The public hearings which the Productivity Commission has been running in relationship to Competition in Financial Services covered a wide range of issues.

One which has surfaced is the Lenders Mortgage Insurance (LMI) sector. With 20% of borrowing households required to take LMI, and just two external providers (Genworth and QBE LMI), the Commission has explored the dynamics of the industry. They called it “an unusual market”, where there is little competitive pricing nor competition in its traditional form. Is the market for LMI functioning they asked? Could consumers effectively be paying twice?

On one hand, potential borrowers are required to pay a premium for insurance which protects the bank above a certain loan to value hurdle. That cost is often added to the loan taken, and the prospective borrower has no ability to seek alternatives from a pricing point of view.

Banks who use external LMI’s appear not to tender competitively.

On the other hand, ANZ, for example has an internal LMI equivalent, and said it would be concerned about the concentration risk of placing insurance with just one of the two external players, as the bank has more ability to spread the risks. The Commission probed into whether pricing of loans might be better in this case, though but the bank said there were many other factors driving pricing.

All highly relevant given the recent APRA suggestion that IRB banks might get benefit from lower capital for LMI’s loans, whereas today there is little capital benefit.

This will be an interesting discussion to watch as it develops towards the release of the final report.

They had already noted that consumers should expect to receive a refund on their premium if they they repay the loan.

The Bank of Queensland has told the Productivity Commission that greater visibility of mortgage rates could make the mortgage broker proposition less compelling for consumers.

Appearing before the Productivity Commission, the bank’s CFO, Anthony Rose, said that “greater transparency [could] see a diminished utilisation of the broker space”.

“We have seen that the broker market has certainly been beneficial in allowing the non-major banks compete in the mortgage space,” Mr Rose said.

Commission chairman Peter Harris acknowledged that smaller banks have been “assisted by the broker revolution and have saved the need to occupy branch space in [more] locations”.

“You’re saying, therefore, if the pricing impact did encourage more people to look for a branch, then the entities with the biggest branch network are advantaged by that,” Mr Harris said.

When asked whether the Bank of Queensland, which receives 25 per cent of its home loans through the third-party channel, has had to re-strategise in response to vertical integration, Mr Rose admitted that the bank has been monitoring aggregator ownership structures with concern.

“We thought that those that own aggregator networks should actually be required to publish the degree of flow relative to their market share for the public interest to understand whether is there anything to see here or not,” the CFO said.

“To be honest, the information that you’ve provided in your report is new information to us as well but doesn’t surprise us. It’s hard for us to access that information as well.”

Representatives from both the PC and the Bank of Queensland agreed that the lack of publicly available data has made it difficult to measure the actual impact aggregator ownership has had on the flow of mortgages in Australia, though Mr Harris has previously suggested that bank-owned aggregators control about 70 per cent of the mortgage broking market.

As such, the Bank of Queensland supports the PC’s proposed duty of care obligations, which would require the Australian Securities and Investments Commission to impose a clear legal duty on lender-owned mortgage aggregators to act in the best interests of the consumer.

“We do think that’s important because the degree to which major banks are getting flow of business over and above their natural market share is, in effect, market access that would have been available to the non-big four that is no longer available to us for whatever reasons that are driving that outcome,” Mr Rose said.

“It does appear that there is quite a trend towards an over-allocation of flow back into the proprietary products of the owned business, which I think is addressed by putting that duty of care obligation in.”

The royal banking commission has rejected CBA’s request not to disclose parts of evidence regarding the bank’s CreditCard Plus product.

The commission only agreed to keep confidential the name and policy number of the CBA consumer who made a complaint about the product.

In a note released last Friday, Commissioner Kenneth Hayne said CBA applied for a non-publication direction under s 6D(3) section of the Royal Commissions Act regarding parts of a draft statement to be given by a CBA employee about CreditCard Plus.

The evidence refers to CBA’s communications with ASIC regarding CreditCard Plus, an add-on insurance policy sold with credit cards, personal loans, home loans, and car loans. CBA said in its non-publication application that those communications should be treated as confidential.

ASIC announced in August 2017 that CBA would refund over 65,000 customers about $10m after selling them the consumer credit insurance product. The regulator said the product was unsuitable for those customers.

Details of the remediation program are among those CBA asked not to be published.

“General assertions are made that certain kinds of communication, such as, for example, communications between CBA and regulators, are confidential. Why the particular communications should be treated in this way is not explained,” said Hayne.

He added that arguments framed in such a way are “unhelpful and unpersuasive”.

