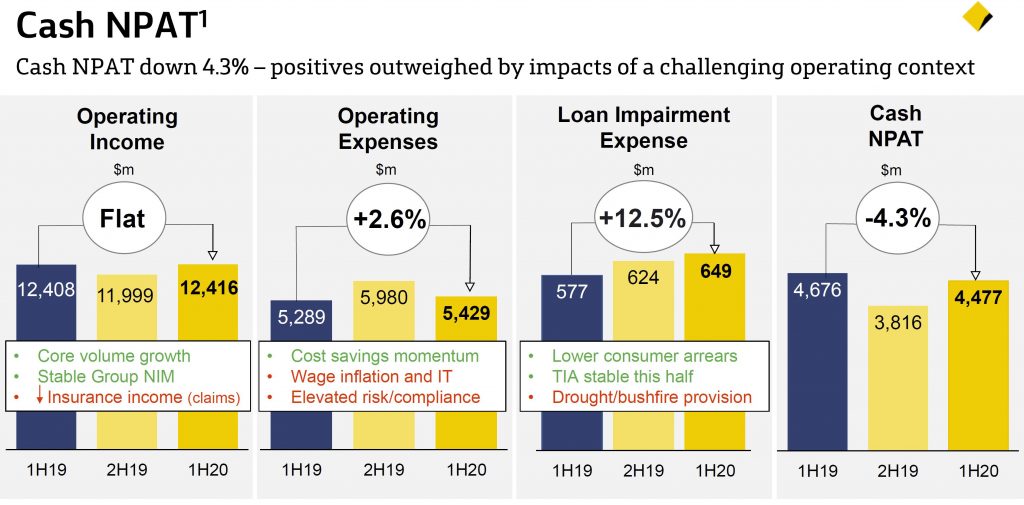

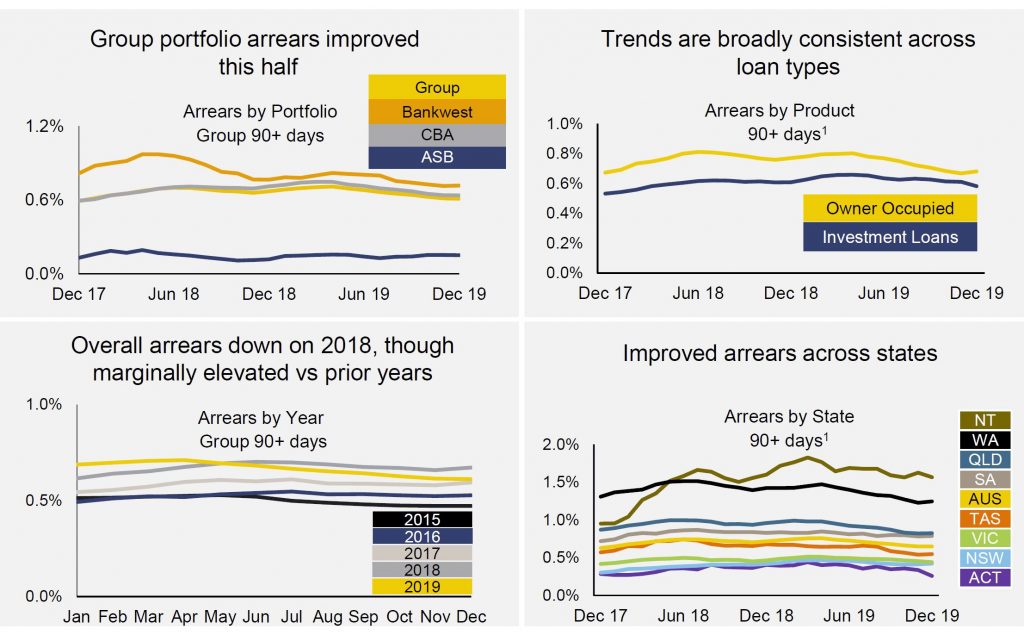

CBA released their 1H20 result today, with a statuary NPAT of $6,161 million, up 34%, but this included a one off gain from the sale of CFSGAM, so its not really meaningful.

On a cash basis, the cost base remains under pressure from compliance, wage inflation and IT investment, plus rising insurance claims and provisions for drought and bushfire. But volume grew, and consumer arrears are lower. Overall one of the better managed banks in Australia.

Thus this cash result on a continuing basis is more relevant. It was down 4.3% on pcp to $4,477m, thanks to stronger revenue growth than anticipated – especially from trading income, despite higher provisions and expenses.

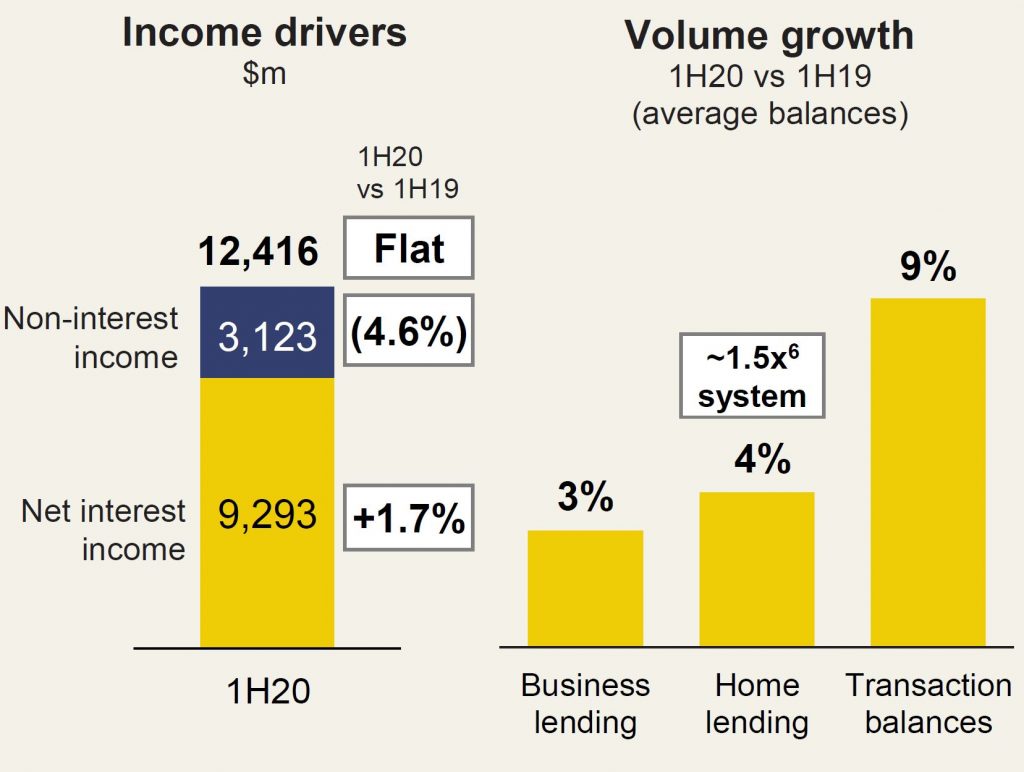

Operating income was flat at $12,416 million while net interest income was up 1.7% thanks to growth of book.

