CBA has announced that it will remove low documentation features on all new home loans and line of credit applications from 29 September, as the bank continues its ongoing move to ‘simplify’ the bank, via The Adviser.

The Commonwealth Bank of Australia (CBA) has told brokers that it is “simplifying” its product suite to ensure that it is “providing a suitable range of products that align with [its] customers’ needs”.

As such, from Saturday 29 September 2018, the big four bank will remove all low documentation features on new home loans and line of credit applications. Should a customer wish to top up an existing home loan or line of credit with the low doc feature, they must provide full financials for all new applications.

All new loans that have low doc feature, including Home Seeker applications, must reach formal approval by close of business on Friday 28 September 2018.

The bank has said that brokers who request an amendment to an application with a removed product or a low doc feature that has not yet reached formal approval by Saturday 29 September 2018 will need to discuss “another product option” with the customer to suit their needs.

Loans must be funded by close of business Friday 28 December 2018.

There are no changes for existing customers that have low doc loans.

The move marks a major change in the lending landscape, but in practice – CBA has not provided true ‘low doc’ loans for some time, requiring more documentation than most historical low doc loans required.

Indeed, this type of loan product makes up a minimal proportion of the bank’s portfolio.

As well as removing the low doc feature, the bank will also remove several home loan products, including:

One-year Guaranteed Rate

Seven-year Fixed Rate loans

12-month Discounted Variable Rate;

Rate Saver products

Three-year Special Rate Saver; and

No Fee Variable Rate

If a customer wants to top up a One-year Guaranteed Rate, Seven-Year Fixed Rate or a 12-month Discounted Rate Home Loan they must complete a switch to another available product that best suits their needs.

An early repayment adjustment and an administrative fee may apply on the One-year Guaranteed Rate and Seven-year Fixed Rate when completing a switch.

Top-up applications for Rate Saver, Three-Year Special Rate Saver and No Fee Home Loans will still be available.

A CBA spokesperson said: “At the Commonwealth Bank, we constantly review and monitor our suite of home loan products and services to ensure we are maintaining our prudent lending standards and meeting our customers’ financial needs.

“From September onwards, we will be streamlining our suite of products to deliver our customers a simplified and competitive range of home loan solutions.”

Highlighting that the bank’s product suite offers “attractive” standard variable rate and fixed rate options, while its extra home loan products offer customers “low interest rates, no monthly fees, and no establishment fees”.

“Whatever our customers’ needs, our network of brokers or home lending specialists can help them find a flexible mortgage and guide them through the entire home buying journey, providing support every step of the way,” they said.

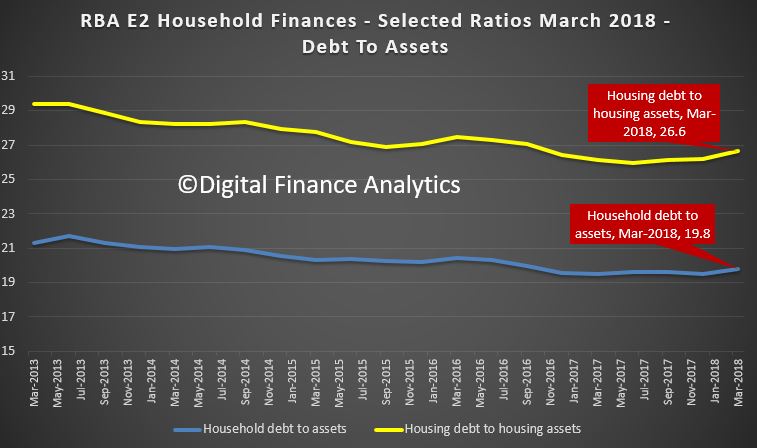

The RBA updated their E2 Household Finances – Selected Ratios to end March, released at the end of June. So they are yet to reflect the latest downturn in home prices and rising debt. But the trajectory is clear and should be ringing alarm bells.

First the ratio of household debt to housing assets and total assets is going up, reflecting mainly falls in property prices. The rate is accelerating, confirming that while debt is still rising, values are not. Expect more ahead.

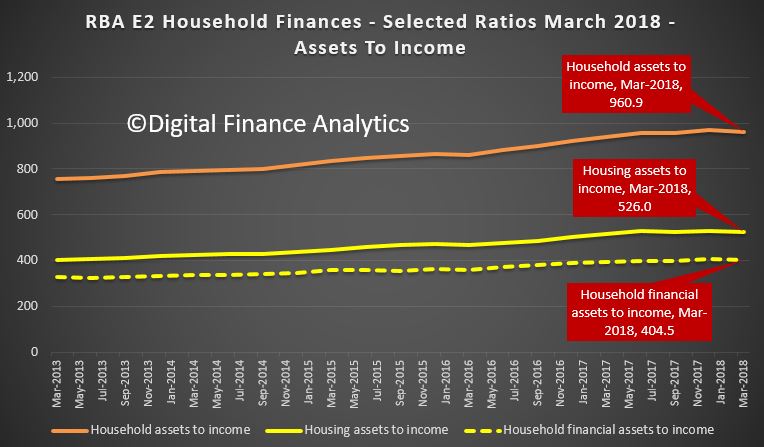

The ratios of assets to income are falling, having been rising for year, again reflecting falls in home prices. So while incomes are flat in real terms, asset values are falling faster.

