The end of the working month heralds another set of credit stats from both the RBA and APRA. The RBA reports via their Credit Aggregates, which is all credit stock in the system, while APRA reports on the banks (ADI’s) and also provides some individual lender loan stock data. And which ever way you look at it, credit growth is still anaemic, as the “great deleveraging” continues. And given the weak credit impulse, home prices may also be growing more slowly than many are claiming, though that is another story, for another day.

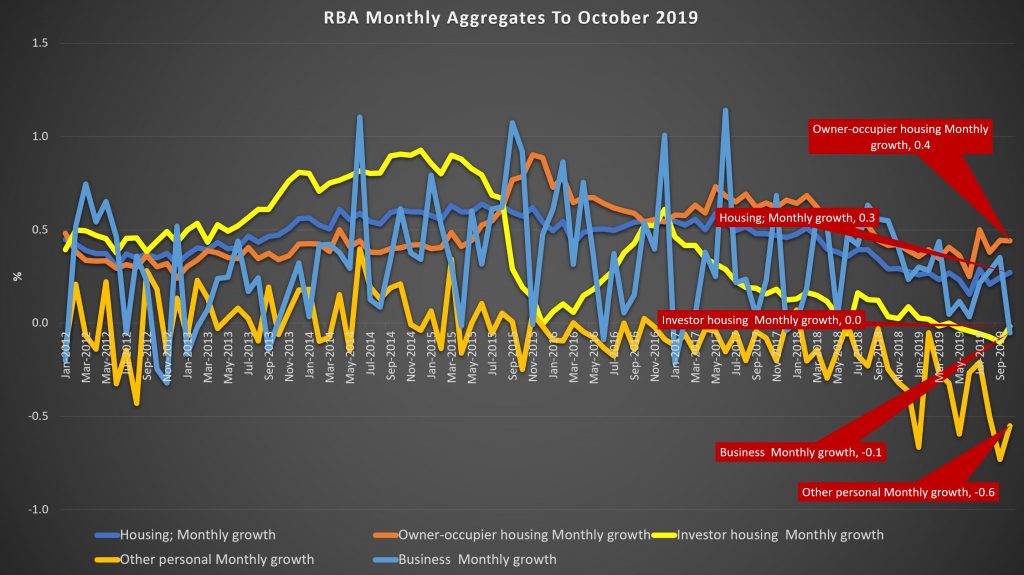

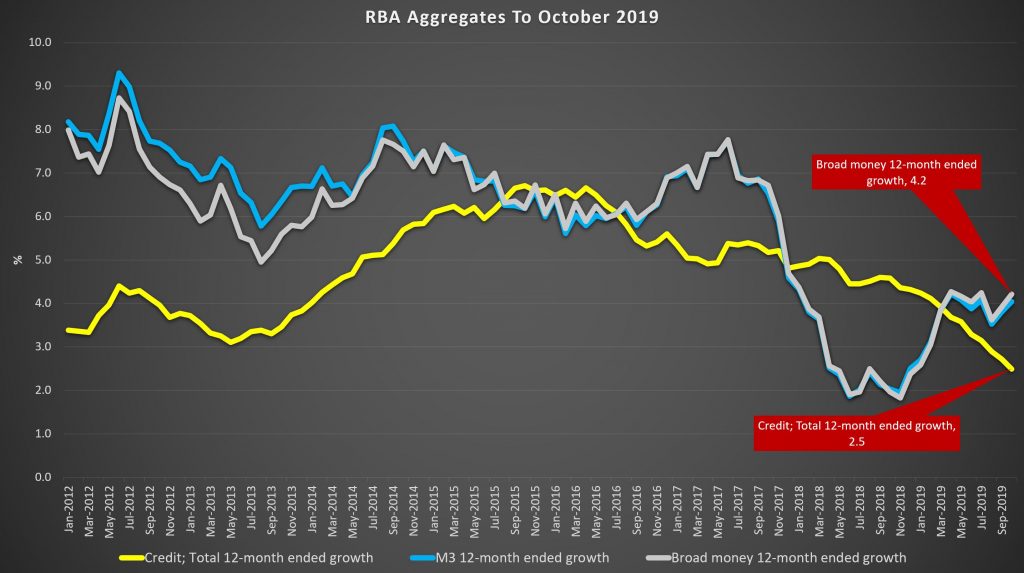

The RBA said that housing credit growth overall was 0.3% higher in October, compared with 0.2% in September. This translates to an annual rate of 3% to October (3.1% last month), compared with 5% just a year back.

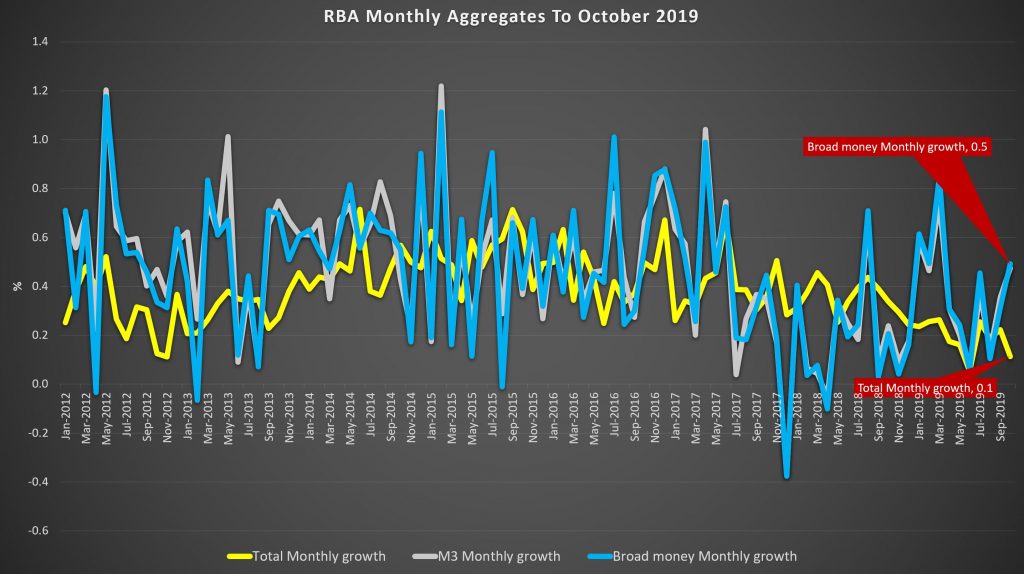

Monthly owner occupied lending rose 0.4% while investor housing lending was flat. Personal credit fell another 0.6% in the month, and business lending was down 0.1%. As a result total credit rose just 0.1%, down from 0.2% last month. Broad money was higher though.

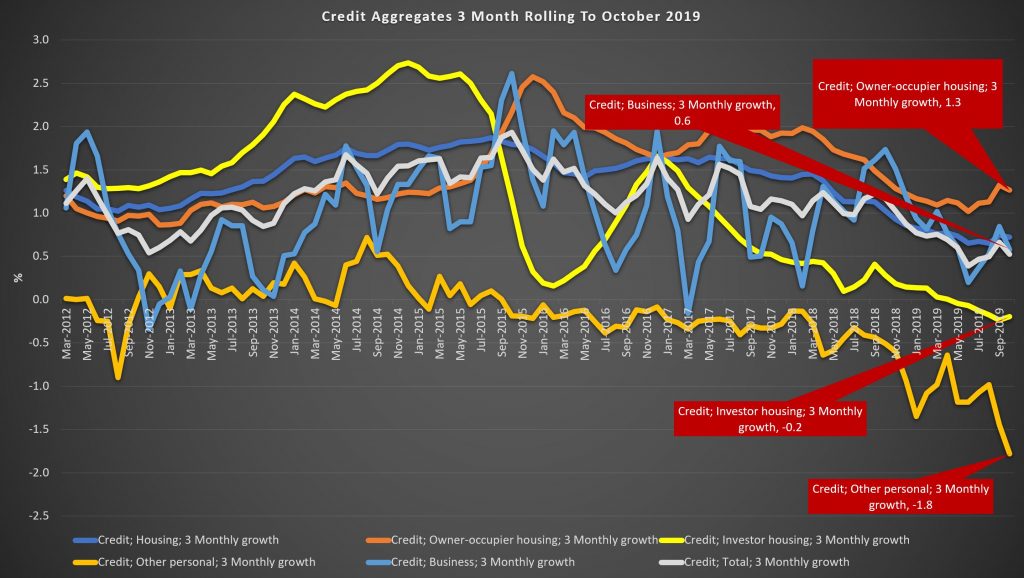

Over a rolling 3 months view, owner occupied credit grew 1.3% while investor credit was down 0.2%, other personal credit was down 1.8% and business credit was up 0.6%.

