The latest and updated edition of our flagship report “The Property Imperative” is now available on request with data to April 2018.

This Property Imperative Report is a distillation of our research in the finance and property market, using data from our household surveys and other public data. We provide weekly updates via our blog – the Property Imperative Weekly, but twice a year publish this report. This is volume 10.

Residential property, and the mortgage industry is currently under the microscope, as never before. The currently running Royal Commission has laid bare a range of worrying and significant issues, and recent reviews by the Productivity Commission and ACCC point to weaknesses in both the regulation of the banks and weak competition in the sector. We believe we are at a significant inflection point and the market risks are rising fast. Portfolio risks are being underestimated. Many recent studies appear to support this view. There are a number of concerning trends.

Around two thirds of all households have interests in residential property, and about half of these have mortgages. More households are excluded completely and are forced to rent, or live with family or friends.

We have formed the view that credit growth will slow significantly in the months ahead, as lending standards tighten. As a result, home prices will fall. We note that household incomes remain flat in real terms, the size of the average mortgage has grown significantly in the past few years, thanks to rising home prices (in some states), changed lending standards, and consumer appetite for debt. In fact, consumer debt has never been higher in Australia. Household finances are being severely impacted, and more recent changes in underwriting standards are making finance less available for many. But the risk is in those loans made in recent years under looser standards, including interest only loans.

Property Investors still make up a significant share of total borrowing, and experience around the world shows it is these households who are more fickle in a downturn. Many use interest only loans, which create risks downstream, and regulators have recently been applying pressure to lenders to curtail their growth. Already we are seeing a drop in investor loans, and a reduction in interest only loans. A significant proportion will be up for review within tighter lending rules. This may lift servicing costs, at very least and potentially cause some to sell.

We hold the view that home prices are set to ease in coming months, as already foreshadowed in Sydney. We think mortgage rates are more likely to rise than fall as we move on into 2019.

We will continue to track market developments in our Property Imperative weekly video blogs, and publish a further update in about six months’ time.

If you are seeking specific market data from our Core Market Model, reach out, and we will endeavour to assist.

Here is the table of contents.

1 EXECUTIVE SUMMARY

2 TABLE OF CONTENTS

3. OUR RESEARCH APPROACH

4. THE DFA SEGMENTATION MODEL

5 PROFILING THE PROPERTY MARKET

5.1 Current Property Prices

5.2 Property Transfer Volumes Are Down

5.3 Clearance Rates Are Easing

5.4 But Can We Believe the Auction Statistics Anyway?

6 MORTGAGE LENDING TRENDS

6.1 Total Housing Credit Is Up

6.2 ADI Lending Trends

6.3 Housing Finance Flows – Bye-Bye Property Investors

6.4 The Rise of the Bank of Mum and Dad

6.5 Lending Standards Are Tightening

6.6 How Low Will Borrowing Power Go?

6.7 The Portfolio Mix Is Changing

6.8 Funding Costs Are Higher

6.9 The Interest Only Loan Problem

7 HOUSEHOLD FINANCES AND RISKS

7.1 Households’ Demand for Property

7.2 Property Active and Inactive Households

7.3 Cross Segment Comparisons

7.4 Property Investors

7.5 How Many Properties Do Investors Have?

7.6 SMSF Property Investors

7.7 First Time Buyers.

7.8 Want to Buys

7.9 Up Traders and Down Traders

7.10 Household Financial Confidence Continues to Fall

7.11 Mortgage Stress Is Still Rising

7.12 But The RBA Is Unperturbed

7.13 Latest Household Debt Figures a Worry

8 THE CURRENT INQUIRIES

8.1 Productivity Commission

8.2 The ACCC Mortgage Pricing Review

8.3 The Royal Commission into Misconduct in Finance Services

8.4 Merge Financial Advice and Mortgage Brokering Regulation

9 AN ALTERNATIVE FINANCIAL NARRATIVE

9.1 Popping The Housing Affordability Myth

9.2 The Chicago Plan

10 FOUR SCENARIOS

11 FINAL OBSERVATIONS

12 ABOUT DFA

13 COPYRIGHT AND TERMS OF USE

Request the free report [85 pages] using the form below. You should get confirmation your message was sent immediately and you will receive an email with the report attached after a short delay.

