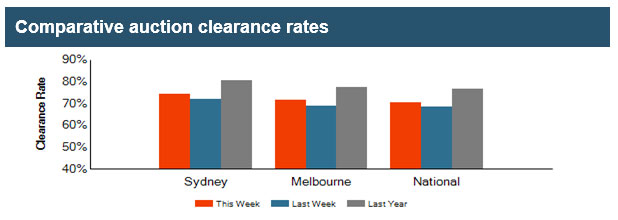

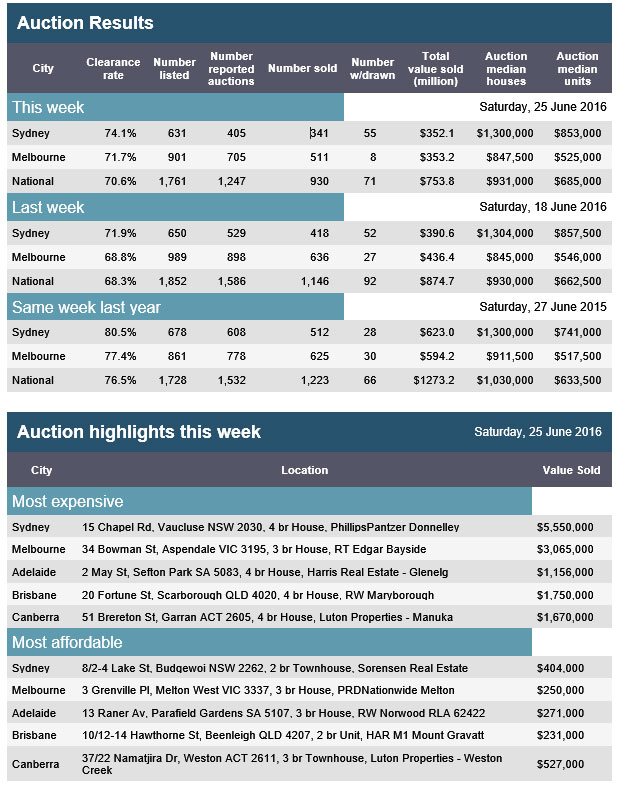

According to CoreLogic, the preliminary auction clearance rate was recorded at 69.1 per cent this week, having risen from 67.4 per cent last week. This week’s rise represents a further improvement from the recent low of 65.7 per cent over the weekend leading up to the Queen’s birthday public holiday. There were 2,189 auctions held across the combined capital cities this week, up from 2,183 over the previous week. Auction performance remains well below the comparable week last year when 76.9 per cent of the 2,249 auctions cleared. For the tenth week in a row, Sydney recorded a clearance rate that was in excess of 70 per cent.

More than 20 years after the first web server started bringing the internet into our lives, a recent conference in San Francisco brought together some of its creators to discuss its future.

In the last twenty years, we’ve managed to nearly ruin one of the most functional distributed systems ever created: today’s Web.

This might seem like a surprising statement. To many of us, the web has become an indispensable part of modern life. It’s the portal through which we get news and entertainment, stay in touch with family and friends, and gain ready access to more information than any human being has ever had. The web today is probably more useful and accessible to more people than it has ever been.

Yet for people such as Sir Tim Berners-Lee, the inventor of the world wide web, and Vinton Cerf who is often referred to as one of the “fathers of the internet”, Doctorow’s comment cuts right to the heart of the problem. The internet has not evolved in the way they had envisioned.

The centralised web

Their main concern is that the internet – and the information on it – has become increasingly centralised and controlled.

In the early days of the web, people who wanted to publish online would run their own web servers on their own computers. This required a reasonably good understanding of the technology, but meant that information was distributed across the internet.

As the web grew, companies that took the technical hurdles out of web publishing were established. With Flickr, for example, a photographer can easily upload his or her photos to the internet and share them with other people.

YouTube did the same thing for video, while tools such as WordPress made it easy for anyone to write blogs.

Social media in particular has made it easy for everyone to get online. The period in which these services really took off is generally referred to as web 2.0.

But along with this development of easy-to-use publishing technologies came a centralisation of the internet, and with that, the loss of some of the internet’s potential.

The decentralised web

Proponents of the decentralised web argue that there are three main problems with the web today: openness and accessibility; censorship and privacy; and archiving of information.

Openness and accessibility refers to the tendency of centralisation to lock people into a particular service. So, for example, if you use Apple’s iCloud to store your photos, it’s difficult to give someone access to those photos if they have a Microsoft OneDrive account, because the accounts don’t talk to each other.