“Absent ASIC joining in an application for a non-publication direction, I do not accept that a non-publication direction should be made in respect of any of those parts of the draft statement.”

Hayne said it was also necessary to bear in mind that CBA acknowledged in its first submission to the commission that the conduct concerned in the evidence fell short of community standards and expectations.

“CBA identified no damage to itself or any other person that would follow from publication of the material,” he said in closing.

In deciding to detail and publish its reasons for the decision, the commission seeks to provide “guidance” to others involved in its inquiry.

“The application made by CBA in respect of this witness statement does warrant a more elaborate statement of reasons and warrant publication of those reasons for the guidance of others who may seek a direction under s 6D(3),” said Hayne.

The royal commission is holding its first round of hearings from 13 to 23 March 2018 focusing on consumer lending.

How far will home prices fall? Welcome to the Property Imperative weekly to 3rd March 2018.

Yet another big big week in property and finance for us to review today. Watch the video or read the transcript.

We start with the latest home price data from CoreLogic. Prices continue to soften. On an annual basis, prices are down 0.5% in Sydney, 2.7% in Perth and 7.4% in Darwin. They were higher over the year in Melbourne, up 6.9%, Brisbane 1.8%, Adelaide 2.2% and Hobart a massive 13.1%. But be beware, these are average figures, and there are considerable variations across locations within regions and across property types. The bigger falls are being seen at the top end of the market.

Over the three months to February, Adelaide was up 0.1% and Hobart 3.2%. These were the only capital cities in which values rose. Sydney, which has been the strongest market for value growth over recent years, saw the largest fall in values over the three-month period, down -2.4%. Sydney was followed by Darwin, which has been persistently weak over recent years, and saw values fall by a further -2.0% over the quarter.

Finally, CoreLogic says month-on-month falls were generally mild but broad based. Over the month, values fell across every capital city except Hobart (+0.7%) and Adelaide (steady), with the largest monthly decline recorded across Darwin (-0.9%) and Sydney (-0.6%). Values were lower in Melbourne (-0.1%), Brisbane (-0.1%), Perth (-0.2%), and Canberra (-0.3%).

The reason for the falls are pretty plain to see. Demand is substantially off, especially from investors, as mortgage underwriting standards are tightening. So it was interesting to hear APRA chairman Wayne Byres’s testimony in front of the Senate Economics Legislation Committee. I discussed this with Ross Greenwood on 2GB. During the session he said that the 10% cap on banks’ lending to housing investors imposed in December 2014 was “probably reaching the end of its useful life” as lending standards have improved. Essentially it had become redundant. But the other policy, a limit of more than 30% of lending interest only will stay in place. This more recent additional intervention, dating from March 2017, will stay for now, despite it being a temporary measure. The 30% cap is based on the flow of new lending in a particular quarter, relative to the total flow of new lending in that quarter. This all points to tighter mortgage lending standards ahead, but still does not address the risks in the back book. The mortgage underwriting screws are much tighter now – our surveys show that about a quarter or people seeking a mortgage now cannot get one due to the newly imposed limits on income, expenses and serviceability.

During the sessions, Senator Lee Rhiannon asked APRA about mortgage fraud. This was to my mind the most significant part.

Yet even now, more than 10% of new loans are being funded at a loan to income of more than 6 times. And whilst the volume of interest only loans has fallen to 20% of new loans, well below the 30% limit, it seems small ADI’s are lending faster than the majors. And we know the non-banks are going gang busters.

Now the HIA said their Housing Affordability Index saw a small improvement of 0.2 per cent during the December 2017 quarter indicating that affordability challenges have eased thanks to softer home prices in Sydney where they are now slightly lower than they were a year ago. This makes home purchase a little more accessible, particularly for First Home Buyers they said. But they failed to mention the now tighter lending standards which more than negates any small improvement in their index.

