Sydney’s housing affordability crisis is being artificially exacerbated by “lunacy” tax incentives, a new report has claimed.

According to the analysis by the UNSW’s City Futures Research Centre, up to 90,000 properties are sitting empty in some of Sydney’s most sought-after suburbs as investors chase capital gains over rental returns.

The analysis’ researchers, Professor Bill Randolph and Dr Laurence Troy, said this is thanks to the “perverse outcomes” of tax incentives such as negative gearing, Fairfax has reported.

“Leaving housing empty is both profitable and subsidised by government,” Randolph and Troy told Fairfax.

“This is taxation lunacy and a national scandal.”

According to Fairfax, the 2011 census revealed that in Sydney’s “emptiest” neighbourhood of the CBD, Haymarket and The Rocks, one in seven dwellings was vacant.

Close behind were Manly-Fairlight, Potts Point-Woolloomooloo, Darlinghurst and Neutral Bay-Kirribilli, which all had vacancy levels above 13%. These neighbourhoods, together with central Sydney, account for nearly 7,200 empty homes.

The UNSW analysis of the 90,000 unoccupied dwellings across metropolitan Sydney compared the number of empty homes in a suburb against the rate of return investors made by renting out a property.

It found that properties in neighbourhoods with lower rental yields and higher expected capital gains were more likely to be unoccupied.

Gordon-Killara on the north shore had the highest share of vacant apartments, with more than one in six unoccupied on Census night, according to Fairfax. By contrast, only one in 42 dwellings (2.4%) in Green Valley-Cecil Hills, in Sydney’s west, was unoccupied.

These results suggest property investors in some of Sydney’s most desirable areas have become indifferent to whether their investment property is rented or not. Instead, investors are chasing capital gains with rental losses offset by negative gearing and capital gains concessions.

According to Troy and Randolph, this calls into question Sydney’s housing supply and affordability problem.

“If you choose to accept that there is a housing shortage in Sydney, then the sheer scale and location of these figures strongly suggest that this is an artificially produced scarcity,” they said, according to Fairfax.

Labor have announced proposals to change the negative gearing and capital gains tax rules relating to property investments. In an interview today on ABC Insiders, Chris Bowen, Shadow Treasurer said that negative gearing would potentially only be available on new property in 2017 , currently half of the benefit goes to top income earners, and proposes changes to CGT concessions, referring to the Murray FSI recommendations. 70% of benefit he says goes to top income earners. What “top” means was not defined.

Expect to see more tax reform shots exchanged as we progress through the year.