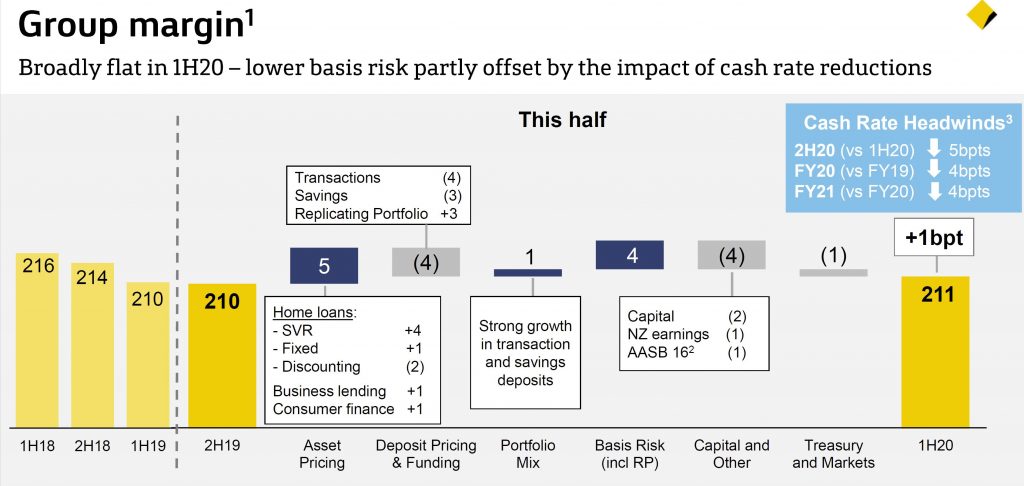

The Group net interest rate margin was 2.11%, up 1 basis point from 2H19. They indicated that the lower cash rate will continue to impact NIM – by around 5 basis points in 2H20, and 4 basis points across the FY 20 and FY 21.

Non-interest income was down 4.6%, mainly thanks to the impact of bushfire related claims ($83m) on insurance income, changes to wealth management fees and hedging losses.

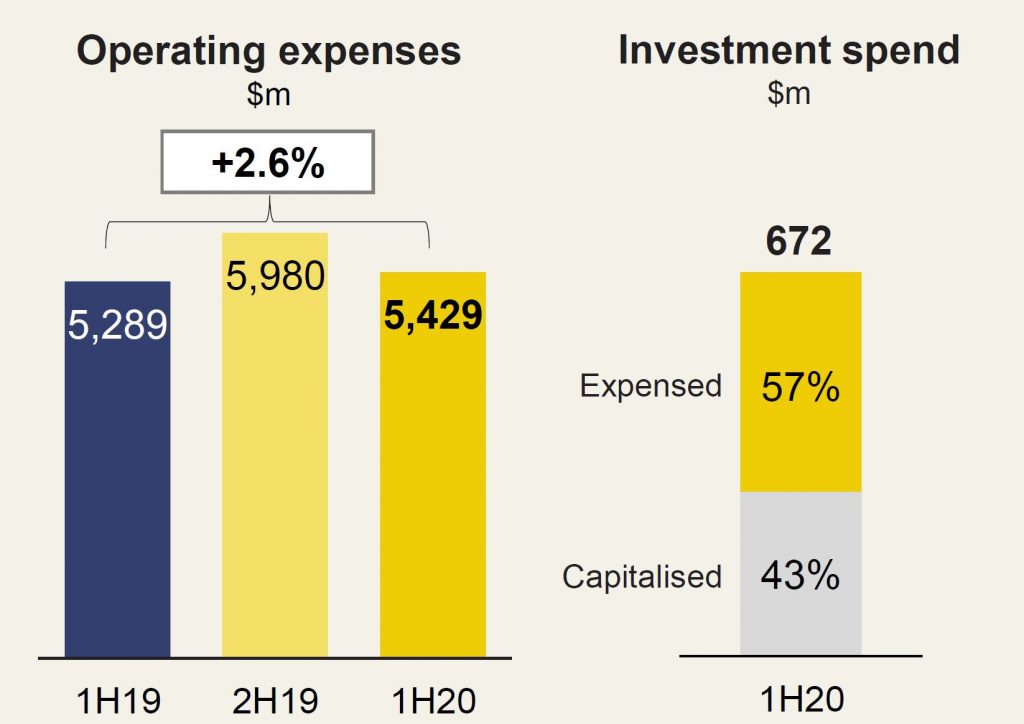

Operating expenses were up 2.6% to %5,429m with $630m was refunded to customers to 31 Dec 2019 following the Royal Commission misconduct and other required remediation. A further $596m is outstanding.