Note this will NOT automatically send you our ongoing research updates, for that register here.

[contact-form to=’mnorth@digitalfinanceanalytics.com’ subject=’Request for The Property Imperative Report 10′][contact-field label=’Name’ type=’name’ required=’1’/][contact-field label=’Email’ type=’email’ required=’1’/][contact-field label=’Email Me The Report’ type=’radio’ options=’Yes Please’ required=’1′ /][contact-field label=’Comment If You Like’ type=’textarea’/][/contact-form]

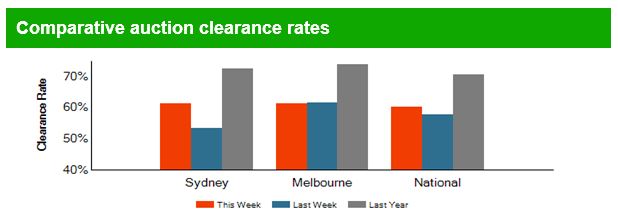

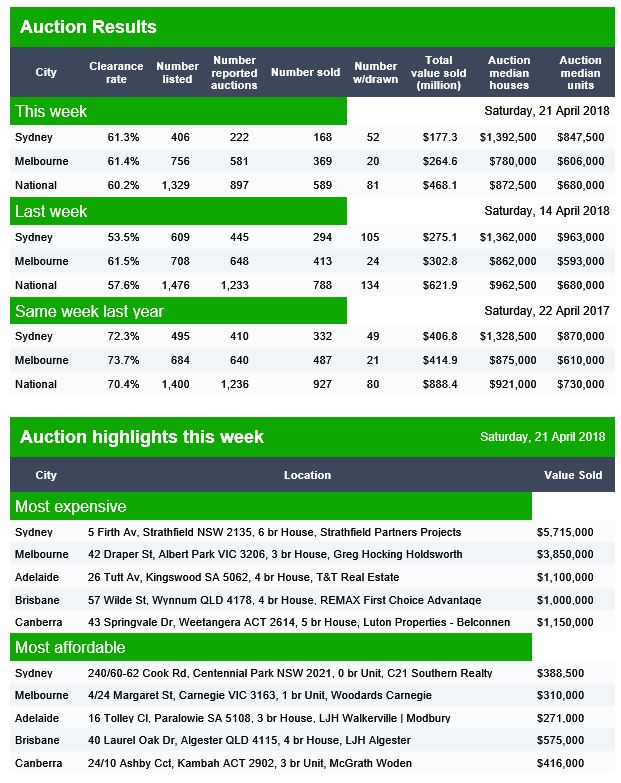

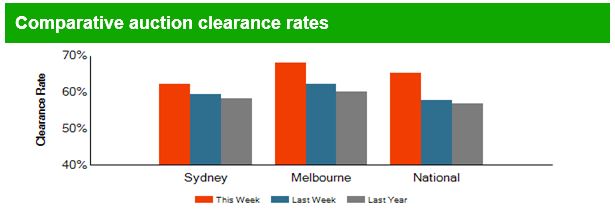

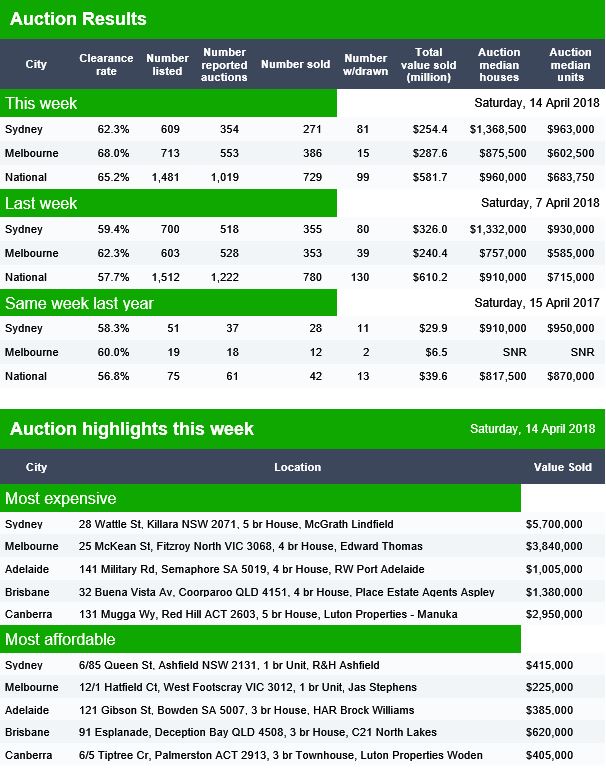

Auction activity remains relatively steady across the combined capital cities this week, with a total of 1,746 homes taken to market, returning a success rate of 63.1 per cent increasing from last week’s final clearance rate which saw the lowest weighted average result so far this year at 61.7 per cent (1,915 auctions).

The results segregated by property type showed that units outperformed houses this week, with 65 per cent of units selling, while the combined houses returned a 62.2 per cent success rate; conversely the house market accounts for a higher proportion of overall auction activity.

Melbourne saw a total of 905 auctions take place this week, returning a 63.8 per cent preliminary clearance rate, which was slightly higher than the 62.4 per cent over the week prior when 873 auctions were held.

The number of homes taken to auction across Sydney fell this week, with 551 held. The lower volumes returned a higher week-on-week clearance rate with 66.4 per cent of properties reportedly selling, increasing on the week prior’s 61.5 per cent final clearance rate when volumes were higher (795).

The performance across the smaller auction markets continues to be quite varied, with Tasmania returning the highest preliminary clearance rate of 75 per cent, while only 19 per cent of auctions were successful across Perth.

Property investors are more likely to support foreign investment in the property market than people without such investments, we have found in a survey of Sydneysiders’ views about foreign real estate investment. Perhaps more surprising, would-be buyers, who might be expected to worry about demand pushing up prices, were also more likely to be supportive than those who were not looking to buy a property.

We reported previously that over 60% of Sydneysiders do not want more individual foreign investment in residential real estate in Sydney.

