The latest edition of our weekly finance and property news digest with a distinctively Australian flavour.

Category: Banking Culture

Why APRA Is Not Fit For Purpose

I discuss the recent APRA Capability Review with Business Man and Ex ANZ Director John Dahlsen. We discuss the need to change APRA, and also look at the structure of banking more generally.

Ex RBS Boss To Head NAB Next Year

Former chief executive of the Royal Bank of Scotland, Ross McEwan has been appointed to the role of group chief executive officer and managing director.

Mr McEwan has been chief executive of the Royal Bank of Scotland since 2013 and led the bank through significant change and recovery.

Mr McEwan will start at NAB no later than April 2020 when his obligations to RBS are wrapped up and will be invited to join the board of NAB at that time.

NAB chairman-elect Philip Chronican said NAB was pleased with its appointment of Mr McEwan given his long-standing knowledge of the banking industry.

“Ross McEwan is the ideal leader for NAB as we seek to transform our operations and culture firmly around leading customer service, experience and products,” Mr Chronican said.

“Ross brings a compelling range of experience across finance, insurance and investment with a track record of delivering important and practical improvements for customers. RBS has been through many of the same challenges which NAB now faces around culture, trust and reputation.”

Mr McEwan who was group executive of retail banking at CBA for five years said he looked forward to returning to Australia.

“It is a privilege to return to Australia and lead NAB at a crucial time for the bank, its customers, employees, shareholders and the broader community.

“There are a number of areas where NAB can extend its lead, such as business banking, agriculture and health, and other areas where I believe we should consistently lead such as customer service. We must also meet and exceed the expectations of our many stakeholders,”he said.

The new appointment means Mr Chronican will now take over Dr Ken Henry’s role as chairman in mid-Novemeber.

The board will put other interim management arrangements suitable to APRA in place if required before Mr McEwan starts.

Fitch Ratings downgrades Westpac, ANZ outlook

Credit rating agency Fitch Ratings has changed its outlook on Westpac and ANZ from “stable” to “negative”, following APRA’s update of its capital requirements for the major banks. Via InvestorDaily.

While the additional operational capital requirements should remain manageable for the banks, Fitch said the main driver for the changes were driven by a concern for governance and culture in the institutions.

Westpac recently released its self-assessment on governance, accountability and culture, admitting significant shortcomings.

The big four evaluated themselves last year when APRA chair Wayne Byres wrote to the country’s banks, insurers and super licensees after the CBA prudential inquiry. He asked them to determine whether weaknesses uncovered at CBA existed in their companies.

The result of the self-assessments led APRA last week to increase the minimum capital requirements by $500 million and prompted Westpac to release publicly its self-assessment.

ANZ is the only bank of the big four which has yet to publish its self-assessment.

“The additional capital requirements should remain manageable and not impair the bank’s ability to meet APRA’s ‘unquestionably strong’ targets starting in 2020, but it indicates material shortcomings in operational risk management, which were not aligned to what Fitch had previously incorporated into its ratings,” Fitch said in its update on Westpac.

“This has resulted in a downward revision to our score for management and strategy and weaker outlook on earnings and profitability.”

The rating agency made a similar note on ANZ, saying APRA’s findings indicated deficiencies within both companies’ management of operational and compliance risks, culture and governance.

However, Westpac said Fitch’s affirmation of its rating at AA- meant despite the challenges the bank faces, the credit agency expects it to “maintain its strong company profile in the short term, which in turn supports its strong financial profile.”

Likewise, ANZ was reaffirmed at AA- for both its banking group and New Zealand company. Fitch stated the group “continues to have robust risk and reporting controls around other risks, including credit, market and liquidity risk, as reflected by its conservative underwriting standards and very high degree of asset quality stability.”

Separately, on 9 July S&P Global Ratings affirmed the AA- long-term and A-1+ short-term issuer credit ratings and revised its outlook on the major Australian banks to “stable” from “negative.”

Westpac commented: “This outlook change reflects S&P’s view that the Australian government remains highly supportive of Australia’s systemically important banks based on APRA’s release on loss absorbing capacity.”

