The Volkswagen “dieselgate” story, in which the company helped their cars pass emissions tests under special conditions that they later failed when the car was driven normally, is not an isolated incident – there has long been a culture of gaming metrics in the automotive industry and other sectors do it too.

Metrics are shorthand for good performance – they focus the mind of the setter and the tested and are costly and embarrassing if targets are missed. So why take the risk?

This gap between the rhetoric of good practice and the reality falling short in manufacturing has been noted elsewhere. And research I co-authored back in 2004 showed how another car supplier which had multiple sites across the world gamed the standards placed on it by customers. Winning business depended on performing well on various measures, with the company’s customers assessing each delivery of parts on quality, cost and whether it was on time and in full. One of us spent six weeks in two different sites carrying out participant observation. We found that the company gamed the system rather than admit issues with performance, presenting an image of good practice which was a facade.

Quarterly or biannually, customer procurement staff visited the supplier and undertook a complex evaluation process of the company we studied and the rest of their supply base. The quality and delivery performance over an extended time period was assessed as were cost increases, manufacturing and the supply chain capabilities and staff performance. League tables were produced and further business was awarded on good performance, or business was lost if the supplier scored badly.

The customers wanted to trust the supplier manufacturing process. This meant believing it was capable of producing good parts and meeting variations in demand. We found three examples of gaming to meet process measures.

1. Presenting a smooth-running operation

The semblance of high quality at every stage of the manufacturing process gives an indication to customers of the eventual product quality. It is common practice for suppliers to provide statistical process control charts where samples of car parts are checked to see if they match up to various metrics. Ideally, all the machinery and equipment should be measured and in control so that it does not produce bad parts. In our research, the supplier sent the charts taken from places in the process they knew were performing best, not a general sample and most certainly not from areas that they knew would make the graphs look bad.

2. Hiding stoppages and delays

The second measure was about stoppages or downtime in the process. Minimising unexpected breakdowns or downtime in the manufacturing process is key to being seen as a capable supplier. In order to achieve this, the best manufacturers plan maintenance periods where the line is stopped deliberately to service machines.

When the supplier process we studied stopped unexpectedly, management immediately reallocated the time to “planned maintenance”, so they met the downtime target and looked like an advanced manufacturer to the customers.

3. Minimising the appearance of waste

A good manufacturing process does not produce much wasted product. On the factory floor the designated container for our study company had an acceptable level of scrap product, which was measured and recorded. Material which could have been counted as scrap was disposed of via conveyor belts intended for other purposes. We even found that it was placed in employee trouser and coat pockets to be hidden and taken out the factory, so that waste targets were met.

Buyers would visit and audit the supplier, so the supplier was well practised at turning the factory floor into a stage where ideal manufacturing practices were displayed and performed during the visit. Examples include the accident reporting chart beginning after the last accident, records of employee skills being up to date, even if the employee went on the course a long time ago and might not be able still to perform the tasks in question. Machines were hidden, cleaned and floor spaces painted, all to create the impression of a competent organisation which lapsed as soon as the buyers left.

The major car manufacturing customers were not above gaming measures themselves. When an employee was honest with a customer about having problems with an aspect of the process they were told to “move the curve up” on the chart, rather than investigate the root cause and improve the process. Perfectly good batches of parts were rejected one week then accepted the next so that customer stock levels met their target.

A Volkswagen car during a test at a technical and testing centre.Reuters/Dado Ruvic

Beyond the car industry

It would be wrong to just demonise VW and the car industry. The downside of having measurement and metrics on performance is a far wider phenomenon. I have witnessed similar processes in the food sector and it seems very similar to the distorted affect of performance measures at the failing Mid-Staffordshire hospitals and even in football. People focus on the measure, not the wider good the measure was intended to represent. Plus, the setters of the measure are equally culpable.

I respectfully disagree with Edward Queen’s article on The Conversation, which makes the case for teaching business students better ethics – this is too little, too late. The problem is far wider and systemic.

Trying to meet measures with no extra effort is considered an ethical activity in many organisations and rewarded at annual appraisal time – another example of targets shaping performance. The attractiveness of metrics lies in their appearing to give managers control; the problem is that they cannot cover all aspects of performance and leave scope for short cuts, interpretation and gaming – by every party involved.

