We discuss our updated scenarios (not good) and answer viewers questions live in the chat.

We predicted the financial crisis, but what happens now?

Digital Finance Analytics (DFA) Blog

"Intelligent Insight"

We discuss our updated scenarios (not good) and answer viewers questions live in the chat.

We predicted the financial crisis, but what happens now?

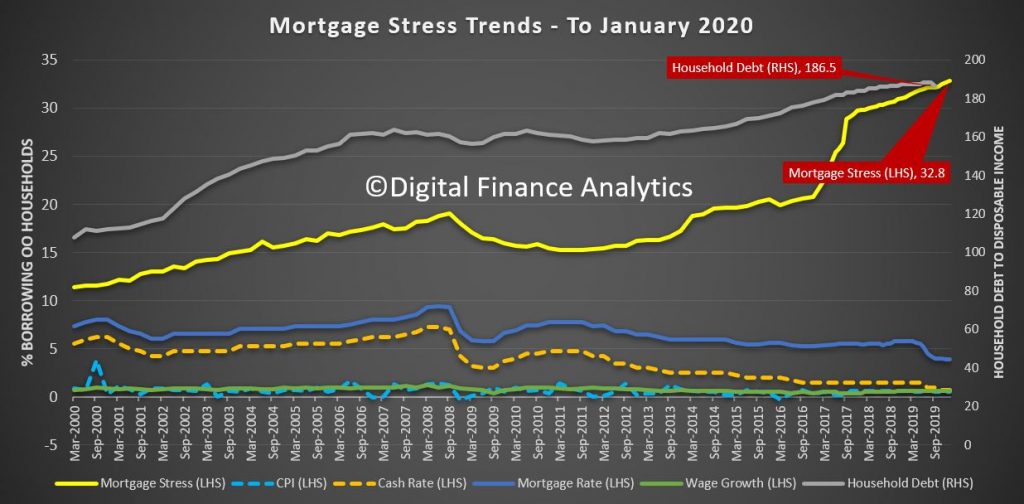

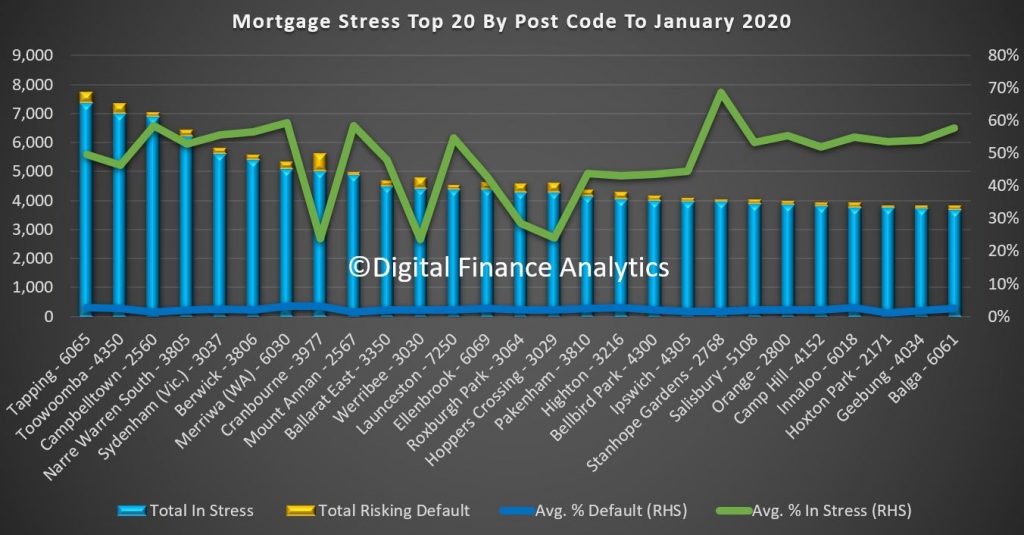

The latest results from our household surveys to end the end of January reveals that mortgage stress continues to push higher with 32.8% of households now impacted, representing more than 1.1 million borrowing households. In addition expectations of defaults are up to more than 83,400 over the next 12 months.

These results are of no surprise, given the ongoing pressure on incomes and rising costs, despite somewhat lower mortgage rates for some borrowers. The banks of course are deeply discounting rates for new loans, but many borrowers are unable to access these “cheap” deals and are stranded on more expensive rates.

Whilst some households who are not stressed continue to pay mortgages down ahead of time (which is why many claim all is well in mortgage-land), the hard fact is that one third of households are facing ongoing financial pressures. These households are not reducing their debt, rather in some cases they are turning to additional finance to try and bridge the cash-flow gap. Or they are raiding savings if they have them, and are putting more on credit cards.