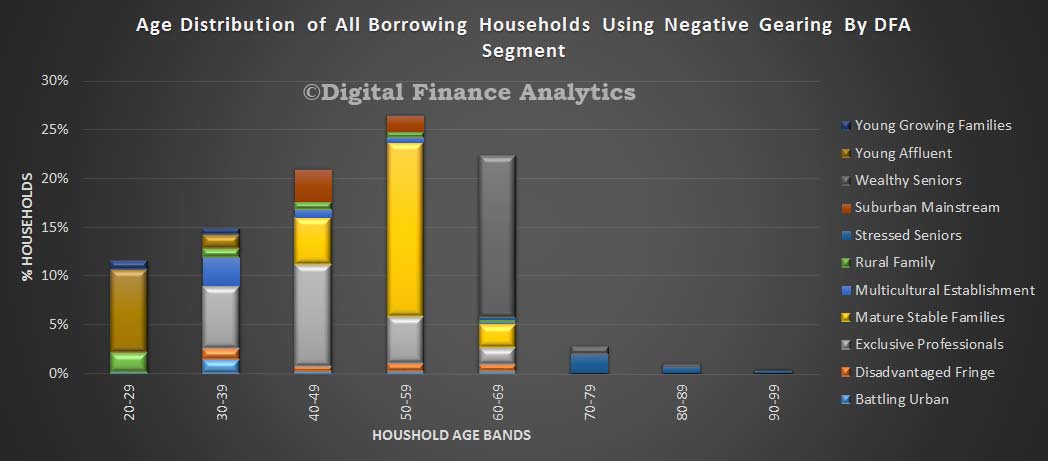

We decided to pull data from the DFA household surveys, to examine the distribution of negative gearing. Our segmented surveys, show some of the nuances in behaviour. We start with age distribution. We find that households of all ages may use negative gearing, but more than a quarter are aged 50-59. We see the DFA household segmentation in evidence, with a number of young affluent households active aged 20-29, especially using an investment property as an alternative to buying their own place to live. We discussed this before. As we progress up the age bands, we see a strong representation by the more affluent segments, including mature stable families and exclusive professionals. In later life, wealth seniors are also active, especially in the 60-69 year bands. So negative gearing is being used by households across all age groups.

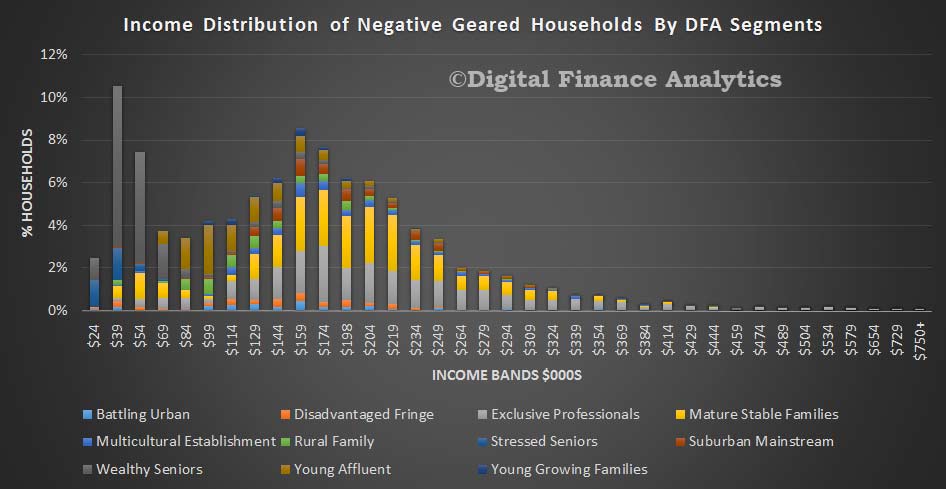

Then we looked at distribution, by segment, across the income bands. The horizontal scale shows the upper cut-off in each band, for example, the first is up to $24,000. Wealth seniors, with lower incomes are well represented in the lower income bands, but as income rises, we see a mix of households using negative gearing. What is true, is that there is a greater proportion of households in the $100-$200k band. Above that, there is a fall in all households represented, but we see those with very large incomes still represented to some extent. Again we see our segments highlighting the strong presence of exclusive professionals and mature stable families.