Returning to the car industry, it’s worth paying heed to the ideas of management expert W Edwards Deming. His ideas are widely attributed to be responsible for improving the reliability and quality of cars and achieving market dominance for companies who followed them. He believed that organisations should not be run on targets, quotas, or objectives, as they are usually a distraction from improving processes. In the case of VW and the car industry, the overarching goal is to lower emissions, which is a far riskier option to ignore in the long term.

Author: Lynne Frances Baxter, Senior Lecturer in Management Systems, University of York

In a move to bolster capital, and ahead of its full year results in November, Westpac has announced a $3.5bn share offer and lifts its mortgage rate for existing owner occupied and investor mortgage borrowers. The company is in a trading halt until 19th October. They claim this will place their CET1 capital ratio in the top quartile of banks globally on a comparable basis.

As we predicted, banks need to bolster their capital, and will raise mortgage rates independent of moves in the RBA cash rate. We expect further rises across the industry, making mortgages more expensive to existing borrowers. We also expect intense competition for new owner occupied business, so special offers will also continue.

Looking at the details, Westpac has announced a $3.5bn share offer, to raise approximately $3.5billion of ordinary equity. The price of the offer has been set at $25.50 which is a discount of 13.1%.

Westpac’s shares have been placed in a trading halt to enable the institutional component of the Entitlement Offer to be completed, with trading expected to recommence on 19 October 2015.

The equity raised will add approximately 100 basis points to Westpac’s Common equity tier 1 (“CET1”) capital ratio and places Westpac ’s CET1 capital ratio within the top quartile of banks globally, with a CET1 capital ratio of over 14% on an internationally comparable basis. Capital raised responds to changes in mortgage risk weights that will increase the amount of capital required to be held against mortgages by more than 50%, with the increased regulatory requirement to be applied from 1 July 2016.

Westpac has also announced an increase in its variable home loan (owner occupied) and residential investment property loan rates by 20 basis points. The new rates take effect from 20 November 2015. It had previously lifted rates on investment loans by 27 basis points in September.

To support the offer, Westpac also announced its unaudited preliminary Full Year 2015 Result. Highlights of the unaudited preliminary result for Full Year 2015 compared to Full Year 2014 include:

Statutory net profit of $8,012 million, up 6%

Cash earnings of $7,820 million, up 3%

Cash earnings per share of 249.5 cents, up 2%

Cash return on equity of 15.8%, down 57 basis points

Westpac also expects to determine a 2015 final, fully franked dividend of 94 cents per share, up 2 cents on the 2014 Final Dividend. New shares issued under the Entitlement Offer are not entitled to the 2015 Final Dividend.

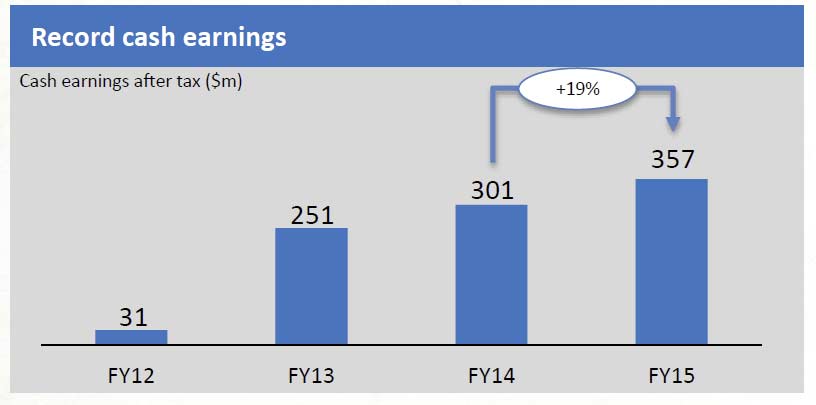

BOQ has delivered record statutory and cash profit results for the financial year to 31 August 2015, despite strong competition, and funding pressure. Growth in broker originated home loans helped. Statutory profit after tax was up 22% on the prior year to $318 million and was helped by a reduction in impaired assets. As a standard capital bank, it may benefit from the higher IRB capital being required of the majors. In summary, BOQ bears the hallmarks of a well run business, so is well positioned to leverage digital transformation and growth beyond Queensland next year. Unless of course the housing market goes pear-shaped!

