AMP Bank has classified non-resident borrowers as an “unacceptable borrower type” amongst a myriad of other tougher lending rules regarding foreign income lending.

In the note sent to mortgage brokers last week, AMP said non-resident borrowers will now be deemed an unacceptable borrower type, unless a spouse or defacto is a citizen or permanent resident of Australia or New Zealand and a borrower of the loan.

In addition, the non-major has also cracked down on foreign lending income from nine currencies, in particular the Chinese Yuan.

The changes, applicable to any applications on or after Monday 30 May 2016, see only 50% of income derived from the Chinese Yuan (salary, investment and rental) as acceptable.

Where the Chinese Yuan is used for serviceability, the maximum LVR has also been reduced to 50%.

Eight other foreign currencies have also been subject to tightened conditions, albeit to a lesser extent than the Chinese Yuan.

Only 80% of the further eight currencies – Canadian Dollar, EURO, British Pound, Hong Kong Dollar, Japanese Yen, New Zealand Dollar, Singapore Dollar and U.S. Dollar – will be deemed acceptable. In addition, these currencies will also now have a reduced maximum LVR of 70%.

In the note sent to mortgage brokers, AMP said the restrictions came “due to recent changes in the market in relation to non-resident and foreign income lending”.

A new article from Knowledge@Wharton highlights the potential disruption to the financial services industry from blockchain technologies. The decentralised approach enabled by blockchain has the potential to change customer relationships, offer new services, and challenge the role of central banks, and core financial systems. Start-ups and incumbents are squaring up in a fight for the future of the industry.

The basic rules of the game for creating and capturing economic value were once fixed in place. For years, or even decades, companies pursued the same old business models (usually selling goods or services, building and renting assets and land, and offering people’s time as services) and tried to execute better than their competitors did. But now, business model disruption is changing the very nature of economic returns and industry definitions. All industries are seeing rapid displacement, disruption, and, in extreme cases, outright destruction. The financial services industry, with its large commercial and investment banks and money managers, is no exception.

“Silicon Valley is coming,” JPMorgan Chase CEO Jamie Dimon warned in his annual letter to shareholders. He said startups are coming for Wall Street, innovating and creating efficiency in areas that are important to companies such as JPMorgan, particularly in the lending and payments space.

The payments startup Stripe has a multibillion-dollar valuation and a partnership with Apple Pay. Bitcoin companies and exchanges such as 21 and Coinbase are attracting tens of millions of dollars from venture capitalists. Peer-to-peer lending is booming in the small loan market with many players, including Upstart, Prosper, Funding Circle, and more. And the financial-planning startup LearnVest just got acquired for more than $250 million.

Many of these organizations are in the lending business, but are using big data and cloud technologies rather than tellers and branches to speed lending and customer acquisition. Others are leveraging network business models, such as peer-to-peer lending, to bring together would-be lenders and borrowers. According to Dimon, “We are going to work hard to make our services as seamless and competitive as theirs.” His underlying thought is this: If his company doesn’t keep pace with today’s well-capitalized upstarts, they will begin to lose relevance in a platform-centric world.

“In lots of areas, it looks like the blockchain will replace the current centralized business model of the financial services industry.”

There are many innovative, network business models that are coming after traditional financial services and banking organizations, and big banks are beginning to realize they must evolve in response if they want to remain viable in a digitally centric world — whether it comes by acquiring, partnering or developing leading-edge technologies. But what’s less clear is why, exactly, these new entrants are so disruptive and powerful. What enables them to skirt perceived constraints of these once ‘too large to fail’ incumbents and exploit unseen possibilities? In short, it is network-centered thinking with platform-based business models.

Control Shifting Away from Central Banks

In London’s Canary Wharf, a team of technologists and executives are trying to understand how to use blockchain technology to change the future of banking globally. Their leader is Blythe Masters, an ex-Wall Street commodities trader turned digital entrepreneur focused on turning the mental model and business model of the massive financial services industry and all its related parties (consumers, lawyers, accountants) on its head.