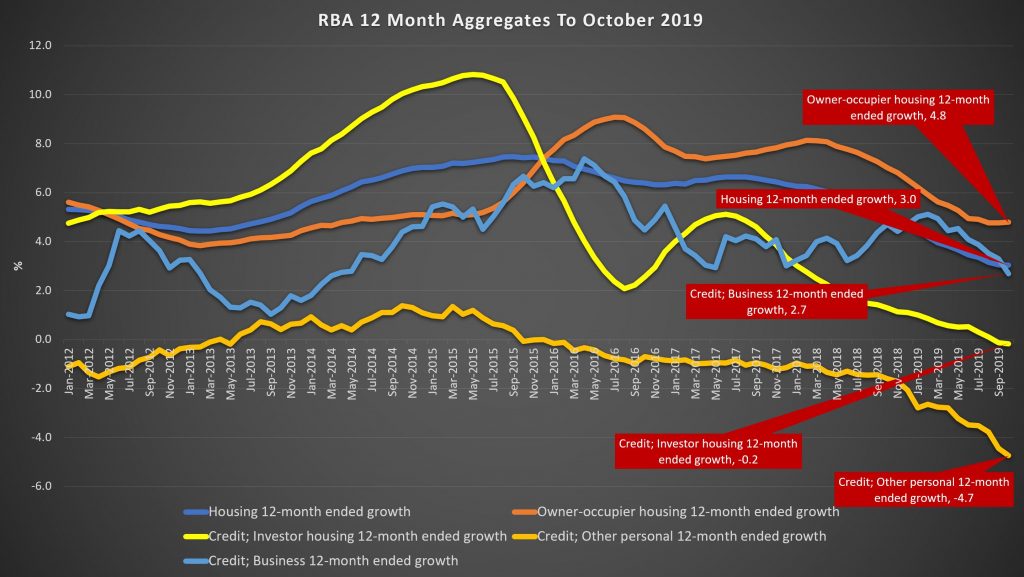

Looking across the rolling 12 month view, housing credit growth dropped from 3.1% to 3%, with owner occupied lending at 4.8% and investor lending down 0.2%. Business credit was 2.7% higher, and personal credit dropped by 4.7%.

As a result, total credit was just 2.5%, as lower as its been for many years, although broad money rose 4.2%.

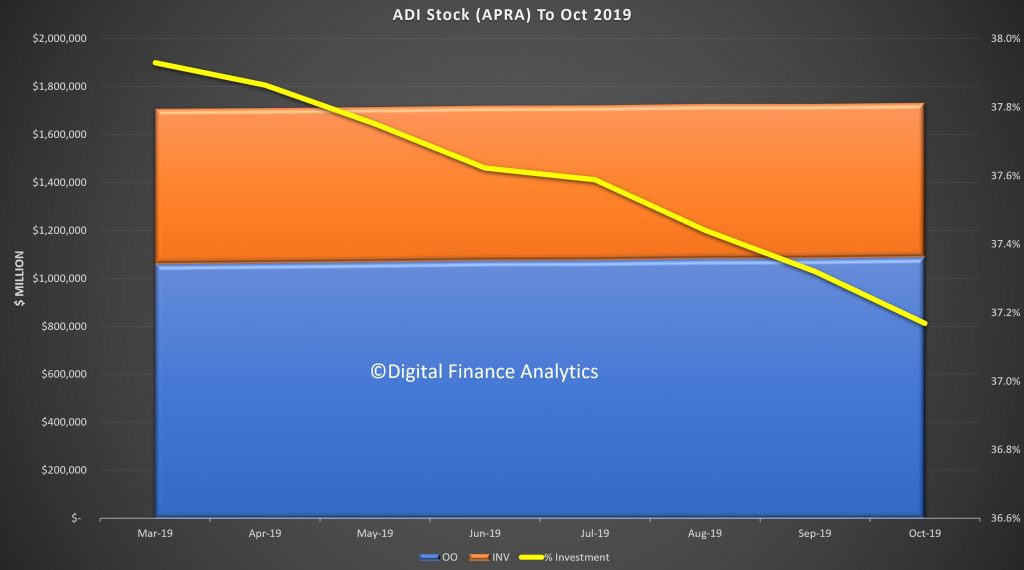

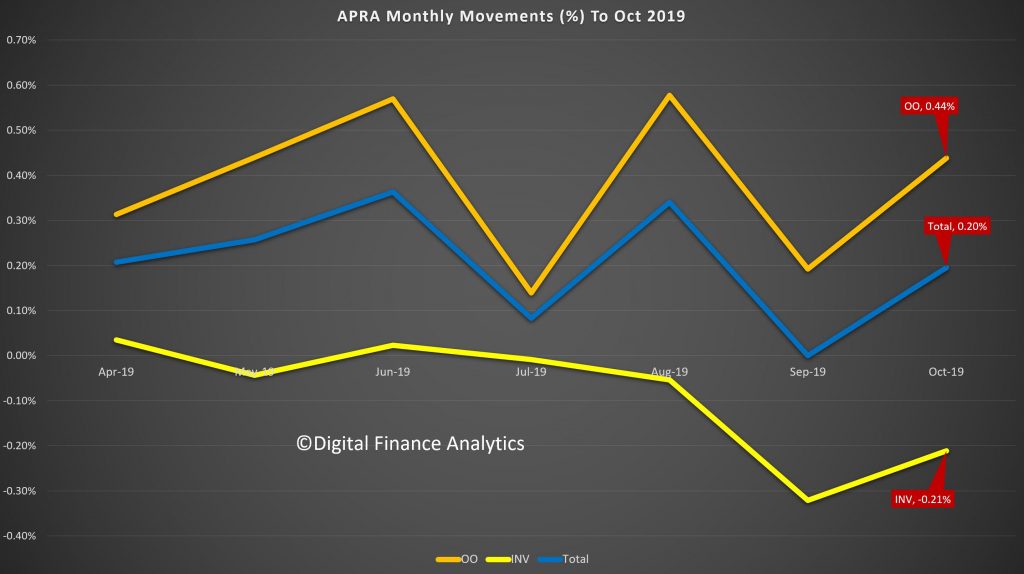

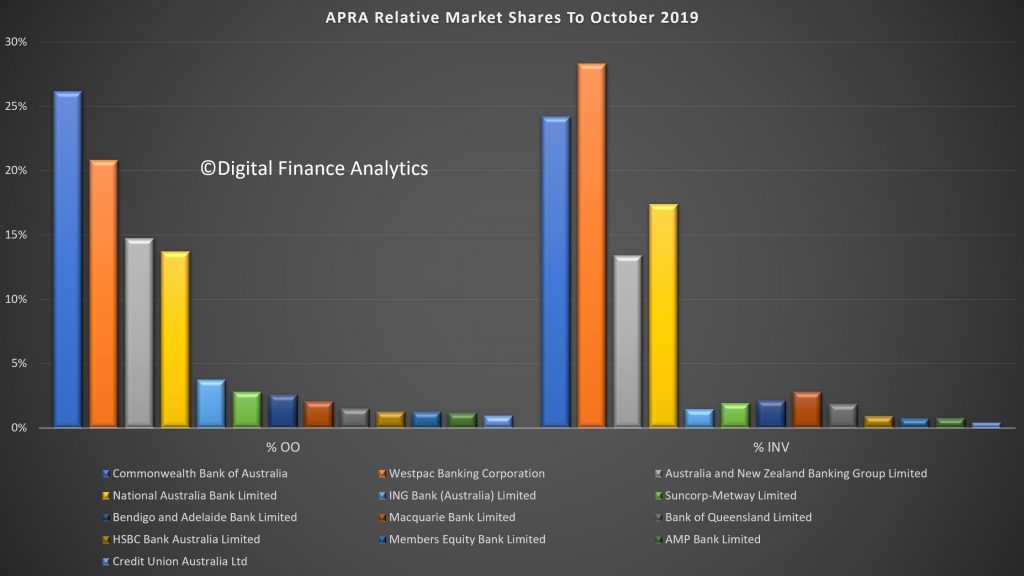

APRA’s new data series continues to contain some surprises. Total lending stock by the banks rose to $1.73 trillion, up 0.2% in the month.

The share of investor loans continues to fall, to around 37.2%, and this is explained by investor loan stock falling by 0.21% in the month, compared with a rise of 0.44% for owner occupied loans. The series still looks a bit weird, so we wonder if there are still reporting issues.

