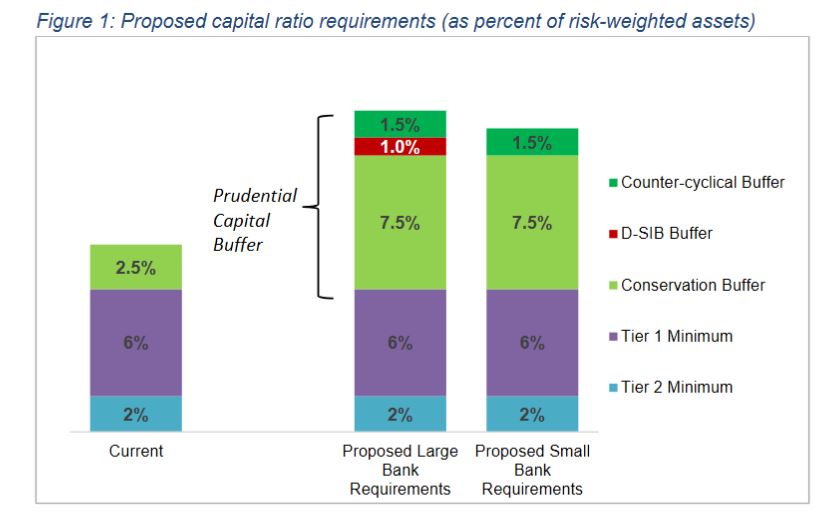

The Reserve Bank of New Zealand has released a discussion paper in which they consult on proposals to lift the capital held by banks in New Zealand.

The expected effect on banks’ capital is an increase of between 20 and 60 percent. This represents about 70 percent of the banking sector’s expected profits over the five-year transition period. They expect only a minor impact on borrowing rates for customers.

They say “Banks currently get the vast majority of their money by borrowing it (usually over 90 percent), with the rest coming from owners (usually less than 10 percent). The Reserve Bank is proposing to change this balance by requiring banks to use more of their own money. This proposal is consistent with steps taken by other banking regulators after the Global Financial Crisis”.

Banks currently get the vast majority of their money by borrowing it (usually over 90 percent), with the rest coming from owners (usually less than 10 percent). The Reserve Bank is proposing to change this balance by requiring banks to use more of their own money. This proposal is consistent with steps taken by other banking regulators after the Global Financial Crisis.

If banks increase their capital, they will be more resilient to economic shocks and downturns, which will strengthen New Zealand’s banking system and economy.

Because the level of a bank’s capital can have an impact on the interest rate it charges on its loans, it is possible that higher capital requirements could make it more expensive for New Zealanders to borrow money from a bank. While we certainly take this into account, we think this impact should be minimal.

Another potential impact is that bank owners would earn less from their investment in the bank. While we agree that this is likely to be the case, we believe this cost would be more than offset by the benefits of a safer banking system for all.

The key changes are:

Limit the extent to which capital requirements differ between the Internal Ratings-Based approach (IRB) and the Standardised approach, by re-calibrating the IRB approach and applying a floor linked to the Standardised outcomes. This reflects one of the principles of the Capital Review: where there are multiple methods for determining capital requirements, outcomes should not vary unduly between methods. In essence, there should be as level a playing field as possible, both between IRB banks and between IRB and Standardised banks;

These proposals are expected to raise risk-weighted assets (RWA) for the four IRB-accredited banks to approximately 90 percent of what would be calculated under the Standardised approach;

Set a Tier 1 capital requirement (consisting of a minimum requirement of 6 percent and prudential capital buffer of 9-10 percent) equal to 16 percent of RWA for banks deemed systemically important, and 15 percent for all other banks;

Assign 1.5 percentage points of the proposed prudential capital buffer requirements to a countercyclical component, which could be temporarily reduced to 0 percent during periods of exceptional stress;

Assign 1 percentage point of the proposed prudential capital buffer requirement to D-SIB buffer, to be applied to banks deemed to be systemically important;

Retain the current Tier 2 capital requirement of 2 percent of RWA, but raise the question of whether Tier 2 should remain in the capital framework; and

Staged transition of the different components of the revised framework over the coming years.

A welcome move, the shadowy Council Of Financial Regulators has started publishing minutes of its quarterly meetings. However, group think, and self-interest is all over it. Specifically the comments about tighter credit, and the need to continue to lend (to keep the debt bomb ticking a bit longer! Also how does independence of the RBA work in this context?

They noted that non-ADI lending for housing has been growing significantly faster than ADI housing lending and there is some evidence that non-ADI lending for property development is also increasing quickly.

As part of its commitment to transparency, the Council of Financial Regulators (the Council) has decided to publish a statement following each of its regular quarterly meetings. This is the first such statement.

The statement will outline the main issues discussed at each meeting. From time to time the

Council discusses confidential issues that relate to an individual entity or to policies still

in formulation. These issues will only be included in the statement where it is appropriate to

do so.

The Council of Financial Regulators (the Council) is the coordinating body for Australia’s

main financial regulatory agencies. There are four members: the Australian Prudential

Regulation Authority (APRA), the Australian Securities and Investments Commission (ASIC),

the Australian Treasury and the Reserve Bank of Australia (RBA). The Reserve Bank Governor

chairs the Council and the RBA provides secretariat support. It is a non-statutory body,

without regulatory or policy decision-making powers. Those powers reside with its members.

The Council’s objectives are to contribute to the efficiency and effectiveness of financial

regulation, and to promote stability of the Australian financial system. The Council

operates as a forum for cooperation and coordination among member agencies. It meets each

quarter, or more often if required.