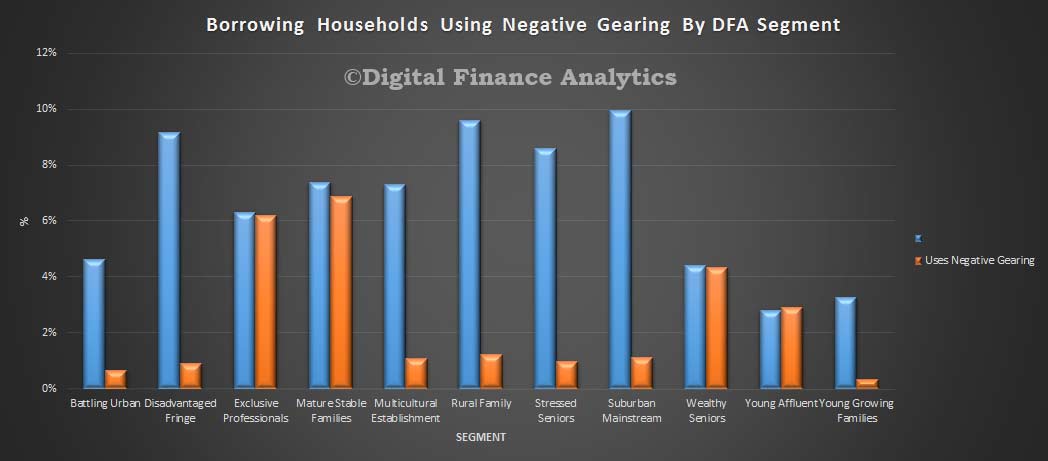

If we then look specifically at borrowing households using negative gearing, as compared to all households in the segments, the picture is quite striking. In our most affluent segment – exclusive professionals, nearly half are using negative gearing for property investment. Wealth seniors and mature steady state families are also well represented. But the most striking observation is that among young affluent households more than half are geared. Other segments are less represented.

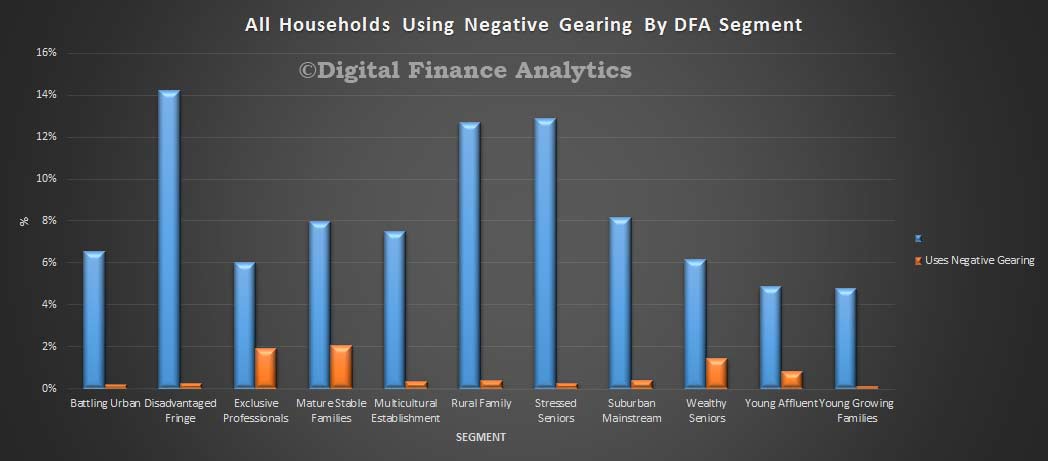

The final picture is all household, compared with those negatively geared. We see a concentration in the more affluent segments, and other segments where negative gearing hardly exists.

So, our survey suggests that negative gearing, whilst it is spread across the income bands, is indeed concentrated among more affluent households. Four segments, exclusive professionals, mature steady state, wealthy seniors and young affluent households contain the lions share of negative geared investment property. These segments are at different life stages, have different income profiles, and different strategies. For example the young affluent are often using investment property as a potential on-ramp to later owner occupied purchase, whereas wealthy seniors are all about income, and the others more wealth creation.

This analysis shows how complex the true situation is. Prospective changes are likely to impact different segments in diverse ways and there is plenty potential for spill-over impacts and unintended consequences. But the truth is, most negative gearing resides among more affluent households. The current settings are not correct.

In the RBA’s submission to the Inquiry on Home Ownership, they argue that negative gearing for investment property should be reviewed, because it has the potential to raise risks in the market, lift prices and distort the market.

John Fraser’s speech yesterday as Secretary to the Treasury, is significant because it does highlight some of the key issues driving future economic outcomes, and even our credit rating.

“The clear message is that we cannot rely on any cyclical bounce to reduce outlays as a percentage of GDP or, for that matter, the deficit. We are not in a crisis. But the Budget is rightly a focus of attention”.

“We have a structural budget problem that arose before the global financial crisis. A very substantial amount of the revenue windfall was used to lock-in long-term spending commitments”.

“Much of the deterioration in the budget position has been the result of revenue collections falling short of forecasts as we experience the flipside of the mining investment boom”.