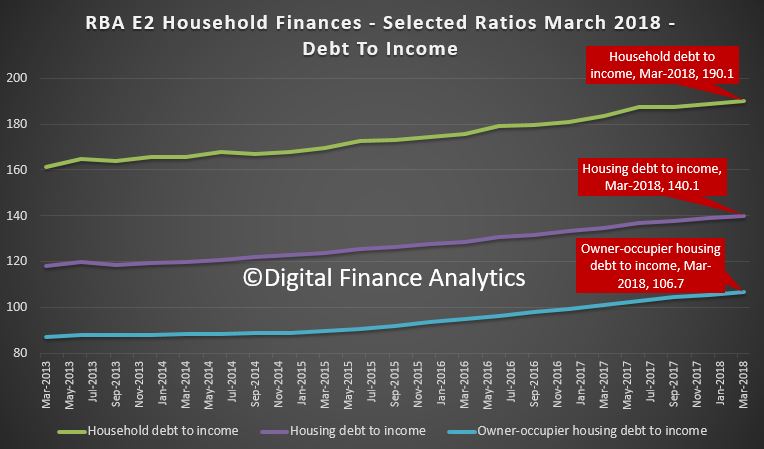

And finally, the killer, the household debt to income ratios continues higher, this despite the greater focus on lending quality, and reduced “mortgage power”. The household debt to income ratio is now at 190.1, the housing debt in income 140.1, and the owner occupied housing debt to income is 106.7. In fact this is moving up more sharply as lenders have focused on owner occupied lending.

Combined this shows the problems in the household sector. No surprise then that mortgage stress is going higher. We release the June data tomorrow.

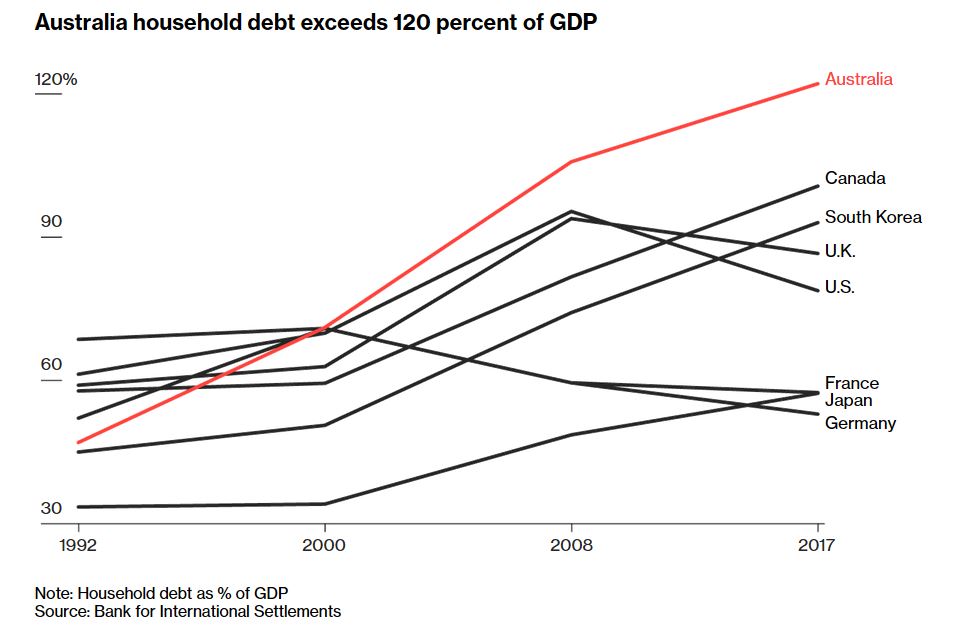

Remember that the debt to GDP ratio is highest in Australia compared with other countries.

The RBA has released their monthly decision and no surprise, we remain at 1.5%. The tenor of the announcement, to me at least sounded less bullish, and I am sure the economists will the parsing the sentences for clues as to their next move. No hint of the next move being up!

To me it is simple, they would like to lift rates to more normal levels, but cannot thanks to high debt, and downside risks. They are stuck. I believe the next move will be down as the economy weakens (dragged down by the fading property market, rising interest rates internationally, and concerns about China’ economic dynamo). But not yet.

At its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent.

The global economic expansion is continuing. A number of advanced economies are growing at an above-trend rate and unemployment rates are low. The Chinese economy continues to grow solidly, with the authorities paying increased attention to the risks in the financial sector and the sustainability of growth. Globally, inflation remains low, although it has increased in some economies and further increases are expected given the tight labour markets. One uncertainty regarding the global outlook stems from the direction of international trade policy in the United States. There have also been strains in a few emerging market economies, largely for country-specific reasons.

Financial conditions remain expansionary, although they are gradually becoming less so in some countries. There has been a broad-based appreciation of the US dollar. In Australia, short-term wholesale interest rates have increased over recent months. This is partly due to developments in the United States, but there are other factors at work as well. It remains to be seen the extent to which these factors persist.

The recent data on the Australian economy continue to be consistent with the Bank’s central forecast for GDP growth to average a bit above 3 per cent in 2018 and 2019. GDP grew strongly in the March quarter, with the economy expanding by 3.1 per cent over the year. Business conditions are positive and non-mining business investment is continuing to increase. Higher levels of public infrastructure investment are also supporting the economy. One continuing source of uncertainty is the outlook for household consumption. Household income has been growing slowly and debt levels are high.