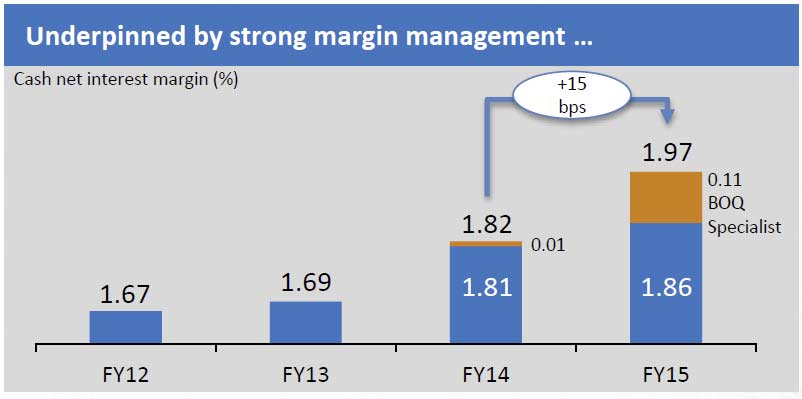

After tax cash earnings increased 19% on FY14 driven by higher net interest margin, a strong full year contribution from BOQ Specialist and further improvement in impairment expense. Basic cash earnings per share grew 9% to 97 cents per share.

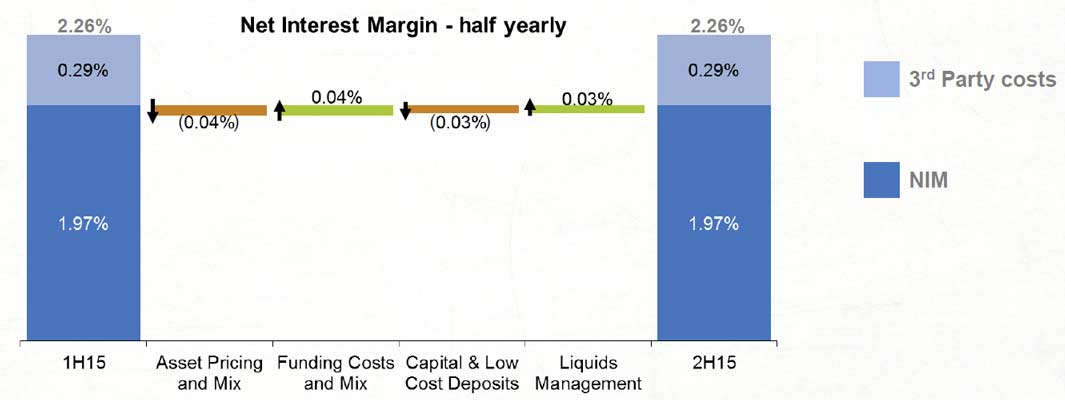

Net interest margin for the full year was 1.97%, up 15 basis points on the prior year due largely to the higher margin BOQ Specialist business.

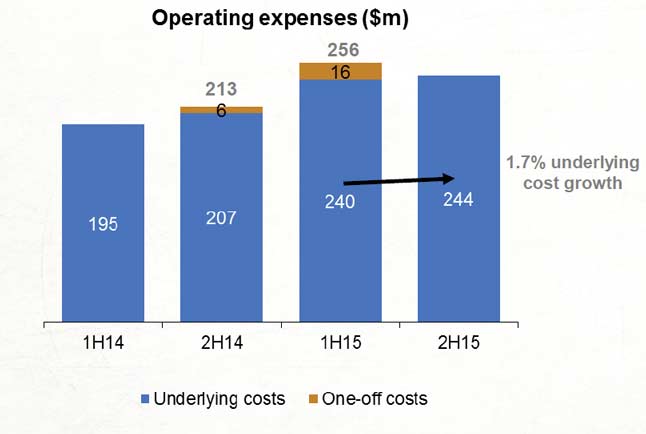

The Group’s cost to income ratio increased to 46%, up from 43.9% in the prior year, due to some one off items.

The FY15 impairment expense of $74 million was a $12 million (14%) improvement on the prior year. Impaired assets declined by $56 million (19%) to $237 million following a reduction in new impaired assets and continued momentum in realisations.

BOQ Finance’s loan impairment expense increased $10 million which was primarily attributable to the impact of the mining industry downturn on associated sectors.

