Westpac has announced it will lift mortgage rates on existing variable loans by 14 basis points. This was expected (I had said by September a few months back!). Others will follow now. More pain for households in a rising cost, flat income economy. More downward pressure on home prices.

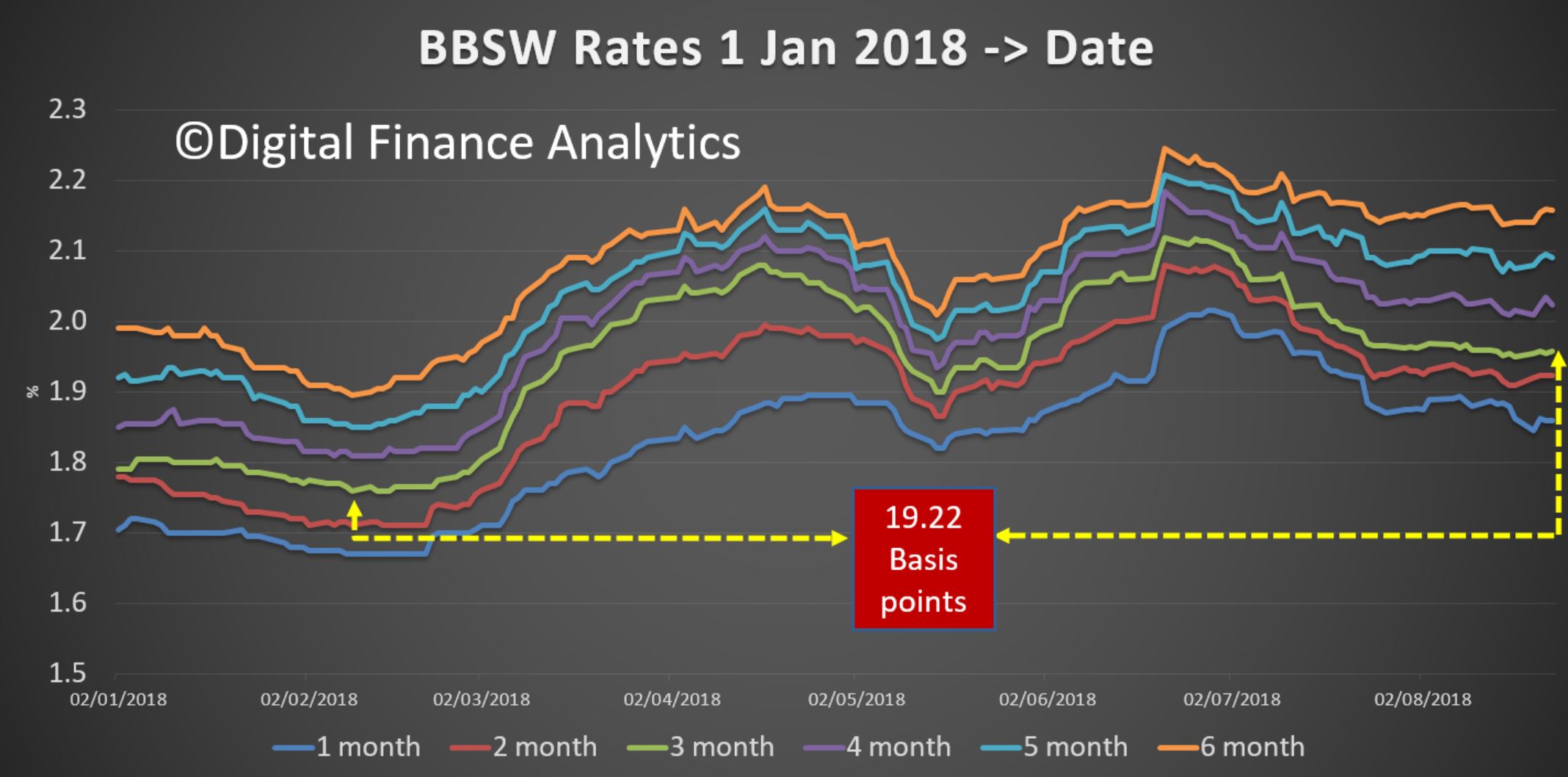

The BBSW stands 19 basis points above where it was in February.

Westpac last week had highlighted a margin problem, and showed the rise in funding, which has squeezed their margins. Expect more “great offers” to attract low risk new customers, at the expense of the back book.

Westpac chief executive Brian Hartzer says he didn’t “relish” having to make the decision to lift variable mortgage rates as higher wholesale funding costs fail to subside.

Following similar moves by several smaller lenders in recent months, Westpac today said variable interest rates for its owner occupied and residential investment property loans would rise 14 basis points due to the “sustained increase in wholesale funding costs” since February.

CEO Brian Hartzer told Westpac Wire it was a “difficult” decision but the bank had “come to the conclusion that what we’re looking at is a sustained increase in that key benchmark wholesale funding cost rate”.

