A new UBS report has said that regulators getting tougher on capital is a threat to dividends, particularly those of the major banks. Via InvestorDaily.

UBS

reported that it was cautious on the Australian big four banks as the

low rates environment made it harder for the banks to generate a lending

spread and challenged the return on equity.

“If the housing

market does not bounce back quickly, this could put material pressure on

the banks’ earnings prospects over the medium term, implying that the

dividend yields investors are relying upon come into question once

again,” said the report.

Recent regulatory actions had also not

helped the outlook, with the recent confirmation by APRA that it was

going ahead with its proposal to reduce related party exposure limits to

25 per cent, in a move already impacting one bank’s capital abilities.

ANZ

announced shortly after the confirmation that it would have limited

capacity to inject fresh capital into NZ as its NZ subsidiary would be

at or around the revised limit.

The

$500 million operation risk change for ANZ, NAB and WBC would lead to a

16-18 bps reduction in CET1, with Westpac revealing in its third

quarter report that it was running thin on capital, with UBS reducing

it’s CET1 forecast in the bank to just 0.49 per cent, below APRA’s

unquestionably strong minimum.

Of the major banks, UBS estimated

that Commonwealth Bank was the in the best capital position, followed by

ANZ, but both NAB and Westpac were in trouble.

Part of the

capital position of CBA and ANZ was due to asset sales that would boost

sales; however, UBS did note that these divestments had not yet been

completed and there was uncertainty around its settlement.

UBS

said many of these behaviours were due to APRA’s interpretation of the

Murray report that said the regulator should set capital standards that

kept institutions unquestionably strong.

“This recommendation,

which was subsequently accepted by the government, was interpreted by

APRA to mean that the major banks’ level 1 CET1 ratios are at least 10.5

per cent.

“However, we believe that if the Australian banks

(level 1) hold substantial positions in their New Zealand subsidiaries,

which are treated as a 400 per cent risk weight rather than a capital

deduction, then double-gearing of capital brings this ‘unquestionably

strong’ mandate set by the FSI into question.”

UBS said a simpler

test was needed to ensure banks did not become overly reliant on capital

repositioning strategies, which effectively double-counted capital in

Australia and New Zealand.

Until this was done, UBS predicted

that banks would continue to cut dividends and that investors would see

through various strategies to ensure double-gearing did not occur.

“We expect CBA and WBC to join ANZ and NAB in cutting dividends should rates continue to fall.”

There is an interesting paper the Reserve Bank NZ has put out, seeking comments by 31 August. The Future of Cash Use. It was issued in June 2019.

The paper describes the transition to digital alternatives, and explains some of the reasons. But what caught my eye was this section. “All members of society will lose the freedom and autonomy that cash provides, be more exposed to cyber threats, and lose the ability to use cash as a back-up form of payment”. And “other activity in the shadow economy is unlikely to be affected by the disappearance of cash as people find other ways to circumvent the law”.

So two points, New Zealand followers you might want to read the paper, and make a submission – not been much publicity so far.

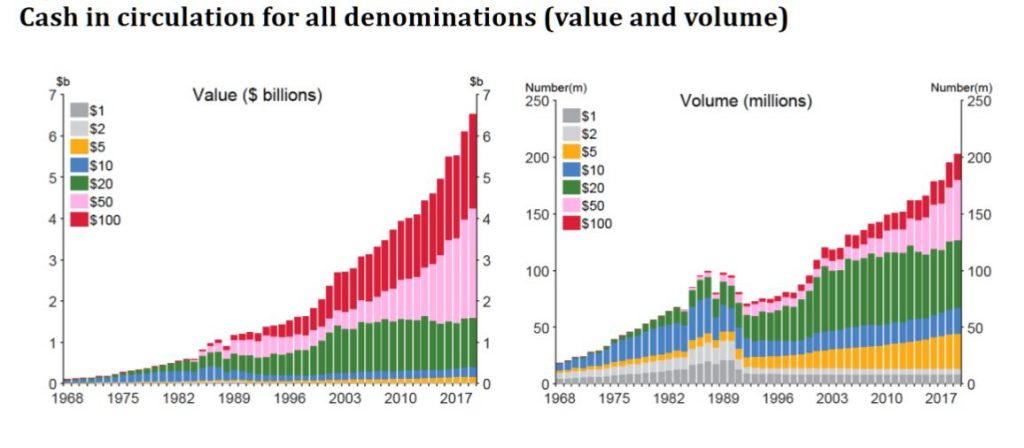

Those following the DFA campaign relating to the War on Cash in Australia, here is more evidence that the proposal to ban cash transactions above $10,000 will not achieve their stated aims – but of course there is a wider monetary policy objective, as we have discussed.

6 Considerations arising from having less cash in society

Given the trends in cash demand and the cost pressures on the

commercial supply of cash in New Zealand, it is possible that cash will

become less widely available or used in the medium to long term. The

effects of less cash in society would be felt more keenly by certain

groups of people who rely on cash and for whom no practicable substitute

exists. The severity of these impacts would be worsened if the

transition to a society with less cash acceptance occured before

mitigating measures could be put in place. Further, the size of the

affected groups might not be large enough to motivate cash providers to

ensure future cash availability, but the size might also not be

negligible.

This section summarises the information in table 1 and Appendix A and

the issues that should be considered if cash use and availability

decline.

Issue 1: People who are financially or digitally excluded could be severely negatively affected.

Cash provides access to the financial system for those who face

barriers to financial inclusion. Further, in a society with less cash,

barriers to digital inclusion could become barriers to financial

inclusion.

Barriers to financial inclusion include limited access to the

banking system due to either a lack of trust in online security, skill

or motivation to use online financial platforms, or banking

restrictions. People who are not banked or have limitations to accessing

the banking system tend to be people without identification and proof

of address, people with convictions, people with poor credit histories,

people with disabilities, illegal immigrants and children.Elderly people

typically rely more than others on cash as a form of payment.

This could be due to low trust in online payments, low ability or

low motivation to learn new payment techniques. People with physical

disabilities, such as sight or intellectual impairments, might also find

cash a useful form of money. Children are also subject to financial

exclusion as banks do not issue debit cards to children under the age of

13. Further, New Zealand banks have full discretion in the customers

they service. This means that some people who do not meet certain bank

policies cannot obtain or keep accounts with those banks. Appendix A

describes additional groups that rely on cash rather than digital money.

Barriers to digital inclusion include insufficient internet

coverage, affordability constraints for technology hardware or data

plans, lack of skills, lack of confidence and low motivation to use

digital platforms. For example, even if people have access to the

internet they might not be motivated to upload personal details to an

online bank account due to privacy concerns.

Issue 2: Tourists, people in some Pacific islands and people who use

cash for cultural customs might be negatively affected if they cannot

use substitutes.

