Internet users in the UK prefer digital channels to in-store shopping in almost every stage of the path to purchase, according to a survey from retail consultancy Pragma conducted in June 2016. In fact, only when it comes to making the final purchase decision and resolving any post-purchase issues do those surveyed prefer the in-store experience.

Internet users in the UK overwhelmingly prefer digital shopping for keeping up-to-date with the latest products, attaining detailed product information, and even simply browsing products. The Pragma survey reveals that in-store experiences are failing users for these basic shopping tasks.

Even the act of making a purchase is one preferred to be done online. Brick-and-mortar shopping was only judged better for making the final decision on a purchase or sorting out any issues afterward.

It’s little wonder that internet users in the UK are directing ever more of their shopping activities to the web. In fact, nearly 95% of those surveyed said in June that they shopped online the same amount or even more often than two years ago. And while, at some point, as more and more people shop exclusively online, that “more” response will top out and shrink, the fact that only 4% say they’re shopping online less than they used to—compared to 32% shopping less in physical stores—reinforces the idea that in-store shopping is failing users.

In June 2016, eMarketer estimated that there will be 44.4 million digital shoppers in the UK in 2016, which accounts for 93.8% of all UK internet users. These digital shoppers will browse and research products online, but not necessarily make a purchase that way. However, a large share of them will go on to buy: 94.9% this year, suggesting shoppers are happy with the experience. By 2020, 95.3% of digital shoppers in the UK will make a digital purchase.

Australia’s banks have always enjoyed a lucrative income from credit card “interchange fees”, the charges that the banks levy on merchants’ sales. These fees amount to AU $2.5 billion a year which are ultimately passed on to consumers.

Unwilling to share any of this revenue with Apple, all but ANZ and American Express have refused to adopt Apple Pay. Instead, four of the largest banks, NAB, Westpac, Commonwealth and Bendigo and Adelaide have asked Australia’s competition regulator, the ACCC, for permission to act collectively to negotiate with Apple over access for their own digital wallet products on its phones, tablets and watches.

The banks, along with their industry representatives are claiming that they are taking this action in the interest of providing “Australians with real choice and better outcomes”. They are also allegedly concerned about security and standards surrounding the way in which customers add their cards to Apple Pay.

Even if granted, the likelihood of Apple negotiating access to the underlying payment mechanisms in the phone to the Australian banks is zero. Ceding on this would not only require Apple to create the mechanisms by which third parties could integrate with the hardware and software in their devices but it would essentially be giving up on the substantial global revenue derived from Apple Pay that is only set to grow.

Giving in to Australian banks, which in total represent a small fraction of their overall Apple Pay earnings, would mean opening up access to Apple Pay to every bank globally. Something that Apple would never do. Apple would be more likely to forego Australia altogether before taking that radical a step.

If anyone had an anti-competitive complaint to make, it would be Google and Samsung whose Apple Pay alternatives, Android Pay and Samsung Pay are also not compatible with the iPhone platform. The fact that they haven’t complained about this as such is because it wouldn’t be worth their while competing with Apple Pay which is integrated into the underlying operating system.

The banks would like to claim that their own technology somehow would be better than using Apple Pay. The banks’ tap and pay apps however require opening them up and entering a PIN, logging in or using a fingerprint login, rather than simply holding the phone against the tap and pay terminal with your thumb on the home button. The banks’ apps have also been historically beset with issues and delays in supporting new versions of Android in particular.

Perhaps Apple should not feel particularly victimised however. The Commonwealth Bank, Westpac and NAB have rejected any support for Android Pay or Samsung Pay as well.

ANZ is the only Australian bank to have taken on Apple Pay after originally being part of the other banks’ initiative to collectively bargain with Apple. The move by ANZ CEO Shayne Elliott to be the bank to adopt the latest mobile digital technology is a smart one because it has clearly differentiated ANZ as a technological leader in this space. Elliott claims that the support of Apple Pay has attracted new customers to the bank.

ANZ’s and American Express’s support for Apple Pay and Android Pay has actually given customers what they want. What they want is to be able to use what large numbers of other people in other countries can use. Being part of the “Apple” or “Samsung” or “Android” group forms part of a user’s self and social identities and fulfils a psychological need of relatedness. Being excluded from this group by banks whose predominant consideration is profits will only cause dissatisfaction and resentment amongst their customers.