“As a result, at 25.9 per cent of GDP, spending in 2015 16 is forecast to be close to the post-GFC peak, and could have been higher were it not for the measures taken by the Government in MYEFO”.”The Commonwealth’s interest bill has reached over a billion dollars a month. This is projected to more than double within the decade, unless action is taken to improve our budgetary position”.

“The Commonwealth achieving surpluses means that the States can run small overall deficits that they can use to finance productive infrastructure investment. This was a key conclusion of the 1993 National Savings Report commissioned by the then Treasurer, John Dawkins. In my view, this is still a sound framework for thinking about fiscal policy today. The rising structural deficits and debt give rise to intergenerational issues”.

“Around two-thirds of Commonwealth public debt is held by non-resident investors. This share has risen since 2009 and remains historically high. This, if anything, leaves Australia’s fiscal position a little more exposed to shocks in global capital markets”.

“It’s important that Australia maintain its top credit ratings, which helps to contain the costs associated with servicing public debt. Australia is one of only ten countries with a triple A credit rating from all three of the major rating agencies, reflecting our reputation for fiscal prudence”.

“But there have also been a number of policy decisions over recent years that have pushed the ratio higher: including increasing base pensions and supplementary payments, increased Defence operations and border protection spending, expenditure related to the carbon compensation package and the outcomes of negotiations around the repeal of the Minerals Resource Rent Tax. And the Government continues to face spending pressures”.

“There are many worthwhile spending programs and, every year, there are more good ideas than government resources to support them. There is also often, a mismatch between what the community expects the government to support and what they are prepared to pay for either in tax or in user charges. In framing budgets, we are really asking ourselves now and in the longer term what sort of society we want to have”.

“The ageing of Australia’s population will weigh heavily on Australia’s potential growth rate and long-term fiscal position. Demographic and broader medium-term pressures will place greater demands on government finances, making deficit and debt reduction more difficult”.

“Structural reform is critical and this includes reforming competition policy and implementing the Harper Review recomendations”.

“Improving productivity is a far more sustainable way to boost economic growth than relying unduly on an exchange rate depreciation”.

“These growth-enhancing policies also very much include tax reform. Tax is not just about raising revenue, it is also about helping to shape the economy so that we attract and deploy resources in a manner to promote long term growth. The arguments for a tax mix switch rest heavily on encouraging more jobs through a higher growth path. Tax reform is a complex issue and is very much the focus of the Government at the current time”.

The ATO has opened community consultation on its Digital by default initiative, as it continues its push to deliver better products and services for all taxpayers.

But unless the clunky and inefficient MyGov processes are substantially improved, this could be a disaster. DFA’s experience has been that the migration to a digital channel was suddenly imposed, without notice, and the supposed email alerts never arrived, leaving a gaping hole in messages from the ATO and risking tax penalties. It simply put the onus on the tax payer to go and log in on the off-chance there might be a new message and the ATO simply blamed “the system”. So whilst the theory might be good, it all comes down to excellence of execution, and so far, this is a major FAIL! A bland email alert, even it it did arrive is not acceptable.

Here is the ATO release:

The proposed change will deliver a simpler, easier, more flexible and adaptable way of interacting digitally with the ATO and puts the taxpayer experience at the forefront of service delivery.

Deputy Commissioner Michelle Crosby said the Digital by default initiative will require most taxpayers to use ATO digital services to send and receive information and payments, except where they do not have the ability to do so.

“More and more, people are carrying out their day-to-day business online and in the last couple of years a focus of ours has been to make sure our digital services meet the community’s needs. The Digital by default initiative is an extension of this commitment,” Ms Crosby said.

“For most people, it just makes more sense to use our online products, which offer a more personalised and convenient service.”

Ms Crosby said while there were lots of benefits to a digital approach, such as improved access to information at convenient times on the device or software of choice, and faster turnaround times, the ATO knows that for those who have relied on paper products it may be a big change.