Tourists

Currently most tourists use cash as a reliable and easy-to-use form

of payment. Reserve Bank research has revealed that cash is typically

issued to Auckland and overseas and sent back to the Reserve Bank from

the South Island. This movement is likely due to the movement of

tourists. Many retailers in New Zealand do not accept credit cards (or

contactless payments) due to their higher interchange fees, preferring

instead to accept debit and EFTPOS cards (which require a New Zealand

bank account) that incur much lower costs for the retailers.We

are not aware of the extent to which inbound tourists’ own financial

services’ fees or portability, or their prior understanding of

transacting in New Zealand, influence this behaviour.

As per Appendix A, tourist access to payments in New Zealand could be

met by overseas-issued debit cards if cash were not available. Further,

competition might cause some retailers to accept tourist credit cards

despite higher interchange fees if cash was not available. Bounie et al

(2015) show that higher competitive pressures (the threat of losing

sales) increase the probability that a retailer will accept credit card

payments despite the higher costs.

Even if electronic payment alternatives were reliable, tourists might

be disadvantaged due to language and cultural barriers that create

actual and perceived barriers to payments in New Zealand. Further,

tourists might be particularly vulnerable to risks of robbery or loss

of payment cards if they could not rely on cash as a back-up payment.

Pacific Islands

Niue, the Cook Islands and Tokelau rely on New Zealand banknotes and

coins for their physical currency. The size of these island economies

has been thought to be a contributing factor to their use of New Zealand

currency. In addition, these islands are formally defined as states in

free association within the Realm of New Zealand. New Zealand banknotes

are also used in the Pitcairn Islands.

The Reserve Bank does not have a formal arrangement to supply these

economies with banknotes and coins. The supply of banknotes and coins to

these islands is facilitated by commercial providers, tourists, and

transfers from families. There are no ATMs on Niue and Tokelau. The Cook

Islands has two ATM providers and also issues its own banknotes and

coins. These islands also have access to digital money as in New

Zealand.

Cultural customs

New Zealand’s banknotes have been referred to as the country’s

business card. The designs on the notes represent many of our cultural

icons and contribute to our national cultural identity. Cash is also

used in many cultural customs in New Zealand. Some cultures that use

cash as gifts in traditional ceremonies might find that part of their

cultural identity is lost if they can no longer access cash easily. For

instance:

A Chinese custom is to give cash to junior family members and

friends during celebrations including New Year (Hoong Bouw — giving

money in red envelopes), at funerals, and during tea ceremonies in

traditional Chinese culture.

Some cultures have a wedding money dance where cash is gifted to

the bride and groom as they dance (the Philippines’ Saya ng Pera, and

the Taualuga in Samoa, Tonga and Western Polynesia).

Western cultures give coins to children who lose their baby teeth (Tooth Fairy).

Issue 3: All members of society will lose the freedom and autonomy

that cash provides, be more exposed to cyber threats, and lose the

ability to use cash as a back-up form of payment.

If cash use and availibility were to decline, an issue for all

members of society could be the loss of freedom that cash provides in

terms of autonomous spending and wealth stores, privacy, ability to live

off the grid, and ability to avoid the banking system. This could

result in a significant loss of social freedom in aggregate and

increased cyber security risks (leading to an increase in national

security risks). Lastly, society would lose the benefit of cash as a

‘back-up’ form of payment, although the usefulness of cash in this role

is limited.

Reduced freedom

Cash is anonymous, so provides consumers with autonomy or discretion

in how they choose to spend their money or store their wealth. The

feature of full anonymity creates personal and societal freedom and has

not been replicated in digital currencies. There are three elements in

this freedom; the first relates to the desire for privacy in making

transactions, the second relates to the desire to avoid banks or

government regulation, and the third relates to exposure to cyber-crime.

First, cash payments and balances cannot easily be traced. Central

agents and third parties (such as banks and governments) cannot easily

intervene or stop cash payments outside the banking system. This is a

unique feature of cash and is not fully replicated by any other form of

money. This anonymity gives people full control of and discretion with

their finances. Independent bank accounts could provide personal

freedoms but they are not always available or sufficient. For example,

individuals who are in abusive and controlling circumstances might

benefit from cash as it is easier to obtain and hide when other personal

freedoms are restricted.35

Additionally, people might feel that they benefit from the choice of

using an anonymous form of payment if it were ever needed.

However, the difficulty in tracing cash makes it relatively more

vulnerable to theft, accidental losses and fraudulent payments

(inadvertently accepting counterfeit notes). For this reason, some argue

that people would be better off with a partially anonymous form of

payment, where only the minimum information is given regarding the

identity of the payer and payee in each transaction, but each

transaction is recorded. These payments include, for example, vouchers,

and prepaid gift (debit or scheme) cards.36

Second, the offline and anonymous features of cash enable people to

separate their transactions and stores of wealth from the banking system

and some government interventions. There are legitimate motivations for

this separation.

There is currently no guarantee of the safety of bank deposits in New Zealand.37

Banks take household and business deposits and lend them to borrowers

— there is a risk that borrowers might not be able to service their

debts. Households and businesses could lose their deposits if banks were

engaging in overly-risky lending or if a severe series of events

occurred and many loans were not repaid.

People might also want to remove their savings from the banking

system if the Reserve Bank charged negative interest rates to stimulate

the economy. Cash provides an avenue for people to avoid this form of

government intervention or any other government intervention that might

occur in the future, such as capital controls.

Relatedly, people might want to store wealth outside the banking

system if they have low fundamental trust in banks or the government.

Examples are individuals who have immigrated to New Zealand from

countries where trust in the financial system is low, or where

government appropriations of assets were not uncommon. If there were

less cash in society, individuals would lose their privacy and autonomy

from government in the sense that all their transactions and savings

would be fully traceable if permitted by law.

Third, storing and transacting in cash reduces exposure to

cybercrime, such as financial losses and identity fraud. On a societal

level, New Zealand might be more exposed to cybercrime such as

state-funded cyber threats if it were totally reliant on the banking

system and digital money for all transactions and savings. On a personal

level, some people might prefer to keep their identities and finances

offline due to cyber concerns.

The loss of freedom in society in the above three areas could result

in demand for a form of digital currency issued by the central bank that

replicates some of the autonomy of cash. There are other assets in

which people could store their wealth that are offline and removed from

the financial system, for example, commodity assets and property.

However, these are more difficult to transform into spendable money and

can come with a different set of risks including fluctuating values.