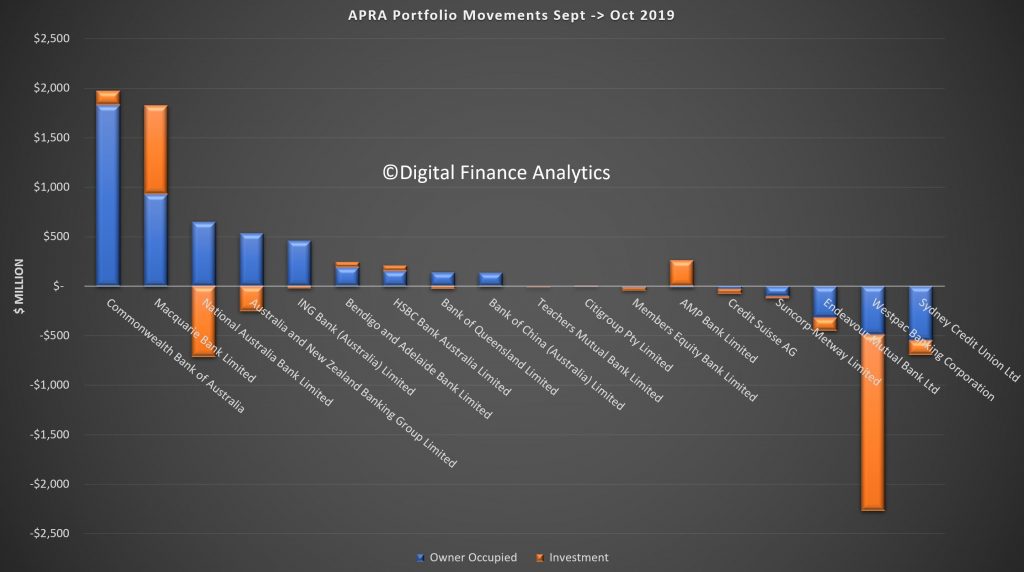

The individual banks stocks of loans varied, with CBA extending their book (consistent with our industry research, as one of the easier lenders at the moment), along with Macquarie – both of which grew both investor and owner occupied pools. NAB and ANZ dropped investor loans, but extended owner occupied loans. But Suncorp and Westpac dropped BOTH investor and owner occupied loan balances (assuming the reporting is correct – lets see if we get a reversal next month).

Finally, market shares hardly changed, with CBA the largest owner occupied lender and Westpac the largest investor loan provider.

Given the weak credit growth, this puts into sharp contrast the reported rises in home prices. We know transaction volumes remain low, but our industry contacts indicate a stronger pipeline of applications. Despite this the run-off of existing loans is translating to low net growth.

Even then, loan growth is still strong relative to income growth. But actually the most significant element is the fall in business credit, as more sectors come under pressure.

These results appear to be at odds with the RBA’s glass half full view of the economy, and may indicate more weakness in the GDP out-turn next week.

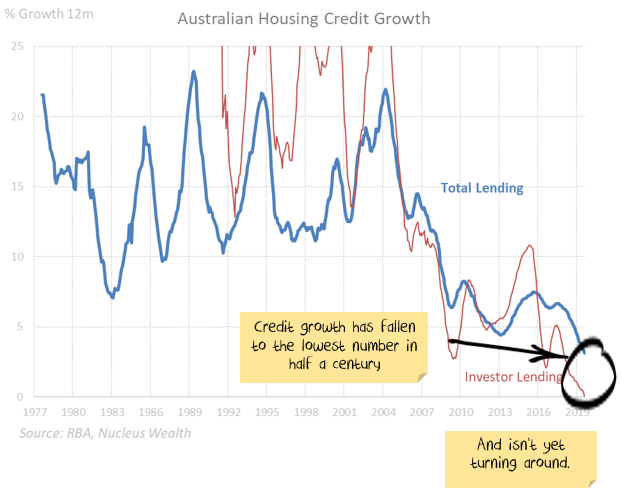

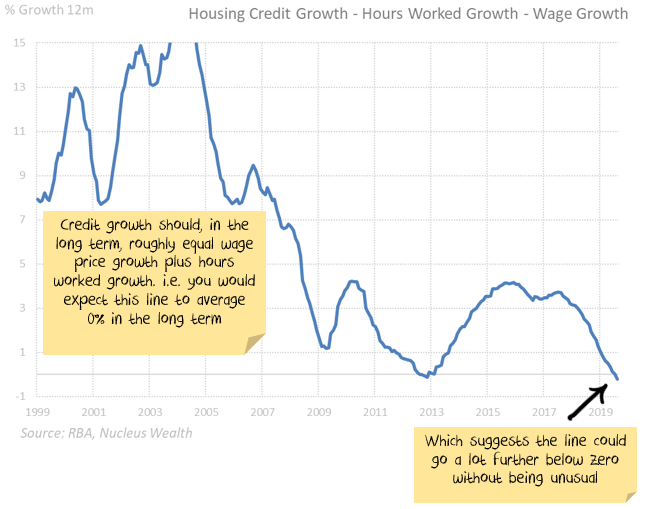

Damien Klassen from Nucleus Wealth penned this recently. It is an excellent summary of the critical issue in play – Can rising house prices drive the rest of the economy on their own without a construction boom? Note the disclaimer below.

I’ve written a few times recently about the imbalances in the Australian economy and how messed up the Australian housing cycle

is. It looks as if the Australian economy is hanging on to positive

growth based on one factor. Without that factor, there is significant

economic downside. The one economic question that matters:

Can rising house prices drive the rest of the economy on their own without a construction boom?

There are three main areas to indicate if this is the case. Two have come out with more negative data since I last posted. One is a glass half empty: better current conditions, worse future conditions.

Upside Case

Can rising house prices drive the rest of the economy on their own without a construction boom?

For

the optimists, the answer is a resounding yes. House prices have not

only stopped falling but have risen over the last few months. Buyer

queues are out the door for limited supply which will inevitably mean

rising house prices. And Morrison’s 95% lending for first home buyers

hasn’t even begun yet. Investors will follow first home buyers, which

will lead prices higher and then upgraders will start buying again.

Rising property prices will mean consumers will start spending once

more, construction will recommence, and a new Australian economic growth

cycle will begin.

It would appear that the Federal Government has this belief.

Downside Case

Can rising house prices drive the rest of the economy on their own without a construction boom?

The

poorer arguments mounted by pessimists tend to have a moral angle:

house prices are too high for children to afford, they will have to come

down to a level that an ordinary person on a regular salary can afford.

If that occurs, house prices will fall 30-40%. While these arguments

are compelling from a social justice perspective, or on a long term

basis, the same arguments have been valid for 15 years. Timing is

important:

Other

weak arguments base the downturn on extrapolating no intervention from

governments. We know the current government is hell-bent on intervening

in the housing market.

The

better argument is that even if construction approvals rebound,

employment would fall for at least another year as the construction

decisions made over the past two years affect the number of people

employed. And construction approvals are not rebounding.

Rising

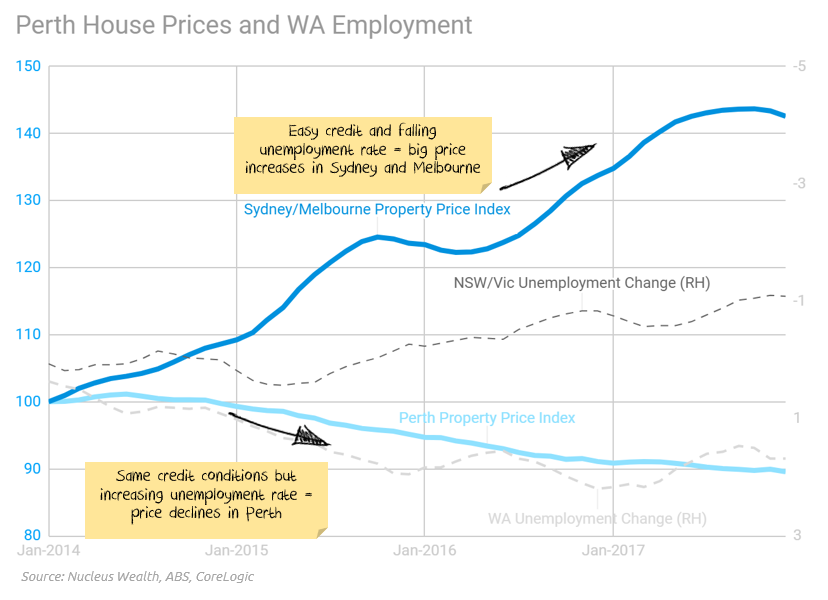

unemployment in Perth led to a 10% house price fall in the 2012-2017

period while Sydney/Melbourne house prices boomed. What is to stop the

same fate for Australia as a whole?