“It’s now been elevated for over six months…reluctantly we came to the conclusion that needed to be reflected in our mortgage costs,” he said. He added that while conscious of the impact the interest rate change would have on consumers’ cost of living, some mortgage rates would remain below where they were three years ago and “from a credit point of view, no, I’m not concerned” about any impact on the bank’s mortgage book.

In an update to the Australian Securities Exchange last week, Westpac said funding costs had risen primarily due to the sharp increase in the bank bill swap rate (BBSW) since February. Compared to the first half, the BBSW was on average 24 basis points higher in the third quarter, the bank added.

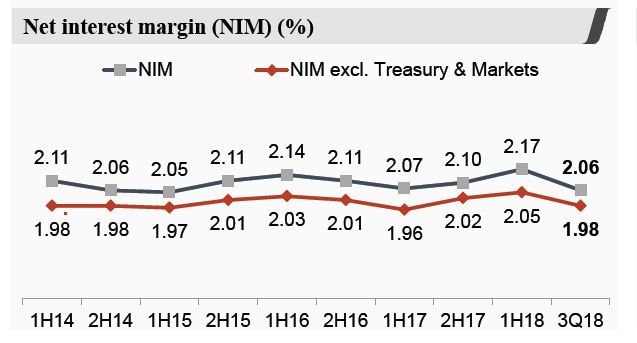

Along with a lower contribution from the Group’s Treasury and other factors including changes in the mix of its mortgage portfolio, the higher funding costs dragged on the bank’s net interest margin, which fell to 2.06 per cent in the June quarter from 2.17 per cent in the first half to March 31.

Mr Hartzer said several factors had driven the increase in wholesale funding costs since February, including greater competition for funds from foreign banks that raise money in the domestic wholesale market. The Reserve Bank of Australia has also noted this rise in competition domestically, plus that the cost of raising funding in the United States and then converting it back into Australian dollars has also increased this year and “at times been well above the cost of raising funds domestically”.

It’s being described as a “mortgage mirage”. It’s an offer from the bank that looks too good to be true and, as it turns out, for many it is; via ABC.

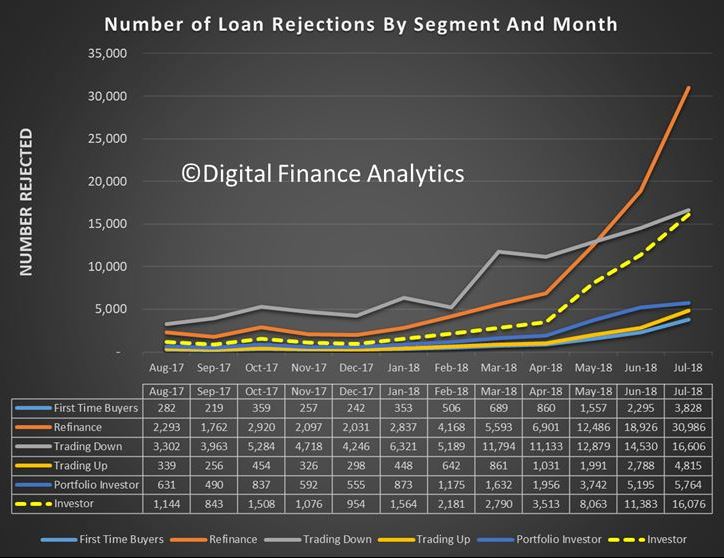

“About 40 per cent of people who tried to refinance were unable to do so,” Digital Finance Analytics principal Martin North said. “If you go back a year it was 5 per cent.”

Data from DFA and investment bank UBS show there has been a spike in the number of failed mortgage refinancing applications.

The reason this is occurring is that, while those applicants cleared the bar for their original loans, that bar has now become a lot higher, following years of banking reform and the fallout from the banking royal commission.

So, now, they simply don’t qualify for the same amount of debt they once did.

“When people took out the loans there was a lot of widespread fudging of the numbers,” chief investment officer with funds management firm, Forager Funds, Steve Johnson said.

“People were getting loans on the basis of a four person family having $30,000 a year of living costs living in Sydney.

“And it’s quite clearly impossible to live in Sydney on that much money a year.

“The biggest issue is that people have borrowed too much money relative to their income and that is a very difficult problem to unwind.”

But, Mr Johnson said, it is not just the banks that have messed up.

Thousands of Australians are either stuck with their current bank or need to move to a “shadow lender” due to tighter lending rules.

“I think the banks have done a lot of unconscionable things, and I think credit has been far too easy to come by, but there is also an element of personal responsibility here in terms of people saying, ‘well, the bank offered to lend me $1.5 million but I don’t really think that is a sensible amount of money for me to borrow’.”

Mr North has calculated there are now close to one million Australians on the edge of mortgage stress – defined by Digital Finance Analytics as borrowers who are going further into debt or eating into savings because their expenses are greater than their income.

Given that, it’s understandable that when the big four banks advertise discounted mortgage rates, financially stressed-out households flock to the banks to bag a better deal.