Higher commodity prices have provided a boost to national income recently. Australia’s terms of trade are, however, expected to decline over the next few years, but remain at a relatively high level. The Australian dollar has depreciated a little, but remains within the range that it has been in over the past two years.

The outlook for the labour market remains positive. Strong growth in employment has been accompanied by a significant rise in labour force participation. The vacancy rate is high and other forward-looking indicators continue to point to solid growth in employment. A gradual decline in the unemployment rate is expected, after being steady at around 5½ per cent for much of the past year. Wages growth remains low. This is likely to continue for a while yet, although the stronger economy should see some lift in wages growth over time. Consistent with this, the rate of wages growth appears to have troughed and there are increasing reports of skills shortages in some areas.

Inflation is low and is likely to remain so for some time, reflecting low growth in labour costs and strong competition in retailing. A gradual pick-up in inflation is, however, expected as the economy strengthens. The central forecast is for CPI inflation to be a bit above 2 per cent in 2018.

Nationwide measures of housing prices are little changed over the past six months. Conditions in the Sydney and Melbourne housing markets have eased, with prices declining in both markets. Housing credit growth has declined, with investor demand having slowed noticeably. Lending standards are tighter than they were a few years ago, with APRA’s supervisory measures helping to contain the build-up of risk in household balance sheets. Some further tightening of lending standards by banks is possible, although the average mortgage interest rate on outstanding loans has been declining for some time.

The low level of interest rates is continuing to support the Australian economy. Further progress in reducing unemployment and having inflation return to target is expected, although this progress is likely to be gradual. Taking account of the available information, the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.

As you know, if you’re after intelligent insight which is independent and data driven on Australian Finance and Property, DFA is the place to come, because whether you own property, are thinking of buying, are a saver, or just a user of financial services, you will find our content immediately relevant. Information is power, data is the lifeblood of insight and we offer objective analysis and balanced insights.

We have been able to release new content most days via our social media channels, including videos on YouTube, podcasts and via this blog, but this is taking significant time and effort, to the point where it is crowding out our other business ventures. So to keep the content coming, and to develop the channel further, (we have some great plans) we need your help.

Using Patreon you can elect to subscribe via various tiers on a monthly basis to either help fund our ongoing production costs or to get access to additional content including behind the scenes and additional interviews, plus polls on future content. In particular, this will help to cover the costs of the interviews we produce.

More importantly, it shows that you value the efforts we are putting in, and the importance of what we are doing.

So please go ahead and subscribe via Patreon, and enjoy the content as it is released. Your contribution will be greatly appreciated and it will ensure the insights keep flowing.

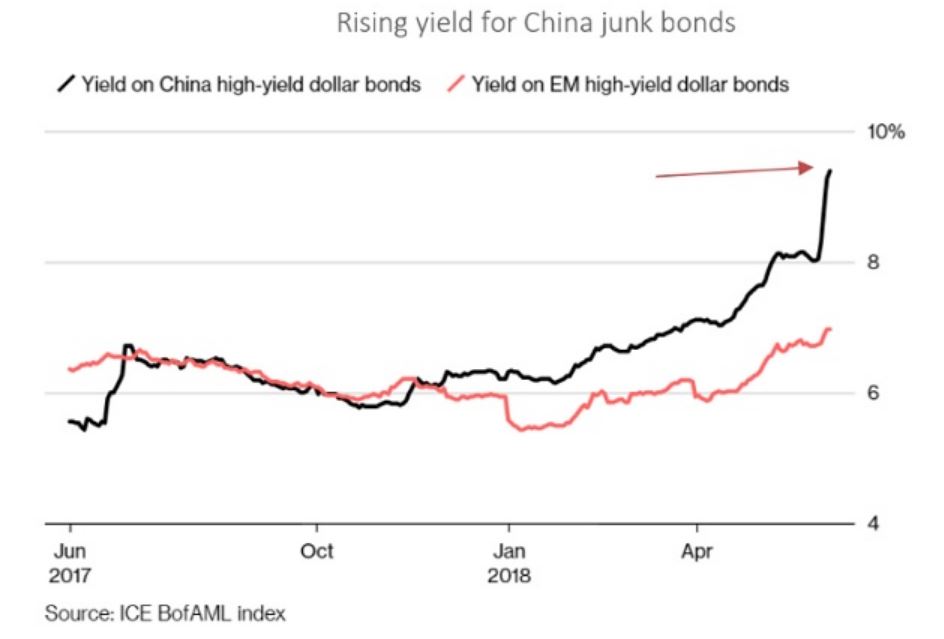

The warning signs are ‘flashing amber’ on a credit crisis in China as the authorities stamp down on excessive lending, says Spectrum Asset Management; via InvestorDaily.

Credit-focused Spectrum Asset Management has issued a note titled Our double Minsky risk that focuses on the likelihood of a credit crisis playing out in China and Australia.

Spectrum principal Damien Wood said both countries have seen a build-up of private debt to record levels: from the business sector in China, and from households (via residential mortgages) in Australia.

Both countries are vulnerable to what is known as a ‘Minksy moment’, a term coined by US economist Paul McCulley in relation to the Russian debt crisis of 1998 and inspired by US economist Hyman Minsky.

The warning sign of a Minsky moment, said Mr Wood, is when the availability of credit starts to shrink.

In China, the government’s “well intended” efforts to cut down on excessive corporate leverage are causing the warning lights to ‘flash amber’ on a Minsky moment, he said.