Within this context, we surveyed almost 900 people in Sydney to examine the relationships between home ownership, real estate investment, housing stress and views about foreign investment. Our analysis shows:

Those who have property market investments are more likely to be supportive of foreign investment than those who don’t have such investments.

Comparing those who are in housing stress to those who are not in housing stress, there are no significant differences in the two groups’ beliefs about foreign real estate investment.

One group with a strong interest in Sydney’s real estate market are local real estate investors. We were interested in whether those with investment properties and those without differed in their views about individual foreign investment in residential real estate.

We found those with investment properties were likely to be more supportive of foreign investment in Sydney’s housing market than those without investment properties.

For example, 29% of the investment property owners agreed that “foreign investors should be able to buy properties in Sydney” compared to 17% of those without investment properties. They were similarly supportive of foreign students being allowed to buy properties while studying in Australia, with 32% agreeing with this compared to 19% among those without investment properties.

Property investors were more positive about the government’s regulation of foreign investment as well: 28% agreed it has been effectively regulated, compared to 16% of those without investment properties.

House hunters’ views

House prices in Greater Sydney have increased rapidly over the last decade and household debt has grown too.

We might expect people who are actively looking to buy a property to be particularly concerned about foreign real estate investment, as they may feel they are competing against and being priced out of the market by foreign buyers.

For this reason, we asked survey participants whether they were actively looking to buy a property. In response, 23% said they were. Of this group, 31% agreed that foreign investors should be able to buy properties in Sydney, compared to 15% of those not looking for a property.

Housing-stressed households’ views

Increasing mortgage and rental costs are a source of discontent within Sydney’s population. Measurements of housing stress are disputed, but are nonetheless used to give a comparative value to how hard it is for a household to meet housing costs. A ratio of housing costs to income of 30% and above is a common benchmark for housing stress.