We analyse mortgage stress in cash-flow terms. If a household is paying out more each month including the mortgage repayments, compared with income received, they are in stress. This is not defined by a set proportion of income going on the mortgage. They may have assets they could sell, but nevertheless in cash-flow terms they are underwater.

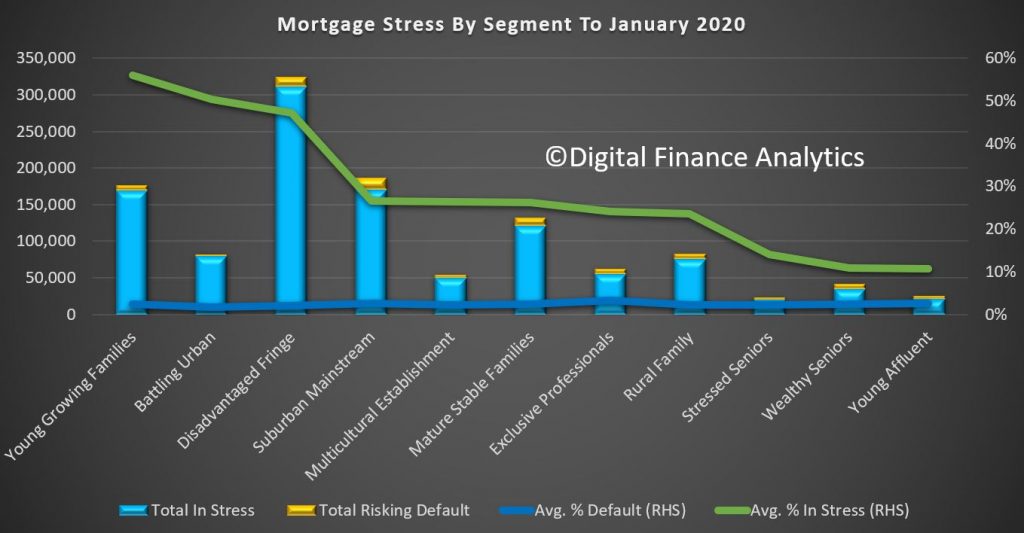

Mortgage stress continues to be visible across most of our household segments, with more than half of young growing families exposed (56%), and this includes a number of recent first time buyers.

Those in the urban fringe, especially on new estates are also exposed (50%) but the largest cohort are in the disadvantaged fringe, where incomes are below average as well. More than 300,000 households in this group are exposed, comprising 47.2% of all household in this segment.

Stress also appears in our more mainstream groups, though at a lower level, and we also see our most affluent segments over-leveraged, with 24% of Exclusive Professionals (the most affluent group) and 10.7% of Young Affluent households impacted. In fact our predicted bank losses are more extreme in these groups, as they have larger mortgages and multiple properties.

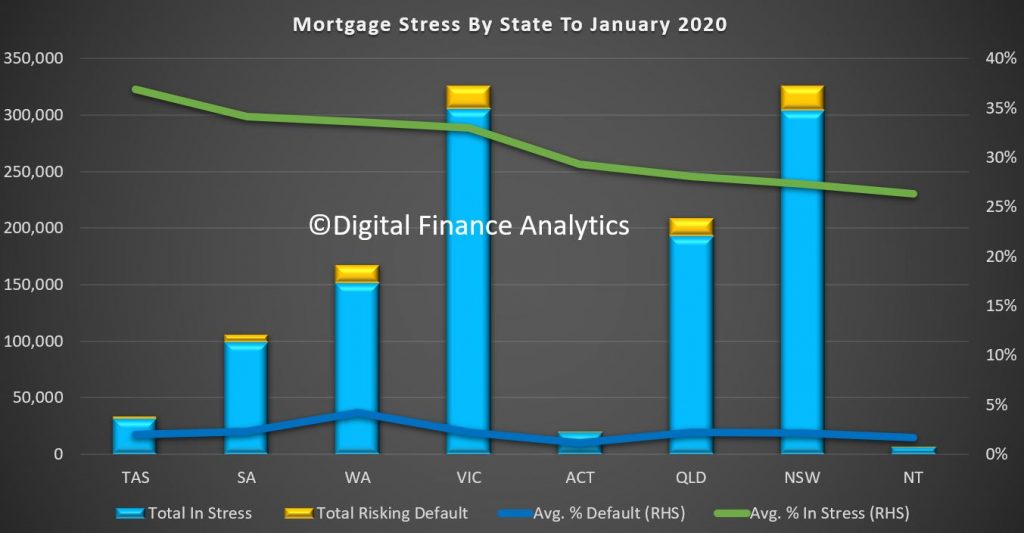

Across the states, 36.9% of households in Tasmania are registering as stressed, which equates to 31,700 households exposed, followed by South Australia at 34.1% (99,700) and Western Australia at 33.6% or 152,000 households. In TAS and SA prices have remained elevated relative to income and housing affordability continues to deteriorate. Victoria has more than 305,000 household in stress, or 32.9%, while Queensland has 193,000 (28.1%) and New South Wales 304,000 (27.3%). The highest rate of default (a forward-looking estimate over the next 12 months) is in WA at 4.2%, while the national average is 2.2%.