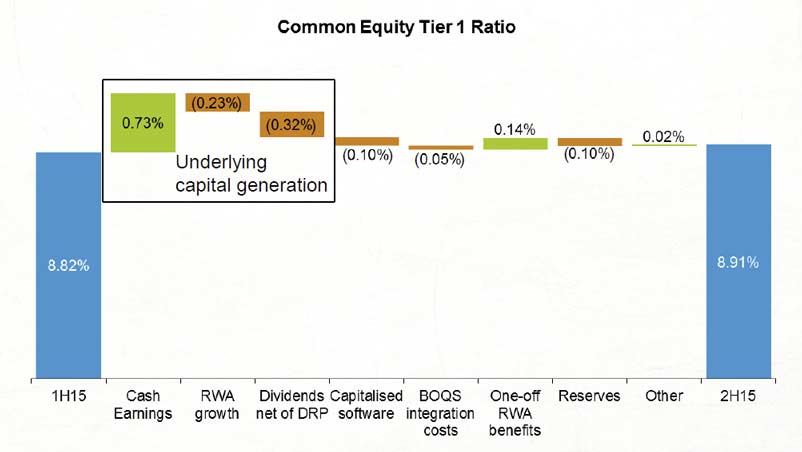

The Group further strengthened its capital ratios during the year with the CET1 ratio increasing 28 basis points to 8.91%. CET1 increased in the second half as underlying cash earnings supported 7% annualised loan growth and a two cent increase in the final dividend.

The Bank will pay a final dividend of 38 cents per share, up two cents on the previous corresponding period, taking full year dividends to 74 cents per share fully franked.

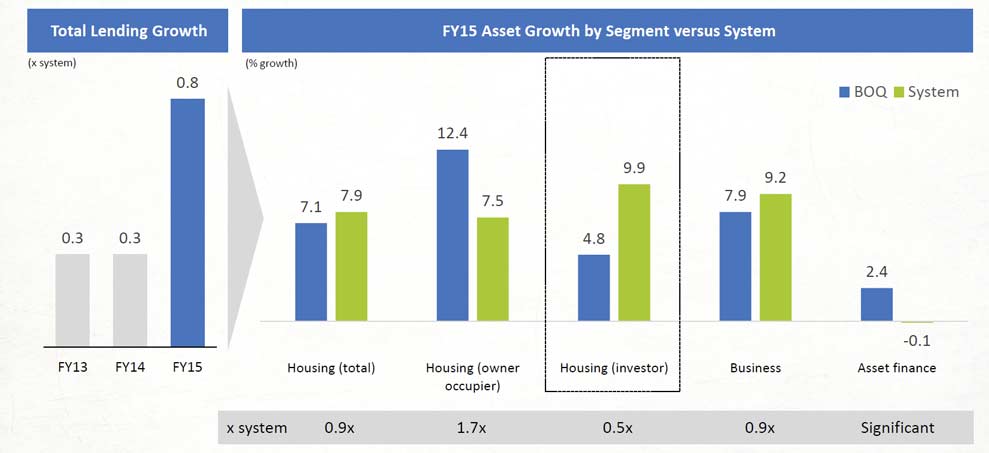

New distribution channels, including brokers, also helped diversify BOQ’s asset base, with the proportion of total lending in Queensland falling below 50% for the first time.

The housing portfolio grew $1.9 billion or 7% (0.9x System) supported by the contribution of BOQ Specialist, which generated growth of $1.3 billion. The mortgage broker channel, which accounted for 15% of the Retail Bank’s housing settlements, was up from 5% in the prior year.

Commercial lending balances grew 8% to $8.3 billion while BOQ Specialist’s commercial book increased 14% to $2.3 billion.

The BOQ Finance portfolio grew by 2% to $4 billion, a solid result in an operating environment that has seen sluggish investment in plant and equipment. BOQ Finance’s strategy of expanding its third party origination sources while continuing to support the Business and Retail Bank network has positioned the business for future growth.

BOQ Specialist contributed $43 million to the Group’s FY15 result in its first full year since acquisition, exceeding the maintainable earnings guidance of $38 million announced at the time of acquisition by 13%.

The business delivered loan growth of $1.6 billion while maintaining margins and credit quality. BOQ Specialist serves health, medical and accounting customers and continues to benefit from the higher growth rates of these segments compared to the broader economy.

