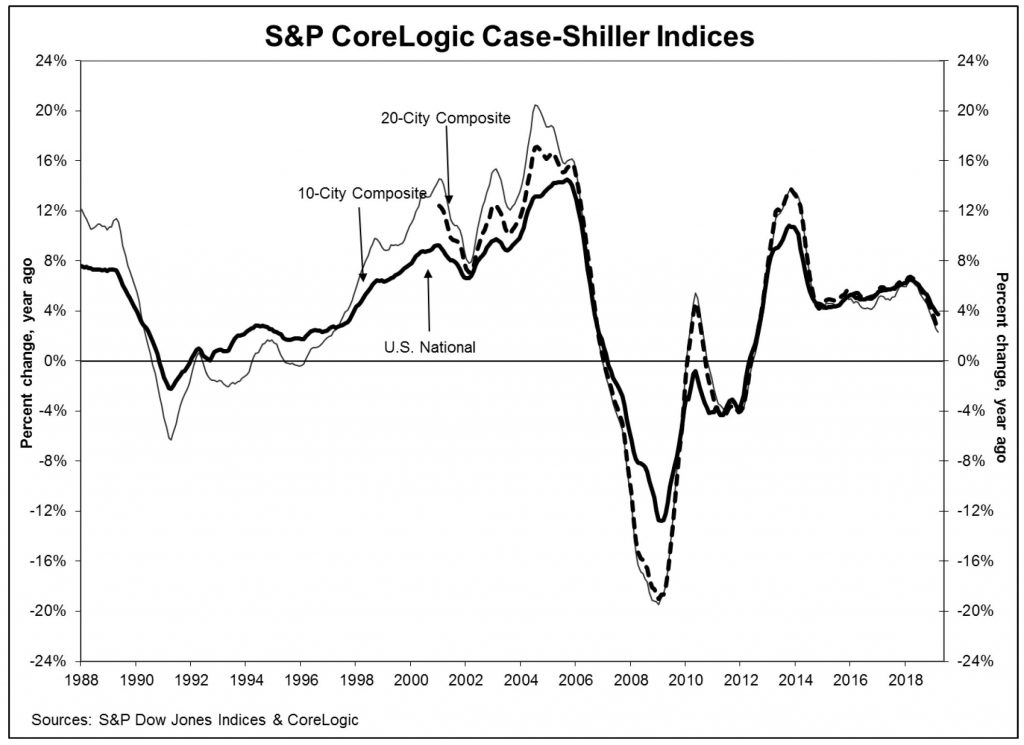

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a 3.7% annual gain in March, down from 3.9% in the previous month. The 10-City Composite annual increase came in at 2.3%, down from 2.5% in the previous month. The 20-City Composite posted a 2.7% year-over-year gain, down from 3.0% in the previous month.

Las Vegas, Phoenix and Tampa reported the highest year-over-year gains among the 20 cities. In March, Las Vegas led the way with an 8.2% year-over-year price increase, followed by Phoenix with a 6.1% increase, and Tampa with a 5.3% increase. Four of the 20 cities reported greater price increases in the year ending March 2019 versus the year ending February 2019.

“Home price gains continue to slow,” says David M. Blitzer, Managing Director and Chairman of the Index Committee at S&P Dow Jones Indices.

“The patterns seen in the last year or more continue: year-over-year price gains in most cities are consistently shrinking. Double-digit annual gains have vanished. The largest annual gain was 8.2% in Las Vegas; one year ago, Seattle had a 13% gain. In this report, Seattle prices are up only 1.6%. The 20-City Composite dropped from 6.7% to 2.7% annual gains over the last year as well. The shift to smaller price increases is broad-based and not limited to one or two cities where large price increases collapsed. Other housing statistics tell a similar story. Existing single family home sales are flat. Since 2017, peak sales were in February 2018 at 5.1 million at annual rates; the weakest were 4.36 million in January 2019. The range was 650,000.