At each meeting, the Council discusses the main sources of systemic risk facing the

Australian financial system, as well as regulatory issues and developments relevant to its

members. Topics discussed at its meeting on 10 December 2018 included the following:

Financing conditions. Members discussed the tightening of credit conditions for households

and

small businesses. A tightening of lending standards over recent years has been appropriate

and

has strengthened the resilience of the system. At the same time, members agreed on the

importance of lenders continuing to supply credit to the economy while they adjust their

lending

practices, including in response to the Royal Commission into Misconduct in the Banking,

Superannuation and Financial Services Industry. Members discussed how an overly cautious

approach by some lenders to incorporating relevant laws and standards into loan approval

processes may be affecting lending decisions.

Members observed that housing credit growth has moderated since mid-2017, with both demand

and supply factors playing a role. The demand for credit by investors has slowed noticeably,

largely reflecting the change in the dynamics of the housing market. In an environment of

tighter lending standards, the decline in average interest rates for owner-occupier and

principal and interest loans suggests that there is relatively strong competition for

borrowers of low credit risk. Credit to owner-occupiers is continuing to grow at 5 to 6 per

cent.

Non-ADI lending. The Council undertook its annual review of non-bank financial

intermediation. Overall, lending by non-ADIs remains a small share of all lending. However,

non-ADI lending for housing has been growing significantly faster than ADI housing lending

and there is some evidence that non-ADI lending for property development is also increasing

quickly. The Council supported efforts to expand the coverage of data on non-ADI lenders,

drawing on new data collection powers recently granted to APRA.

Housing market. Members discussed recent developments in the housing market.

Conditions have eased, but this follows a period of considerable strength in the market.

Housing prices have been declining in Sydney, Melbourne and Perth, but are stable or rising

in most other locations. The easing in the housing market is occurring in a period of

favourable economic conditions, with low domestic unemployment and interest rates and a

supportive global economy. The Council will continue to closely monitor developments.

Prudential measures. APRA briefed the Council on its latest review of the countercyclical

capital buffer, the results of which will be published in the new year. It also provided an

update on its residential mortgage measures, including the investor lending and

interest-only lending benchmarks. In line with APRA’s announcement in April 2018 that it

would remove the investor lending benchmark subject to assurances of the strength of lending

standards, the benchmark has now been removed for the majority of ADIs. The interest-only

lending benchmark, introduced in 2017, has resulted in a reduction in the share of new

interest-only lending, along with the share of interest-only lending that occurs at high

loan-to-valuation ratios.

Financial sector competition. The Council discussed work by its member agencies in response

to the Productivity Commission’s Final Report of its Inquiry into Competition in the

Australian Financial System. The Council strongly supports improved transparency of mortgage

interest rates and a working group is examining a number of options. The Council also

discussed the Productivity Commission’s recommendations relating to lenders mortgage

insurance and remuneration of mortgage brokers.

Both the Productivity Commission and the Financial System Inquiry recommended a review of the

regulation of payments providers that hold stored value – referred to in legislation as

purchased payment facilities (PPFs). The Council released an issues paper in September and held

an industry roundtable in November. Members considered the feedback received from these

processes and received an update on progress with the review.

Limited recourse borrowing by superannuation funds. Members discussed a report to Government

on leverage and risk in the superannuation system, as requested in the Government’s response to

the Financial System Inquiry. The use of limited recourse borrowing arrangements remains

relatively small, but has risen over time. Leverage by superannuation funds can increase

vulnerabilities in the financial system, though near-term risks have reduced with the shift in

dynamics in the housing market.

International Monetary Fund’s Financial Sector Assessment Program (FSAP). The FSAP review of

Australia was conducted during the course of 2018; preliminary findings were presented to the

Australian authorities in November. The Council held an initial discussion of the main FSAP

recommendations and how they could be addressed. The FSAP will be finalised in early 2019, at

which time summary documents will be published. (Further information on the FSAP review was

published in the Reserve Bank’s October 2018

Financial Stability Review.)

Representatives of the Australian Competition and Consumer Commission and the Australian

Taxation Office attended the meeting for discussions relevant to their responsibilities.

A class action lawsuit that was being planned on behalf of “Australian bank customers that have entered into mortgage finance agreements with banks since 2012” has been dropped due to a lack of a “clear cause of action”; via The Adviser.

Law

firm Chamberlains has announced that its major class action against

various Australian banks will no longer proceed despite interest in the

matter.

In May of this year, it was announced that law firm

Chamberlains had been appointed to act in the planned class action

lawsuit, which was instructed by Roger Donald Brown of

MortgageDeception.com to represent various Australian bank customers

that had been “incurring financial losses as a result of entering into

mortgage loan contracts with banks since 2012”.

The law firm had

been calling on bank customers to join the class action, led by Stipe

Vuleta, if they had “incurred financial losses due to irresponsible

lending practices”.

In an update to interested parties, seen by

The Adviser, Chamberlains commented: “Over the last few months, we have

been busy investigating the scope of a potential legal claim, which

could be commenced as a class action against various Australian banks.

“During

this process, we have engaged with senior and junior counsel to assist

with the questions of law to be raised if an action were to be commenced

in the Federal Court of Australia.

“Despite

our efforts, we have been unable to identify a clear class of claimants

who have a clear cause of action against a particular Australian bank.”

It continued: “As a result, we are unable to take this process further.”

While

the law firm has said that some may still have “an individual case

arising from [their] dealings with the banks, which may have merit

outside of the framework of a class action”, it would encourage those

people to “seek independent legal advice about [their] claim”.

Class actions in focus

Several

class actions against major lenders have already been initiated

following some of the revelations from the royal commission, including four separate class actions against AMP on

the grounds that the company breached its obligations to customers and

engaged in “misleading and deceptive representations to the market”.