Bank executives worldwide are trying to figure out what this evolution in technology will mean for their firms. “We could go the way that file transfer technology changed music, allowing new businesses like iTunes to emerge. That is why there is such feverish activity at the moment,” said Michael Harte, chief operations and technology officer at Barclays, according to a recent article in The Financial Times.

For the massive financial services sector, blockchain technology (the software behind the digital currency, Bitcoin) offers an opportunity to overhaul its existing business model, including its banking infrastructure, approach to settlements and customer interactions. But acting on this opportunity, and making the most of the blockchain, is no easy task given the core beliefs and reinforcing systems that are embedded in the industry.

Networks Are Taking Over

What is the blockchain? It is a distributed database of computers that maintains records and manages transactions. Rather than having a central authority (such as a bank), blockchain uses the network to approve “blocks,” or transactions, which are then added to the “chain” of computer code. Cryptography is used to keep transactions secure, and the distributed nature of transaction approval makes the system harder to tamper with.

“It is only a matter of time before the broader financial services and banking industries shift to blockchain and network-based approaches.”

Blockchain technology has been hailed by its VC supporters as having revolutionary promise for all involved. “You should be taking this technology as seriously as you should have been taking the development of the Internet in the early 1990’s. It’s analogous to email for money,” said Masters, according to The Financial Times.

And blockchain enthusiasts believe that the application possibilities are endless — improving the way we hold and transfer secure goods from money to deeds to music to intellectual property. In fact, blockchain, as a pure platform technology, may be able to cut out the middlemen (or middle companies) everywhere, even disrupting other disruptors like Airbnb or Uber.

In the present financial services business model, a central ledger most often acts as the custodian of that information (such as the Federal Reserve and its member banks). But in a blockchain world, the information regarding each transaction is transparently held in a digitally shared database in the cloud, without a single central body acting as the middleman. This lack of central authority is the very feature that is turning the current mental and business models of traditional financial institutions on their heads.

In a lot of areas, it looks like the blockchain will replace the current centralized business model of the financial services industry and it is easy to see how it could revolutionize all of Wall Street. The ability of the technology to provide an unforgeable record of identity, including the history of an individual’s transactions, is one area being eagerly explored. David Grace, head of global finance at PwC, said that “if you have a secure distributed ledger, it could be used to store validated ‘know your customer’ data on individuals or companies. … It’s a potentially global application that could provide more security over identity data and where that data are stored.”

“It seems that the code can perform better than a real middleman in most cases.”

Clearly, we are entering a period of rapid evolution, as the financial services industry determines blockchain and what it means for their business models. Or, another scenario: A slew of startups identifies the possibilities and pulls the rug out from under big institutions. Traditional perceptions about the roles of financial players are already under attack — as it seems that the code can perform better than a real middleman in most cases. Old business models will soon fall prey to the quickly evolving technology and mental models. The network is about to do its magic: Grow and evolve without central control.

Network Business Models Will Dominate

Blockchain is already seeing use outside of the financial services sector, where it got its start. Technology and services giant IBM is adapting the blockchain methodology to develop a currency-less system that could be used for any purpose — for example, executing contracts upon delivery.

Arvind Krishna, senior vice president of IBM Research, believes that in the long run, this technology could facilitate transactions between banks or international businesses. “I want to extend banking to the 3.2 billion people who are going to come into the middle class over the next 15 years,” he said. “So I need a much lower cost of keeping a ledger. Blockchain offers some intriguing possibilities there.” A firm-centered or centrally controlled banking system clearly will not get him there, and the blockchain will allow him to leverage a digitally-enabled network as the way forward.

Join the Network Revolution

With companies such as IBM and JPMorgan Chase, as well as preeminent venture capitalist firm Andreessen Horowitz, backing this new way of facilitating financial transactions, it is only a matter of time before the broader financial services and banking industries shift to blockchain and network-based approaches Twitter to complement, or replace, the current centralized approach. The question is not whether network business models supported by blockchain technology will disrupt these organizations, but when. So if you are a member of the current financial services industry elite — or a local bank or credit union — it’s time to become part of the digital revolution and join the network and platform-emerging world.