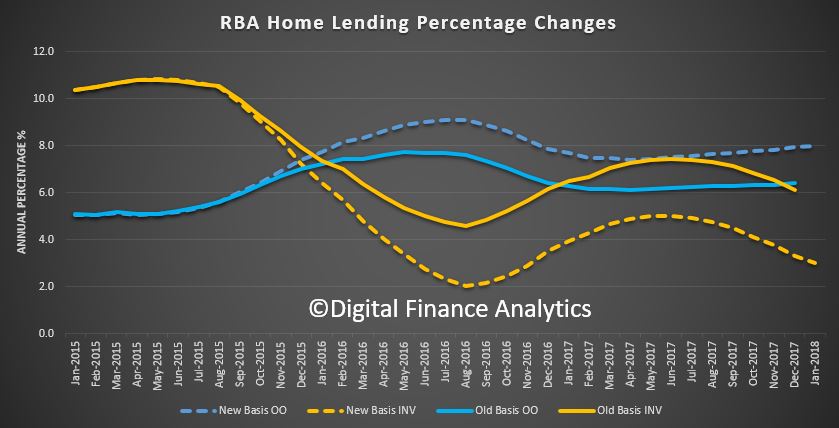

The impact of this tightening came through in the latest data on housing finance from both the RBA and APRA. I made a separate video on this if you want the gory details. The RBA said that in January owner occupied lending rose 0.6%, or 8% over the past year to $1.14 trillion. Investment lending rose 0.2% or 3% over the past year to $587 billion and comprises 34% of all housing lending. They changed the way they report the data this month. It changes the trend reporting significantly. Since mid-2015 the bank has been writing back perceived loan reclassifications which pushed the investor loans higher and the owner occupied loans lower. They have now reversed this policy, so the flow of investment loans is lower (and more in line with the data from APRA on bank portfolios). Investor loans are suddenly 2% lower. Magically! Once again, this highlights the rubbery nature of the data on lending in Australia. What with data problems in the banks, and at the RBA, we really do not have a good chart and compass. It just happens to be the biggest threat to financial stability but never mind.

The latest APRA Monthly Banking Statistics to January 2018 tells an interesting tale. Total loans from ADI’s rose by $6.1 billion in the month, up 0.4%. Within that loans for owner occupation rose 0.57%, up $5.96 billion to $1.05 trillion, while loans for investment purposes rose 0.04% or $210 million. 34.4% of loans in the portfolio are for investment purposes. So the rotation away from investment loans continues, and overall lending momentum is slowing a little (but still represents an annual growth rate of nearly 5%, still well above inflation or income at 1.9%!). Looking at the lender portfolio, we see some significant divergence in strategy. Westpac is still driving investment loans the hardest, while CBA and ANZ portfolios have falling in total value, with lower new acquisitions and switching. Bank of Queensland and Macquarie are also lifting investment lending.

Now searching questions are being asked about Lax Mortgage Lending, and the risks the banks are sitting on at the moment. While better lending controls will help ahead, we have a significant problem now, with many households facing financial difficulty. First there is the issue of basic cash flow, as incomes remain contained, costs of living rise, and mortgage payments still need to be met. We estimate 51,500 households risk default in the year ahead, a small but growing problem. We will release the February mortgage stress data on Monday, so look out for that.

Then there is the question of banks and brokers not doing sufficient due diligence on loan applications. This is something the Royal Commission will be looking at in the next couple of weeks. We worked with the ABC on a story, which aired this week, looking at the issues around poor lending. Its complex of course, because borrowers have to take some responsibility for the applications they made for credit, and need to be truthful. But both brokers and lenders have obligations to make sufficient inquiry into the applicant’s circumstances to ensure the loan is “not unsuitable” – which is nothing to do with the “best” mortgage by the way, it’s a much lower hurdle. But if a loan were deemed to be unsuitable, the courts may change the terms of the loan, or cancel the loan, meaning a borrower could leave a property without debt. An upcoming court case may clarify the law. But in the ABC piece, Brian Johnston, one of the best analysts in the business said this means it moves from being the borrowers problem to being the banks problem!

This also touches on the role of mortgage brokers, and whether their commission based remuneration might influence their loan recommendations, to the detriment of their customers, which is more than half the market. This is something which both ASIC and the Productivity Commission have been highlighting. Speaking at a CEDA event, Productivity Commission chairman Peter Harris said more than $2.4bn is now paid annually for mortgage broker services. The commission’s draft report released in early February says that based on ASIC’s findings, lenders pay brokers an upfront commission of $2,289 (0.62%) and a trail commission of $665 (0.18%) a year on an average new home loan of $369,000. He zeroed in on trailing commissions – which he said are worth $1bn per annum – and questioned their relevance.

The Banking Royal Commission says the first round of public hearings will be held in Melbourne at the Owen Dixon Commonwealth Law Courts Building at 305 William Street from Tuesday 13 March to Friday 23 March. They listed the range of matters they are exploring, from mortgages, brokers, cards, car finance, add-on insurance and account administration, with reference to specific banks, including NAB, CBA, ANZ, Westpac, Aussie, and Citi. Responsible lending is the theme.