ANZ’s acceptance of Apple Pay will presumably also weaken the case of the other banks that they are being disadvantaged by Apple’s closed payment system. The brinkmanship of the banks will come to a head next year when the NSW transport system starts trialling the use of tap-and-pay cards to pay for travel. If the experience in London is anything to go by, this will drive even greater use of mobile tap-and-pay which for iPhone or Apple Watch users benefits only ANZ, American Express and Apple.

Author:David Glance, Director of UWA Centre for Software Practice, University of Western Australia

A status update has just been released describing some of the steps taken to reform the wholesale Fixed Income, Currency and Commodities (FICC) markets, following the earlier review. Whilst some of the legal and process related issues have been addressed, there are many cultural and behaviourial issues which remain to be addressed by market participants. The review stresses that Firms must create, both individually and collectively, cultures that place integrity, professionalism and high ethical standards at their core to ensure that behaviours are not limited to complying with the letter of regulation or laws. It took years for the ‘ethical drift’ that resulted in misconduct to occur and it will take time to build new ethical norms in financial markets. Progress is at a critical point.

The Fair and Effective Markets Review (FEMR) was launched in June 2014 to conduct a comprehensive and forward-looking assessment of the way the wholesale Fixed Income, Currency and Commodities (FICC) markets operate; help to restore trust in those markets in the wake of a number of high profile abuses in both UK and global financial markets; and to influence the international debate on trading practices.

On 10 June 2015 a Final Report was published, setting out 21 recommendations to:

raise standards, professionalism and accountability of individuals;

improve the quality, clarity and market-wide understanding of FICC trading practices;

strengthen regulation of FICC markets in the United Kingdom;

launch international action to raise standards in global FICC markets;

promote fairer FICC market structures while also enhancing effectiveness; and

promote forward-looking conduct risk identification and mitigation.

Now a status update has been presented to Chancellor of the Exchequer, the Governor of the Bank of England and the Chairman of the Financial Conduct Authority.

The job is far from done. A key theme that came out of the ‘Open Forum’ held by the Bank in November 2015 was that there remains a lack of trust in financial markets and financial institutions because of past misconduct. Participants saw cultural and ethical changes as an essential component of building a social licence for financial markets.

Responsibility must now fall increasingly to market participants to see through the changes in market practices and behaviours that are necessary to restore the reputation of the industry and thereby deliver markets that are both fair and effective. Firms must create, both individually and collectively, cultures that place integrity, professionalism and high ethical standards at their core to ensure that behaviours are not limited to complying with the letter of regulation or laws. As was indicated in the Final Report, a failure to do so will inevitably lead to further regulation and/or legislation.

While authorities can put in place legislation and regulation, firms are responsible for creating, both individually and collectively, cultures that place integrity, professionalism and high ethical standards at their core to ensure that behaviours are not limited to complying with the letter of regulations or laws. The work of the FMSB to ensure that market practices and structures are consistent with broader principles of fairness and effectiveness is therefore of vital importance and must be sustained. The complementary work of the Banking Standards Board (BSB) to promote high standards of behaviour and competence in the banking sector has a crucial role to play in this area too and we strongly support its work.

They state that the initial momentum must not be lost. It took years for the ‘ethical drift’ that resulted in misconduct to occur and it will take time to build new ethical norms in financial markets. Progress is at a critical point. It requires all involved to see through the changes that have begun, and to be alert to future challenges, if the financial services of tomorrow are to be characterised by the high standards of fairness and effectiveness to which we aspire.