The legal action was announced after senior AMP executives appeared before the royal commission as

witnesses. Some of the executives admitted to a number of potential

crimes and suggested that these were repeatedly mischaracterised to the

Australian Securities and Investments Commission (ASIC) and to its

customers as being “administrative errors”.

These included

providing false and misleading statements to the regulator and charging

customers for services that were not provided.

Westpac incurred a first strike against its remuneration report at its annual general meeting this week, where chairman Lindsay Maxsted said the ruling would send a strong message to the board; via InvestorDaily.

CEO Brian Hartzer along with Mr Maxsted also addressed the royal

commission, the bank’s financial performance for the past year and the

executives’ remuneration in the company’s AGM.

Peter Hawkins, non-executive director, retired following the AGM,

after 10 years of being on the board. Westpac will be electing two new

non-executive directors in the first half of calendar 2019.

While the poll on the remuneration report among shareholders had not

been completed at the time of the chairman’s address, more than half of

the votes already received were against the resolved salaries.

“Feedback from shareholders has varied, but the key point from those

voting against the remuneration report has been that although the board

took events over the year into account, many have questioned whether we

went far enough, particularly in reducing short-term variable reward

paid to the CEO and other executives,” Mr Maxsted said.

The short-term variable reward for the Westpac CEO and group

executives in Australia were on average, 25 per cent lower than last

year.

No long-term variable reward was vested in 2018. Around one-third of

the board’s potential remuneration forfeited, which Mr Maxsted said was

equivalent to about $18 million.

The CEO saw his short-term variable reward outcome cut by 30 per cent, or $900,000 over the past year.

The largest individual year on year reduction was 50 per cent, although Westpac did not disclose who it was, or for what reason.

“This is entirely consistent with the relatively weak performance of

shares in the banking sector, including Westpac, over the last few

years, including the 2018 financial year,” Mr Maxsted said.

“Putting this another way, for the CEO, his total variable reward outcome was 36 per cent of his total target variable reward.”

The chairman said the key failings from Westpac in light of the royal

commission were not fully appreciating the underlying risks in the

financial planning business, employee remuneration contributing to poor

behaviour and inadequacy in dealing with complaints.

“Better training and supervision, changes to the way financial

planners were remunerated, and better documentation of advice was

required,” Mr Maxsted said.

“As we have seen across the industry, where we get it wrong, the remediation is costly,” Mr Hartzer said.

“What has been clear is that we have not always embedded strong

enough controls and record-keeping around ensuring that customers

received the advice they had signed up for.”

Mr Maxsted also cited Westpac’s slowness in focusing on non-financial risks.

“In 2018, our financial performance was mixed; we have further built

on the balance sheet and financial strengths that are a hallmark for

Westpac but our annual profit was relatively flat over the year,” Mr

Maxsted said.

Cash earnings for the year ended 30 September was $8 billion, $3

million up on the year before. Reported profit reached $8.1 million,

increasing by 1 per cent from the prior corresponding period.

Business Bank grew profits by 8 per cent and New Zealand was up 5 per

cent. Excluding the cost of remediation provisions, BT’s profit was

down 1 per cent.

Institutional Banking saw its profit go down by 6 per cent, which Mr

Hartzer said largely represents a slowdown in financial markets

activity.

The bank also saw a slowdown in housing lending, with credit growing

5.2 per cent in the past 12 months, when it was 6.6 per cent in 2017.

“The group began the year solidly with good growth and well-managed

margins in the first half. Conditions in the second-half, however, were

more difficult with higher funding costs, lower mortgage spreads, and a

reduced markets and treasury contribution,” Mr Maxsted said.

“In addition, we needed to lift provisions associated with customer

refunds and regulatory/litigation costs as we address some of the legacy

issues alluded to earlier.”

The board determined a final dividend of 94 cents per share,

unchanged over the prior half and consistent with the final dividend for

2017. The full year dividend comes to 188 cents per share, unchanged

from the year before.

Mr Maxsted also noted Westpac removing grandfathered commission

payments in the past year, saying it was the first in the market to do

so.

“With revenue growth continuing to be a challenge, we have re-doubled

our efforts to reduce costs by simplifying our products, automating

process and modernising our technology platform,” Mr Hartzer said.

“Over recent years, we have delivered productivity savings of around

$250-300 million per year. In 2019, we aim to lift that to more than

$400 million – almost one third higher than 2018.”

Mr Maxsted also mentioned the bank’s development of its new Customer

Service Hub, the group’s multibrand operating system. The system is now

in pilot and will go live with new Westpac mortgages in 2019.

In terms of outlook, Mr Hartzer said that while it seemed positive as

a whole for the Australian economy, for banks, it looked more

challenging.

“Although credit quality is likely to remain a positive, low interest

rates, slowing credit growth, and a fall in consumer and business

confidence – especially about house prices – puts pressure on bank

earnings growth,” he said.

In a statement this morning, Bank of Queensland said the BOQ and Freedom had mutually agreed to terminate the St Andrews Insurance sale and purchase agreement.

“Following the termination of the agreement with Freedom, BOQ will continue to assess its strategic options in relation to St Andrew’s. In the meantime, St Andrew’s continues to be a strongly capitalised business that remains focused on delivering for its customers and corporate partners,” BOQ said.

The troubled Freedom Insurance Group last week completed its

strategic review, which was prompted by ASIC’s recommendations about the

life insurance industry.

As part of the review, which was conducted in collaboration with

Deloitte, the Freedom board identified that the company may face a

liquidity shortfall during calendar year 2019 arising from the timing of

payments of commission clawbacks in the absence of receipts of

commissions from new business sales.