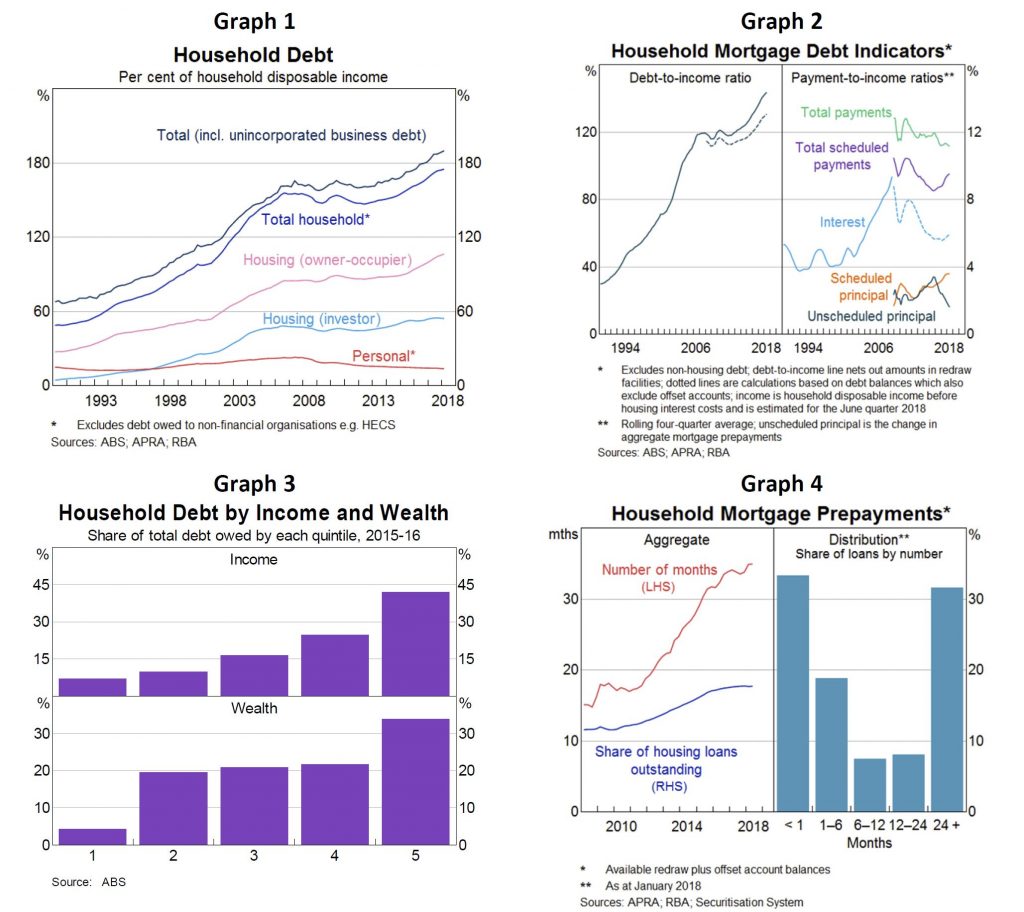

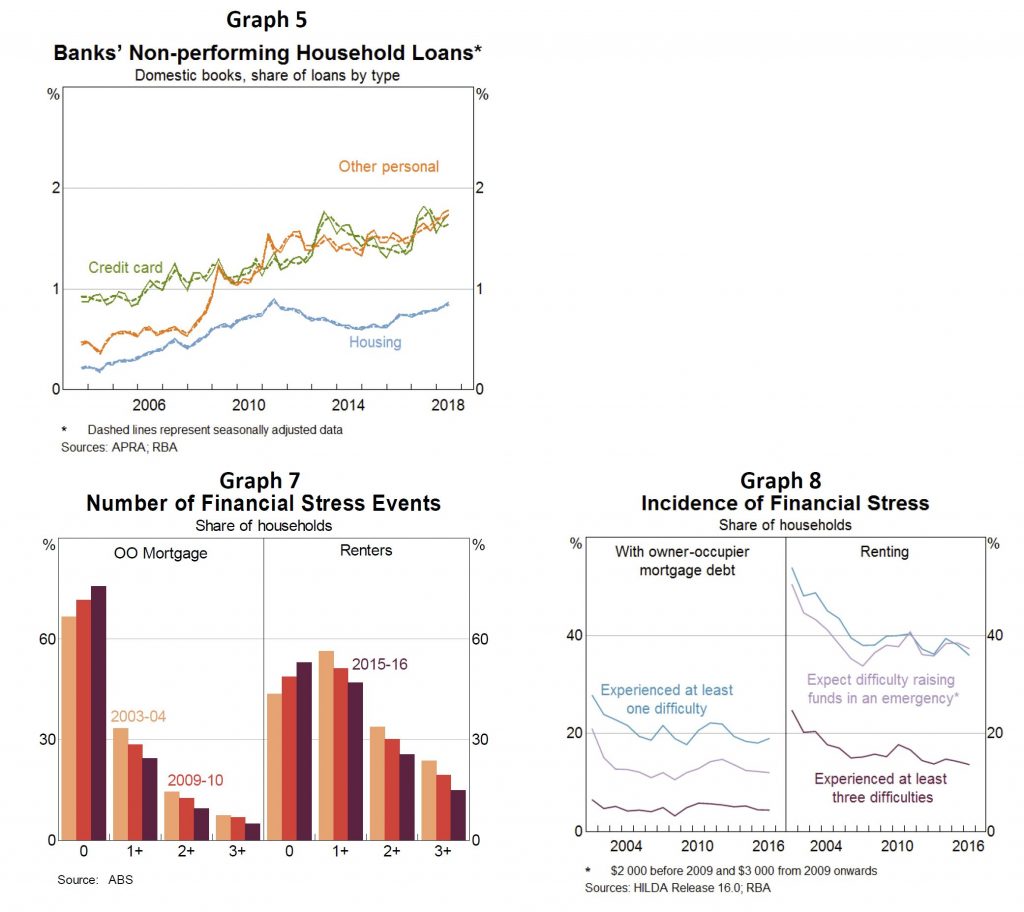

RBA On Household Debt And Financial Stress – FOI

The RBA released a freedom of information request today. They say:

Household debt-to-income has drifted up, to 190 per cent (Graph 1 – broad measure, includes debt of unincorporated enterprises, new migrants’ offshore debt, HECS and to non-financials).

More frequently we cite housing debt-to-income which has increased to over 140 per cent (up 23 percentage points over five years) (Graph 2); net of offset accounts this is around 130 per cent (up 16 percentage points over five years).

High income and wealthy households hold a large proportion of household debt (Graph 3). In 2015-16 the top income quintile accounted for about 40 per cent of total debt and the top wealth quintile owed one-third of total debt; this share has been stable over time.

Debt servicing ratios have been broadly steady: falling rates offset rising debt.

Aggregate mortgage prepayments (offsets and redraws) are equivalent to 18 per cent of outstanding mortgages and nearly 3 years of scheduled repayments at current interest rates (Graph 4). One-third have no buffer: many are investors, on fixed-rate or new borrowers. Largest buffers typically: wealthier, higher income and more seasoned mortgages.

The housing non-performing loan (NPL) ratio has increased since the end of 2015 (mostly WA), but remains below the most recent peak in 2011 (Graphs 5 and 6).

NPL ratios for personal loans and credit cards remain high relative to recent history (personal credit is only about 4 per cent of banks’ household lending).

