Any advantages of funding property portfolios with popular interest-only loans are rapidly disappearing as lenders hit the red alert button by raising rates, tighten terms and offer lucrative incentives to pay down debt.

Trend-setting big banks are responding to regulatory pressure by hiking rates on the loans, which are used by 70 per cent of investors, by up to 50 basis points and encouraging switches to principal and interest loans by reducing rates by about 50 basis points.

Other lenders are following the lead by requiring bigger deposits and tougher scrutiny of income.

An investor with a $3.5 million portfolio and 70 per cent loan-to-value ratio will have to find another $1500 a month in repayments, or about $18,800 a year, if interest-only repayments increase by 50 basis points, according to analysis by finder.com, which monitors prices and costs of financial products. Lenders from the big four are already paying higher rates.

The same investor on a principal and interest loan would have to pay an additional $1100 a month, or $13,200 a year, if rates rose by 50 basis points because these loans have become more attractive, says finder.com.

Traditionally loan repayments have been cheaper on interest-only loans — both because repayments don’t include principal and rates have been lower than on principal and interest loans.

Rate blow out

But moves by the big four lenders and their subsidiaries, which provide the vast bulk of loans,are changing this. During the past 12 months, for example, CBA interest-only loans have risen by more than 30 basis points to 5.94 per cent as principal and interest loans have fallen 10 per cent to 5.25 per cent. That’s based on a borrower with a $500,000 loan and 20 per cent deposit.

The average Australian property investor has two properties, says Digital Finance Analytics’ principal Martin North, with the bulk of the remainder having between three and five.

North says the “striking observation” about households with large numbers of investment properties is the size of their debt, preference for interest-only loans and smaller number of quality portfolios. Many “serial” investors rely on multiple lenders and rely on rental income to repay interest.

Annual rents are falling in Perth, Brisbane and Darwin by between 1 per cent and 9 per cent, according to SQM Research. They are rising in Hobart by 11 per cent, Melbourne 5 per cent and Sydney 3 per cent.

Investors with high debt and falling income, says North, are the most vulnerable to a rapid interest rate increase or a downturn in property values, which is likely to impact lower-quality properties first.

Navid Guia has three investment houses, each with an attached granny flat — two in St Marys, 45km west of Sydney’s central business district, and one in Sacramento, in the US, close to his family.

He purchased the two- and three-bedroom Australian properties for between $249,000 and $310,000 during 2011 and 2012. The Sacramento house, which cost $117,000, was added last year.

All the properties are interest-only with a loan to value ratio of between 10 per cent and 20 per cent.

He is protecting his portfolio from rising rates and peaking prices by positive gearing, ie, income from the investments is higher than interest and other expenses.

Guia, 30, who trained as a civil engineer, says: “To me it does not make sense to buy a property and then negatively gear it. I have a cash flow from the rent that can be used for investing and buying other properties.” Negative gearing uses borrowed money for an investment whose losses can be offset against the investor’s income.

Guia says reliable, well-priced rents means he can comfortably absorb recent rate rises.

Lower interest

Other portfolio investors, such as Mario Borg, finance strategist, with Mario Borg Strategic Finance, says: “There are many home owners making interest-only home loan repayments, not realising that they could be paying a much lower interest rate if they choose to make principal and interest repayments.”

Regulators, including the Reserve Bank of Australia, are nervous about the rapid growth in interest-only loans in the absence of clear evidence borrowers have a strategy to repay the principal and have put pressure on lenders to raise rates and toughen terms.

The big fear is that static and falling incomes combined with rising rates, fewer tenants and increased supply of apartments and houses will cause widespread financial stress, which could lead to defaults, weaker consumer confidence and lower economic growth.

Fund managers, whose investment strategies can profit from volatile and falling markets, are warning high levels of personal debt could cause “Australia’s sub-prime crisis”, a reference to the US mortgage crisis that accelerated the slide into the global financial crisis.