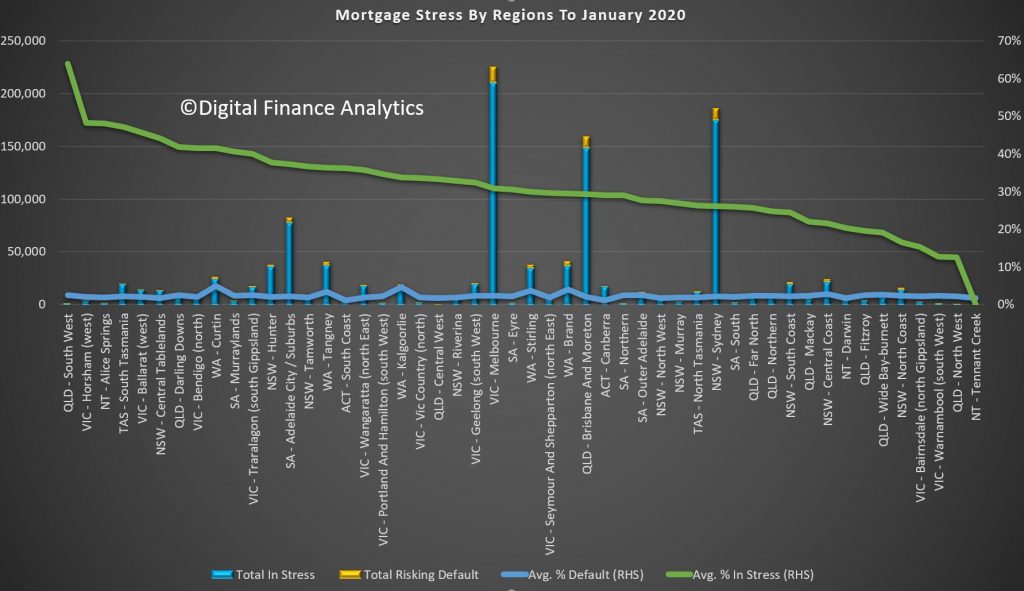

Across the regions, Regional Queensland, Horsham (VIC), Alice Springs and the Southern Half of Tasmania recorded the highest proportion exposed. But the main urban centres of Melbourne, Sydney, Brisbane and Adelaide had the highest counts. Default rates were highest in Curtin WA at 5% and Brand WA (4%). This is driven by multiple years of poor economic performance across the state and underscores that mortgage stress is a precursor to defaults, which tend to occur significantly later. The majority are still working, though income is under pressure. Given current economic headwinds and settings, we expect defaults to continue to rise.

Finally, across the most stressed post codes, WA 6065, which includes Tapping, Wangara and Wanneroo recorded 50% of households in stress, or 7,360 households, followed by Queensland postcode 4350, the area around Toowoomba with 7,000 households in stress, NSW post code 2560, the area around Campbelltown with 6,900 households in difficulty, or 59% of households, and then Victorian post code 3805, the area around Narre Warren, with 6,200 households in stress, which is equivalent to 53% of households.

Most of these areas are fast-growing highly developed suburbs, often on the fringes of our major centres, with many relatively newly built properties on small lots, and often with little local infrastructure. As a result, a significant proportion of income goes on transport costs, and so despite many households having above average incomes, their larges mortgages and high expenses are putting them under continued severe pressure.

Finally, a couple of comments for those in stress, bearing in mind many we survey seem unaware of their plight, because they do not maintain a cash flow. So step one is to draw up a cash flow of money in and money out – ASIC’s Money Smart web site has some excellent tools. Next prioritise spending, and focus on repaying high interest debt (like credit card debt). Third, be cautious of refinancing and restructuring as while this may provide a short term path to relief, unless households in difficulty change their behaviour, it will not be a long-term fix. And finally, do not count on income growth ahead, as given the current economic conditions across the country, we expect wages to remain lower for longer.