Bank Negara Malaysia hosted the tenth meeting of the Financial Stability Board (FSB) Regional Consultative Group (RCG) for Asia in Kuala Lumpur.

At their meeting, members of the FSB RCG for Asia began by reviewing the FSB’s work plan and 2016 policy priorities, namely: promoting full, consistent and timely implementation of the international financial reforms; finalising the design of the remaining post-crisis reforms; and addressing new risks and vulnerabilities. They next considered vulnerabilities in the global financial system, their potential impact on Asia and possible policy responses, and regional financial stability issues.

In terms of new risks and vulnerabilities, members discussed the latest developments in financial technology and implications for financial stability. Related to this, they exchanged views on the latest trends and challenges in cybersecurity, supervisory approaches to enhance information technology risk management at financial institutions and market infrastructures, and the need for cooperation in cyber intelligence sharing, both domestically and cross-border. This discussion drew upon a 19 May workshop that took place in Hong Kong organised by the RCG – and involving both the public and private sector – that focused on financial technology and cybersecurity.

Members next turned their attention to corporate governance and steps being taken by regulators to address weaknesses identified during the financial crisis. Members shared experiences on how a robust governance framework can help the allocation of authority and responsibilities in a firm, in particular to its board and senior management; monitor performance; and ensure employees conduct business in a legal and ethical manner. Members also discussed mechanisms for strengthening individual accountability, including the role and responsibilities of the board, management and control functions.

In December 2015, the Basel Committee on Banking Supervision issued a second consultative document on Revisions to the Standardised Approach for credit risk as part of its broader review of the capital framework to balance simplicity and risk sensitivity, and to promote comparability by reducing variability in risk-weighted assets across banks and jurisdictions. Members discussed the revised proposal, including the use of external credit ratings to determine risk weights and the risk weighting methodology for different classes of assets. They also considered how the new proposal will impact banking systems in Asia.

The meeting concluded with a session during which members shared experiences with the implementation of resolution regimes, including requirements for recovery and resolution planning for domestically systemically important financial institutions. As part of the discussion, members explored ways to facilitate cross-border cooperation in the event of resolution actions.

The FSB Regional Consultative Group for Asia is co-chaired by Mr Norman T. L. Chan, Chief Executive, Hong Kong Monetary Authority and Mr Ashraf Mahmood Wathra, Governor, State Bank of Pakistan. Membership includes financial authorities from Australia, Cambodia, China, Hong Kong SAR, India, Indonesia, Japan, Korea, Malaysia, New Zealand, Pakistan, Philippines, Singapore, Sri Lanka, Thailand and Vietnam.

The FSB has six Regional Consultative Groups, established under the FSB Charter, to bring together financial authorities from FSB member and non-member countries to exchange views on vulnerabilities affecting financial systems and on initiatives to promote financial stability.

The FSB has been established to coordinate at the international level the work of national financial authorities and international standard setting bodies and to develop and promote the implementation of effective regulatory, supervisory and other financial sector policies in the interest of financial stability. It brings together national authorities responsible for financial stability in 24 countries and jurisdictions, international financial institutions, sector-specific international groupings of regulators and supervisors, and committees of central bank experts. Through its six Regional Consultative Groups, the FSB conducts outreach with and receives input from an additional approximately 65 jurisdictions.

The FSB is chaired by Mark Carney, Governor of the Bank of England. Its Secretariat is located in Basel, Switzerland, and hosted by the Bank for International Settlements.

Imagine not being able to go on holiday because you cannot get travel insurance or it costs more than the trip itself because of your health. Or what about being denied free car insurance with your new car or turned down for a mortgage because you’re too old. Then there are a whole host of banking services that aren’t easy to access – from sorting out your current account to managing your pension and savings – if you’re unsure about the internet or cannot afford to go online.

These are common experiences for millions of people across the UK who are denied access to everyday financial services because of disability, disease, age, lack of digital skills or because of where they live, and are the findings of a paper I co-authored, published by the Financial Conduct Authority, the major UK regulator.

In the course of the research, we came across numerous cases. For example, one man in his 30s and working for the armed forces was refused an extension to his mortgage. The reason was that it would take the term past the age of 60, the compulsory retirement age for the Armed Forces, even though he intended to work longer and his state pension would not start until the age of 67.

