We continue the results from the latest Digital Finance Analytics household surveys, by looking at property investors, who now make up around 35% of all residential property borrowers. This is much higher than in any other similar economy (e.g. UK 17%). The appetite for investment property is still strong, and despite some tightening of lending criteria and slowing capital growth momentum, investors still wish to transact. Bank lending to investors in June 2016 rose by 0.1% or $0.6 billion.

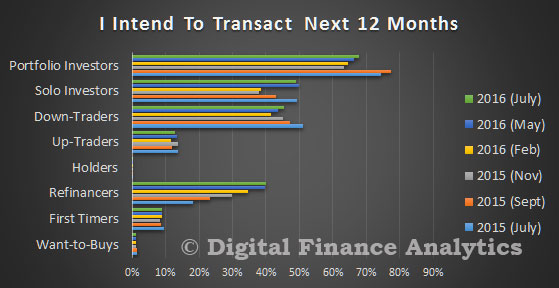

As a reminder, we showed that investors (either those with one or two properties – solo investors, or those with a portfolio of properties – portfolio investors) were the most likely to purchase, even compared with those seeking to refinance.

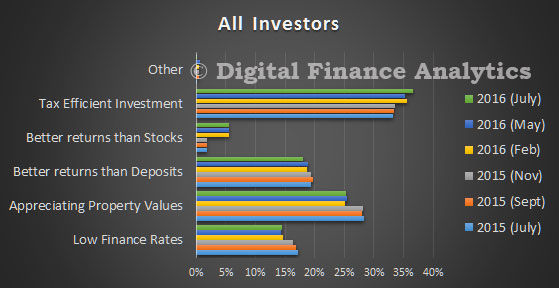

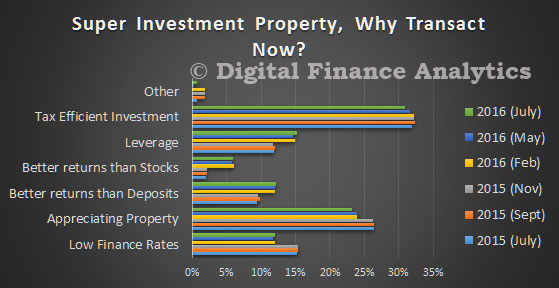

The driver to transact relate firstly to the tax effectiveness of the investment (37%) and capital gains from appreciating property values (25%). Low finance rates are helping, and investment property is perceived as offering better returns than bank deposits or stocks. We know that many in the eastern states will not make positive pre-tax returns, but taking tax breaks into account, they are still ahead, and will remain so unless there is a significant fall in home prices.

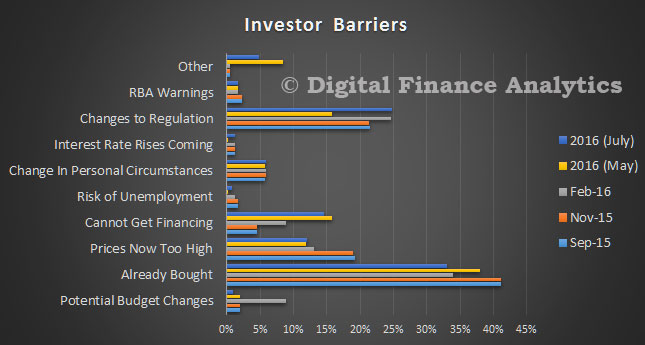

There are some barriers which investors have to negotiate, the most obvious is they have already bought (40%), potential changes to regulation (25%), and inability to get financing (15%). Risks relating to budget changes have dissipated, and some are concerned about static or falling rents (bundled in the other category at around 5%).

Solo investors have similar drivers with a focus on tax efficiency and potential capital gains, supported by low finance rates. We note that they have lower expectations of future gains than other investors (portfolio and those investing via SMSF).

Looking in detail at SMSF property investment, tax effectiveness, leverage and potential capital gains all drive the decisions. We did note some concerns about changes to superannuation regulation, especially around the caps, but this has not deterred prospective purchasers.

There are about four percent of SMSF’s holding residential property, and typically it comprises just a proportion of the total fund. A further three percent are actively considering adding in property to their SMSF.

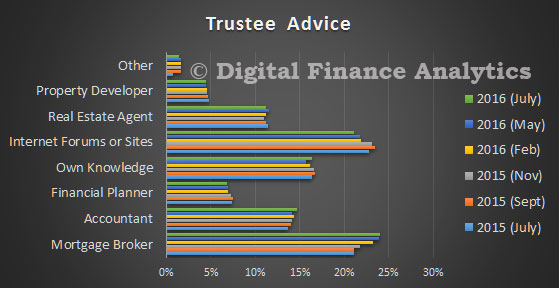

It is also worth noting that mortgage brokers are becoming more influential in providing advice to trustees seeking SMSF advice, alongside accountants. Internet forums and web sites still play a significant role in providing advice to trustees. 17% say they know enough, and rely on their own knowledge and experience.

So, investors will continue to sustain the market, and should the RBA cut rates again tomorrow, we should expect additional momentum, thanks to lower funding costs and paltry returns from bank deposits. Property investors are making logical decisions, given past performance, but at some point the tide just has to turn. But at the moment, returns from property simply outperforms other investment classes, and are perceived to be “as safe as houses”.