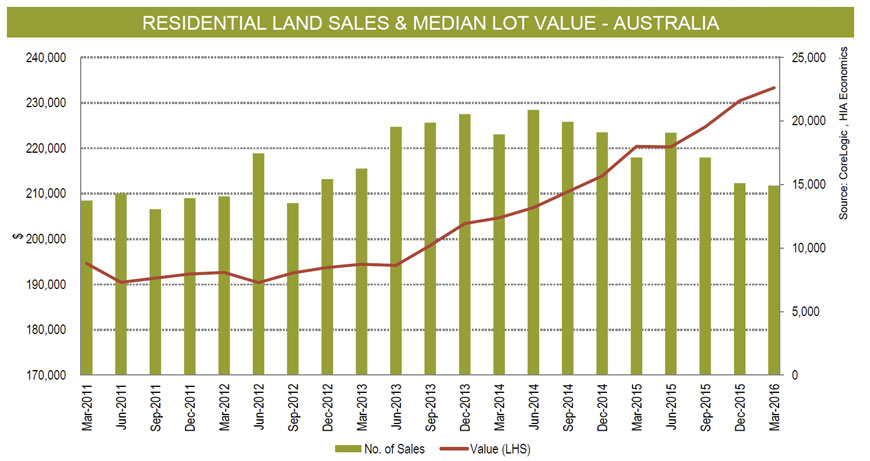

The March 2016 edition of the HIA-CoreLogic Residential Land Report has just been released by the Housing Industry Association, and CoreLogic. The report provides detailed results relating to prices and sales activity across Australia’s residential land markets.

During the March 2016 quarter, the pace of growth in national land prices slowed to 1.2 per cent, while turnover in the market fell by 1.3 per cent. The easing of price pressures was helped by a 3.4 per cent increase in land sales in capital city markets, although the number of transactions in regional Australia fell by some 8.1 per cent over the same period.

During the March 2016 quarter, vacant residential land sales increased most strongly in Perth (+22.3 per cent) followed by Melbourne (+5.2 per cent). However, land market turnover fell in Hobart (-28.4 per cent), Adelaide (-8.3 per cent), Sydney (-5.9 per cent) and Brisbane (-3.4 per cent) over the same period.

“The easing of price growth in the market for residential land is an encouraging sign, particularly given more favourable supply conditions in capital city markets,” HIA Senior Economist, Shane Garrett pointed out.

“However, the value of residential land remains at record highs. This is a key source of affordability difficulties confronted by the many Australian families wishing to purchase their first home,” Shane Garrett cautioned.

“Current arrangements around the funding and delivery of the infrastructure that services new housing are inadequate and preventing the release of more affordable residential land stocks.”.

“As well as hurting ordinary families, the absence of comprehensive reform is paring back Australia’s future growth prospects,” concluded Shane Garrett.

According to CoreLogic research director Tim Lawless, the moderation in the number of vacant land sales has been evident for some time. “National land sales peaked during the June quarter of 2014 and have been trending lower since this time. The quarterly number of vacant land sales hasn’t been this low since the third quarter of 2012,” said Mr Lawless.

“It’s encouraging to see capital city land sales bucking the national trend with an increase of 3.4 per cent over the March 2016 quarter. However, despite the quarterly rise in sales, the number of transactions was still 12.3 per cent lower than in the March quarter of 2015,” added Mr Lawless.

“The fact that vacant land prices are still broadly rising on both a median price and rate per square metre measure, albeit at a reduced pace, at a time when transactions numbers are consistently trending lower sends a clear signal that demand for well-located vacant land remains strong,” Mr Lawless noted.

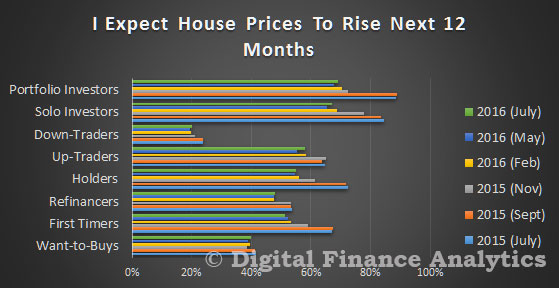

Today we continue our discussion of the latest Digital Finance Analytics household surveys, which looks in detail at intentions to purchase property in the next 12 months. This includes data up to late July, so is clear of potential election impacts. The analysis uses a large sample size, so is statistically robust. We use a segmentation model to flush out the main differences between household types. This is described in our publication “The Property Imperative” which is available on request. These results will flow into the next edition later in the year.

We start with some cross-segment comparisons. First, we find that households are just a little less confident house prices will rise in the next year, compared with 12 months ago. However, around half of all households still believe price growth will roll on. Property investors are the most optimistic, whilst those seeking to sell-down, the least.

