The RBA released their Minutes of the Monetary Policy Meeting of the Reserve Bank Board from 3 March 2015. Clearly housing is the potential brake on further cuts, but that said further falls are possible.

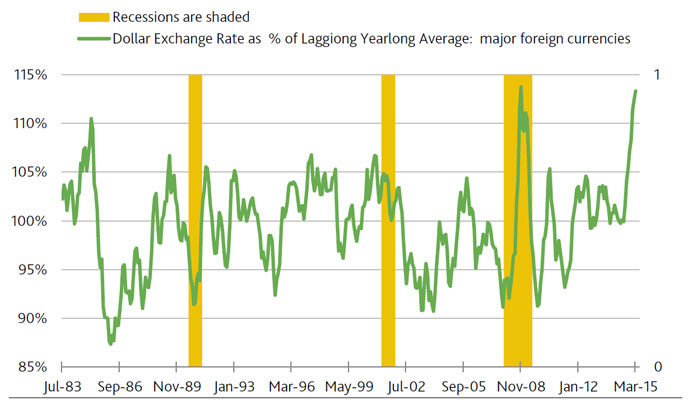

In assessing the appropriate stance for monetary policy in Australia, members noted that the outlook for global economic growth had not changed, with Australia’s major trading partners forecast to grow by around the average of recent years in 2015. Lower oil prices were expected to boost growth in major trading partners and reduce inflation temporarily. More generally, although the decline in many commodity prices over the past year had largely been in response to expansions in global supply, members observed that demand-side factors, including the weakness in Chinese property markets, had also played a role. Although the Australian dollar had depreciated, particularly against the US dollar, it remained above most estimates of its fundamental value, particularly given the significant declines in key commodity prices. Conditions in global financial markets remained very accommodative. Changes to the stance of monetary policy by the major central banks were likely to be important influences on financial markets over the coming year.

Data available at the time of the meeting suggested that the Australian economy had continued to grow at a below-trend pace in the December quarter and that domestic demand growth had remained weak overall. There had been some evidence suggesting that growth of dwelling investment and consumption had picked up in the December quarter, but there had also been indications that business investment could remain subdued for longer than had been previously expected. On balance, the evidence suggested that labour market conditions were likely to remain subdued and the economy would continue to operate with a degree of spare capacity for some time. As a result, wage pressures were expected to remain contained and inflation was forecast to remain consistent with the target over the next year or so, even with a lower exchange rate.

At the same time, activity in the housing market had remained strong. Housing prices had continued to increase strongly in Sydney and at a solid pace in Melbourne. In other capital cities, trends had been more mixed and annual increases in capital city housing prices (excluding Sydney and Melbourne) had averaged about 3 per cent. Growth of dwelling investment was estimated to have picked up in the December quarter and was expected to remain at a high level in the near term. While credit had continued to grow a little faster than incomes, household leverage had not increased significantly and the Bank would continue to work with other regulators to assess and contain risks that might arise from the housing market.

Members noted that the current setting of monetary policy had been accommodative for some time and that the recent reduction in the cash rate would provide some further support to the economy. They also acknowledged that a lower exchange rate would help achieve balanced growth in the economy. Nonetheless, on the basis of the current forecasts for growth and inflation, members were of the view that a case to ease monetary policy further might emerge.

In considering whether or not to reduce the cash rate further at this meeting, members saw benefit in allowing some time for the structure of interest rates and the economy to adjust to the earlier change. They also saw advantages in receiving more data to indicate whether or not the economy was on the previously forecast path. Further, they noted the greater degree of uncertainty about the behaviour of borrowers and savers in a world of very low interest rates. Taking account of all these factors, members judged it appropriate to hold the cash rate steady for the time being, while recognising that further easing over the period ahead may be appropriate to foster sustainable growth in demand while maintaining inflation consistent with the target.

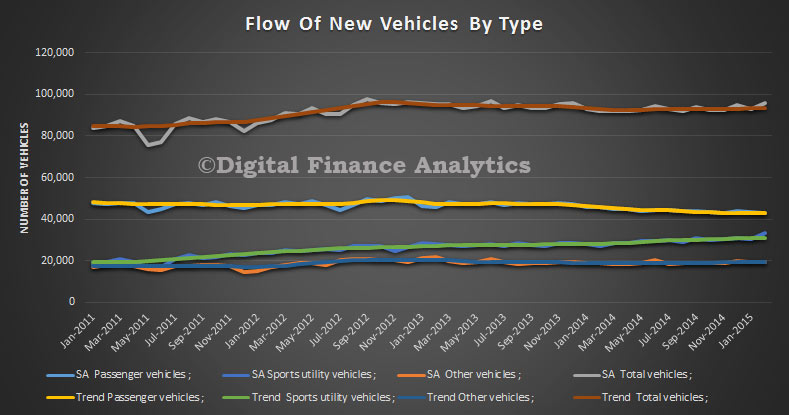

Five of the eight states and territories experienced an increase in new motor vehicle sales when comparing February 2015 with January 2015 in trend terms. Tasmania recorded the largest percentage increase (1.7%), followed by Queensland (0.6%) and both Victoria and South Australia (0.3%). Over the same period, Western Australia, the Northern Territory and the Australian Capital Territory all recorded decreases in sales of 0.3%.

Five of the eight states and territories experienced an increase in new motor vehicle sales when comparing February 2015 with January 2015 in trend terms. Tasmania recorded the largest percentage increase (1.7%), followed by Queensland (0.6%) and both Victoria and South Australia (0.3%). Over the same period, Western Australia, the Northern Territory and the Australian Capital Territory all recorded decreases in sales of 0.3%.