Using this measure, we found that more than half (52%) of our survey participants were experiencing housing stress. Another 33% spent less than 30% of their income on their housing and 15% indicated they did not know.

Comparing those over the 30% threshold with those who spend less of their income on housing, we found no significant differences in beliefs about foreign real estate investment.

Other drivers of concern

We found those who are active in the local real estate market remain concerned about foreign investment in general.

If housing stress levels do not lead to differences in attitudes to foreign investment, as our findings suggest, cultural or other factors may be at work in the general discontent about foreign investors in Sydney.

We need to investigate further how being active in the housing market informs Sydneysiders’ views about the right of foreign investors to use real estate as a vehicle for growing capital.

Sydneysiders with equity in the housing market, such as home owners or investors, might view foreign buyers pushing up housing values as positive. As a result, they might fear that restricting foreign investors might depress their assets.

If this type of shared commitment to real estate investment were present across the domestic-foreign investor divide, this could reinforce the idea of treating real estate as an asset class at the global scale, while cultural tensions between foreign and local investors remain at the local level.

Authors: Dallas Rogers, Program Director, Master of Urbanism. School of Architecture, Design and Planning, University of Sydney; Alexandra Wong, Engaged Research Fellow, Institute for Culture and Society, Western Sydney University; Jacqueline Nelson, Chancellor’s Postdoctoral Research Fellow, University of Technology Sydney

The preliminary auction results are in from Domain. Once again volumes are down, and clearance rates will settle lower than last year. Also, it looks like more property is being withdrawn.

Brisbane sold 15 of 38 reported auctions from 67 scheduled. Adelaide ran 31 auctions from the 69 listed, with 23 sold. Canberra ran 25 auctions from 31 listed with 14 sold.

The finance sector unmentionable hits the proverbial fan. Welcome to the Property Imperative Weekly to 21st April 2018.

We start this week’s review of the latest finance and property news with the latest from the Royal Commission into Financial Services Misconduct.

After the shameful disclosures relating to poor lending practices, bad advice, misaligned incentives and poor regulation last time; now they have been looking to the nether regions of financial planning and advice. And guess what, the same behaviours are evident again, in spades. Bearing in mind 48% of the $4.6 billion annual revenue from wealth management goes to the big four banks and AMP, they were forced to admit their mistakes in public. You can watch our separate video on the detailed findings “More Cultural Badness from The Finance Sector”. But here are a few highlights.

AMP apologised unreservedly for the misconduct and failures in regulatory disclosures in the advice business as revealed in the Royal Commission and Chief Executive Officer, Craig Meller will step down from his role with immediate effect.

The Australian Bankers Association admitted that the issues raised have been unacceptable and do not meet the high standards the community rightly expects of banks. And the Treasurer announced significant increases in penalties ASIC can impose. The government will increase penalties under the Corporations Act to: “For individuals: 10 years’ imprisonment; and/or the larger of $945,000 OR three times the benefits; For corporations: the larger of $9.45 million OR three times benefits OR 10% of annual turnover. “The Government will expand the range of contraventions subject to civil penalties, and also increase the maximum civil penalty amounts that can be imposed by courts, to the maximum of: the greater of $1.05 million (for individuals, from $200,000) and $10.5 million (for corporations, from $1 million); or three times the benefit gained or loss avoided; or 10% of the annual turnover (for corporations). “In addition, ASIC will be able to seek additional remedies to strip wrongdoers of profits illegally obtained, or losses avoided from contraventions resulting in civil penalty proceedings.”

These increases are right, as before the financial impact of poor behaviour was very low. However, do not be misled, changing penalties will not address the fundamental cultural, structural and economic issues which have combined to deliver a finance sector which is simply not fit for purpose.

We need to remove incentives from the advice sector (mortgage brokers included). Actually we need unified regulation across credit and wealth sectors (the current two regimes are an accident of history).

We need structural separate and disaggregation of our financial conglomerates. We need a realignment of interests to focus on the customer – which by the way is not at odds with shareholder returns, as customer focus builds franchise value and returns in the long term.

We need cultural reform and new values from our finance sector leaders. And Executive Pay should come under the spot light.