Wayne Byres, chairman of the Australian Prudential Regulation Authority, says: “If we are going to put an increasing number of eggs into a single basket, we had better make sure that basket is an unquestionable strong one.”

Analysts and mortgage brokers expect rates on interest-only loans to continue rapidly rising.

Christopher Foster-Ramsay, of Foster Ramsay Finance, reckons the difference between investor interest-only loans and owner-occupier principal and interest rates will blow out to 100 basis points by the end of the year.

DFA’s North says key market indicators, such as the yield curve, which reflects expectations of future returns, suggests fixed rates will rise by 50 basis points in coming months.

The need for lenders to control loan growth and wanting to deter “risky” loans will add to the pressure because stressed borrowers will have fewer options.

Falling rents or loss of tenants could jeopardise the financial viability of nearly 36,000 property investment portfolios around the country, according to North.

More than one in three portfolios with Sydney property would be at risk, he says, compared with Melbourne where one in four properties could be impacted. These are investors who would not have income or savings to pay for their property investments if rent were to stop, he says.

When it comes to the housing debate, there’s one number that just won’t go away: 20 per cent.

Many fear that’s how much they’ll have to save for a deposit. It’s easy to understand why – popular measures of affordability, such as those compiled by CoreLogic and CoreData, often assume a 20 per cent lump sum.

Except it’s not.

Back in 2015, the Reserve Bank noted: “the deposit required of a first home buyer is no longer necessarily around 20 per cent of the purchase price, but rather, more often in the 5–10 per cent range.”

Regulators have tightened the screws since then, but there are still mortgages with below 20 per cent deposits to be found, according to Dr Ashton De Silva from RMIT’s Centre for Urban Research.

He said homebuyers taking out bigger loans should consider the benefits of getting into the housing market now, rather than waiting to reach a certain deposit.

“It’s not just a case of working out that you’ve got to pay another $50,000 in interest. What is the economic benefit of securing that place now?” Dr De Silva told The New Daily.

“We expect people are making the decision that: ‘It is better for me to take on that extra cost and secure this dwelling.’”

Two Australians earning the average full-time wage, with average living costs, will likely qualify for a loan just over $1 million with one of Australia’s big banks.

Finder, a financial comparison website, lists a bevy of acronyms that offer low deposit loans, including: NAB, ME, CUA, IMB and HSBC.

Many lenders have created new financial products to help homebuyers enter the market, resulting in Australia having, according to Dr De Silva, “one of the most product diverse markets in the world”.

One option is lenders’ mortgage insurance, which lowers required deposits to a minimum of 5 per cent, meaning purchasers of a $500,000 property can require a lump sum of only $25,000.

Mortgage insurance is usually paid as a one-off charge, with the cost calculated as a percentage of the loan amount and based on the size of your deposit.

Occasionally, it can even be ‘capitalised’ into the value of the loan – which means you borrow more to cover the cost of the insurance. If you do this, you’ll pay slightly higher repayments, rather than a big sum up front.

It’s important to note the insurance only protects the lender against the risk of you defaulting on the mortgage, not you.

You need $200,000 to meet the 20 percent deposit on a $1 million dollar mortgage, an enormous sum for most Australians.

With mortgage insurance, a couple taking out a loan with a 5 per cent deposit would need $50,000, plus the cost of the insurance.

Some lenders won’t charge insurance on loans with a 10 per cent deposit, but this depends on job security and credit history.

Two Australians earning the average full-time wage, with average living costs, will likely qualify for a loan just over $1 million with one of Australia’s big banks.

Dr De Silva warned home buyers should do their homework and weigh up the costs and benefits of different loans.

“One thing that needs to be at the forefront is, ‘Can I afford to ride out any crisis that may arise?’”

Associate Professor Chyi Lin Lee, an expert in property market economics at the University of Western Sydney, pointed to 20 per cent deposits as a main source of difficulty for many homebuyers.

“We need to find an innovative way to help owner-occupiers to get into the market,” he told The New Daily.

Professor Lee said schemes which help homebuyers jump over the deposit hurdle – such as controversial first homebuyer grants – can be successful, despite the upward pressure they put on prices.