Broad data sources suggest the number of households experiencing financial stress has fallen over the past decade, but there are regional variations. Household Expenditure Survey (2015/16): the number of households experiencing financial stress has fallen steadily since the mid-2000s (Graph 7). HILDA (2016): measures of financial stress are little changed over the decade and are lower than the early 2000s (Graph 8).

ASIC’s recent report on credit cards links problematic debt with multiple credit card usage, corroborating messages from liaison (but overall more households are paying off each month).

Some private surveys point to rising mortgage stress. These surveys are timely but their methodologies often seem to overstate financial stress (e.g. using actual, rather than required mortgage payments, which include prepayments).

Concerns about stress when IO loan converts to a principal-and-interest (P&I) loan. Required repayments are estimated to increase by 30-40 per cent (about $7,000 per year) for a ‘representative interest-only borrower with a $400,000 mortgage converting to P&I.

Based on loans in the Securitisation Dataset, a large share of borrowers should qualify for an IO extension or could refinance with a different lender.

Borrowers that can’t meet new lending standards and are unable to service P&I repayments might sell their properties or default. We estimate this is a small group (eg borrowers with multiple highly leveraged investment properties).

Tighter lending standards are unlikely to bind for borrowers that: undertook a serviceability assessment at loan origination that already took into account the step up in repayments at the end of the interest-only periods (as APRA has required for all such assessments since end 2014); Did not borrow (close to) the maximum loan size available to them; Have experienced income growth since the loan was originated; Have made prepayments on their loans; and/or Were assessed for their original loans at significantly higher interest rates than current assessment rates.