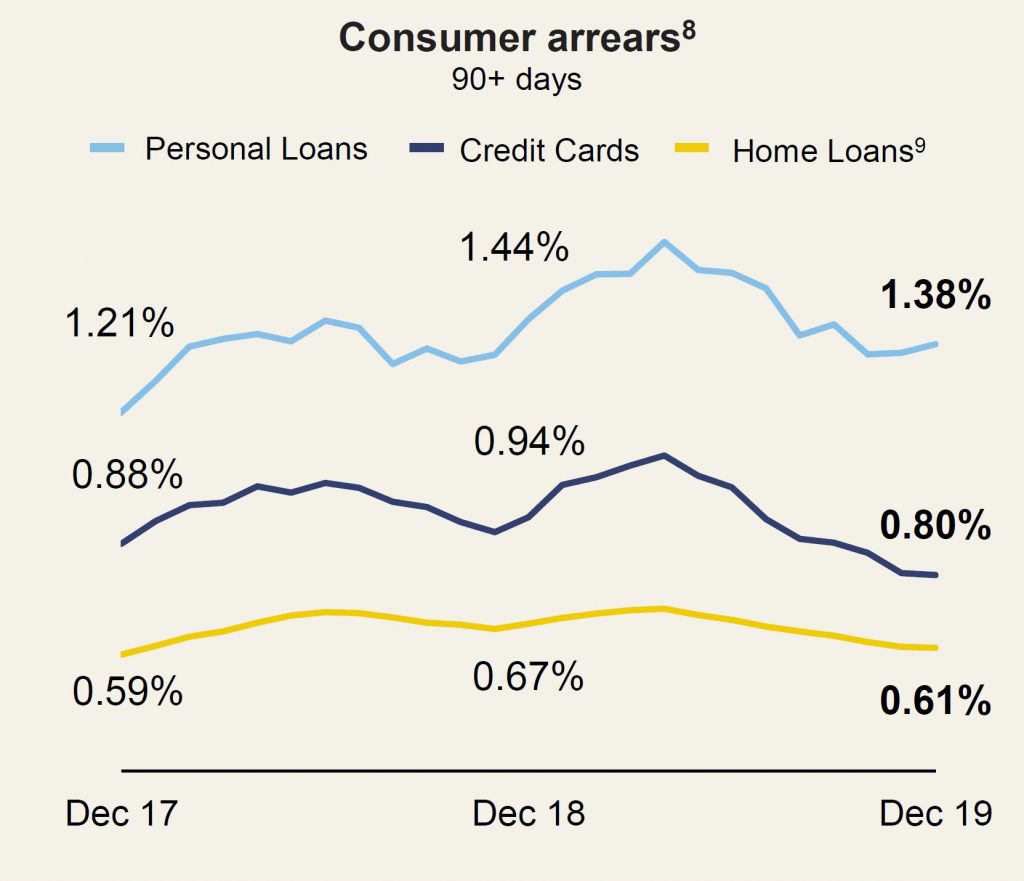

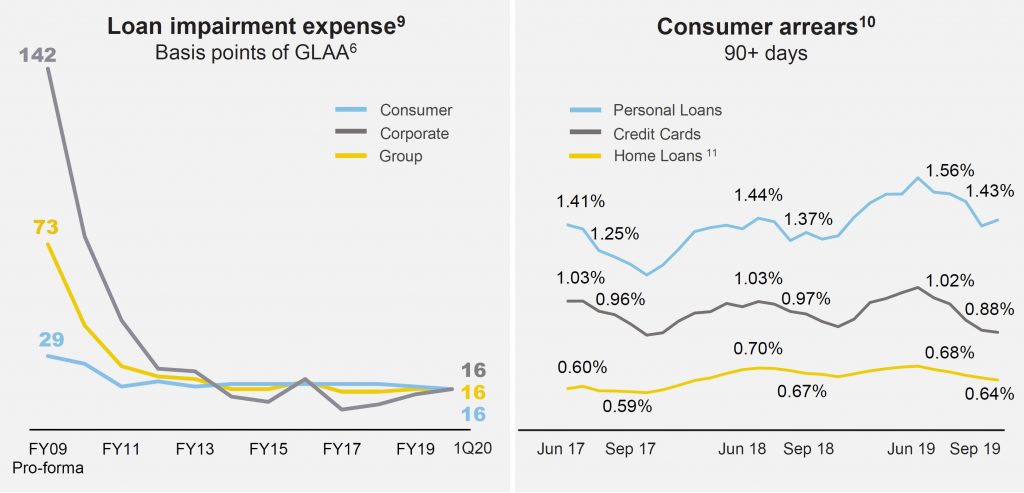

Loan impairment expenses were 17 basis point of average gross loans and acceptances. This was up 2 basis points, but includes 3 basis points for drought and bushfire provisions. They note a fall in consumer arrears thanks to the improved property market, but said pockets of stress remain in the discretionary retail, agricultural and construction sectors. Provisions lifted from 1.28% to 1.34% to $5,026 million.

Mortgage arrears are down a little, though are marginally elevated vs prior years.

Exposure to apartment development has reduced b y 63% since December 2016. Sydney represent 60% of the development exposure.

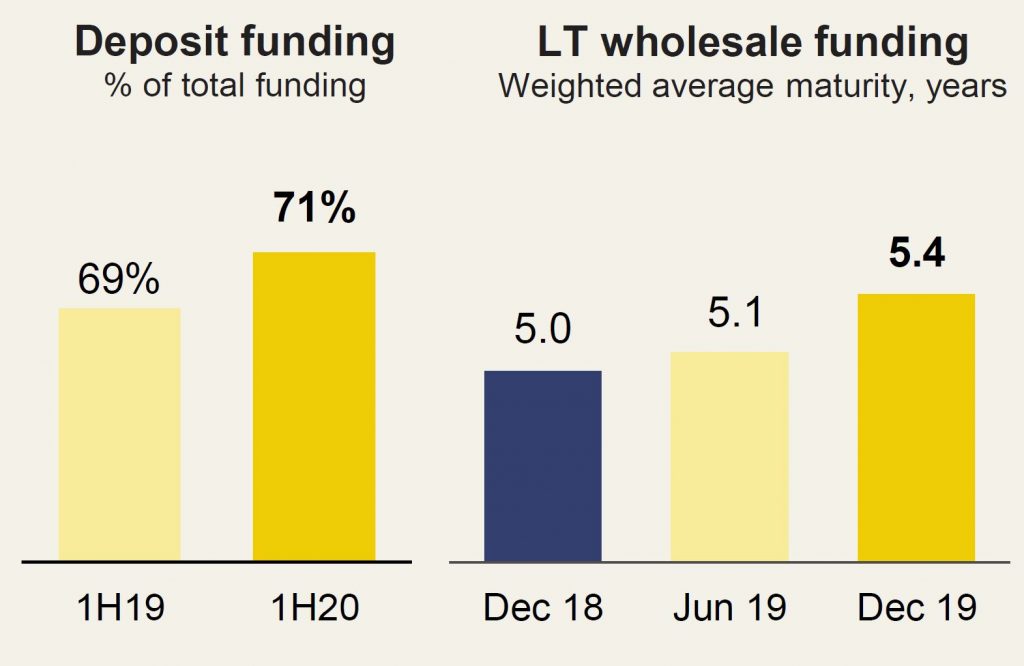

The percentage of book funded by deposits rose to 71% from 69% in 1H19. Overall average wholesale funding is 5.4 years. The Net Stable Funding ratio improved 1% to 113% and the Liquidity Coverage Ratio increased by 3% to 134%.

