Since the beginning of the Australian fintech boom, headlines have proclaimed how Australia’s largest financial institutions should be running scared from startups.

Now the big four have had a chance to retaliate, what can their reaction tell us about how these stoic organisations deal with disruption?

Each of the big four has dealt with their fintech rivals in a very different way, and for some of them, the cracks are starting to show.

Speaking at an event in Sydney in June 2016, NAB chief executive Andrew Thorburn said the bank emulated the traits of its startup rivals.

“I actually think we are a fintech company ourselves. We have to have the mindset of a fintech company, and I actually think we’ve got a lot of the assets of a fintech company,” he said.

In that same month, NAB launched a product – the QuickBiz Loan – from its innovation hub “NAB Lab” on its own — that is, without partnering with a fintech startup.

At the time of the launch, Mr Thorburn said “There does remain a question mark around the credit capabilities around some of the fintechs.”

“We’ve watched developments in the space and been very determined…to make sure we have our own NAB-branded solution that we’ve built from scratch.”

A similar venture, this time jointly founded by NAB and Telstra, was small business marketplace ProQuo.

Despite the size of both corporations, ProQuo considers itself a startup and even housed itself next to startup accelerator Blue Chilli.

While NAB has gone its own way on several ventures, including those outlined above, it has pledged $50 million to invest in startups and develop partnerships with innovative companies through its NAB Ventures fund.

Commonwealth Bank has taken a very different approach than NAB. The bank partnered with payments startup Kounta earlier in the year, following that with a partnership with small business lender OnDeck.

The partnership with OnDeck saw it pick up the Fintech-Bank Collaboration of the Year at the Australian Fintech Awards in 2016.

While partnerships between financial institutions and startups have become common, it’s Commonwealth Bank’s attitude towards the fintech sector that also sets it apart.

Speaking at an Australian Information Industry Association lunch in Sydney, Commonwealth Bank’s chief information officer David Whiteing spoke of the need to embrace newer technologies and be ahead of the market.

“We should mirror the society in which we operate, so if we become really good at being inclusive we will be able to harvest the ideas and respond quickly,” he said.

“One of the things that my leadership team talks about quite a bit is that today we are a technology team in a bank that has a technology halo, tomorrow if we get this right, we will be a technology company that does banking services.”

The big four lender has already established an innovation lab in Hong Kong and begun experimenting with blockchain technology.

At 180 years old, ANZ is far beyond its startup years. Earlier this year, ANZ boss Shayne Elliot told a Melbourne fintech meetup he was ready to forge partnerships and invest in startups.

However, speaking with the Sydney Morning Herald, Elliot also outlined the bank’s challenges:

“Investing in startups is not hard for banks, we have lots of money to write cheques, the difficult thing is figuring out how we can internalise that intellectual capital,” he said.

Two key partnerships announced by the bank include York Butter Factory, a Melbourne incubator and co-working space; and Honcho, where customers are referred from its small-business banking websites to receive discounted business registration, marketing and data storage.

ANZ’s recent venture with Apple to offer phone users Apple Pay is also a mark of things to come for the bank, signalling its willingness to adopt technologies built elsewhere.

“The days of a bank needing to own every piece of technology are gone,” ANZ managing director for pensions and investment Peter Mullins noted recently.

“We believe we can achieve better outcomes for our customers by partnering with a specialist provider committed to the technology investment and product innovation needed to provide a world-class offering.”

Westpac is arguably the big four bank that is furthest along the fintech curve. Reinventure Fund, of which Westpac is the largest funder, has invested in a huge number of fintech startups.

Through Reinventure $50 million will be invested in Australian technology startups such as Society One, Valiant Finance and Coinbase. Outside of the fund, Westpac has also partnered with SME lender Prospa.

Speaking at the 2016 Banking and Wealth Summit, Westpac CIO David Curan spoke about the new technology ecosystem he sees developing between banks and fintechs.

“My guess is we will continue to see more collaboration in financial services, and that will start with more partnerships between banks and startups – because that’s what we’re used to – just a few people and easy to define contracts,” he said.

“Over time we’ll move to more of an ecosystem model, where more and more people will be working together, with new inter-relationships that aren’t that clear. That starts with more partnerships and moving into new ecosystems, the technology is taking us there whether we like it or not.”

So, what can the big four teach us about fintech?

The banks that are not going to lose at fintech are going to find the best tools at their disposal and admit when they don’t have them; thus the partnerships.