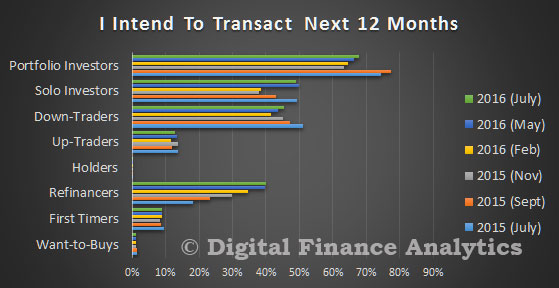

Looking next at whether households expect to transact, we find that investors are mostly likely to make a purchase, but there is a continued rise among those wanting to refinance. 40% of those seeking to refinance expect to do so in the coming year.

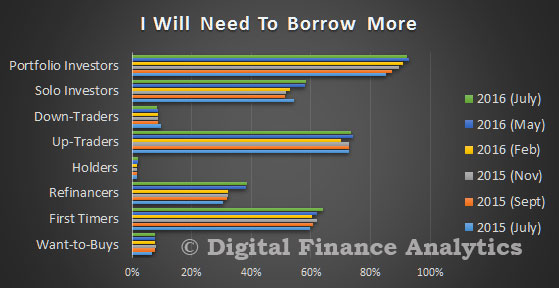

Turning to borrower expectations, first time buyers, those trading up, and portfolio investors are most likely to seek additional mortgage funding. In fact, as interest rates have fallen, demand is even stronger.

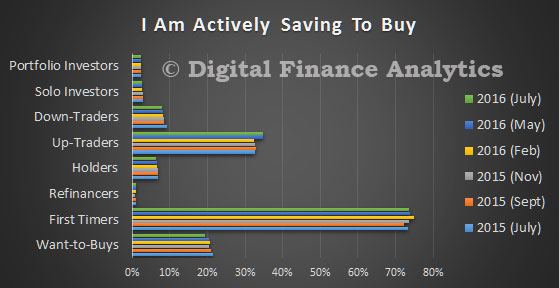

Those saving to assist in a purchase are mainly confined to households who are yet to transact, or who are trading up. More than 70 per cent of first time buyers wishing to purchase, continue to save.

We will look in more detail at the forces which are driving investors in a later post, but this summary chart gives a good flavour of what we found. Tax efficiency is the single most powerful driver, and property capital appreciation is also important. Together these are perceived to give better returns that from deposits (in this low interest rate environment). Around 15 per cent of investors cited the low finance rates currently available.

Finally, in this post, we look at which household segments are most likely to use a mortgage broker. Given that half of all new transactions are originated via this route, understanding which customer groups are most likely to reach of advice is important. Those seeking to refinance are most likely to transact via a broker.

Next time we will look at some of the more detailed segment specific analysis. But in summary, whilst property transaction, and lending volumes may be falling, there is still strong demand for property. This will provide ongoing support for prices in the coming months, and also suggests that households will be seeking deals from lenders. There is life in the old dog yet!

The Fed just released their latest update on monetary policy, and once again kept the rate at its current low level. The tone of the note was slightly more positive. They are still chasing the 2% inflation target and underscore that future cash rate lifts will be slow. The market hardly moved on the news.

Information received since the Federal Open Market Committee met in June indicates that the labor market strengthened and that economic activity has been expanding at a moderate rate. Job gains were strong in June following weak growth in May. On balance, payrolls and other labor market indicators point to some increase in labor utilization in recent months. Household spending has been growing strongly but business fixed investment has been soft. Inflation has continued to run below the Committee’s 2 percent longer-run objective, partly reflecting earlier declines in energy prices and in prices of non-energy imports. Market-based measures of inflation compensation remain low; most survey-based measures of longer-term inflation expectations are little changed, on balance, in recent months.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee currently expects that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace and labor market indicators will strengthen. Inflation is expected to remain low in the near term, in part because of earlier declines in energy prices, but to rise to 2 percent over the medium term as the transitory effects of past declines in energy and import prices dissipate and the labor market strengthens further. Near-term risks to the economic outlook have diminished. The Committee continues to closely monitor inflation indicators and global economic and financial developments.