Next time we will round out the survey results by looking at some of the other property active segments.

The digital economy is a transformative process, brought about by advances in information and communications technology (ICT) which has made technology cheaper and more powerful, changing business processes and bolstering innovation across all sectors of the economy, including traditional industries. Today, sectors as diverse as retail, media, manufacturing and agriculture are being impacted in some way by the rapid spread of digitalisation. In the broadcasting and media industry, for instance, the expanding role of data through user-generated content and social networking have enabled internet advertising to surpass television as the largest advertising medium.

In other words, “digitalisation” is pervasive, making it very difficult, if not impossible, to ring-fence the digital world from the rest of the economy, including for tax purposes. This is the first finding regarding the tax challenges of the digital economy agreed by all G20 and OECD countries, under the Base Erosion and Profit Shifting (BEPS) Project. BEPS refers to tax strategies that allow Multinational Enterprises to shift profits away from the locations where the actual economic activity and value creation takes place, into low or no-tax locations.

Action 1 in the 15-point Action Plan to address BEPS, the work on the tax challenges of the digital economy, aimed to consider whether the international tax rules were sufficient to meet the demands arising from new business models and ways of creating value that are emerging with the rise of new technologies.

While finding that the digital economy cannot be separated out from the rest of the economy, it was equally clear that some specific features of the digital economy may exacerbate the risks of base erosion and profit shifting for tax purposes–namely mobility (e.g. intangibles, business functions), reliance on data (and other forms of user input), network effects, and the spread of multi-sided business models.

Thanks to digitalisation, we now see businesses across all sectors having the capacity to design and build their operating models around technological capabilities, with a view to improve flexibility and efficiency and extend their reach into global markets. These advances, coupled with liberalisation of trade policy and reduction in transportation costs, have significantly expanded the ability of certain business models of the digital economy–e.g. electronic commerce, online advertising and cloud computing–to take advantage of BEPS opportunities. The techniques used to achieve BEPS by these businesses however, are generally not different from the ones used in other parts of the economy, and as such, countries agreed that the digital economy does not generate any unique BEPS issues, and that the solutions designed to tackle BEPS practices in the 14 other points of the BEPS Action Plan should suffice to address these concerns.

Second, beyond the issue of BEPS and tax avoidance, the key features of the digital economy raise more systemic challenges for tax policy makers that are generally grouped into three categories–the so-called “broader tax challenges”: (i) the difficulty of collecting VAT/GST in the destination country where goods, services and intangibles are acquired by private consumers from suppliers based overseas which may not have any direct or indirect physical presence in the consumer’s jurisdiction; (ii) the ability of some businesses to earn income from sales from a country with a less significant physical presence in the past, thereby calling into question the relevance of existing rules that look at physical presence when determining tax liabilities; (iii) the ability of some businesses to utilise the contribution of users in their value chain for digital products and services, including through collection and monitoring of data, which raises the issue of how to attribute and value that contribution.

On VAT/GST collection, the project resulted in international agreement on recommendations to allocate the collection of VAT on cross-border B2C supplies to the country where the customer is located. For the remaining two broader tax challenges, the continuing technological developments and business models–the Internet of things, robotics and the “sharing economy”, to name a few–may prove influential and disruptive in the near future, and accordingly, raise questions as to whether the existing paradigm used to determine where economic activities are carried out and where value is generated for income tax purposes continues to be appropriate.

It is still too early to determine whether these challenges are sufficiently critical in scale and impact to justify more fundamental changes of the existing international framework, beyond what is proposed in the package of measures to tackle BEPS endorsed by OECD and G20 in October 2015. Some potential options to address these challenges have been analysed, ranging from a withholding tax on digital sales to a new concept of nexus based on having a “significant economic presence”. In the coming years, the Task Force on the Digital Economy under the Committee on Fiscal Affairs will continue to monitor new developments–both in terms of technologies as well as new tax policy responses governments develop to address them, with a review of the 2015 report on BEPS Action 1 planned for 2020.

Needless to say, the stakes in this work are high, and so are the objectives: appropriate policy solutions need to be considered that address these challenges, even while the digital world continues to advance at an exponential rate. In a short period of time, it is possible that we may be confronted with a fully-digital world that disrupts some of the fundamental assumptions of the international tax system.

OECD (2015), Addressing the Tax Challenges of the Digital Economy, Action 1 – 2015 Final Report, OECD/G20 Base Erosion and Profit Shifting Project, OECD Publishing, http://dx.doi.org/10.1787/9789264241046-en

The Coalition has scraped into a second term. How credible is its economic growth program, and what else should it do to strengthen growth?

The good news is that the transition from the mining boom is proceeding about as well as should have been expected. It is true that national income per person is lower than five years ago (see figure below) and that wages are also stagnating. But these changes are mostly due to falling resource prices. GDP growth, while subdued in recent years, has been fast enough to keep unemployment in check (though average hours per worker have declined), and it even shows signs of picking up. And while non-mining investment has remained flat despite record low interest rates, it’s not unrealistic to hope that Australia will, for the first time in our history, complete a mining cycle without ending in recession.