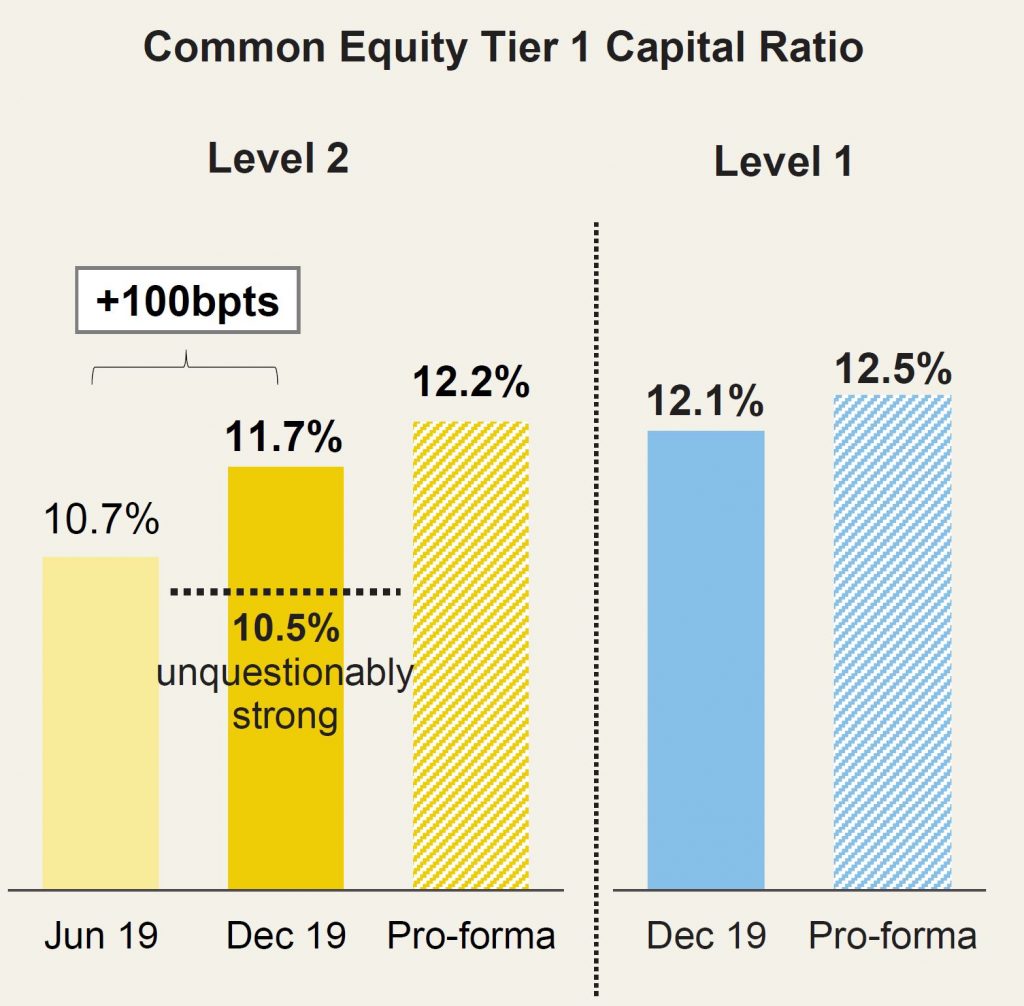

The Lever 2 CET1 ratio rose by 100 basis points to 11.7% and is above the APRA threshold. This was helped by recent asset sales. Further divestment proceeds will assist ahead.

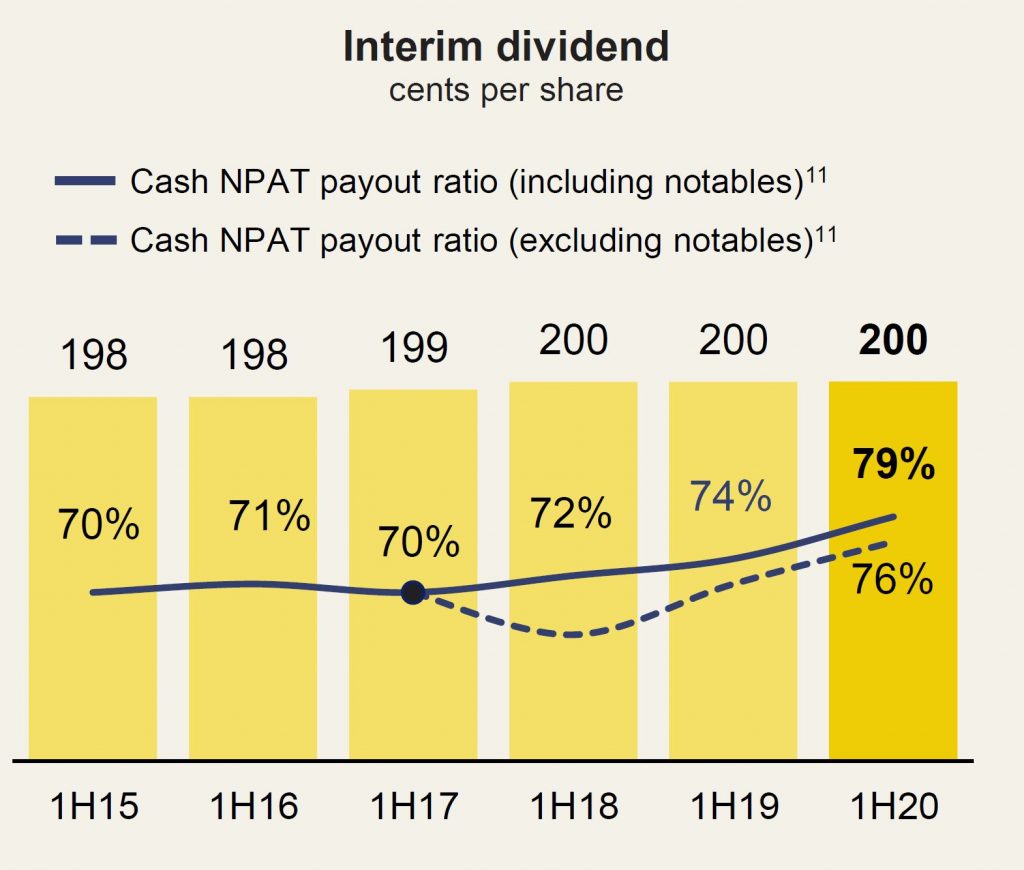

A $500m on-market purchase will support the Dividend Reinvestment Plan. No discount will be applied to shareholders.

The bank declared a dividend of $2.00 per share, fully franked – unchanged from 1H19 interim.

Commonwealth

Bank has today launched X15 Ventures, an Australian technology venture

building entity, designed to deliver new digital solutions to benefit

Australian consumers and businesses.

X15

will leverage CBA’s franchise strength, security standards and balance

sheet to build stand-alone digital businesses which benefit from and

create value for CBA’s core business. CBA customers will benefit from a

broader range of solutions which complement the bank’s core product

proposition.

The bank will partner with Microsoft and

KPMG High Growth Ventures to deliver X15 Ventures. Microsoft will bring

its platform and engineering capability to the initiative, while KPMG

will provide advisory services.

CBA Chief Executive Officer Matt Comyn

said: “We remain focused on bringing together brilliant service with the

best technology to deliver exceptional customer outcomes in the core of

our business. X15 will enable us to innovate more quickly, and continue

to offer the best digital experience for our customers.”

X15 will be a wholly-owned subsidiary of

CBA, with funding provided from CBA’s $1 billion annual technology

investment envelope, its own delivery model, and a dedicated management

team. X15 will be headed by Toby Norton-Smith who has been appointed

Managing Director of X15 Ventures.

Mr Norton-Smith said: “X15 allows us to

open the door and partner more easily with entrepreneurs than ever

before. Under its umbrella, we will create an environment for new

businesses to flourish, we’ll empower Australia’s innovators and bring

new solutions to market designed to empower customers as never before.

“X15 businesses will be nurtured and

developed as start-ups but will have the scale and reach of CBA behind

them to achieve rapid growth. We are pleased today to be unveiling our

first two new ventures, Home-In, a digital home buying concierge, and

Vonto, a business insights aggregation tool. We intend to launch at

least 25 ventures over the next five years.”

Microsoft Australia Managing Director

Steven Worrall said: “Commonwealth Bank has always excelled in terms of

its technology vision and we have partnered with the bank for more than

20 years. Today’s announcement takes that innovation and transformation

effort to the next level with the launch of X15 Ventures. I believe that

the next wave of major technology breakthroughs will come from

partnerships such as this, bringing together our deep technical

capabilities and absolute clarity about the business challenges that

need to be addressed.”

Amanda Price Head of High Growth Ventures

KPMG said: “A performance mindset can be the difference between success

and failure for start-ups. We look forward to working with CBA and X15

Ventures to build the ecosystem of support these new ventures need. From

founder programs designed to unlock sustained high performance, to

business and strategy solutions for high-growth ventures, there will be a

wealth of smart tools at their disposal to help them overcome the

challenge of scaling at speed.”