Against this backdrop, the Committee decided to maintain the target range for the federal funds rate at 1/4 to 1/2 percent. The stance of monetary policy remains accommodative, thereby supporting further improvement in labor market conditions and a return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. In light of the current shortfall of inflation from 2 percent, the Committee will carefully monitor actual and expected progress toward its inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction, and it anticipates doing so until normalization of the level of the federal funds rate is well under way. This policy, by keeping the Committee’s holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; James Bullard; Stanley Fischer; Loretta J. Mester; Jerome H. Powell; Eric Rosengren; and Daniel K. Tarullo. Voting against the action was Esther L. George, who preferred at this meeting to raise the target range for the federal funds rate to 1/2 to 3/4 percent

A six year legal battle came to an end yesterday when the High Court ruled in favour of ANZ Bank, finding by a 4-1 majority that the bank could enforce late payment fees on credit cards.

The lead plaintiff in the class action was Mr Paciocco, who opened two MasterCard accounts with the bank. One card had a credit limit of A$18,000 the other had a A$4,000 limit.

Mr Paciocco was late in meeting his monthly repayments on a number of occasions, and was required to pay late payment fees. The fee was initially $35, with the bank later reducing it to $20. Mr Paciocco was not the only ANZ customer who was late in repaying their credit card debts. During the financial year ended September 2009 the bank had around two million consumer credit card accounts. It charged late payment fees on around 2.4 million occasions, for which it received $75 million.

Mr Paciocco claimed the bank could not enforce the late payment fees because they were “penalties”. Australia’s common law will not allow a party to a contract to enforce a penalty amount under a contract. The question the High Court grappled with was what precisely did the common law understand a penalty to be. Rather annoyingly the Court has returned to the bad habit of each of the five judges hearing the case writing a separate decision. Each judge’s decision covers much of the same ground as the others, with subtle differences here and there. This makes it rather difficult to discern any coherent majority view on any particular issue.

In any event, the Court appeared to agree that a “fee” amounts to being a penalty if it is in the nature of a punishment for non-observance of the credit card contract. That is, it is a penalty if the fee is out of all proportion to the costs or loss caused to the bank by the customer’s late repayment. One view was that a fee becomes a penalty if it is extravagant, exorbitant or unconscionable. That definition sets a very high hurdle for bank customers to surmount when trying to prove a fee is a penalty.

Having decided what a penalty is, the judges were required to determine whether the fee/penalty charged was out of all proportion to the resulting losses caused to the bank. ANZ admitted the late payment fees were not a genuine pre-estimate of the losses it suffered as a result of the late repayment. The Court, however, found the mere fact there was no pre-estimate of the losses to the bank did not automatically mean it was a penalty.

Experts differ

Two expert witnesses gave evidence before the lower courts about the costs to the bank of a customer making a late repayment. One witness estimated the average cost to be $2.60. The other expert took into account a range of factors including the “loss provision costs, regulatory capital costs and collection costs” to the bank, and arrived at a much higher figure.

The Court then debated which of the experts had adopted the correct methodology. The majority found in favour of the second witness, the minority judge found the correct figure was closer to that calculated by the first witness, and therefore found the late repayment fee to be a penalty.

The majority also considered whether the bank had acted unconscionably or unjustly under the provisions of relevant legislation, and concluded that the bank had not breached the legislation.

The case confirms that a person alleging a requirement under a contract to make a certain payment amounts to a penalty must jump a very high bar. He or she must establish that the amount being imposed is extravagant, exorbitant or unconscionable.

The case also illustrates the difficulty in calculating the costs to the bank of customers making late repayments. The onus is on the customer to show the bank is acting extravagantly. It is somewhat disappointing for the many bank customers who are subjected to late payment fees that the Court favoured a costing methodology that itself was arguably extravagant and exorbitant.

Author: Justin Malbon, Professor of Law, Monash University

The UK’s approach to financial crime has taken a turn for the better recently. The successful prosecutions in the LIBOR-rigging scandal are a signal that British authorities are coming close to their US peers in slapping down errant bankers. The trouble is, there is pressure to take the foot off the pedal.

Not only has the new boss of the City watchdog suggested that banks should be keeping their own houses in order, the threat of Brexit opens up the possibility that the UK will have to fight to maintain the primacy of London as a financial centre. If that effort leads to a softening of the controls on the banks and bankers, it would be a grave mistake.

London is currently listed as the top financial capital in the world. Its main strengths are stability and dynamism. Effective regulatory and enforcement regimes can promote trust and confidence from the public, which helps to underpin that financial stability.