“And then they’re stuck, because suddenly they find that that wonderfully alluring low rate that’s being hung out to them is inaccessible,” Mr North said.

He calls these borrowers “mortgage prisoners” because they go home empty-handed, trapped in a financial squeeze.

Royal commission behind loan approval lull

While Forager Funds’ Steve Johnson sympathises with these borrowers, he said he is not in the least bit surprised there has been a recent spike in the number of loan refinancing rejections.

“It’s a perfectly natural consequence of more conservative lending standards,” he observed.

“You just can’t have one of those things without the other.”

Mr Johnson said the banking royal commission is behind the loan approval lull.

“It has accelerated it, and made it a lot more dramatic than it otherwise would have been,” he argued.

But it seems the royal commission has also inspired aggressive sales tactics and interest rate discounting from the banks – for the right customers.

“The banks are seeking out low risk, low LVR [loan to value ratio] borrowers, and are trying to hook them” Mr North said.

“Because without them they are pretty much out of profits.”

Big four play down 40 per cent figure

CBA, NAB and ANZ confirmed to RN Breakfast they had reached out to new customers with lower rates.

But how many of the moths drawn to this low interest rate light have been burned in the process by having their applications rejected?

CBA and NAB say they don’t have any data on that, but questioned the accuracy of Mr North’s figures.

ANZ did appear to have such a database and said: “We have seen a small increase in the number of unsuccessful applications for internal refinance since March, but it is much lower than the 40 per cent figure that has been referred to.”

Westpac responded to the ABC by saying that, “No matter the market appetite, we take our responsible lending obligations seriously, ensuring good outcomes for customers”.

Mr North said he sympathised with borrowers who have become ineligible for lower rate loans.

“The typical saving could be up to $150 a month,” he observed.

“They see this mirage of a lower rate opportunity and then it’s snatched away from them when they don’t actually meet the standards.”

Concerns for the rest of the economy

Mr Johnson wanted to use the new data to highlight how serious Australia’s record level of personal debt has become.

“We are in a position now where all those people owe extraordinary amounts of money to the bank and it’s not an easy situation to unwind or extract ourselves from,” he said.

Independent banking analyst Brett Le Mesurier warned there are also important implications for the economy. “There are certainly signs of deterioration,” he said.

“I suspect the issue is not so much their ability to service those loans, it’s more the other spending they don’t make anymore and the broader impact that has on the economy.

“I therefore expect that to push downward pressure on economic growth.”

As for the extent of Australian home loan stress?

The nation’s biggest lender said it simply isn’t an issue.

The Commonwealth Bank said it has seen a slight uptick in 90-day home loan arrears.

But, as noted in its recent results, the uptick in arrears rates reflected “pockets of stress as some households experienced difficulties with rising essential costs and limited income growth”.

ASIC’s review of the reverse mortgage industry highlights that some taking a reverse mortgage could face financial difficulty later in life. This despite the fact that borrowers can never owe the bank more than the value of their property, and can remain in their home until they pass away or decide to move out

Thus, while this type of finance may assist older home owners (70% aged 55-85 own their own home), they face the dual risks of compounding effects on the original loan value as interest is rolled up…

… and significant risks should home prices fall, leading to loss of all or most capital. 63% of borrowers may end up with less equity than the average upfront cost of aged care for one person by the time they reach 84.

Plus there is limited competition, as just 2 credit licensees wrote 80% of the dollar value of new loans from 2013 to 2017.

A review by ASIC has found that reverse mortgages are allowing older Australians to achieve their immediate financial goals – improving their lifestyles in retirement – but longer-term challenges exist.

For older Australians who own their home with few other assets, a reverse mortgage can allow them to draw on the wealth locked up in their homes, while they continue to live in their property.

ASIC reviewed data on 17,000 reverse mortgages, 111 consumer loan files, lender policies, procedures, and complaints. We also commissioned in-depth interviews with 30 borrowers and consulted over 30 industry and consumer stakeholders.

The review found borrowers had a poor understanding of the risks and future costs of their loan, and generally failed to consider how their loan could impact their ability to afford their possible future needs. Lenders have a clear role to play here and need to do more: for nearly all of the loan files we reviewed, the borrower’s long term needs or financial objectives were not adequately documented.

Importantly, under legal protections in place since 2012, borrowers can never owe the bank more than the value of their property, and can remain in their home until they pass away or decide to move out. However, depending on when a borrower obtains their loan, how much they borrow, and economic conditions (property prices and interest rates), they may not have enough equity remaining in the home for longer term needs (e.g. aged care).

ASIC Deputy Chair Peter Kell said “Reverse mortgage products can help many Australians achieve a better quality of life in retirement.”

“But our review shows that lenders and brokers need to make inquiries that would lead to a genuine conversation with customers about their possible future needs, not just a set of tick boxes on a form.”

ASIC’s report also finds that there is an opportunity for lenders to reduce the risk of elder abuse. Under the new Code of Banking Practice, recently approved by ASIC, banks will be required to take extra care with customers who may be vulnerable, including those who are experiencing elder abuse.