Therefore, people might demand a central bank digital currency that

provides lower traceability than current electronic payments and

accounts and presents an alternative to the banking system. This could

be in the form of accounts with the central bank or tokens issued by the

central bank, which carry a very low risk of default and sit outside

the commercial banking system. A central bank digital currency could

also be designed to provide a low cost form of payment to put downward

pressure on uncompetitive prices in the payment system. Alternatively,

consumers might ask for deposit protection and greater regulation of the

banking system.38

People might also value the freedom and autonomy of cash for

illegitimate reasons. As noted in section 2, cash is used in the shadow

economy to facilitate illegal transactions or as a means to hide income

and reduce tax and other obligations. The International Monetary Fund

estimated New Zealand’s shadow economy at 11.7 percent of GDP in 1991

-2015. 39

It is difficult to assert what might occur in the shadow economy if we

had less cash. At the margin, some shadow economy activities could be

reduced as people consider the additional difficulty of engaging in them

without anonymous payments. For example, some people might be

dissuaded from buying illegal goods and services if they could not avoid

leaving electronic records of their purchases. However, it is also

possible that criminal activity would innovate to other mechanisms or

forms of payment discussed below.

There is debate on whether the anonymity of cash enables crime or

whether illegal transactions would continue without cash. Rogoff (2016)

and McAndrews (2017) agree that, without cash, criminals could use

commodity money (i.e. gold), foreign currency, and inflated invoices.

But they disagree on the extent to which these substitutes would be

used. Rogoff (2016) argues that there is no complete substitute for

cash, so criminal activity would be hindered if there were less cash in

society. McAndrews (2017) argues that inflated invoices would become the

most likely medium of exchange for criminals. He suggests that a

society without cash would likely move towards deeper institutional

corruption of businesses as criminals launder money obtained from

illegal transactions. He also warns that innocent businesses could find

themselves forced into money laundering as criminals look for businesses

to issue inflated invoices.

Issue 4 considers how some tax evasion might be reduced by less cash.

Loss of emergency back up

Cash can be a back-up payment mechanism when electronic payment

systems are not in operation or otherwise unavailable. The Reserve Bank

survey on cash use indicated that 37 percent of people held cash just in

case it was needed (i.e. not for immediate transactions). Cash is

particularly useful in case of ‘personal emergencies’, or localised or

short disruptions in electronic payments systems, and after large-scale

events conditional on the availability of retail stores able to accept

it. Figure 2 shows a spike in CIC as a percent of GDP in 1999 that could

be attributed to the ‘Y2K’ uncertainty.

Cash has several limitations in its usefulness as a back-up payment

in case of large-scale events or natural disasters. Because the supply

of cash and most retail operations are reliant on electricity and

communications, IOUs between small groups or people who are known to

each other might be more effective in periods of long electricity

outages such as those that occur in natural disasters. There might also

not be sufficient cash infrastructure capacity to meet a national

transition to cash in an emergency.

In addition, the National Risk Unit does not recommend including cash

in a civil defence kit or give guidance on the best means of payment in

a national disaster response period. This could be because people

already have their essentials in their civil defence kits, retail stores

might not be operating, and emergency responders will provide

additional supplies. In the weeks following the Christchurch February

2011 earthquake, public demand for cash did not increase substantially.

Commercial banks anticipated an increase in demand for cash and

increased their stores of cash and set up temporary ATMs based on

generators. However, the bulk of these cash stores returned to the

Reserve Bank relatively quickly. Figure 2 shows CIC did not peak as a

share of the population during 2011.

Issue 4: On balance, there would be limited effects on budgeting, financial stability and government revenue.

Transitioning to a society with less cash does not significantly or

negatively affect household budgeting, financial stability and

government revenue.

Budgeting

Cash is widely cited as a budgeting tool. Psychological studies show

that paying in cash incites a higher psychological pain of parting with

funds. This is because the tangible nature of cash results in high

transparency of payments and so generates a greater awareness of

spending.40

This greater ‘pain of paying’ encourages less spending and is useful

for managing discretionary spending, but it could reduce willingness to

pay bills or debt. Shah et al. (2016) suggest that consumers should

automate their essential payments and savings using online banking then

spend disposable (leftover) income using cash. Cash might also be useful

for limiting spending when people need to keep money separate for other

purposes.

People who prefer to use cash for budgeting might benefit from new

electronic budgeting tools such as budgeting applications on mobile

phones. For example, several banks in Dubai provide real time balance

updates or notifications every time money is spent, replicating the

relatively high ‘pain of paying’ that cash provides.

Cash is not the only nor the most important budgeting tool available

for people with low or no disposable incomes, high debts, overspending

habits, or poor mental health. For these groups, commonly cited

budgeting tools include awareness and education, direct credits,

multiple bank accounts, and removing overdrafts and credit. Cash is used

for people who are in full financial management in a Total Money

Management programme as they are allocated their weekly spending in

cash.41

However, the anonymity of cash makes it difficult for budgeting

advisors to identify areas of overspending. Cash also enables people to

default on automatic payments (for bills or debts) as they can withdraw

their full bank account balances into cash. Further, withdrawing money

into cash puts people at a higher risk of robberies than if they did not

withdraw their money. For example, people who withdraw their income

payments from ATMs at night to avoid automatic payments (processed in

the morning) face a risk of robbery, particularly if these habits are

well known in the community.

Financial stability

A society with less cash does not pose a risk to financial stability.

Cash represents a claim on the government and carries low default risk.

In theory, the ability of depositors to convert their savings into cash

represents a form of market discipline on banks that encourages them to

operate prudently. However, there is little empirical evidence to

support this. Engert et al. (2018) evaluate the bank runs during the

2007 – 2008 Global Financial Crisis and determine that cash withdrawals

are a small and unimportant source of market discipline on banks. Shin

(2009) finds that the Northern Rock bank run was triggered predominantly

by wholesale runs, and the in-branch runs to cash were insignificant.

Market discipline is only one form of discipline safeguarding our

financial system. Another form is regulatory discipline. The Reserve

Bank is mandated to use prudential regulation and supervision to

contribute to a stable financial system. The third form is

self-discipline, whereby financial market institutions self-regulate to

ensure their ongoing prudent operation.

The second aspect of stability is payment stability. Migrating from

two payment systems to one payment system would consolidate operational

risk in the single payment system. Greater emphasis would be required

on ensuring the operational reliability of the single payment system if

people could not easily revert to cash if there were a system outage.