A caution: don’t overextend

Professor Lee warned lower deposits shouldn’t be an excuse for buyers to take out bigger loans than they can pay off.

This was backed by Dr Rachel Ong, deputy director at the Bankwest Curtin Economics Centre, who said people taking out loans with low equity can expose themselves to higher repayments.

“It isn’t a good idea to try and lower the minimum deposit because there’s people who might not be able to meet the payments, and the consequences of that are all the negative and quite severe,” Dr Ong said.

“There’s a reason why the minimum deposit is set at what it is.”

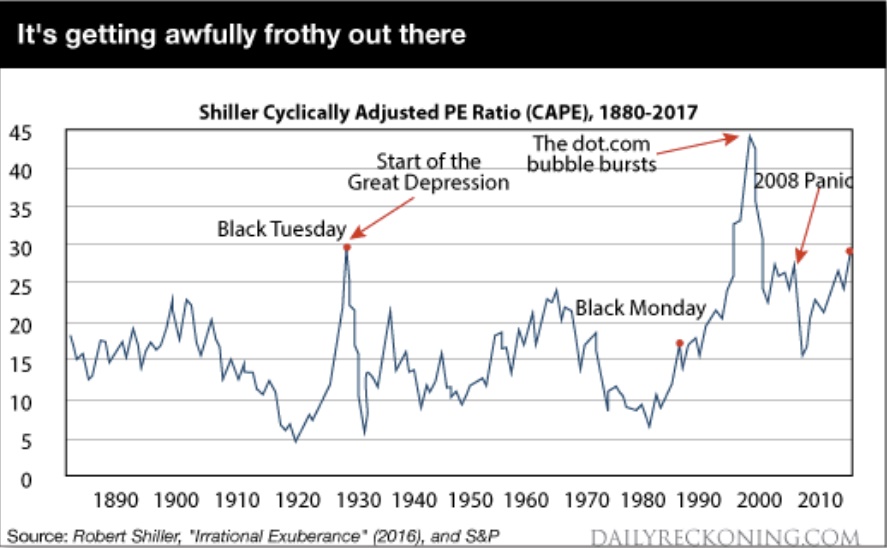

The key to bubble analysis is to look at what’s causing the bubble. Based on data going back to the 1929 crash, this current bubble looks like a particular kind that can produce large, sudden losses for investors.

This chart shows the Shiller Cyclically Adjusted PE Ratio (CAPE) from 1880-2017. Over this 137-year period, the mean ratio is 16.75, media ratio is 16.12, low is 4.78 (Dec 1920) and high is 44.19 (Dec 1999). Right now the 29.45 ratio is above the level of the Panic of 2008, and about equal to the level of the market crash that started the Great Depression.

My preferred metric is the Shiller Cyclically Adjusted PE Ratio or CAPE. This particular PE ratio was invented by Nobel Prize-winning economist Robert Shiller of Yale University.

CAPE has several design features that set it apart from the PE ratios touted on Wall Street. The first is that it uses a rolling ten-year earnings period. This smooths out fluctuations based on temporary psychological, geopolitical, and commodity-linked factors that should not bear on fundamental valuation.The second feature is that it is backward-looking only. This eliminates the rosy scenario forward-looking earnings projections favored by Wall Street.

The third feature is that that relevant data is available back to 1870, which allows for robust historical comparisons.

The chart below shows the CAPE from 1870 to 2017. Two conclusions emerge immediately. The CAPE today is at the same level as in 1929 just before the crash that started the Great Depression. The second is that the CAPE is higher today than it was just before the Panic of 2008.

Neither data point is definitive proof of a bubble. CAPE was much higher in 2000 when the dot.com bubble burst. Neither data point means that the market will crash tomorrow.

But today’s CAPE ratio is 182% of the median ratio of the past 137-years.

Given the mean-reverting nature of stock prices, the ratio is sending up storm warnings even if we cannot be sure exactly where and when the hurricane will come ashore.