Talking of mortgage brokers, another question to consider is the ownership relationship between a broker, their aggregator and the Bank. Not only are many brokers effectively directly employed by the big banks, but more have strong associations, these relationships are not adequately disclosed.

The New Daily did a good piece on showing these linkages, most of which are hard to spot. They said that Fans of Married at First Sight and My Kitchen Rules may have noticed over the past few days that popular property website realestate.com.au has started advertising a new product: home loans. But Realestate.com.au Home Loans is not an independent initiative. Far from it. It is a deal between Rupert Murdoch’s News Corp, which owns 61.6 per cent of realestate.com.au, and big-four bank NAB. Last June REA Group, the company behind the realestate.com.au website, signed what it called a “strategic mortgage broking partnership” with NAB. What REA Group is actually doing is piggy-backing on a mortgage broker called Choice Home Loans. In other words, while the branding may be realestate.com.au, the actual mortgage broking firm is Choice Home Loans. And who owns Choice Home Loans? NAB does. If you get conditional approval through realestate.com.au, it will be provided by NAB. However, getting conditional approval with NAB does not commit you to a NAB home loan. First, you could choose a realestate.com.au ‘white label’ loan. This is a loan that on the face of it looks like it is provided by realestate.com.au. But once again appearances are deceptive. REA Group does not have a mortgage lenders’ licence. So while these loans may be branded realestate.com.au, they are actually provided by a nationwide mortgage lender called Advantedge. And who owns Advantedge? NAB does. If you don’t fancy the realestate.com.au home loan, there are other choices. First, there is a range of NAB mortgages. And then, there is a list of mortgages from other providers – more than 30 of them, including big names like Westpac, ANZ, Commonwealth Bank, Macquarie, ING, ME, UBank – the list goes on. Oh, and by the way, that last bank mentioned – UBank – is also owned by NAB. All this highlights the hidden connections and the market power of the big banks. Like I said, these relationships are hard to spot!

Another little reported issue this week was the financial viability of Lenders Mortgage Insurers in Australia, those specialist insurers who cover mortgages over 80% loan to value. QBE Insurance reported their full year 2017 results today and reported a statutory 2017 net loss after tax of $1,249 million, which compares with a net profit after tax of $844 million in the prior year. This is a diverse and complex group, which is now seeking a path to rationalisation. They declared their Asia Pacific result “unacceptable” and said the strategy was to “narrow the focus and simplify back to core” with a focus on the reduction in poor performing segments. This begs the question. What is the status of their Lenders Mortgage Insurance (LMI) business? They reported a higher combined operating ratio consistent with a cyclical slowdown in the Australian mortgage insurance industry, higher claims and a lower cure rate. Very little detail was included in the results, but this aligns with similar experience at Genworth the listed monoline who reported a 26% drop in profit, and provides greater insight into the mortgage sector. Both LMI’s are experiencing similar stresses, with lower premium income, and higher claims. And this before the property market really slows, or interest rates rise! Begs the question, how secure are the external LMI’s? Another risk to consider.

Last week’s auction preliminary results from Domain said nationally, so far from the 2,627 properties listed for auction, only 1,794 actually went for sale, and 1,325 properties sold. So the real clearance rate against those listed is 50.4%. Domain though calculates the clearance rate on those going to auction, less withdrawn sales over those sold. This give a higher measure of 68.8% nationally, which is still lower than a year ago. But, we ask, which is the real clearance rate?

Finally, there is a rising chorus demanding that APRA loosen their rules for mortgage lending in the face of slipping home prices. This despite the RBA’s recent comments about the risks in the system, especially relating to investor and interest only loans. But this is unlikely, and in fact more tightening, either by a rate rise, or macroprudential will be needed to contain the risks in the system. The latter is more likely. Some of this will come from the lenders directly. For example, last week ANZ said it will be regarding all interest-only loan renewals as credit critical event requiring full income verification from 5 March. If loans failed this assessment these loans would revert to P&I loans (with of course higher repayment terms). We are already seeing a number of forced switches, or forced sales thanks to the tighter IO rules more generally. We will release updated numbers next week. But, as ANZ has pointed out in a separate note from David Plank, Head of Australian Economics at ANZ; household leverage is still increasing, this despite a moderation in housing credit growth over the past year. Household debt continues to grow faster than disposable income. With household debt being close to double disposable income it will actually require the growth in household debt to slow well below that of income in order for the ratio of household debt to income to stabilise, let alone fall. In fact, he questions whether financial stability has really been improved so far, when interest rates are so very low.