But deeper economic challenges persist. Global growth remains weak, with China’s economy likely to slow, and the European Union more fragile since the UK’s Brexit vote. Slow growth and rising inequality helped drive the populist anger and political instability we now see in the EU and US.

The coalition campaigned on jobs and growth, but in reality its growth program is patchy. The signature policy – phased cuts in the company tax rate – would ultimately increase national income by about 0.6%. But business tax cuts could drag on national income for up to a decade, as foreign investors pay less tax from the beginning, while benefits from greater investment take time.

Other parts of the coalition plan are far from being fleshed out. The government will seek to implement its already announced innovation and competition policy agendas. It plans to ratify the TPP, though the TPP itself may now be doomed to fail, as neither of the likely US presidential candidates supports it.

The Turnbull government also plans to pursue further trade agreements with the European Union, India, and Indonesia. On the downside, its Smart Cities Plan, which aims to finance improvements in urban transport and housing, lacks detail. And its plan to slowly reduce the budget deficit relies mostly on revenue increases that may not materialise.

Overall, the plan for jobs and growth is far from complete. The government should consider five further options to increase economic growth.

Taxes and work

First, the government should shift the tax base towards taxes that do less to discourage investment and work. For example, cutting the capital gains discount to 25%, and limiting negative gearing, would create space to reduce other more distorting taxes. So would broadening the GST base and/or increasing the GST rate (while cutting income tax and adjusting welfare payments), though benefits may be modest.

General property taxes should replace stamp duties, which deter people from moving to a home that suits their current needs. A 0.5% levy on unimproved land values could raise enough to replace stamp duties nationwide, would provide a more stable tax base for states, spread the tax burden more fairly, and add up to $9 billion a year to GDP. While these are state matters, the Commonwealth could consider providing incentive payments to states to make the switch, since its revenues will ultimately rise as the reforms increase incomes.

Second, government should help people stay in work, or get back to work. Female labour force participation in Australia is below that of many high-income economies. Low rates of take-home pay deter some women from joining the labour force or working full-time. The system of family payments and childcare support needs an overhaul to encourage greater female labour force participation.

Older Australians, too, are less likely to work than in many comparable economies. The age at which people can access superannuation or the age pension affects when some workers decide to retire. Australia is already increasing the pension eligibility age from 65 to 67, and phasing up from 55 to 60 the age at which people can begin to draw down their superannuation. Government should further increase pension and superannuation access ages.

Fourth, government should remove barriers to innovation, while only funding programs that are supported by evidence that they actually help innovators at a reasonable cost. The National Innovation and Science Agenda will cut barriers to new business creation and improve research-business collaboration.

The vast majority of innovations used in Australia are produced elsewhere. Government should remove barriers to the local spread of global innovations such as cloud computing and peer-to-peer business models such as Uber and Airbnb. States are responsible for barriers such as taxi regulation, while labour regulation and tax are largely Commonwealth responsibilities. Intellectual property rules can also impede the spread of productive ideas.

Finally, investment in high quality infrastructure (along with rules such as user charging to encourage efficient use) promotes growth. Yet governments have already spent large amounts of money, not always wisely, on new public infrastructure over the past decade.

Political realities

To enact any of these policies, the coalition will likely first seek support in the Senate from Labor or the Greens, rather than from the 10 or so independent and small party senators. Some policies are very unlikely to pass the Senate: for example, the proposed broad corporate tax cut is probably dead (though an alternative like an investment allowance might get up).

But some policies have a fighting chance, such as the City Deals, borrowed from the UK and new initiatives to cut superannuation costs. If many other policies (including family payments reform and the flexibility initiatives) are to have a chance of making it into law, the Coalition will first have to make a case for them and win public support.

The Coalition campaigned on its ability to provide jobs and growth. But its campaign platform for jobs and growth was far too narrow. To turn talk into action, it will need to win support for a much more expansive and ambitious agenda.

Author: Jim Minifie, Productivity Growth Program Director, Grattan Institute

The ABC reported that “a Treasury document obtained by the ABC under Freedom of Information (FOI) shows most of the windfall from the property tax break goes to high-income earners. The modelling said more than half of the negative gearing tax benefits go to the top 20 per cent of incomes in Australia. “Negative gearing benefits high-income families,” the document said. The report stated those in the bottom 20 per cent were getting just over 5 per cent of negative gearing tax benefits”.

On the other hand, the Government has continued to argue “mum and dad” investors and Australians on average earnings are the main beneficiaries. “It does not change the fact that two thirds of Australians using negative gearing have a taxable income of less than $80,000,” Treasurer Scott Morrison said. This is of course axiomatic, but misses the point, because the whole idea of negative gearing is to offset interest costs and other losses to reduce total income, and therefore taxable income. Mr Morrison played down the heavily-redacted Treasury submission. “The numbers in the document released by Treasury are not Treasury numbers, but are a summary of a report from an ANU associate professor, Ben Phillips, that Labor uses to justify their negative gearing policy,” he said.