With the likelihood of a bubble clear, we can now turn to bubble dynamics. The analysis begins with the fact that there are two distinct types of bubbles.

Some bubbles are driven by narrative, and others by cheap credit. Narrative bubbles and credit bubbles burst for different reasons at different times. The difference is critical in knowing what to look for when you time bubbles, and for understanding who gets hurt when they burst.

A narrative-driven bubble is based on a story, or new paradigm, that justifies abandoning traditional valuation metrics. The most famous case of a narrative bubble is the late 1960s, early 1970s “Nifty Fifty” list of fifty stocks that were considered high growth with nowhere to go but up.

The Nifty Fifty were often referred to as “one decision” stocks because you would just buy them and never sell. No further thought was required. Of course, the Nifty Fifty crashed with the overall market in 1974 and remained in an eight-year bear market until a new bull market began in 1982.

The dot.com bubble of the late 1990s is another famous example of a narrative bubble. Investors bid up stock prices without regard to earnings, PE ratios, profits, discounted cash flow or healthy balance sheets.

All that mattered were “eyeballs,” “clicks,” and other superficial internet metrics. The dot.com bubble crashed and burned in 2000. The NASDAQ fell from over 5,000 to around 2,000, then took sixteen years to regain that lost ground before recently making new highs. Of course, many dot.com companies did not recover their bubble valuations because they went bankrupt, never to be heard from again.

The credit-driven bubble has a different dynamic than a narrative-bubble. If professional investors and brokers can borrow money at 3%, invest in stocks earning 5%, and leverage 3-to-1, they can earn 6% returns on equity plus healthy capital gains that can boost the total return to 10% or higher. Even greater returns are possible using off-balance sheet derivatives.

Credit bubbles don’t need a narrative or a good story. They just need easy money.

A narrative bubble bursts when the story changes. It’s exactly like The Emperor’s New Clothes where loyal subjects go along with the pretense that the emperor is finely dressed until a little boy shouts out that the emperor is actually naked.

Psychology and behavior change in an instant.

When investors realized in 2000 that Pets.com was not the next Amazon but just a sock-puppet mascot with negative cash flow, the stock crashed 98% in 9 months from IPO to bankruptcy. The sock-puppet had no clothes.

A credit bubble bursts when the credit dries up. The Fed won’t raise interest rates just to pop a bubble — they would rather clean up the mess afterwards that try to guess when a bubble exists in the first place.

But the Fed will raise rates for other reasons, including the illusory Phillips Curve that assumes a tradeoff between low unemployment and high inflation, currency wars, inflation or to move away from the zero bound before the next recession. It doesn’t matter.

Higher rates are a case of “taking away the punch bowl” and can cause a credit bubble to burst.

The other leading cause of bursting credit bubbles is rising credit losses. Higher credit losses can emerge in junk bonds (1989), emerging markets (1998), or commercial real estate (2008).

Credit crack-ups in one sector lead to tightening credit conditions in all sectors and lead in turn to recessions and stock market corrections.

What type of bubble are we in now? What signs should investors look for to gauge when this bubble will burst?

My starting hypothesis is that we are in a credit bubble, not a narrative bubble. There is no dominant story similar to the Nifty Fifty or dot.com days. Investors do look at traditional valuation metrics rather than invented substitutes contained in corporate press releases and Wall Street research. But even traditional valuation metrics can turn on a dime when the credit spigot is turned off.

Milton Friedman famously said the monetary policy acts with a lag. The Fed has force-fed the economy easy money with zero rates from 2008 to 2015 and abnormally low rates ever since. Now the effects have emerged.

On top of zero or low rates, the Fed printed almost $4 trillion of new money under its QE programs. Inflation has not appeared in consumer prices, but it has appeared in asset prices. Stocks, bonds, commodities and real estate are all levitating above an ocean of margin loans, student loans, auto loans, credit cards, mortgages, and their derivatives.

Now the Fed is throwing the gears in reverse. They are taking away the punchbowl.

