Westpac announced their 1H results today, with cash earnings of $3,778 million, flat compared with the prior corresponding period and 2% lower than 2H14. Statutory net profit was $3,609 million, flat on 1H14, and 8% lower than 2H14. The expense to income ratio was 42.5% from 41.2% and there was a further improvements in asset quality with impaired assets as a percentage of gross loans falling 16 basis points to 0.35%. Whilst provisions were down, and net margins maintained at 2.01% (excluding treasury), weaker treasury income eroded the overall performance. Overall result was a little below consensus forecasts. The interim fully franked dividend was 93 cents per share, up 3% from 1H14, but 1% from 2H14.

Retail banking did quite well, but the Investment bank earnings were 17% lower due to the $85 million post tax charge as a result of derivative adjustments and a lower impairment benefit, despite customer revenues rising 6% and strong lending growth.

We see indications of building headwinds ahead relating to capital requirements, significant deposit repricing to offset mortgage discounts, and a continued reliance on the mortgage book to underpin growth. We also note a tightening of lending criteria in terms of interest rate buffers, and an intent to reduce investment property lending to below the 10% growth “alert” level. We, in other words, see responses to the dead hand of the regulator.

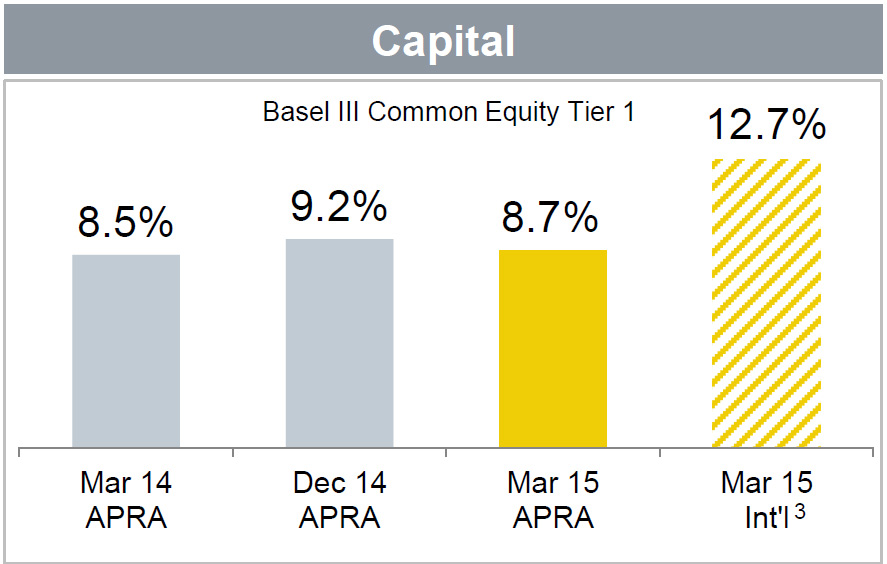

The Group’s common equity Tier 1 (CET1) capital ratio of 8.8% is well above regulatory minimums. However, due to other items, including changes in mortgage risk factors implemented during the half, the ratio is currently at the lower end of the Group’s preferred capital range of 8.75% to 9.25%. Given the current uncertainty over future capital settings, including the introduction of the next set of reforms from the Basel Committee on Banking Supervision, and the Federal Government’s assessment of the final recommendations from the Financial System Inquiry, the Group will operate at the upper end of the preferred capital range. So the Group will issue shares to satisfy the DRP for the interim dividend (at a 1.5% discount), and partially underwrite the DRP to increase CET1 capital by approximately $2 billion.

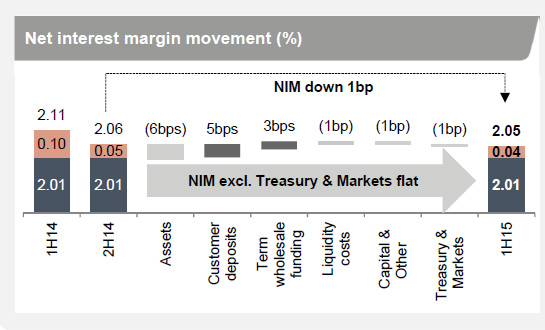

Overall net operating income was up 1%, and within that, net interest income rose 2%, supported by growth of 3% mostly from rise in Australian mortgages, and customer deposit growth of 3%, with focus on growing efficient deposits. However, net interest margin were down 1bp due to lower Treasury revenue. Margins excluding Treasury and Markets were overall flat. Turning to non-interest income, it was down 2%, whilst fees and commissions were up 1% to $1,478m, wealth and insurance fell 1% to $1,134m, trading income was down 10% to $425m (up 16% excluding derivative adjustments) and other income was down 17% to $49m.