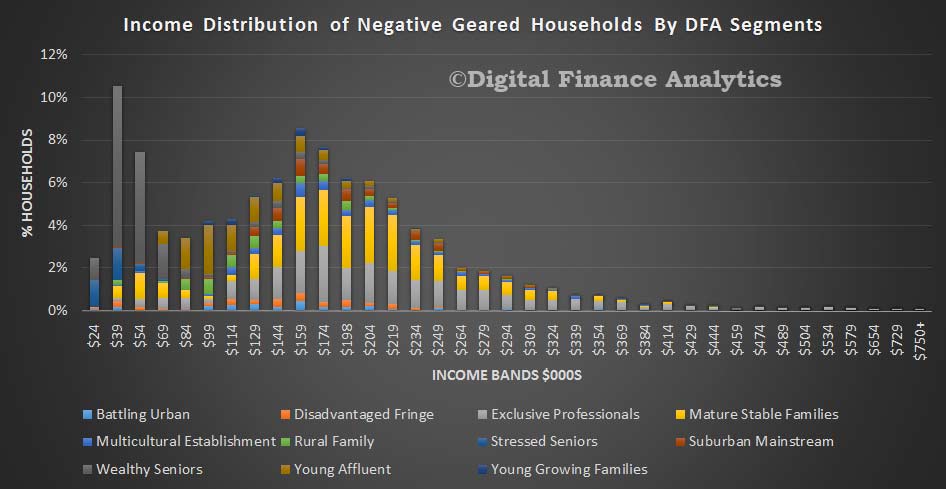

Worth then reflecting on earlier DFA analysis which showed how complex the negative gearing questions is. We pulled data from the DFA household surveys, to examine the distribution of negative gearing. Our segmented surveys, show some of the nuances in behaviour. We start with age distribution. We find that households of all ages may use negative gearing, but more than a quarter are aged 50-59. We see the DFA household segmentation in evidence, with a number of young affluent households active aged 20-29, especially using an investment property as an alternative to buying their own place to live. We discussed this before. As we progress up the age bands, we see a strong representation by the more affluent segments, including mature stable families and exclusive professionals. In later life, wealth seniors are also active, especially in the 60-69 year bands. So negative gearing is being used by households across all age groups.

Our survey suggests that negative gearing, whilst it is spread across the income bands, is indeed concentrated among more affluent households. Four segments, exclusive professionals, mature steady state, wealthy seniors and young affluent households contain the lions share of negative geared investment property. These segments are at different life stages, have different income profiles, and different strategies. For example the young affluent are often using investment property as a potential on-ramp to later owner occupied purchase, whereas wealthy seniors are all about income, and the others more wealth creation.

This analysis shows how complex the true situation is. Prospective changes are likely to impact different segments in diverse ways and there is plenty potential for spill-over impacts and unintended consequences. But the truth is, most negative gearing resides among more affluent households. The current settings are not correct.

Excellent post from Cameron Kusher, CoreLogic RP Data, discussing the impact of the higher tax being imposed by several states on foreign investors in the context of state tax raising – they are highly dependent on stamp duty to support their coffers. He concludes that ultimately these changes may deter some foreign investment but these changes are not going to scare off all foreigners from investing in housing market. At the same time it will raise much needed revenue for these governments. If state governments are looking at taxes on property, they should move away from stamp duty to a more efficient land tax.

The state governments of New South Wales, Victoria and Queensland are all now charging additional tax on foreign investment in residential property. In New South Wales foreign buyers are being charged a 4% stamp duty surcharge from June 21. In Victoria, foreign buyers are charged a 7% tax and in Queensland foreign buyers are being charged a 3% surcharge. All three of these taxes are specifically targeted on transactions of property by foreign buyers.

Property (both residential and non-residential) is already the largest source of taxation revenue for state and local government. These additional charges to foreign investors in the three most populous states will probably raise additional revenue (as long as the higher cost of doing business doesn’t result in a downturn in demand from overseas buyers). For each government there is a benefit in these changes outside of additional revenue, foreigners don’t vote so politically it is likely to be a fairly popular decision. Especially in New South Wales and Victoria where housing affordability is a growing problem and there is a perception that foreign investors are bidding up prices and contributing to locking first home buyers out of the market.

In New South Wales, state and local governments collected $14.705 billion in property taxes over the 2014-15 financial year. Property tax revenue increased by 12.8% over the year and has increased by 80.5% over the decade to 2014-15. Property taxes accounted for 48.5% of total taxation revenue to New South Wales state and local government in 2014-15.

In Victoria, state and local governments collected $12.246 billion in property taxes over the 2014-15 financial year which accounted for 53.1% of total taxation revenue. Property tax revenue increased by 10.7% over the 2014-15 financial year to be 109.9% higher over the past decade.

Queensland property tax revenue increased by 12.6% over the 2014-15 financial year to be 80.7% higher over the decade. Over the 2014-15 financial year Queensland state and local governments collected $8.267 billion in property tax revenue which accounted for 51.5% of total state and local government tax revenue.

Over the decade to June 2015, property taxes have increased by 80.5% in New South Wales, 109.9% in Victoria and 80.7% in Queensland, over the same timeframe inflation has increased by 30.1% which is significantly lower than growth in property taxation.

Given the importance of property tax revenue to state and local governments it is no wonder that the three largest states have decided to increase taxes on foreign investment. These changes don’t impact on voters and they collect additional much needed revenue.