The Fed has raised rates three times in the past sixteen months and is on track to raise them three more times in the next seven months. In addition, the Fed is preparing to do QE in reverse by reducing its balance sheet and contracting the base money supply. This is called quantitative tightening or QT, which I’ve discussed recently.

Credit conditions are already starting to affect the real economy. Student loan losses are skyrocketing, which stands in the way of household formation and geographic mobility for recent graduates. Losses are also soaring on subprime auto loans, which has put a lid on new car sales. As these losses ripple through the economy, mortgages and credit cards will be the next to feel the pinch.

The momentum for U.S. bank deregulation continues to grow, but it is becoming more likely that it will take the form of multiple smaller bills targeting relief for specific segments of the financial sector as opposed to a single, comprehensive bill, says Fitch Ratings.

The Financial Choice Act (FCA) remains the benchmark for the full deregulation agenda given the upcoming House vote on a revised version that was passed by the House Financial Services committee earlier this month. The updated version (FCA 2.0) is mostly in line with the original bill from 2016 and still calls for the full repeal of the Volcker Rule, the Orderly Liquidation Authority (OLA) and the Department of Labor (DOL) Fiduciary Rule.

Broad and deep deregulation is generally viewed by Fitch as likely to have a negative impact from a bank credit risk perspective; however, the ultimate form of regulatory change and its application by individual banks will determine the ratings implication.

A repeal of Volcker is unlikely to result in banks’ returning to full-scale proprietary trading, but it could carry negative rating implications depending on banks’ response. The elimination of OLA could expose the banking sector to significant systemic risk in the event of a crisis, though resolution planning could be a mitigating factor to large bank failures. While eliminating the DOL Fiduciary Rule would likely benefit banks’ wealth management businesses and asset managers’ profitability, reputational and litigation risks would remain.

Key differences between FCA 2.0 and the original bill include simplifying the threshold for banks to opt out of most regulations, changing operational risk weights for global systemically important banks (G-SIBs), replacing the Consumer Financial Protection Bureau (CFPB) and relaxing some components of stress-testing.

Fitch does not believe proposed changes to the CFPB would directly affect most banks’ and non-bank financial institutions’ credit profiles, though they could reduce the regulatory burden and associated costs. Further revision to bank stress testing as proposed under FCA 2.0 is likely to be ratings neutral.

Further on the bank tax, an interesting segment from ABC The Business, where the Greens Senator, Peter Whish-Wilson argues for a higher rate to be applied.

He argues for a floor on the levy to take account of the tax offsets. Also touches on the impact on the smaller banks and competition.

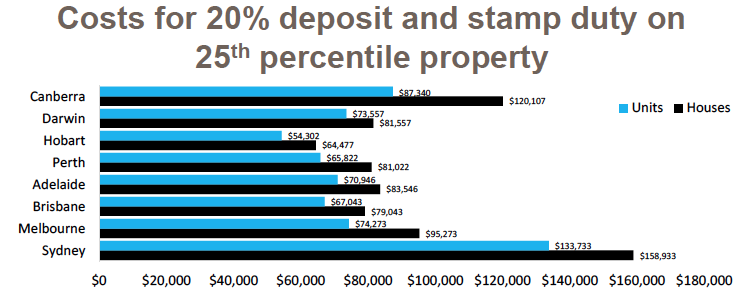

The 20% deposit and stamp duty required to buy a house in Sydney is $158,933, based on new CoreLogic data. That’s equivalent to 20 years’ worth of smashed avo.

The 20 per cent deposit and stamp duty required to buy a house in Sydney is $158,933, according to new data from CoreLogic. That’s the equivalent of 7,224 serves of $22 avocado on toast – or avocado on toast every day for 20 years.

Even in the nation’s most affordable city, Hobart, buyers must accumulate $64,477 for the deposit on a house and to cover stamp duty. That’s 2,930 serves of your favourite brekkie – or avo on toast every day for eight years.

Source: CoreLogic.