The second issue – censorship and privacy – is a deep concern for people like Doctorow and Berners-Lee. Centralised web services make it relatively easy for internet use to be monitored by governments or companies. For example, social media companies make money by trading on the value of personal information.

As we use social media, fitness trackers and health apps to document our lives, we generate a lot of personal data. We freely give this personal data to social media companies by agreeing to their terms of service when we create our accounts.

The third issue with today’s web is that it is ephemeral; information changes and websites go offline all the time, and very little is retained or archived. Vinton Cerf has referred to this as the “digital dark age” because when historians look back at this point in history, much of the material on the internet won’t exist anymore – there will be no historical record.

A good example of this loss of history occurred when GeoCities, which hosted millions of web pages created by individuals, was first bought out by Yahoo and then discontinued.

The technologies to support a more decentralised web are already being developed, and are based upon some you are probably already familiar with.

One of the key technologies to support a decentralised web is peer-to-peer networking (or more simply, P2P). You might be familiar with this concept already, as it’s the technology behind BitTorrent – the software used by millions of Australians to illegally download new episodes of Game of Thrones.

On P2P networks, information is distributed across thousands or millions of computers rather than residing on a single server. Because the contents of the files or website are distributed and decentralised, it’s much more difficult to take the site offline unless you own of the files.

It also means that information uploaded to these networks can be retained, creating archives of old information. There are already organisations such as MaidSafe and FreeNet who are creating these P2P networks.

Other technologies, such as encryption and something called blockchain, provide levels of security that make transactions on these networks extremely difficult to track, and very robust.

Together these technologies could protect the privacy of internet users and would make censorship very difficult to enforce. It could also allow people to securely pay creators for online content without the need to an intermediary.

For example, a musician could make a song available online and people could pay the artist directly to listen to it, without the need for a recording company or online music service.

But do we need it?

Perhaps the biggest question with decentralising the web is whether it is actually something most people want or value. While archiving some parts of the internet is clearly valuable, there is probably a lot on the internet that can safely be forgotten, and some things that should be.

The technology itself is a hurdle to adoption. Peer-to-peer and blockchain technology are clever, but they are also complex. If decentralised web technologies are going to be widely used, they need to be easy to install and operate.

This isn’t an insurmountable problem, though. In the early 1990s, installing the software to get the internet working on your computer required substantial technical knowledge. Today it’s simple, and that’s one of the main reasons the internet took off.

Beyond the technical challenges, there are other social concerns that are potentially more substantial. Recently Facebook’s live streaming facility has raised questions about the level of control that should be exercised over internet media.

At the end of the day, it may be that the decentralised web is ready for us, but we’re not yet ready for it.

Author: Sam Hinton, Assistant Professor in Web Design, University of Canberra

Britain’s decision to leave the European Union has opened a fundamental crack in the western world. Australia’s relationship with the United Kingdom is grounded in the UK’s relationship with the EU.

Given Australia’s strong and enduring ties with the UK and the EU, the shockwaves from this epoch-defining event will be felt in Australia soon enough. Most immediately, the impending Australia-EU Free-Trade Agreement becomes more complicated and at the same time less attractive.

What will happen to trade ties?

The importance of Australia’s relationship with the EU tends to get under-reported in all the excitement about China. We might ascribe such a view to an Australian gold rush mentality. Nevertheless, Australia’s trading ties to the EU are deep and strong.

Such ties looked set to get stronger. In November 2015 an agreement to begin negotiations in 2017 on a free-trade deal was announced at the G20 summit in Turkey. Trade Minister Steven Ciobo said in April 2016 that an Australia-EU free trade agreement:

… would further fuel this important trade and investment relationship.

When considered as a bloc, the EU consistently shows up as one of Australia’s main trading partners. Consider the statistics below:

in 2014 the EU was Australia’s largest source of foreign investment and second-largest trading partner, although the European Commission placed it third after China and Japan in 2015;

in 2014, the EU’s foreign direct investment in Australia was valued at A$169.6 billion and Australian foreign direct investment in the EU was valued at $83.5 billion. Total two-way merchandise and services trade between Australia and the EU was worth $83.9 billion; and

the EU is Australia’s largest services export market, valued at nearly $10 billion in 2014. Services account for 19.7% of Australia’s total trade in goods and services, and will be an important component of any future free trade agreement.