My concern is that it shows that none of these states have any intention of moving away from transactional taxes on property to more efficient land taxes. Keep in mind that in a typical year only around 5% to 7% of residential properties are transacting so you are only collecting stamp duty from a small proportion of the housing market that are deciding to move. When transactions and values slow or fall, stamp duty revenue is also susceptible to large declines.

In New South Wales and Victoria, governments are gaining substantial revenue from stamp duty as property values and transactions rise. In New South Wales, stamp duty collection rose 22.2% in 2014-15, in Victoria it rose by 18.9% and in Queensland it was 12.3% higher. Over the past decade, the total increase in stamp duty revenue has been recorded at: 125.1% in New South Wales, 116.8% in Victoria and 56.1% in Queensland.

Some of the commentary around the increases in tax have been around the fact that without foreign investors many of the new housing (particularly unit) projects would never have even commenced construction. To me, this is really the crux of the problem. As the resource investment boom has faded to some extent housing construction has helped to fill the void. If a projects viability is totally dependent on foreign demand, to me that suggests that it is not really a viable project. The reality is that the current home value growth phase has now been running for four years and new housing construction and unit construction in particular has hit record highs. Foreign investment has increased quite significantly over this time however, many of these purchasers are buying units which many locals wouldn’t purchase due to the size, location and price of these properties. Furthermore, anecdotally many of these properties don’t actually create additional housing because they are left empty and not made available for rent.

I believe that these additional charges will provide some deterrent for foreign buyers investing as the costs continue to add up with FIRB application fees and now these additional charges. Of course, while these changes may deter some investors other will just see it as a cost of doing business and it shouldn’t impact them too much if they are investing for the long-term. If fewer foreign investors results in some new housing projects not going ahead, that is not necessarily a problem either in light of the fact that housing supply has increased dramatically over recent years and will continue to do so over the coming years given the housing currently under construction. Finally if it means that certain developers decide to rotate their offering away from one catering to foreign buyers and towards one which is more palatable to a local market, I believe that is a good thing.

Ultimately these changes may deter some foreign investment but these changes are not going to scare off all foreigners from investing in housing market. At the same time it will raise much needed revenue for these governments. If state governments are looking at taxes on property I would once again call on them to look for a way to move away from stamp duty to a more efficient land tax.

The Real Estate Institute of Australia (REIA) has unleashed the hounds on Labor’s proposed reforms to negative gearing. The REIA’s campaign, Negative Gearing Affects Everyone, follows the lead of the Property Council, which describes the Australian housing market as a “house of cards”, with the REIA stressing how “fragile” the Australian economy is. You might be tempted to dismiss this as propaganda from people who exaggerate for a living, but evidence is mounting of instability close to the REIA’s home: the off-the-plan apartment sector.

An array of forces are converging to give the multi-unit house of cards a shove. Over the past couple of years apartment development has boomed. The Australian Bureau of Statistics shows building approvals for new flats, units and apartments reached a huge peak last year. It has stepped down in the most recent quarter, but is still very high.

You can see this development in the skylines of our cities, especially in Sydney, Melbourne, Brisbane and Canberra – and in the RLB Crane Index. RLB counts a total of almost 650 cranes engaged in construction in our capital cities, and says more than 80% of these are on residential projects.

This coming supply is reflected in CoreLogic’s projections for new units hitting the market. It estimates that sales for more than 92,000 new units will be settled in the next 12 months, only slightly less than last year’s total number of sales of new and established units. The year after, a further 139,000 new units sales are due to be settled, substantially more than total sales (new and established) last year.

But for all this supply, it appears there may be much less demand than anticipated, particularly from the foreign investors who did so much to stoketheboom. Evidence for this includes:

Over the last six months the Chinese government has tightened controls over currency exchange by its citizens. This has restricted their capacity to buy – and repay loans to buy – property in Australia and elsewhere. This in turn has led to…

Credit restrictions by Australian banks. Last month each of the Big Four banks restricted how much they’ll lend to foreign buyers (lower loan-to-valuation ratios), with Westpac withdrawing altogether. This month, Macquarie has pulled its horns in.

Foreign demand for new dwellings (as gauged by the NAB’s Quarterly Australian Residential Property Survey) was already down over the first quarter of the year, before the credit restrictions cut in. Now the media are reporting that Chinese demand for apartments has “fallen off dramatically”: Meriton says the number of Chinese buyers of its apartments halved in the last month.

As those cranes in the sky indicate, there’s a lot of people out there – foreign and local – who’ve paid deposits and entered into contracts to pay boom-era prices on completion of their units. When they go to the bank to borrow the balance, they may find that, between lower loan-to-valuation ratios and lower valuations, they are caught short. Some might make up the difference by selling another property, but many of those settlements projected by CoreLogic may not settle at all.

The result: deposits forfeited, unsold units dumped on the market – accelerating the bust – and possibly, at least for buyers who are actually in the jurisdiction, the threat of being sued by developers for the loss of the contracted higher price.

So what might policymakers do?

Faced with such a calamity, why won’t our politicians do something to shore up demand for all these newly constructed rental properties? Oh wait….

