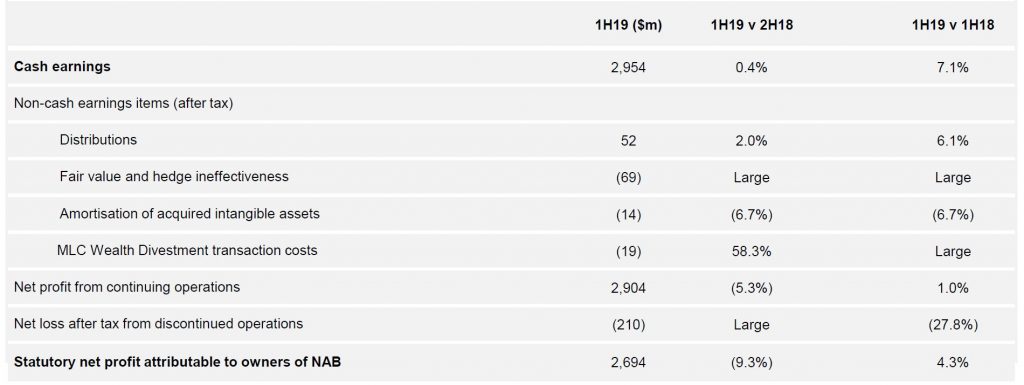

NAB reported their IH2019 results today. The statutory net profit in 1H19 was $2,694 million dollars, which is 9.3% lower compared with the 2H18, but 4.3% higher than 1H18.

Significantly they dropped the dividend to 83 cents per share, a drop of 16.2% compared with 1H18 – this was more than was anticipated by the market. But this is still an annualised dividend of circa 6.4%, compared with CBA and ANZ who are around 5.7%. This will help NAB build capital.

The cash ROE excluding restructuring and customer remediation was down 60 basis points to 13%, compared to ANZ’s 11.7%.

There were a number of one-offs which impacted the cash earnings, (their preferred measure) of $2,954 million, which is up 0.4% from 2H18, and 7.1% from 1H18.

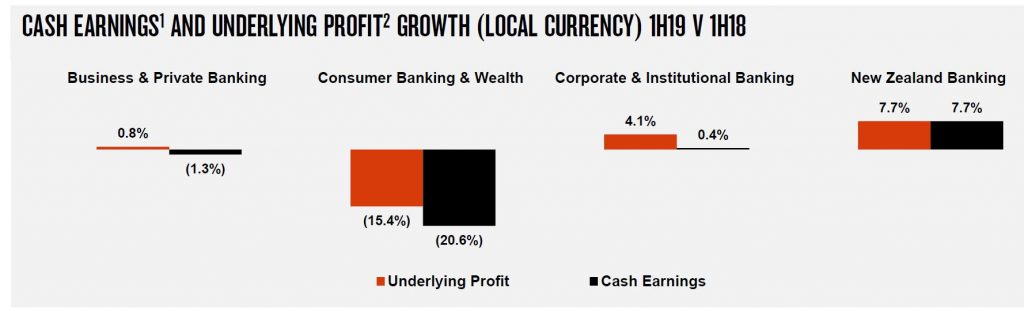

Consumer Banking dropped cash earnings by 20.6%.

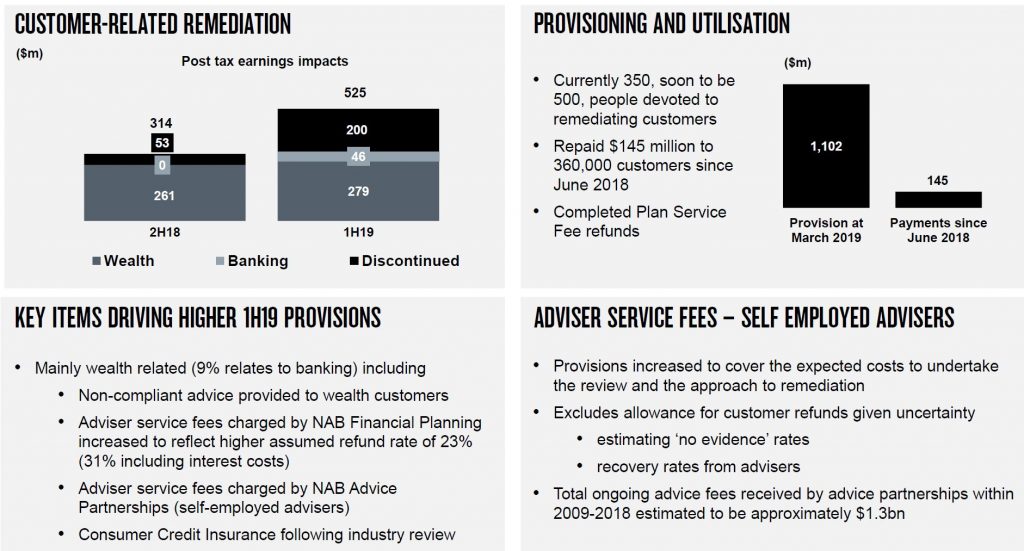

Customer remediation provisions stood at $1,102 million, and they plan to have 500 people devoted to this activity.

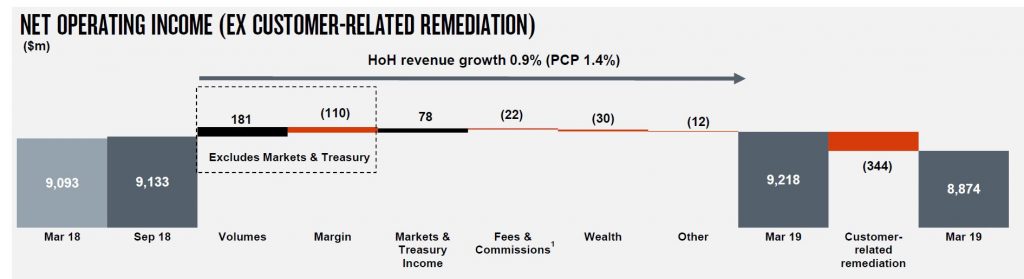

Overall income was higher, thanks to volume, but offset by margin compression of $110 million, a fall in fees and commissions, down $22 million and a customer remediation charge of $334 million, to give a net lower income of $8,874 million.

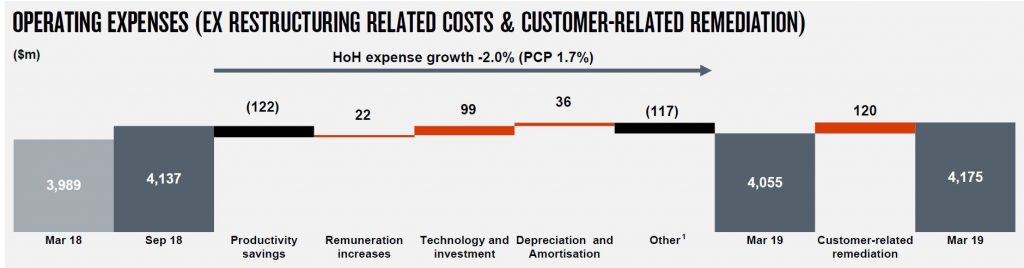

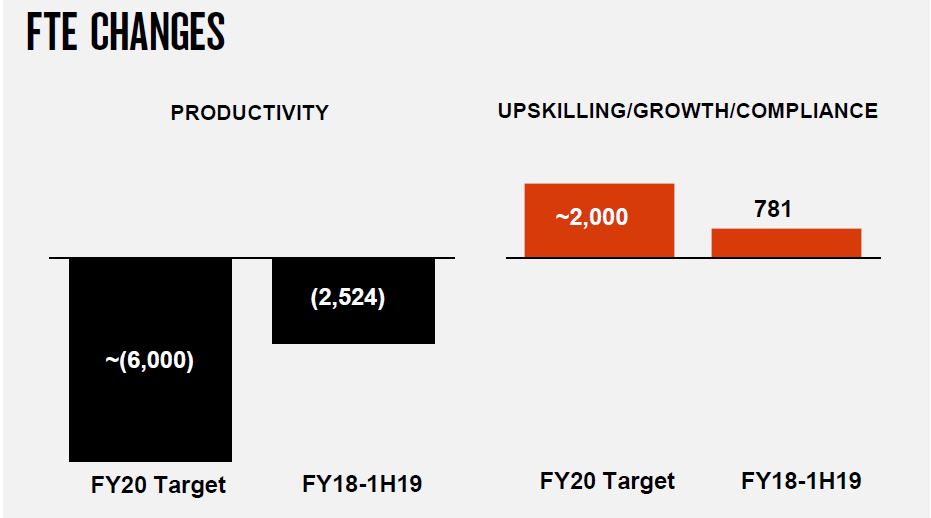

Operating expenses were flat(ish), but total FTE rose from 33,283 in 2H18 to 33,790 in 1H19.

They said that the banks is midway through its 3 year transformation program with additional investment target of $1.5bn, and that cost savings and FTE reduction are broadly on track.