“Given the broader economic picture, housing should be doing better. Mortgage rates are at 4% for a 30-year fixed rate loan, unemployment is close to a 50-year low, low inflation and moderate increases in real incomes would be expected to support a strong housing market. Measures of household debt service do not reveal any problems and consumer sentiment surveys are upbeat. The difficulty facing housing may be too-high price increases. At the currently lower pace of home price increases, prices are rising almost twice as fast as inflation: in the last 12 months, the S&P Corelogic Case-Shiller National Index is up 3.7%, double the 1.9% inflation rate. Measured in real, inflation-adjusted terms, home prices today are rising at a 1.8% annual rate. This compares to a 1.2% real annual price increases in housing since 1975.”

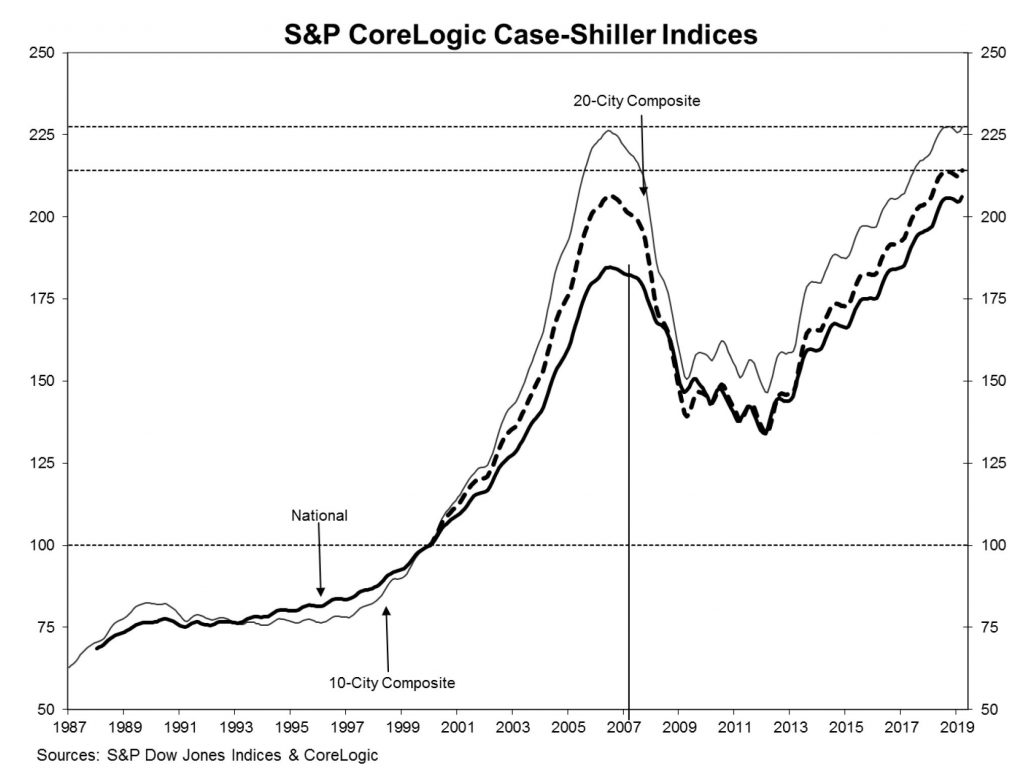

One other point to note, after the 2007 financial crisis, home prices continued to fall for a further three years. A salutatory warning to those in Australia who think prices are about to rebound! In fact it took more than a decade for prices to return to their 2007 levels.

Despite the recent surge of optimism regarding the property market, one financial analyst feels that the relief is misplaced, via Australian Broker.

“There are some people now claiming that property prices have hit

bottom and it’s all up and away from here. But then, there are others

who rightly focus on the burden of debt, which is very big and means

there will be some limitation to how far property prices can reverse,”

explained Martin North, principal of Digital Finance Analytics.