Home-in, which is live for select

customers today, is a virtual home buying concierge that will simplify

the complex process of buying a home. Smart app technology helps buyers

navigate the purchase process more easily from end-to-end, leverage a

platform of accredited service providers like conveyancers and utility

companies, access tailored checklists and a dedicated home buying

assistant who will respond to queries with the touch of a button. More

information is available at www.home-in.com.au.

Vonto, launched today, is a free app

available to all small business owners, not matter who you bank with. It

draws data from Xero, Google Analytics, Shopify and other online

business tools and presents the data and analytics in one location,

allowing users to obtain a quick, holistic and rich view of their

business for ease and increased control. For more information on Vonto,

please visit: www.vonto.com.au.

The

Commonwealth Bank of Australia has confirmed that brokers will be able

to apply for CBA’s First Home Loan Deposit Scheme loans for their

clients from 2 January 2020, while NAB has outlined that brokers will

need to wait a while longer.

The federal government’s First Home Loan Deposit Scheme (FHLDS) is due to commence operations on 1 January 2020.

The

scheme aims to allow up to 10,000 FHBs per year to get into the

property market sooner, requiring just a 5 per cent deposit, yet still

giving them access to competitive interest rates and waiving the need

for lender’s mortgage insurance (LMI).

The

government has agreed to guarantee the difference between the

borrower’s 5 per cent deposit and the standard 20 per cent deposit

required to take out a home loan without paying LMI.

It

has previously been announced that the two major banks involved in the

scheme, NAB and CBA, would be the first two lenders to start accepting

applications for the scheme from borrowers, while the other 25 non-major

lenders on the lending panel (mainly mutual banks and credit unions)

will be accepting applications from 1 February 2020.

Brokers can offer CBA FHLDS loans from 2 January

CBA customers will be able to apply for the scheme via the CBA website and call centres from 1 January.

However, given that

1 January 2020 is a public holiday, CBA has confirmed that it will make

FHLDS loans available to customers on 2 January, via all channels –

including branch and broker.

A

Commonwealth Bank spokesperson told The Adviser: “We’re excited that,

from 2 January 2020, customers will be able to apply for the First Home

Loan Deposit Scheme with Commonwealth Bank through our home loan

channels, including brokers.

“As

Australia’s largest lender, we help more Australians buy their first

home than any other bank, and its exciting that we can help get more

first home buyers into the market under the scheme.”

NAB to offer FHLDS loans online first

However,

brokers wishing to write FHLDS loans via NAB will need to wait a while

longer before applying, as the bank will be taking a “phased approach”.

According

to the bank, eligible customers will be able to apply for the scheme

through NAB via its website and call centres from 1 January 2020, as

well as through “select direct and retail channels”.

No

date has yet been released for full rollout of the FHLDS loans via

broker or the wider branch network, but NAB has said it will update

broker partners in January with how the phased approach is tracking.

A NAB spokesperson told The Adviser: “It

has always been our intention to offer the scheme through the broker

channel. However, given the short timeframe between being announced as a participant lender and the go-live date, we’ve needed to take a phased approach to implementation.

“We are working hard to implement the

scheme in the broker channel, and across our branch network, as quickly

as possible,” the spokesperson said.

The

delay will be a blow to brokers looking to write FHLDS loans for their

clients, especially given the fact that the scheme is capped at just

10,000 loans per year and the choice of lenders available to brokers is

limited.

While

Minister for Housing Michael Sukkar commented that the “composition of

the panel should also enable strong activation of mortgage broker

channels and promote choice for first home buyers”, many brokers have

highlighted that many of the smaller/regional lenders (who are expected

to take up 50 per cent of the 10,000 loans) are not members of their

aggregator’s panel – and therefore brokers would not be able to write

loans to these lenders unless they directly accredit with them.

For

example, brokers operating under the larger broker groups – AFG,

Aussie, Connective, Loan Market and Mortgage Choice – are unable to

access more than half of the lenders chosen under the FHLDS, as they are

not on the groups’ lender panel (according to the lender panels listed

on the groups’ websites).

These

include: Australian Military Bank, Bank First, Bank of us, Community

First Credit Union, Defence Bank, G&C Mutual Bank, Indigenous

Business Australia, Mortgageport, People’s Choice Credit Union,

Queensland Country Credit Union, Regional Australia Bank, The Mutual

Bank or WAW Credit Union.

CBA, who is on a different reporting cycle to the other majors, released their trading update to 30th September 2019 today. These are unaudited numbers and included some one-off items, but generally it looks like CBA managed to navigate the complexities of the current market quite well. But its all a matter of relativity as all the banks remain under pressure.

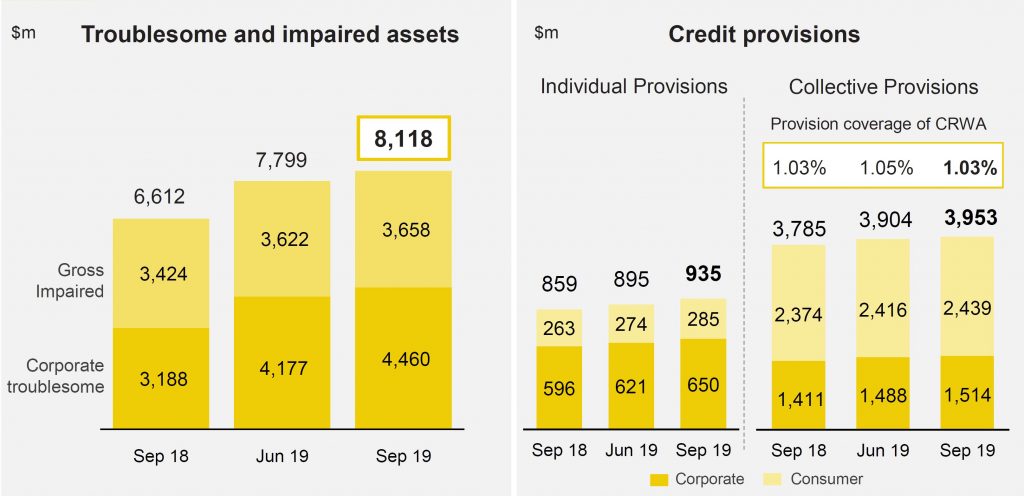

That said, the CET1 ratio was down, there was a considerable increase in corporate troublesome assets (discretionary retail, construction and agriculture), plus pockets of stress across its personal loans portfolio in Western Sydney and Melbourne. The Net Interest Margin was “lower than June 2019 due to headwinds associated with a low interest rate environment, which will continue to impact margins in future periods”. $2.2bn is flagged for customer remediation in program spend and provisions.

They made comparisons with the average of the previous two quarters, which might flatter the results a little. And they may have been later to implement the revised tighter HEM, which might have flattered their loan growth. Overall capital risk wights for mortgages sat at 25.8%.

Worth also noting that according to Banking Day:

Commonwealth Bank was the subject of the highest number of complaints to the Australian Financial Complaints Authority over the year to June, with the other big banks not far behind.