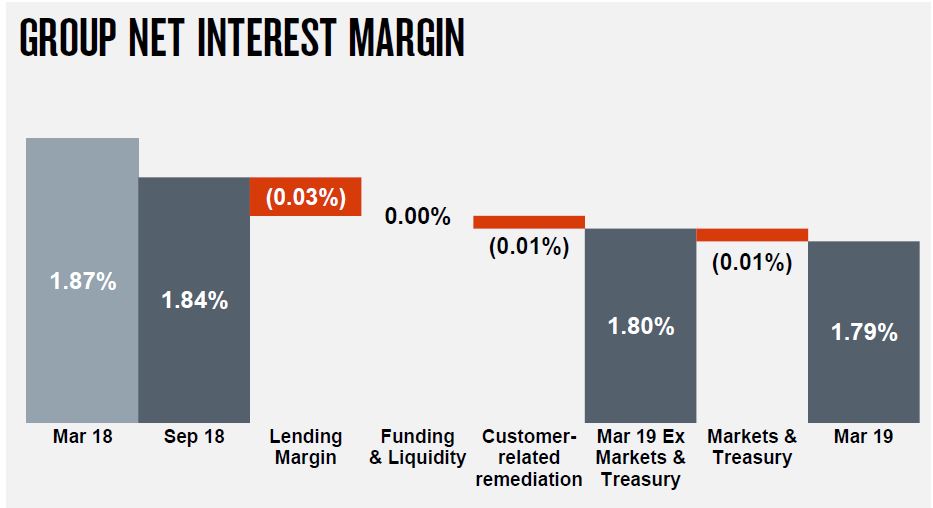

Group net interest margin fell 7 basis points. Of course NAB delayed their Australian mortgage book repricing, and clearly this cost. Corporate and Institutional helped support the result. The subsequent mortgage repricing may help ahead.

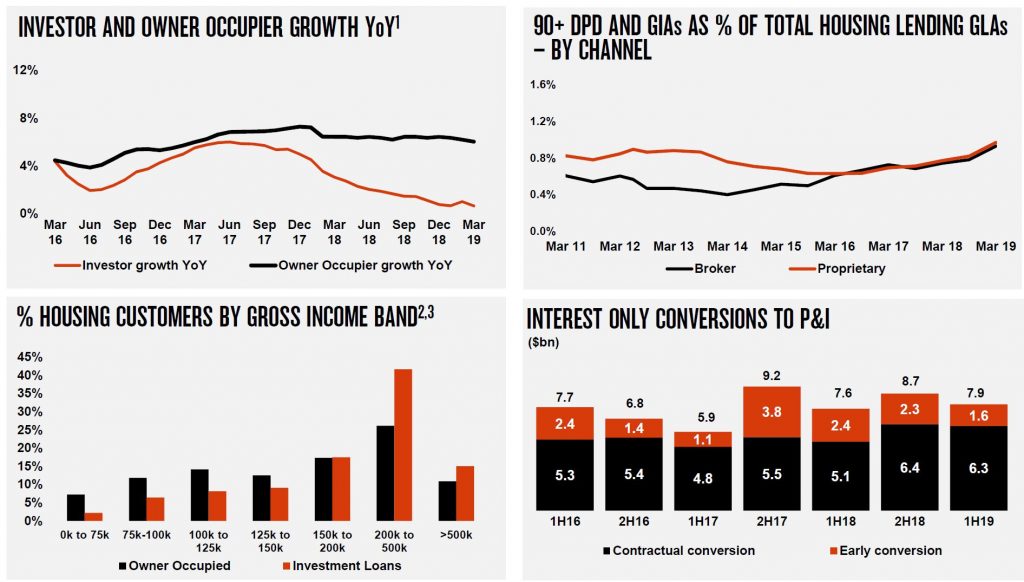

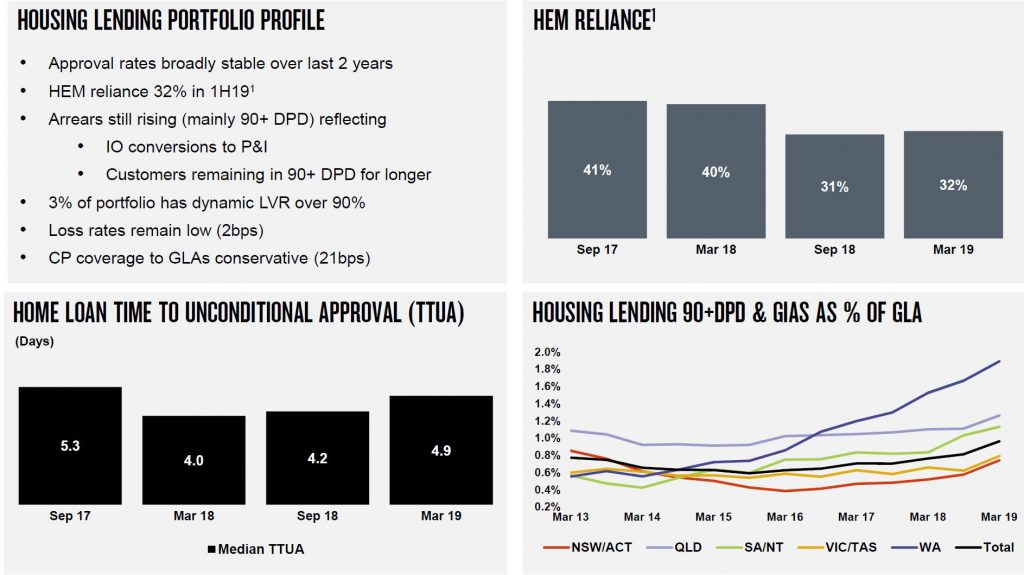

Home lending in Australia shows that approvals rates have remained stable over the past 2 years, and that reliance on HEM has fallen to 32% in March 19, compared with 41% in September 2017.

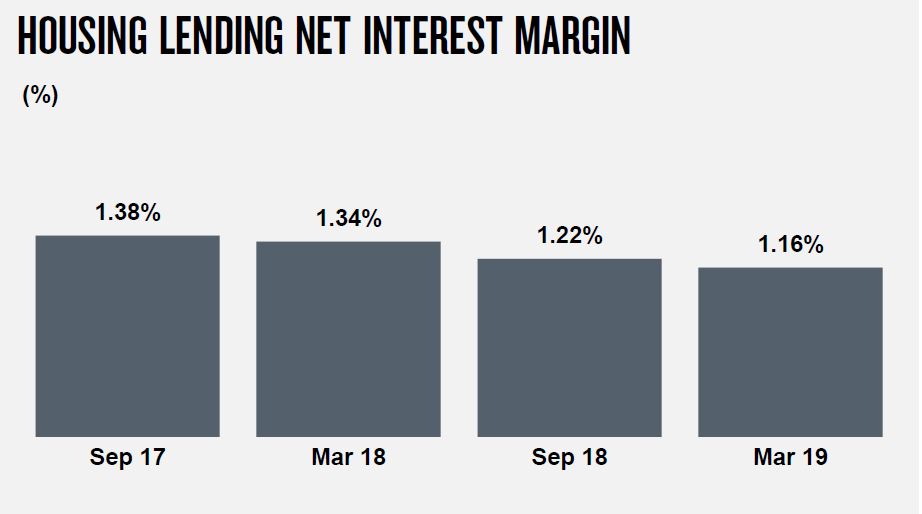

Net interest margin across Australian home loans fell 6 basis points from Sep 18 to Mar 19, and continues the slide from 2017.

Loan growth slowed, especially investor lending, and defaults are similar in both proprietary and broker channels now

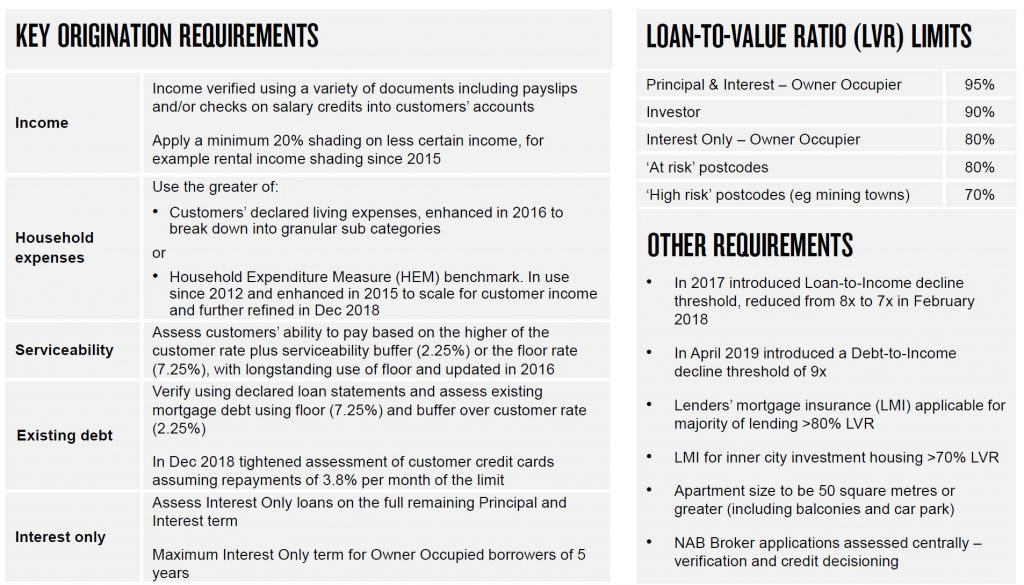

They implemented Comprehensive Credit Reporting (CCR) for mortgages in February 2019 (first major bank to reach this milestone).

Lending standards have become tighter.