“In October 2017, China’s central bank governor warned specifically of a Minsky moment for China. In the reported statement, he noted high corporate leverage and rising household debt,” Mr Wood said.

“One key step was to reduce lending from yield chasing ‘shadow’ banks. The concerns were that these key providers of speculative lending were an unsustainable source of finance that promoted poor allocation and management of capital.”

Shadow banking is falling in China, and the net impact is that overall lending growth is slowing, Mr Wood said.

Chinese authorities are looking to “smooth the transition of China Inc’s loan book” by cutting reserve requirements, reducing taxes, and directing banks and lenders to help financial SMEs.

But if these measures do not work, China could look to socialise credit losses.

“Notwithstanding the steps taken, a key fall-out from the reduction in credit availability can be seen in the Chinese corporate bond market. Bond default rates are accelerating and credit spreads on corporate bonds have jumped,” Mr Wood said.

If defaults on Chinese corporate bonds continue (see graph above) a “stampede for the exit could begin”, Mr Wood said. “And then we are one step closer to a Minsky moment.”

Australia is facing the prospect of its own Minsky moment when it comes to household debt (which is sitting at 120 per cent), where Spectrum rates the warning light flashing ‘green to amber’.

“The problem is, even if household debt does not cause excessive problems locally, a rapid deleveraging in China would likely hit local financial markets,” said Mr Wood.

“A large debt reduction in China will risk lower than expected demand for our goods from our major export market,” he said.

“Conversely, we doubt a domestically-driven downturn locally would raise an eyebrow in China’s financial markets.”

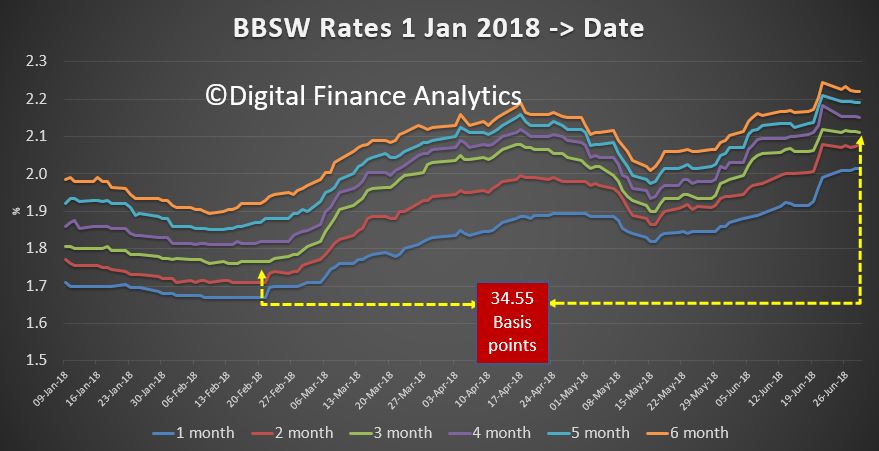

Analysis of the Bank Bill Swap Rates today shows that short term bank funding continues to rise, with one and two month funding costs now 37 basis points higher. Longer term debt went sideways.

More pressure on banks to lift mortgage rates. Which is the big four will be first to blink, after the spate of smaller lenders, including ING late Friday, all lifted?

APRA has released a discussion paper on making changes to the related parties framework for ADI’s. As APRA says an ADI’s associations with related entities can expose the ADI to substantial risks, including through financial and reputational contagion. Complex group structures may also adversely impact on the ability of an ADI to be resolved in a sound and timely manner. The consultation period open until 28 September 2018 and changes would come into force in 2020.

The existing requirements established by the Australian Prudential Regulation Authority (APRA) for authorised deposit-taking institutions (ADIs) governing associations with related entities are a long-standing and important component of the prudential framework for ADIs. The requirements have not been materially updated since 2003.

Since then, international developments have emphasised that deficiencies in prudent controls can expose an ADI to substantial risks in relation to its related entities. For example, during the global financial crisis, reputational pressures meant that overseas banks were inclined to support, often beyond their legal obligations, certain funds management vehicles that suffered significant falls in value or impaired liquidity. In effect, these banks were exposed to substantial credit and liquidity risks through their associations.

APRA is proposing to update its existing related entities framework to account for lessons learned from the global financial crisis on mitigating the flow of contagion risk to an ADI, particularly from related entities, and incorporate changes to the revised large exposures framework, published in December 2017. This update includes revisions to the:

definition of related entities to capture all entities (including individuals) that may expose the ADI to contagion and step-in risk. This is expected to impact all ADIs;

measurement of exposures to related entities by aligning with requirements in the revised large exposures framework. This is expected to impact all ADIs;

prudential limits on exposures to related entities. APRA is proposing to adjust the size of the limits and align the capital base used in limit calculations with the more appropriate Tier 1 base now used in the revised large exposures framework. The proposal is expected to primarily impact ADIs that have a small capital base;

extended licensed entity (ELE) framework by amending the criteria for a subsidiary to be consolidated in an ADI’s ELE. This is expected to impact those ADIs that utilise the ELE framework and particularly those that have offshore ELE subsidiaries, which hold or invest in assets; and

reporting requirements to capture more prudential information on substantial shareholders and subsidiaries that are treated as part of an ADI’s ELE. This is expected to impact more complex ADIs.