Given the role of banks in the global financial crisis, it is a dangerous time to soften controls, even if the pressure from the industry is ever present. There is a clear risk that some bankers will return to prioritising profit at the expense of customers and ultimately, at the expense of the wider economy. That would suit no one in the capital and beyond over the long term.

Motivation

Brexit though, has upset the apple cart. The US watchdog for monitoring financial stability, the US Office for Financial Research recently said that political and financial uncertainties caused by Brexit may last for months or even years. That leaves the financial industry in flux.

In effect, UK voters’ decision to leave the European Union gives a potential opportunity for countries such as France, Germany and Luxembourg to strengthen their positions as international financial centres. The most immediate concern is whether banks will be able to sell financial products and services from London to customers in Europe when Brexit takes place. Bullish noises from politicians may not be enough to convince banking executives that their strategic decision should be left to the whim of EU negotiators.

London will fight to stay competitive, but the focus should be a determination for regulators, politicians and investigators to maintain their improving proactive and robust styles. A race to the bottom on oversight would be potentially dangerous. It would leave the door open to fresh scandals; even a fresh crisis. It is hugely important that the new chancellor of the exchequer, Philip Hammond, leads a tough regulatory approach.

You see, an effective, efficient and enforced regulatory regime can be a competitive advantage. Australia and Canada both emerged better than the UK from the global financial crisis. One of the many reasons is that the regulators in Australia and Canada were more proactive and robust in monitoring and supervising their banks.

In the UK, the Bank of England’s report into the failure of the Financial Supervisory Authority (predecessor of the current watchdog, the Financial Conduct Authority) found that there were inadequate resources. This affected the authority’s ability to supervise banks such as HBOS. Simply put, you need sufficient resources (both human and financial) to enable the various authorities to perform their jobs effectively.

Taking the lead

The Financial Conduct Authority (FCA) is the regulator for the financial sector. It sets guidelines, monitors behaviour and can stop people from operating in the industry if they break its rules. Its remit is to protect consumers, and it did so with a budget of £479m in 2015-16 and £452m in 2014-15.

That is already more than the budgets of equivalent bodies in Germany and in the US. But while it is encouraging that the FCA is well funded relative to its peers, it is also a worry that policy makers might see this as fat that can be trimmed.

I believe the funding levels for the UK regulator should actually be boosted as it seeks to rubber-stamp Britain’s reputation in the face of threats to the financial sector, and a change to the law would do it.

Until 2012, regulators were able to use the fines collected from banks to fund their work. However, the then chancellor, George Osborne, changed the law to draw the fine revenues into the Treasury. Under Osborne’s control, armed forces charities and the emergency services received the fines, not the authorities which had imposed them.

Clearly, these charities and services perform very important roles in society but a boost to the budget for policing financial crime would help society in its own and important way, while helping London to maintain that competitive edge. Although fines against individuals by the FCA have declined in recent years, the new senior managers regime, designed to improve individual accountability, may reverse this trend.

As old investigations close – some with success – it is vital that there are the resources and support to start new investigations. The UK has the largest financial services sector in the European Union, at least for now: if it is to grow sustainably, to support a post-Brexit economy, then oversight and enforcement must be stronger than ever.

Author: Alison Lui, Senior Lecturer in Law, Liverpool John Moores University

The privatisation of public assets is “severely damaging” the Australian economy by lifting prices and hampering productivity, according to Australian Competition and Consumer Commission chair Rod Sims.

Speaking at the Melbourne Economic Forum on Tuesday, Sims urged Australian governments to put an end to explicitly trying to maximise proceeds from the sale of public assets, something the competition boss says is causing him to become increasingly “exasperated”.

“I think a sharp uppercut is necessary and that’s why I’m saying: stop the privatisation,” Sims said, according to Fairfax.

It’s a view shared by Peter Strong, chief executive of the Council of Small Business of Australia, who told SmartCompany Sims’ comments are “spot on”.

“Governments need to stop and have a look at what their role is, “ Strong says.

“Privatisation should make markets more efficient.”

Sims said recent sales of government-owned ports and electricity infrastructure, as well as the deregulation of the vocational education sector, has caused him to change his views on the effects of privatisation on the economy.

“I’ve been a very strong advocate of privatisation for probably 30 years; I believe it enhances economy efficiency,” Sims said at the forum.