We need a reform of the regulatory structure in Australia, because they are captured at the moment at least by group think, and their interests are aligned too closely to the finance sector. This must include ASIC, APRA, RBA and ACCC. All have bits of the finance puzzle, but no one is seriously accountable.

But there is a more fundamental issue. We have relied on overblown credit, and superannuation sectors, as a proxy for high quality economic growth. This inflated housing and lifted household debt and GDP. We need a fundamental economic reset, because reforming financial services alone won’t solve our underlying issues.

The Government, who resisted the Royal Commission, has now also indicated they are receptive to expanding the scope and term of the inquiry, which in my view should include regulation of the sector, and the macroprudential settings in place. So write to the Commissioner, and your MP advocating a broader scope.

Finally, on this, it is worth noting that former deputy prime minister Barnaby Joyce went with a full-monty confession. “In the past I argued against a Royal Commission into banking. I was wrong. What I have heard … so far is beyond disturbing”, he tweeted. Joyce is now a backbencher, and free with his opinions. It’s another story with current ministers. They continue trying to score political points over Labor, which had been agitating for a royal commission long before it was set up.

My suggestion is this financial sector mess is so significant, that both sides of politics should set aside party differences and focus on the main game. Because what happens next will fundamentally determine the future economic success of the country, no less. If we continue with the current sets of assumptions we will run the country into the ground as the debt burden becomes unbearable, and savings for retirement are devalued and destroyed. It’s that serious.

Turning now to more immediate economic news, the latest lending stats from the ABS underscores that the “Great Credit Binge Is Ending”. You can watch our recent video where we discuss the results in full. To start at the end of the story, we see significant falls across most states in investment lending flows, with the most significant falls in the Sydney market. The share of investment flows continues to drift lower, to around 35%. But that is still substantial investment lending! Finally, the percentage of investment lending of all lending flows is below 20%, and shows a small fall. But we also see a fall in business lending to around 55%, excluding investment property lending.

The ABS also released their March 2018 unemployment statistics. It was not good with the trend unemployment rate increasing slightly to 5.6 per cent though the trend participation rate increased to a record high of 65.7 per cent. WA has the highest rate of unemployment at 6.4% and is still rising, whilst rates in NSW and ACT also rose.

The HIA released their latest Housing Affordability report, claiming that affordability improved in most of Australia’s capital cities during the first three months of 2018 as house price pressures eased. But this is largely spin, as their calculations do not necessarily take account of the now tighter, and becoming even tighter lending standards now in play. And in any case, in most centres, affordability is still well below the long term averages. But of course, they are advocates for the property sector, so there should be no surprise.

There was important evidence of the rising costs of funds this week as ME Bank says it has lifted its standard variable rate on existing owner-occupier principal and interest mortgages, effective April 2018. ME’s standard variable rate for existing owner-occupier principal-and-interest borrowers with an LVR of 80% or less, will increase by 6 basis points to 5.09% p.a. Variable rates for existing investor principal-and-interest borrowers will increase by 11 basis points, while rates for existing interest-only borrowers will increase by 16 basis points. ME CEO Mr Jamie McPhee said the changes are in response to increasing funding costs and increased compliance costs. More hikes will follow, across the industry together with reductions in rates paid on deposits as the fallout of the Royal Commission and higher international funding costs take their toll.

For example, the 10-year US Bond rate is moving higher again, following some slight fall earlier in April. Have no doubt, funding cost pressure will continue to rise. We discussed the whole question of debt and the potential trigger for a recession in a recent video blog, “Global Debt and the Upcoming Recession”. The outlook looks more and more like our Armageddon scenario, as we discussed in detail in an earlier programme “Four Scenarios (None Good)”. Worse, regulators in the USAand China are both weakening banking regulation, at this time of high risk, high debt.

Oh, and by the way, we think it quite possible the RBA will need to do its own form of quantitative easing down the track, and that they will most likely buy pools of residential mortgages (yes including those with breached lending standards) to assist the banks in their liquidity, to assist home prices to rise, and allowing the debt bomb to tick for longer. Sound of can being kicked firmly down the road! But that would be the time to buy Australian equities, and even property. Maybe we need a scenario 5!