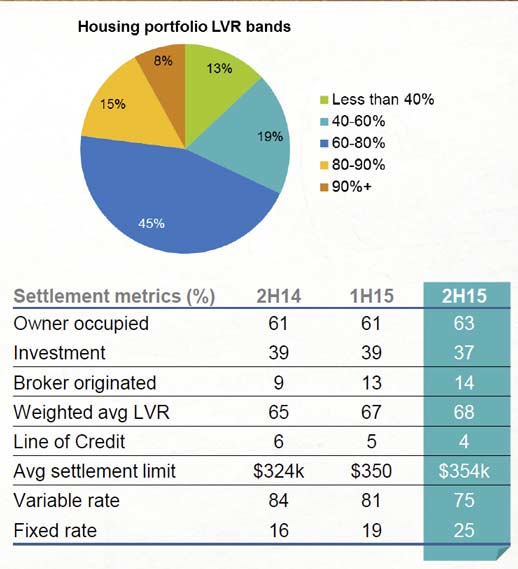

Looking at the housing data in more detail, the LVR and loan mix remains stable.

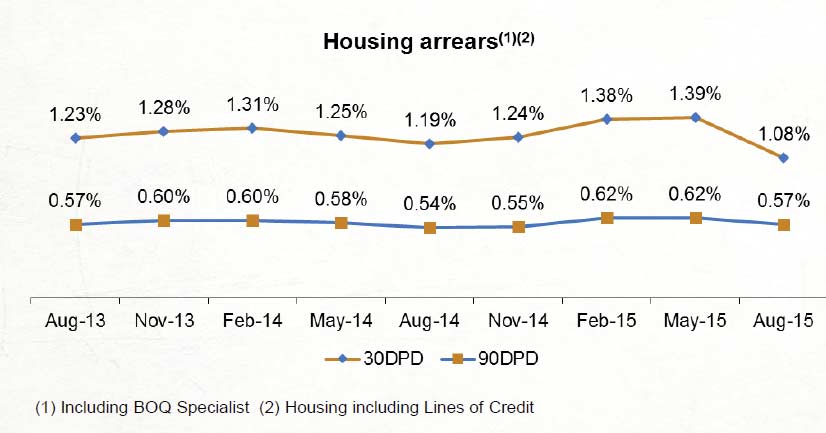

Housing loan arrears are under control, and fell a little in August.

As part of its regular investor communications program, Macquarie Group will be presenting at the CLSA Investors’ Forum in Hong Kong on 15 and 16 September 2015.

Contained within the presentation is an update to the short term outlook statement that Macquarie provided at the Group’s Annual General Meeting on 23 July 2015.

Macquarie continues to expect the FY16 result to be up on FY15:

As a result of the continued weakening of the Australian dollar and improved trading conditions across most businesses including Macquarie Securities and Macquarie Asset Management (MAM), which benefited from strong performance fees, Macquarie expects the 1H16 result to be up approximately 40 per cent on 1H15, subject to the completion rate of transactions and the conduct of period end reviews

The 2H16 result is expected to be broadly in line with 1H16, noting MAM is expecting lower performance fees in 2H16 than 1H16.

Mortgage Choice Limited said today that as a consequence of a comprehensive strategic and operational review, the company has made the decision to shut down its Help Me Choose business unit. Mortgage Choice presented its FY15 financial results in August and chief executive officer John Flavell made it clear that Help Me Choose’s financial result needed addressing.

“The less than favourable financial result of the Help Me Choose business prompted a comprehensive review of the operation and a decision has been made to close it down in its current form,” Mr Flavell said. “Mortgage Choice will continue to focus on evolving the Mortgage Choice business by building a compelling and differentiated financial services offering and, in turn, providing sustainable earnings for its shareholders. “Capitalising on the significant opportunities facing Mortgage Choice requires focus, and continuing to invest in a business that is unlikely to be profitable in the foreseeable future does not make sense.”

The operation was acquired in October 2010 when the comparison website HelpMeChoose.com.au, was said to be one of the top websites of its kind in Australia, offering guidance on home loan, health insurance and life insurance.

Mortgage choice total loan book reached $48.4 billion, up 4.5% from $46.4 billion at 31 December 2013 and they expect it to reach $50 billion by 1H16.