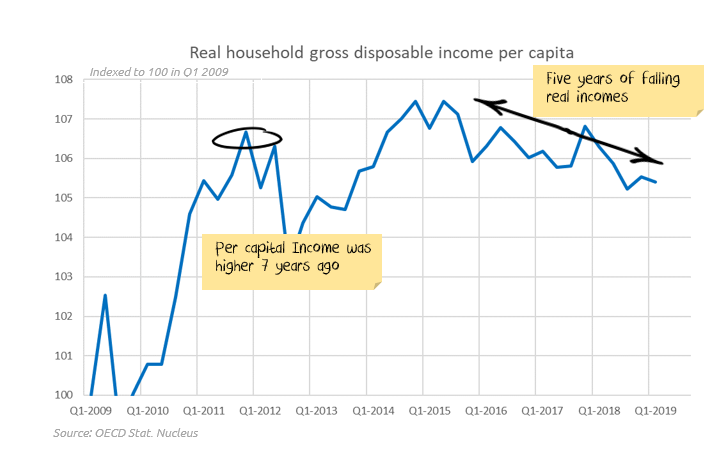

Per capita income has gone nowhere for 7 years, so it is hard to see any rescue coming from that front:

If

rising unemployment does mean house prices fall further, then there are

a range of probable adverse effects. There are some seriously negative

economic effects if the effects snowball. And we won’t even get started

about the impact on a fragile Australian housing market if an

international shock (Brexit, Trade wars, Hong Kong unrest, corporate

debt accidents, European recession) hits.

It doesn’t need to be one or the other

You

don’t need to buy into the entire negative story to be cautious. If

employment holds up, then the positive story has a chance (assuming

benign international conditions). But, if unemployment rises, then

Australia won’t need a global shock to see house prices resume a

downward path.

When

presented with an asset class that has limited upside in positive

scenarios and significant downside in adverse scenarios, I usually opt

to avoid the asset class and look for returns elsewhere.

Update 1: Australian Credit growth:

The

Royal Commission into banking reversed the credit boom and was enough

to see house prices down around 10%. This came even while most other

factors affecting house prices were still positive.

Will

the Morrison government manage to get the already over-levered

Australian households to take on even more debt? If I am too bearish,

particularly in the short term, this is where you will see the effects.

So far there are none:

On

the regulatory front, the Westpac v ASIC responsible lending court case

win for Westpac has the potential to lead to easy lending conditions.

ASIC is taking the case to the Federal court, so we are in limbo for

some time.

Update 2: Unemployment

There

is not enough space here to go into the detailed links between house

prices and unemployment. Indicatively, during the 2012 to 2017 housing

boom years, the Perth market faced mostly the same factors as

Sydney/Melbourne except for (a) slightly weaker population growth and

(b) rising unemployment. And Perth property prices fell more than 10%

while the rest of Australia boomed.

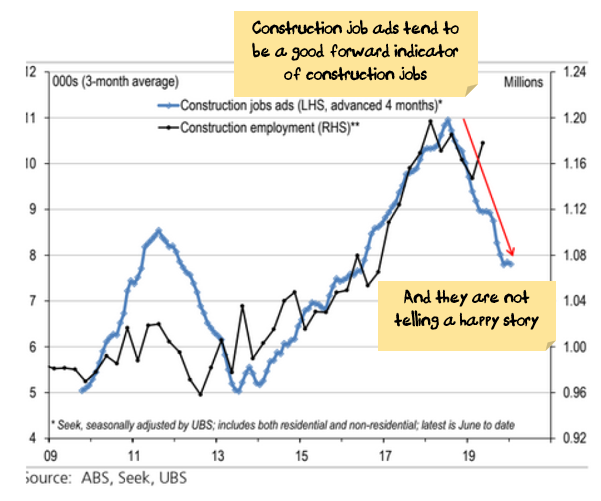

We are expecting considerable job losses in the construction sector.

Having

said that, construction jobs have been resilient so far. Forward

indicators (job ads and approvals) continue to point to sizeable job

losses.

Source: ABS, Seek, UBS

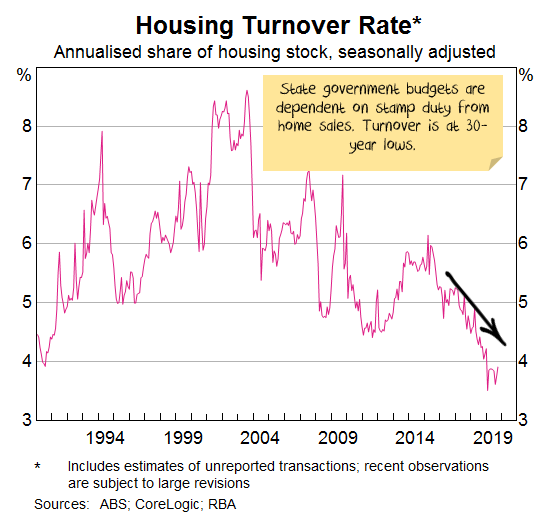

Add

to this scenario, job losses from state government austerity as budgets

have been struck by falling transaction numbers in the housing market:

Finally,

any global shock (trade wars, recessions, debt crises) is likely to be

transmitted to the housing market through higher unemployment.

Update 3: Foreign Buyers

Foreign demand was substantial for both the boom and the bust:

China

cracking down on its capital account and deteriorating relations

between Australia and China suggests foreign investment will remain low.

The question is whether Hong Kong unrest translates to increased demand for Australian property.

The Answer

So, the answer to the one question

Can rising house prices drive the rest of the economy on their own without a construction boom?

will be found in whether increases in unemployment remain contained.

I’m skeptical. But if I’m wrong, the charts above will be where we will see the signs.

Recent data suggest my skepticism is warranted.

Disclaimer

This blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Nucleus Advice Pty Ltd – AFSL 515796.

Broadcast on Thursday 28th November 2019, Nucleus Wealth’s Head of Investment Damien Klassen, Head of Operations Tim Fuller, and founder of Digital Finance Analytics, Martin North discuss “Australia’s Housing Market Dilemma.”

According to an article in InvestorDaily, RBA Governor Philip Lowe has poured water on the prospects of quantitative easing (QE), saying Australia “shouldn’t forget about fiscal policy” to prevent a recession.

“QE is not on the agenda at this time,” Governor Lowe told at the annual dinner of the Australian Business Economists.

Interest

rates will have to hit 0.25 per cent before the RBA considers QE –

something that economists are predicting by mid-2020. But Governor Lowe

doesn’t think QE will be necessary, saying that the Australian economy

is in a good position and that the RBA will achieve its goals.

“At

the moment, though, we are expecting progress towards our goals over

the next couple of years and the cash rate is still above the level at

which we would consider buying government securities.”

However,

Governor Lowe hinted again that he would prefer the use of fiscal policy

rather than monetary policy to ward off a recession, citing a report

from the Committee on the Global Financial System (CGFS), which he

recently chaired.

“The

report also notes that there may be better solutions than monetary

policy to solving the problems of the day,” Governor Lowe said.

“It

reminds us that when there are problems on the supply-side of the

economy, the use of structural and fiscal policies will sometimes be the

better approach. We need to remember that monetary policy cannot drive

longer term growth, but that there are other arms of public policy than

can sustainably promote both investment and growth.”

Governor Lowe

also said that the willingness of central banks to provide liquidity

could reduce the incentive for financial institutions to hold their own

adequate buffers and create an “inaction bias” from prudential

regulators or fiscal authorities.

“If this were the case, it could lead to an over-reliance on monetary policy,” he said.

The

sentiments about quantitative easing have been echoed by fund managers.

Sarah Shaw, chief investment officer at 4D infrastructure and Chris

Bedingfield, principal at Quay Global Investors have urged the

government to instead allocate investment in infrastructure to create

jobs and boost productivity.

Ms Shaw noted the need to replace

roads, bridges and other structures with better planned

“forward-thinking” infrastructure is high.

“If you think about the

need for infrastructure spend that I’m talking about, if you put a

number on it, it’s maxed at $4 trillion by 2040 of infrastructure

capacity that’s needed,” she said.

“If you think about that and

you’re in an interest rate environment as low as it is today, if you’re

not borrowing to invest in a much-needed infrastructure, then there’s

something wrong.”

She added she looks for companies that are

locking in fixed term bet to invest for future cash flows, because “now

is the time to do it” with the current low cash rate.

“Why shouldn’t countries be doing that?” Ms Shaw queried.

“I’ll

give you an example: China during the GFC, biggest form of quantitative

easing – 35,000 kilometres of high-speed rail. That’s the sort of

quantitative easing that we should be looking at here in Australia.”

VanEck has predicted there will be more rate cuts in 2020.

As discussed with John Adams in our recent post, we did not come away with the same conclusion, and Westpac, for example is forecasting QE will hit during 2020.

Last night, in a much anticipated speech broadcast live on the Reserve Bank’s website, Governor Phil Lowe laid out in very clear terms the circumstances in which the bank would resort to quantitative easing and the way in which it would implement it. Via The Conversation.