“I’m now almost at the point of opposing privatisation because it’s been done to boost proceeds, it’s been done to boost asset sales and I think it’s severely damaging our economy.”

Sims told the forum that the privatisation of electricity infrastructure in Queensland and New South Wales has caused consumer prices to almost double over five years.

“When you meet people in the street and they say ‘I don’t want privatisation because it boost prices’ and you dismiss them … recent examples suggest they’re right,” he said.

“The excessive spend on electric poles and wires has damaged our productivity. The higher energy price we’re getting from some gas and electricity policies are damaging some of the our productive sectors.”

Sims also highlighted the privatisation of ports, including Port Botany and Port Kembla in NSW and the Port of Melbourne, which he said has created monopolistic circumstances.

Strong adds the operation of airports to the list of sectors where there is potential for a large, private operators to control the market with little competition.

“An example of why [Sims] is right is the second airport in Sydney,” Strong says, referring to Sydney Airport Corporation, the operator of the Sydney Airport, having the right of first refusal to develop the Western Sydney airport site.

“Where’s the competition?”

Strong says the presence of oligopolies, or markets that are dominated by a small number of firms, can have detrimental effects on small businesses operating in the same space.

While Australian governments have in recent times spoken about the need for innovation in the economy, Strong points to figures from the OECD in 2014 that found Australian SMEs were ranked fifth out of 29 OECD countries in terms of innovation, while large Australian businesses were ranked the 21st most innovative out of 32 OECD nations.

“I believe the reason why big businesses aren’t innovative is because they have no need to be; they have market dominance so there is no motivation,” Strong says.

A group of Australian financial institutions have lodged an application with the Australian Competition and Consumer Commission (ACCC) seeking authorisation to enter joint negotiations with providers of third-party mobile wallets according to NAB. The application cites three digital wallets in particular: Apple Pay, Android Pay and Samsung Pay.

Through joint negotiations, the applicants want to ensure that Australian consumers can make payments easily through their choice of mobile wallet providers, have access to the latest developments in contactless payment technology, and can benefit from common security standards across the mobile payment system.

The applicants believe consumers will benefit if they can choose the best mobile wallet that suits their own needs using their own devices. That way all consumers could have access to new features, apps and technologies developed by the makers of different mobile wallets.

“This is about providing Australians with real choice and better outcomes. If successful, the application would have tremendous benefits for the entire Australian mobile payments landscape including for public transport fares, airlines, ticketing, store loyalty and rewards programs and many more applications yet to be developed,” said Novantas Senior Advisor Lance Blockley, on behalf of the applicants.

The application lodged by Bendigo and Adelaide Bank, the Commonwealth Bank of Australia, National Australia Bank and Westpac is subject to authorisation by the ACCC. A notable absence from the list of applicants is ANZ which is the first Australian bank to offer support for Apple Pay.

The application does not request authorisation to enter joint negotiations on the amount of fees or charges, meaning financial institutions are responsible for individually negotiating contractual arrangements with wallet providers. The period of authorisation sought is three years.

Australia is at the forefront of contactless card payments, which have been well accepted by consumers and merchants. The negotiations, if successful, will ensure that consumers and merchants can be confident that Australia has a competitive, innovative and transparent system of mobile payments, including third-party wallets. With major public transport systems in Australia soon to begin trials of open loop contactless payment technology, the time is pressing for consumers to be offered a choice of mobile wallet providers.

If the application is granted, other businesses and institutions can join negotiations if they believe it would benefit their customers.

Internet users in the UK overwhelmingly prefer digital shopping for keeping up-to-date with the latest products, attaining detailed product information, and even simply browsing products. The Pragma survey reveals that in-store experiences are failing users for these basic shopping tasks.

In June 2016, eMarketer estimated that there will be 44.4 million digital shoppers in the UK in 2016, which accounts for 93.8% of all UK internet users. These digital shoppers will browse and research products online, but not necessarily make a purchase that way. However, a large share of them will go on to buy: 94.9% this year, suggesting shoppers are happy with the experience. By 2020, 95.3% of digital shoppers in the UK will make a digital purchase.