We released the latest Digital Finance Analytics Household Finance Confidence Index for March 2018 shows a further slide in confidence compared with the previous month. The current score is 92.3, down from 94. 6 in February, and it has continued to drop since October 2016. The trend is firmly lower and below the neutral setting. You can watch our separate video on this “Why Household Finance Confidence Fell Again”. But in summary, across the states, confidence is continuing to fall in NSW and VIC, was little changes in SA and QLD, but rose in WA. There were there were falls in all age groups. Turning to the property-based segmentation, owner occupied householders remain the most confident, while property investors continue to become more concerned about the market. Those who are property inactive – renting, or living with parents or friends remain the least confident. Nevertheless, those who are property owners remain more confident relative to property inactive households. Based on the latest results, we see little on the horizon to suggest that household financial confidence will improve. We expect wages growth to remain contained, and home prices to slide, while costs of living pressures continue to grow. There will also be more pressure on mortgage interest rates as funding costs rise, and lower rates on deposits as banks trim these rates to protect their net margins.

Finally, we turn to CoreLogics’s auctions data. They suggest that fewer auctions will take place this week, with a total of 1,592 properties scheduled, compared with last week’s final result of1,915 auctions held. This is also lower than a year ago when 1,751 auctions were held across the capital city markets. Sydney is set to see the most significant drop in activity this week. Victoria’s Reservoir and Surfers Paradise in Queensland both top the busiest suburb list this week, each with 19 properties scheduled to go to auction. Following with 14 scheduled auctions each is Burwood and Point Cook both in Victoria.

Turning to last week’s final results the clearance rate was a 61.7 per cent success rate which was lower than the week prior when 62.8 per cent. Melbourne’s final auction clearance rate fell to 62.4 per cent last week across a slightly higher volume of auctions week-on-week with 873 held, up on the 723 over the week prior when a higher 68.2 per cent cleared. In Sydney, the final clearance rate fell to 61.5 per cent, down on the 62.9 per cent the previous week, with volumes across the city remaining steady over the week with a total of 795 held. Clearance rates improved across all of the remaining auction markets last week, with the exception Tasmania which remained unchanged. Geelong recorded the highest clearance rate of the non-capital city regions, with 77.1 per cent of 54 auctions clearing.

You might want to watch my video on “Auction Results Under The Microscope”, where we discuss how the results are collated and whether we can trust them.

So overall, there is little evidence to suggest the property market is recovering (despite more from the Industry claiming that this was the case, this week). And we have yet to see the impact of tighter lending standards flowing through. Our survey data indicates that more households are finding it tougher to meet the income and expenditure hurdles now, and as a result we expect credit and therefore home prices to continue to fall. And if anything, that fall will likely accelerate, unless we get unusual measures in the budget, which by the way we think are quite likely.

There were 1,890 homes taken to auction across the combined capital cities this week, with preliminary results showing a 64.5 per cent success rate. In comparison, 1,839 auctions were held last week and the final clearance rate came in at 62.8 per cent.

Over the same week last year, auction volumes were significantly lower due to the Easter weekend with just 493 homes going under the hammer across the combined capital cities, although the clearance rate was a stronger 73.9 per cent.

In Melbourne, a preliminary auction clearance rate of 64.3 per cent was recorded across 874 auctions this week, down from 68.2 per cent across 723 auctions last week. Over the same week last year, 102 homes were taken to auction across the city, returning a clearance rate of 81.3 per cent.

Sydney was host to 774 auctions this week, with preliminary results showing a 64.9 per cent success rate, up from 62.9 per cent across 795 auctions last week. This time last year, the clearance rate was a stronger 77.0 per cent across 279 auctions.

Canberra recorded the highest preliminary clearance rate this week (74.3 per cent), followed by Adelaide (70.6 per cent).

Looking at auction volumes, Melbourne was the only city to see an increase in the number of homes taken to auction this week, while all other cities saw lower volumes week-on-week.