“There is significantly more interest in property now than there was a

few weeks ago, yes. But the jury is still out on whether that will

translate to sustainable reductions in the fall of home prices, and

rises ahead. The probability of coming into a property boom anytime soon

is very limited.”

According to North, a large part of the issue lies in a crucial and crippling disparity in supply and demand.

ABS data reports there are more than one million vacant properties in

Australia currently, yet 200,000 new dwellings are scheduled to be

built in the next two years.

Aspiring housing market entrants are being barred by tightened

lending, immigration has stagnated and investors are not only

disinterested in returning to the market, but many are actively trying

to sell the properties they do have.

“That’s why I’m still thinking that there’s plenty of room on the

downside for property values to continue to fall,” explained North.

Even the initiatives recently proposed, such as APRA changing the

servicing rate floor or the promised first home buyer scheme, are likely

to have only a “small and positive effect, not a dramatically large

one.”

“We’ve still got the very high level of household debt, we’ve still

got very high levels of mortgage stress, we’ve still got the banks tight

on their lending standards,” the anaylst reminded.

While North feels confident that the last 18 months of property

values sliding is outside the natural ebb and flow of the housing market

and indicates the presence of a deeper issue, he doubts the validity of

using home prices as the key indicator of the state of the economy.

He explained that there are too many factors that play into the

property market for it to be an accurate litmus test, calling it “a

follow up, rather than a lead indicator.”

Instead, he suggested attention should be given to monitoring any

significant rises in unemployment, mortgage defaults, or the consumer

price index.

Property expect Joe Wilkes and I discuss the latest New Zealand data, and consider the drive to attract first time buyers in both NZ and Australia. What does the data say?

It is time for a new way of talking about housing in Australia. The housing crisis is quickly turning into a crisis of care.

We call on the newly re-elected Morrison government and new Housing

Minister Michael Sukkar to recognise that the value of housing is not

just economic. Housing is an infrastructure of care. Australian

governments need to ask: is this a housing system that cares?

A location for essential care

Houses are hubs of care practices and relations. They are places of

everyday care, of cooking, cleaning and washing, of care between

household and family members. Houses are where we care for children,

elders, partners and ourselves.

Houses are also anchors for community and neighbourhood-based care.

We keep an eye on neighbours’ homes, support older neighbours to age in place, and care for pets.

This care work is what keeps us alive.

Even though care is not always done well, it is an essential practice

that is connected in fundamental ways with housing. Without housing it

can be very difficult to meet basic needs.

The care work of housing

But housing is more than just a place where care takes place. Housing

systems – through housing policy, markets and design – organise the

distribution of care and the ability of people to give and receive care.

In our research this drives us to ask: how does the housing system support or limit the capacity of households to care?

We argue that housing is a care infrastructure and call for this understanding of housing to be at the centre of housing reform.

Home owners benefit

In Australia we value housing as an individual investment and asset. The economic values of housing (how much we can buy, sell or otherwise leverage housing for) are at the heart of how housing is usually discussed.

For affluent households housing markets can work very well as a care

infrastructure. This is because these households can more readily afford

housing that meets household care needs. They are also more able to

invest in housing to cover the costs of care in later life and to

support the needs and ambitions of children. For home owners housing is a

private welfare net for funding care needs.

Australian housing and related policies create and reinforce the

value of home ownership. Subsidies for first home owners, the proposed

First Home Loan Deposit Scheme (which will be a focus of efforts by the new housing minister),

preferential treatment for owner occupation in pension tests and tax

breaks for investor landlords underpin the value of home ownership as an

infrastructure of care.

However, for the growing numbers of households not in a position to

own a home the picture is less rosy. In many cases housing becomes an

infrastructure that inhibits access to necessary care. As increasing numbers of households rent for longer periods, we risk a housing system that only cares for some.

Housing affordability

Housing affordability is a central concern. Lower income earners have

less ability to choose to live in places that are well serviced or

where family-based care networks are located. Less affluent areas often

have less access to public and private care services like doctors and other specialists.