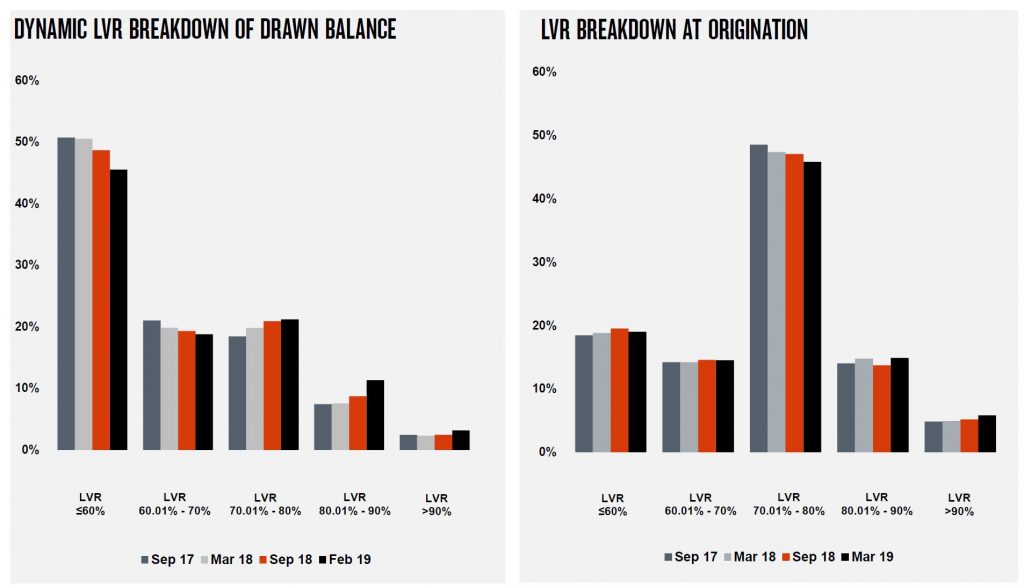

LVR Bands still include loans above 80% (and rising).

Default are rising, with 90 day+ defaults partly attributed to the conversion of interest only loans to P&I. WA has the highest levels, but other states also rose.

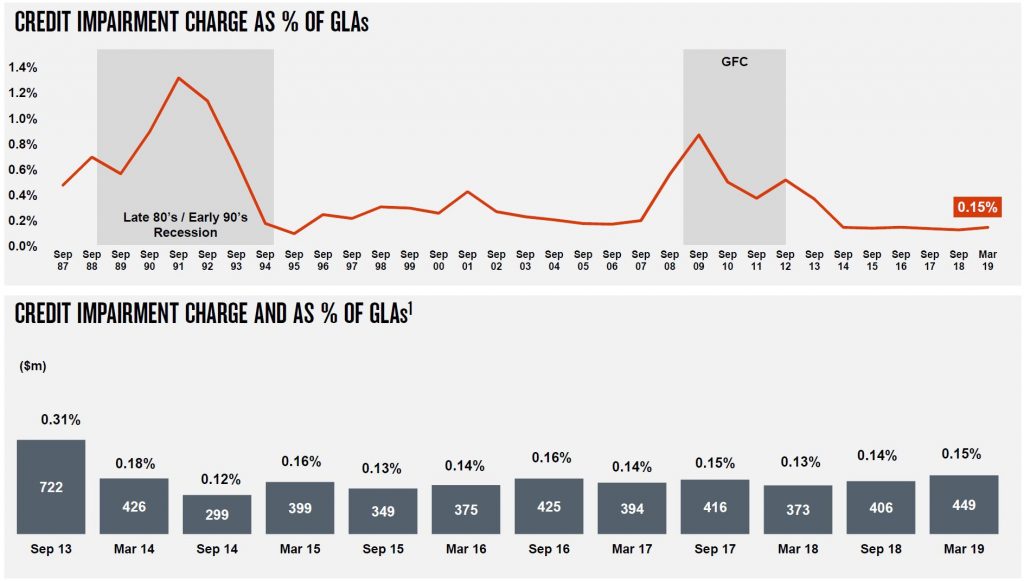

Group credit impairments rose to 0.15% of GLA’s.

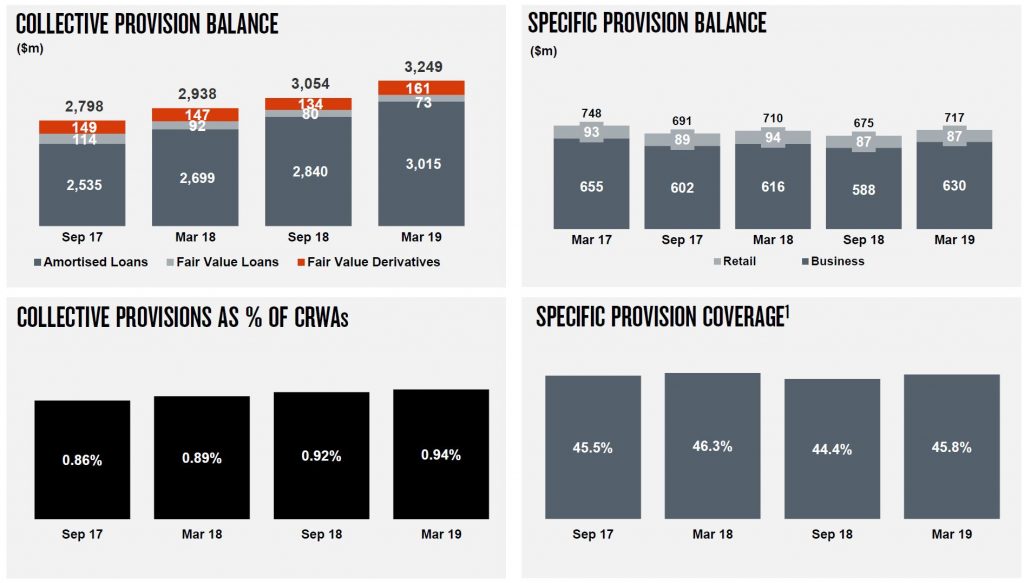

The group provisions are higher, as are the specific provision balances.

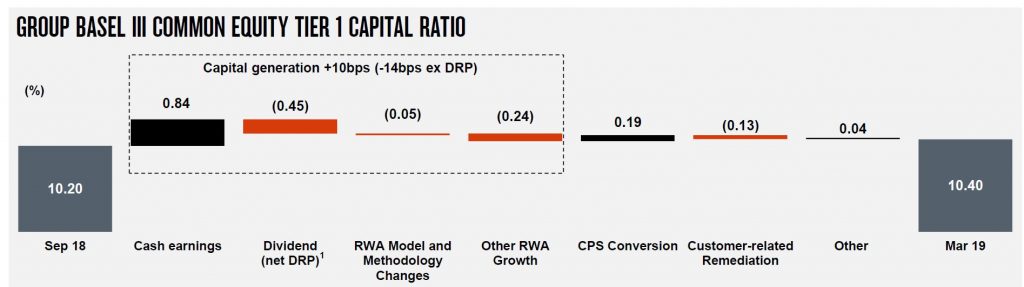

The CET1 ratio is 10.40, up from 10.20 in Sep 18, and they say they are on track for “unquestionably strong”.

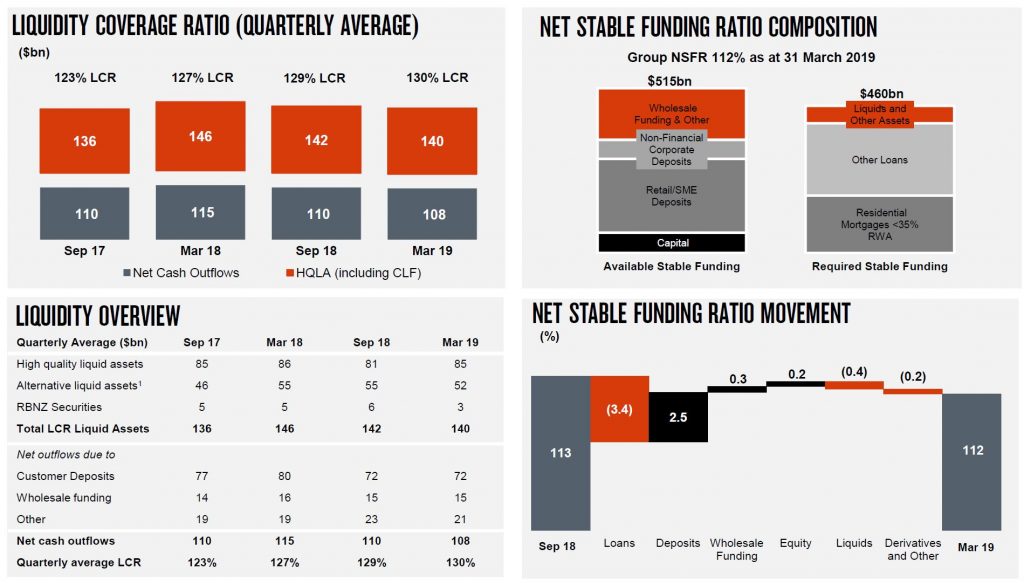

The LCR and NSFR remain strong.

So the underlying franchise still looks in reasonable shape, but the weakening housing sector needs to be watched.

The Fed held their rate (some were expecting a cut), and as a result, markets eased back, while bond yields rose. They underscored the patient approach ahead, but also a willingness to look though low inflation in the nearer term.

The Board of Governors of the Federal Reserve System voted unanimously to set the interest rate paid on required and excess reserve balances at 2.35 percent, effective May 2, 2019. Setting the interest rate paid on required and excess reserve balances 15 basis points below the top of the target range for the federal funds rate is intended to foster trading in the federal funds market at rates well within the FOMC’s target range.

Information received since the Federal Open Market Committee met in March indicates that the labor market remains strong and that economic activity rose at a solid rate. Job gains have been solid, on average, in recent months, and the unemployment rate has remained low. Growth of household spending and business fixed investment slowed in the first quarter. On a 12-month basis, overall inflation and inflation for items other than food and energy have declined and are running below 2 percent. On balance, market-based measures of inflation compensation have remained low in recent months, and survey-based measures of longer-term inflation expectations are little changed.