This is all well and good. But when not considered as a bloc, 48% of Australia’s exports in services to the EU were via the UK; of the $169 billion in EU foreign direct investment, 51% came from the UK; and of Australia’s foreign direct investment into the EU, 66% went to the UK.

You get the picture.

The UK was Australia’s eighth-largest export market for 2014; it represented 37.4% of Australia’s total exports to the EU. As Austrade noted:

No other EU country featured in Australia’s top 15 export markets.

In short, the EU is not as attractive to Australia without Britain in it.

Beyond trade numbers

But the Australia-EU-UK relationship cannot be reduced to numbers alone. It also rests on values shared between like-minded powers.

Brexit represents the further fracturing of the West at a moment when that already weakening political identity is in relative decline compared to other regions of the world, notably Asia (or more specifically China).

EU-Australia relations rest on shared concerns such as the fight against terrorism advanced through police collaboration and the sharing of passenger name records. The EU and Australia also collaborated to mitigate climate change at the Paris climate summit. And they work for further trade liberalisation in the World Trade Organisation – but don’t mention agriculture.

Without the UK, these shared political tasks become harder.

Clearly, Australia-UK relations rest on a special historical relationship. However, it has seen efforts at reinvigoration, as British governments buckled under the pressure of the Eurosceptics among the Conservatives.

David Cameron addresses the Australian parliament in 2014.

Beyond everyday trade, historical links have been reinforced through the centenary of the first world war and the UK-Australia commemorative diplomacy that has come with this four-year-long event.

Cultural ties are most regularly and publicly affirmed through sporting rivalries such as netball, rugby and most notably cricket. Expect these ties to be reinforced as the UK seeks trade agreements and political support from its “traditional allies”.

For those with British passports, there will be a two-year period of grace as the UK negotiates its exit. After that, it will be quicker to get into the UK at Heathrow, but this might be small consolation for the loss of a major point of access to the EU.

The vote to leave is a major turning point in Europe’s history. It marks a significant crack in a unified concept of “the West”. It is not in Australia’s interests.

It’s time for Australia to make new friends in Europe.

Author: Ben Wellings, Lecturer in Politics and International Relations, Monash University

British people have woken up to the news that their country has voted to leave the European Union. Along with this, there has been turmoil in financial markets – the pound has hit a 30-year low and the FTSE dropped more than 8%.

Though the Brexit process will probably take two years (and the UK will remain a full member of the EU in the meantime), some aspects of the decision will affect British people straight away.

1. The pound in your pocket

There is inevitably going to be a period of uncertainty and turmoil. As the referendum result emerged, the pound fell 10% against the US dollar on the foreign exchange markets and 7% against the Euro. If this persists, things the UK imports, such as oil (affecting domestic fuel prices and petrol), foreign cars, coffee, bananas and clothing, will cost more. Overall, then, the general price level may rise meaning that your income will not stretch quite so far.

If you’re holidaying abroad over the coming months and haven’t bought your currency yet, the weaker pound means you’ll also now pay more.

2. Your job and income

A weak pound affects industry as well and so may impact on jobs. Company costs will rise if they import their raw materials and most firms will be hit by higher fuel prices. But the fall in sterling makes it easier for exporters to sell their goods and services abroad. So some jobs and wages may be more at risk, while recruitment rises in other areas.

Longer term, economists have been remarkably consistent in predicting that UK growth is likely to be lower outside the EU than it would have been inside. Businesses do not like uncertainty, so they may put off investing in new plant, machinery and jobs, as being outside the EU trading bloc may make trading with other countries more difficult and some firms may decide to quit the UK. This could mean that jobs and wages will be lower than they might otherwise have been, though not necessarily lower than today.

Before the referendum, Chancellor George Osborne threatened a post-Brexit emergency Budget that would cut public spending and raise taxes. This seems an unlikely immediate response since it would further depress the UK economy just when it is reeling with uncertainty and MPs across all parties were quick to say they would not support such measures. A new prime minister, due from October, may well appoint a new chancellor with his or her own ideas.

3. Your savings and pensions

Uncertainty while markets adjust and firms decide how to respond means the UK stock market is likely to be volatile for some time. Anyone who has recently retired and opted to take an income using drawdown (periodic cashing in of a pension fund still invested in the stock market) may have to take tough decisions about drawing less income now or risk running out of retirement savings later on.