In another case, Alison was living with terminal cancer and was given two to five years to live though was in relatively good health. When arranging a holiday, she was turned down flat by many travel insurers while others said they would call her back but never did. In the end she went with the only firm that would cover her, paying £1,300 for insurance for a ten-day cruise in Europe.

Computer says no

Our research suggested that problems like these are only likely to grow as more services shift online and use automated processes that are not set up to deal with non-standard, “imperfect” consumers. This doesn’t even include people who live in rural areas with few bank branches and inadequate broadband and mobile reception, or the 17% of over-55s who have no access to the internet at all.

Many of us will have experienced the frustration of online systems that don’t quite fit our real-world circumstances. For “imperfect” consumers, the problem is far worse. Caught in a maze of impersonal processes, with decisions made by computers instead of people, there are those who are denied credit because their data is “thin” after working abroad for a number of years or on becoming newly widowed or divorced, with no financial products in their name.

In addition, as the population ages, more will bump up against blanket age limits and the proportion of people with health conditions is likely to rise.

The numbers above for different groups are stark and measuring the scale of these access to financial services issues is difficult. Many people turned down for a product do not complain, so do not appear in complaints statistics, and firms do not keep data on how many would-be customers they turn away. Other consumers self-exclude, not bothering to apply because they expect to be turned down, often based on bad experiences in the past.

Since the government abolished Consumer Futures (originally the National Consumer Council) in 2014, the UK no longer has a statutory consumer body with a remit to research these kinds of issues and without proof of the scale of a problem, regulators, government and firms are often reluctant to act. The sad irony is that these consumers are shut out of the system and therefore cannot communicate their needs or wants to firms designing and delivering basic products like pensions and mortgages.

Access issues are especially important. The cradle-to-grave welfare state is a thing of the past, if it ever really existed. There was, at least, a belief that social housing, the NHS and state benefits would catch the homeless, the sick, the frail and the elderly, as part of a caring society.

These days, we are all expected to look out for our own financial well-being, sorting out our own safety nets, secure places to live and viable retirement. But being denied access to financial services means being shut out of modern life and put in a very vulnerable situation.

Author: Jonquil Lowe, Lecturer in Personal Finance, The Open University

AAP says Australia’s major banks face soft profit growth amid growing macroeconomic risks linked to low interest rates and government tax policy, according to Fitch. However. the agency has reaffirmed the ratings of all four major Australian banks at AA- with a Stable Outlook.

The credit rating agency believes low interest rates and government tax policies have likely contributed to risks that include rising household debt and diminishing housing affordability related to strong house price growth.

“Pockets of Australia’s property market may encounter potential oversupply of new residential housing and hurt house prices in those areas,” Fitch says.

“However, a stable labour market and historically low interest rates should limit the impact on the banks’ asset-quality.”

Fitch expects housing price rises to moderate to about 2% in 2016 due to tightened mortgage underwriting standards for investors and non-resident borrowers.

It highlighted continued challenges for Commonwealth Bank, Westpac, National Australia Bank and ANZ from the downturn in the resources sector, which has already led to an increase in bad loans in WA and Queensland.

“Fitch expects soft profit growth in 2016, mainly reflecting asset competition, low interest rates, moderate credit growth and rising impairment charges,” Fitch said in a statement on Friday.

ANZ has already cut its interim dividend after its first-half profit slumped by nearly a quarter, Westpac this month lifted first-half cash earnings a below-expectations 3.3 per cent, and Commonwealth Bank lifted first-half cash earnings 3.9 per cent back in February.

NAB posted the best results of the big four, lifting cash earnings 6.5 per cent following the disposal of its unprofitable UK business.

However, Fitch said a stable labour market and historically low interest rates should limit the negative impact on banks’ asset quality should residential property prices decline in some areas due to potential oversupply.

The agency also forecast a continuation of tightened underwriting criteria imposed last year.

“Some portfolios, such as resources, are likely to continue experiencing asset-quality pressure due to weak commodity prices, which Fitch does not expect to improve in the short-term,” Fitch said.