Housing affordability also shapes the ability to afford other care

resources like quality food and electricity. Households that face high

housing costs are often forced to compromise in these areas.

In Emma’s and otherrelated research

older retirees in the private rental market depended on local food

charities for nutritious food. And in winter they restricted their use

of heating to avoid bill blow-outs.

There are also connections between paid work, caring capacity and

housing affordability. High-cost housing markets can drive people to

work longer hours and multiple jobs, or require multiple income earners

within a household. This can reduce the ability of individuals and

households to meet domestic care responsibilities.

Tenure and care

Non-home owners also face restrictions around their use of private rental properties. For a start, rental housing is notoriously insecure. There are also restrictions on the ability of renters to make a house into a home.

Private rental legislation typically does not require landlords to

agree to property modifications to meet the needs of a person with

disability or ageing body, even when tenant-funded.

Women in Emma’s research reported losing bonds to cover costs associated with removing modifications that had been agreed to during a tenancy. In Kathy’s research,

the fear of eviction meant private renters found it difficult to ask

for and be granted repairs that would make their homes habitable. They

endured leaking roofs and mouldy walls that made housing unsuitable for

meeting basic care needs.

As growing numbers of households find themselves locked out of home

ownership and face difficulties securing affordable housing in our expensive private rental markets, Australia badly needs housing reform.

The care work of housing must be at the centre of housing policy. The

new government and minister for housing must ask: first, is this a

housing system that cares? And, second, who does this housing system

care for?

Historically, this question has been answered with calls to increase

home ownership. But there is value in a diverse housing system because

different households have different needs.

Further, those who invest in housing are dependent on the people who will rent that housing. These people in turn have the right – and need – for housing that supports their care needs. Affordable housing is only the starting point.

Authors: Emma Power, Senior Research Fellow, Geography and Urban Studies, Western Sydney University; Kathleen Mee, Associate Professor of Geography, University of Newcastle

It used to be that everyone wanted to buy a home, seeking pleasure and security, as well as the potential for future wealth.

But younger Americans are buying homes far less often than their

elders’ generations did, and that puts a large sector of the U.S.

economy at risk.

Millennial home ownership levels

are dramatically lower than the those of previous generations at a

similar age. In 1985, 45.5% of 25- to 34-year-olds owned homes in the

U.S. By 2015, this had fallen about 25%.

Researchers like me

who are interested in the future of the U.S. economy are faced with

some difficult questions about how millennials’ behavior is changing the

housing market.

My recent research suggests that both increases and decreases in home

prices can be directly tied to where millennials choose to live. If a

long-term behavioral change is afoot, and this generation continues not

to buy homes, it will very directly impact GDP.

Homeownership

Research has shown that younger generations lag behind previous generations in terms of milestones like homeownership and marriage.

One of the assets that set previous generations apart is home equity.

In 2001, Gen-Xers held an average of US$130,000 in assets, compared to

millennials in 2016 that held almost 31% less.

However, assets attributed to home equity are subject to the whims of the housing market. Just ask anyone still underwater on a home purchased before the financial crisis.

And home equity isn’t just vulnerable to large-scale economic upheavals. In fact, it’s constantly fluctuating.

Age and cost

I analyzed data from the U.S. Census Bureau and American Community

Survey from about 800 of the most populous counties in the U.S., or

about 85% of the population, in a study that has not yet been published.

The data show a rather disconcerting trend.

If no one ever moved from one county to another, almost all counties would gradually grow older in terms of average age.

However, the migration of primarily younger individuals has caused an

escalation in this aging shift. Some areas are aging much more quickly

than expected. In those areas, home prices have been vulnerable to

long-term declines.

In other words, the trend of rising or falling home values follows patterns of migration in the U.S.

From 2010 to 2016, counties with aging populations were about 50%

more likely to have experienced a decline in home values than those

counties that were becoming “younger.” Not surprisingly, counties that

were becoming younger were often experiencing increases in both

populations and in the prices of homes.