Pensioners may face some complications.shutterstock.com

Savers have suffered since the global financial crisis of 2008 with rock-bottom interest rates. It’s unclear what might happen to these. On the one hand, rising consumer prices may push interest rates up; and credit rating agencies have said they may downgrade UK government debt which means the government would have to raise interest rates to persuade savers to buy its debt. But, if the economy struggles to grow, the Bank of England – which has said it stands ready to deploy any measures to maintain financial stability – might embark on new rounds of quantitative easing to keep interest rates low to encourage economic growth.

4. Your home and mortgage

While savers would welcome a rise in interest rates, this would increase mortgage repayments for borrowers and could even trigger repossessions. The International Money Fund has predicted that UK house prices could drop sharply post-Brexit. You might be concerned about that if you are in one of the six out of ten UK households that own their own home. But this could be good news for younger generations who have been struggling to afford a home.

Author: Jonquil Lowe, Lecturer in Personal Finance, The Open University

The results from APM Pricefinder for 25 June 2016 are out, and nationally, auction rates were 70.9%, up from 68.3% last week. Sydney cleared 341 sales at 74.1%, whilst Melbourne sold 511 at 71.7%. Results are still strong, though still a little lower than this time last year.

These results provide a leading indicator of property market activity based on a majority sample of auctions that take place every Saturday.

Bank of England Governor Mark Carney was admirably quick to read the unfolding economic dangers of a Brexit when the referendum result was declared. While stock markets and sterling plummeted amid developing financial stress, the governor’s statement immediately brought to mind the famous “whatever it takes [to save the euro]” intervention by European Central Bank chief Mario Draghi at the height of the eurozone crisis in July 2012.

Carney started by making clear that the British banks are safe since their capital requirements are now ten times higher than before the 2008-2009 financial crisis. The purpose of these high requirements is to ensure banks will be able to pay off their depositors, which aims to reduce the risk of a banking panic.

Indeed, the UK banks have been stress-tested against more adverse scenarios than what the Treasury thought that Brexit might trigger. The scenarios included residential property prices falling by over 30% and the level of GDP falling by 4% at the same time as a 5% rise in unemployment.

The governor was obviously seeking to reassure the public that whatever the economic/financial headwinds after the Brexit vote, British banks are rock solid and won’t see a repeat of the queues outside Northern Rock branches nine years ago.

Carney was absolutely right to do this. Lack of confidence in domestic banks often triggers recessions as depositors withdraw money, which restrict the banks’ ability to lend and keep the economy growing. This can be particularly lethal when combined with capital flight, which is where nervous investors offload a country’s currency and assets priced in the currency for fear that it is falling in value.

In Britain’s case, there were reasons on the ground to justify the intervention. British customers have queued outside banks to ditch sterling in an attempt to “hedge” against Brexit. And the news of sterling dropping like a stone on the night of the count was a strong signal that investor confidence was deserting the UK.

The worries of these investors are well summed up by the IMF’s warnings over Brexit:

[It] could entail sharp drops in equity and house prices, increased borrowing costs for households and businesses, and even a sudden stop of investment inflows into key sectors such as commercial real estate and finance.

The UK’s record-high current account deficit and attendant reliance on external financing exacerbates these risks. Such market reactions could sharply contract economic activity, further depressing asset prices in a self-reinforcing cycle.

The liquidity weapon

As well as the reassurances about strong banks, Mark Carney also said the Bank of England is prepared to inject up to £250bn of liquidity for financial institutions to keep the economy going in these difficult times ahead. Without doubt, this is substantial financial help amounting to some two-thirds of the £375bn that the central bank has already pumped into the system in the form of quantitative easing in recent years.

Carney also referred to “extensive contingency planning” with Chancellor George Osborne throughout the night, as well as mentioning potential “additional measures” such as providing substantial liquidity in foreign currency if it was needed. That might desperately be needed by British companies trading internationally which might be exposed to large fluctuations in exchange rates because of turbulence with sterling.

Yet the governor deliberately didn’t spell out what any other measures might be. One option might be to cut the base rate down to zero or even charge banks for “parking” their cash with the Bank of England. The European Central Bank is already doing this to encourage European banks to continue lending to the private sector.

Carney was right not to reveal his full defensive armour yet. Suffice for the time being to let both the public and the markets know he has other policy weapons in place and is ready to be tested if the economic conditions make it necessary.

Cameron steps down

The governor’s speech came shortly after David Cameron resigned. The British prime minister was trying to show a very brave face by delaying his departure to October. This makes absolute economic and political sense because the captain of a sinking (UK) ship has a moral obligation to be the last one to abandon it.