Consumers also had limited choices for finding a reverse mortgage. Several providers withdrew from the market after the global financial crisis. From 2013 to 2017, two credit licensees provided 80% of the dollar value of new loans from 2013 to 2017.

Background

Reverse mortgages are a credit product that allows older Australians to borrow using the equity in their home. The loan does not need to be repaid until a later time, typically when the borrower has vacated the property or passed away. They are a more expensive form of credit compared to standard variable owner occupier home loans; the interest rates are typically 2% higher and, as there are no repayments required, interest compounds.

Consumer demand for reverse mortgages has grown gradually since the global financial crisis, with the total exposure of ADIs to reverse mortgages increasing from $1.3 billion in March 2008 to $2.5 billion by December 2017.

ASIC commenced a review of lending practices and consumer outcomes in the reverse mortgage market to proactively examine issues that might emerge for older Australians.

As part of this review, we evaluated the effectiveness of enhanced responsible lending obligations for reverse mortgages which were introduced five years ago into the National Consumer Credit Protection Act 2009 (National Credit Act).

This review examined five brands, who collectively lent 99% of the dollar value of approved reverse mortgage loans in 2013-17. These brands were: Bankwest, Commonwealth Bank, Heartland Seniors Finance, Macquarie Bank and Westpac (comprising St George Bank, the Bank of Melbourne and BankSA). As of late 2017, Macquarie Bank and Westpac are no longer providing new reverse mortgages.

This project forms part of ASIC’s broader work for older Australians to help bring about positive changes for these consumers in credit and financial services: see REP 537Building seniors’ financial capability report 2017 and REP 550ASIC’s work for older Australians.

ASIC’s MoneySmart website has information for consumers about reverse mortgages. Consumers can also use MoneySmart’s reverse mortgage calculator to see how a reverse mortgage can impact the equity in their home.

The Combined Industry Forum has agreed “in principle” to extend its good consumer outcomes requirement to incorporate a “conflicts priority rule” as a “customer first duty”, via The Adviser.

In its interim report, released on Monday (27 August), the Combined Industry Forum (CIF) stated that throughout 2018, it has been considering ways to build upon its good customer outcomes reforms published in its response to the Australian Securities and Investments Commission’s (ASIC) review into mortgage broker remuneration.

In its review, ASIC noted that a broker would satisfy the requirement if the “customer has obtained a loan which is appropriate [in terms of size and structure], is affordable, applied for in a compliant manner and meets the customer’s set of objectives at the time of seeking the loan.”

However, the CIF has proposed that the provision could be extended to include a “conflicts priority rule”.

“The ‘conflict priority rule’ could be formulated as a requirement for the customer’s interests to be placed above the providers, or those of their organisation, based on the information reasonably known to the provider, at the time of providing the service,” the CIF noted.

“The effect of this approach would be a requirement to place the customer’s interests first. The combination of the good customer outcome definition and a customer first duty allows both an easy to follow principle – put the customer’s interests first – and structure to follow for brokers when assessing loan suitability.”

The CIF added that further governance metrics could be built for “monitoring and oversight”.

However, the CIF acknowledged that the development and application of the customer first duty is “multifaceted and complex”, noting that “there may be unknown impacts”.

“These include the potential for limiting access to credit, and a disproportionate impact on smaller and regional lenders if lender panels require rationalisation,” the CIF continued.

The CIF noted that it had “not yet settled on a final position”, but claimed that the reform should be underpinned by the following principles:

placing the customer first, and having ‘good’ consumer outcomes at the centre of its approach

fit-for-purpose for the mortgage broking industry, considering the nature of services provided, the form of conflicts of interests inherent to the industry, the current evidence of risks to customer outcomes, and considering the current regulatory framework

promoting competition, and ensuring that no part of the value chain is unfairly disadvantaged

all parts of the value chain will have a role to play to support the implementation and monitoring the customer duty

providing transparency for all participants, and

promoting simple, achievable solutions. Finally, the CIF is aware that there is merit in moving a customer first principle from an implicit expectation, to an explicit statement that a customer and mortgage advice provider can easily understand.

The CIF concluded that it is “aware that there is merit in moving a customer first principle from an implicit expectation, to an explicit statement that a customer and mortgage advice provider can easily understand”.

The report also outlined CIF’s progress in implementing other reforms proposed in its response to ASIC, which include the standardisation of commission payments, the removal of bonus commissions, the removal of “soft dollar payments”, and the drafting of the “Mortgage Broking Industry Code”.

Steve Keen, the controversial economist, and I discuss the nature of debt, why home prices will fall and why the regulators and authorities are unable to disassemble the debt bomb.

You can watch the video, or listen to the podcast:

“The Great Financial Crash had cataclysmic effects on the global economy, and took conventional economists completely by surprise. Many leading commentators declared shortly before the crisis that the magical recipe for eternal stability had been found. Less than a year later, the biggest economic crisis since the Great Depression erupted.