Consistent with its statutory mandate, the Committee seeks to foster

maximum employment and price stability. In support of these goals, the

Committee decided to maintain the target range for the federal funds

rate at 2-1/4 to 2-1/2 percent. The Committee continues to view

sustained expansion of economic activity, strong labor market

conditions, and inflation near the Committee’s symmetric 2 percent

objective as the most likely outcomes. In light of global economic and

financial developments and muted inflation pressures, the Committee will

be patient as it determines what future adjustments to the target range

for the federal funds rate may be appropriate to support these

outcomes.

In determining the timing and size of future adjustments to the

target range for the federal funds rate, the Committee will assess

realized and expected economic conditions relative to its maximum

employment objective and its symmetric 2 percent inflation objective.

This assessment will take into account a wide range of information,

including measures of labor market conditions, indicators of inflation

pressures and inflation expectations, and readings on financial and

international developments.

ANZ reported their 1H19 results today. Their “shrink to greatness strategy” did work to an extent, but their results were flattered by higher than expected Institutional performance, which offset the pressure on the Australian retail bank from lower mortgage growth and margins, and higher customer remediation costs. They are well capitalised, which is a good thing, given the higher and building mortgage delinquency. They foresee tough times ahead. Tricky times to be a banker.

The results are also muddied by the many business exits and restatements and a significant reduction in staff. But among the big four, they are probably the best placed, but will be hit if mortgage delinquency continues to rise (as we suspect they will) as the Australian economy stalls.

They announced a Statutory Profit after tax for the Half Year ended 31 March 2019 of $3.17 billion, down 5% on the prior comparable period.

Cash Profit for its continuing operations was $3.56 billion, up 2%. The return on equity was 12% compared with 11.9% 1H18, while the return on average assets fell 2 basis points from 0.79% in 1H18 to 0.77% 1H19.

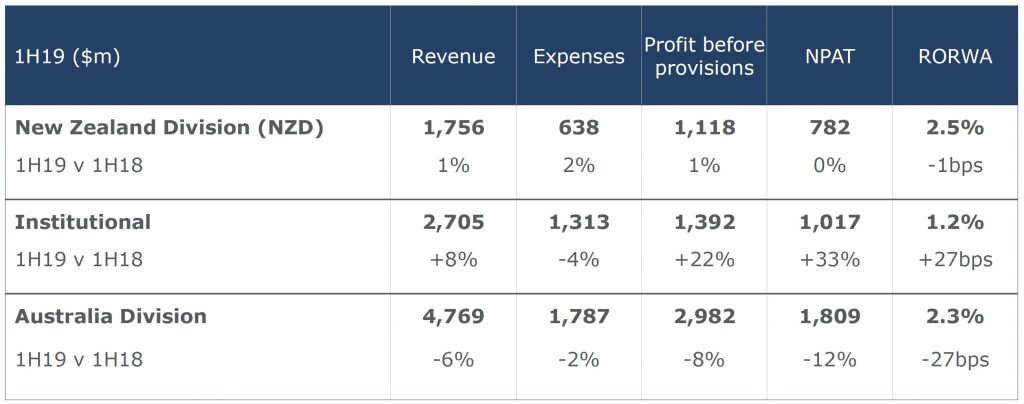

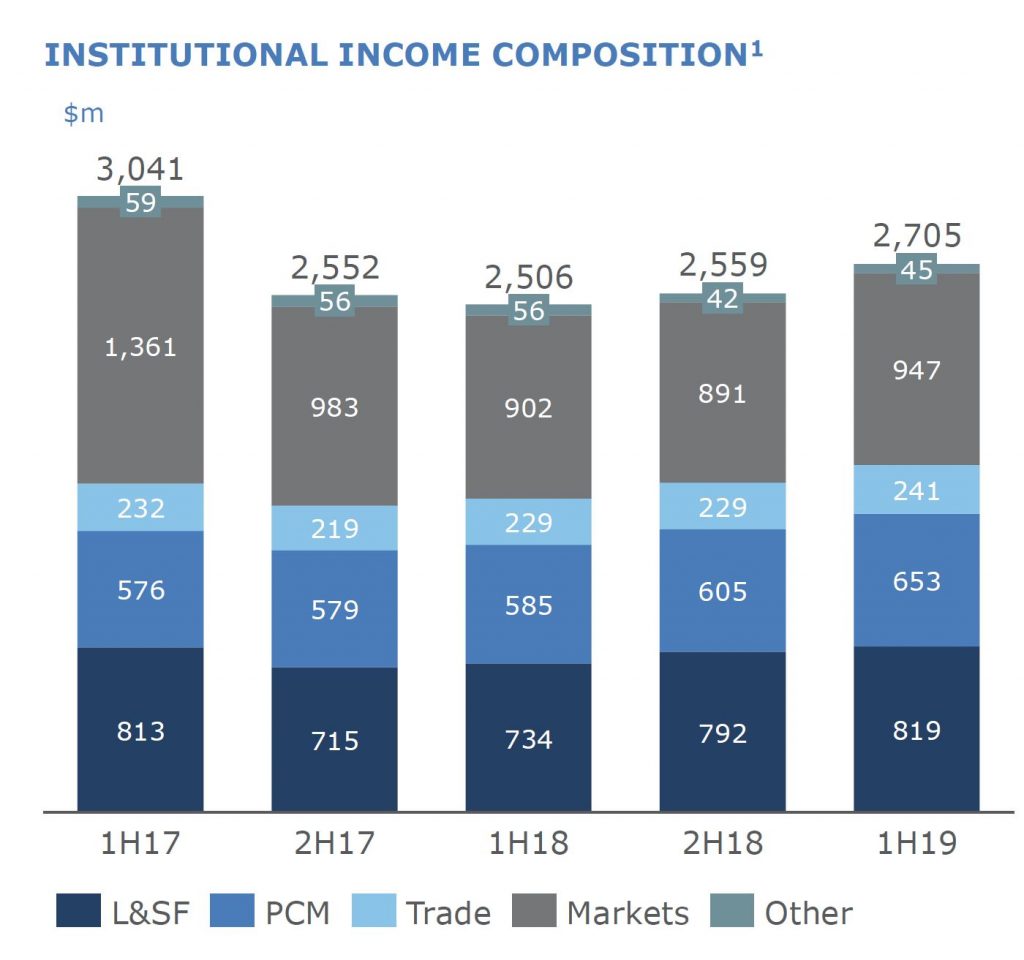

Institutional delivered a higher than expected income (but that may not be sustainable), while other sectors were under more pressure. Institutional profit was up 33%.

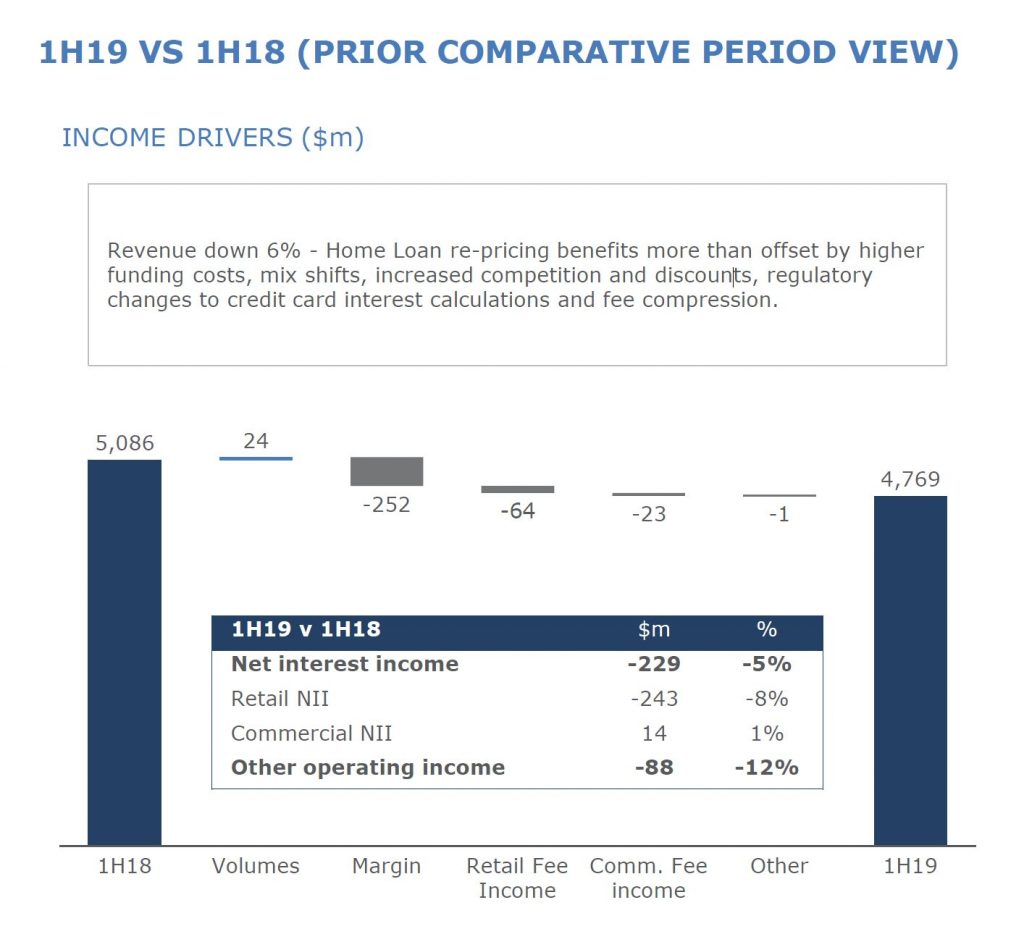

Slower credit demand put pressure on the retail bank, through lower volume growth and reduced fee income. Australian revenue was down 6% as home loan repricing benefit was more than offset by higher funding, increased competition, discounts and regulatory changes.