So, nothing we have seen this week changes our view of more, and significant falls in property values ahead as mortgage lending is tightened further. This also shows that it is really credit supply and demand, not property supply and demand which is the critical controller of home price movements. Another reason to revisit the question of negative property gearing in my view.

Investment guru Warren Buffet wasn’t commenting on the Australian mortgage market when he said, “Only when the tide goes out do you discover who has been swimming naked”, but it is no less relevant.

Key points:

42 per cent of home loan customers told banks they had incomes in excess of $500,000 last year

Westpac is the first bank to face ASIC court action over irresponsible lending allegations

Mortgage contracts can be voided if the bank provides credit to someone who cannot afford it

When interest rates start rising and/or if property prices fall, the market’s vulnerabilities will be exposed.

The prospect of higher interest rates is considered a distant threat because inflationary pressures will take time to build.

We also know households are sitting on a mountain of property debt and one false interest rate move by the RBA could trigger a collapse with far-reaching consequences.

That isn’t the only trigger.

Overstated income

The banks’ Achilles heel — irresponsible lending — is shaping up as a major threat to the banks and financial system, depending on the outcome of the banking royal commission and a low-profile battle currently being waged in courts.

“Irresponsible lending is endemic in Australia,” Digital Finance Analytics director Martin North said.

“More than 900,000 households are already in mortgage stress.

“We’re seeing a lot of households who are actually getting loans that are five, six, seven, eight, nine times income and that is astronomically high and in my mind will lead to grief later.”

Even though customers of the big four banks are representative of the Australian population, their claims about the incomes of those customers are not.

“The free and loose lending standards that banks have demonstrated, particularly over the last decade through the use of benchmarking tools and interest only loans, has the potential to be catastrophic for the Australian economy,” Maurice Blackburn lawyer Josh Mennen said.

Financial planning crisis, money laundering scandals, market manipulation … you ain’t seen nothing yet.

The Productivity Commission (PC) had posed the question in its draft report into competition in the Australian financial system of whether consumers should pay service fees, with the aim of finding out if such a model would ensure consumer interests are being served without any conflicting commercial influence.

In a public hearing on Wednesday (28 February), Travis Crouch, divisional CFO for revenue at Bendigo and Adelaide Bank, contended that a “fee-for-service brokerage [would] remove the inherent conflicts involved in a commission-based structure and ensure fees earned are aligned with the value of the service provider”.

The representative explained that the bank relies less on mortgage brokers than other banks, as its primary focus for the last two decades has been on developing a strong branch network.

“We have been focused on the development of a strong branch network primarily since the advent of our community banking model, some 20 years ago, where communities can open a branch of a Bendigo Bank as a franchisee. That remains a reverse enquiry model… We’re not out there selling to a community that you should open a community bank; rather, [the] community comes to us and [says], ‘We would like to open a branch’,” Mr Crouch told the PC in the hearing.

“There is a significant process including feasibility studies [that] they need to go through to show that they could be successful. But we continue to increase our branch footprint primarily through that community bank model.”

Mr Crouch further explained the difference between the organisation’s Adelaide Bank and Bendigo Bank brands, saying: “Our brand that we use in the broker market is the Adelaide Bank brand. The Bendigo Bank brand is our retail offering through our retail and community bank network. The Adelaide Bank brand is effectively an online brand once you take out the mortgage through a mortgage broker.”

Trail “an absurd option”

In response, a PC representative commented that if Adelaide Bank is ultimately an online brand, paying trail commissions must be an “absurd option”.

“For the average loan, $665 per year in perpetuity for an online-based product seems very expensive,” the PC said.

“You presumably have very little choice about that because, as you say, you have to play in the market.”

The Bendigo and Adelaide Bank representative agreed with the comment, drawing back to why the bank believes that a fee-for-service model is “more appropriate”.

Mr Crouch did not, however, deny the importance of brokers, saying that it would be a “brave decision to not participate in that market”, given that “roughly half of Australians [are] choosing to select a mortgage by going to a broker”.

When asked about whether the bank has had to make “either/or” decisions around opening branches in the same location as brokerages, Mr Crouch noted that it has separate strategies for its retail and broker businesses.

“The reality is both are generally competing in the same market, whether that be a geographic market or anything else, and quite often you’ll find one of our branches in the same shopping strip as an outlet of a major broker. So, it is not an either/or in our organisation,” the CFO explained.