Yet in truth, the eurosceptic Tories would hardly trust him to start the Brexit negotiations with the EU when he has fought passionately to stay in. He therefore might lose his job much earlier than he thinks. Not that this would have made any difference to the markets – his defeat made his departure unavoidable. The only thing that might have further traumatised the markets would have been if he had not resigned.

But despite Carney and Cameron’s efforts to steady the markets, they could do nothing to disguise the UK’s lack of preparation or plans for handling the Brexit negotiations. There are many possible options for trade deals with the EU but no clear direction.

The Brexit camp, particularly Justice Secretary Michael Gove, has attacked the economic “experts” who overwhelmingly warned of the huge economic and financial risks of such a move. They warned that four UK companies would lose out for every one that benefits from leaving the EU.

The odd argument of the Brexit camp is that these experts have to be wrong because they did not predict the 2008-09 financial crisis. “Once wrong, always wrong,” in other words. Now that Mark Carney has had to step in while the politicians try and work out what happens next, we will know pretty soon whether we economists are going to be wrong this time around. Don’t be surprised if we haven’t seen the last intervention from the Bank of England.

Authors:Costas Milas,Professor of Finance, University of Liverpool; Gabriella Legrenz,Senior lecturer in economics, Keele University

The first stage of this year’s US bank stress tests highlights improving resilience with solid results despite a severely harsher scenario that included a more severe downturn than previous tests and negative short-term US Treasury rates, Fitch Ratings says. All 33 US bank holding companies passed the minimum capital ratio requirements. Tested firms overall generally performed better, posting higher capital ratios and smaller declines in capital ratios than in the past.

The largest global banks generally performed better than last year, although they still account for over half of projected losses under the severely adverse scenario, since they are subject to global market shock and counterparty default component. Pre-provision net revenue (PPNR) projections were noticeably higher this cycle, particularly for the five largest global trading and universal banks – Goldman Sachs, JP Morgan, Morgan Stanley, Citigroup and Bank of America. This more than offset higher losses from the stress scenario and may mean that some large global firms that typically revised capital plans post-DFAST won’t do so this year.

The test hit Morgan Stanley hardest in terms of capital erosion, although very high starting risk-weighted capital ratios gives it greater flexibility. It is more constrained by the leverage ratio, which had a projected minimum of 4.9%, leaving only a 90bp cushion above the requirement.

Among other weaker performers, two firms in the midst of M&A performed significantly worse than last year. Capital ratios for Huntington Bancshares may have taken a hit from the pending FirstMerit acquisition, resulting in a projected minimum common equity tier 1 (CET1) ratio of 5% – the lowest of all 33 banks. The First Niagara merger may be a key driver for the erosion of KeyCorp’s CET1 ratio to minimum 6.4%. These banks and others close to the 4.5% CET1 minimum threshold may constrain their capital return requests.

For firms that fared well quantitatively, the threat of a capital plan rejection for qualitative reasons under the second stage – Comprehensive Capital Adequacy Review (CCAR) – is still a significant hurdle. Modeling negative interest rates is likely to be more challenging for regional banks than global banks, like Citigroup, that already operate in markets with negative rates. The qualitative assessment may also bring up issues for new participants. Both are foreign-owned banks, which historically haven’t performed as well in the CCAR.

Credit card issuers and trust and processing banks performed well with the least capital erosion. However, their pre-provision net revenue projections were down compared to 2015, probably because of negative rate assumptions depressing interest income, which particularly impacts processing banks. Bank of New York Mellon and State Street’s PPNR projections fell around 20%-30%. Still, as in previous cycles, these firms showed projected net income over the nine quarters of the stress horizon, in contrast to net losses for firms with other business models.

Negative rates also had more impact on regional banks. The Fed said that firms more focused on traditional lending activities were more affected by this assumption.

Almost three quarters of the $526 billion in losses projected under the severely adverse scenario stemmed from loans, while 21% arose from trading and counterparty positions subject to the global market shock and counterparty default component. Projected loan loss rates varied significantly from 3.2% on domestic first lien mortgages to 13.4% on credit cards. The loss rate for domestic commercial real estate loans improved by 160bp to 7%, the first rise since 2012. The rate for commercial and industrial (C&I) loans deteriorated, jumping 90bp to 6.3%. C&I loan growth has been strong and the weaker performance may reflect energy sector weakness within these portfolios.