Most borrowers will have positive equity given the rate of housing price growth over the last five years.

The RBA FOI On First Home Loan Deposit Scheme

The RBA just released a FOI relating to the Federal Government’s proposed First Home Loan Deposit Scheme. How many loans might be made?

“the point of the estimates is that the various caps on the scheme (10,000 loan cap, income and house prices) are likely to be the binding constraint on the amount of loans provided rather than the scheme’s equity funding”.

To provide some context:

Based on ABS numbers, in the year to February there were 110,000 loans to first home buyers. The average loan size in February to FHB was $337,412. Usual caveats apply to these data.

Using the average loan size to FHB and assuming the scheme covers 15 per cent, the government will guarantee around $50,000 per loan. If the scheme has $500 million in funding, this implies

– 9,879 loans if the scheme holds reserves covering 100 per cent of its commitments.

– 49,395 loans with 20 per cent reserves.

– 98,790 loans with 10 per cent reserves.

– 197,583 loans with 5 per cent reserves.Average loan size data are biased downwards, so can use average house prices instead as arguably an upper bound. In the December quarter ABS average house prices were $650,000. 15 per cent of this is $97,500.

– 5,128 loans if the scheme holds reserves covering 100 per cent of its commitments.

– 25,641 loans with 20 per cent reserves.

– 51,282 loans with 10 per cent reserves.

– 102,564 loans with 5 per cent reserves.

RBA flags ‘overhang effect’ of rising mortgage debt

Well, surprise, surprise, the RBA has realised that high mortgage debt reduces household consumption, according to new research they published. Yet they also note the positive economic impact of higher debt, and say the the overall impact is “unclear”! Well, the DFA surveys make it quite clear, many households are “full” of debt” and cannot spend.

New research from the Reserve Bank has highlighted the link between mortgage debt and household spending amid debate over home loan serviceability assessment guidelines.

The Reserve Bank of Australia (RBA) has published new research from its economic research department, which has identified evidence of a link between “high levels of owner-occupier mortgage debt” and a fall in household spending, referred to as the “overhang effect”.

According to The Effect of Mortgage Debt on Consumer Spending report, if mortgage levels remained at “2006 levels”, annual aggregate consumption would have been approximately 0.2 to 0.4 per cent higher.

The RBA added that the negative effect of debt on spending is “pervasive” across households with owner occupied home loans.

“Our results also suggest that an increase in aggregate owner-occupier mortgage debt can have important implications for aggregate spending, all else constant, and go at least part of the way to resolving the post-crisis ‘puzzle’ of unusually weak household spending in Australia,” the RBA report stated.

The central bank’s research comes amid continue debate over home loan serviceability assessment standards, with the Australian Prudential Regulation Authority (APRA) and the Australian Securities and Investments Commission (ASIC) moving to reform current practices.

ASIC’s proposed update of its responsible lending guidance (RG209) has been met with a renewed call from stakeholders for a revision to the way a borrower’s spending habits are assessed.

The RBA’s research has supported claims from some stakeholders, including Westpac, who have noted that changes in a borrower’s spending behaviour after they assume mortgage debt should be reflected in regulatory guidance.

In its submission to ASIC during the regulator’s first round of consultation, Westpac called for greater flexibility in the assessment of a borrower’s living expenses.

“Adopting a modest lifestyle for a period of time in order to acquire real property has been the means by which many Australians have secured long-term financial security,” Westpac stated.

“Experience shows that many customers are prepared to, and do actually, make lifestyle adjustments after acquiring a home and can then service their home loan obligations without substantial hardship.

“As such, Westpac submits that placing too much emphasis on the customer’s pre-application living expenses when determining suitability, without allowing scope for reasonable lifestyles adjustments (‘belt-tightening’), would have the effect of denying credit to many customers.”

Impact on economy still ‘unclear’

Despite confirming the direct impact of higher mortgage debt on household spending, the RBA has maintained that the impact of the “debt overhang’ on the overall economy remains “unclear’, noting the positive stimulatory contribution of the credit boom. stating that

“[These] estimates abstract from other stimulatory effects of debt,” the report noted.

“The increase in mortgage debt has likely lifted house prices and by this also supported consumption over this period.

“Our estimates are thus best interpreted as the loss in consumption had all other trends, such as the growth in house prices, occurred even though debt remained constant.”