Freedom had been pursuing equity funding for the purposes of the St Andrews acquisition, the process of which has included the provision of confidential due diligence to prospective third-party investors and negotiation of related transaction documentation.

it became clear that the conditions of the transaction would not be satisfied within the time limits contained in the sale agreement they said..

“In this regard, the company is considering alternate options to address the potential shortfall,” the group said in a trading update”.

“In addition, Freedom is implementing initiatives to improve operational efficiency and reduce costs.”

Freedom expects to make a provision for net remediation costs in its

financial accounts for the period ending 31 December 2018 of between

approximately $3 million and $4 million.

He concludes that “Global developments undoubtedly influence Australian financial conditions. In particular, developments abroad can influence the value of the Australian dollar and affect global risk premia. But changes in monetary policy settings elsewhere need not, and do not, mechanically feed through to the funding costs of Australian banks, and hence their borrowers are insulated from such changes”.

But the higher bank funding rate spreads which see here are perhaps more of a reflection of the risks the markets are pricing in, than anything else. Yet this was not discussed. Too low rates here for several years are the root cause (and guess where the buck for that stops?). This led to overheated lending, and home prices, which are now reversing, with obvious pressures on the banks. This leaves the economy open to higher rates, from overseas ahead.

This is the speech:

Australia is a small open economy that is influenced by developments in the rest of the world.

Financial conditions here can be affected by changes in monetary policy settings elsewhere, most

particularly in the United States given its importance for global capital markets. However,

Australia retains a substantial degree of monetary policy autonomy by virtue of its floating

exchange rate. In other words, a change in policy rates elsewhere need not mechanically feed

through to Australian interest rates. While Australian banks raise significant amounts of

funding in offshore markets, they are able to insulate themselves – and by extension

Australian borrowers – from changes in interest rates in other jurisdictions.

Just before delving into the details, some context is in order. First, Australian banks have long

borrowed in wholesale markets, including those offshore. However, they do so much less than used

to be the case (Graph 1).[1]

For a number of reasons, domestically sourced deposits have become an increasingly large share of

overall funding for banks.[2]

Graph 1

Second, to the extent that Australian banks have continued to tap offshore wholesale markets, it

is worth reflecting on some of the characteristics of this borrowing. For instance, some

banking sectors around the world borrow in US dollars in order to fund their portfolios of US

dollar assets.[3] This

can leave them vulnerable to intermittent spikes in US interest rates. However, this is

generally not the case for Australian banks. Rather, a good deal of the borrowing by Australian

banks in US dollars reflects the choice of the banks to diversify their funding base in what are

deep, liquid capital markets. By implication, if the costs in the offshore US dollar funding

market increased noticeably relative to the home market, then Australian banks can pursue other

options. They might opt to issue a little less in the US market for a time, switching to other

markets or even issuing less offshore. They are not ‘forced’ to acquire US dollars

at any price, as some other banks may be. Another important feature of this offshore funding, as

I will address in detail in a moment, is that the banks are not exposed to exchange rate risks

as they hedge their borrowings denominated in foreign currencies.

Independence – It’s an Australian Dollar Thing

As you are well aware, the US Federal Reserve has been raising its policy rate in recent years,

and interest rates in the United States are now higher than in Australia. These developments

reflect differences in spare capacity and inflation: unemployment in the United States is at

very low levels, inflation is at the Fed’s target and inflationary pressures appear to be

building. Since August 2016 – the last time the Reserve Bank changed its cash rate

target – the Federal Reserve has raised its policy rate seven times, by 175 basis points

in total (Graph 2). Yet while Australian banks raise around 15 per cent of their

funding in US dollars, interest rates paid by Australian borrowers since then have been little

changed.

Graph 2

How is it that interest rates for Australian borrowers have been so stable, despite Australian

banks having borrowed some US$500 billion in the US capital markets, in US dollars, paying US

dollar interest rates? The answer lies in the hedging practices of the Australian financial

sector. As I’ll demonstrate, Australian banks use hedging markets to convert their US

interest rate obligations into Australian ones.

The Australian banks fund their Australian dollar assets via a number of different sources. Some

of their funds are obtained in US dollars from US wholesale markets. In order to extend these

USD funds to Australian residents, they convert the US dollars they have borrowed into

Australian dollars soon after the securities are issued in the US. On the surface it would

appear that such transactions could give rise to substantial foreign exchange and interest rate

risks for Australian banks given that:

the banks must repay the principal amount of the security at maturity in US dollars. So an

appreciation of the US dollar increases the cost of repaying the loan in Australian dollar

terms; and

the banks must meet their periodic coupon (interest) payments in US dollars, which are tied to

US interest rates (either immediately if the security has a floating interest rate, or when

the security matures and is re-financed). So a rise in US interest rates (or an appreciation

of the US dollar) would increase interest costs for Australian banks that extend loans to

Australian borrowers.

However, it is standard practice for Australian banks to eliminate, or at least substantially

reduce, these risks. They can do this using a derivative instrument known as a cross-currency

basis swap. Such instruments are – when used appropriately – a relatively

cost effective way of transferring risks to parties with the appetite and capacity to bear them.