“This ATO-led initiative will require people still using paper products to switch to ATO digital services. We’ll be providing time and support for those who need help to make the shift from paper to digital,” Ms Crosby said.

“We have released a consultation paper and are seeking feedback from all sections of the community. We want to make sure we have a fully-rounded understanding of the support needed to transition to digital services, the approach we take for those who cannot use digital services, and any concerns people might have.”

Ms Crosby said there would be some instances where it would not be possible to go digital due to individual circumstances.

“We will ensure that alternative services are available to this small group of people,” Ms Crosby said.

The current international tax regime was developed in the last century when the internet was not yet invented. At that time, a foreign company would typically require a substantial physical presence in Australia before it could be in a position to earn significant amount of income from Australian customers. This is what’s known in the tax world as permanent establishment.

The concept of permanent establishment is embedded in most domestic tax laws as well as virtually all the 3,000 plus tax treaties in the world. It dictates that in general, business profits of a foreign company will be subject to tax in Australia only if the company has a permanent establishment in Australia. In other words, the ATO cannot tax a foreign company’s profits if it has no permanent establishment in Australia.

The recent hearings of the Senate inquiry into corporate tax avoidance made it clear the tax structures of Uber, Airbnb, like their older peers Google and Microsoft, are designed to ensure income from Australian customers is earned by a foreign company that does not have a permanent establishment here. The permanent establishment concept is not effective for today’s digital economy.

Uber’s business and tax structure

Take Uber, which though established in the US, has a wholly-owned subsidiary in the Netherlands, which in turn has a wholly-owned subsidiary in Australia.

The most important asset of Uber is its digital platform that supports the app linking individual drivers and their customers. It’s unlikely this app was developed in the Netherlands. Despite this, Uber-Netherlands has the right to book income generated from customers in Australia.

For example, if a customer pays $100 for a ride in Sydney booked through the Uber app, the money is in fact paid to Uber-Netherlands. Out of the $100, Uber pays the driver about $75. The gross profit of $25 is booked in the Netherlands. This is so even though the transaction happens largely in Australia, including the driver, the customer and the ride.

Uber-Australia receives a service fee from Uber-Netherlands for its marketing and support services performed in Australia. The fee is determined based on the operating costs of Uber-Australia, plus a mark-up of 8.5%. The mark-up is effectively the taxable profit of Uber in Australia under its tax structure.

Airbnb’s business and tax structure

Airbnb, another young business founded in the US, has a structure very similar to that of Uber. Airbnb’s parent company in the US has a wholly-owned subsidiary in Ireland, which in turn has a wholly owned subsidiary in Australia.

Airbnb charges fees to both hosts and guests for accommodation booking through its digital platform. Instead of Airbnb-Australia, Airbnb-Ireland books the fee income generated from accommodation bookings in Australia. This is so even if the host, the guest and the accommodation are all in Australia. For example, if a Sydneysider uses the Airbnb app to book accommodation in Melbourne, the payment is in fact paid to Airbnb-Ireland. The host of the accommodation is then paid by Airbnb-Ireland which charges a fee of 3%.

Airbnb-Australia is responsible for the marketing activities in Australia. It receives a service fee from Airbnb-Ireland for those activities, and the fee is again computed based on its operating costs plus a mark-up.

Déjà vu – Google and Microsoft

Comparing the tax structures of Uber and Airbnb with that of Google and Microsoft reveals striking similarities. It suggests that the appetite for tax planning is comparable between established and relatively “young” technology companies.

The common pattern: a parent company in the US establishes wholly owned subsidiaries in market jurisdictions (such as Australia) as well as in low-tax countries.

While the commercial reality is that all companies in a group are effectively one single enterprise, the tax law in general treats each company as a separate taxpayer.

On one hand, the Australian subsidiary typically is responsible for marketing and support services that have to be physically done in Australia, and earns a service fee on a cost plus basis. The amount of profits subject to tax in Australia is usually very small compared to the income generated from Australian customers.