And this is a warning too to those contemplating the new first owner incentives. Be conservative in your cash flow estimates, do not count on automatic income acceleration. This would be a path to mortgage stress sooner rather than later.

We plan to publish some stress geo-mapping in a later post.

The Financial Stability Board (FSB) today published two reports that consider the financial stability implications from an increasing offering of financial services by BigTech firms, and the adoption of cloud computing and data services across a range of functions at financial institutions.

BigTech in finance: Market developments and potential financial stability implications

The entry of BigTech firms into finance has numerous benefits, including the potential for greater innovation, diversification and efficiency in the provision of financial services. They can also contribute to financial inclusion, particularly in emerging markets and developing economies, and may facilitate access to financial markets for small and medium-sized enterprises.

However, BigTech firms may also pose risks to financial stability. Some risks are similar to those from financial firms more broadly, stemming from leverage, maturity transformation and liquidity mismatches, as well as operational risks.

The financial services offerings of BigTech firms could grow quickly given their significant resources and widespread access to customer data, which could be self-reinforcing via network effects. An overarching consideration is that a small number of BigTech firms may in the future come to dominate, rather than diversify, the provision of certain financial services in some jurisdictions.

A range of issues arise for policymakers, including with respect to additional financial regulation and/or oversight. Regulators and supervisors also need to be mindful of the resilience and the viability of the business models of incumbent firms given interlinkages with, and competition from, BigTech firms.

Third-party dependencies in cloud services: Considerations on financial stability implications

Financial institutions have used a range of third-party services for decades, and many jurisdictions have in place supervisory policies around such services. Yet recently, the adoption of cloud computing and data services across a range of functions at financial institutions raises new financial stability implications.

Cloud services may present a number of benefits over existing technology. By creating geographically dispersed infrastructure and investing heavily in security, cloud service providers may offer significant improvements in resilience for individual institutions and allow them to scale more quickly and to operate more flexibly. Economies of scale may also result in lower costs to clients.

However, there could be issues for financial institutions that use third-party service providers due to operational, governance and oversight considerations, particularly in a cross-border context and linked to the potential concentration of those providers. This may result in a reduction in the ability of financial institutions and authorities to assess whether a service is being delivered in line with legal and regulatory obligations.

The report concludes that there do not appear to be immediate financial stability risks stemming from the use of cloud services by financial institutions. However, there may be merit in further discussion among authorities to assess: (i) the adequacy of regulatory standards and supervisory practices for outsourcing arrangements; (ii) the ability to coordinate and cooperate, and possibly share information among them when considering cloud services used by financial institutions; and (iii) the current standardisation efforts to ensure interoperability and data portability in cloud environments.

An important discussion about the long, medium and short term economic trends, and how this impacts investment strategy, with Nucleus Wealth‘ s Damien Klassen.

Damien runs the investment side of Nucleus, selecting stocks suggested by analysts and implementing the asset allocation.

Note: DFA has no business or financial relationship with Nucleus Wealth.

Caveat Emptor! Note: this is NOT financial or property advice!! Please note the disclaimer in the show.