Two areas that provide an illustration of this are key to the oil and

gas industry: the Midland-Odessa area of Texas and Ward County, North

Dakota. Both areas have experienced not only a net decrease in the age

of residents, but also a net increase in population.

This is far from a rural phenomenon. In Allegheny County, the

Pennsylvania county that’s home to Pittsburgh, a similar increase in

population has also decreased the average age of its residents.

In 2018, such transactions are reaching levels just below the

pre-crisis highs, accounting for almost 11% of all homes sold last year.

The prices are inflated by buyers looking to “flip” houses. This forces

younger buyers to compete with the professionals, pushing them out of

the markets they are migrating to.

Younger buyers are further frustrated by the cost of what economists refer to as frictions. Frictions include commissions that average 5% to 6%

of the purchase price, myriad inspection and appraisal fees, as well as

mortgage and title insurance. All of this runs counter to the

transparency and ease of access many millennials have become used to in

the modern world.

Since the younger generation is better educated,

one might expect significant wage increases to counter some of these

frictions. But recent graduates between the ages of 22 and 27 earn about 2% less than their predecessors did in 1990.

If home prices

had also stayed relatively flat, this likely wouldn’t be an issue.

However, from 2000 to the present, average home prices have increased by

about 3.8% annually, though this varies dramatically from county to

county.

As urban areas continue to attract more new residents, many young

people may need to reassess the true value that home ownership offers.

Meanwhile, older generations are likely just becoming aware of the

impact of millennial migration on the American dream. If you live in an

area that is aging faster than the natural rate, the probability of your

home value decreasing is very real.

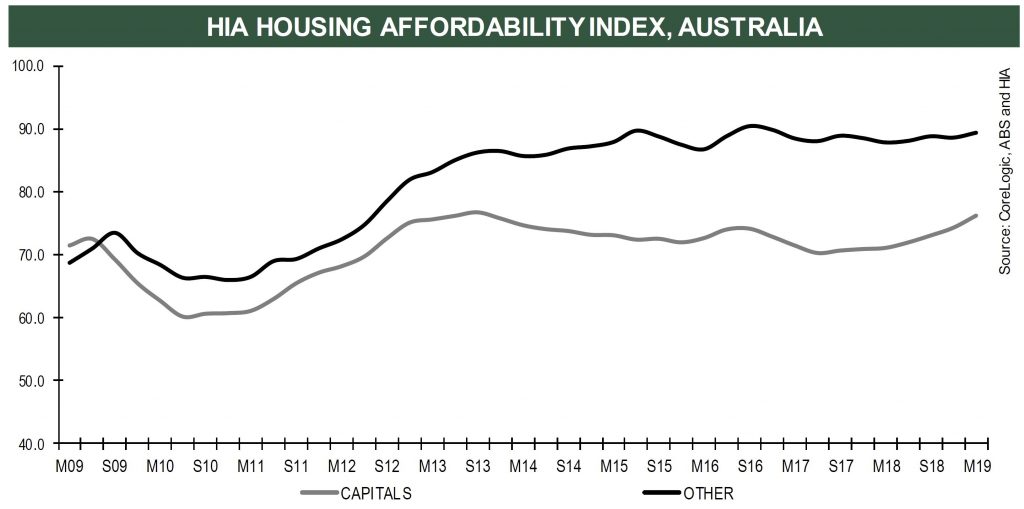

The HIA reported today that there was been a 10% improvement in affordability in a year. They attribute this to – wait for it, more building and wage rises – but do not mention the elephant in the room, the home price falls, which are continuing – at more than 10% in Sydney and Melbourne! No surprise, as home prices fall, affordability improves…

Five of the eight capital cities saw improved affordability over the year to March 2019. Sydney continues to be home to the greatest improvements, its index is up by 12.4 per cent. This was followed by Melbourne (+9.6 per cent), Perth (+7.7 per cent), Darwin (+5.9 per cent) and Brisbane (+2.5 per cent). Affordability deteriorated in Hobart (-5.1 per cent), Canberra (-5.1 per cent) and Adelaide (-1.1 per cent).