In this explosive book, Steve Keen, one of the very few economists who anticipated the crash, shows why the self-declared experts were wrong and how ever–rising levels of private debt make another financial crisis almost inevitable unless politicians tackle the real dynamics causing financial instability. He also identifies the economies that have become ‘The Walking Dead of Debt’, and those that are next in line – including Australia, Belgium, China, Canada and South Korea.

A major intervention by a fearlessly iconoclastic figure, this book is essential reading for anyone who wants to understand the true nature of the global economic system”.

The Royal Commission in Financial Services Misconduct has announced that the sixth round of public hearings will focus on the Insurance Industry and will be held in Melbourne from Monday 10 September to Friday 21 September. AMP, CommInsure, IAG and Youi are among the case studies to be considered. More grief for the industry we suspect as more bad behaviour is uncovered!

The sixth round of public hearings will consider issues associated with the sale and design of life insurance and general insurance products, the handling of claims under life insurance and general insurance policies, and the administration of life insurance by superannuation trustees. The hearings will also consider the appropriateness of the current regulatory regime for the insurance industry.

The Commission presently intends to deal with these issues for the purposes of the public hearings by reference to the case studies set out below. These include the natural disaster case studies that were originally to have been examined in the fourth round of public hearings. Entities are named in alphabetical order and not in the order in which the evidence of those entities will be heard.

Topic

Case Studies

1.

Life insurance

AMP

ClearView

CommInsure

Freedom Insurance

REST

TAL

2.

General insurance

AAI (Suncorp)

Allianz

IAG

Youi

3.

Regulatory regime

Code Governance Committee

Financial Services Council

Insurance Council of Australia

During the hearings, evidence will also be given by consumers of their particular experiences. The entities that are the subject of consumer evidence will be informed by the Commission.

Australian fintech Tic:Toc, has today announced a reduction in its fixed home loan (live-in) rates by up to 0.10%, bringing their headline 1-year fixed rate to 3.59% (comparison rate 3.64%).

Tic:Toc’s 2-year fixed home loan (live-in) will match their standard variable rate at 3.64% (comparison rate 3.65%).

The rate cut increases Tic:Toc’s standing as holding the lowest 1 and 2 year fixed rates in the market (27 August, https://www.finder.com.au/home-loans/fixed-rate-home-loans), possible due to the cost efficiencies in Tic:Toc’s automated assessment and approval platform.

Tic:Toc founder and CEO, Anthony Baum, said the decision to reduce fixed rates was great news for home loan customers and new home buyers looking for stability for the foreseeable future.

“We recognised there is a lot of confusion in today’s market; with slumps in house prices; out of cycle rate changes; and erratic predictions around interest rate rises.

“Helping Australians better manage their home loan repayments, or move into home ownership, is our priority, and we want to do so with full transparency.”

Since its launch, Tic:Toc has received over $1.3billion in value of submitted home loan applications.

The home loans originated by Tic:Toc and backed by Australia’s fifth largest retail bank, Bendigo and Adelaide Bank, are available throughout Australia at tictochomeloans.com; with the latest fixed rates advertised at www.tictochomeloans.com/instant-fix.

On 20 August, according to Moody’s, Bank Australia Limited sold AUD125 million of three-year sustainability bonds, its first issuance of environment, social and governance (ESG) themed bonds. The bank plans to use the proceeds to finance, or refinance, green and social projects. Bank Australia’s ability to tap the growing demand for ESG investments is credit positive because it adds diversity to its funding sources and allows it to lengthen the overall maturity of its funding portfolio.