CBA was way out in front, with 3,890 complaints. ANZ, at number two, received more than 1,000 fewer complaints.

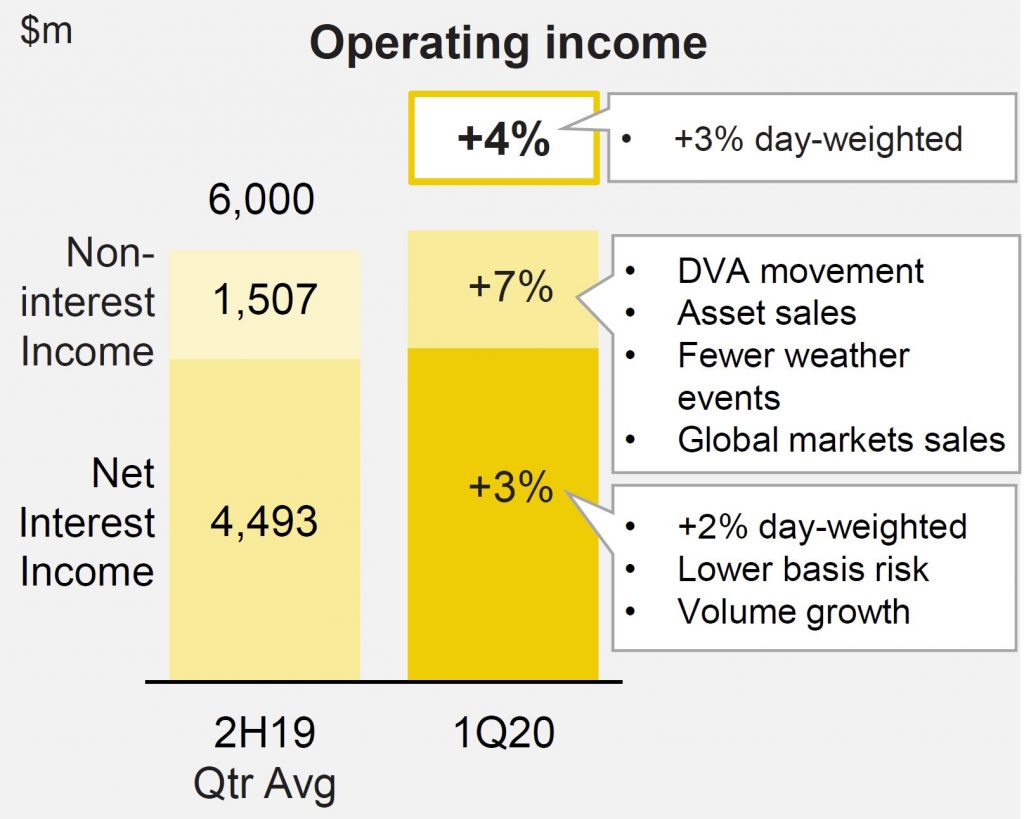

Unaudited statutory net profit was around $3.8 billion in the quarter, but this included a $1.5 billion gain from the sale of Colonial First State Global Asset Management(CFSGAM) to Mitsubishi UFJ Trust and Banking Corporation, with a post-tax gain on sale of approximately $1.5 billion.

Net cash profit from continuing operations was around $2.3 billion, up 5% excluding one-offs. This is the figure they want you to focus on!

Operating income was up 3% (day-weighted)

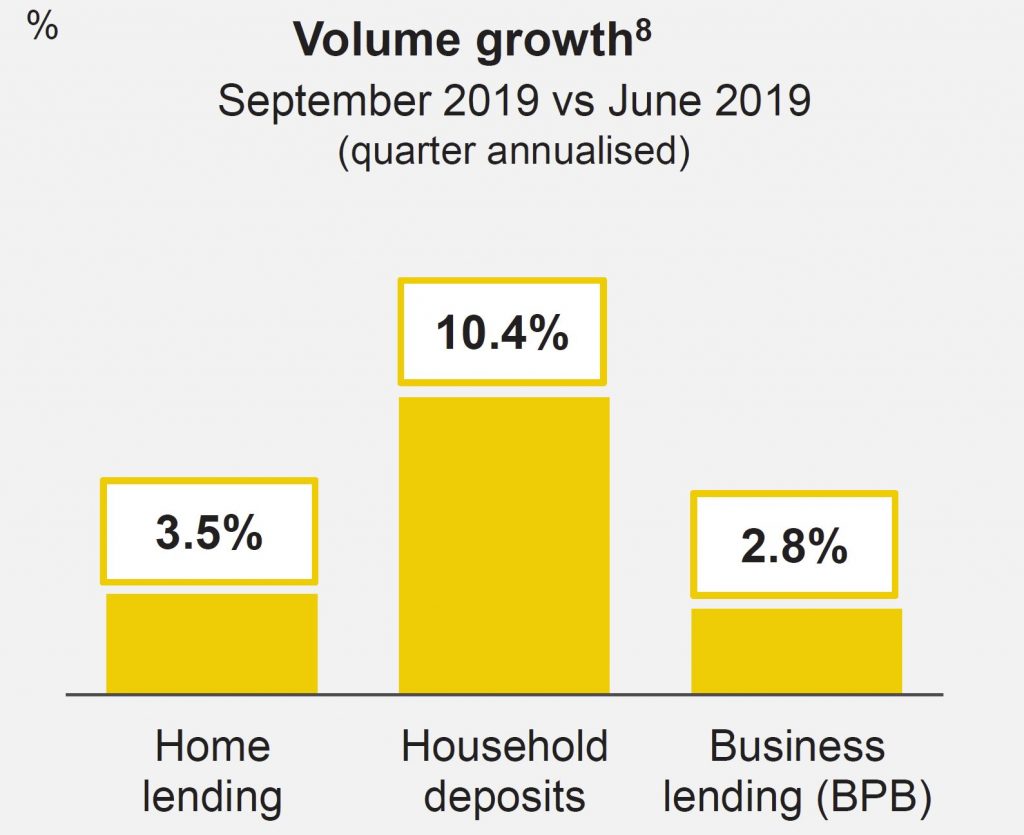

Net interest income increased 3%, benefiting from 1.5 additional days in the quarter. On a day-weighted basis, Net Interest Income was 2% higher, underpinned by volume growth in core markets of home lending, business lending and household deposits.

Excluding a 4 bpt benefit from lower basis risk, the Group’s Net Interest Margin was lower than June 2019 due to headwinds associated with a low interest rate environment, which will continue to impact margins in future periods.

Non-interest income increased 7%, benefiting from timing differences and one-off items including a favourable movement in the derivative valuation adjustment (DVA), asset sales in Structured Asset Finance (SAF), higher insurance income from fewer weather events/claims and higher global markets sales. These were partly offset by lower Funds Management income and the ongoing impact of the Bank’s Better Customer Outcomes program, which continues to deliver customer savings equivalent to annualised income forgone of $415m.