The impact of the proposed changes on each ADI will depend on, among other factors, the number and size of entities captured by the proposed definition of related entities; the size of exposures to related entities relative to an ADI’s capital base; the extent to which an ADI undertakes business through subsidiaries; and differences in how an ADI currently measures to related entities compared with the proposed methodology.

APRA is cognisant of the impact these reforms may have on ADIs and is particularly interested in receiving feedback on whether the proposed reforms best meet APRA’s mandate to improve financial safety and financial system stability without material adverse impacts on efficiency or competition. ADIs are encouraged to provide alternative proposals where it is considered that an alternative will better meet the prudential objectives.

APRA is seeking feedback on the proposed amendments with the consultation period open until 28 September 2018. Given the potentially material nature of the proposals, APRA anticipates that a finalised framework would come into force on 1 January 2020, with transition potentially offered to ADIs that are most impacted by the reforms.

In a release late last week, the FED said that as part of its annual examination of the capital planning practices of the nation’s largest banks, the Federal Reserve Board did not object to the capital plans of 34 firms but objected to the capital plan from DB USA Corporation due to qualitative concerns.

Due in part to recent changes to the tax law that negatively affected capital levels, two firms will maintain their capital distributions at the levels they paid in recent years. Separately, one firm will be required to take certain steps regarding the management and analysis of its counterparty exposures under stress.

The Comprehensive Capital Analysis and Review, or CCAR, in its eighth year, evaluates the capital planning processes and capital adequacy of the largest U.S.-based bank holding companies, including the firms’ planned capital actions, such as dividend payments and share buybacks. Strong capital levels act as a cushion to absorb losses and help ensure that banking organizations have the ability to lend to households and businesses even in times of stress.

“Even with one-time challenges posed by changes to the tax law, the CCAR results demonstrate that the largest banks have strong capital levels, and after making their approved capital distributions, would retain their ability to lend even in a severe recession,” said Vice Chairman Randal K. Quarles.

When evaluating a firm’s capital plan, the Board considers both quantitative and qualitative factors. Quantitative factors include a firm’s projected capital ratios under a hypothetical scenario of severe economic and financial market stress. Qualitative factors include the strength of the firm’s capital planning process, which incorporates risk management, internal controls, and governance practices that support the process.

This year, 18 of the largest and most complex banks were subject to both the quantitative and qualitative assessments. The 17 other firms in CCAR were subject only to the quantitative assessment. The Board may object to a capital plan based on quantitative or qualitative concerns.

The Board objected to the capital plan from DB USA Corporation due to qualitative concerns. Those concerns include material weaknesses in the firm’s data capabilities and controls supporting its capital planning process, as well as weaknesses in its approaches and assumptions used to forecast revenues and losses under stress.

The Board issued a conditional non-objection to the capital plans of both Goldman Sachs and Morgan Stanley and both firms will maintain their capital distributions at the levels they paid in recent years, which will allow them to build capital over the next year. Each firm’s capital ratios, under the capital plans they originally submitted and with the one-time capital reduction from the tax law changes, fell below required levels when subjected to the hypothetical scenario. This one-time reduction does not reflect a firm’s performance under stress and firms can expect higher post-tax earnings going forward.

The Board also issued a conditional non-objection for the capital plan from State Street Corporation. The stress test revealed counterparty exposures that produced large losses under the hypothetical scenario, which assumes the default of a firm’s largest counterparty under stress. The firm will be required to take certain steps regarding the management and analysis of its counterparty exposures under stress.

The Federal Reserve did not object to the capital plans of Ally Financial, Inc.; American Express Company; BB&T Corporation; BBVA Compass Bancshares, Inc.; BMO Financial Corp.; BNP Paribas USA; Bank of America Corporation; The Bank of New York Mellon Corporation; Barclays US LLC.; Capital One Financial Corporation; Citigroup, Inc.; Citizens Financial Group; Credit Suisse Holdings (USA); Discover Financial Services; Fifth Third Bancorp; HSBC North America Holdings, Inc.; Huntington Bancshares, Inc.; JP Morgan Chase & Co.; Keycorp; M&T Bank Corporation; MUFG Americas Holdings Corporation; Northern Trust Corp.; The PNC Financial Services Group, Inc.; RBC USA Holdco Corporation; Regions Financial Corporation; Santander Holdings USA, Inc.; SunTrust Banks, Inc.; TD Group US Holdings LLC; U.S. Bancorp; UBS Americas Holdings LLC; and Wells Fargo & Company.

U.S. firms have substantially increased their capital since the first round of stress tests led by the Federal Reserve in 2009. The common equity capital ratio–which compares high-quality capital to risk-weighted assets–of the 35 bank holding companies in the 2018 CCAR has more than doubled from 5.2 percent in the first quarter of 2009 to 12.3 percent in the fourth quarter of 2017. This reflects an increase of more than $800 billion in common equity capital to more than $1.2 trillion during the same period.

A number of factors have contributed to this, including instability in the market value of farms, policy changes that make farms more reliant on financial instruments, and shifts in the global positioning of farm land relative to other forms of property.

The commission has heard that local lending brokers were not qualified to value farm properties, and that farm valuations have become fluid and unpredictable.

Sometimes farms and farmland were deliberately overvalued. Higher values enable farmers to borrow more money for farm improvements, and the local lending branch manager to earn higher commissions.

Not only do the central administrators in banks lack the information and expertise to question these assessments, their business models have encouraged overvaluation and overborrowing as a means to grow their businesses.