Most electronic payments (except cryptocurrencies) rely on the same

back-end payment systems which, exhibit several single points of

failure.42

Increased tax revenue and reduced seignorage

Government revenue could be affected in two ways if cash use and

availability declined. First, removing the availability of notes and

coins might increase tax revenue as businesses would no longer use cash

to reduce their tax bills. The Inland Revenue Department has reported

that the most common ‘hidden economy’ activity is the underreporting of

taxable income, which includes income from cash jobs and transactions.43

Exactly how much tax revenue is lost due to this type of activity is

unknown. A tax working group paper suggests that unincorporated

self-employed individuals under-report approximately 20 percent of their

gross income. This estimate is based on a study commissioned by Inland

Revenue44

and could represent $850 million per annum in lost tax revenue from

unincorporated (non-trust or non-corporation) taxpayers. There is

considerable uncertainty as to the extent to which this number includes

self-employed people who are evading tax by underreporting cash revenue

versus other types of underreporting. It is also not certain that those

reducing their tax burdens by underreporting cash revenue would increase

their tax payments if cash were used less.45

Second, seignorage revenue might decline if the value of CIC declined

significantly. Seignorage revenue is the profit the Reserve Bank makes

from producing and selling cash and investing the profits, as well as

any profit the Reserve Bank makes from financial market trading. 46

The Reserve Bank estimates that it made around $148 million in

seignorage revenue last financial year by issuing cash and investing the

profits.

Other activity in the shadow economy is unlikely to be affected by

the disappearance of cash as people find other ways to circumvent the

law, as described in Appendix A. People who can no longer launder cash

will likely switch to other methods.

As we recently highlighted APRA only looks at loan data not household mortgage data in their analysis. They have now confirmed this again in a piece in their newly released APRA insight 01 2019.

As I have argued before, this myopic view of mortgage land helps to explains the excesses we have seen in the sector, and the lack of effective supervision.

The

Quarterly Authorised Deposit-taking Institution Property Exposures

(QPEX) statistical publication provides bank, credit union and building

society aggregate statistics on commercial property exposures,

residential property exposures and new residential loan approvals. The

QPEX publication is published each quarter on APRA’s website.

In the most recent QPEX publication – March 2019

(issued in June 2019), APRA’s data (as seen in Chart 1) highlighted

negative growth in housing lending over 2018. Between the year ending 31

March 2019 and 31 March 2018, there was a decrease of:

7.2 per cent in owner-occupied new housing loan approvals, and

14.9 per cent in new housing investment loans.

While there has been a decrease in housing loan approvals, the average loan size has continued to grow (as seen in Chart 2).

Since the last QPEX (December 2018) was published, some commentators have misinterpreted APRA’s data in their analysis of the average balance of housing loans. They have assumed that an increase in the number of housing loans (as seen in Chart 2) meant an increase in the number of borrowers with a housing loan. This misinterpretation has resulted in a suggestion that the average balance of housing loans represents the level of indebtedness of Australian households. This conclusion cannot be drawn from the data.

The QPEX publication reports data from the ADI’s perspective (e.g.

the value of loans and number of loan accounts on the ADI’s books)

rather than the borrower’s perspective. The data is a simple average

calculated as the total balance of all housing loans divided by the

total number of housing loans extended by ADIs. In practice, a customer

may have multiple housing loans, which means that the average balance of

housing loans cannot be used to determine the average housing debt of

each borrower. When APRA supervises an ADI, we do not consider the

average loan size to be a reliable indicator of risk; rather the data is

just one of many inputs to identify potential changes to the overall

structure and size of loans.

APRA requires ADIs’ to maintain high lending standards to ensure they

are effectively managing risk when issuing new housing loans to

borrowers. When a borrower applies for a housing loan, APRA requires the

ADI to assess the borrower’s ability to repay the loan, taking into

account the borrower’s other debt commitments and everyday expenses. We

set out our expectations for ADIs on lending standards in Prudential Practice Guide APG 223 Residential Mortgage Lending.

The RBA released their minutes from their last meeting today. What is clear now is the a weakening global economic outlook may make them cut again, not just a weaker labour market – a significant shift, which actually gives them a paper thin alibi in terms of plausible deniability for bad policy! In fact they spun the local economic outlook more positively.

Yet we know they are considering government bond purchases to drive rates lower. QE is coming.

Members commenced their discussion of the global economy by noting that global growth had remained reasonable, having eased since mid 2018. Near-term indicators relating to trade, manufacturing and investment had remained subdued, although consumption growth had been relatively resilient, supported by strong labour market conditions especially in the advanced economies. Despite wages growth having generally trended higher over the preceding few years, inflation had remained below target in a range of economies.

Growth in major trading partners was expected to slow a little in 2019 and 2020. This outlook had been

revised down a little since the May Statement on Monetary Policy in light of the escalation

of the US–China trade and technology disputes and the related weakness in indicators of

investment. Members noted the recent announcement by the US administration of a 10 per cent

tariff to be imposed on a further US$300 billion of Chinese exports to the United States. Further

escalation presented a downside risk to the outlook, particularly if heightened uncertainty weighed

further on business investment. Members noted that investment intentions had already eased significantly

in a number of economies, including the United States and the euro area, and investment had fallen in a

number of economies with a high exposure to international trade, including South Korea.

In China, a range of activity indicators suggested that domestic economic conditions had slowed further

in the June quarter. Further monetary and fiscal stimulus measures had also been announced. Fiscal

support had encouraged investment in infrastructure, while residential construction had continued to

grow relatively strongly, which in turn had supported steel production. The outlook for the Chinese

economy had been revised lower, largely because of the ongoing US–China trade and technology

disputes. Uncertainty about how these disputes would play out and how effective domestic policy measures

would be in supporting Chinese demand continued to be an important consideration for the global growth

outlook and, from an Australian perspective, the future demand for steel and bulk commodities.

The US–China disputes and the slowing in Chinese domestic demand had affected export and

investment growth in the east Asian region. However, exports to the United States had increased for some

economies in the region, including Vietnam, as a result of trade diversion. By contrast, growth in

consumption in the east Asian region had generally remained more resilient. Growth in output in India

had slowed and the outlook was weaker than previously forecast, largely because there had been less

fiscal support and trade tensions with the United States were emerging.

In the major advanced economies, risks to the outlook remained tilted to the downside, reflecting the

trade disputes. The US economy had continued to grow relatively strongly into the June quarter. This was

despite the effects of the trade dispute on the manufacturing sector and on business investment more

generally, partly because tight labour markets had supported strong consumption growth. Members noted

that the most recent round of tariff announcements would affect US imports of consumption goods from

China and could boost US consumer prices to some extent. Further slowing in investment seemed likely as

the effect of earlier fiscal stimulus waned and the uncertainty related to the trade and technology

disputes persisted.

Weaker global trade and greater uncertainty had also affected growth in output in the euro area. Growth

in Japan was expected to be boosted temporarily by spending brought forward ahead of an increase in the

consumption tax in October, although weaker external demand had weighed on export growth.

Commodity prices had generally fallen since the previous meeting, partly in response to the escalation

of trade tensions in early August. After more than doubling in the first half of 2019, iron ore prices

had declined to be below US$100 per tonne. Coal and oil prices had also declined over the previous

month. Rural commodity prices had been little changed. Members noted that the terms of trade for

Australia in the June quarter had been higher than expected.