Quantitative easing is simply a change in the way it eases monetary policy when the official interest rate approaches zero.

Usually it does it by cutting the so-called cash rate, which is the rate banks pay each other for money deposited overnight.

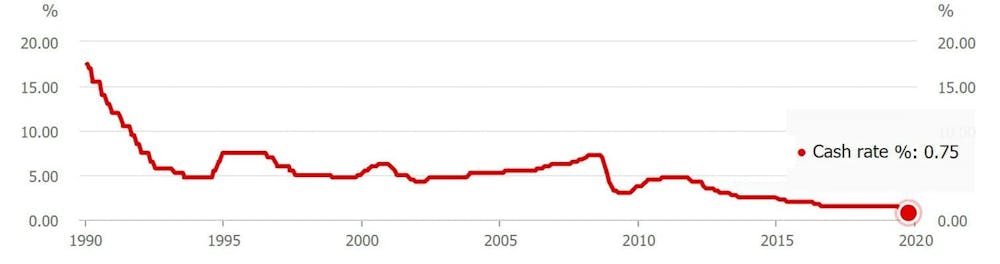

Eight years ago the cash rate was 4.5%. Three years ago it was 1.5%.

After the most recent three cuts in June, July and October, it is just

0.75%

Last night, Governor Lowe said the effective lower bound was 0.25%.

Rather than let the cash rate get any lower or negative (an option he

explicitly ruled out), the bank will push down other longer-term rates

by buying government bonds.

It’s the “quantitative easing” approach adopted by the US Federal Reserve between 2009 and 2014.

Government bonds are sold by governments in return for money, a means

of borrowing. The buyer gets guaranteed interest payments and a

guarantee that their money will be returned in full after three, five,

ten or even 20 years depending on the length of the bond.

Once issued, bonds can be traded on a market, and the price at which

they change hands can be expressed as an implied interest rate, which

becomes the risk-free rate against which all other interest rates are

benchmarked.

How quantitative easing would work

Buying bonds from investors would push down that risk-free rate, pushing down the entire structure of long-term interest rates.

All other things being equal, this should also push down the exchange

rate by reducing the return on Australian dollar denominated financial

investments.

Governor Lowe indicated he might buy state government bonds as well as Commonwealth bonds.

Importantly, he argued that although the bank would be mindful of the

need to ensure private banks had enough access to the bonds they needed

to hold for regulatory purposes, those holdings would not be an

impediment to quantitative easing.

He ruled out buying residential mortgage-backed securities and other

private assets given that those markets are currently functioning well

and Reserve Bank purchases could distort them.

The approach borrows heavily from the US Fed.

As in the US, Lowe says quantitative easing would be complemented by

“forward guidance,” where the Reserve Bank would signal early how

long-term interest rates would be kept low and the circumstances in

which it expected to raise them again.

The guidance is designed to influence market expectations for future

interest rates, enhancing the effectiveness of cuts in long term

interest rates.

When it would happen

In addition to “how,” Governor Lowe spelled out “when” – the economic

circumstances in which the bank would resort to quantitative easing.

It would do it when the cash rate was at 0.25% and inflation and unemployment were moving away from its objectives.

The bank targets 2-3% inflation on average over time and has recently

identified 4.5% as the “full employment” unemployment rate.

Importantly, Lowe emphasised that the Australian economy has not yet

reached the point where a cash rate as low as 0.25% would be needed and

argued quantitative easing was unlikely to be needed in future.

The cash rate is at present 0.75%. Setting 0.25% as the effective

lower bound gives the Governor 0.5 percentage points left to cut before

implementing quantitative easing.

Implicitly, Governor Lowe is saying that those cuts of 0.5 percentage points will be enough to stabilise the economy.

A pause for a breath at 0.25%

Lowe also indicated the bank would not seamlessly transition to quantitative easing.

He implied there was an additional hurdle or threshold that would

need to be crossed, suggesting he would be reluctant to make the

transition.

His big problem is that neither inflation nor the unemployment rate are moving in the right direction.

The bank has undershot its inflation target since the end of 2014,

giving the economy a weak starting point going into an emerging global

downturn.

My research

on the US experience for the United States Studies Centre shows that

the main problem with is quantitative easing was that it was not done

soon enough or aggressively enough.

It might be better to be bold

While quantitative easing was effective, it could have been made more so had what was going to happen been made clearer.

The Fed went out of its way to limit the transmission of quantitative

easing to the rest of the economy, fearful it would be too potent and

lead to excessive inflation.

Those concerns proved misplaced. By pulling its punches, the Fed

ended up being less effective and having to pursue quantitative easing

for longer than if it had used it more aggressively.

Governor Lowe’s very obvious reluctance to go down the quantitative easing route suggests the Reserve Bank is in danger of making the same mistake, but it is not too late to learn from what happened in the US.

Author: Stephen Kirchner Program Director, Trade and Investment, United States Studies Centre, University of Sydney

NAB has announced it will be taking part in the government’s first home loan deposit scheme, operational from 1 January 2020. Via Australian Broker.

The bank has been selected by the National Housing Finance and Investment Corporation (NHFIC) to offer mortgages under the scheme.

“We are proud to be chosen to partner with the federal government and

NHFIC,” said Mike Baird, NAB chief customer officer of consumer

banking.

“Every year our bankers help more than 15,000 Australians achieve

their dream of owning their first home. This scheme is a fantastic way

of helping even more customers, allowing them to potentially save

thousands of dollars on their mortgage.”

The scheme will provide 10,000 eligible Australians per year access

to a home loan with a deposit of as little as 5%. To implement the

scheme, the NHFIC will contract with a panel of selected lenders rather

than having direct contact with borrowers.

Before offering the guaranteed loans, lenders will need to update

their internal systems and train front-line lending staff on how to

apply the scheme eligibility criteria alongside regular considerations,

such as loan serviceability.

The NHFIC has communicated key considerations in its selection of

lender partners includes the loan products on offer, including interest

rates and other fees, as well as the quality of the customer experience.

According to Baird, NAB is the only major to have a special rate for

first homebuyers, which is currently 2.88% fixed for two years. The

major bank also emphasised it will not charge eligible customers higher

interest rates than equivalent customers outside of the scheme.

“We see this appointment as a great endorsement of NAB’s home loan

offering and our support of Australians looking to buy their own home

for the first time,” said Baird.

Before the scheme is live in the new year, customers are able to check their potential eligibility on the NHFIC website.

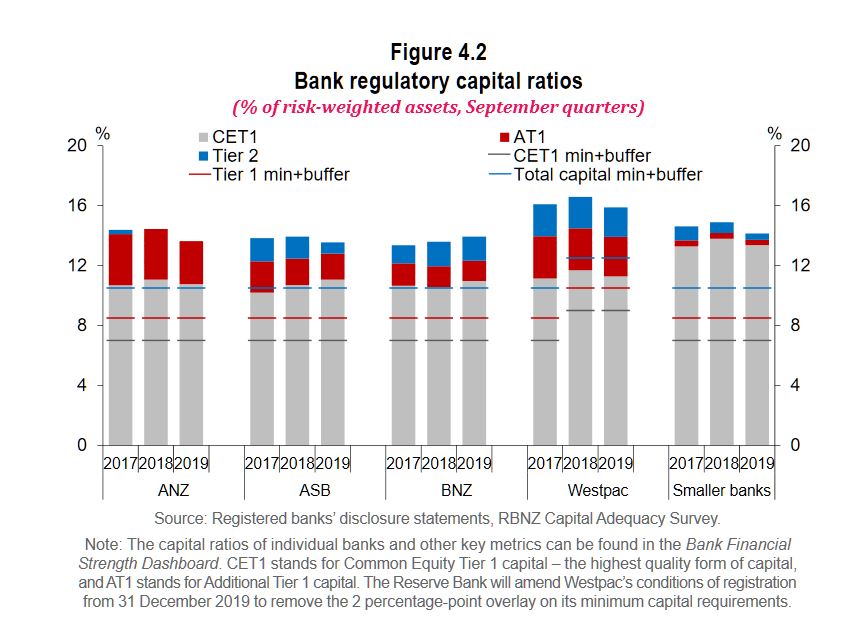

Financial system vulnerabilities remain elevated and more effort is required to ensure that the system remains resilient over the longer-term, Reserve Bank Governor Adrian Orr says in releasing the November Financial Stability Report.

International risks to the

financial system have increased. Global growth has slowed amid continued

uncertainty about the outlook for world trade. This has resulted in reductions

in long-term interest rates to historic lows, including in New Zealand. While

necessary to maintain near-term inflation and employment objectives, prolonged

low interest rates can promote excess debt and investment risk-taking, and

overheat asset prices, Mr Orr says.