The people of the United Kingdom have voted to leave the European Union. Inevitably, there will be a period of uncertainty and adjustment following this result. There will be no initial change in the way our people can travel, in the way our goods can move or the way our services can be sold. And it will take some time for the United Kingdom to establish new relationships with Europe and the rest of the world.

Some market and economic volatility can be expected as this process unfolds. But we are well prepared for this. The Treasury and the Bank of England have engaged in extensive contingency planning and the Chancellor and I have been in close contact, including through the night and this morning. The Bank will not hesitate to take additional measures as required as those markets adjust and the UK economy moves forward. These adjustments will be supported by a resilient UK financial system – one that the Bank of England has consistently strengthened over the last seven years.

The capital requirements of our largest banks are now ten times higher than before the crisis. The Bank of England has stress tested them against scenarios more severe than the country currently faces. As a result of these actions, UK banks have raised over £130bn of capital, and now have more than £600bn of high quality liquid assets. Why does this matter? This substantial capital and huge liquidity gives banks the flexibility they need to continue to lend to UK businesses and households, even during challenging times. Moreover, as a backstop, and to support the functioning of markets, the Bank of England stands ready to provide more than £250bn of additional funds through its normal facilities. The Bank of England is also able to provide substantial liquidity in foreign currency, if required. We expect institutions to draw on this funding if and when appropriate, just as we expect them to draw on their own resources as needed in order to provide credit, to support markets and to supply other financial services to the real economy. In the coming weeks, the Bank will assess economic conditions and will consider any additional policy responses.

Conclusion. A few months ago, the Bank judged that the risks around the referendum were the most significant, near-term domestic risks to financial stability. To mitigate them, the Bank of England has put in place extensive contingency plans. These begin with ensuring that the core of our financial system is well-capitalised, liquid and strong. This resilience is backed up by the Bank of England’s liquidity facilities in sterling and foreign currencies. All these resources will support orderly market functioning in the face of any short-term volatility. The Bank will continue to consult and cooperate with all relevant domestic and international authorities to ensure that the UK financial system can absorb any stresses and can concentrate on serving the real economy. That economy will adjust to new trading relationships that will be put in place over time. It is these public and private decisions that will determine the UK’s long-term economic prospects. The best contribution of the Bank of England to this process is to continue to pursue relentlessly our responsibilities for monetary and financial stability. These are unchanged. We have taken all the necessary steps to prepare for today’s events. In the future we will not hesitate to take any additional measures required to meet our responsibilities as the United Kingdom moves forward.

The UK has voted to leave the European Union but even before all the votes were counted volatility made its way across Asian markets and to Australia.

The S&P ASX200 has finished 3.3% down at the close, wiping off approximately $50 billion in value, while the Australian dollar has dropped 3.4% to 73.4 US cents.

Richard Holden, Professor of Economics at UNSW says the volatility is likely to continue at least for another 24 hours.

“We could see volatility, perhaps not as extreme as the current levels, for a really extended period of time,” Professor Holden says.

One of the major factors in this will be how affected UK banks and therefore Australian banks will be by this decision, as they rely on short term funding for their operations.

“If those markets start to dry up and there’s uncertainty about their funding getting rolled over, one day to the next, then that’s when things can go pear shaped within an incredibly short period of time,” he adds.

The position of hedge funds, banks and other financial institutions in betting on currencies in over-the-counter markets (not regular currency markets) in times like this, also adds to the uncertainty.

“Basically we don’t know, what we don’t know and suddenly there’s a liquidity crunch and someone gets into trouble and that has flow-on effects like we saw in 2008,” Professor Holden says.

The S&P ASX200 index closed -3.3% following the Brexit vote.S&P ASX 200

He also warns that a drop in the Australian dollar shows that money could flow out of Australia and back to the UK as financial institutions there change their positions.

In the longer term, Brexit could affect the way Australian companies trade with the European Union through the UK.

“All of a sudden that’s going to be more complicated, it’s going to have to go through under some new trade agreement and we know that a series of bilateral trade agreements are always more complicated and have more nuance than large multilateral trade agreements,” Professor Holden says.

All this comes as Australia goes into the last week of an election campaign and this volatility will keep economic management top of mind for Australian voters.

“I don’t think either side of politics in Australia has an exclusive right to say they are going to be the best economic managers, I guess we’ll have to wait and see about that as well.”

Jenni Henderson, Assistant Editor, Business and Economy, The Conversation Interviewed Richard Holden,Professor of Economics, UNSW Australia