Net Interest Margin was down 1 bp to 2.05%. NIM up across WRBB (1bp), New Zealand (2bps), and slightly down in St.George (2bps). Most margin pressure was in WIB (down 11bps). NIM excluding Treasury and Markets flat at 2.01%. Within that, we see a 6bps decrease in asset spreads primarily from impact of competitive pricing in mortgages. Business and institutional spreads also lower, 5bps increase from improved customer deposit spreads on term deposits, online accounts and savings deposits, partially offset by 1bps impact of lower hedging benefit on low-rate deposits, 3bps benefit from term wholesale funding as pricing for new term senior issuances was lower than maturing deals, 1bp decrease from increased holdings of high quality liquid assets and cost of CLF and 1bp decline in capital and other due to lower hedging rates. Treasury and Markets down 1bp, reflecting lower Treasury earnings.

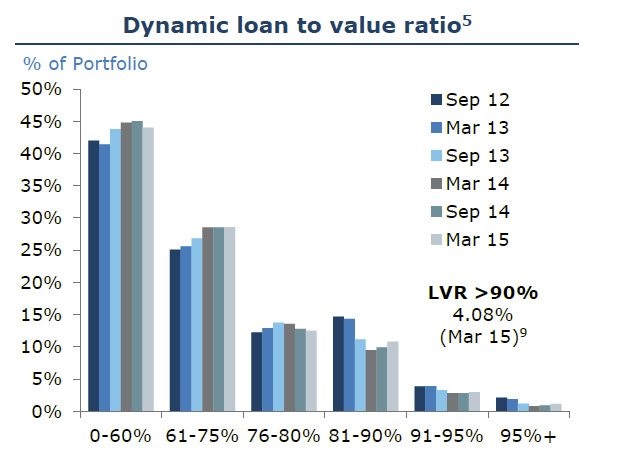

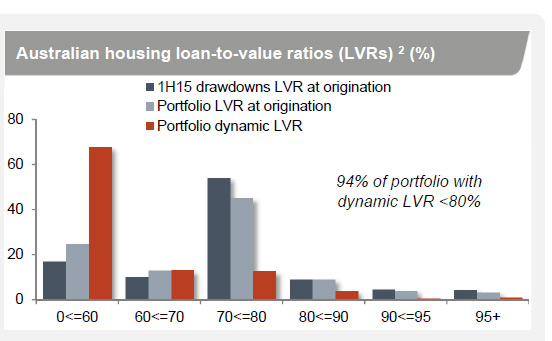

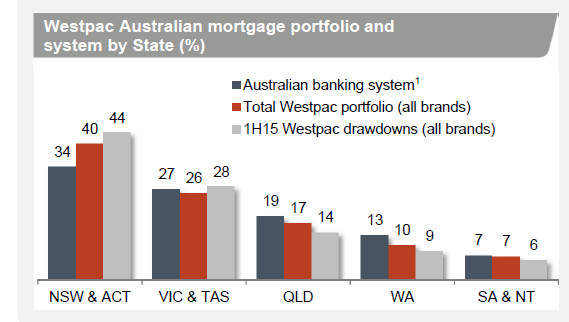

Looking at the Australian mortgage business, they have an Australian mortgage market share of 23.1% and the book grew by 0.9x system. The 3% lift in balances was partly offset by run-off of $25.2bn, up 6%. Around 20% of loans were above 80% LVR, little changed from last period, with the average LVR on new loans at 71%. 53.2% of new loans were through WBC’s proprietary channels, the share via brokers therefore continuing to rise (1H14 was 57.5% through own channels).

Looking at the Australian mortgage business, they have an Australian mortgage market share of 23.1% and the book grew by 0.9x system. The 3% lift in balances was partly offset by run-off of $25.2bn, up 6%. Around 20% of loans were above 80% LVR, little changed from last period, with the average LVR on new loans at 71%. 53.2% of new loans were through WBC’s proprietary channels, the share via brokers therefore continuing to rise (1H14 was 57.5% through own channels).