Domestic Economic Conditions

Turning to the domestic economy, members noted that GDP growth was expected to have been firmer in the

June quarter after three weak quarters. This was partly because resource exports had recovered from

earlier supply disruptions and mining investment was likely to be less of a drag on growth. Partial

indicators suggested that consumption growth had remained subdued in the June quarter; the volume of

retail sales had been subdued and sales of new cars had declined. While dwelling investment was expected

to have declined further in the June quarter, public demand and non-mining business investment were

expected to have continued to support growth.

Members observed that the lower near-term GDP growth forecast mostly reflected the fact that

consumption growth had been weaker than expected over recent quarters. Members noted that consumption

growth per capita had been particularly weak recently. The forecast for GDP growth over 2019 had been

lowered to 2½ per cent. Growth was expected to pick up to 2¾ per cent over

2020 and to around 3 per cent over 2021. This was supported by a range of factors, including

lower interest rates, tax measures, signs of an earlier-than-expected stabilisation in some established

housing markets, the lower exchange rate, the infrastructure pipeline and a pick-up in activity in the

mining sector.

Members noted that although the outlook for consumption remained uncertain, the risks around the

outlook were more balanced than they had been for some time. The low- and middle-income tax offset was

expected to boost income growth, with a surge in the lodgement of tax returns since the end of June. In

addition, signs of a recovery in some established housing markets suggested that the dampening effect of

declining housing prices on consumption could dissipate earlier than had previously been assumed.

The evidence that conditions in housing markets were showing signs of a turnaround had strengthened in

July. In Sydney and Melbourne, housing prices had increased, housing turnover appeared to have reached a

trough and auction clearance rates had risen further. Outside the two largest cities, housing market

conditions had shown tentative signs of improvement; prices had risen in Brisbane, while the pace of

decline had slowed in Perth. Rental vacancies had been low in most cities except in Sydney, where they

had risen further as new apartments were added to the rental stock.

Members observed that it could take some time for the stabilisation of conditions in the established

housing market to translate into a pick-up in construction activity. Indeed, leading indicators

suggested that dwelling investment was likely to decline further in the near term. Residential building

approvals had declined further over May and June and were around their lowest levels in six years.

Timely information from liaison contacts suggested that increased buyer interest had yet to translate

into more housing sales. However, members noted that signs of a turnaround in housing markets suggested

there were some upside risks to dwelling investment later in the forecast period, particularly given the

expected strength in population growth.

Forward-looking indicators for business investment had been mixed. Survey measures of business

conditions had been less positive than a year earlier, especially in the retail and transport sectors,

but generally had remained around average. By contrast, non-residential building approvals had trended

up in recent months and the pipeline of work under way was already quite high. There was also a large

pipeline of private sector projects to build transport and renewable energy infrastructure, which was

expected to support non-mining business investment.

Although mining investment had declined in the March quarter as large liquefied natural gas (LNG)

projects approached completion, the medium-term outlook for mining investment had remained positive. A

number of projects had been committed and others were under consideration, which would add to investment

in coming years if they went ahead. Members noted that the outlook for mining investment had not been

affected by the recent elevated levels of iron ore prices. However, they observed that higher iron ore

prices would add to government taxation revenues and boost household income and wealth through dividends

and the effect on share prices. At the margin, this could provide greater impetus to spending than

currently assumed.

Resource exports had picked up during the June quarter as some supply disruptions to iron ore had been

resolved and LNG production had increased further. Resource exports were expected to contribute to

growth over the forecast period and the recent depreciation of the Australian dollar was expected to

support further growth in service and manufacturing exports.

Members noted that recent labour market data had been mixed. The unemployment rate had remained at

5.2 per cent for the third consecutive month, which was higher than had been expected in May.

However, growth in employment had continued to exceed growth in the working-age population in the June

quarter and had been stronger than forecast in May. As a result, the employment-to-population ratio and

the participation rate had remained around record highs. Over the previous year, there had been a

particularly notable increase in the participation rates of women aged between 25 and 54 years

and workers aged 65 years and over. Members noted that the increase in participation by older

workers had more than offset any tendency for the ageing of the population to reduce aggregate

participation in the labour force. Members discussed some of the factors that could be contributing to

these trends, including slow income growth, improvements in health and greater flexibility in the labour

market.

Leading indicators implied a moderation in employment growth over the following six months: job

vacancies had declined slightly over the three months to May (but remained high as a share of the labour

force) and firms’ near-term hiring intentions had moderated, to be just above their long-run

average. The unemployment rate forecast had been revised higher, with the unemployment rate expected to

remain around 5¼ per cent for some time before declining to about 5 per cent as

growth in output picked up.

Members noted that the outlook for the labour market was one of the key uncertainties for the

forecasts, with implications for growth in wages, household income and consumption. The outlook for

wages growth had been revised a little lower because the outlook for the labour market suggested that

there would be more spare capacity than previously thought. Private sector wages growth was expected to

pick up only modestly, while public sector wages growth would be contained by government caps on wage

increases. Members observed that the outlook for household consumption spending could be weaker if

households expected low income growth to persist for longer.

Members noted that the June quarter CPI had been largely as expected. Trimmed mean inflation had

increased a little to 0.4 per cent in the June quarter, but had remained at

1.6 per cent over the preceding year, consistent with the forecast in May. Headline inflation

had been 0.7 per cent (seasonally adjusted), partly because fuel prices had increased by

around 10 per cent in the June quarter; over the year, headline inflation had also been

1.6 per cent. Overall, members noted that there had been few signs in the June quarter CPI

numbers of inflationary pressures emerging.

Inflation in market-based services had remained steady, which was consistent with a lack of wage

pressures in the economy. Inflation in the housing-related components of the CPI had been around

historical lows. New dwelling prices had declined again in the June quarter, reflecting the use of bonus

offers and purchase incentives by developers to counter the weak housing conditions. Rent inflation had

been flat in the quarter in aggregate, but had fallen noticeably in Sydney, consistent with the rising

vacancy rate; rent deflation had eased in Perth and had been steady in most other cities. Members noted

that low inflation in new dwelling costs and rents, which represent around one-sixth of the CPI basket,

was likely to persist in the near term.

There had been an increase in inflation for retail items because there had been some pass-through of

the exchange rate depreciation and the drought had boosted certain food prices. These effects were

expected to dissipate if there was no further exchange rate depreciation, as is usually assumed in the

forecasts, and once normal seasonal conditions returned. Inflation in the prices of administered items

and utilities had remained well below typical increases recorded a few years earlier.

Inflation was expected to pick up more gradually than previously forecast because of subdued wage

outcomes and the evidence of spare capacity in the economy. The experience of other economies suggested

that any pick-up in wages growth might take longer to translate into inflation than in the past.