This is precisely what Labor’s proposed negative-gearing reform promises do, by allowing rental losses to be set against non-rental income only where the property is newly built. Under Treasurer Bowen, Australia’s dedicated army of negative gearers would be given new direction and purpose, switching from the established dwelling market into the new-built market deserted by foreign buyers. Furthermore, because no-one after the first purchaser can call a dwelling new (and hence get the same preferential treatment on their gearing), they may be inclined to hang on to their properties even as demand looks weak.

We should still expect such a reform to reduce total investor demand for housing, and hence reduce house prices overall. These are both good things. But it may also help cushion what might otherwise be a drastic and painful collapse in the new-build sector.

Both the REIA and the Coalition government talk about Australia’s “transitioning” economy. They should consider negative-gearing reform as a measure for transitioning out of our presently fragile, property-bubble-led economy.

Author: Chris Martin, Research Fellow, Housing Policy and Practice, UNSW Australia

When politicians talk about tax and fairness, it’s easy for them to point out undeserved loopholes benefiting the wealthy, or multinational companies. But the elephant in the room is the difference between those who own and those who rent (or have recently bought and have huge mortgages) the house they live in.

The tax advantages of housing offend against justice on every count: they place financial stresses on the poor, they are unequal, and the increase in price is not deserved.

Owner-occupied houses are exempt from income and capital gains tax, and from social welfare means tests. Negative gearing gives investment properties a tax advantage, which is exacerbated by discounts on rates of capital gains tax. Rent assistance given to those on social security (currently a maximum of A$130 per week) is not sufficient to compensate for the difference.

The high price of housing is created by tax inequalities and by supply and demand imbalances created by government failure. At the same time, the government has encouraged banks to borrow hundreds of billions offshore to fund greater mortgage debt – pushing prices higher. Foreign depositors are faced with a low 10% withholding tax (reduced from 15%), and have not been subject to adequate money laundering controls.

And there is not much social benefit in higher house prices to counteract the costs to non-homeowners. Higher prices have not led to a significant increase in supply over time; people do not spend the increase, nor use it much to fund their retirement.

Defining ‘justice’

The word justice is used so widely, it needs some definition. While “fairness” is applied more widely, justice can be used to incorporate four sometimes conflicting objectives. Justice seeks, as much as possible to:

Contribute to economic equality

Give each person their just deserts

Meet people’s essential needs

Allow for personal liberty by not interfering in people’s lives.

Such a model of justice can be used to evaluate tax systems.

For those concerned that justice comes at a cost to efficiency and economic growth – there is considerable evidence to show that the relationship, where it exists, is positive. Giving people their just deserts provides the material incentives so beloved of economists. Evidence from a broad group of countries shows little overall relationship between income inequality and rates of growth and investment. Fairer taxes lead to greater compliance with tax laws. Research has found a significant increase in Australian tax morale between 1981 and 1995, which was explained by reforms that people saw as making the system more just.

Clouded by politics

Amid the ongoing debate about tax reform during the last year, many had hoped for some meaningful changes in the coming federal budget.

Instead, the current debate on the tax system, and more recently negative gearing, is concerned with perceptions of political acceptability.

This was also typified by the dismissal of any change to the taxation of housing in the Re:think tax discussion paper:

“Given the central importance of the home for Australian families, there is a strong consensus that it would not be appropriate to tax either the imputed rent on owner-occupied housing or capital gains derived from it.”

“Strong consensus”, whatever that means, is not a good reason if it involves injustice. The argument works the other way: given the central importance of the home, and its place in income and assets, it is essential for housing to be included in our tax and welfare systems. Let’s be the land of the fair go, even if we have to give up some personal advantages.

Reform options

Addressing the issue is complicated politically in that around 70% of voters own their houses, and a significant minority have borrowed heavily to get into the market in recent times. If prices drop, they will suffer through no fault of their own, as would the banking industry. With more than two million shareholders, banks are also strong politically.

The Henry tax review did, however, recommend a transition from stamp duties to a land tax, a significant increase in rental assistance and the removal (albeit with a high threshold) of the exemption of owner occupied homes from the means test for pensions.

The greater efficiency, and justice, of land taxes means that they have fairly widespread support from informed commentators. Taxes on property currently raise A$29 billion annually for the states and another A$14 billion for local governments in Australia. If land accounts for 50% of the value of residential housing, the additional revenue would be of the order of A$75 billion. Another A$40 billion might be possible if commercial land was also be included.

Removing capital gains discounts and taxing imputed rents should also be considered. Research released in 1994 found the latter would be both efficient and more equitable in Australia. The advantage of this is that such a system allows for the tax deductibility of mortgage repayments, so would provide compensation for the minority that had recently bought into the housing market. A higher withholding tax on international deposits would also reduce the availability of funds to push up assets, and encourage local businesses by removing some of the artificial support for the currency.

Housing accounts for more than 60% of the value of total assets held by Australians. Translated into imputed rent it amounts to about A$150 billion annually, or 20% of the gross personal income of those who own their homes. If taxed at marginal rates of tax, imputed rents would add about a third to current personal tax of A$190 billion annually.

This article is a summary of a paper “The justice of 2016 Australian tax and redistribution” to appear in the St Mark’s Review.

Author: Anthony Asher, Associate Professor, UNSW Australia

Long overdue changes to negative gearing and capital gains tax would save the Commonwealth Government about $5.3 billion a year, according to a new Grattan Institute report.