During the March 2016 quarter, vacant residential land sales increased most strongly in Perth (+22.3 per cent) followed by Melbourne (+5.2 per cent). However, land market turnover fell in Hobart (-28.4 per cent), Adelaide (-8.3 per cent), Sydney (-5.9 per cent) and Brisbane (-3.4 per cent) over the same period.

During the March 2016 quarter, vacant residential land sales increased most strongly in Perth (+22.3 per cent) followed by Melbourne (+5.2 per cent). However, land market turnover fell in Hobart (-28.4 per cent), Adelaide (-8.3 per cent), Sydney (-5.9 per cent) and Brisbane (-3.4 per cent) over the same period. Looking next at whether households expect to transact, we find that investors are mostly likely to make a purchase, but there is a continued rise among those wanting to refinance. 40% of those seeking to refinance expect to do so in the coming year.

Looking next at whether households expect to transact, we find that investors are mostly likely to make a purchase, but there is a continued rise among those wanting to refinance. 40% of those seeking to refinance expect to do so in the coming year. Turning to borrower expectations, first time buyers, those trading up, and portfolio investors are most likely to seek additional mortgage funding. In fact, as interest rates have fallen, demand is even stronger.

Turning to borrower expectations, first time buyers, those trading up, and portfolio investors are most likely to seek additional mortgage funding. In fact, as interest rates have fallen, demand is even stronger. Those saving to assist in a purchase are mainly confined to households who are yet to transact, or who are trading up. More than 70 per cent of first time buyers wishing to purchase, continue to save.

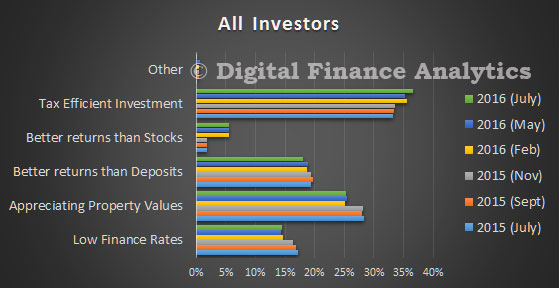

Those saving to assist in a purchase are mainly confined to households who are yet to transact, or who are trading up. More than 70 per cent of first time buyers wishing to purchase, continue to save. We will look in more detail at the forces which are driving investors in a later post, but this summary chart gives a good flavour of what we found. Tax efficiency is the single most powerful driver, and property capital appreciation is also important. Together these are perceived to give better returns that from deposits (in this low interest rate environment). Around 15 per cent of investors cited the low finance rates currently available.

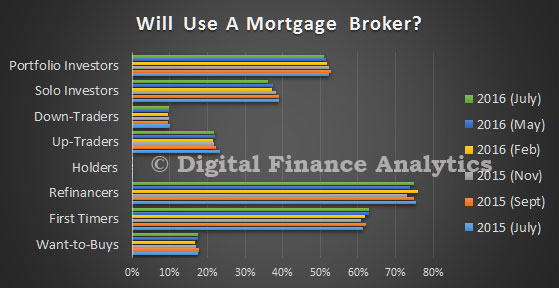

We will look in more detail at the forces which are driving investors in a later post, but this summary chart gives a good flavour of what we found. Tax efficiency is the single most powerful driver, and property capital appreciation is also important. Together these are perceived to give better returns that from deposits (in this low interest rate environment). Around 15 per cent of investors cited the low finance rates currently available. Finally, in this post, we look at which household segments are most likely to use a mortgage broker. Given that half of all new transactions are originated via this route, understanding which customer groups are most likely to reach of advice is important. Those seeking to refinance are most likely to transact via a broker.

Finally, in this post, we look at which household segments are most likely to use a mortgage broker. Given that half of all new transactions are originated via this route, understanding which customer groups are most likely to reach of advice is important. Those seeking to refinance are most likely to transact via a broker. Next time we will look at some of the more detailed segment specific analysis. But in summary, whilst property transaction, and lending volumes may be falling, there is still strong demand for property. This will provide ongoing support for prices in the coming months, and also suggests that households will be seeking deals from lenders. There is life in the old dog yet!

Next time we will look at some of the more detailed segment specific analysis. But in summary, whilst property transaction, and lending volumes may be falling, there is still strong demand for property. This will provide ongoing support for prices in the coming months, and also suggests that households will be seeking deals from lenders. There is life in the old dog yet!