Underlying inflation and headline inflation were both expected to pick up to be a little above

2 per cent over 2021, as spare capacity in the labour market declined and as growth increased

to run above potential. Members noted that there were downside risks to some individual CPI components.

In the near term, electricity prices could grow at a below-average pace or even fall, and government

cost-of-living initiatives could weigh on other items in the CPI basket. Inflation rates for both new

dwelling prices and rents were also expected to remain low in the near term, but were more uncertain

towards the end of the forecast period.

Financial Markets

Members commenced their discussion of financial markets by noting that central banks in the major

economies had eased, or were expected to ease, policy settings in response to downside risks to growth

and subdued inflation outcomes. Financial market volatility had increased recently from low levels, in

response to the escalation of the trade and technology disputes between the United States and

China.

The US Federal Reserve lowered its policy rate target by 25 basis points in July. Market pricing

suggested that the federal funds rate was expected to decline by a further 100 basis points or so

over the following year. The Federal Reserve noted that the US labour market had remained strong.

However, it was perceived by members of the Federal Open Market Committee that there was room for some

easing of monetary policy given the implications of global developments for the US economic outlook and

subdued inflation pressures. Elsewhere, the European Central Bank (ECB) had foreshadowed additional

monetary stimulus unless the outlook for inflation in the euro area improved. The ECB indicated that it

could expand its bond-buying program, among other measures, and market pricing suggested that the ECB

was likely to reduce its policy rate over the following months. Market participants were also expecting

the Bank of Japan to ease monetary policy further in the period ahead.

In response to the shift in the outlook for monetary policy, long-term interest rates had declined to

historical lows in several markets, including in Australia. Yields on government bonds were negative

for a number of European sovereigns and Japan. In addition, corporate bond spreads were low globally,

with a growing portion of corporate debt in the euro area trading at yields below zero. Members

discussed the implications of the low level of bond yields for corporate balance sheets and

investment.

Global equity markets had declined sharply prior to the meeting, in response to the recent escalation

of the trade and technology disputes. Nevertheless, equity market indices were still well above their

levels earlier in the year, supported by lower bond yields and expectations that earnings growth would

be reasonable. During July, equity market indices in the United States and Australia had reached record

high levels.

In foreign exchange markets, prior to the meeting there had been an increase in volatility, from very

low levels, in response to the escalation of the trade and technology disputes. In particular, the yen

had appreciated against the US dollar while the Chinese yuan had depreciated. Members took note of

the market commentary that the US and Japanese authorities could intervene in an effort to lower the

value of their currencies. The Australian dollar had depreciated in recent times to be at its lowest

level in many years.

In Australia, the reduction in variable mortgage rates had been broadly consistent with the reduction

in the cash rate in June and July. The degree of pass-through of the cash rate reductions was also

comparable to that observed over the preceding decade. Housing credit growth had declined in June, for

both owner-occupiers and investors. At the same time, however, loan approvals had picked up in June,

which for investors was the first sizeable increase for some time. This was consistent with other

indicators suggesting that the housing market had stabilised over recent months. However, loan

approvals to property developers had remained subdued. Members also noted that access to finance for

small businesses continued to be tight.

Banks’ debt funding costs and borrowing rates for households and businesses were at

historically low levels. Rates in short-term money markets, bank bond yields and deposit rates had all

declined to historically low levels. The proportion of bank deposits that attract no interest had

increased marginally to be just under 10 per cent. Despite the low level of funding costs,

banks’ bond issuance remained subdued. This reflected slow credit growth, along with the banks

increasing their issuance of hybrid securities to fulfil new regulatory capital requirements. Members

also noted that mergers and acquisitions activity had not been especially high, despite funding

conditions being very accommodative for large businesses.

Market pricing implied that the cash rate was expected to remain unchanged in August. A 25 basis

points reduction had been fully priced in by November 2019, with a further 25 basis points

reduction expected in 2020. The low level of bond yields implied that the cash rate was expected to

remain very low for several years.

Members reviewed the experience of other advanced economies with unconventional monetary policy

measures over the preceding decade. These measures comprised: very low and negative policy interest

rates; explicit forward guidance; lowering longer-term risk-free rates by purchasing government

securities; providing longer-term funding to banks to support credit creation; purchasing private sector

assets; and foreign exchange intervention. Members considered the key lessons from the international

experience, noting that a full evaluation could not be undertaken as many of these measures were yet to

be unwound. One key lesson was that the effectiveness of these measures depended upon the specific

circumstances facing each economy and the nature of its financial system. Some measures had been

successful in reducing government bond yields, which had flowed through to lower interest rates for

private borrowers. Other measures had been effective in addressing dislocations in credit supply.

Members noted that a package of measures tended to be more effective than measures implemented in

isolation. Finally, it was important for the central bank to communicate clearly and consistently about

these measures.

Considerations for Monetary Policy

Turning to the policy decision, members observed that the escalation of the trade and technology

disputes had increased the downside risks to the global growth outlook, although the central forecast

was still for reasonable growth. Uncertainty around trade policy had already had a negative effect on

investment in many economies. Members noted that, against this backdrop, the low inflation outcomes in

many economies provided central banks with scope to ease monetary policy further if required. Indeed, a

number of central banks had reduced interest rates this year and further monetary easing was widely

expected. In China, the authorities had taken steps to support economic growth, while continuing to

address risks in the financial system.

Overall, global financial conditions remained accommodative. Long-term government bond yields had

declined further and were at record lows in many economies, including Australia. Borrowing rates for

both households and businesses were also at historically low levels and there was strong competition for

borrowers of high credit quality. Despite this, demand for housing credit, particularly from investors,

remained subdued, while access to credit for some types of borrowers, especially small businesses,

remained tight. The Australian dollar had depreciated to its lowest level in recent times.

Domestically, growth had been lower than expected in the first half of 2019. Looking forward, growth

was expected to strengthen gradually, to 2¾ per cent over 2020 and to around

3 per cent over 2021. This outlook was supported by a number of developments, including lower

interest rates, higher growth in household income (including from the recent tax cuts), the depreciation

of the Australian dollar, a positive outlook for investment in the resources sector, some stabilisation

of the housing market and ongoing high levels of investment in infrastructure. Overall, the domestic

risks to the forecast for output growth appeared to be tilted to the downside in the near term, but were

more balanced later in the forecast period.

Employment growth had been stronger than expected and labour force participation had increased to a

record high. However, the unemployment rate had increased and there appeared to have been more spare

capacity in the labour market than previously appreciated, although there was uncertainty around the

extent of this. The unemployment rate was expected to decline to around 5 per cent over the

following couple of years, consistent with the gradual pick-up in GDP growth. Wages growth had been

subdued and there were few signs of wage pressures building in the economy. Combined with the

reassessment of spare capacity in the labour market, this had led to a more subdued outlook for wages

growth than three months earlier.