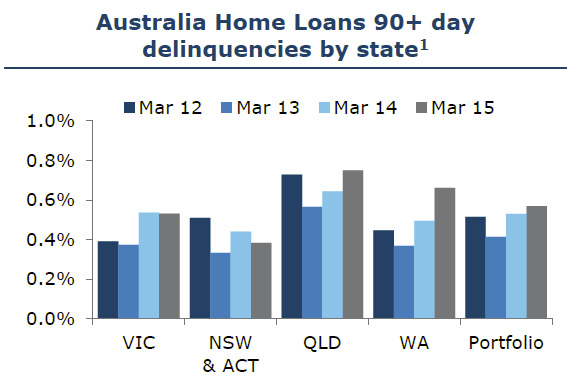

Portfolio losses of $38m in 1H15 represent an annualised loss rate of 2bps (net of insurance claims) and loss rates remain very low by international standards. Mortgage insurance claims for 1H15 were $1m (2H14 $6m, 1H14 $3m). Properties in possession remain <2bps of the portfolio, however have increased, mainly in Qld, where natural disasters and a decline in mining investment have seen weaker conditions and a review of treatment of hardship will likely see a rise in reported delinquencies in future periods.

Portfolio losses of $38m in 1H15 represent an annualised loss rate of 2bps (net of insurance claims) and loss rates remain very low by international standards. Mortgage insurance claims for 1H15 were $1m (2H14 $6m, 1H14 $3m). Properties in possession remain <2bps of the portfolio, however have increased, mainly in Qld, where natural disasters and a decline in mining investment have seen weaker conditions and a review of treatment of hardship will likely see a rise in reported delinquencies in future periods.

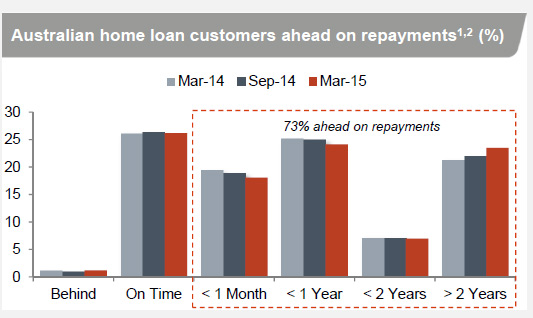

Australian mortgage customers continue to display a cautious approach to debt levels, taking advantage of historically low mortgage rates to pay down debt and build buffers. Including mortgage offset account balances, 73% of customers are ahead of scheduled payments, with 23% of these being more than 2 years ahead. Mortgage offset account balances up $3.3bn or 14% (up 29% 1H15/1H14) to $27bn. Credit decisions across all brands are made by the Westpac Group, regardless of the origination channel.

Australian mortgage customers continue to display a cautious approach to debt levels, taking advantage of historically low mortgage rates to pay down debt and build buffers. Including mortgage offset account balances, 73% of customers are ahead of scheduled payments, with 23% of these being more than 2 years ahead. Mortgage offset account balances up $3.3bn or 14% (up 29% 1H15/1H14) to $27bn. Credit decisions across all brands are made by the Westpac Group, regardless of the origination channel.

Westpac has made significant changes to their serviceability assessment. Loan serviceability assessments include an interest rate buffer, adequate surplus test and discounts to certain forms of income (e.g. dividends, rental income). Westpac now has a minimum assessment rate, often referred to as a floor rate, set at 7.10% p.a. The minimum assessment rate is at least 210bps higher than the lending rate and is applied to all mortgage debt, not just the loan being applied for. We note that the minimum assessment rate and buffer has increased from 6.80% p.a. and 180bps respectively – the regulators quiet word perhaps?

