The Reserve Bank of New Zealand today urged greater attention be given to reducing housing market imbalances that are presenting an increasing risk to financial and economic stability.

In a speech to the Rotorua Chamber of Commerce, Reserve Bank Deputy Governor Grant Spencer said that: “Irrespective of the mix of demand and supply-based factors, the longer the excess demand persists, the further prices will depart from their underlying fundamental determinants, and the greater the potential for a disruptive correction.

In a speech to the Rotorua Chamber of Commerce, Reserve Bank Deputy Governor Grant Spencer said that: “Irrespective of the mix of demand and supply-based factors, the longer the excess demand persists, the further prices will depart from their underlying fundamental determinants, and the greater the potential for a disruptive correction.

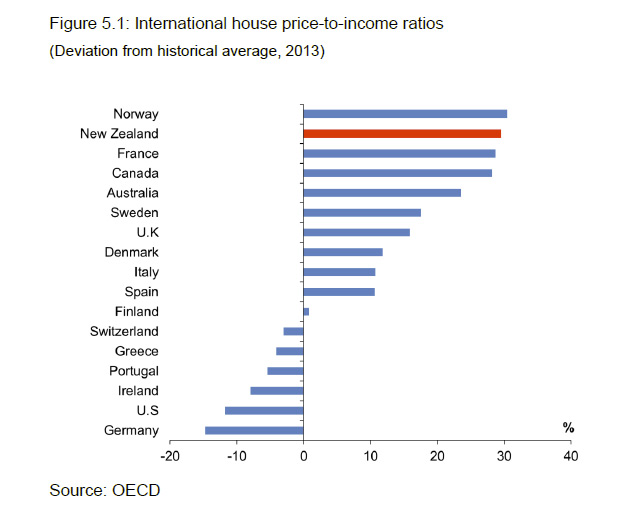

“Since late 2014, housing market imbalances have become more accentuated, particularly in Auckland where the supply shortage is greatest, and house prices are particularly stretched, having increased by three times since the start of 2002.

“New Zealand is one of the few advanced economies that has not had a major house price correction in the past 45 years.”

Mr Spencer said that a downward correction in house prices in New Zealand could be prompted by a range of potential shocks, such as rising global interest rates, or a downturn in the global economy and financial markets.

With 60 percent of its lending in residential mortgages, the New Zealand banking system could be put under severe pressure in such a downturn. The resulting contraction in credit would amplify the impact to the domestic economy and financial system, making it more difficult to avoid a severe downturn.

Mr Spencer said that policies to ease the supply constraints must be the main priority, but are unlikely to yield quick results.

Considerable scope exists to streamline the multiple approval processes required to complete a residential development. There is also a need to adopt a more integrated approach to the planning and funding of new infrastructure.

“The proposed RMA reforms have the potential to significantly improve the planning and resource consenting processes.

“The best prospect for substantially increasing the supply of dwellings over the next one to two years appears to be in apartment development. The Government and the Auckland Council might consider focussing their efforts on simplifying the approvals process and increasing the designated areas for high-density residential development.”

On the demand side, Mr Spencer said that there are practical difficulties in using migration policies to manage the housing cycle.

“Nor can monetary policy be used currently to dampen housing demand, as CPI inflation is below the Reserve Bank’s target range.”

However, measures should be considered to counter the growth in investor and credit based demand for housing.

The Reserve Bank would like to see fresh consideration of possible policy measures to address the tax-preferred status of housing, especially housing investment.

“Investors are often setting the marginal market prices that are then applied to the full housing stock within a regional market. Indicators point to an increasing presence of investors in the Auckland market and this trend is no doubt being reinforced by the expectation of high rates of return based on untaxed capital gains.”

Mr Spencer said that macro-prudential policy is a potential instrument to help restrain credit-based demand pressures and improve the resilience of bank balance sheets to a potential housing downturn.

“The introduction of loan-to-value ratio restrictions (LVRs) in October 2013 helped to moderate housing market pressures despite strong net inward migration and the ongoing shortage of housing. The LVR restrictions have also improved the resilience of bank balance sheets. They will be removed or modified as market conditions allow.

“Other macro-prudential options are being assessed, including in relation to investor lending. However, such tools are not a panacea – their impact is inevitably smaller than the main drivers of the current housing market imbalance.”