In the June quarter, inflation had been broadly as expected at 1.6 per cent. Members noted

that inflation had averaged a little below 2 per cent for a number of years. In the near term,

there were few signs of inflationary pressures building, but, over time, inflation was expected to

increase gradually to be a little under 2 per cent over 2020 and a little above

2 per cent over 2021.

Based on the information available and the central scenario that was presented, members judged it

reasonable to expect that an extended period of low interest rates would be required in Australia to

make sustained progress towards full employment and achieve more assured progress towards the inflation

target. Having eased monetary policy at the previous two meetings, the Board judged it appropriate to

assess developments in the global and domestic economies before considering further change to the

setting of monetary policy. Members would consider a further easing of monetary policy if the

accumulation of additional evidence suggested this was needed to support sustainable growth in the

economy and the achievement of the inflation target over time.

The Decision

The Board decided to leave the cash rate unchanged at 1.00 per cent.

The Australian Prudential Regulation Authority (APRA) has released a strengthened prudential standard aimed at mitigating contagion risk within banking groups. The new rules will come in from 1 January 2021. Until then the 100 or so such operations within a small number of ADIs will remain obscured, with potential higher risks exposure in a down turn.

Such complex group structures could potentially make it difficult for APRA to resolve an ADI quickly and protect depositors’ savings in the unlikely event of a bank failure.

The updated Prudential Standard APS 222 Associations with Related Entities (APS 222) will further reduce the risk of problems in one part of a corporate group having a detrimental impact on an authorised deposit-taking institution (ADI).

Deputy Chair John Lonsdale said APRA began consulting last July on proposed changes to APS 222 to incorporate some of the lessons learned from the global financial crisis.

“Concessions in the existing framework led to some ADIs establishing operations in foreign jurisdictions, which are managed and funded within the domestic bank.

“APRA has only limited visibility of these operations, which also fall outside the purview of foreign regulators. They complicate operating structures and there is no certainty their assets would be available to an ADI if it were to enter resolution. There are currently around 100 such operations within a small number of ADIs.

“Additionally, if an ADI were to fully utilise some of the limits within the existing framework, they would be exposed to excessive levels of contagion risk,” Mr Lonsdale said.

APRA received submissions from 10 stakeholders to its consultation; most supported updating the requirements, however some raised concerns about the complexity of implementing certain proposed changes.

Responding to the consultation, APRA confirmed that APS 222 will be updated to include:

a broader definition of related entities that includes board directors and substantial shareholders;

revised limits on the extent to which ADIs can be exposed to related entities;

minimum requirements for ADIs to assess contagion risk; and

removing the eligibility of ADIs’ overseas subsidiaries to be regulated under APRA’s Extended Licensed Entity framework.

Additionally, APRA will require ADIs to

regularly assess and report on their exposure to step-in risk – the likelihood

that they may need to “step in” to support an entity to which they are not

directly related.

Mr Lonsdale said the stronger APS 222 will enhance the prudential safety of

ADIs and reinforce financial system stability.

“As we saw during the global financial crisis, deficiencies in governance or

internal controls in one part of a corporate group can quickly spread and cause

financial or reputational damage to an ADI. Furthermore, complex group

structures could potentially make it difficult for APRA to resolve an ADI

quickly and protect depositors’ savings in the unlikely event of a bank

failure.

“By updating and strengthening the requirements of APS 222, APRA will ensure

ADIs are better able to monitor, manage and control contagion risk within their

organisations.

“While aspects of the revised standard will have a material impact on some

ADIs, we have adjusted our original proposals in some areas to make the

requirements less burdensome. We are open to considering appropriate transition

arrangements on a case-by-case basis where specific entities request it,” Mr

Lonsdale said.

The new APS 222 will come into effect from 1 January 2021.

The ABC have written a piece on the proposed cash restrictions (even if it was after the closing date for submissions to Treasury relating to the exposure draft). It appears opposition is mounting, given they cite One Nation, CPA Australia, The Institute of Public Affairs and The Australian Chamber of Commerce. However, Chartered Accountants Australia and New Zealand argued the $10,000 cash limit was high, and needed to be lowered.

Australians could face two-year jail sentences and fines of up to $25,200 under proposed laws that limit the use of cash to $10,000 — a move some groups argue would create an Orwellian state by giving authorities greater control over people’s finances.

Key points:

The proposed law would apply to all

payments of more than $10,000 to a business with an ABN, such as buying a

car from a car yard

Private transactions between individuals with no ABN would be exempt from the new rules

One

Nation has indicated it will vote against the bill, as some business

groups argue it is an attack on the basic liberty of free exchange

A number of stakeholders have called on the Federal

Government to withdraw the proposed laws, which were first announced in

the 2018-19 budget as part of measures to fight the so-called black

economy.

The Government’s Black Economy Taskforce had argued a

$10,000 cash limit for transactions between businesses and individuals

would help fight the cash economy by stamping out tax evasion, money

laundering and other crimes.

The

laws would apply to all payments made to businesses with an ABN for

goods or services, affecting major purchases like cars, boats, housing

and building renovations.

The Government has said the measure

would not apply to individual-to-individual transactions, such as

private sales where the seller does not have an ABN, or cash payments to

financial institutions.

The laws, if passed, would take force on January 1, 2020, and for certain AUSTRAC reporting entities from January 1, 2021.

Last week the Judge delivered his verdict in the ASIC-Westpac HEM case, essentially because of the ~260,000 loans examined in the case less than 5,000 would have potentially had their loans tweaked lower if the HEM was not used, whereas the bulk of the loans would have been bigger if HEM was not utilised in the decisioning.

I have now had the chance to speak to a number of industry

players, and most have fallen into expected camps. Lenders in the main welcome

the decision, suggesting that common sense has prevailed, and that ASIC was not

reasonable in its interpretation of responsible lending guidelines. On the

other side, consumer advocates are calling for tighter controls and suggesting

that the HEM benchmarks, even in their revised form are too low – meaning that

households are committed to servicing loans they cannot afford. And ASIC has

commenced a review of responsible lending by years end.

But among my conversations on this topic, I found a sensible and balance view expressed by Fintech CEO Mark Jones from SocietyOne. They of course are on the cutting edge of technological innovation through their lending processes in Australia.

Mark made the point that recently lenders have been raising

their standards, but the question becomes whether a lender has to try and

uncover untruthful declarations from prospective borrowers. In Australia there

is no clear-cut legal obligation of borrowers to be honest and transparent in

their declarations, whereas in the USA there is such a legal obligation, and in

New Zealand a Code of Conduct.

He cited examples where applicants had clearly lied on loan

application forms.