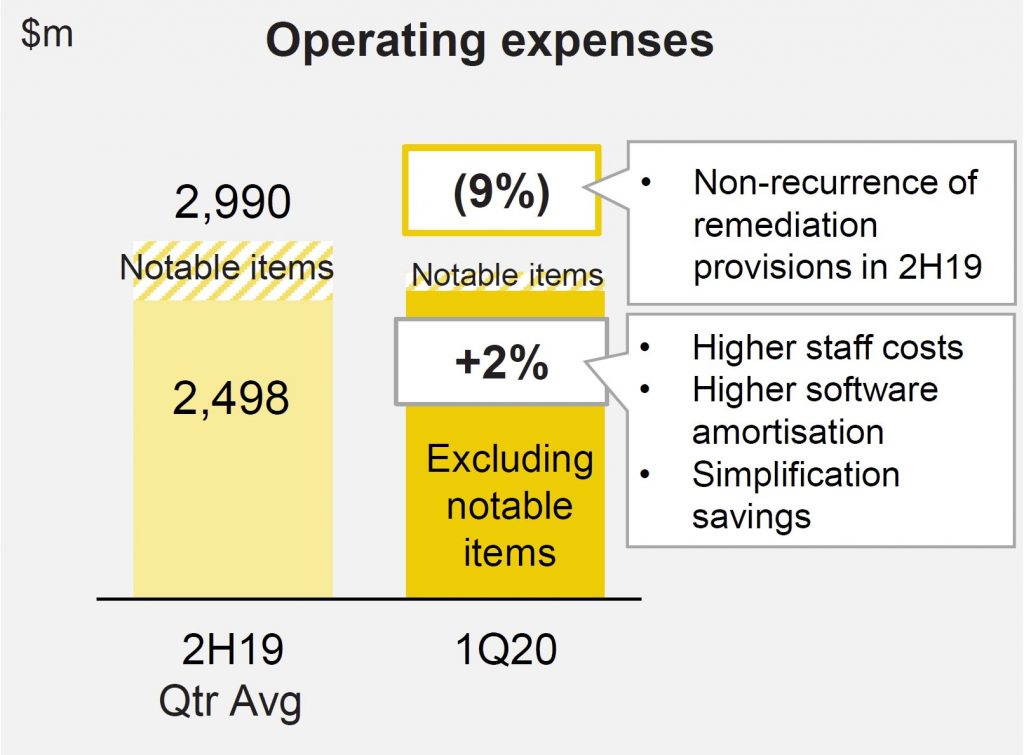

Operating expenses were up 2% (excluding notable items), reflecting higher staff costs and IT amortisation.

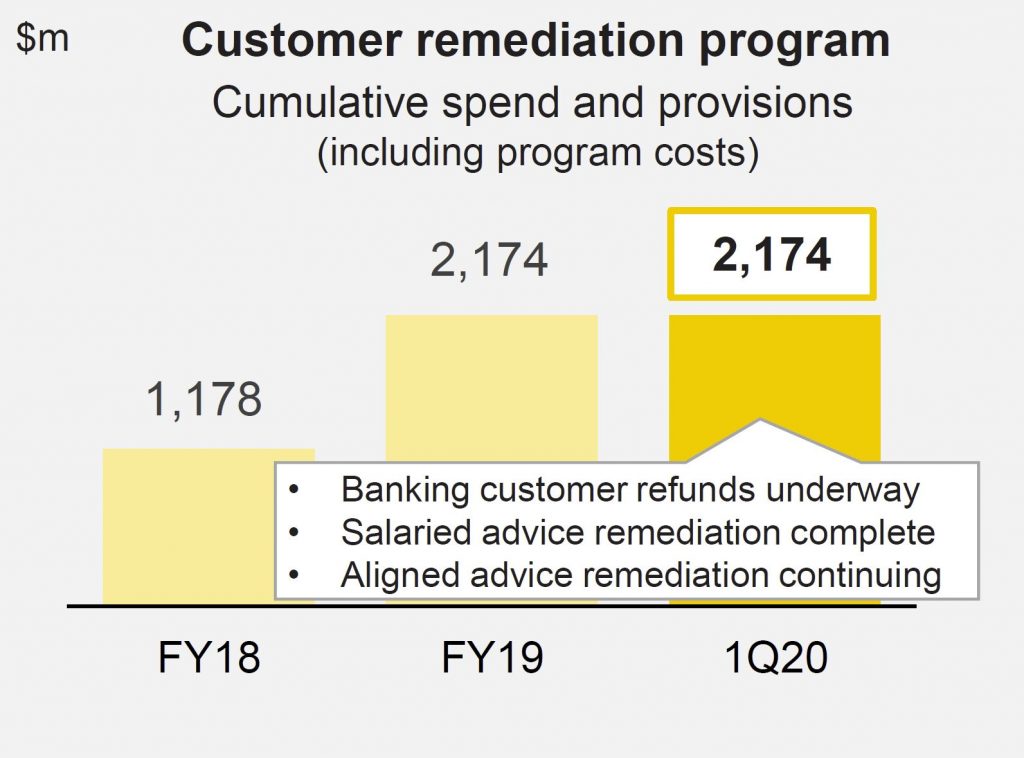

Customer remediation continues to drag the results. Of the $2.2bn in total program spend and provisions, $1.2bn relates to customer refunds of which approximately $600m has been paid to banking and wealth management customers to-date (ex aligned advice). Salaried adviser ongoing service remediation is now complete and represented a refund rate of 22% (ex interest). Aligned advice remediation work relating to ongoing service fees charged between FY09 and FY18 is continuing. The aligned advice remediation provision recognised in FY19 of $534m included program costs of $160m, $251m in customer refunds and $123m in interest. This assumed a refund rate of 24% (ex interest) and36% (incl.interest).

Loan Impairment Expenses were $299m in the quarter equated to 16bpts of Gross Loans and Acceptances, unchanged onFY19.

Consumer arrears improved in the quarter due to seasonality and the benefit of higher tax refunds. Personal Loan arrears rates remained elevated due to lower portfolio growth and continued pockets of stress in Western Sydney and Melbourne.

Troublesome and impaired assets increased to approximately $8.1bn. Corporate Troublesome assets continued to reflect weakness in discretionary retail, construction and agriculture,as well as single name exposures.

Total provisions increased by $89m to approximately $4.9bn.

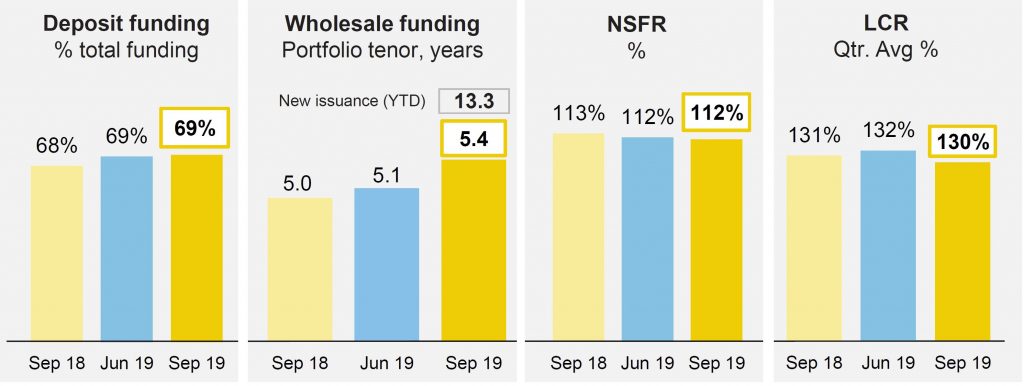

Customer deposit funding was at 69% and the average tenor of the long term wholesale funding portfolio at 5.4 years. The Group issued $5.8bn of long term funding in the quarter, including two long-dated Tier 2 transactions following the release of APRA’s loss-absorbing capacity proposal in July2019, contributing to a weighted average maturity of new issuance in the quarter of 13.3 years.