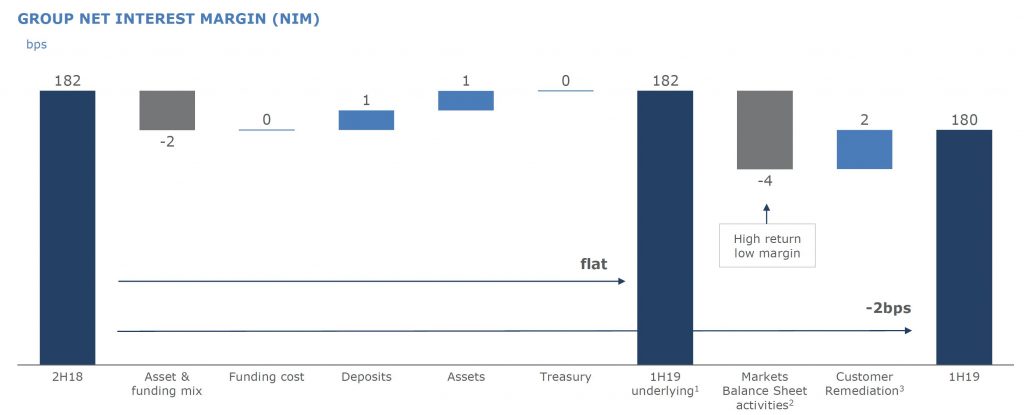

Net interest margin (continuing operations), dropped 2 basis points from 2H18, impacted by funding and asset mix, and markets. Customer remediation added 2 basis points, weirdly. Management, in their briefing said that underlying NIM pressures will persist into 2H19.

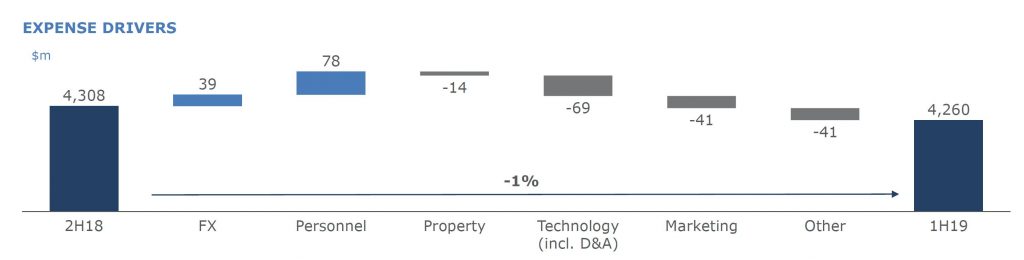

ANZ’s programme of asset sales and restructure benefited the business, and staff (FTE) fell 5% from 41,580 1H18 to 39,359 1H19. Costs were cut as a result, reducing the cost of running the bank by approximately $300 million and they absorbed ~$550m inflation.

However the customer remediation programme is up to $926m ($657m post tax) since 1H17, $698m on Balance Sheet at 31 March 2019. They are currently resolving issues with more than 2.6m customers across retail a commercial lines.

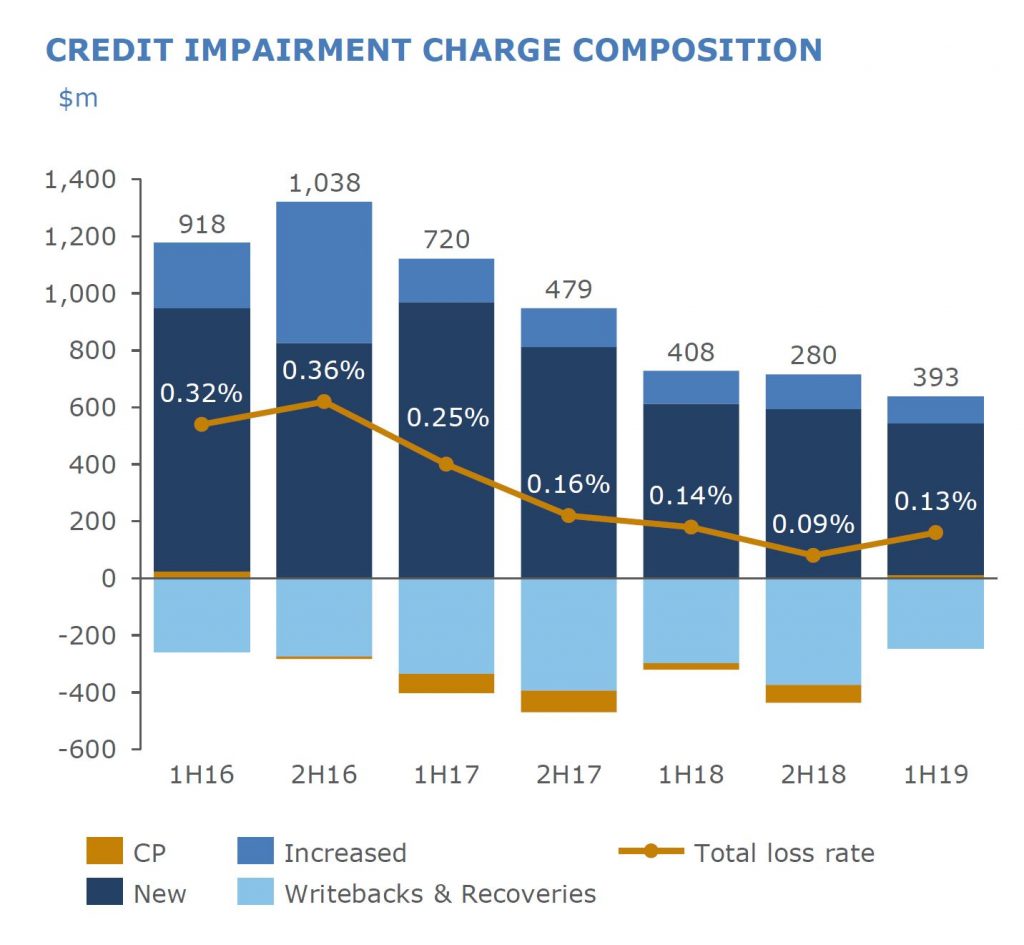

The total provision charge for the half was $393 million, down 4% from this time last year. The Group Loss rate decreased marginally to 13bps for the half (from 14bps in the first half of 2018). New Impaired assets declined to $890 million, down 8% compared to this time last year with Gross Impaired Assets broadly flat over the same period.

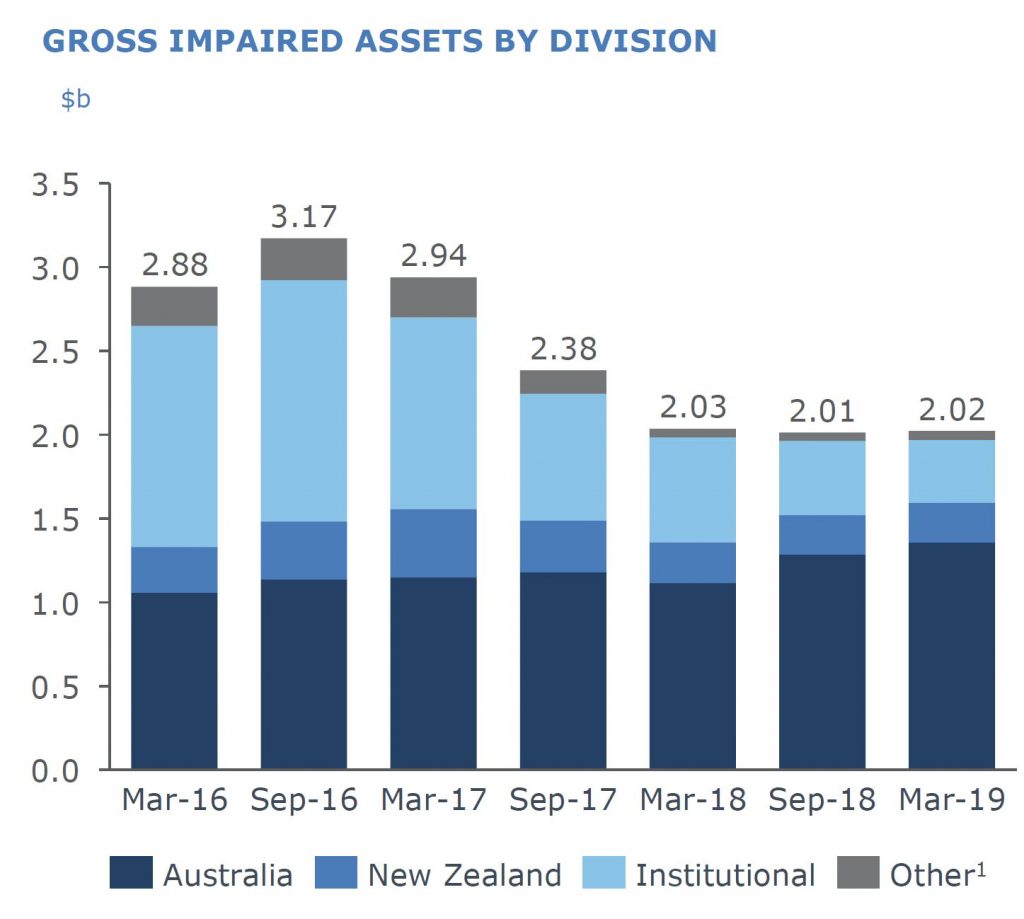

Australian gross impairments have rise from a low of March 2018, offset by lower provisions from Institutional.