The numbers put Bernard Salt’s jocular observation of young adults wasting money on smashed avo into perspective: even if young Australian do give up extravagant brunches and put the funds towards saving for a house, it will take years, even decades, to accumulate enough cash for the deposit and stamp duty on a home.

Core Logic has used house and apartment prices in the 25th percentile to compile the data, considering that first-home buyers are generally purchasing at the more affordable end of the property spectrum.

Cameron Kusher, research analyst with CoreLogic, said the research does not factor in stamp duty exemptions below a certain price threshold in some states.

Kusher also said it’s not always necessary to have the whole 20 per cent deposit, although a lesser deposit will usually mean that required lenders mortgage insurance, which is an additional cost for the home buyer.

In a paper on the research, Kusher said housing affordability is worsening as property prices soar higher as wages growth stagnates.

In the 12 months to April 2017, Sydney dwelling values increased by 16.0 per cent, and Melbourne values rose 15.3 per cent. Yet household incomes in Sydney only rose 4.6 per cent in the year to March 2017, while household incomes rose a mere 2.7 per cent in Melbourne, according to data from the Australian National University

“Entry into the housing market remains a real challenge,” said Kusher.

“Even in cheaper areas, household income growth is fairly slow which makes saving a deposit difficult,” he said.

“It is unclear as to how, absent a big fall in property prices, housing affordability for first home buyers can be greatly improved,” he said.

So eat your smashed avo and enjoy it; scrimping on brunch isn’t going to be enough to buy you a property in the current market.

A simple email phishing attack impersonating big four bank NAB was reportedly sent to thousands of Australians yesterday, notifying them their account was disabled in an attempt to steal users’ banking details.

Mailguard reports the email was sent around on Thursday afternoon, stemming from a legitimate looking email address,”discharge.authority@nab.com.au”.

The subject line included just the word “Notification” with the email itself being nothing more than a four line message telling customers their account had been “disabled”.

The malicious email then directed users to a website with a realistic-looking NAB login screen, inviting users to enter their NAB ID and password. The website included links to register for a NAB account and “forgotten password” prompts to boost the appearance of legitimacy.

The purpose of a phishing scam is to steal an unsuspecting users’ login details or personal data by posing as a legitimate company. Examples in the past have included emails appearing to be from Australia Post, Amazon, and Twitter.

In response, Fairfax reports NAB had successfully issued a takedown notice for the fake website, with a spokesperson saying “we remind customers, NAB will never ask you to confirm, update or disclose personal or banking information via email or text”.

On the bank’s website, it advises customers to forward any malicious emails to spoof[at]nab.com.au and then delete the email.

Source: Mailguard

Many recent phishing emails have relied on well-crafted and apparently legitimate websites to fool customers, and founder of IT services company Combo David Markus told SmartCompany this morning that setting one of these fake sites up is a matter of “a few hours work” for a cyber criminal.

“Once it’s created, a cyber criminal can create multiple copies of multiple different web servers and run the phishing attack over and over again,” he says.

“Phishing attacks have become a numbers game, with hackers looking for the cheapest and most efficient way to get dollars out of our bank accounts, and it’s all about the number of people they catch.

“If they make $100, that’s a good day.”

Markus says the scammers have chosen to pose as a big bank like NAB in hopes of increasing the number of users duped by the attack, saying people are more likely to click on something they’re familiar with. However, on the spectrum of cyber attacks, Markus call this one “relatively unsophisticated”.

“I would say these days it’s a relatively unsophisticated attack, but unfortunately there are enough unsophisticated recipients they’re going to keep catching enough people out to make it worthwhile,” he says.

Markus’ advice is to avoid clicking on any links in emails like these ones and instead using traditional channels to check the status of your bank account.

“If someone sends you something that you click on and it wants you to enter your password, don’t,” he says.

“Go via the company’s homepage or however you would usually check your account. Never follow any links in emails that ask for your username or password.”