Simply put, cross-currency basis swaps allow parties to ‘swap’ interest rate streams

in one currency for another. They consist of three components (Figure 1):

first, the Australian bank raises US dollars in the US wholesale markets. Next, the

Australian bank and its swap counterparty exchange principal amounts at current spot

exchange rates; that is, the Australian bank ‘swaps’ the US dollars it has just

borrowed and receives Australian dollars in return. It can then extend Australian dollar

loans to Australian borrowers;

over the life of the swap, the Australian bank and its swap counterparty exchange a stream

of interest payments in one currency for a stream of interest receipts in the other. In this

case, the Australian bank pays an Australian dollar interest rate to the swap counterparty

and receives a US dollar interest rate in return. The Australian bank can use the interest

payments from Australian borrowers to meet the interest payments to the swap counterparty,

and it can pass the interest received from the swap counterparty onto its bondholders;

At maturity of the swap, the Australian bank and its swap counterparty re-exchange principal

amounts at the original exchange rate. The Australian bank can then repay its bond

holders.[4]

In effect, the Australian bank has converted its US dollar, US interest rate obligations into

Australian dollar, Australian interest rate obligations.

Figure 1

An analogy related to housing can help to further the intuition here. Imagine a

Bloomberg employee who owns an apartment in New York but has accepted a temporary job in Sydney.

She fully expects to return to New York and wishes to keep her property, and she does not wish

to purchase a property in Sydney. The obvious solution here is for her to receive rent on her

New York property and use it to pay her US dollar mortgage. Meanwhile, she can rent an apartment

in Sydney using her Australian dollar income. In other words, our relocating worker can

temporarily swap one asset for another. As a result, she can reduce the risks associated with

servicing a US mortgage with an Australian dollar income.

As I mentioned earlier, it is common practice for Australian banks to hedge their foreign

currency borrowings with derivatives to insulate themselves and their Australian borrowers from

fluctuations in foreign exchange rates and interest rates. The most recent survey of hedging

practices showed that around 85 per cent of banks’ foreign currency liabilities

were hedged (Graph 3). Also, the maturities of the derivatives used were well matched to

the maturities of the underlying debt securities.[5]

This means that banks were not exposed to foreign currency or foreign interest rate risk for the

life of their underlying exposures. By matching maturities, banks also avoided the risk that they

might not be able to obtain replacement derivatives at some point in the future (so called

roll-over risk).

Graph 3

For the very small share of liabilities that are not hedged with derivatives, there is almost

always an offsetting high quality liquid asset denominated in the same foreign currency of a

similar maturity, such as US Treasury Securities or deposits at the US Federal Reserve. Taken

together, these derivative hedges and natural hedges mean than Australian banks have only a very

small net foreign currency and foreign interest rate exposure overall (Graph 4).

Graph 4

So who is bearing the risk?

Despite Australia’s external net debt position,

in net terms Australian residents have passed on – for a cost, as we shall see – key

risks associated with their foreign currency liabilities to foreign residents. Australian

residents have found enough non-residents willing to lend them Australian dollars and to receive

an Australian interest rate to extinguish their foreign currency liabilities. As a result,

Australians are net owners of foreign currency assets, not borrowers.[6] Collectively,

Australians have used hedging markets and natural hedges to (more than) eliminate their

exchange-rate exposures associated with raising funds in offshore markets.

Australians’ ability to find non-residents willing to assume Australian dollar and Australian

interest rate risks is a reflection of the willingness of non-residents to invest in Australian

dollar assets. This in turn reflects Australia’s status as a country that has long had strong

and credible institutions, a high credit rating and mature and liquid capital markets. The

willingness of these non-resident counterparties to assume these risks via a direct exposure to

Australia’s banking system – sometimes for as long as thirty years – reflects the fact that

Australia’s banks are well-capitalised and maintain high credit ratings. In short, Australians

have found a source of finance unavailable domestically (at as reasonable a price), and

non-residents have found an asset that suits their portfolio needs.

Since there are no free lunches in financial markets, there is the question of the cost for

Australian banks to cover these arrangements. One part of this cost is known as the basis.

An imperfect world

Some swap counterparties have an inherent reason to enter into

swap transactions with Australian banks. In other words, such exposures actually help them to

manage their own risks. Non-residents that issue Australian dollar debt – in the so called

Kangaroo bond market – are a case in point. These issuers raise Australian dollars to fund

foreign currency assets they hold outside of Australia. This makes them natural counterparts to

Australian banks wanting to hedge their foreign currency exposures. Similarly, Australian

residents invest in offshore assets. To the extent that they want to hedge the associated

exchange rate exposures, they too would be natural counterparties for the Australian banks.

However, it turns out that these natural counterparties do not have sufficient hedging needs to

meet all of the Australian dollar demands of the Australian banks. So in order to induce a

sufficient supply of Australian dollars into the foreign exchange swap market, Australian banks

pay an additional premium to their swap counterparts on top of the Australian dollar interest

rate. This premium, or hedging cost, is known as the basis. Simply put, the basis is the price

that induces sufficient supply to clear the foreign exchange swap market.[7]

Since the start of the decade, the basis has oscillated around 20 basis points per annum (Graph 5).

Typically, though not always, the longer a bank wishes to borrow Australian dollars, the higher

the premium it must pay over the Australian dollar interest rate.

Graph 5

You may be wondering why Australian banks are willing to pay this premium; why don’t they

instead only borrow Australian dollars in the Australian capital markets to meet their financing

needs? In addition to the prudent desire to have a diversified funding base as I mentioned

earlier, the short answer is that it may not be cost-effective to raise all their funding at

home. What tends to happen is that banks – to the extent possible – seek to equalise

the marginal cost of each unit of funding from different sources. If they were to obtain all of

their funding at home, that would be likely to increase the cost of those funds relative to

funds sourced from offshore. So the all-in-cost of the marginal Australian dollar from domestic

sources will tend to be about the same as the marginal dollar obtained from offshore.