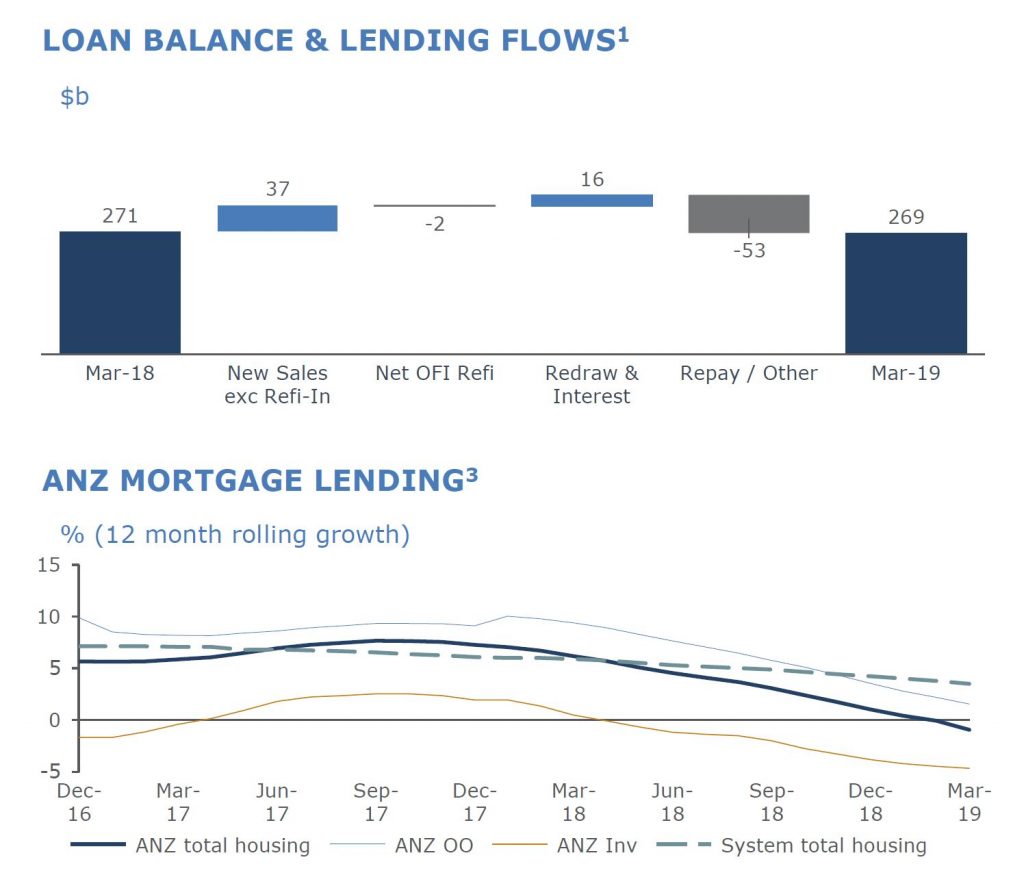

Mortgage arrears in Australia rose quite significantly, despite below system mortgage growth by ANZ. In their briefing, ANZ said its Australian mortgage book will shrink further 2H19, because their strategies which are aimed at improving momentum in this business will take time to flow through.

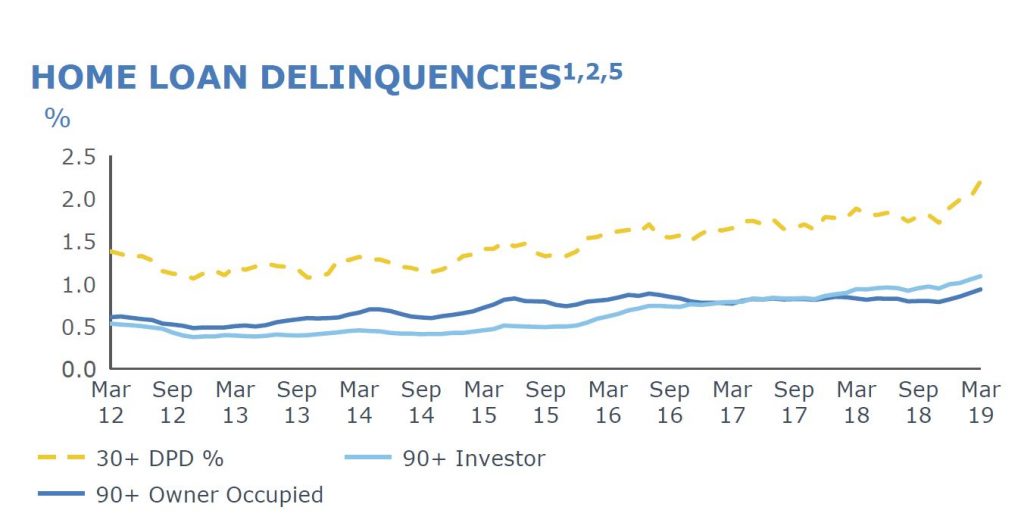

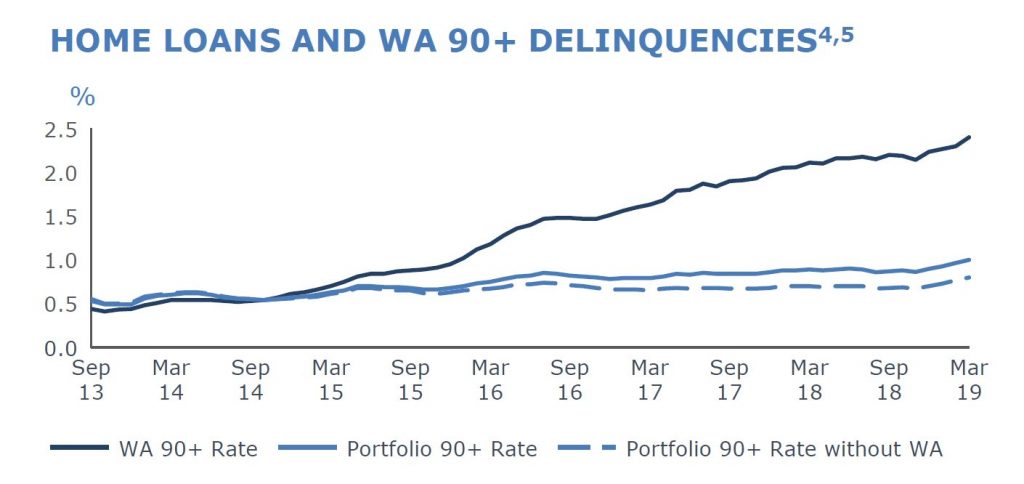

30 day and 90 delinquencies (missed payments) are rising, with property investors higher than owner occupied borrowers. 90+ day past due is at 100 basis point compared with 89 basis points prior, as well as the hike in 30+ day past due.

WA delinquency comprise 30% of 90 day plus delinquency, despite being just 13% of the portfolio, and 65% of losses come from WA. Whereas NSW/ACT makes up 32% of the portfolio but 23% of 90 day plus past due.

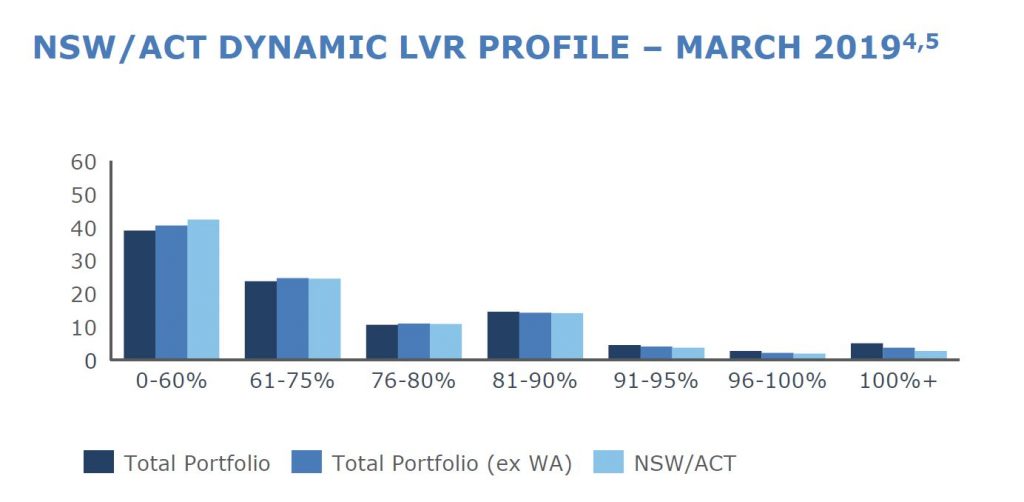

The NSW “dynamic LVR” includes 8.2% of loans above 90% (but note they say “valuations updated to February 2019 where available”, so this is understated in my view – what share of the portfolio is marked to market?. Given falling prices in NSW, more loans will drop into negative equity. And remember this is LOANS not HOUSEHOLDS. Losses in Australian mortgages housing was 4 basis points in 1H19, up from 2 basis points prior.

In the briefing, they attributed the rise in mortgage delinquencies to:

the shift from interest-only to principal and interest loans, demanding higher repayments

subdued wage growth putting more financial pressure on households

the trend in falling house prices

a longer cure time-frame, as delinquencies are now taking a longer time to cure thanks to extended property sale time-frames

the “denominator effect” of lower loan growth and shrinking mortgage book

None of this is going to change anytime soon.