SmartCompany contacted NAB but was not provided with a statement prior to publication

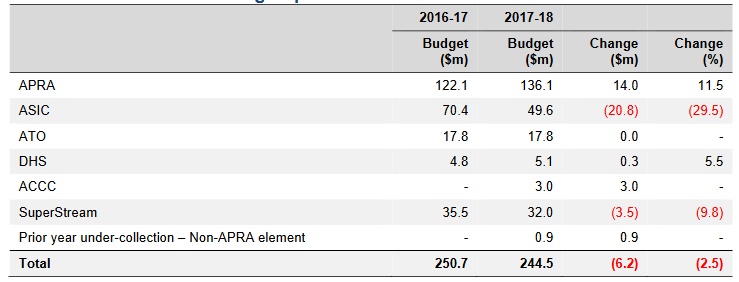

The Treasury has released a paper to seek industry views on the proposed Financial Institutions Supervisory Levies (‘the levies’ or FISLs) that will apply for the 2017-18 financial year.

The paper, prepared by Treasury in conjunction with APRA, sets out information about the total expenses for the activities to be undertaken by APRA and certain other Commonwealth agencies and departments in 2017-18 to be funded through the commensurate levies revenue to be collected in 2017-18.

The financial industry levies are set to recover the operational costs of APRA and other specific costs incurred by certain Commonwealth agencies and departments, including the Australian Securities and Investments Commission, the Australian Taxation Office, and the Department of Human Services.

The total funding required under the levies in 2017-18 for all relevant Commonwealth agencies and departments is $244.5 million. This is a $6.2 million (2.5 per cent) decrease from the 2016-17 requirement. The components of the levies are outlined below:

From Christopher Joye In The AFR today. Once again, excellent insight!

“The one thing the big banks are not is systematically stupid or misanthropic. CBA’s Ian Narev is a truly outstanding chief executive and very generous private philanthropist, supported by what is probably the best retail banking team in the world. Westpac’s Brian Hartzer is no less capable and years ago personally mentored me through a career transition when he had no good reason to do so. ANZ’s Shayne Elliot has thus far displayed tremendous judgement—arguably superior to his peers—under the guidance of Gonski. And Macquarie’s Nicholas Moore is the finest financier this country has ever known. (I have yet to meet NAB’s Kiwi import.)

Setting aside the hyperbole whipped up by gullible hedge fund shorts, the major banks are materially less risky concerns than they were only a few years ago. Under the terrific leadership of Wayne Byres, the Australian Prudential Regulation Authority has been relentless in repeatedly forcing them to boost the austerity of their lending standards. APRA has also been unwavering in its mission to deleverage the big banks’ highly geared balance-sheets. The final chapter in this journey should be unveiled when APRA releases its long overdue report defining what robust capital ratios are required to meet the government’s objective of bequeathing us “unquestionably strong” banks.

Morgan Stanley’s Richard Wiles says that even if this hikes the minimum common equity tier one capital ratio to 11 per cent, which would be wise, the “pro forma capital deficit would be $26 billion”. Some non-core asset sales and a few years of organic capital generation will do the trick.

Which brings me to Standard & Poor’s decision this week to elevate Australia’s Banking Industry Country Risk Assessment (BICRA) score, which automatically downgraded the credit ratings of all non-major banks while increasing the four majors’ too-big-to-fail subsidy from two notches to three.

Blame for this downgrade can be sheeted home to the RBA’s August and May rate cuts, in the absence of which house price growth would not have reaccelerated, compelling S&P to sound the alarm. On May 11 I warned officials that “there is a growing concern amongst non-major banks, which I 100 per cent share, that S&P is trigger-happy on the BICRA score and could increase it in the next few months”. I added that “all the signals from S&P have been negative on this subject, and they seem to want to make a decision after the next house price index release in June”. CBA’s credit strategist commented that “the move by S&P has surprised us, particularly the timing rather than the rationale”. ”

The negative outlook on the BICRA was a two year view in October last year,” CBA explained. “We spoke to S&P in March when the last round of ABS house price data (the December 2016 data) came out [and they] advised they needed to see a trend emerge before they acted. We took this to mean at least another quarter’s data before acting—if at all.” After placing Australia’s BICRA score on “negative outlook” on October 31, S&P led the market to believe it would be altered only if house price growth remained unsustainably strong over the next 6 to 12 months.