On the other hand, intellectual properties – which are often the most important and valuable assets of technology companies – are located in low-tax jurisdictions such as Ireland, the Netherlands and Singapore. This structure allows those low-tax subsidiaries to book the income generated from customers in Australia, and effectively shields the income from the Australian tax net.

Policy responses

Action item 1 of the OECD’s base erosion and profit shifting (“BEPS”) project is “tax challenges of digital economy”.

The original intention of the OECD was to explore how the 20th century international tax regime should be reformed in response to the digital economy in the 21st century. It quickly realised it was extremely difficult, if not impossible, to achieve international consensus on the intended reform. The often conflicting and vested interests among countries present a formidable obstacle to international consensus on meaningful reform of the international tax regime.

Instead of relying on the BEPS project to resolve the issue, Australia has followed the lead of the UK and is in the process of introducing the Multinational Anti-Avoidance Law – commonly known as the Google tax – to address the issue. As the new law incorporates concepts that are new and untested, it is not clear whether it will be effective.

In any case, it’s important to remember that multinational corporations are very agile. They may replace their “avoided permanent establishment” structures to circumvent any Google tax or to incorporate new tax avoidance tools.

Author: Antony Ting, Associate Professor, University of Sydney

Discussion of an increased GST at this week’s leaders’ retreat is based on two motivations.

Firstly, state governments expect future structural budget deficits if they are to meet growing outlays for expenditure on health, education and the national disability support scheme.

Second, as argued in the 2010 Henry Review and the current Re:think review, tax reform including an adjusted GST would contribute to a more productive and larger economy. A larger economy directly means more taxation revenue. Also, a larger economy is required to support entrenched community aspirations for more and better government services as well as more private expenditure.

There are pros and cons to a larger GST. On the positive side, relative to income tax and state stamp duties, a broad based consumption tax is a less distorting and costly tax to raise government revenue. On the negative side, a GST is a regressive tax which is passed forward to households as higher prices.

Balancing the pros and cons of a larger GST requires a package of tax changes, as was the case with the introduction of the GST in 2000.

The package would include:

a larger GST, involving a broader base, a higher rate or both

the replacement of existing high distorting state indirect taxes, including stamp duties

the recycling of some of the increased GST revenue as higher social security rates and a lower and more progressive personal income tax rate.

The latter would offset the regressive distribution effects of the GST. Specific details of the reform package should be topics for detailed assessment and then community discussion.

Manage the fairness issue

GST funds collected by the Commonwealth, net of administration costs, are currently distributed as general purpose, or non-tied, grants to the states (and territories). The allocation formulae is designed to meet an equity objective so that if each state applied a similar tax system it could provide a similar level of services to its citizens, referred to as horizontal fiscal equalisation (HFE).

The base of the current GST represents just under a half of a comprehensive measure of consumption expenditure. New Zealand’s GST is more comprehensive.

In Australia the main exemptions are fresh food, education, health, child care, water and sewage, and imports valued at less than A$1000. While these exemptions provide an element of progressivity to the GST, the effect is relatively small. Lower income households in general allocate a larger share of their expenditure to the exempt items. But, higher income households spend many more dollars on the exempt items.

The progressive income tax system and the means tested social security system are better targeted and more effective ways to redistribute income to meet social equity objectives.

Australia’s 10% GST rate compares with 15% for New Zealand, and above 20% for many European countries.

Broaden the base

Additional GST revenue could be collected if the base was broadened by removing some to all of the current exemptions, by raising the rate, or both. Either option could generate a similar additional revenue stream. For example, removing all exemptions would double the revenue stream, as would a doubling of the rate to 20%.

In terms of efficiency and simplicity, the base broadening option has the advantage.

On an equity basis, there is little difference between an approximate revenue neutral larger GST tax base and a larger GST tax rate. Why treat a necessity food now exempt different to a necessity clothing now taxed, or a utility electricity now taxed but not water now exempt?

While the current exemptions from the GST base add an element of progressivity to the GST when compared with a comprehensive base, the redistribution effect is small.