In today’s market update, we got a glimpse of the banks intentions under CEO Brian Hartzer. They are looking to add more than 1 million new customers (2015-17), and increase the number of products per customer. There is a strong focus on digital transformation, including the development of a customer service hub which links multiple systems to create a single view of a customer; as well more revamped branches, with 55% of the network changed by 2018. The aim is to drive the expense to income ratio below 40% within 3 years, reducing the groups expense growth run-rate to 2-3% per annum.

They plan to lift investment by $200m to $1.1 billion which is directed to growth, service and efficiency initiatives, focussing on digital, simplification and customer service.

They reaffirmed a target ROE of more than 15%.

Nothing wrong with in intent, but the question will be excellence of execution.

No further disclosure on current banking performance. We think a close eye on the performance of the investment mortgage book is warranted given current market dynamics.

The latest results from YBR, in their 2015 annual report shows a 42% increase in loan settlements over the year to June. They grew their loan book to more than $30 billion or about 4% of Australia’s total home loan settlements. The mortgage and wealth franchise business includes Vow Financial and Resi Mortgage Corporation.

Yellow Brick Road’s own branded product, Empower, showed a 42% rise in settlements in the six months to June to $2 billion in loans over the 2015 financial year, whilst Vow Financial increased its annual settlements 46% to $10.38 billion and Vow Financial grew its advisor base by 29.7% and its broker agreements by 25.1%.

YBR has been expanding their franchise network which is now 255 branches across the country, the increase thanks partly to the addition of Resi’s 19 branches. Vow now has 891 independent mortgage and finance brokers as members of its network.

APRA today released the Quarterly Authorised Deposit-taking Institution Performance publication for the June 2015 quarter. This publication contains information on ADIs’ financial performance, financial position, capital adequacy and asset quality. There were 160 ADIs operating in Australia as at 30 June 2015, compared to 165 at 31 March 2015. There were eight changes were mainly to some credit unions having their licences revoked.

Over the year ending 30 June 2015, ADIs recorded net profit after tax of $38.0 billion. This is an increase of $5.7 billion (17.6 per cent) on the year ending 30 June 2014.

As at 30 June 2015, the total assets of ADIs were $4.4 trillion, an increase of $376.4 billion (9.3 per cent) over the year. The total capital base of ADIs was $238.1 billion at 30 June 2015 and risk-weighted assets were $1.8 trillion at that date. The aggregate capital adequacy ratio for all ADIs was 13.2 per cent.

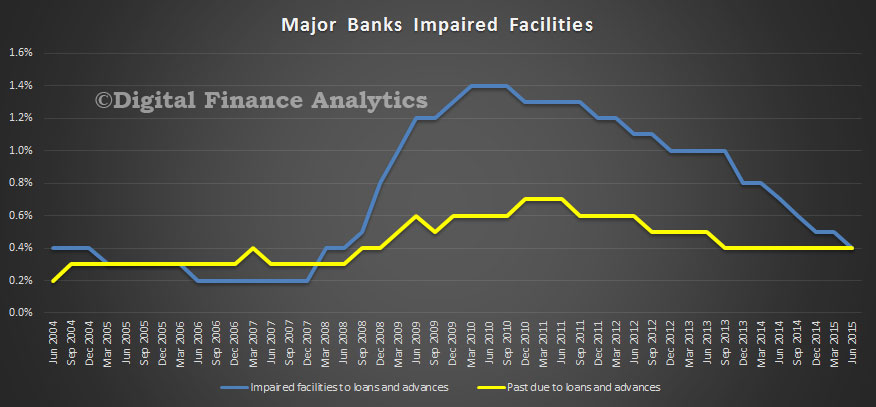

Impaired assets and past due items were $26.7 billion, a decrease of $5.4 billion (16.8 per cent) over the year. Total provisions were $13.4 billion, a decrease of $5.2 billion (27.9 per cent) over the year.