“I can’t think of a time when we made a decision around our branch network based on ‘should we actually use a third party in that particular space’.”

While the bank is in support of consumers paying service fees to brokers, its representative acknowledged that “such a change will have significant and varied implications, which will need to be carefully considered before such a change is implemented”.

The proposed monetisation model has been met with criticism from the aggregator and broker community, with Connective director Mark Haron previously telling The Adviser that if brokers charged a fee for service, the Australian broker population would decline significantly, which, in turn, would negatively impact the non-major banks and non-banks that depend on brokers for business. It was his contention that such a model would decrease competition in the Australian financial system.

The major banks — which already control more than 80 per cent of all owner-occupied housing loans and 85 per cent of investor housing loans, according to the Australian Prudential Regulation Authority — would therefore gain additional market share if consumers chose to go directly to banks for their loans in order to avoid paying broker fees, Mr Haron said.

The Connective director also warned that a fee-for-service model could make financial advice less accessible to customers who need it the most, such as first home buyers, and further noted that, by managing home loan applications, brokers actually reduce the workload for banks.

“[Brokers are doing] the work that the banks would have to do themselves, so it’s only fair that the brokers get remunerated by the banks,” the director said.

The global banking sector, which has benefited from its “inertia” for decades, is under cost pressure as it attempts to reconcile legacy IT systems with a newly ‘digitised’ front end, says Ariel Investments.

Speaking in Sydney, Chicago-based Ariel Investments director of research for international and global equities Chaim Schneider said banks are transforming “tremendously” as they shift from ‘offline’ bank branches to the online world.

“Banks are absolutely making a lot of investments in mobile, in adapting to the new paradigm, because clearly the new world around them is changing tremendously and rapidly,” Mr Schneider said.

“But the problem is that banks were not designed for this way,” Mr Schneider said.

Many banks were still using IT architecture that could be up to 50 years old in a “coding language which was not designed for an omni-channel world,” he said.

“They have these back ends, these core banking platforms, that are sub-optimally established, and then they have this front end, where they’re investing heavily in digital and mobile and online banking, and they need to bridge the gap between the two.

“But in doing so, this patchwork comes at a significant cost. Part of it has to do with simply the infrastructure costs with making these investments, which are huge.”

A further cost-related pressure on banks was the open banking regime and the increased competition this would bring to the sector, he added.

“Banks, more than anything else, benefit from inertia. And you can hope in some ways, this threat will be mitigated by other factors, but either way it’s a real threat challenging the costs of these institutions.”

Banks are also looking to “future-proof” their branch networks, he said.

“Effectively, banks around the world are taking steps to reshape the branch network to future-proof their branch network,” Mr Schneider said.

“But there are significant limits and constraints on their abilities to do so.”

He said the closure of bricks-and-mortar bank branches was often seen as a cost-cutting measure – but that this was in fact hurting banks in other ways.

“Strange as this may seem, the majority of people around the world in country after country look at that bank that they may pass on their way to work every day and believe their cash, their deposits, are inside the vault in that bank.

“We all know the way banking systems work these days doesn’t exactly work that way. But that is truly ingrained in [the] mindset of people around the world,” Mr Schneider said.

“And what that means is when that bank branch closes, banks in that region sometimes have a problem sustaining those customer relationships amongst both retail customers as well as small businesses who just like the presence, the comfort, of driving by their bank on a regular basis.”

He also pointed to the “very important role” bank branches played as “deposit-gathering frameworks for banks”.

“The raw material for any bank is deposits. Without deposits, banks can’t make loans. And the branches play a mission-critical role in deposit-gathering, in particular low-cost deposit gathering.

I did a mapping between the old and new basis for investor and interest only loans in the RBA credit aggregates. I posted the data earlier.

Since mid-2015 the bank has been writing back perceived loan reclassifications which pushed the investor loans higher and the owner occupied loans lower.

They have now reversed this policy, so the flow of investment loans is lower (and more in line with the data from APRA on bank portfolios). Investor loans are suddenly 2% lower. Magically!

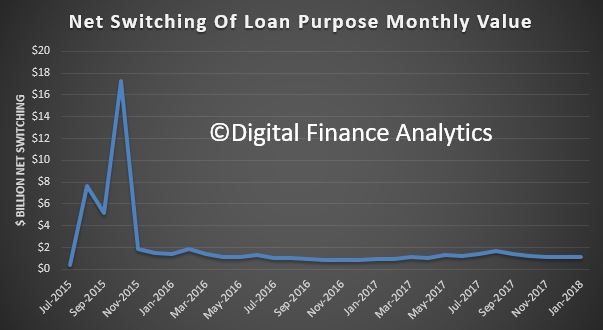

This is the monthly switching:

But two points.