“However, the banks’ exposures to mining and dairy remain manageable relative to total exposures.”

Fitch said a hard landing for the Chinese economy could hit the big Australian banks, but that such a scenario is not its base case.

The latest NAB research shows that anxiety is the main detractor of personal wellbeing in Australia – mirroring the results in many other advanced countries. But, some of us are managing our anxiety much better than others.

In this report, we asked how well “highly” anxious Australians think they are managing their anxiety. On average, around 60 per cent of highly anxious Australians believe they are coping well, around 25 per cent are managing but around 16 per cent are not coping.

The survey also reveals significant differences in how well different groups are coping with their anxiety. While both young men and young women identify as having high levels of anxiety, around 1 in 3 young women who have “high” anxiety say they are not managing their anxiety well – by far the biggest share of any group. In contrast, fewer than 1 in 10 young men with “high” anxiety believe they are not managing it well.

According to NAB Chief Economist, Alan Oster, “while this is clearly a concern, it is unclear to what extent young women feel more comfortable speaking about their ability to cope with anxiety than young men”.

Around 1 in 4 highly anxious singles and defactos are also not managing their anxiety well.

The report also updates NAB’s Wellbeing Index for the March quarter 2016. Wellbeing fell to 64 in Q1 2016 (64.4 in Q4 2015), with all measures rated lower, except anxiety, albeit it remains the biggest detractor of personal wellbeing.

Among key demographic groups, wellbeing was highest in Tasmania, capital cities, for high income earners (+$100K), men, over 50s, widows, two person households, those without children and professional and part time workers.

In contrast, wellbeing was lowest for singles, young Australians (particularly women), low income earners (less than $35,000) and labourers.

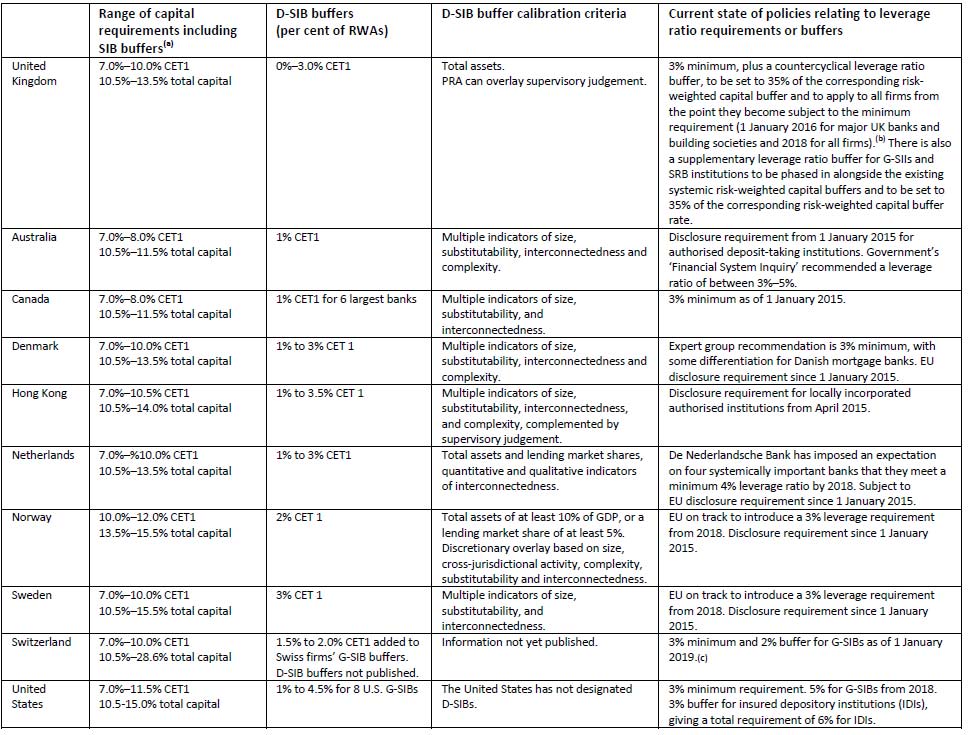

The framework highlights again that further risk capital will need to be held so that financial firms will be able to absorb losses while continuing to provide critical financial services. In the UK, depending on the size of the institutions, the buffer will be set between 0 and 3%. The SRB increases the capacity of UK systemic banks to absorb stress, thereby increasing their resilience relative to the system as a whole. The FPC judges that the appropriate Tier 1 capital requirement for the banking system is around 13.5% of Risk Weighted Assets.