Switching from IO to PI will continue.

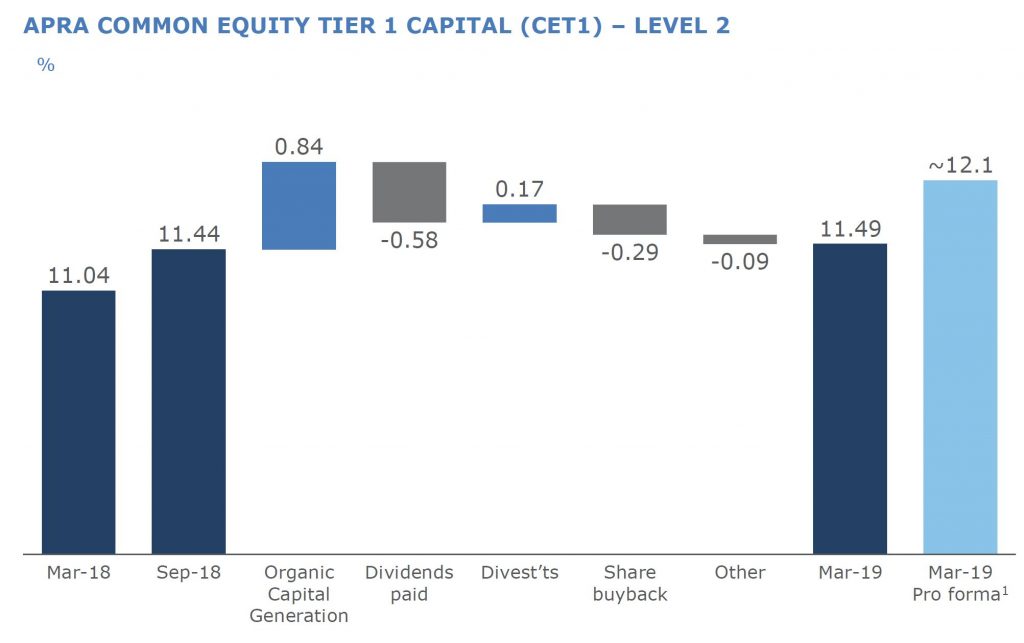

ANZ’s Common Equity Tier 1 Capital Ratio increased to 11.5%, up 45 basis points (bps). Return on Equity increased 13 bps to 12.0% with Cash Earnings per Share up 5% to 124.8 cents.

The Group’s funding and liquidity position remained strong with the Liquidity Coverage Ratio at 137% and Net Stable Funding Ratio at 115%.

The Interim Dividend is 80 cents per share, fully franked. This equates to $2.27 billion to be paid to shareholders. The 3.7% reduction in shares due to the completion of the $3 billion buy-back assisted.

The CEO said :

Retail banking in Australia will remain under pressure for the foreseeable future with subdued credit growth, intense competition and increased compliance costs impacting earnings.

“New Zealand is performing well, however it is starting to share similar characteristics with the Australian market due to strong competition and a slowing Auckland housing market. The major concern in New Zealand remains the impact of the proposed capital changes on the broader economy.

“Institutional banking is performing well and positioned to provide positive earnings diversification, which will partially offset the headwinds in other parts of the Group

Westpac has provided an update on accounting provisions for remediation associated with authorised representatives in relation to certain ongoing advice service fees.

This follows the group’s 25 March 2019 ASX announcement on remediation provisions, where it announced an increase in provisions for its salaried planners and indicated that assessments were underway in relation to authorised representatives. Authorised representatives are advisers who maintain direct relationships with their customers for financial planning services, while operating under the Magnitude and Securitor advice licenses.

Westpac

said these advisers received ongoing advice service fees from their

customers of approximately $966 million between 2008 and 2018. Based on

the information currently available, Westpac today said that its cash

earnings in First Half 2019 will be reduced by $357 million for

accounting provisions associated with this matter.

The $510 million provision (pre-tax) is based on a

range of accounting assumptions relating to potential payments of $297

million (pre-tax), interest costs of $138 million (pre-tax) and $75

million (pre-tax) in remediation program costs.

That part of the

current estimated provision which relates to potential payments

represents around 31 per cent of the ongoing advice service fees

collected over the period which compares to 28 per cent estimated for

salaried planners.

Westpac said it will continue to work with

current and prior authorised representatives and their customers to

determine where a payment should be provided. The final cost of

remediation will not be known until all relevant information is

available and payments have been made. The bank is yet to finalise its

remediation approach, which may change following industry and regulator

discussions.

“While it is disappointing that we have needed to

make these provisions, I said at the end of last year that our priority

was to deal with any outstanding issues and process payments as quickly

as possible,” Westpac CEO Mr Brian Hartzer said.

“As part of our

‘get it right put it right’ initiative we are fixing issues and are

determined to ensure that they don’t reoccur.”

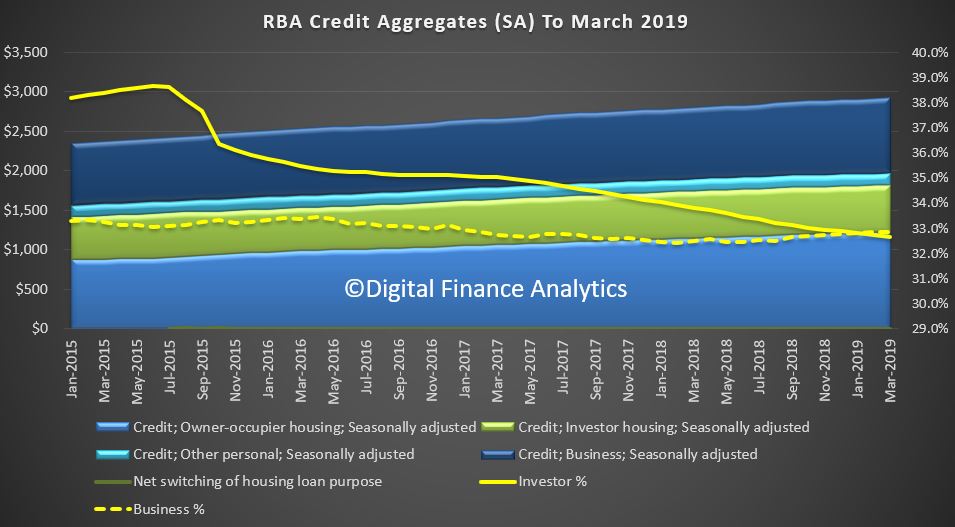

The headline news is the overall housing credit is up, to a new record of $1.82 trillion dollars up 0.31% from last month, or 0.31%. Within that owner occupied lending rose 0.32% to $1.22 trillion dollars and investment lending was flat. 32.7% of lending stock is for investment lending purposes, a slight fall from last month, whilst business lending as a proportion of all lending rose from 32.9% from 32.8% to reach $963.7 billion dollars. Personal credit fell 0.27% or $0.4 billion, to $147.1 billion, and continues to fall.

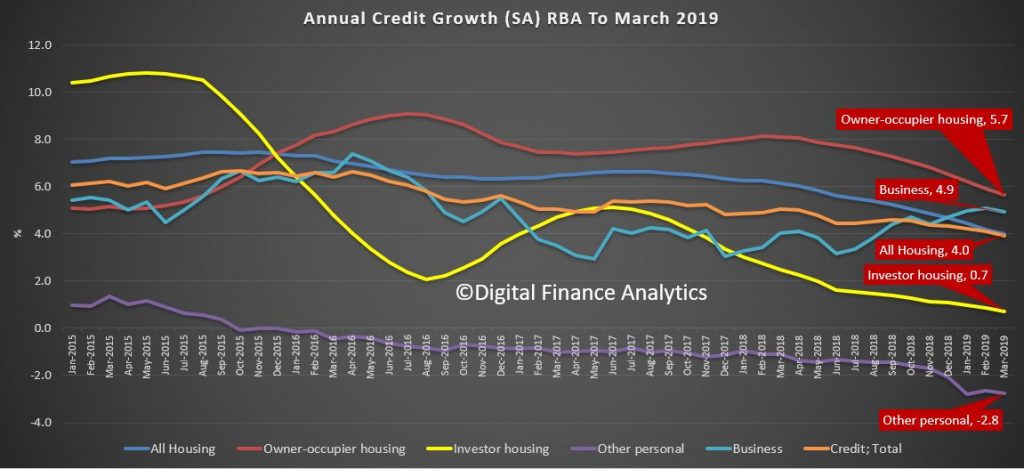

The annualised movements by category shows further weakness, with lending for owner occupied housing now at 5.7%, investment housing lending at 0.7%, giving housing overall growth of just 4% (though still higher than wages growth I would add). Personal credit fell 2.8% over the past year, while business lending rose 4.9% annualised. All these figures are on a seasonally adjusted basis

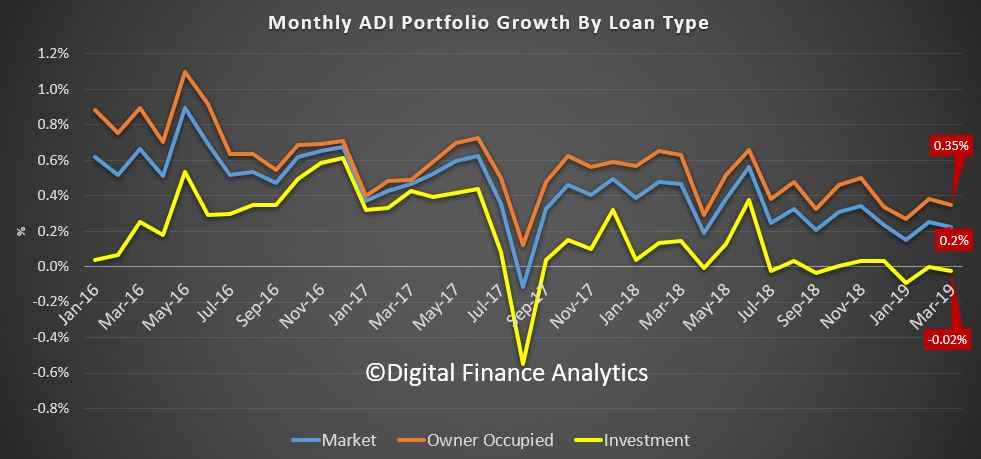

Turning to the APRA data on the banks, owner occupied lending rose 0.35% in March, while investment lending fell by 0.02%, giving total credit growth of just 0.2%. Over the past year owner occupied loans grew by 4.8% (compared with 5.7% at the aggregate level) and investor loans grew 0.4% (compared with 0.7% at the aggregate level). So the banks loan portfolios are growing more slowly than the market.