Hot property: negative gearing and capital gains tax reform shows that the interaction of a fifty per cent capital gains tax discount with negative gearing distorts investment decisions, makes housing markets more volatile and reduces home ownership.

The two measures in combination allow investors to reduce and defer personal income tax, at an annual cost of $11.7 billion to the public purse. Other taxes, which often drag more on the economy than a capital gains tax does, must be higher as a result.

And like most tax concessions, these tax breaks largely benefit the wealthy.

The report recommends that the capital gains tax discount should be reduced from 50 to 25 per cent, and that negatively geared investors should no longer be allowed to deduct losses on their investments from labour income.

A smaller discount would save about $3.7 billion a year, while the change to negative gearing would raise $2 billion a year in the short term, falling to $1.6 billion as losses start to be written off against positive investment income.

The reforms would provide relief to the Budget in tough times and slightly improve housing affordability with little impact on how much people save, says Grattan CEO and report co-author John Daley.

‘We estimate property prices would be up to two per cent lower under these reforms than they would be otherwise,’ Mr Daley says.

‘Contrary to urban myth, rents won’t change much, nor will housing markets collapse. The effects on property prices would be small compared to factors such as interest rates and the supply of land.’

The report recommends phasing in the reforms, to make them easier to sell and to prevent a rush of investors selling property before the changes come into force.

While other proposals, such as restricting negative gearing to new properties or limiting the dollar value of deductions, would improve the current regime, they nevertheless leave too many problems in place and introduce unnecessary distortions.

‘These two sensible reforms won’t hurt private savings much but will save the government a lot of money,’ Mr Daley says.

Australian prime minister Malcolm Turnbull has taken negative changes off the table for the May budget.

The announcement was made at a doorstop in Sydney this morning by Turnbull and treasurer Scott Morrison who noted that the federal government “had the common sense to leave the system as it is”.

They criticised Labor’s “reckless change, reckless housing tax” that would lead to homes being devalued and less investment.

“Labor’s housing tax plan will deliver a reckless trifecta of lower home values, higher rents and less investment,” said Turnbull. “The key to improving housing affordability is more houses, more dwellings.”

“Labor is taking a sledgehammer to the ambitions of mums and dads who want to invest — whether it’s established houses and apartments, commercial property, shares in listed companies, or shares in their own business,” he said.

The announcement confirms comments made earlier this morning by government minister Michaelia Cash.

“We have made a determination that based on where the housing market in Australia is at the moment, and it is unfortunately looking at prices dropping, we will be making no changes to negative gearing,” Cash told Sky News.

“We are going to back the Australian people every step of the way and not impose a tax.”

Shadow treasurer Chris Bowen said that the Turnbull government was determined to run “a great big scare campaign” noting that “the level of first home buyers is at its lowest, the number of investors buying is at its highest”.

The Panama Papers is a treasure trove of information on the activities and clientele of a large, but not atypical law firm operating in an offshore financial centre. In this case, it is a firm called Mossack Fonseca, based in Panama. It follows a series of spectacular leaks by the International Consortium of Investigative Journalists, including the HSBC files and the Luxembourg leaks. Here are six things that stand out from the latest revelations.

1. Same old techniques

Although it is still early days and it will take some time for the 11.5m files that were leaked from the Panama-based law firm Mossack Fonseca to be analysed, I have not come across any information on any new or unfamiliar techniques of tax avoidance. Everything that has been revealed so far: the use of offshore entities, nominee directors, accounting firms, legal firms and the like, is depressingly familiar.

2. Part of modern business

I am least surprised to learn about the profile of the typical Mossack Fonseca client. They are members of the globe-trotting elite: politicians, top echelon lawyers and accountants from a vast number of countries, some businessmen, many more in the business of finance.

In a book written by Richard Murphy, Christian Chavagneux and me on tax havens, we use the sub-title: How Globalization Really Works. We argue that tax havens are now a central component of the way international business is conducted. The Panama Papers leak is just further evidence that tax havens are an integral component of modern business.

3. A lot of it is legal

The law firm Mossack Fonseca is probably not any worse or better than your typical law firm specialising in offshore activities. If we have learnt anything from the various leaks about what takes place in the offshore economy, then it is that the accountancy and legal firms are key players in making them function.

Will this law firm be subject to penalties or taken to court? Very, very unlikely. In response to the leak, Mossack Fonseca have stressed the legality of their activities:

Our firm, like many firms, provides worldwide registered agent services for our professional clients (e.g., lawyers, banks, and trusts) who are intermediaries …

Finally, it is well established that many countries (e.g. UK, USA) have trust laws that permit a person or enterprise to represent a third party in a fiduciary capacity, which is 100% legal and serves an important purpose in global commerce.

It is up to the Panamanian government to take the firm to court to establish whether it broke the laws on compliance, due diligence and money laundering standards. Only then will we know if all their actions were legal, despite what the Panama Papers show.

What is worrying, though, is that when it comes to fighting tax avoidance (and evasion), it is highly likely that governments around the world will turn yet again to these large accounting firms and top law firms. The problem here is that these advisers then have the power to sell their expertise in tax planning to wealthy clients – after all, they know the law best, as they more or less wrote it.