The main categories of GST exempt spending are fresh food, health, education, rent, and financial supplies.Re:think discussion paper – Treasury estimates using ABS 2011, Household Expenditure Survey 2009-10, cat. no. 6530.0, ABS, Canberra

More importantly, appropriate increases in social security rates and reductions in lower income tax rates as a part of a tax reform policy package are more direct and better ways to achieve distributional equity with a broader tax reform package.

Scrap inefficient state taxes

The revenue gained from a larger GST could be used to replace more distorting and inefficient state indirect taxes. A revenue neutral package would generate large productivity gains and some simplicity gains with minimal changes in equity and distribution of the aggregate tax burden.

State taxes that should be replaced include stamp duties on insurance, and perhaps a component of a wider reform package to replace conveyance duty on the transfer of property with a broad base and higher tax rate on property. Both the ACT and SA have begun a reform package to replace conveyance duty.

A GST reform package would change Commonwealth-state financial relations. Government leaders would have to resolve both the split of aggregate revenue from the reform package between the commonwealth and the states, and then the distribution of the aggregate revenue gain to the states between the different states. Clearly, there would be very different views about the plausible options to do this.

Author: John Freebairn, Professor, Department of Economics at University of Melbourne

Then we looked at distribution, by segment, across the income bands. The horizontal scale shows the upper cut-off in each band, for example, the first is up to $24,000. Wealth seniors, with lower incomes are well represented in the lower income bands, but as income rises, we see a mix of households using negative gearing. What is true, is that there is a greater proportion of households in the $100-$200k band. Above that, there is a fall in all households represented, but we see those with very large incomes still represented to some extent. Again we see our segments highlighting the strong presence of exclusive professionals and mature stable families.

Then we looked at distribution, by segment, across the income bands. The horizontal scale shows the upper cut-off in each band, for example, the first is up to $24,000. Wealth seniors, with lower incomes are well represented in the lower income bands, but as income rises, we see a mix of households using negative gearing. What is true, is that there is a greater proportion of households in the $100-$200k band. Above that, there is a fall in all households represented, but we see those with very large incomes still represented to some extent. Again we see our segments highlighting the strong presence of exclusive professionals and mature stable families. If we then look specifically at borrowing households using negative gearing, as compared to all households in the segments, the picture is quite striking. In our most affluent segment – exclusive professionals, nearly half are using negative gearing for property investment. Wealth seniors and mature steady state families are also well represented. But the most striking observation is that among young affluent households more than half are geared. Other segments are less represented.

If we then look specifically at borrowing households using negative gearing, as compared to all households in the segments, the picture is quite striking. In our most affluent segment – exclusive professionals, nearly half are using negative gearing for property investment. Wealth seniors and mature steady state families are also well represented. But the most striking observation is that among young affluent households more than half are geared. Other segments are less represented. The final picture is all household, compared with those negatively geared. We see a concentration in the more affluent segments, and other segments where negative gearing hardly exists.

The final picture is all household, compared with those negatively geared. We see a concentration in the more affluent segments, and other segments where negative gearing hardly exists. So, our survey suggests that negative gearing, whilst it is spread across the income bands, is indeed concentrated among more affluent households. Four segments, exclusive professionals, mature steady state, wealthy seniors and young affluent households contain the lions share of negative geared investment property. These segments are at different life stages, have different income profiles, and different strategies. For example the young affluent are often using investment property as a potential on-ramp to later owner occupied purchase, whereas wealthy seniors are all about income, and the others more wealth creation.

So, our survey suggests that negative gearing, whilst it is spread across the income bands, is indeed concentrated among more affluent households. Four segments, exclusive professionals, mature steady state, wealthy seniors and young affluent households contain the lions share of negative geared investment property. These segments are at different life stages, have different income profiles, and different strategies. For example the young affluent are often using investment property as a potential on-ramp to later owner occupied purchase, whereas wealthy seniors are all about income, and the others more wealth creation.