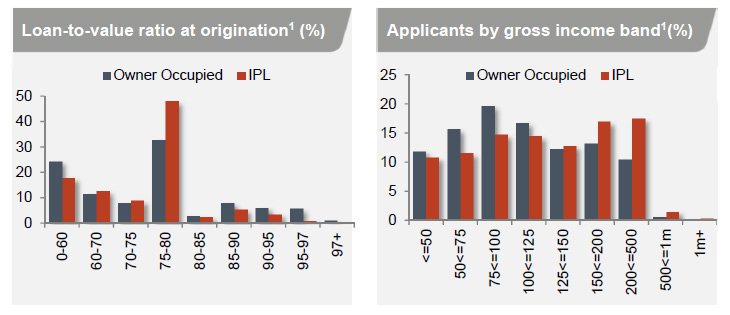

Investment property loans (IPLs) are 46.3% of Westpac’s Australian mortgage portfolio and compared to owner-occupied applicants, IPL applicants are on average older (75% over 35 years), have higher incomes and higher credit scores. 87% of IPLs originated at or below 80% LVR. Majority of IPLs are interest-only, however the repayment profile closely tracks the profile of the principal and interest portfolio, and 62% of interest-only IPL customers are ahead on repayments. IPL 90+ days delinquencies is 36bps and continue to outperform the total portfolio average. IPL portfolio losses represent an annualised loss rate of 2bps (net of insurance claims) – in line with total portfolio losses of 2bps. Self-managed Superannuation Fund balances are a very small part of the portfolio, at 1% of Australian mortgage balances.

Investment property loans (IPLs) are 46.3% of Westpac’s Australian mortgage portfolio and compared to owner-occupied applicants, IPL applicants are on average older (75% over 35 years), have higher incomes and higher credit scores. 87% of IPLs originated at or below 80% LVR. Majority of IPLs are interest-only, however the repayment profile closely tracks the profile of the principal and interest portfolio, and 62% of interest-only IPL customers are ahead on repayments. IPL 90+ days delinquencies is 36bps and continue to outperform the total portfolio average. IPL portfolio losses represent an annualised loss rate of 2bps (net of insurance claims) – in line with total portfolio losses of 2bps. Self-managed Superannuation Fund balances are a very small part of the portfolio, at 1% of Australian mortgage balances.

We are told that All IPLs are full recourse and loan serviceability assessments include an interest rate buffer, minimum assessment rate, adequate surplus test and discounts to certain forms of income (e.g. dividends, rental income). In adiditon, all IPLs, including interest-only loans, are assessed on a principal & interest basis and specific credit policies apply to IPLs to assist risk mitigation, including holiday apartments subject to tighter acceptance requirements, additional LVR restrictions apply to single industry towns, minimum property size and location restrictions apply, restrictions on non-resident lending include lower maximum LVR and discounts to foreign income recognition.

Westpac says it had more than 10% growth in investment loans (which may trigger interest from APRA and potentially additional capital), so it is actively managing the number down to 10%. We suspect this translates into tighter underwriting criteria. That said, bank portfolio stress testing indicates that even under extreme scenarios, losses, including those via their captive Lenders Mortgage Insurer would be manageable.

Westpac says it had more than 10% growth in investment loans (which may trigger interest from APRA and potentially additional capital), so it is actively managing the number down to 10%. We suspect this translates into tighter underwriting criteria. That said, bank portfolio stress testing indicates that even under extreme scenarios, losses, including those via their captive Lenders Mortgage Insurer would be manageable.

They predict that investment property lending will remain buoyant and that whilst the property market supply is not meeting demand, the market is fundamentally sound.

Turning to capital, Westpac’s preferred common equity Tier 1 (CET1) capital range is 8.75% – 9.25%. The management buffer above regulatory minimums takes into consideration the capital conservation buffer (CCB) requirement from January 2016, stress testing to maintain an appropriate buffer in a downturn, quarterly volatility of capital ratios associated with dividend payments. Given current regulatory uncertainties the Group has decided it is appropriate to move capital ratios to the upper end of the preferred range and will be issuing shares to satisfy the DRP at a 1.5% discount. They flag a number of potential capital headwinds. These include, RBNZ changes to risk weighting of investor property loans, BCBS2 initial consultation on standardised approach for determining Credit RWA and consults on RWA capital floors for advanced banks, proposals announced December 2014 with first consultation due mid-2015. BCBS work plan target date for completion end 2015. Implementation date and transition arrangements to be advised. In addition, they are awaiting Government and APRA response to provide more information on implementation of FSI recommendations, leverage ratio disclosure expected during 2015 and applicable (Pillar 1) from 2018, FSB3 undertaking a QIS4 on TLAC5 during 2015 with rules for G-SIBs expected to be finalised at G20 summit in 2015. D-SIB impacts unknown and risk model enhancements and recalibrations – IRRBB. Net net, as we have discussed we expect capital demands to be raised in the future, and this will require the bank to lift its capital buffers.