The banks that are becoming the best innovators are working with fintech, not against it. They are admitting that while they are market-leading, a startup may be worth listening to.

While there is no clear answer whether partnerships are the best strategy for every company, any answer that best drives innovation for a fintech company (bank or otherwise) should be what’s adopted.

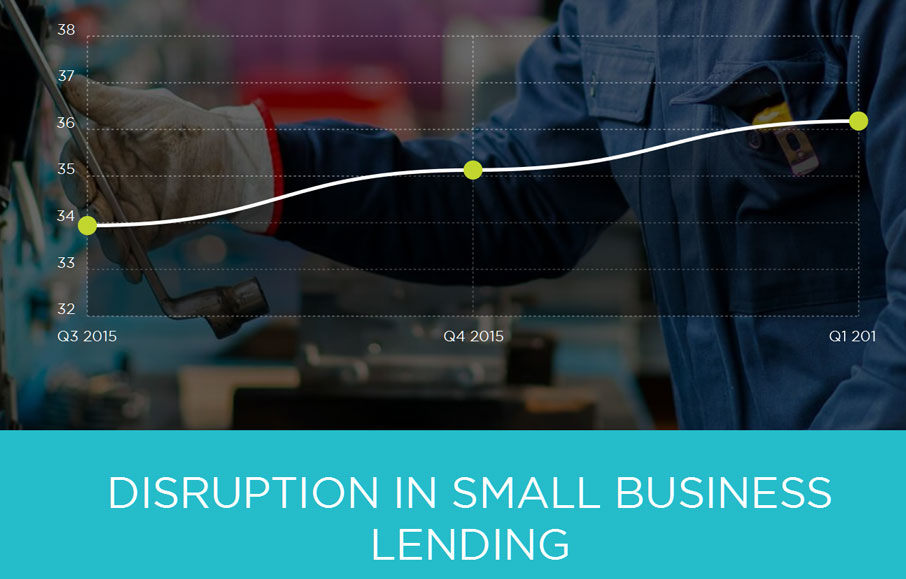

The Disruption Index tracks change in the small business lending sector, and more generally, across financial services. The Financial Services Disruption Index, which has been jointly developed by Moula, the lender to the small business sector; and research and consulting firm Digital Finance Analytics (DFA).

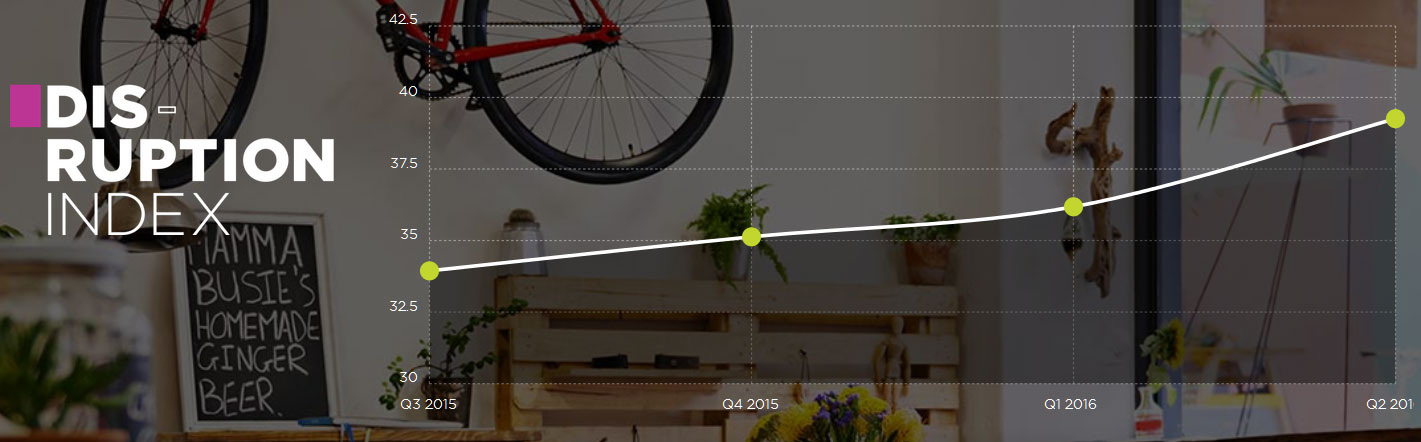

The Disruption Index tracks change in the small business lending sector, and more generally, across financial services. The Financial Services Disruption Index, which has been jointly developed by Moula, the lender to the small business sector; and research and consulting firm Digital Finance Analytics (DFA).