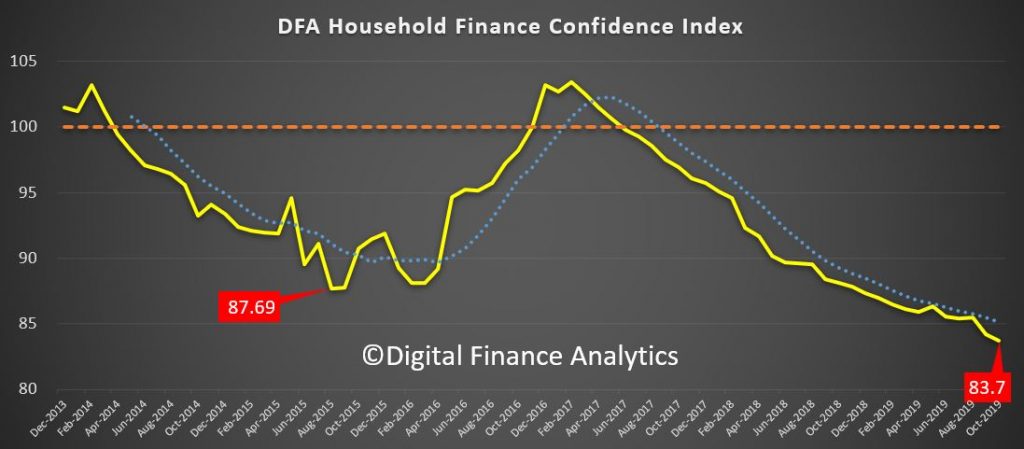

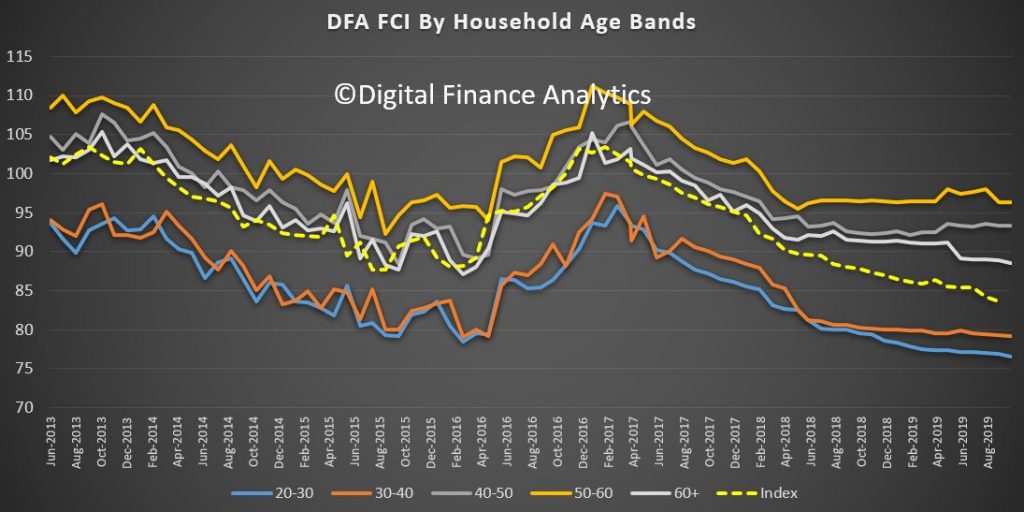

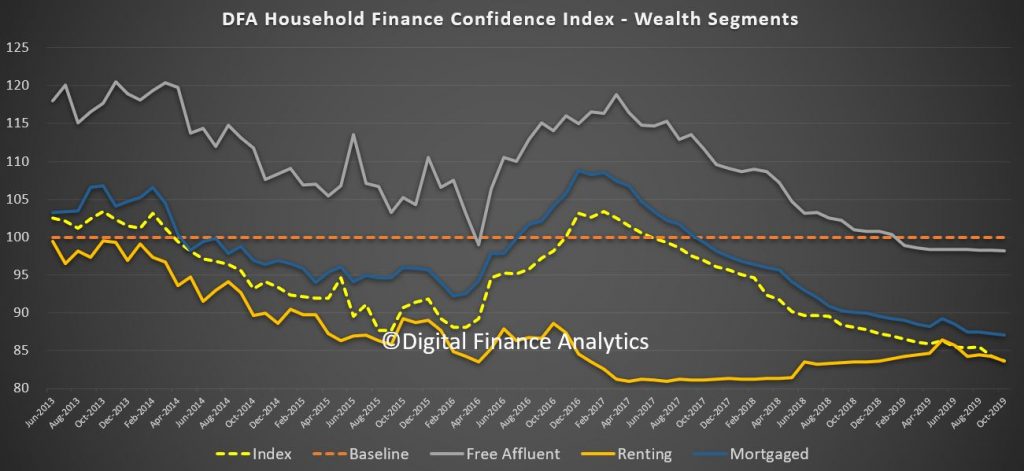

The bad news keeps coming, with the latest DFA Household Financial Confidence Index for October at the lowest ever of 83.7.

This continues the trends of recent months, since dropping through the neutral 100 score in June 2017.

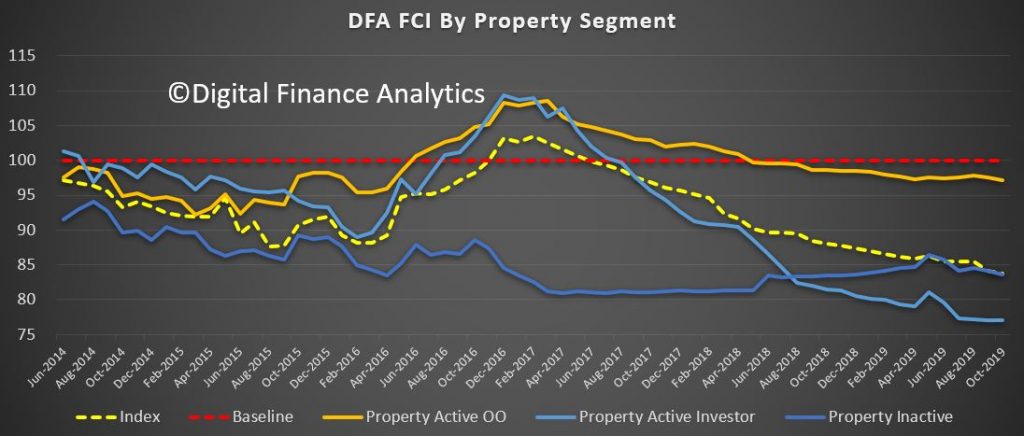

The falls were widespread across our property segments, with investors still way down, under the pressure from low net rental yields, the need to switch to principal and interest from interest only, and worries about construction defects. Owner occupied households were less negative, but those renting continue to struggle with higher levels of rental stress.