First I am amazed the banks feels its OK to suddenly change the basis of their calculations, when its such a critical issue. The provided reasoning is perverse – loan switching is “normal”. Suddenly back tracking over the past two years is plain weird. The section in the Stability Report said it was going to happen. That is all.

Second, it once again highlights the rubbery nature of the data on lending in Australia. What with data problems in the banks, and at the RBA, we really do not have a good chart and compass. It just happens to be the biggest threat to financial stability but never mind.

Standing back though, despite the static growth in investment lending, do not forget that overall debt is still rising faster than incomes, by a factor of two to three times.

Owner occupied lending must be tamed too if we are to ever get back to a more even keel – the case for more macro-prudential intervention just got stronger!

ASIC says the Federal Court in Melbourne has published its findings and reasons for ordering Australia and New Zealand Banking Group Ltd (ANZ) to pay a penalty of $5 million for breaches of the responsible lending provisions by its former car finance business, Esanda.

The Court’s judgment follows ASIC’s announcement of a package of actions against ANZ for contraventions of various responsible lending provisions of the National Consumer Credit Protection Act (refer: 18-013MR).

In relation to the civil penalty proceedings, the Court found (in summary):

in respect of 12 car loan applications from three brokers, ANZ failed to take reasonable steps to verify the income of the consumer because ANZ relied solely on a document which appeared to be the consumer’s payslip in circumstances where ANZ:

knew that payslips were a type of document that was easily falsified;

received the document from a broker who sent the loan application to Esanda; and

had reason to doubt the reliability of information received from that broker;

income is one of the most important parts of information about the consumer’s financial situation in the assessment of unsuitability, as it will govern the consumer’s ability to repay the loan;

while ANZ did not completely fail to take steps to verify the consumers’ financial situation, it inappropriately relied entirely on payslips received from these brokers; and

ANZ management did not ensure that relevant policies were complied with and, in the case of the contraventions involving one broker, no action was taken despite management personnel having become aware of the issues about the broker.

The judgment annexes a statement of facts which sets out why ANZ had reason to doubt the reliability of the payslips being provided with the 12 applications, including that one of the brokers had been previously investigated for fraud. ANZ had also become aware of issues with payslips being provided by the brokers that gave it reason to doubt the authenticity of the submitted payslips.

The statement of facts also sets out that reasonable steps to verify a consumer’s income would have included requesting from the consumer a bank statement showing a history of salary deposits or substantiating salary deposits in ANZ bank accounts for an existing customer.

In its judgment, the Court made clear that where unlicensed brokers submit loan applications in reliance on the “point of sale” exemption under regulation 23 of the National Consumer Credit Protection Regulations 2010 (Cth), lenders have a heightened obligation to exercise particular care. This was the basis for the higher penalties imposed on ANZ relating to the loans submitted by one of the brokers under the point of sale exemption.

ASIC Deputy Chairman Peter Kell said, ‘A consumer’s income is an essential component in determining their ability to repay a loan. Lenders must take reasonable steps to verify a consumer’s financial situation, and this includes checking the reliability of documentation that is provided to them. Lenders must be alert to the potential for documents to be falsified and ensure that their controls are sufficiently robust. ‘

ANZ will be remediating approximately 320 car loan customers for loans taken out through the three broker businesses from 2013 to 2015 which are likely to have been affected by fraud. The remediation will total around $5 million.

ANZ will:

offer eligible customers the option of entering into a new loan on more favourable terms than the existing loan;

provide refunds to some customers who have paid their loan out or had the car repossessed; and

remove any default listings resulting from the loan.

The chairman of the Productivity Commission has said that while it may be in the interests of the bank and the broker to limit churn, it is not in the interests of the borrower.

Speaking at the Committee for Economic Development of Australia (CEDA) in Melbourne on Monday, Productivity Commission chairman Peter Harris reiterated some of the questions raised in the commission’s draft report into competition in the Australian financial system, which scrutinised broker remuneration and the purpose of trail commissions.

The PC is also questioning whether consumers should pay brokers a fee for service.

Speaking on Monday, Mr Harris said: “Despite some recently announced industry changes to parts of the commission payment structure, commission earned by brokers remains far from aligned with the interests of the customer.