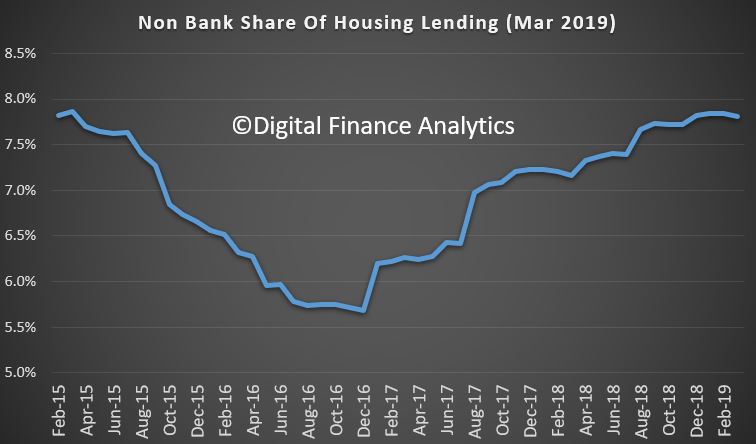

This can be illustrated by comparing the RBA and APRA data (warts and all) to show the non-bank sector is growing faster than the banks. Overall, they have over 7.5% of the market, which is up from the low in December 2016.

In addition, the rate of growth is significantly higher than the banks. Non-bank owner occupied loans are growing at an annual rate of 14%, while investment loans are 2.2%; both significantly higher than the ADI’s. Non-banks have weaker regulation, and more ability to lend. APRA has yet to truly engage with the sector.

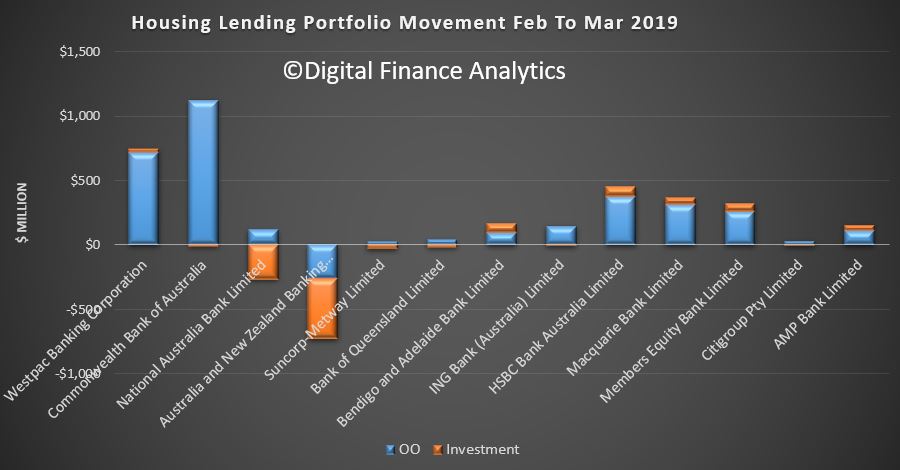

Turning back to the individual lenders, the changes in their portfolios over the month show that Westpac and CBA offered the most new owner occupied loans, while ANZ dropped back, on both owner occupied and investment loans, while NAB dropped investment lending. HSBC, Macquarie and Member Equity Bank (ME) lend more than the regionals.

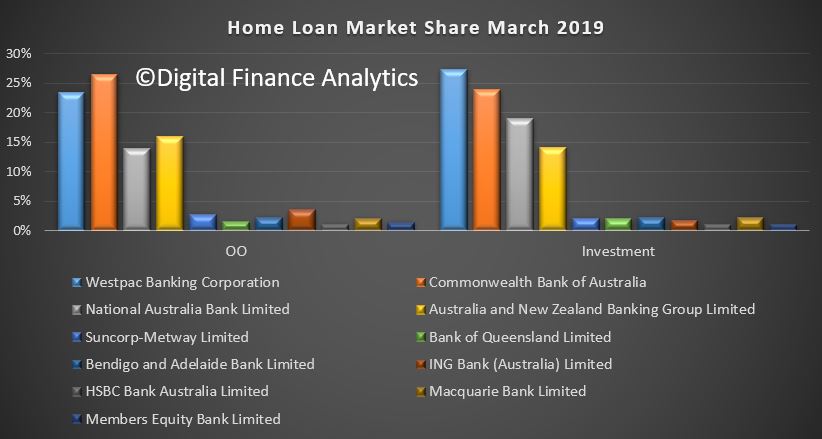

Overall market shares hardly moved, with CBA still the largest owner occupied lending, and Westpac the biggest investor lender.

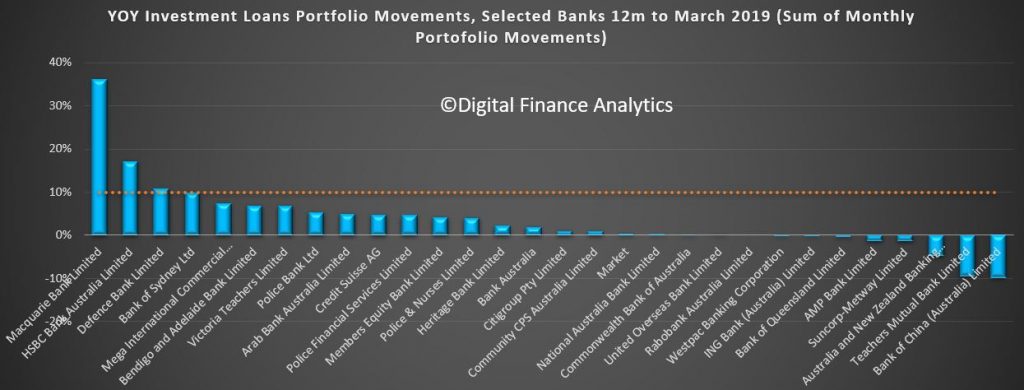

Investment lending growth over the past 12 months has been anemic, but some lenders such as Macquarie are making hay. Of course the old 10% speed limit from APRA has gone now, but the relative growth highlights the fact that the four majors are well below market growth levels – and ANZ the weakest (which is why they said they wanted to lend more).

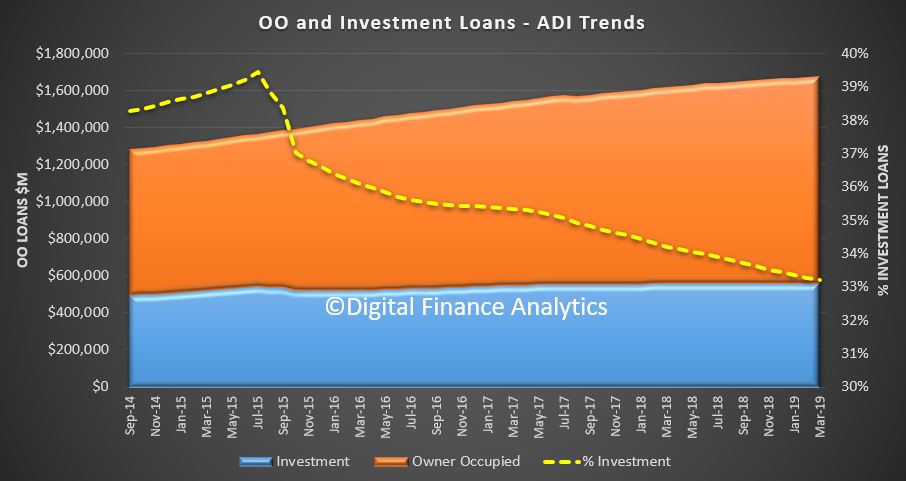

So finally, the total ADI lending book is at $1.68 trillion dollars, with owner occupied loans comprising $1.12 trillion dollars and investment loans $557 billion dollars, and comprising 33.2% of the portfolio – as the ratio continues to fall.

In conclusion, the credit impulse – the rate of change of credit being written is the most significant forward indicator of house price trajectory. The weak state of the market suggests more and significant price falls ahead. Yet despite all this, household debt will continue to rise. There is absolutely no reason to loosen lending requirements, or drop the hurdle rate on these numbers. More households will get into trouble ahead.

I discuss how Ireland navigated their financial crisis a decade ago with Eddie Hobbs, the financial writer, adviser and. broadcaster, who lived through the crash and commented on the events in Ireland.

He wrote and presented a programme on state broadcaster RTE entitled Rip-Off Republic in 2005.

Specifically we discuss how Australia should be preparing…. now….