Across the Murray Darling Basin banks have taken the separation of water from land – a precursor to the marketisation of water – as a cue to devalue land.

This has provided a reason to void existing loan agreements and to offer refinancing under more arduous conditions. Farmers have no option to refuse, and so borrow with the expectation that a couple of good years will put them back on track.

And if the good years don’t materialise, farms fall into financial stress.

This confronts a third issue, which is that in the bad years farms are harder to sell so their market value plummets. This compounds the problem.

Farmers are more reliant on banks

Policy changes have made farms more reliant on banks.

Since Australia adopted open-market policies in the 1980s and agricultural markets have become global, farmers have been exposed to global price changes.

Drought assistance has also been reoriented to rely on market-based instruments, such as loans from banks rather than grants from governments. In the wake of the deregulation of the financial system, and the post-financial crisis consolidation of the farm lending sector, many farm-specific loan products have disappeared. So banks tend to treat farms as businesses like any other.

The open-market policies also create an imperative to expand landholdings (“get big or get out”) and to invest in the latest equipment and technologies. Since this requires borrowing, it thrusts farmers onto a credit treadmill.

Of course, low interest rates have also stimulated borrowing for farm expansion.

Increasing corporate control of farm inputs (seeds, fertiliser etc.) and outputs is squeezing farmers’ capacity to earn enough to service their loans.

To make matters worse, the declining terms of trade impel farmers to increase productivity just to stand still.

The farmers before the royal commission have mostly managed to stay on the treadmill, but only until the banks’ rule changes cranked up the speed to throw them off.

It’s clear that despite their crucial role, many banks still don’t really “get” the vagaries of farming. They don’t understand how different farm lending is – or should be – to commercial and housing lending. Neither do they seem to appreciate the broader social and economic dimensions of the role they have in managing farm risks.

Dramatic revisions to land valuations, as discussed in numerous cases described in the commission, can undermine an entire farming region’s equity.

The accelerated thinning out of the farming population impacts on local economies and sporting teams, among others. In the lead-up to and during the whole process of deregulation, farmers were continually reassured – in reports by the Productivity Commission, for example – that the credit market would evolve to meet their needs.

The evidence that the commission has heard in many respects represents a case of market – and regulatory – failure.

Since the global financial crisis, farm land has become an attractive investment for wealthy families and institutional investors, and for governments worried about food security.

As this pushes up land values, banks can be more aggressive towards failing farms. Foreclosures free up land for deep-pocketed investors.

It would be a mistake, then, to conclude that the stories coming out of the commission are an isolated issue relating to the one bank’s heavy-handed mopping up after the failure of a specialised rural lender – as was the case with ANZ and Landmark.

On the contrary, there are many stories of different banks imposing financial risk frameworks on farmers that are ill-equipped to accommodate the vagaries of farming production and pricing.

When farmers jest about being owned by the banks, they aren’t joking.

We should ask why the government took so long to acknowledge the problems of rural finance and the effects on farming communities.

After the commission concludes, it is likely that banks and regulators will tighten the risk parameters on farm lending and make it harder for smaller family farmers to access finance.

Vulnerable farms will not be able to borrow as much money as in the past. This might be prudent from a financial risk perspective.

However, if city bankers don’t understand farming and don’t make allowances for the volatile and uncertain economies of farming, there’s still no guarantee that tighter rules will translate into better decisions and more positive outcomes.

Rather, tighter rules are likely to have uneven consequences, further disadvantaging smaller family farms relative to deep-pocketed agribusinesses. So, in effect, restricting credit is likely to accelerate the transfer of farmland from family farms to more corporate entities including transnational corporations.

Author: Sally Weller Reader, Australian Catholic University; Neil Argent Professor of Rural Geography, University of New England

Welcome to the Property Imperative weekly to 30th June 2018, our digest of the latest finance and property news with a distinctively Australian flavour.

Watch the video, listen to the podcast or read the transcript.

On the global stage, U.S. stocks were met with heavy selling pressure this week as the trade war hotted up. While earlier in the week, Donald Trump decided against imposing measures to restrict Chinese investment in U.S. based technology, the market is still reacting to the initial U.S. and Chinese tariffs which are coming into effect next week. In the world of bricks and click, Amazon was back in the headlines after the e-commerce giant announced its entry into the pharmacy sector with the purchase of Pillpoint. This triggering widespread panic, sending shares of brick-and-mortar drug stores sharply lower. Nike, meanwhile, showed improved results after revealing its first positive North America sales number in over a year. The S&P 500 closed 0.08% higher to close 2,718.37.

Boomberg says a leaked report from a Chinese government-backed think tank has warned of a potential “financial panic” in the world’s second-largest economy, a sign that some members of the nation’s policy elite are growing concerned as market turbulence and trade tensions increase. Bond defaults, liquidity shortages and the recent plunge in financial markets pose particular dangers at a time of rising US interest rates and a trade spat with Washington, according to a study by the National Institution for Finance & Development The think tank warned that leveraged purchases of shares have reached levels last seen in 2015 – when a market crash erased $US5 trillion of value. “We think China is currently very likely to see a financial panic,” NIFD said in the study, which appeared briefly on the internet on Monday, before being removed. “Preventing its occurrence and spread should be the top priority for our financial and macroeconomic regulators over the next few years.” The Australian dollar fell against the Chinese yuan from March to early May.