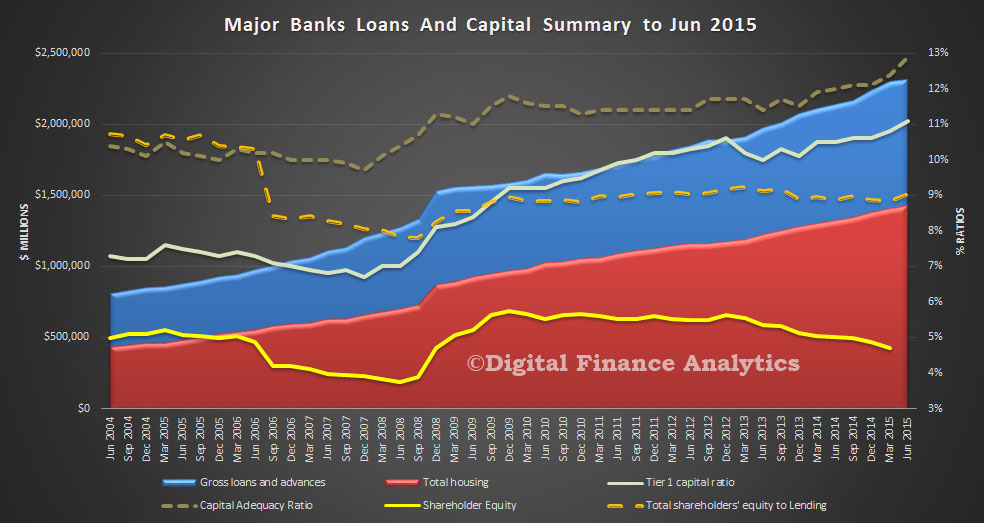

Looking in detail at the average of the four majors, we have plotted loans, housing loans and capital ratios again, to June 2015. We see the growth in lending, and the ongoing rise of housing lending. We also see the capital adequacy ratio and tier 1 ratios rising. However, the ratio of loans to shareholder equity is just 4.7% now. This should rise a bit in the next quarter reflecting recent capital raisings, but this ratio is LOWER than in 2009. This is a reflection of the greater proportion of home lending, and the more generous risk weightings which are applied under APRA’s regulatory framework. It also shows how leveraged the majors are, and that the bulk of the risk in the system sits with borrowers, including mortgage holders. No surprise then that capital ratios are being tweaked by the regulator, better late then never.

At the moment impairments are low, this of course may change if economic momentum slows, unemployment or interest rates rise, or house prices slip. Other risks include external shocks, like China and the impact of rates in the US rising.

As we come to the end of another financial year end reporting season and await the deluge of impenetrable financial reports, we can only lament that another year has passed and an important reporting mechanism widely used in many international exchanges, is still not with us.

In Australia financial statement information continues to be provided to users in detailed and complex reports, that are not user friendly. These may now be provided electronically in pdf format, but the problem is that the data can’t be extracted electronically; accurately and efficiently. There is a solution which is passing us by.

I am talking about XBRL – which stands for eXtensible Business Reporting Language – and it represents a standardised form of electronic reporting by companies which facilitates the preparation and exchange of financial statement information.

The formats for the preparation of data are now well established and the International Accounting Standards Board publishes a taxonomy that reflects the requirements of International Accounting Standards which are in use in most countries around the world (http://www.ifrs.org/xbrl/ifrs-taxonomy/Pages/ifrs-taxonomy.aspx).

It is required in many countries and if Australia wants to be a financial centre it needs to catch up. In the US the Securities Exchange Commission has since 2011 required all public registrants to file XBRL information. This is no longer new or untried technology and there many companies providing services for the preparation and use of XBRL information.

What are the benefits of XBRL? At a very practical level XBRL is a relatively straight-forward format for sharing financial information. As it uses standardised formats, which financial reports already follow, it allows for software to be developed which extracts relevant information and presents it in formats that makes it more relevant, understandable and facilitates it use.

Importantly, XBRL can make annual reports more transparent and reduces the risk of important information being lost in the notes. Not surprisingly XBRL usage has been found to improve analyst forecast accuracy. Software using XBRL may be proprietary or publicly available for sale, and it may allow sophisticated analysis to be undertaken.

This is simply not possible at the moment as financial data is provided by various data aggregators who manually key data. This naturally limits the amount of data provided and there are potentially issues of accuracy. Requiring firms to provide XBRL information will reduce the cost of data collection and increase the ability for international investors who might otherwise overlook Australian firms.

Australia operates in a global economy and this is part of the membership price. There is evidence that the provision of XBRL information reduces the cost of capital, and this is most pronounced for small, high growth firms that likely have low analyst coverage. So, while the relative costs might be higher for small firms, the benefits might be relatively higher too.