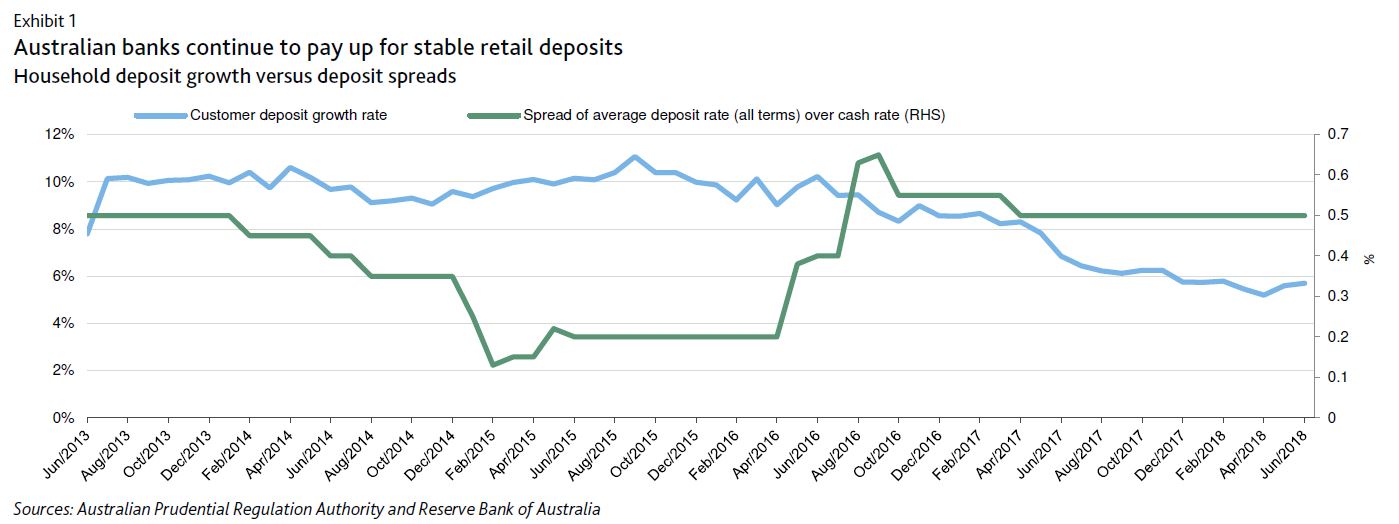

Bank Australia is a mutually owned bank that is primarily deposit-funded and must compete with larger commercial banks at a time when deposit growth has been slowing, but new liquidity regulations have incentivised banks to gather stable customer deposits. This has caused average deposit spreads to remain high.

The ability to diversify funding to include wholesale sources is therefore attractive. However, Bank Australia is a small mutually owned bank with a market share of 0.2%. Its limited scale means that, inevitably, investors will not have the same familiarity with its credit profile as Australia’s major banks, such as the Commonwealth Bank of Australia. This makes it more challenging and costly for Bank Australia to raise long-term funding in the senior unsecured market.

However, increasing investor interest in environmental and socially responsible investing has provided an opportunity for issuers like Bank Australia to tap longer-tenor wholesale funding in meaningful amounts.

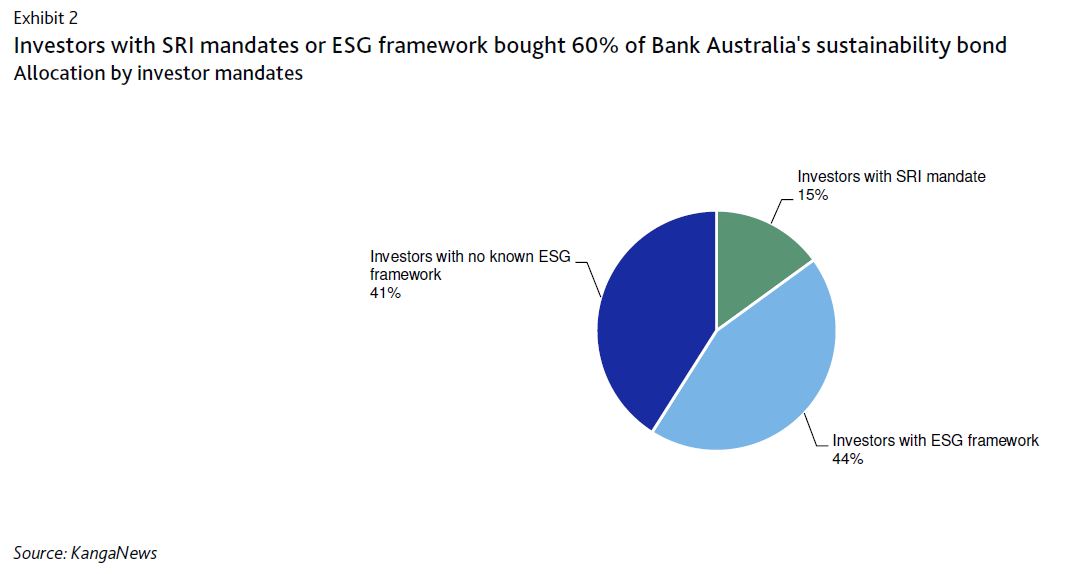

A total of 60% of Bank Austalia’s AUD125 million sustainability bond issuance was allocated to investors with socially responsible investing (SRI) mandates or an ESG framework (Exhibit 2). The scale of investor demand also allowed the bank to increase its final issuance by 25% over the initial offer and to improve its pricing.

Other Australian issuers have also gained traction with bonds providing environmental and social benefits. Teachers Mutual Bank Limited, another small mutual bank, sold an ethical bond in June 2018. Demand has driven Australia’s issuance of green, social and sustainability bonds in the past four years at competitive spreads compared with regular issuance.

Following its sustainability bond issue, Bank Australia’s wholesale funding will increase to 12% from 10% of total funding, on a pro forma basis. Importantly, the sustainability bond, which has a tenor of three years, will lengthen the bank’s overall funding maturity profile.

Bank Australia will likely be able to issue further sustainability bonds in future, because of its involvement in social and environmental projects. For example, it makes loans for affordable housing, community housing, and disability housing.