Mr Orr noted that the Reserve Bank’s Loan-to-Value Ratio (LVR) restrictions have been successful in reducing the more excessive household mortgage lending, thereby improving the resilience of banks to a significant deterioration in economic conditions.

But, there remains the risk that prolonged low interest rates could lead to a resurgence in higher-risk lending. As such, we have decided to leave the LVR restrictions at current levels at this point in time.

Mr Orr says the Reserve Bank

is committed to bolstering the long-term resilience of the financial system.

“Strong bank capital buffers are key to enabling banks to absorb losses and

continue operating when faced with unexpected developments. The Reserve Bank

has proposed increasing these buffers further with final decisions on the

Capital Review proposals to be announced on 5 December.”

Deputy Governor Geoff

Bascand says good governance and robust risk management processes within

financial institutions are important to maintain long term resilience. Our

recent reviews of banks and life insurers, and the number of recent breaches in

key regulatory requirements, reinforces the need for financial institutions to

improve their behaviour.

“We are engaging with

industry to ensure that they strengthen their own assurance processes and

controls. We have also reviewed our own supervisory strategy and will be taking

a more intensive approach, which will involve greater scrutiny of institutions’

compliance,” Mr Bascand says.

“Some life insurers have low

solvency buffers over minimum requirements. Recent falls in long-term interest

rates are putting further pressure on solvency ratios for some of these

insurers. Affected insurers are preparing plans to increase solvency ratios and

are subject to enhanced supervisory engagement. This highlights the need for

insurers to maintain strong buffers, and insurer solvency requirements will be

reviewed alongside an upcoming review of the Insurance (Prudential Supervision)

Act.”

Governor Philip Lowe spoke at the Australian Economists Dinner last night. In many ways, little new here, but the RBA thinks the zero bounds cash rate is 0.25%, and QE is an option, but only in a crisis. “There may come a point where QE could help promote our collective welfare, but we are not at that point and I don’t expect us to get there”.

He said: As I discussed in the Sir Leslie Melville lecture at the ANU a month ago, low interest rates are not a temporary phenomenon. Rather, they are likely to be with us for some time and are the result of some powerful global factors that are affecting interest rates everywhere.[1]

Given this assessment, it is not surprising that there is a lot of discussion internationally about the

use of so-called ‘unconventional’ monetary policies. People are rightly asking: if

interest rates are going to stay low and be constrained by a lower bound, what other monetary policy

options are there?

I have been part of these international discussions through chairing the Committee on the Global

Financial System (CGFS) at the Bank for International Settlements in Basel. Last month, the Committee

published a report titled: ‘Unconventional Monetary Policy Tools: a Cross-country

Analysis’.[2] The report reviews the experience with the use of unconventional policy tools and

discusses how these tools can be used by central banks to achieve their objectives. If you are

interested in these issues and have not looked at the report, I encourage you to do so.

This evening I would like to summarise some key observations of the report and then explore how those

observations might be applied to Australia.

The CGFS Report – the ‘Unconventional’ Policy Tools

The report discusses four unconventional policy tools.

The term ‘unconventional’ monetary policy has now become the conventional shorthand for a

wide range of policies, although I am not sure it is the best terminology. I say this because most of

these tools have always been in the toolkit of central banks and have been used in one way or another in

the past. What has been unconventional over recent times is the way these tools have been

used.

Negative interest rates

The first of the four tools discussed in the report is negative policy rates.

This is one tool that is truly unconventional.

Prior to the financial crisis, it was widely thought that zero was the lower bound for the policy

interest rate – so it was common to talk about the ‘ZLB’, or the zero lower bound.

It was thought that if interest rates went below zero, people would hold their savings in banknotes

rather than be charged by their bank to deposit their money.

But zero has not turned out to be the constraint that it was once thought to be. So we now talk about

the ELB – the effective lower bound – not the ZLB. While countries with negative interest

rates have seen some shift to banknotes, it has been on a limited scale only. This reflects the use of

bank deposits for making transactions and the fact that most banks in countries with negative interest

rates have set a floor of zero on retail deposit rates. These banks have judged that it doesn’t

make sense, either commercially or politically, to charge households and small businesses negative

interest rates on their deposits.

It is worth pointing out that negative policy interest rates have largely been a European phenomenon.

Policy interest rates have been negative in the euro area, Denmark, Sweden and Switzerland. Rates have

been lowest in Switzerland, at minus ¾ per cent (Graph 1). The only country outside

of Europe that has had negative policy interest rates is Japan, but even there it is only a very small

share of bank reserves at the Bank of Japan that earns a negative rate, at

minus 0.1 per cent.

Graph 1

Extended liquidity operations

The second unconventional policy discussed in the report is the extended use of central bank liquidity

operations.

In response to the financial crisis, many central banks made significant changes to their normal market

operations to deal with strains in financial markets that were impairing the supply of credit to the

economy.

While the specifics differ across countries, the changes to market operations included: expanding the

range of collateral accepted; providing much larger amounts of liquidity; extending the maturity of

liquidity operations; increasing the range of eligible counterparties; and providing funding to banks at

below the cost that was then prevailing in highly stressed markets, sometimes on the condition that the

banks provide credit to businesses and households.

This graph shows the size of the extended liquidity operations of the major central banks

(Graph 2). The biggest operations were during the crisis period of 2008 and 2009, with significant

liquidity support also being provided in 2011 and 2012 to support bank lending during the European

sovereign debt crisis.

Graph 2

It is worth recalling that during these periods of stress, banks had become very nervous about their

access to liquidity. This, in turn, made them nervous about lending to others, making the possibility of

a severe credit crunch very real. By providing financial institutions with greater confidence about

their own access to liquidity, central banks were able to support the supply of credit to the economy.

The CGFS report recognises that there were some side-effects of doing this, but the strong conclusion of

the report is that these measures eased liquidity strains in highly stressed bank funding markets and

helped restore monetary transmission channels to the broader economy.

Asset purchases – quantitative easing

The third policy tool discussed in the report is the outright purchase of assets from the private

sector, paying for those assets by creating central bank reserves – also known as quantitative

easing or QE.

These asset purchases were on an unprecedented scale and led to very large expansions of central bank

balance sheets (Graph 3). Before the financial crisis, the major central banks owned securities

equivalent to around 5 per cent of GDP. In recent years, this has risen to nearly

30 per cent. This is a very large change.

Graph 3

As part of their QE programs, central banks bought a wide range of assets, but the main asset purchased

was government securities. Central banks now hold nearly 30 per cent of government securities

on issue, which is equivalent to around 20 per cent of GDP. The largest purchases have been

made by the Bank of Japan, which holds almost 50 per cent of Japanese government bonds on

issue.

In the United States, the Federal Reserve also bought large quantities of agency securities backed by

the US government. Elsewhere, central banks bought private securities such as covered bank bonds,

corporate bonds and commercial paper. And the Bank of Japan bought equities via exchange traded funds

(ETFs) and real estate investment trusts.

The precise motivations for these asset purchase programs varied across countries, but a common

motivation was to lower risk-free interest rates out along the term spectrum, well beyond the short-term

policy rate. Buying government bonds was seen as reinforcing policy rate cuts and/or acting as a

substitute for further reductions in the policy rate once it was at its lower bound. The expectation was

that lower risk-free rates would flow through to most interest rates in the economy, boost asset prices

and push down the exchange rate.

A related motivation for buying government securities was to reinforce market expectations that policy

rates were going to stay low for a long time. This ‘signalling channel’ added to the

downward pressure on long-term bond yields.

Another motivation in some countries was addressing problems in specific markets. In the United States,

for example, the Federal Reserve purchased government-backed agency securities to support mortgage

markets. And the Bank of England purchased commercial paper to ease highly stressed conditions in

corporate credit markets.

Finally, the expansion of the central bank’s balance sheet through money creation should, in

theory, have stimulatory effects through the so-called ‘portfolio balance channel’. The

idea here is that as the central bank purchases securities with bank reserves, investors seek to

rebalance their portfolios, and in so doing push up other asset prices and lower risk premiums for

borrowers. It is difficult, though, to isolate this effect from the other channels I just spoke

about.

Forward guidance

The fourth policy response was forward guidance.

This took two forms: calendar based and state based. Under calendar-based guidance, the central bank

makes an explicit commitment not to increase interest rates until a certain point in time. Under

state-based guidance, the central bank says it will not increase rates until specific economic

conditions are met. We have seen examples of both in practice. Some central banks also have provided

forward guidance regarding their asset purchase programs.