HIA’s Affordability Index is calculated for each of the eight capital cities and regional areas on a quarterly basis and takes into account the latest dwelling prices, mortgage interest rates and wage developments.

“The HIA Affordability Index rose by 2.2 per cent in the March 2019 quarter to post the most significant improvement in affordability since September 2013,” said Tim Reardon, HIA Chief Economist.

“The improvement in housing affordability has been experienced across the country, with the exception only of Tasmania and the ACT, where ongoing house price growth has seen affordability remain static,” added Mr Reardon.

“The boom in home building of the past five years is a key factor behind the improvement in housing affordability. With completions of new homes remaining at elevated levels, affordability is poised to continue to improve.

“Wage growth also contributed to the improvement in affordability.

“The improvement in affordability is most significant in east coast capital cities. Affordability in Sydney deteriorated to an extent that in June 2017 it required two average Sydney incomes to be able to afford repayments on an average Sydney home. In just over a year this has improved to only requiring 1.8 standard incomes to purchase the same home.

“Similarly, in Melbourne the Affordability Index has improved by almost 10 per cent in a year,” concluded Mr Reardon.

The Tasmanian Government announced yesterday that they have extended their first home builders grant.

The Hodgman Liberal Government is a strong supporter of our building and construction industry, and we want to boost dwelling construction so more Tasmanians can be in a position to own their own home.

The Hodgman Liberal Government will extend the first home builders grant in the upcoming budget so more young Tasmanians can realise the dream of building their first home.

The extension comes after we doubled the first home builders grant to $20,000 in the 2016-17 Budget.

We understand that there is high demand for new housing, and the first home builders grant is one part of our multi-pronged approach to address housing stress in Tasmania.

According to the latest ABS figures, Tasmania continues to lead the nation in the annual growth in building approvals.

The number of dwelling approvals grew 24.1 per cent in March 2019 compared to March 2018, with Tasmania one of only two jurisdictions to record growth. This is in stark contrast to the sharp fall in National approvals, which was down by 22.4 per cent over the same period.

This initiative will give Tasmanians a greater opportunity to build and own their own home, adding to supply, and complementing the action the Government is taking through our Affordable Housing Strategy.

The extension of the grant will have positive flow-on effects for Tasmania’s booming building and construction industry, creating more work, and more jobs.

Tasmanian prices are still rising, as MyStateBank media release from 9th May reveals.

Median house prices are falling across most parts of the country, yet Hobart is bucking the national trend. Dwelling values in Hobart grew by 3.8% in the year ending April 2019, the highest of all other capital cities and one of only three capital cities to experience growth. Nationally, house price growth fell 7.2% over the same period.

“Australian homeowners see the appeal of selling up in markets like Sydney and Melbourne and buying in Tasmania, where it is more likely they’ll be able to afford a bigger property for a much cheaper price. The state’s strong economic conditions and attractiveness as a lifestyle choice are also big drawcards for residents on mainland Australia, fuelling housing demand,”

“A tightening in credit supply is also driving prospective buyers out of larger property markets like Melbourne and Sydney where demand from investors and owner occupiers has dampened.”

In fact, Tasmania is the only state to have experienced an increase in mortgage applications (+1.5%) over the year to December 2018. Mortgage applications in Victoria and New South Wales fell over the same period by 15.4% and 19.1% respectively.

Pressure on Tasmanian rental market unlikely to continue in the long term.

“Population growth and lack of new housing supply is putting considerable pressure on the Tasmanian rental market.”

MyState’s analysis shows Hobart’s strong rental yield position has increased to 5.2% in the year to April, the highest in the country. The median weekly house rent is $450 – now $10 more than Melbourne.

However, the issue of a lack of housing supply is unlikely to be a long-term one, with the state recording nation leading growth in the number of residential building approvals at 24% from March 2018 to March 2019.