Astute students of finance will also wonder why the basis is not arbitraged away.[8]

The answer is that structural changes in financial markets have widened the scope for market

prices to deviate from values that might prevail in a world of no ‘frictions’. This

is consistent with the concept of ‘limits to arbitrage’ (which the academic

community only started to re-engage with in the past couple of decades). Arbitrage typically

requires the arbitrageur to enlarge their balance sheet and incur credit, mark-to-market and/or

liquidity risk. As Claudio Borio of the BIS has noted: balance sheet space is rented, not free.

And the cost of that rent has gone up.[9]

What about financial conditions more generally?

None of this is to suggest that

monetary policy settings in the United States (and elsewhere for that matter) have no impact on

financial conditions here in Australia. But the link is neither direct nor mechanical.

The primary channel through which foreign interest rates influence Australian conditions is

through the exchange rate. An increase is policy rates elsewhere will, all else equal, tend to

put downward pressure on the Australian dollar, because capital is likely to be attracted to the

higher rates of return available abroad. A depreciation of the Australian dollar in turn will

tend to enhance the competitiveness of our exporters, including those services priced in

Australian dollars like tourism and education. Through various channels, exchange rate

depreciation can also loosen financial conditions in Australia, which is not always the case in

other countries, particularly those for which inflation expectations are not well anchored and

where there are substantial foreign currency borrowings that are unhedged.[10]

Foreign monetary policy settings, particularly those in the United States, can also affect global

risk premia. We are now approaching a period when US monetary policy is moving to a neutral

stance. This follows a lengthy period of very easy monetary conditions, which may have

encouraged investors to ‘search for yield’ to maintain nominal portfolio returns in

an environment of low interest rates. The expectation of low and stable policy rates and

inflation outcomes in turn compressed risk premia across a range of asset classes. In the period

ahead, it seems plausible that term and credit risk premia will rise, which will increase costs

for all borrowers, Australian banks included.

The board of IOOF Holdings has today announced that IOOF managing director, Christopher Kelaher and chairman, George Venardos, have agreed to step aside from their respective positions effective immediately, pending resolution of proceedings brought by the Australian Prudential Regulation Authority (APRA) and announced last Friday, 7 December.

Mr Renato Mota, currently group general manager – wealth management,

has been appointed acting chief executive officer and Mr Allan

Griffiths, a current non-executive director of IFL, is acting chairman.

Both Mr Kelaher and Mr Venardos will be on leave while they focus on

defending the actions brought against them by APRA.

Chief financial officer David Coulter, company secretary Paul Vine

and general counsel Gary Riordan will remain in their positions, however

will have no responsibilities in relation to the management of the IOOF

trustee companies and will have no engagement at all with APRA during

this period, including in relation to the matters the subject of APRA’s

announcement of Friday 7 December.

“We maintain our position that the allegations made by APRA are

misconceived, and will be vigorously defended. The Board believes that,

in the interests of good governance, it is appropriate that Chris and

George step aside from their positions. The Board will also commence a

search for an additional non-executive Director,” Acting chairman, Allan

Griffiths said

“We acknowledge the seriousness of these allegations. We have a

responsibility to our superannuation members, shareholders, advisers,

employees and the wider community, to take decisive action.

“We are entirely focused on addressing the governance issues in the

interests of all stakeholders and will do so in an orderly manner.

“I will personally lead our review of the situation and, alongside

acting CEO Renato Mota, will work cooperatively with APRA to continue to

implement previously agreed initiatives. Many of these actions are

already complete.”

IOOF posted an underlying net profit after tax result in financial

year 2018 of $191.4 million, up 13 per cent on the financial year 2017

result.

“These results have been delivered by our unwavering commitment to

our clients, driven by our talented people and a recognition of the

importance of advice. We remain committed to the ANZ transaction and we

are working cooperatively with ANZ as they consider their position,” Mr

Griffiths said.

The prudential regulator is seeking to impose additional licence

conditions and issue directions to APRA-regulated entities in the IOOF

group.

The proceedings in the Federal Court seek to disqualify five

individuals that were responsible persons at IOOF Investment Management

Limited (IIML) and Questor Financial Services.

The proceedings are also seeking a court declaration that IIML and Questor breached the SIS Act.

The announcement drove ANZ to rethink the sale of its wealth business

to IOOF. ANZ released an update on its sale following APRA’s move to

disqualify IOOF individuals and its move to apply licence restrictions

on the group.

ANZs deputy chief executive Alexis George said ANZ would reassess the

sale of its OnePath Pensions and Investments business to IOOF.

“Given the significance of APRA’s action, we will assess the various

options available to us while we seek urgent information from both IOOF

and APRA.

“The work to separate Pensions and Investments from our Life

Insurance business continues. There is a framework available to complete

the Zurich transaction that does not involve IOOF,” he said.

The Australian Prudential Regulation Authority (APRA) has announced a number of actions against IOOF entities, directors and executives for failing to act in the best interests of superannuation members.

APRA has commenced disqualification proceedings and is seeking to impose additional licence conditions and issue directions to APRA-regulated entities in the IOOF group.

APRA has issued a show cause notice setting out APRA’s intention to direct IOOF Investment Management Limited (IIML) to comply with its Registrable Superannuation Entity (RSE) Licence and impose additional conditions on the licenses of IIML, Australian Executor Trustees Limited (AET) and IOOF Ltd (IL). These entities have 14 days to respond to this notice.

The proposed conditions and directions to comply with conditions seek to achieve significant changes to the identification and management of conflicts of interest by IIML, AET and IL and facilitate APRA’s ability to take further enforcement action should this not occur. The proposed additional conditions on the licences of IIML, AET and IL are based on issues and concerns raised by APRA since 2015 relating to the entities’ organisational structure, governance and conflicts management frameworks, and require the entities to address these within specified timeframes. The proposed directions for IIML relate to an independent report issued by Ernst & Young, the findings of which provide a reasonable basis to conclude that IIML has breached section 52 of the Superannuation Industry (Supervision) Act 1993 (SIS Act), Prudential Standard SPS 520: Fit and Proper and Prudential Standard SPS 521: Conflicts of Interest.