A primary motivation of forward guidance is to reinforce the central bank’s commitment to low

interest rates. A related motivation is to provide greater clarity about the central bank’s

reaction function and strategy in unusual times. The experience has mainly been positive, with the

guidance helping to reduce uncertainty. There are, however, some examples where a change in guidance

caused market volatility. The ‘taper tantrum’ in the United States in 2013 is an example

of this.

Some Observations

Before I discuss the relevance of all this to Australia, I would like to make three broad observations,

drawing on the report as well as my own reading of the evidence.

The first is that there is strong evidence that the various liquidity support measures and targeted

interventions in stressed markets were successful in calming things down and supporting the

economy.

When markets broke down and became dysfunctional, the actions of central banks helped stabilise the

situation and helped avoid a damaging gridlock in the financial system. They also helped contain risk

premiums in highly stressed markets. It is also worth pointing out that many of the measures to support

liquidity were successfully unwound once the job was done – so they proved to be temporary,

rather than a permanent intervention.

The CGFS report also documents the positive effects of some of the other unconventional measures. In

general, though, I find this evidence less compelling. These various measures certainly pushed down

long-term yields and provided monetary stimulus in the depths of the crisis when it was needed. But

these extraordinary measures have continued way past the crisis period. In some countries, asset

purchases have yet to be unwound and it remains unclear when, and even if, this will happen. So a full

evaluation is not yet possible.

This brings me to my second general observation. And that is that there have been some side-effects of

the various unconventional measures. I will touch on a few of these that the CGFS report discusses.

The first is that the extensive use of unconventional monetary tools can change the incentives of

others in the system, perhaps in an unhelpful way.

It is possible that the willingness of a central bank to provide liquidity reduces the incentive for

financial institutions to hold their own adequate buffers, making episodes of stress more likely in the

future.[3]

It is also possible that the willingness of a central bank to use its full range of policy instruments

might create an inaction bias by other policymakers, either the prudential regulators or the fiscal

authorities. If this were the case, it could lead to an over-reliance on monetary policy.

A second side-effect is the impact on bank lending and the efficient allocation of resources.

Persistently low or negative interest rates and a flattening of the yield curve can damage bank

profitability, leading to less capacity to lend. In some countries, there are concerns that low interest

rates allow less-productive (zombie) firms to survive. There are also financial stability risks that can

come from low interest rates boosting asset prices (and perhaps borrowing) at a time of weak economic

growth.

A third side-effect is a possible blurring of the lines between monetary and fiscal policy. If the

central bank is buying large amounts of government debt at zero interest rates, this could be seen as

money-financed government spending. In some circumstances, this could damage the credibility of a

country’s institutional arrangements and create political tensions. Political tensions can also

arise if the central bank’s asset purchases are seen to disproportionality benefit banks and

wealthy people, at the expense of the person in the street. This perception has arisen in some countries

despite the strong evidence that the various monetary measures supported both jobs and income growth and

thereby helped the entire community.

These are all side-effects we need to take seriously.

The third general observation is that experience suggests that a package of measures works best, with

clear communication that enhances credibility. Exactly what that package looks like varies from country

to country and depends upon the specific circumstances. But clear communication from the central bank

about its objectives and its approach is always important.

The report also notes that there may be better solutions than monetary policy to solving the problems

of the day. It reminds us that when there are problems on the supply-side of the economy, the use of

structural and fiscal policies will sometimes be the better approach. We need to remember that monetary

policy cannot drive longer-term growth, but that there are other arms of public policy than can

sustainably promote both investment and growth.

Application to Australia

I would now like to turn to what this all implies for us in Australia.

I will make five sets of observations.

The first is that the Reserve Bank has long had flexible market operations that allow us to ensure

adequate liquidity in Australian financial markets. We have used this flexibility in the past,

particularly during the global financial crisis, and we are prepared to use it again in periods of

stress if necessary.[4]

At the moment, though, Australia’s financial markets are operating normally and our financial

institutions are able to access funding on reasonable terms. In any given currency, the Australian banks

can raise funds at the same price as other similarly rated financial institutions around the world, and

markets are not stressed. So there is no need to change our normal market operations to do anything

unconventional here. Having said that, if markets were to become dysfunctional, you can be reassured by

the fact that we have both the capacity and willingness to respond. But this is not the situation we are

currently in. Things are operating normally.

The second observation is that negative interest rates in Australia are extraordinarily unlikely.

We are not in the same situation that has been faced in Europe and Japan. Our growth prospects are

stronger, our banking system is in much better shape, our demographic profile is better and we have not

had a period of deflation. So we are in a much stronger position.

More broadly, though, having examined the international evidence, it is not clear that the experience

with negative interest rates has been a success. While negative rates have put downward pressure on

exchange rates and long-term bond yields, they have come with other effects too. It has become

increasingly apparent that negative rates create strains in parts of the banking system that can impair

the ability of some banks to provide credit. Negative interest rates also create problems for pension

funds that need to fund long-term liabilities. In addition, there is evidence that they can encourage

households to save more and spend less, especially when people are concerned about the possibility of

lower income in retirement. A move to negative interest rates can also damage confidence in the general

economic outlook and make people more cautious.

Given these considerations, it is not surprising that some analysts now talk about the ‘reversal

interest rate’ – that is, the interest rate at which lower rates become contractionary,

rather than expansionary.[5] While we take the possibility of a reversal rate seriously, I am confident that

here, in Australia, we are still a fair way from it. Conventional monetary policy is still working in

Australia and we see the evidence of this in the exchange rate, in asset prices and in the boost to

aggregate household disposable income.

My third observation is that we have no appetite to undertake outright purchases of private sector

assets as part of a QE program.

There are two reasons for this. The first is that there is no sign of dysfunction in our capital

markets that would warrant the Reserve Bank stepping in. The second is that the purchase of private

assets by the central bank, financed through money creation, represents a significant intervention by a

public sector entity into private markets. It comes with a whole range of complicated governance issues

and would insert the Reserve Bank very directly into decisions about resource allocation in the economy.

While there are some scenarios where such intervention might be considered, those scenarios are not on

our radar screen.

My fourth point is that if – and it is important to emphasise the word

if – the Reserve Bank were to undertake a program of quantitative easing, we would

purchase government bonds, and we would do so in the secondary market. An important advantage in buying

government bonds over other assets is that the risk-free interest rate affects all asset prices and

interest rates in the economy. So it gets into all the corners of the financial system, unlike

interventions in just one specific private asset market.

If we were to move in this direction, it would be with the intention of lowering risk-free interest

rates along the yield curve. As with the international experience, this would work through two channels.

The first is the direct price impact of buying government bonds, which lowers their yields. And the

second is through market expectations or a signalling effect, with the bond purchases reinforcing the

credibility of the Reserve Bank’s commitment to keep the cash rate low for an extended period.

Currently, the government bond yield curve sits around 20 basis points above the overnight indexed

swaps (OIS) curve, which represents the market’s average expectation of the future monetary policy

rate (Graph 4). Purchasing government securities could compress this differential and could also

flatten the OIS curve through the expectations effect I just mentioned. A lower term premium would lower

borrowing costs for both governments and private borrowers, and would bring the benefits that come with

that. An exchange rate effect could also be expected.

Graph 4

Our current thinking is that QE becomes an option to be considered at a cash rate of

0.25 per cent, but not before that. At a cash rate of 0.25 per cent, the interest

rate paid on surplus balances at the Reserve Bank would already be at zero given the corridor system we

operate. So from that perspective, we would, at that point, be dealing with zero interest rates.[6]

My fifth, and final, point is that the threshold for undertaking QE in Australia has not been reached,

and I don’t expect it to be reached in the near future.

In my view, there is not a smooth continuum running from interest rate reductions to quantitative

easing. It is a bigger step to engage in money-financed asset purchases by the central bank than it is

to cut interest rates.

There are, however, circumstances where QE could help. The international experience is that in stressed

market conditions, the central bank can help stabilise the situation by buying government securities.

That experience also suggests that QE does put additional downward pressure on both interest rates and

the exchange rate. In considering the case for QE, we would need to balance these positive effects with

possible side-effects.

We would also need to consider the effects on market functioning. We are conscious that government

securities play a crucial role as collateral in some of our financial markets. Given the limited supply

of government debt on issue, the Reserve Bank and APRA have already had to put in place special

liquidity arrangements for the banking system. We are also conscious that the Australian

government’s fiscal position means that the gross stock of government debt is projected to decline

relative to the size of the economy over the years ahead. These considerations are not impediments to

undertaking QE, but we would need to take them into account.

It is a reasonable question to ask what might be the threshold to undertake QE in Australia.

It is difficult to be precise, but QE would be considered if there were an accumulation of evidence

that, over the medium term, we were unlikely to achieve our objectives. In particular, if we were moving

away from, rather than towards, our goals for both full employment and inflation, the purchase of

government securities would be on the agenda of the Board. In this world, I would hope other public

policy options were also on the country’s agenda.