“Trailing commissions are an example of that. These are only paid while a customer remains with a loan. They are worth $1 billion per annum. There is nothing immaterial about them.

“The industry itself has said that trailing commissions are designed to reduce churn and manage customers on behalf of banks.

“Despite the hint to the contrary, we do actually understand quite well why it might be in a bank’s interest and a broker’s interest to jointly limit churn.

“But not the customer’s interest, who (the data is surprisingly unavailable, as noted earlier) is most probably paying for the service.”

He continued: “Given the unhappy experience with misaligned incentives in wealth management, being able to substantiate the assurance that a broker is acting in the customer’s best interest would seem to be pretty desirable today.”

He said that the commission would “prefer” that banks imposed this interest via contract rather than have the standard introduced via regulation. (However, the commission’s chairman added that as the commission has no power to recommend what banks do, it has instead proposed regulation in the draft report.)

“It would have been valuable to put the cost-benefit side by side”

Once again, the chair highlighted a data gap in the industry, stating that he believes the “default position among data holders in this industry is set against transparency”.

“[W]e were genuinely surprised to find that they either do not hold data at all on some important aspects of decision making, or for another reason could not supply them,” Mr Harris said, stating that “the cost of mortgage brokers is quite high”.

Mr Harris added that brokers cost $2,300 for the average loan of $369,000, plus a trailing commission of $665.

He said: “Other analysts have suggested higher numbers than these in high-priced locations, but we will stick with national averages.

“More than $2.4 billion is now paid annually for these services. Some in the broking industry want to know why there is suddenly attention being paid to commissions.

“The sum I just cited, as a large apparent addition to industry costs since the mid ’90s, by itself suggests a public analysis of why it is so large might be in order.”

He argued that the $2.4 billion figure “becomes problematic when it is also suggested that customers aren’t burdened by this as they don’t pay these costs”, adding that “anyone with a slight amount of common sense knows that somewhere in any product purchase it is only a customer or a shareholder who could be paying this charge, unless offsetting costs have been stripped out”.

Mr Harris continued: “Shareholders returns are pretty constant, so we would have liked to unpack that cost question a little, to see if the price was supported by cost savings. With the data provided by banks, this proved to be near impossible.

“For smaller banks, we were able to develop some estimates of the branch costs they would potentially face, without broker assistance. But we received insufficient information from most (not all) banks, and so could not create a clear picture.

“Thus, we can’t say whether there has been a net improvement in efficiency, even as a large sum in commissions has been added to industry costs. We have also shown in the report that brokers do produce slightly better rates for their clients than going in to the bank branch. But that benefit for consumers has been declining since the GFC. It would have been valuable to put the cost-benefit side by side.”

Mr Harris also took aim at vertical integration, suggesting that bank-owned aggregators control about 70 per cent of the mortgage broking market.

He added that in-house products or white label loans appear to “dominate disproportionately” the outcomes for borrowers who use bank-owned aggregators.

The PC chair noted that, in 2015, the Commonwealth Bank had 21 per cent overall market share in the broker channel but a 37 per cent market share via Aussie Home Loans.

However, while it has concerns about vertically integrated groups, the Productivity Commission said that forcing banks to divest of their broking businesses should be “a last resort”.

“Of course, if the necessary solutions prove commercially unpalatable, institutions themselves may then choose to divest,” Mr Harris said.

Many in the industry have spoken out against the Productivity Commission’s draft report, with some suggesting that the remuneration figures cited are “incorrect”, others stating that the recommendation to charge fees would be “anti-competitive”, and both broker associations calling out some findings of the report (which relied heavily on figures from CHOICE consumer group and UBS reports) as “limited”, “amateur” and — in some cases — “nonsense”.

One which has surfaced is the Lenders Mortgage Insurance (LMI) sector. With 20% of borrowing households required to take LMI, and just two external providers (Genworth and QBE LMI), the Commission has explored the dynamics of the industry. They called it “an unusual market”, where there is little competitive pricing nor competition in its traditional form. Is the market for LMI functioning they asked? Could consumers effectively be paying twice?

One which has surfaced is the Lenders Mortgage Insurance (LMI) sector. With 20% of borrowing households required to take LMI, and just two external providers (Genworth and QBE LMI), the Commission has explored the dynamics of the industry. They called it “an unusual market”, where there is little competitive pricing nor competition in its traditional form. Is the market for LMI functioning they asked? Could consumers effectively be paying twice?