Note, separately, an additional capital weight, per the Basel framework will apply for global systemically important banks (G‐SIBs).

Of special interest to Australian Banks is this table which shows that on a comparable basis, local banks here currently are required to hold less capital than peers in many other countries. Is the D-SIB here at 1% correctly calibrated? – especially, given 63% of all bank lending is residential property related?

The UK document just released, sets out the framework for the SRB that will be applied by the PRA to ring‐fenced banks, and large building societies that hold more than £25 billion in deposits and shares (excluding deferred shares), jointly, ‘SRB institutions’. The aim of the SRB is to raise the capacity of ring‐fenced banks and large building societies to withstand stress, thereby increasing their resilience. This reflects the additional damage that these firms could cause to the economy if they were close to failure. The FPC intends that the size of a firm’s buffer should reflect the relative costs to the economy if the firm were to fall into distress. The PRA will apply the framework from 1 January 2019 and later this year will consult on elements relating to the implementation of the SRB.

Overall, based on an analysis of the economic costs and benefits of going concern bank equity, the FPC judged the appropriate non‐time‐varying Tier 1 capital requirement for the banking system, in aggregate, should be 11% of RWAs, assuming those RWAs are properly measured. As up to 1.5 percentage points of this can be met with additional Tier 1 contingent capital instruments, the appropriate level of common equity Tier 1 capital is around 9.5% of RWAs. This judgement was made on the expectation that some of the deficiencies in the measurement of risk weights would be corrected over time. Until remedies are put into place to address this, the appropriate level of capital is correspondingly higher. On current measures of risk weighting, the FPC judges that the appropriate Tier 1 capital requirement for the banking system is around 13.5% of RWAs. This assessment refers to the structural equity requirements applied to the aggregate system that do not vary through time. In addition to baseline capital requirements, the FPC intends to make active use of the countercyclical capital buffer that will apply to banks’ UK exposures.

Under the SRB Regulations, the FPC is required to produce a framework for the SRB at rates between 0 and 3% of risk‐weighted assets (RWAs) and to review that framework at least every two years. The legislation implements the recommendation made in 2011 that ring‐fenced banks and large building societies should hold additional capital due to their relative importance to the UK economy. The FPC has considered its equality duty, and has set out its assessment of the costs and benefits of the framework.

Systemic importance is measured and scored using the total assets of ring‐fenced bank sub‐groups and building societies in scope of the SRB, with higher SRB rates applicable as total assets increase through defined buckets.

Those with total assets of less than £175bn are subject to a 0% SRB. The FPC expects the largest SRB institutions, based on current plans, to have a 2.5% SRB initially. Thresholds for the amounts of total assets corresponding to different SRB rates could be adjusted in the future (for example, in line with nominal GDP or inflation) as part of the FPC’s mandated two‐year reviews of the framework.

In July 2015, the FPC issued a Direction and a Recommendation to the PRA to implement the leverage ratio framework for UK G‐SIBs and other major UK banks and building societies on a consolidated basis. The FPC anticipates that the leverage ratio framework will be applied to UK G‐SIBs and other major UK banks and building societies at the level of the ring‐fenced bank sub‐group from 2019 (where applicable), as well as on a consolidated basis.

The Real Estate Institute of Australia (REIA) has unleashed the hounds on Labor’s proposed reforms to negative gearing. The REIA’s campaign, Negative Gearing Affects Everyone, follows the lead of the Property Council, which describes the Australian housing market as a “house of cards”, with the REIA stressing how “fragile” the Australian economy is. You might be tempted to dismiss this as propaganda from people who exaggerate for a living, but evidence is mounting of instability close to the REIA’s home: the off-the-plan apartment sector.