By moving pre-emptively this week, S&P ignored the official house price data for 2017, which will not be published until June, and the more timely CoreLogic numbers that indicate prices have been declining since March 31.

A final oddity is S&P’s suggestion that the wonderfully innovative Macquarie Bank warrants a two notch credit rating upgrade because it is too-big-to-fail while Suncorp, Bendigo & Adelaide and Bank of Queensland are not. This makes no sense at all: the government is more likely to bail-out Bendigo, which has a bigger domestic deposit book than Macquarie, than the millionaire’s factory.

I will leave you with the wise words of Ian Macfarlane, the former RBA governor: “By designating four banks as being systemically important, it implies that the other banks…are not important. It is therefore not surprising that the public (and the ratings agencies) assume that the important ones will receive more official support in a crisis than the unimportant ones. It is just not credible for a government…to promise not to step in and prevent large scale bank failure [of big and small institutions] in a financial crisis. The public know they will, and no amount of words will dispel this expectation.”.

Low rates combined with recent changes to various first home buyer initiatives has helped encourage more potential property buyers into the market, new research has revealed.

“In the first quarter of 2017, we saw a rise in the number of first home buyers taking out loans through Mortgage Choice,” Mortgage Choice chief executive officer John Flavell said.

“This growth in first home buyer demand can be attributed to a number of factors, including low interest rates, stagnating property price growth and enhanced first home buyer incentives.

“In the first instance, property prices have started to stagnate across the country, with CoreLogic data showing the median dwelling value in Australia rose just 0.1% over the month of March.

“Furthermore, interest rates remain at historical lows, which has helped keep the cost of borrowing at affordable levels.

“In addition, some states have made changes to their various first home buyer incentives over the first quarter of 2017.

“In Western Australia, the Government announced a temporary $5,000 boost to the First Home Owners Grant. The boost payment is available to eligible first home buyers who enter into a contract between 1 January and 30 June 2017 to purchase or construct a new home, and owner builders who commence laying foundations of their home between those dates.

“As a result of all of these factors, we have seen a slight uptick in the total level of first home buyer demand.”

Looking ahead, Mr Flavell said he wouldn’t be surprised to see first home buyer demand increase further as potential buyers look to take advantage of the low rate environment and various home buyer incentives soon to be on offer.

“In Victoria, some first home buyers will soon be given access to a $20,000 boosted grant. Those purchasing or constructing new homes in regional Victoria will be eligible for the grant.

“In addition, from 1 July 2017, first home buyers purchasing a home with a dutiable value of no more than $600,000 will not have to pay stamp duty – which can be a real financial impost for many first home buyers.

“These two initiatives alone are likely to encourage more first home buyers in Victoria – especially regional Victoria – onto the property ladder.”

But while Mr Flavell said he wouldn’t be surprised to see first home buyer demand climb slightly higher in places like Victoria, he said more still needs to be done by the other states and territories to help this home buyer group.

“While we have seen a slight improvement in first home buyer demand over the first few months of the year, total first home buyer demand remains very low.

“In April 2014, first home buyers made up 17.8% of all loans written through Mortgage Choice. Today, that percentage has slumped to just 14%.

“We believe more needs to be done to help first home buyers get onto the property ladder.

“The Federal Government announced earlier this month that it would allow first home buyers to salary sacrifice part of their income into their superannuation account in order to help them build their property deposit faster.

“While this initiative is great in theory, it is unlikely to have a huge impact. At best, a couple who salary sacrifice a portion of their income into their super might be able to scrape together enough money to pay for the stamp duty charged in markets like Sydney.

“Indeed, there is nothing to suggest that this new scheme will deliver a different result to the spectacularly unsuccessful First Home Saver Account initiative that was launched by the Rudd Government in 2008 and withdrawn from the market in 2014.”