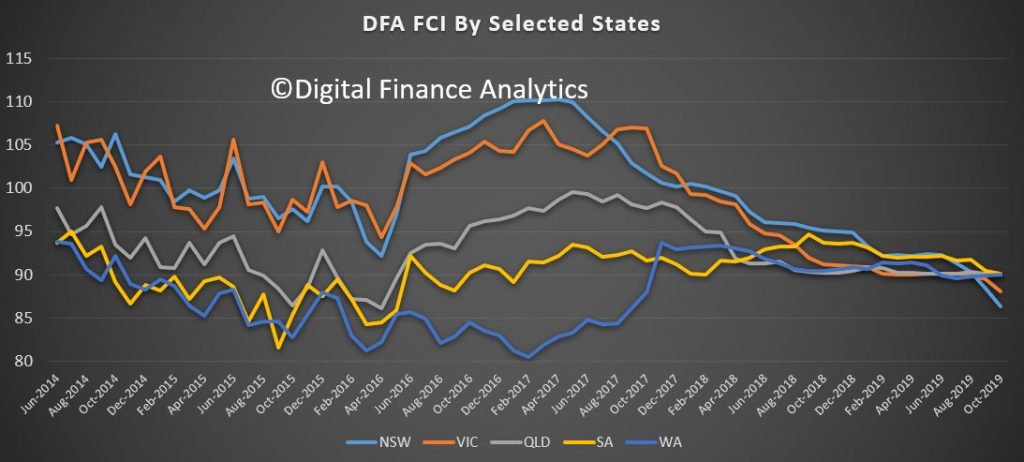

Across the states there were significant falls in NSW and VIC, whilst other states continued to track as in recent months. The main eastern states are now lower than WA and SA, which is a surprising new development.

Across the age bands, the falls are mainly among lower aged groups, while those aged 50-60 are feeling more positive thanks to recent stock market rises.

This is also reflected across our wealth segments, with those holding property mortgage free and other financial assets more positive (though still below neutral) compared with mortgage holders and those not holding property at all.

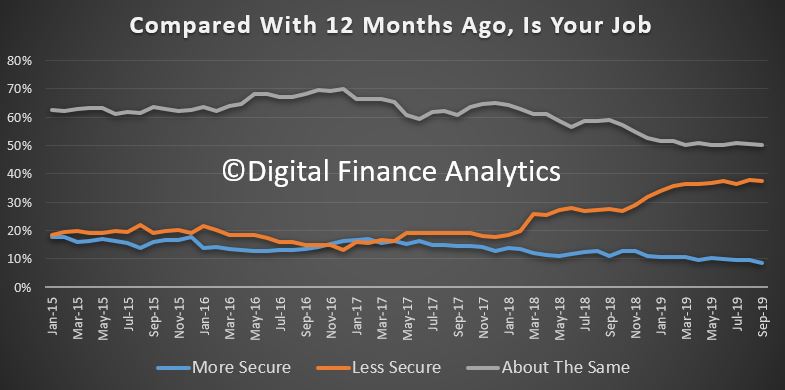

We can then turn to the moving parts within the index, based on our rolling 52,000 household surveys. Employment prospects continue to look shaky, both in terms of under-employment and job security. Jobs in retail and construction and also finance are under-pressure, and the impact of the drought is also hitting some areas. 8% of household felt more secure than a year ago, the lowest read ever in this part of the survey. More households have multiple part-time jobs.

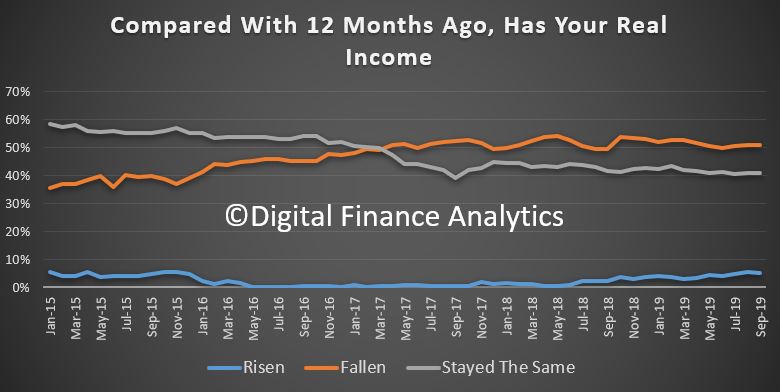

Income remains under pressure, with 51% saying their real incomes have fallen in the past year, while 5% reported an increase, often thanks to switching jobs or employers.