APRA has also commenced proceedings in the Federal Court of Australia to seek the disqualification of five individuals that, at relevant times, were responsible persons of IIML and Questor Financial Services Limited (Questor). The proceedings also seek a court declaration that IIML and Questor (which at the material times were RSE Licensees owned by IOOF Holdings Limited) breached the SIS Act.

The individuals included in the disqualification proceedings are Managing Director Chris Kelaher, Chairperson George Venardos, Chief Financial Officer David Coulter, General Manager – Legal, Risk and Compliance and Company Secretary Paul Vine, and General Counsel Gary Riordan.

The Concise Statement seeks disqualification orders and declarations in relation to breaches of sections 52 and 55 of the SIS Act and Prudential Standards, and associated conduct. As outlined in the Concise Statement, APRA considers that IIML, Questor and the relevant individuals did not appropriately acknowledge and address issues concerning conflicts of interest raised by APRA from 2015 to date. In particular, APRA identified that on three separate occasions in 2015, Questor and IIML contravened the SIS Act by deciding to differentially compensate superannuation beneficiaries and other non-superannuation investors for losses caused by Questor, IIML or their service providers, with superannuation beneficiaries being compensated from their own reserve funds rather than the trustees’ own funds or third-party compensation.

If successful, the disqualification proceedings would prohibit the above individuals from being or acting as a responsible person of a trustee of a superannuation entity.

APRA Deputy Chair Helen Rowell said APRA had sought to resolve its concerns with IOOF over several years but considered it was necessary to take stronger action after concluding the company was not making adequate progress, or likely to do so in an acceptable period of time.

“APRA’s efforts to resolve its concerns with IOOF have been frustrated by a disappointing level of acceptance and responsiveness to the issues raised by APRA, which is not the behaviour we expect from an APRA-regulated entity,” Mrs Rowell said.

“The actions we are now taking are aimed at achieving enduring change to ensure that the trustees of the superannuation funds operated by IOOF fully meet their obligation to put the interests of members ahead of all other interests.

“Furthermore, the individuals included in the proceedings have shown a lack of understanding of their personal and trustee obligations under the SIS Act and at law, and a lack of contrition in relation to the breaches of the SIS Act identified by APRA.”

The Central Bank has finally released details of the landmark prosecution that involved two of its subsidiary companies involved in bribing overseas officials for note-printing contracts, via InvestorDaily.

Following a decision by the Supreme Court of Victoria this week, the Reserve Bank of Australia (RBA) is able to disclose that in late 2011, its subsidiaries – Note Printing Australia (NPA) and Securency – entered pleas of guilty to charges of conspiracy to bribe foreign officials in connection with banknote-related business.

The offences were committed over the period from December 1999 to September 2004.

The RBA and the companies were not permitted to disclose these pleas prior to today due to suppression orders, which have now been lifted. The orders were not sought by the RBA or the companies.

In a statement this week, the RBA said the boards of NPA and Securency decided to enter guilty pleas at the earliest possible time rather than to defend the charges, reflecting an acceptance of responsibility and genuine remorse.

“The decisions to plead guilty were based on material that became available to the boards after allegations about Securency had been referred to the Australian Federal Police (AFP) and followed extensive legal advice. The decisions also took into account the public interest in avoiding what was expected to be a costly and lengthy court process,” the central bank said.

No evidence of knowledge or involvement by officers of the RBA, or the non-executive members of either board appointed by the RBA, has emerged in any of the relevant legal proceedings or otherwise.

“The Reserve Bank strongly condemns corrupt and unethical behaviour,” Reserve Bank governor Philip Lowe said.

“The RBA has been unable to talk about this matter publicly until today, although the guilty pleas were entered in 2011. The RBA accepts there were shortcomings in its oversight of these companies, and changes to controls and governance have been made to ensure that a situation like this cannot happen again.”

In 2011, the Reserve Bank Board commissioned a thorough external review of the RBA oversight of the companies. The RBA oversaw a comprehensive strengthening of governance arrangements and business practices in the two companies.

In early 2013, the RBA sold its interest in Securency, having ensured that all the compliance issues of which the RBA was aware had been addressed.

With the lifting of the suppression orders, the RBA is now also able to disclose that the companies paid substantial penalties as a result of the court proceedings.

NPA paid fines totalling $450,000 and a pecuniary penalty under the Proceeds of Crime Act 2002 of $1,856,710. Securency paid fines totalling $480,000 and a pecuniary penalty under the Proceeds of Crime Act of $19,809,772.

Since the companies entered their pleas, four former employees of Securency have pleaded guilty to charges of conspiring to bribe and/or false accounting. Charges against four former employees of NPA were permanently stayed on the basis that continued prosecution of these individuals would bring the administration of justice into disrepute.

The use of the Household Expenditure Measure to assess serviceability was initially less common for broker-originated loans, but such is no longer the case, ANZ chief Shayne Elliott has revealed, via The Adviser.

Appearing before the financial services royal commission in its seventh and final round of hearings, ANZ CEO Shayne Elliott was questioned over the bank’s use of the Household Expenditure Measure (HEM) to assess home loan applications.

In round one of the commission’s hearings, ANZ general manager of home loans and retail lending practices William Ranken admitted that the bank did not further investigate a borrower’s capacity to service a broker-originated mortgage.

In his interim report, Commissioner Kenneth Hayne alleged that using HEM as the default measure of household expenditure “does not constitute any verification of a borrower’s expenditure”, adding that “much more often than not, it will mask the fact that no sufficient inquiry has been made about the borrower’s financial position”.