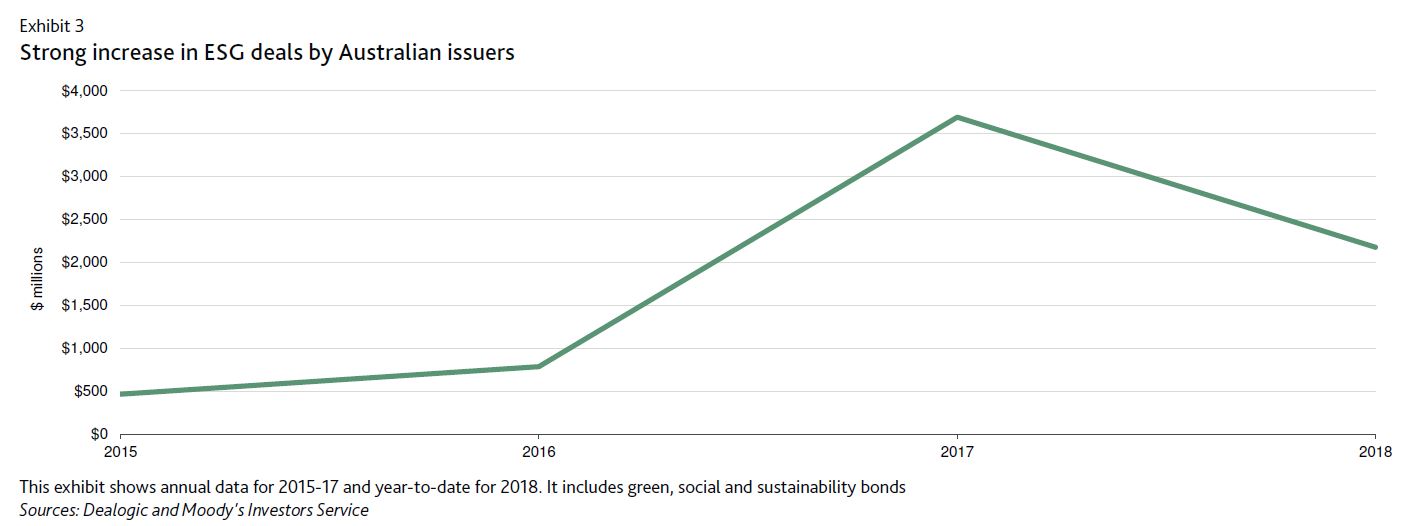

We expect issuers’ increasing awareness of the benefits of issuing green, social and sustainability bonds to spur additional supply. There is some risk that issuance by larger banks may crowd out some small issuers like Bank Australia. However, any increase in issuance will build on a low base since these notes comprise only 2% of total issuance so far in 2018, according to financial market data collector Dealogic. Investor demand is also growing and is likely to absorb more supply.

DFA research was featured in a number of the weekend papers, discussing the rising number of mortgage loan applications which are being rejected by lenders due to tighter lending standards, meaning that many households are unable to access the low refinance rates currently on offer.

NEARLY half of all homeowners are now shackled to their mortgage, with refinance rejections up significantly cent in less than a year as banks rattled by the royal commission drastically tighten borrowing rules.

Loan sizes are being slashed by 30 per cent, trapping many financially stressed customers including some who have been slugged with “out of cycle” interest rate rises. House hunters are also being hit by the credit crunch, with dramatic implications for property markets. The crunch stems from two big shifts in the way banks judge borrowers.

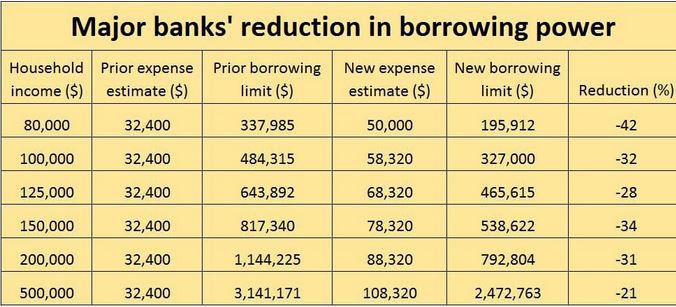

Expense estimates have been raised substantially — the minimum outgoings for an average household are now assumed to be a third higher, according to bank analysts UBS.

On top of this, granular cost breakdowns must be provided. After the royal commission revealed in March that expense checks were so lax as to be borderline illegal, new tests have been imposed requiring in some cases detail of weekly, fortnightly, monthly, quarterly and annual spending in as many as 37 categories from alcohol and haircare to shoes and pets, as well as doctor visits.

As a result, we think that now four in 10 households would now have difficulty refinancing. That means you are basically a prisoner in the loan you’ve currently go. This is based on our 52,000 household surveys plus data from a range of official sources. We estimate that 31,000 households’ refinance applications were rejected in July versus 2,300 in August last year.

Comparison service Mozo’s lending expert Steve Jovcevsk said . “There’s such a huge pool of people who are in that boat.” The most common motivation among those seeking to refinance was to save money by finding a better deal. Many were feeling the pinch because living costs were rising faster than wages and rates on interest-only or investment loans had increased.