Has there been progress with implementing XBRL? There have been a number of initiatives to bring XBRL to Australia and these envision widespread application, encompassing all companies rather than just listed companies and the provision of information to multiple government agencies, including the Australian Securities and Investments Commission, the Australian Prudential Regulation Authority and the Australian Taxation Office.

This level of ambition while on the face it desirable, has committed us to a long and tortuous negotiations about format rather than achieving outcomes in a timely manner.

Our immediate focus should probably just be on firms listed on the Australian Stock Exchange and including this requirement in their Listing Rules.

Author: Peter Wells, Head of Accounting Discipline Group, Accounting at University of Technology Sydney

AMP Limited has reported strong growth and a net profit of A$507 million for the half year to 30 June 2015, up 33 per cent on A$382 million reported for 1H 14. Underlying profit was A$570 million compared with A$510 million for 1H 14, up 12 per cent half on half.

AMP Australian wealth management net cash-flows were A$1.2 billion in 1H 15, up A$36 million on net cash flows of A$1.1 billion in 1H 14. Total cash flows on AMP platforms continue to perform strongly, growing 11 per cent to A$1.9 billion in 1H 15. These flows were partially offset by higher net cash outflows on external platforms of A$774 million.

AMP Capital external net cash-flows were A$3.0 billion, an increase of A$1.4 billion from net cashflows of A$1.6 billion for 1H 14. This was driven by stronger inflows generated by the China Life AMP Asset Management joint venture as well as institutional and retail domestic client flows.

The cost to income ratio was 43.1 per cent for 1H 15, an improvement of 1.9 percentage points on 1H 14. Controllable costs increased 1.1 per cent.

Underlying return on equity increased 1 percentage point to 13.5 per cent in 1H 15, largely reflecting the increase in underlying profit.

AMP has A$2.3 billion capital above minimum regulatory requirements at 30 June 2015, up from A$2.0 billion at 31 December 2014. The increase is due to retained profits and the AMP Wholesale Capital Notes issuance, but partially offset by AMP’s investment in China Life Pension Company in Q1 2015.

The Board has declared a 12 per cent increase to the interim dividend to 14 cents per share compared with 12.5 cents per share for the 2014 interim dividend. This represents a payout ratio of 73 per cent of underlying profit and is within AMP’s target range of paying 70-80 per cent.

Segmentals:

AMP Capital: Operating earnings increased 26 per cent reflecting stronger performance fees and supportive market conditions for much of the half. There was a A$1.4 billion improvement in external net cashflows to A$3.0 billion, strong investment performance led by flagship funds and the continued success of the internationalisation of the business. The cost to income ratio of 58.7 per cent is below the target range of 60-65 per cent largely because of strong performance fees in 1H 15.

North AUM grew 16 per cent to A$18.6 billion: Customer numbers increased 14 per cent on the North platform to over 87,000 and North AUM increased A$2.6 billion to A$18.6 billion since December 2014. However net cashflows fell 4 per cent to A$2.3 billion for 1H 15 largely as a result of more pension customers drawing down an income stream.

AMP Bank delivered A$50 million operating earnings, up 19 per cent compared with 1H 14, reflecting an increase in residential mortgages and improved net interest margin. AMP aligned advisers contributed almost a quarter of new business in a period of intense competition.

New Zealand operating earnings of A$61 million, up 11 per cent compared with 1H 14, reflecting a turnaround in experience, favourable currency movements and costs being tightly managed. Cashflows continue to reflect the success of KiwiSaver, with KiwiSaver AUM up 20 per cent to NZ$3.7 billion.

In wealth management, operating earnings for 1H 15 were up 13 per cent compared with 1H 14, reflecting stronger net cashflows and investment returns alongside a continued focus on managing costs.

In wealth protection, operating earnings were A$99 million, up 9 per cent half on half, reflecting the impact of management actions. The environment continues to be volatile however claims and lapse outcomes remain in line with best estimate assumptions.

Future of advice strategy: A package of measures to lift the quality of advice is underway alongside a new approach to advice being piloted with encouraging results from consumer testing in five locations. AMP continues to invest in service, platforms and digital capability to improve adviser quality and productivity. Australian adviser numbers are stable at 3,762 in a period of considerable change.