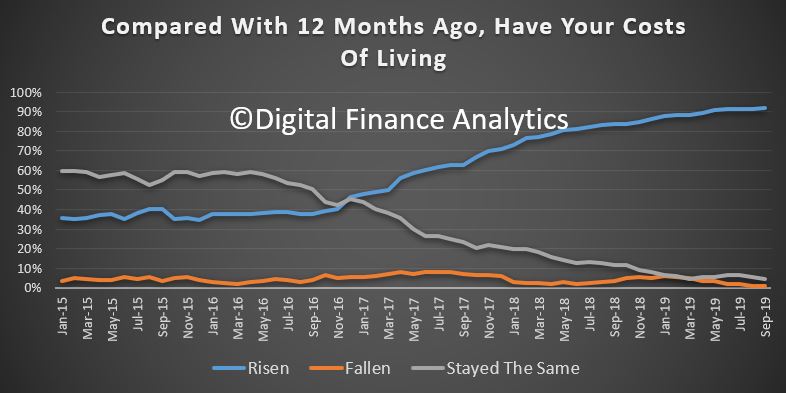

Household budgets are under pressure as costs of living rise, with 91% reporting higher real costs that a year ago, this is a record in our survey. Expenses rose across the board, from child care, health care, school fees and rates. Food costs were higher partly thanks to the drought. There was a small fall in the costs of power, and fuel, but not enough to offset rises elsewhere. Mortgage interest rate falls were blotted up quickly, and the tax refunds where they were received were much lower than people had been expecting.

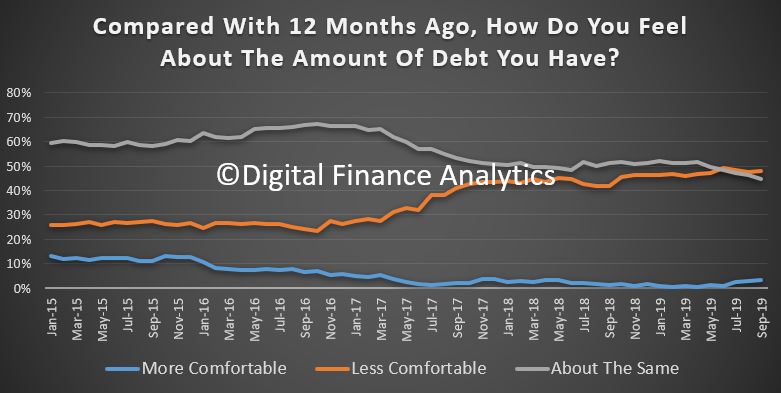

Some households are deleveraging (paying down debt) , while others are more concerned about the amount they owe from mortgages to credit cards and on other forms of credit. 48% of households are less comfortable than a year ago. Lower interest rates are only helping at the margin.

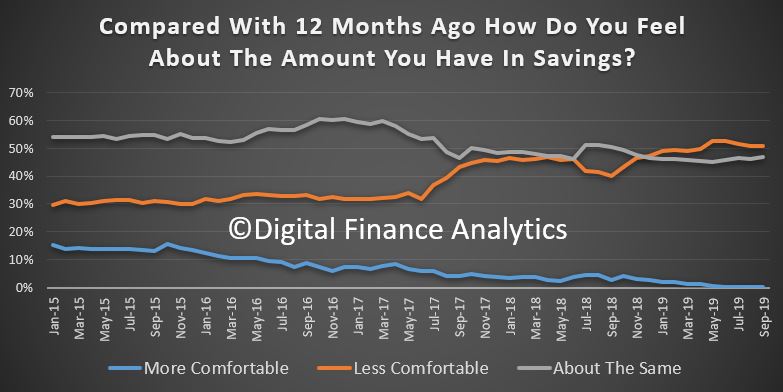

Savings are under pressure from several fronts. Some households are tapping into savings to keep the household budget in check – but that will not be sustainable. Others are seeing returns on term deposits falling away, yet are unwilling to move into higher-risk investment assets. Those in the share markets are enjoying the current bounce, but many expressed concerns about its sustainability. 49% of households are less comfortable than a year ago, while 47% are about the same. Significantly around 27% of households have no savings at all and would have difficulty in pulling $500 together in an emergency. Around half of these households also hold a mortgage. Worth reflecting on this with 32.2% of households in mortgage stress as we also reported today!