An array of forces are converging to give the multi-unit house of cards a shove. Over the past couple of years apartment development has boomed. The Australian Bureau of Statistics shows building approvals for new flats, units and apartments reached a huge peak last year. It has stepped down in the most recent quarter, but is still very high.

You can see this development in the skylines of our cities, especially in Sydney, Melbourne, Brisbane and Canberra – and in the RLB Crane Index. RLB counts a total of almost 650 cranes engaged in construction in our capital cities, and says more than 80% of these are on residential projects.

This coming supply is reflected in CoreLogic’s projections for new units hitting the market. It estimates that sales for more than 92,000 new units will be settled in the next 12 months, only slightly less than last year’s total number of sales of new and established units. The year after, a further 139,000 new units sales are due to be settled, substantially more than total sales (new and established) last year.

But for all this supply, it appears there may be much less demand than anticipated, particularly from the foreign investors who did so much to stoketheboom. Evidence for this includes:

Over the last six months the Chinese government has tightened controls over currency exchange by its citizens. This has restricted their capacity to buy – and repay loans to buy – property in Australia and elsewhere. This in turn has led to…

Credit restrictions by Australian banks. Last month each of the Big Four banks restricted how much they’ll lend to foreign buyers (lower loan-to-valuation ratios), with Westpac withdrawing altogether. This month, Macquarie has pulled its horns in.

Foreign demand for new dwellings (as gauged by the NAB’s Quarterly Australian Residential Property Survey) was already down over the first quarter of the year, before the credit restrictions cut in. Now the media are reporting that Chinese demand for apartments has “fallen off dramatically”: Meriton says the number of Chinese buyers of its apartments halved in the last month.

As those cranes in the sky indicate, there’s a lot of people out there – foreign and local – who’ve paid deposits and entered into contracts to pay boom-era prices on completion of their units. When they go to the bank to borrow the balance, they may find that, between lower loan-to-valuation ratios and lower valuations, they are caught short. Some might make up the difference by selling another property, but many of those settlements projected by CoreLogic may not settle at all.

The result: deposits forfeited, unsold units dumped on the market – accelerating the bust – and possibly, at least for buyers who are actually in the jurisdiction, the threat of being sued by developers for the loss of the contracted higher price.

So what might policymakers do?

Faced with such a calamity, why won’t our politicians do something to shore up demand for all these newly constructed rental properties? Oh wait….

This is precisely what Labor’s proposed negative-gearing reform promises do, by allowing rental losses to be set against non-rental income only where the property is newly built. Under Treasurer Bowen, Australia’s dedicated army of negative gearers would be given new direction and purpose, switching from the established dwelling market into the new-built market deserted by foreign buyers. Furthermore, because no-one after the first purchaser can call a dwelling new (and hence get the same preferential treatment on their gearing), they may be inclined to hang on to their properties even as demand looks weak.

We should still expect such a reform to reduce total investor demand for housing, and hence reduce house prices overall. These are both good things. But it may also help cushion what might otherwise be a drastic and painful collapse in the new-build sector.

Both the REIA and the Coalition government talk about Australia’s “transitioning” economy. They should consider negative-gearing reform as a measure for transitioning out of our presently fragile, property-bubble-led economy.

Author: Chris Martin, Research Fellow, Housing Policy and Practice, UNSW Australia