At the moment, though, we are expecting progress towards our goals over the next couple of years and

the cash rate is still above the level at which we would consider buying government securities. So QE is

not on our agenda at this point in time.

It is important to remember that the economy is benefiting from the already low level of interest

rates, recent tax cuts, ongoing spending on infrastructure, the upswing in housing prices in some

markets and a brighter outlook for the resources sector. Given the significant reductions in interest

rates over the past six months and the long and variable lags, the Board has seen it as appropriate to

hold the cash rate steady as it assesses the growth momentum both here and elsewhere around the world.

The Board is also committed to maintaining interest rates at low levels until it is confident that

inflation is sustainably within the 2 to 3 per cent target range.

The central scenario for the Australian economy remains for economic growth to pick up from here, to

reach around 3 per cent in 2021. This pick-up in growth should see a reduction in the

unemployment rate and a lift in inflation. So we are expecting things to be moving in the right

direction, although only gradually.

The Board continues to discuss what role it can play in ensuring that this progress takes place and how

it might be accelerated. It recognises the benefits that would come from faster progress, but it also

recognises the limitations of monetary policy and the importance of keeping a medium-term perspective

squarely focused on maximising the economic welfare of the people of Australia. There may come a point

where QE could help promote our collective welfare, but we are not at that point and I don’t expect

us to get there.

As the member of the Executive Board of the Deutsche Bundesbank responsible for cash management, I arguably very much represent what many of you may consider the “”old world of payments””. A world in which there is limited space for innovation and progress. A world that is generally high in risk but low in reward. That is what is often claimed, at least.

In giving you my European and my German perspective, in particular, let me tell you: this case is not as straightforward as it may seem. In Germany and the euro area at large, the circulation of cash remains on the rise. The Bundesbank has issued more than half of the value of euro banknotes currently in circulation. Handling and distributing cash is a major operational task performed by national central banks in the euro area – particularly the Bundesbank. This also means that we need to continue investing in our cash infrastructure.

Cash serves various economic functions – making payments is just one of them. Our estimates suggest that roughly one out of ten banknotes issued by the Bundesbank is used for making payments in Germany. This limits the size of the pie that is up for grabs by the various non-cash payment alternatives.

Let us focus on cash as a payment instrument nonetheless. Usage of cash as a means of payment is declining – this is true both internationally and in Germany. But the level of cash usage is still high in many countries – and especially so in Germany. There may be less cash around, but we are far from being cashless. So why is it that, as of yet, physical cash has not disappeared beneath the waves in the vast ocean of digital payment methods?

2. Cash as an independent means of payment

In my view, this has to do with the special features that cash offers. We regularly monitor payment behaviour in Germany to understand households’ motives for using particular forms of payment over others. Protection against financial loss, personal privacy and a clear overview of spending are crucial features that households expect from payment instruments. Cash scores favourably in all of these areas, according to our surveys. My interpretation of these results: German households value independence – and physical cash offers three unique forms of independence, which distinguishes it from digital payment systems.

First, independence from one’s socio-economic background. Cash is tactile and does not require any technical equipment. The use of cash is easily understood across the generational divide. It is this haptic nature of cash, which, in my view, is an important element of strengthening financial inclusion. Ensuring access to cash may be particularly relevant in rural areas with insufficient banking or technological infrastructures. Cash is, in that sense, also a means of safeguarding social cohesion.

Second, independence from technological ecosystems. Given the still fragmented payments landscape in Europe, cash currently remains the one truly universal means of payment when it comes to P2P transactions in the euro area. Fintech companies are shaking up the traditional banking system in Europe. These companies can often leverage their global reach and huge customer base. This may bring benefits for consumers, for instance regarding cross-border payments. But it also means that customers are becoming locked into particular payment ecosystems. Cash offers an easy way out, at least for certain transactions.

Third, independence from social control and data collection. As legal tender, cash is fully backed by the domestic central bank. Cash is the obvious choice of payment method when it comes to personal privacy. This strengthens individual freedom. At the end of the day, digital payment systems work by using personal data. Collecting data is not harmful per se. But in the age of Big Data, collecting detailed data means obtaining valuable information which, in turn, makes it possible to construct patterns of individual behaviour. From a consumer protection point of view, the question arises as to how much information is necessary to carry out a particular transaction. From an economic point of view, personal data may be seen as an additional source of transaction costs to be factored in when comparing the underlying cost structures of different payment methods.

3. Retailing – the source of future transformations?

Payment methods tend to evolve in stages. For example, the adoption of mobile payment solutions is typically preceded by the widespread use of credit and debit cards. This is the case in Germany, where contactless payments have just started to catch on. China, on the other hand, seems to be a case in its own right. A comparative study in China and Germany supports this. The evidence reported there for the year 2017 suggests that cash and debit card payments account for the bulk of German retailers’ revenue. Mobile-based payment solutions did not play a noticeable role at that time. The reverse picture emerges for Chinese consumers in major cities. Third-party mobile payment providers clearly dominate here, having leapfrogged debit and credit card payments.

Payment habits in China are still in a state of flux as payment technologies continue to evolve. Seamless payment methods are on the rise. These methods essentially try to counter the “pain of paying” with a physical smile. To what extent similar shopping experiences are becoming popular in Germany remains to be seen. There are serious concerns surrounding data protection, and these would need to be alleviated first. In my view, the transition towards a society with less cash has to be driven by the user and not the supplier. It appears that, at least in Germany, consumers value the existing diversity of payment options. Cash continues to be an important part of this. In the bank-centred financial system in Germany, commercial banks are a major actor in the provision of a payment infrastructure that can cater for both cash and its digital alternatives.

Retailing in Germany is transforming, too. On the one hand, German retailers are increasingly turning to Chinese providers of mobile payment solutions, with a particular view to increasing sales to Chinese tourists. On the other hand, retailers have also increased the scope of their activities by closing the cash cycle in Germany. Nowadays, more and more shops are providing basic banking services for their customers such as cash withdrawals and deposits at the counters. To me, this shows that the transformation of the payments landscape is anything but complete.

4 CBDC as a cash substitute?

In the digital era, it should not be surprising that central banks, too, are discussing the potential merits and drawbacks of digital forms of a central bank currency (CBDC). There are currently many operational issues relating to CBDC that remain unresolved. This pertains, for example, to the technology implemented. Blockchains and the underlying distributed ledger technology seem promising, and central banks are open to them in principle. There are several potential use cases in settlement and payment systems, for instance, which are worth exploring further. But handling and safely storing vast amounts of data does not necessarily require distributed ledgers. We need to understand the underlying technologies better in terms of operational risk.

Also, the exact set-up of a CBDC needs to be thought through as the specifications may determine the potential effects. Broadly speaking, there are two conceivable variants of a CBDC. The wholesale type restricts access to CBDC to selected financial market participants for a specific purpose. The retail type, on the other hand, could grant domestic or even non-domestic non-banks access to CBDC on a wide scale.

The wholesale variant may be seen as an improvement on existing structures in terms of processing securities trading and foreign exchange transactions, but it would have little or no effect on monetary policy. The retail variant, however, could potentially mean a paradigm shift in the economic relationships between households, commercial banks and central banks that have evolved to date. uch a fundamental shift is not free of risks, and it requires careful consideration.

There is also the question of how strong households’ appetite for such a form of CBDC would actually be. This user perspective should not be left out in the discussion.

We need to see matters in perspective. After all, many of these debates have been fuelled by the plans announced by the Libra consortium. To me, what this shows, first and foremost, is the need to offer fast and cost-efficient systems for cross-border payments. We should go one step at a time. There are already several innovative market solutions that have the potential to be transformed into an efficient pan-European digital payment solution. In addition SEPA instant credit transfers could serve as a basis for pan-European payment solutions. We should develop these systems further before contemplating further, more radical steps.

5. Conclusion

The old world of payments versus the new world. This story is not new. At the turn of the millennium, there was a strong admiration for what was referred to as the new economy in Germany. New economy was a term used to describe internet start-ups which often relied on little physical capital to generate, at times, staggering market valuations. This was in contrast to the old economy. Think of brick-and-mortar car plants with, in some cases, considerable overheads. At this point, we can say that “”the new has become a bit old and the old has become a bit new””. Economic structures have integrated. The basic market forces still apply: the companies that survive are those that are competitive and offer a unique product. I view the world of payments in very much that spirit. To me, digital payments offer exciting prospects. But that does not necessarily imply the extinction of existing payment methods. It may very well actually increase the diversity of payment methods. Cash offers these unique forms of independence from social and electronic networks, which suggests to me that it will continue to enjoy great popularity in the euro area.