4. Watch out for the whistleblower

The person who is likely to suffer most from the leak is its originator: the whistleblower. Their life – if they are identified – will be hell. Members of our globe-trotting elites will make sure of that. They are as likely to suffer from Putin’s henchman as from the courts of a leading and supposedly fair nation such as Sweden or the UK where they could be sued for the theft of the data.

Edward Snowden.360b / Shutterstock.com

The whistleblower who exposed wrongdoing at HSBC’s Swiss bank, Hervé Falciani, was sentenced to five years in prison by a Swiss court for industrial espionage, data theft and violation of commercial and banking secrecy. He has managed to escape imprisonment by living in exile in France, but it goes to show that whistleblowers do not necessarily have the law on their side. Edward Snowden who released the Wikileaks files remains in Russia, hiding from US prosecutors.

5. There’s a long way to go

The OECD may claim that there are no longer any unco-operative tax havens in the world; UK prime minister, David Cameron, may say that Britain is taking a lead in the fight against tax abuse. The reality is that there are a number of tax havens facilitating these secretive deals and Britain is connected to a lot of them. More than 100,000 companies in the leak are based in the British Virgin Islands, a British overseas territory.

The Panama Papers, which revealed the activity of only one legal firm operating largely in one of the less glamorous tax havens, Panama, is another reminder that we face a very long fight against tax abuse in the offshore economy, and anyone professing to have conquered that world is either wilfully misleading us or blissfully ignorant.

6. Public outcry is needed

To end on a positive note, the Panama Papers when added to previous leaks will have a cumulative effect on the public that cannot easily be predicted. It may fuel a complete and utter disgust with the establishment, and the further rise of either right-wing populist politicians such as Donald Trump in the US, or a left-wing social democratic response such as that espoused by Bernie Sanders in the US or Jeremy Corbyn in the UK. The perpetrators may get off lightly, as has been the experience so far with the other leaks, but the impact on society may yet be far reaching.

Author: Ronen Palan, Professor of International Politics, City University London

The driver to transact relate firstly to the tax effectiveness of the investment (37%) and capital gains from appreciating property values (25%). Low finance rates are helping, and investment property is perceived as offering better returns than bank deposits or stocks. We know that many in the eastern states will not make positive pre-tax returns, but taking tax breaks into account, they are still ahead, and will remain so unless there is a significant fall in home prices.

The driver to transact relate firstly to the tax effectiveness of the investment (37%) and capital gains from appreciating property values (25%). Low finance rates are helping, and investment property is perceived as offering better returns than bank deposits or stocks. We know that many in the eastern states will not make positive pre-tax returns, but taking tax breaks into account, they are still ahead, and will remain so unless there is a significant fall in home prices. There are some barriers which investors have to negotiate, the most obvious is they have already bought (40%), potential changes to regulation (25%), and inability to get financing (15%). Risks relating to budget changes have dissipated, and some are concerned about static or falling rents (bundled in the other category at around 5%).

There are some barriers which investors have to negotiate, the most obvious is they have already bought (40%), potential changes to regulation (25%), and inability to get financing (15%). Risks relating to budget changes have dissipated, and some are concerned about static or falling rents (bundled in the other category at around 5%). Solo investors have similar drivers with a focus on tax efficiency and potential capital gains, supported by low finance rates. We note that they have lower expectations of future gains than other investors (portfolio and those investing via SMSF).

Solo investors have similar drivers with a focus on tax efficiency and potential capital gains, supported by low finance rates. We note that they have lower expectations of future gains than other investors (portfolio and those investing via SMSF). Looking in detail at SMSF property investment, tax effectiveness, leverage and potential capital gains all drive the decisions. We did note some concerns about changes to superannuation regulation, especially around the caps, but this has not deterred prospective purchasers.

Looking in detail at SMSF property investment, tax effectiveness, leverage and potential capital gains all drive the decisions. We did note some concerns about changes to superannuation regulation, especially around the caps, but this has not deterred prospective purchasers. There are about four percent of SMSF’s holding residential property, and typically it comprises just a proportion of the total fund. A further three percent are actively considering adding in property to their SMSF.

There are about four percent of SMSF’s holding residential property, and typically it comprises just a proportion of the total fund. A further three percent are actively considering adding in property to their SMSF. It is also worth noting that mortgage brokers are becoming more influential in providing advice to trustees seeking SMSF advice, alongside accountants. Internet forums and web sites still play a significant role in providing advice to trustees. 17% say they know enough, and rely on their own knowledge and experience.

It is also worth noting that mortgage brokers are becoming more influential in providing advice to trustees seeking SMSF advice, alongside accountants. Internet forums and web sites still play a significant role in providing advice to trustees. 17% say they know enough, and rely on their own knowledge and experience. Finally, we highlight the “honeypot effect”, where interstate investors prefer to buy in the more buoyant states of NSW and VIC, than in their home states. We discussed this in detail in a previous post. And of course some first time buyers are going direct to the investment sector.

Finally, we highlight the “honeypot effect”, where interstate investors prefer to buy in the more buoyant states of NSW and VIC, than in their home states. We discussed this in detail in a previous post. And of course some first time buyers are going direct to the investment sector.