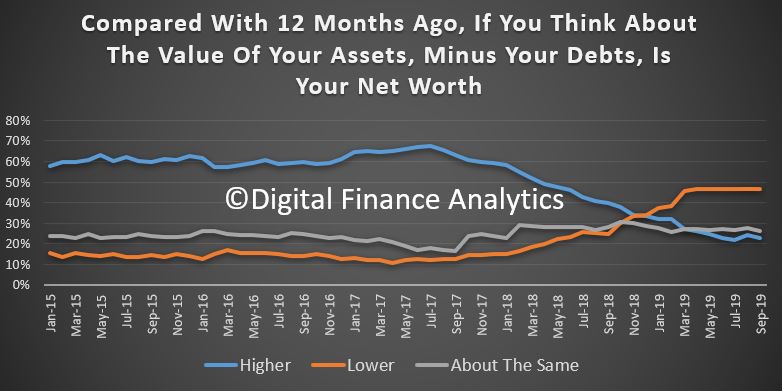

And finally, we consider net worth (assets less liabilities). Here the news is mixed as some households are now convinced their property is worth more citing the recently if narrowly sourced data on rises in Sydney and Melbourne. However other households reported net falls. 24% of households said their net financial position was better than a year ago (up 1.3%), while 45% said they were worse off (down 1.6%). There are also significant regional differences with households in Western Australia and Queensland significantly worse off, while some in inner city areas of Sydney and Melbourne claimed significant advances.

So, overall the status of household confidence continues to weaken, which is consistent with reduced retail activity, and a focus on repaying debt. Unemployment is lurking, but underemployment is real. We also see weaker demand for mortgages ahead, and we will discuss this in more detail in our upcoming household survey release. Without significant economic change, these trends are likely to continue for some time. If the RBA and Government is relying on households to start spending, they will need a very different strategy – including a significant fiscal element. Lower interest rates alone will not cut the mustard.

Following on from our show on Deposit Bail-In, we discuss the Deposit Insurance arrangements in Australian and New Zealand.

What happens in a “gone” situation?

https://www.rba.gov.au/publications/bulletin/2011/dec/pdf/bu-1211-5.pdf

https://www.fcs.gov.au/are-your-savings-protected

We look at deposit bail-in using readily available information from the RBNZ.

https://bankdashboard.rbnz.govt.nz/summary

https://www.rbnz.govt.nz/regulation-and-supervision/banks/open-bank-resolution

See our earlier post for what needs to be done in Australia.

Kudos to Stephen Long from the ABC for an accurate and thoughtful piece on the state of the economy “How a consumer go-slow and a pile of debt is killing the economy“.

I am not just saying this because I featured in the article and news segment on the ABC last night, but because he hits the nail on the head.

In the face of the undeniable weakness, Mr Frydenberg has not dropped the reference to a “strong” economy, instead describing it as “resilient”.

That’s a fair call; a world-record 28 years without a recession is evidence enough

Australia’s weathered the Asian financial crisis of the 1990s, the tech wreck of the 2000s, and the Global Financial Crisis a decade ago without succumbing. But that record has involved some sound management and a lot of luck.

At some stage, the luck will run out.

Alongside spluttering economic growth and households hunkering down at home, a series of risks lurk offshore — a bad Brexit, the US-China trade war, underlying problems in the Chinese economy blowing up among them.

“Any one of those could play us into a GFC 2.0,” says Mr North.

“And if that happens then essentially all bets are off.”

“We are going to see very high levels of unemployment, we’re going to see a lot of households defaulting on their mortgages and that would have a spillover effect on the economy. That would hit the banks and take us into a very dark corner, in my view.”

In recent times, it’s only been population growth that’s kept Australia out of recession. More people have created more demand but high immigration has also helped to suppress wages.

While the pie’s been growing larger, the slices have been getting smaller (leaving aside the distribution of the pie, which is skewed towards those at the top).

Per head, living standards have fallen — a phenomenon that’s been dubbed a “per capita recession”.

The government and the RBA will be banking on the tax cuts which commenced in July and interest rate cuts to lift the economy out of the doldrums. If we’re lucky, things may start to turn around.

But if the luck runs out, there could be far worse to come.

We look at the latest ABS stats on household wealth. How do falls in real estate values compare with recent lifts in share prices?

Property expert Joe Wilkes and I discuss some of the hidden traps when budgeting for a mortgage.