The China effect is on top of damming criticism of Central Bank’s policy by the Bank For International Settlements, which we discussed in our post “Red Alert From The Bankers’ Banker”. They say, economies are trapped in a series of boom-bust boom-bust cycles which are driving neutral interest rates ever lower and driving debt higher. The bigger the debt the worse the potential impact will be should rates rise (as they are thanks to the FED). Yet in each cycle “natural” interest rates are driven lower. Implicitly the current settings are wrong. This was in the Bank for International Settlements latest annual report. They also discussed how banks are fudging their ratios using Repo’s in our post “Are Some Banks Cooking the Books?” Within its 114 pages, the BIS report painted a worrying picture of where the global economy stands. In fact, the risks in the global monetary system remain from the Lehman crisis in 2008 and aggregate debt ratios are almost 40 percentage points of GDP higher than a decade ago.

Crude oil prices were strongly up, their highest since November 2014 extending a rally for a fourth-straight week as focus shifted to the prospect of deeper losses of Iranian crude supplies as the U.S. threatened sanctions on countries that fail to halt Iranian crude imports by Nov. 4. Then there were unexpected disruptions in Canada, Libya and Venezuela, together curbing supply and in addition, U.S. crude supplies fell by 9.9 million barrels. Crude futures settled 65 cents higher on Friday as data showed U.S. oil rigs counts fell for the second straight week, pointing to signs of tightening domestic output.

The US dollar was roughly unchanged for the week as heavy selling pressure on Friday reversed earlier gain after the euro rallied sharply on news of EU members agreeing on measures to tackle the migrant crises in the EU including stepping up border security and setting up holding centers to handle asylum seekers. A signal of easing political uncertainty within the bloc sent the EUR/USD sharply higher, to $1.1677, up 0.94%. The US dollar fell 0.82% to 94.22 against a basket of major currencies on Friday.

Gold tumbled further again this week and suffered its biggest monthly slump since September as investors preferred the US$. This was partly because the FED indicated they were comfortable with inflation running above the inflation target over the near-term, in reaction to the news that inflation hit the Fed’s 2% target for the first time since May 2012, raising the prospect of a faster pace of rate hikes.

And the crypto crunch continues. Bitcoin for example went below $6,000 and it could go lower still. No one is sure where the firm base is, so expect more volatility ahead.

And talking of volatility the COBE VIX index ended the week at 16.09, having been higher earlier in the week, up from the 10-12 range seen earlier in the year, but well below the peaks seen in February. As an indicator of perceived risk, this suggests there are more in the system than last year.

Locally the Australian Dollar ended at 74 cents, and the trend down since February is striking, perhaps mirroring rising UD Bond rates, higher capital market interest rates, and the Financial Services Royal Commission which recommenced this week in Brisbane with a focus on country’s $50 billion farm sector and farm finance, 70% of which resides in Queensland, New South Wales and Victoria. And it was more really bad news for the banks, who again demonstrated poor practice, and in some cases deception. But this is a complex area, with farmers sensitive to weather extremes, global commodity prices, and changing land prices. And players such as liquidators seemed to profit from the failure of farmers, despite selling land and equipment well below value. They are not in scope for the Royal Commission, but we think they should be. There is clearly a case for ASIC to take a more hands-on role in farm finance as some rural lenders, such as the non-bank ones, are not covered by existing complaints-handling systems. But overall, this is another example of poor culture in the banking industry, and players including ANZ and CBA are under the microscope. The findings were so damming that the Commission decided to spend more time looking at farming case studies. For bank-originating farm debt, some lenders changed loan contract terms for farm businesses that were late with payments or in default without warning or explanation. More broadly, the Commission heard about declining access to banking services for the 6.9 million Australians in rural areas, the inflexibility of lenders toward farm-specific challenges like weather, trade disputes, and lack of customized regulations for the sector.

The latest credit data from APRA and RBA, out yesterday, showed that May credit slowed sharply to equal a 6-year low of 0.2% m/m, and a 4-year low of 4.8% y/y. We discussed this in our post “May Credit Snapshot Tells the Story”.

As UBS highlights, private credit growth has weakened more quickly than expected to only 0.2% m/m, the equal weakest since 2012; also dragging the y/y to an equal 4-year low of 4.8% (after 5.1%). Also, total deposits growth collapsed in recent months to only 2.4% y/y, the weakest since the last recession in 1991. Meanwhile, the household debt-to-income ratio lifted to a record high of 190% in Q1- 18. However, mainly due to falling house prices, household wealth declined by 0.4% q/q, the largest fall since 2011. While this followed a surge to a record high level of $10.3 trillion in Q4-17, the change in wealth drives the household saving ratio, consistent with a fading ‘household wealth effect’ dragging consumption ahead. They say this will spill over and an ~8-10% fall in new car sales volumes is a strong possibility, Further evidence of the second order impacts.

Housing auction clearance rates slid to a ~6-year low of ~54%, housing credit growth eased to a >4- year low dragged by investors slumping to a record low, while industry data on owner occupier home loans suggests this also started to drop in May; while home prices are falling the most since 2012. Macroprudential policy is reducing borrowing capacity and leading to a clear weakening of housing, which will continue ahead.

CoreLogic says last week, 1,849 auctions were held across the combined capital cities, returning a final clearance rate of 55.5 per cent, increasing from the previous week when 52.4 per cent of the 2,002 auctions held were successful, the lowest clearance rate seen since late 2012. This time last year, the clearance rate was 66.5 per cent across 2,355 auctions.