Counsel assisting the commission Rowena Orr QC pointed to a review of ANZ’s HEM use by consultancy firm KPMG upon the Australian Prudential Regulation Authority’s (APRA) request.

The KPMG review found that 73 per cent of ANZ’s loan assessments defaulted to the HEM benchmark.

Mr Elliott noted that since the review, ANZ has taken steps to reduce its reliance on HEM, with the CEO stating that the bank plans to reduce the use of HEM for loan assessments to a third of its overall applications.

When asked if there was a disparity between the use of HEM through the broker channel and branch network, Mr Elliott revealed that prior to the bank’s move to reduce its reliance on the benchmark, the use of HEM was less prevalent for broker-originated loans.

“Perhaps surprisingly, when we did the review, when we were talking about the mid-70s [percentage], the branch channel actually had slightly higher usage or dependency on HEM as opposed to the broker [channel].

“[That] actually is counterintuitive,” he added. “I think it would be reasonable to expect that if [ANZ] knows these customers, one might expect to use HEM less.”

Mr Elliott attributed the disparity to the higher proportion of “top-ups” for existing loans through the branch network, noting that ANZ’s home loan managers would be more likely to “shortcut the process” through the use of the HEM benchmark.

However, the CEO said that according to the latest data that he’s reviewed, the branch network’s reliance on HEM is lower than in the broker channel.

“[It’s] changing as we speak,” he said.

“As in the latest data I saw, the branch network is now lower in terms of its usage or reliance on HEM versus the broker channel. And that’s because we are in, if you will, greater control of that process in terms of our ability to coach and send signals to our branch network.”

However, he added that the use of the benchmark for broker-originated loans is “coming down rapidly” in line with the bank’s overall commitment to reduce its reliance on HEM.

Flat-fee ‘credible alternative’ to commission-based model

Further, as reported on The Adviser’s sister publication, Mortgage Business, Mr Elliott told the commission that a flat fee paid by lenders to brokers is a “credible alternative” to the existing commission-based remuneration model.

When asked by Ms Orr about his view on broker remuneration, Mr Elliott said that a flat fee paid by lenders is a “credible alternative” to the current commission-based model.

In a witness statement provided to the commission, Mr Elliott said that there’s “merit in considering alternative models for broker remuneration to ensure that the current model remains appropriate and better than any alternative”.

Reflecting on his witness statement, Ms Orr asked: “Is that because you accept that there’s an inherent risk that incentives might cause brokers to behave in ways that lead to poor customer outcomes?”

The ANZ CEO replied: “There is always that risk. [The] term incentive is to incent behaviour. Therefore, it can be misused or it can cause unintended outcomes if the broker is apt to be led by their own financial reward.”

Mr Elliott acknowledged that “no system’s perfect” and that a “fixed fee is also capable of being misused and leading to unintended outcomes”.

However, he added: “It is just my observation that there is at least some data on this from other markets, most notably in northern Europe. It seems a model that’s worth looking at.”

Mr Elliott continued: “I’m not suggesting it’s necessarily an improvement. It just feels like a credible alternative.”

The ANZ CEO compared a flat-fee model in the broking industry to the financial planning industry.

“The service is the work you are paying for, and perhaps the fee should not necessarily be tied to the outcome.

“I think that’s not an unreasonable proposition.”

However, the ANZ chief noted the negative implications of a flat-fee model, stating that with lenders ultimately passing on costs to consumers, the model would be a “major advantage” to higher income borrowers.

“The difficulty with the fixed fee, if I may, is it essentially is of major advantage to people who can afford and have the financial position to undertake large mortgages,” he said.

“[A] subsidy would be paid by those least able to afford it, and it runs the risk of making broking a privilege for the wealthy.”

There’s ‘merit’ in a fees-for-service model

Ms Orr also asked Mr Elliott for his view regarding a consumer-pays or “fees-for-service” model.

The QC asked whether such a model would address some of the concerns expressed by Mr Elliott about a flat-fee model.

Mr Elliott said that if a fee is paid by borrowers, it would be “uneconomic” for people seeking a loan to visit a broker, repeating that using a broker would become a “service for the wealthy”.

Ms Orr then asked the CEO for his thoughts on a Netherlands-style fees-for-service model, supported by Commonwealth Bank CEO Matt Comyn, in which both branches and brokers would charge a fee for loan origination.

Mr Elliott replied: “There’s merit in looking at that, [but] it still is an imposition of cost that would otherwise not have been there.”

Mr Elliott added that there would be “new costs” associated with a Netherlands-style model, noting that borrowers seeking a “top-up” for an existing loan would need to pay an additional fee.

In response, Ms Orr alleged that under the current commission-based model, costs are also “filtered back down” to consumers.

To which Mr Elliott replied: “In general terms, yes. Not necessarily in direct terms like that fee I charge you as a borrower, [and] at ANZ, we have, for some time, disclosed [commissions]. So, when you do get a mortgage through a broker, we do advise the customer what we have paid that broker. So, it is disclosed to them.”

The ANZ CEO also said that under a fees-for-service model, consumers could be incentivised to take out larger loans to avoid paying a fee if they wish to top up their loan.

Conversely, Mr Elliott added that if a flat fee is paid by lenders, some brokers may be incentivised to encourage clients to borrow less and “come back for more top-ups so that they get more fees”.

Mr Elliott reported that top-ups on existing loans make up 30 per cent ($17 billion) of total volume settled by ANZ.

The ANZ chief also told Ms Orr that he doesn’t believe a move to introduce an alternative remuneration model would be “hugely successful” without regulatory intervention.