What is the right balance between asking in painful detail

for information from applicants, some of which are unsure of their specific

spending patterns, and the fact that in any case if they take a loan, they may

be capable of “life-style modification”?

So, he sees HEM in the context of the broader loan

assessment processes, with data from applications tested again HEM, and

additional dialogue around other unusual commitments which might include school

fees, alimony, and other elements. This

is all around knowing your customer. And

there needs to be a focus on both discretionary and non-discretionary categories

to give a complete picture.

The systems which Fintech’s like SocietyOne use are more sophisticated and can handle the complex algorithms which reflect real life. Positive credit and now Open Banking, both of which are arriving, are helpful in uncovering critical information. As a result, there are better outcomes for customers. No lenders want to make a loan which is designed to fail! And it opens the door to more sophistication around risk-based pricing

So, in summary, the trick is to get the right balance between getting every scrap of potential data from a customer, thus getting bogged down in the detail but missing the big picture; and applying simplistic ratios which do not provide sufficient precision to spot good and bad business. And it is this balance which needs to be defined in responsible lending, to a level which passes both community expectations and the operational requirements of lenders. To that end, the debate should not really be about HEM at all!

The Treasurer has now (finally) released the proposed timetable for implementation of the recommendations from the Royal Commission made back in February.

It is entitled “Restoring Trust In Australia’s Financial System”, but of course the big question is, will these measures once implemented really get to the heart of the issue – we doubt it.

This is because the final Commission report ducked the critical conflict of interest issue between selling financial services products and delivering them.

There is first the issue of unequal power between a consumer and a financial services organisation.

We know from the Commission that financial services players consistently sought to maximise their returns, even when the best interests of consumers are businesses are voided.

And we know that the general level of financial knowledge and expertise in the community is very low – indeed many do not understand, for example the concept of compound interest, the impact of fees on returns, and even what annual percentage benchmarks really mean.

So, my view is that the RC implementation will not be necessary and sufficient to restore trust in the financial system, even if the large players chose to address their cultural deficits in relation to doing right by their customers. And industry bodies are still fighting rear guard actions to avoid significant change.

Which then takes us back to the weak and compromised regulatory system we have, where APRA and ASIC appear to land more on the side the financial system rather than consumers. So, out of all this, who is minding the back of households and businesses?

In other words Frydenberg’s introduction to this small (14 page) document has a hollow ring to it – or as bankers use to write on bad cheques “words and figures differ!”:

On 4 February 2019, I released Restoring trust in Australia’s financial system, the Morrison Government’s comprehensive response to the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry. In it, the Government committed to take action on all 76 of the Royal Commission’s recommendations and, in a number of important areas, go further. It represents the largest and most comprehensive corporate and financial services law reform package since the 1990s. Of the Royal Commission’s 76 recommendations, 54 were directed to the Government, 12 to the regulators and 10 to the industry. Of the 54 recommendations directed to the Government, over 40 require legislation.

In addition to the Commission’s 76 recommendations, the Government in its response announced a further 18 commitments to address issues raised in the Final Report.

The Government has implemented 15 of the commitments it outlined in response to the Royal Commission’s Final Report. This comprises eight out of the 54 recommendations that were directed to the Government and seven of the 18 additional commitments the Government made as part of its response. Significant progress has also been made on a further five recommendations with draft legislation either introduced to the Parliament, released for comment or detailed consultation papers issued.

The Government’s implementation timetable is ambitious. Excluding the reviews that are to be conducted in 2022, under the Implementation Roadmap by mid-2020, close to 90 per cent of our commitments will have been implemented. By the end of 2020 remaining Royal Commission recommendations requiring legislation will have been introduced.

In this Implementation Roadmap, we set out how we will deliver on the remaining Royal Commission recommendations and additional actions committed to. This will provide clarity and certainty to consumers, industry and regulators on the roll out of the reforms. Of course, the Government’s actions alone will not be sufficient to address the widespread misconduct identified by the Royal Commission. Individual firms must make the changes needed to their culture and remuneration practices to put consumers at the core of their business. I expect industry to also align with the urgency and priority the Government is giving to its implementation task.

The Government will ensure that key firms in the financial sector continue to address the issues identified by the Royal Commission.

At the request of Government, the House of Representatives Standing Committee on Economics will inquire into progress made by major financial institutions, including the four major banks, and leading financial services associations in implementing the recommendations of the Royal Commission. As previously announced, we will also establish an independent review in three years’ time to assess the extent to which changes in industry practices have led to improved consumer outcomes.

The Government is delivering lasting change in the financial sector to ensure public confidence is restored.

Finally, the Australian Banking Association came out with this:

Australia’s banks have welcomed the Government’s timetable for legislative change following the Hayne Royal Commission and will work with the Commonwealth to continue implementing the Commission’s recommendations.

While the forward agenda for the required legislative changes was announced this morning, banks are well down the track of implementing recommendations for which they are responsible to improve customer outcomes and earn back the trust of the Australian community.

Of the Commission’s 76 recommendations, 54 were directed to Government and more than 40 of those recommendations require legislative change. 12 are to be taken forward by the regulators, 10 are for industry to implement – eight of these are specific to the banking industry.

ABA CEO, Anna Bligh said: “Since the Final Report was handed down six months ago, banks have been working to make changes to ensure that the recommendations become part of their operating fabric.

“Make no mistake, banks understand what the community and Government expects of them and are raising their standards to rightly meet those expectations.

“The recommendations included six changes to the Banking Code. All six are underway. The ABA has already drafted provisions implementing five of the changes, had them agreed to by banks and submitted them to the regulators for approval. These are now on track for full implementation by March 2020,” Ms Bligh said.

The sixth change relates to the definition of small business. Consistent with the Commission’s recommendation, the definition was recently changed in the new Banking Code to include businesses with fewer than 100 employees and this measure is now fully operational. The further recommendation to change the financial threshold from $3M to $5M will be subject to a review that will be overseen by ASIC who will examine the potential impacts on the provision of credit to small business. The review is underway and expected to be completed in early 2021.

“In relation to culture within banks, many, including the major banks, have already completed reviews. These banks have also introduced mechanisms for the ongoing tracking of culture to determine whether actions are having the necessary impact. But banks understand that effective cultural change is not going to come about through implementing the Royal Commission recommendations alone. It will only be achieved by putting the customer at the heart of every decision our banks make.

“In addition, all banks continue to review how they remunerate staff, with a focus on good customer outcomes, not just meeting financial targets,” Ms Bligh said.

Following the release of the Final Report, the ABA established a dedicated Royal Commission Taskforce to oversee the industry’s implementation of the recommendations. This Taskforce has met six times over the past six months and will continue to meet regularly to ensure the industry responds swiftly to the Government’s legislative processes and acts to fully implement the recommendations