The RBA concluded: “As a result, the net effect of the increase in debt since the mid-2000s is unclear.”

APRA applies additional capital requirements to ANZ, NAB and Westpac

The Australian Prudential Regulation Authority (APRA) is applying additional capital requirements to three major banks to reflect higher operational risk identified in their risk governance self-assessments.

APRA has written to ANZ, National Australia Bank (NAB) and Westpac advising of an increase in their minimum capital requirements of $500 million each. The capital add-ons will apply until the banks have completed their planned remediation to strengthen risk management, and closed gaps identified in their self-assessments.

The increase in capital requirements follows APRA’s decision in May last year to apply a $1 billion dollar capital add-on to Commonwealth Bank of Australia (CBA) in response to the findings of the APRA-initiated Prudential Inquiry into CBA.

Following the CBA Inquiry’s Final Report, APRA wrote to the boards of 36 of the country’s largest banks, insurers and superannuation licensees asking them to gauge whether the weaknesses uncovered by the Inquiry also existed in their own companies. Although the self-assessments raised no concerns about financial soundness, they confirmed that many of the issues identified in the Inquiry were not unique to CBA. This included the need to strengthen non-financial risk management, ensure accountabilities are clear, cascaded and enforced, address long-standing weaknesses and enhance risk culture.

APRA Chair Wayne Byres said: “Australia’s major banks are well-capitalised and financially sound, but improvements in the management of non-financial risks are needed. This will require a real focus on the root causes of the issues that have been identified, including complexity, unclear accountabilities, weak incentives and cultures that have been too accepting of long-standing gaps.

“The major banks play a vital role in the stability of the entire financial system, and APRA expects them to hold themselves to the highest standards of risk governance. Their self-assessments reveal that they have fallen short in a number of areas, and APRA is therefore raising their regulatory capital requirements until weaknesses have been fully remediated,” Mr Byres said.

APRA supervisors continue to provide tailored feedback to other banks, insurers and superannuation licensees that provided self-assessments to APRA. Where weaknesses have been identified, the level of supervisory scrutiny is being increased as remediation actions are implemented. Where material weaknesses exist, APRA is also considering the need for the application of an additional operational risk capital requirement.

Fed Confirms Easing Bias

In the latest FOMC minutes, the tone suggests a potential easing rate bias, recognising the rising economic risks. Uncertainties have increased they say.

In their discussion of monetary policy for the period ahead, members noted the significant increase in risks and uncertainties attending the economic outlook. There were signs of weakness in U.S. business spending, and foreign economic data were generally disappointing, raising concerns about the strength of global economic growth. While strong labor markets and rising incomes continued to support the outlook for consumer spending, uncertainties and risks regarding the global outlook appeared to be contributing to a deterioration in risk sentiment in financial markets and a decline in business confidence that pointed to a weaker outlook for business investment in the United States. Inflation pressures remained muted and some readings on inflation expectations were at low levels. Although nearly all members agreed to maintain the target range for the federal funds rate at 2-1/4 to 2-1/2 percent at this meeting, they generally agreed that risks and uncertainties surrounding the economic outlook had intensified and many judged that additional policy accommodation would be warranted if they continued to weigh on the economic outlook. One member preferred to lower the target range for the federal funds rate by 25 basis points at this meeting, stating that the Committee should ease policy at this meeting to re-center inflation and inflation expectations at the Committee’s symmetric 2 percent objective.

Members agreed that in determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee would assess realized and expected economic conditions relative to the Committee’s maximum-employment and symmetric 2 percent inflation objectives. They reiterated that this assessment would take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. More generally, members noted that decisions regarding near-term adjustments of the stance of monetary policy would appropriately remain dependent on the implications of incoming information for the economic outlook.

With regard to the postmeeting statement, members agreed to several adjustments in the description of the economic situation, including a revision in the description of market-based measures of inflation compensation to recognize the recent fall in inflation compensation. The Committee retained the characterization of the most likely outcomes as “sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective” but added a clause to emphasize that uncertainties about this outlook had increased. In describing the monetary policy outlook, members agreed to remove the “patient” language and to emphasize instead that, in light of these uncertainties and muted inflation pressures, the Committee would closely monitor the implications of incoming information for the economic outlook and would act as appropriate to sustain the expansion, with a strong labor market and inflation near its symmetric 2 percent objective.

The Great KiwiSaver Robbery

Property expert Joe Wilkes and I discuss who is saving, and why.