The Net Stable Funding Ratio (NSFR) was at 112%, the Liquidity Coverage Ratio(LCR) at 130% and the Group’s Leverage Ratio at 5.5% on an APRA basis (6.4%internationally comparable).

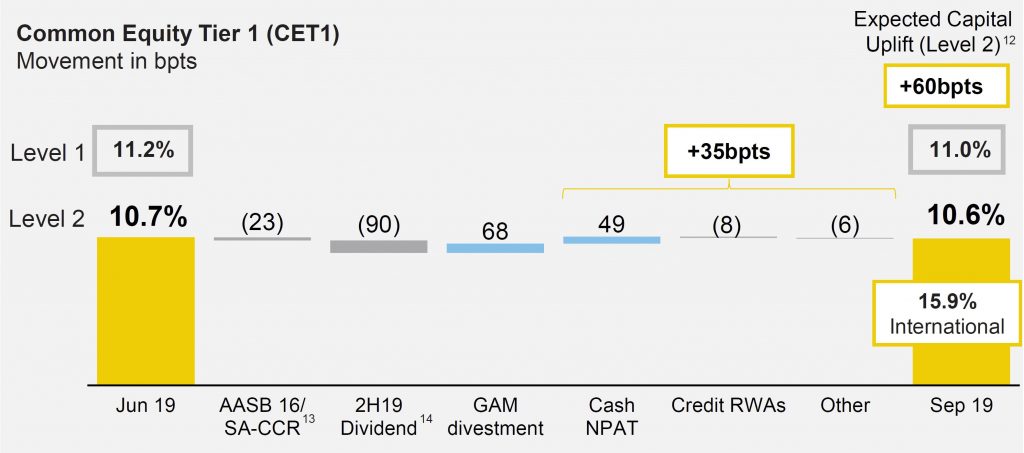

The Common Equity Tier 1 (CET1) APRA ratio was 10.6% as at 30 September 2019. After allowing for the impact of the 2019 final dividend and one-off impacts from regulatory changes and the CFSGAM divestment, CET1 increased 35bpts in the quarter. This was driven by capital generated from earnings, partially offset by higher Credit Risk Weighted Assets driven by revised regulatory treatments and lending volume growth. As at 30 September 2019, the Level1 CET1 was 11.0%, 40bpts above the Group’s Level2 CET1 Ratio.

The Group’s remaining previously announced divestments are expected to collectively provide an uplift to Level2 CET1 of approximately 60bpts. As outlined in the Group’s FY19 results, a strong expected capital position creates flexibility for the Board in its consideration of capital management initiatives.

While the ATM and EFTPOS merchant services are working and debit and credit cards are working, some debit card payments may be affected.

But BPAY services including PAY-ID payments not available and Cardless Cash not available. In addition some in-branch service, some call centre services and business services on CommBiz were hit.

The CommBank app and NetBank are available with limited functionality.

A small number of branches have closed.

They said “We are experiencing higher than normal volume of calls to our contact centres which means there are longer wait times. Some of our contact centre services are also impacted limiting what services we can provide”.

Now, consider the situation where cash is less available. Sometime good old cash is still king!

Commonwealth Bank has responded to the Reserve Bank of Australia’s cash rate decision by reducing home loan interest rates.

New Standard Variable Rates

Owner Occupied Principal and Interest Standard Variable Rate home loans reduced by 0.13% per annum (p.a) to 4.80% p.a.

Investor Principal and Interest Standard Variable Rate home loans reduced by 0.13% p.a. to 5.38% p.a.

Owner Occupied Interest Only Standard Variable Rate home loans reduced by 0.13% p.a. to 5.29% p.a.

Investor Interest Only Standard Variable Rate home loans reduced by 0.25% p.a. to 5.64% p.a.

New Fixed Rates

2 and 3 Year Owner Occupied Principal and Interest Fixed Rates in

the Wealth Package reduced to 2.99% p.a. available from Thursday.

Commonwealth Bank has responded to the Reserve Bank of Australia’s

(RBA) cash rate decision by reducing the Standard Variable Rate (SVR)

for home loan customers by between 0.13% p.a. and 0.25% p.a.

“Today’s announcement means our SVR for Owner Occupied customers,

with Principal and Interest repayments, will be at record low levels,”

Angus Sullivan, Group Executive Retail Banking Services said.

“As the Reserve Bank cash rate has reached record lows, we face a

difficult balancing act between the multiple, valid interests of our

stakeholders. Particularly given it is currently not feasible to pass on

the full rate reduction to more than $160 billion of our deposits which

are at, or near, zero rates.

“In balancing these interests, we have carefully considered how to

best meet the needs of over 6 million savings customers – who may find

it challenging to make ends meet with record low savings interest rates –

with the needs of our 1.6 million home loan customers, who want to pay

less on their mortgages; and the needs of our shareholders, many of whom

are retirees who rely on our dividend.

“In this environment, while reducing the SVR for home loan customers

by between 0.13% p.a. and 0.25% p.a., we have also decided to limit the

base rate reduction for savings customers in our popular NetBank Saver

product to 0.05%. These changes are in addition to the fee removals,

fee reductions and pre-emptive fee alerts we have already introduced,

which have helped save our customers over $415 million.

“We are also announcing a new 2.99% p.a. 2 and 3 year Owner Occupied

Principal and Interest Fixed Rate, available to new and existing Wealth

Package customers taking out a Fixed Rate loan. This allows customers

who prefer certainty to lock-in this historically low rate. This means

we have reduced our 2 and 3 year Fixed Rates by 0.80% p.a. since July

for Owner Occupied Principal and Interest customers,” Mr Sullivan said.

For Owner Occupied customers paying Principal and Interest, the SVR

has reduced by 0.57% p.a. since June, which on a $400,000 home loan

equates to a reduction in the minimum monthly repayment of $140 or an

annual saving of $1680.

For Investor customers paying Interest Only, the SVR has reduced by

0.75% p.a. since June, which on a $400,000 home loan, equates to a

monthly saving of $250 or an annual saving of $3000.

Customers who have questions regarding today’s rate change are

encouraged to speak to one of our home lending specialists in branch or

over the phone.

The new SVR will take effect on 22 October 2019

The new Fixed Rates will be available to new and existing customers switching to a Fixed Rate on 3 October 2019

The NetBank Saver base rate reduction will take effect on 4 October 2019

Blog")