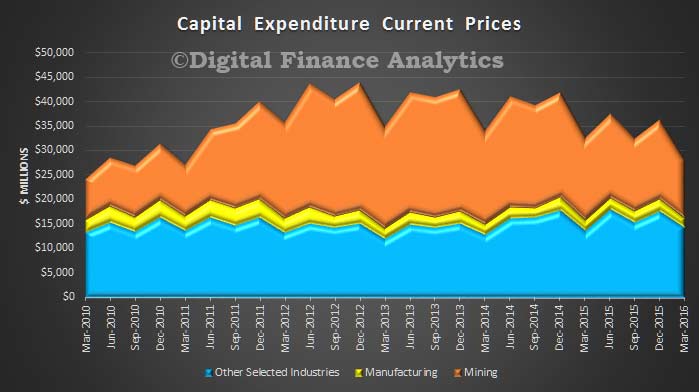

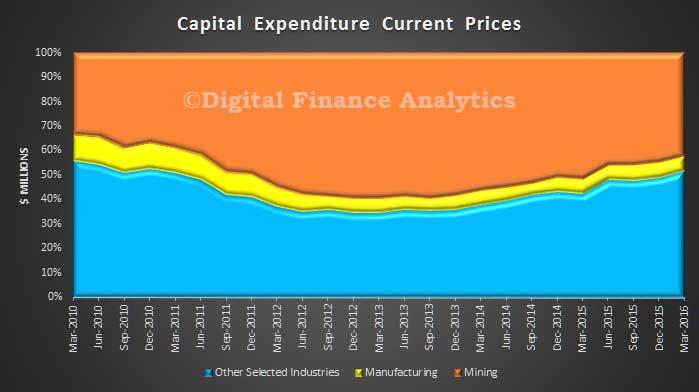

The latest ABS data on new private business capital expenditure highlights a further fall, with the trend volume estimate falling by 2.8% in the March quarter 2016 while the seasonally adjusted estimate fell by 5.2%. Within that, the estimate for buildings and structures fell by 3.6% in the March quarter 2016 while the seasonally adjusted estimate fell by 7.9% while the trend volume estimate for equipment, plant and machinery fell by 1.0% in the March quarter 2016 while the seasonally adjusted estimate fell by 0.5%.

The proportion of mining related expenditure continues to fall, relative to other sectors.

However. non-mining sectors also took a dive. Further evidence of a lack of business confidence and a reluctance to invest. Not good for prospective economic growth.

Earlier today, the Reserve Bank of Australia Payments System Board (PSB) published its Standard which relates to surcharges by merchants when charging customers for the use of a credit or debit card. Surcharges will be excessive where they exceed the permitted cost of acceptance, as defined in the Standard.

“In short, the new provisions will limit the amount businesses can surcharge customers for use of payment methods such as most credit and debit cards. The limit will be linked to the direct costs of the payment method such as bank fees and terminal costs,” ACCC Chairman Rod Sims said.

The Standard defines what businesses are able to include in setting a surcharge and sets out a two-staged implementation, with the ban commencing on 1 September 2016 for ‘large merchants’ and 1 September 2017 for all other merchants.

The Standard defines a ‘large merchant’ to be one that satisfies at least two of the following requirements: it has a consolidated gross revenue of $25 million or more, the value of its consolidated gross assets is $12.5 million or more, or it employs 50 or more employees.

The Standard will apply to six card systems – EFTPOS, Debit MasterCard, MasterCard Credit, Visa Debit, Visa Credit and American Express cards issued by Australian banks.

“The ACCC is finalising online guidance material for consumers and businesses, which will provide further information on the ACCC’s enforcement role, what businesses need to do in order to comply, and how consumers can make complaints if they believe a business has charged a payment surcharge that is excessive,” Mr Sims said.

“We will focus on education and awareness in the early stages but won’t turn a blind eye to possible breaches, particularly for those large businesses clearly on notice of these changes.”

The ban has no effect on businesses that choose not to impose a payment surcharge, such as the many businesses in Australia that incorporate payment system costs into their overall prices.

Material on the RBA’s website provides detailed information for businesses about the Standard, including how businesses can identify and quantify those costs that can be passed on to a consumer as a surcharge.

Those with total assets of less than £175bn are subject to a 0% SRB. The FPC expects the largest SRB institutions, based on current plans, to have a 2.5% SRB initially. Thresholds for the amounts of total assets corresponding to different SRB rates could be adjusted in the future (for example, in line with nominal GDP or inflation) as part of the FPC’s mandated two‐year reviews of the framework.

However. non-mining sectors also took a dive. Further evidence of a lack of business confidence and a reluctance to invest. Not good for prospective economic growth.

However. non-mining sectors also took a dive. Further evidence of a lack of business confidence and a reluctance to invest. Not good for prospective economic growth.