Melbourne’s final clearance rate was recorded at 59.9 compared with a clearance rate of 70.7 per last year. Sydney’s final auction clearance rate was 50.1 per cent compared with a clearance rate of 68.2 per cent last year. Across the smaller auction markets, clearance rates improved everywhere except Tasmania, however only 3 auctions were held there over the week. Of the non-capital city auction markets, Geelong returned the highest final clearance rate, with a success rate of 71.4 per cent across 26 auctions.

This week they expect to see a lower volume of auctions this week with CoreLogic currently tracking 1,557 auctions, down from 1,849 last week.

Home prices are falling with the CoreLogic 5-city daily dwelling price index, which covers the five major capital city markets, declined another 0.15%. So far in June home values have fallen 0.24%, driven by Melbourne, Sydney and Perth. So far in 2018, home values have declined by 1.72%, with only Brisbane and Adelaide recording a value increase. Over the past 12 months, home values have fallen by 1.72%, driven by Sydney and Perth. Despite the continuing falls. values are now up 36.2% since the 2010 peak at the 5-city level, driven overwhelmingly by exceptionally strong gains in Sydney at 60.2% followed by Melbourne 42.6% and Adelaide 9.8%. Brisbane is 8.3% and Perth is down 11.4% This is before inflation adjustments, which means in real terms only Sydney and Melbourne prices are ahead.

We see more banks lifting rates on the back of the higher BBSW and LIBOR rates. For example, effective Friday 3 July, ING in Australia said it was making changes to variable rates for existing owner occupier home loan customers. This means interest rates for existing residential home loan customers will increase by 0.10%.

Bank of Queensland announced the variable home loan rate for owner occupiers (principal and interest repayments) will increase by 0.09 per cent, per annum; variable home loan rate for owner occupiers (interest only repayments) will increase by 0.15 per cent, per annum; variable home loan rate for investors (principal and interest and interest only repayments) will increase by 0.15 per cent, per annum; and Owner occupier and investor Lines of Credit will increase by 0.10 per cent, per annum. Anthony Rose, Acting Group Executive, Retail Banking said today’s announcement is largely due to the increased cost of funding. “Funding costs have significantly risen since February this year and have primarily been driven by an increase in 30 and 90 day BBSW rates, along with elevated competition for term deposits.

This just extends the list of players lifting rates, and we think more will follow. So it was interesting to see Bendigo Bank chairman Robert Johanson saying that he believes the RBA has waited too long to move rates. “They’ve been trying to do too much work with monetary policy,” he told Banking Day. “I’m concerned that apart from the impact we’ve already seen on asset values, mortgage rates are going to break from the official cycle and will do so in a disruptive way.” The funding pressures on lenders are emerging at an awkward time for the Turnbull Government, which is required to call a federal election within the next 12 months. A series of out-of-cycle increases across the industry could induce a blistering political response from government politicians who are cognizant of the historical links between election outcomes and mortgage rate rises. Even small hikes would create significant pain as a piece on Nine News, using our mortgage stress data explained.

I discussed the current situation with Economist John Adams this week in an extended interview – see Australia’s Debt Bomb. I recommend this post as we go through the critical issues are how it may play out.

Finally, as we hit the end of the financial year, it’s worth reflecting on the highlights and lowlights of the past year. It has been a bit of a roller coaster, but those with shares invested direct, or via superfunds will have done well, again – as in 9 of the past 10 years has proved to be. We suspect the next 12 months will be less positive, as rising interest rates, trade wars and political tensions all mount. We also have an election ahead, which will also potentially create waves. Trade wars is the area to watch. Our dollar has been sliding through the year, and this is likely to continue next year as we struggle with GDP growth in this volatile environment.

Corporate profits have been growing fast, as companies cut costs and rationalise their businesses and this has translated to higher dividends – and about half have come from the financial services sector overall. Banks will be hard pressed to maintain their dividends ahead, as lending growth slows, pressure on their culture continues thanks to the Royal Commission and regulators exercising their muscles. And the greatest of these is mortgage lending growth which we think will continue to languish. Provisions, which were cut this year, may need to rise ahead as 90 days plus default rates are rising, as wages and cost pressure hit home. Remember also the next round of penalty rate reductions for 700,000 workers in across sectors such as retail will cut pay by 10% comes in 1 July.

Property has done less well, despite being well up over the past year, in that the recent monthly trends are signalling a fall. In some states we will end the year well up, for example Hobart, Adelaide and Melbourne, in others less well. We expect more falls ahead because prices are most strongly linked to credit supply, which is being throttled back. Most centres will be impacted as investors tread water and foreign buyer momentum slows. This might be good news for first time buyers who have been enticed back into the market, partly thanks to recent FTB incentives. We are bearish on the property sector next financial year.

Those needing to get income from savings and deposit accounts have had a torrid time, as banks have cut, and cut again their returns on savings. Many are getting less than inflation, so their hard earned cash has taken a hit. This is likely to continue, despite banks lifting mortgage rates as international funding pressure continues to bite in the months ahead. Households continue to be taxed on their savings at their marginal rate, while those with property get massive tax breaks. If Labor does win the next election, this is set for a shake up!

So overall a mixed year, with some highs and lows, and we think next year will be no different, only more so. Credit trajectory is the one to watch.