The main issue these households are facing in seeking a new deal was banks’ definition of a “suitable loan now is different to six months ago because of the royal commission” and a clampdown by the Australian Prudential Regulation Authority. So there has been a big rise in loan rejections, particularly refinancing.

The borrowing power of hosueholds are being crimped, as shown on the banks website mortgage calculators. Those calculators, compared to a year or 18 months ago, are now on average showing a 30 per cent lower number. For some, the reduction in borrowing power is even greater. The head of UBS’s bank analysis team Jon Mott said that for a household with pre-tax income of $80,000 would get 42 per cent less from a bank; for a $150,000-a-year household, would get 34 per cent less.

Mozo’s Mr Jovcevski said in one example he was personally aware of, a person pre-approved to borrow $630,000 last year was recently offered just $480,000. The would-be borrower’s job and income hadn’t changed.

The implications for property markets were severe, Mr Jovcevski said. “There are fewer qualified buyers,” Reduced borrowing power would drag down selling prices and eventually cut valuations.

“It’s a double whammy for those mortgage prisoners,” Mr Jovcevski said. “Their valuations come in lower so their equity may end up being less than 20 per cents so they have to pay lenders mortgage insurance again” if they refinance.

Australian Banking Association CEO Anna Bligh said banks had to make reasonable inquiries to satisfy APRA’s strengthened mortgage lending standards but she said the term ‘home loan prisoners’ does not represent the facts of a fiercely competitive home loan market where everyday banks are seeking to attract new customers.

Mozo’ Jovcevski said homeowners seeking to give themselves the best chance of successfully refinancing should reduce their expenses in the months prior to applying and ensure all bills have been paid on time.

Mark Hewitt — general manager of broker and residential at AFG which arranges 10,000 home loans a month — said would-be borrowers whose budgets were at breaking point or beyond could still get a loan if they had equity, a clean repayments history and the ability to ditch key expenses such as fees for private school if under the pump.

Some people seeking their first home loan are signing documents in which they promise to cut their spending if a new loan is approved.

“When you get a mortgage you make sacrifices — you continue some of your discretionary spending but not all of it,” said Brett Spencer, head of Opica Group, which sells software to brokers that works out how much a prospective customer can cut back.

A figure is agreed between the broker and the would-be borrower which is then provided to the bank, which would otherwise rely on the higher, raw expense figures.

This makes in interesting point, mortgage brokers will be diving into household expenses more than ever before, but of course, household saying they will cut their expenses to get a loan is not the same a clear cash flow.

Thus even in this tighter market, the industry is still trying to find ways to bend the affordability rules. And it’s worth remembering that according to the latest figures from APRA more than 5% of new loans currently being written are outside standard assessment criteria.

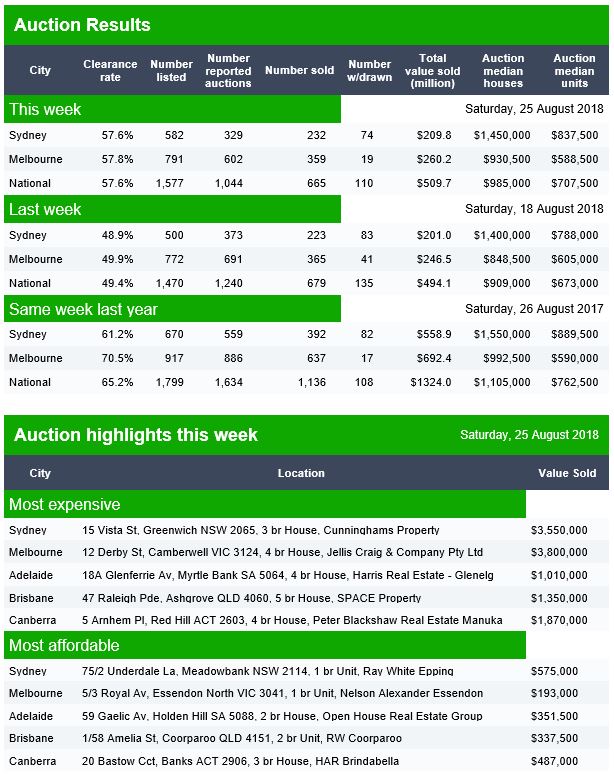

This suggests that even now; bank lending standards are still too lose. All this points to more home prices falls ahead. This is reinforced by the latest Domain auction clearance rate data which was released yesterday, and shows that the final auction clearance rate last week in Sydney, Melbourne and Nationally ended up below 50% way lower on both volume and clearance rates than a year ago.

Yet despite all this, some are still sprooking the market, saying it’s a great time to buy. We do not agree.

Westpac last week had highlighted a margin problem, and showed the rise in funding, which has squeezed their margins. Expect more “great offers” to attract low risk new customers, at the expense of the back book.

Westpac last week had highlighted a margin problem, and showed the rise in funding, which has squeezed their margins. Expect more “great offers” to attract low risk new customers, at the expense of the back book.