One of the benefits of the DFA channel, as it develops, is the discussion and questions raised in the community. I have already been able to create content to meet specific requests and issues and will do more as we progress. For example, I am working on a series relating to crypto currencies, and another on property ownership (or not) across various household segments. Then there is more to say about The Chicago Plan, and how it might be practically be implemented.

But one of the most common threads is this. Ok, so I understand the risks in the property and finance sectors are increasing, but what should I do, how should I plan, and react. In fact, that often translates to two subsequent questions. First is, where should I put my savings in this high risk environment and second, I have been hearing about the risks in the systems for years, and so did not buy property then and consequently have missed out on significant capital gains. My friends thought I was nuts. So what’s different this time? Why should I stay away from property now?

So I want today to begin explore these questions further. And I need to say upfront, this is not financial advice. I am neither qualified to provide such advice and in any case, in this piece I could not take individual needs or financial situations into account. But, you might want to refer to my earlier programme – “Should I Buy Now”? which I published on 27th January this year.

But what I can do is to go beyond the often cartoonish statements being made at the moment. My favourite silly remark this past week was “the fall in property value offers the change for great buying, now”. I won’t embarrass the person who said this, other than to say they represent, no surprise, perhaps, the real estate industry. The RBA’s recent assertion that most households will cope with a rise in interest rates, and the switch from interest only to principle and interest loans would be another.

So let’s start with where should I put my savings in this high risk environment. As context, let’s look at what happened to UK bank Northern Rock.

Northern Rock, one of Britain’s Biggest Bank, began as a mutual in the North East, but then in 1997 it converted to a bank, offering members “free shares”. Later it became home to the 125% mortgage, and made the error of borrowing very short term, on the bond markets, whilst lending to customers for 25 years or more. Worse they then packaged those mortgages up and sold them on mainly to US banks. Whilst property prices were rising, and credit was free and easy all was well. Savers also put their money with the bank and got above average returns. The bankers looked like magicians and investors piled in. But then came the crash. House prices fell. The value of the mortgages fell too and the Bond markets then stopped lending to the Rock. So the cash flow stopped, but the bank needed billions of pounds just to keep the bank running. They were forced to seek assistance from the Government. No reason for depositors to panic, said the commentators at the time. Well that set the cat among the pigeons. Banks did not trust each other enough to lend to each other in the money markets and customers found their money in the bank was not as safe as people thought. And that was around 18 billion pounds.

The bank was nationalised in 2008, but this was just the start, and the UK Government was forced to spend $1 trillion pounds, yes, $1 trillion pounds on rescuing banks. In a subsequent review, the banking regulators were accused of applying light tough approaches to regulation. The assumption was that the financial system was full of such clever people, that self-regulation was sufficient – something with FED Chair Greenspan later came to recognise was a fallacy.

Five years later, on the other side of the crisis, when debt had been reduced, the full impact on the economy was clearer to see.

So, back to the present. We know that household debt is very high in Australia, the banks have made massive volumes of “liar loans” and global interest rates are rising. In addition, we are already seeing credit being tightened, and home prices are sliding. There is more to come, as discussed in our four scenarios video, which you might want to watch.

If you hold property, as an owner occupier, chances are the value of your property will fall, and the paper profits you think you have may be illusory. But the mortgage won’t be, and we know that many are struggling with big debts and poor cash flow. The good news, is that provided you can continue to make repayments, slipping into negative equity is not an immediate problem, but of course it may mean people are locked into the current properties. In Ireland and the UK, 10 years later, values have recovered, but it was a slow recovery. But if jobs dry up, default becomes more likely.

If you are an investor in property, and given many are not seeing any growth in rental receipts, you may find things more problematic – especially if you have several properties, on interest only loans. Repayments on these loans are likely to increase, as the RBA said the other day. In fact, some of the smartest money in the investment sector has already sold to realise their capital gains – but as values slide, this becomes a less attractive option. Research shows that investors are four time more likely to default on their mortgages, and so will be forced to sell in a downturn. Less experienced investors will likely be left holding the baby.

If you have savings in deposits, chances are the interest rates on those balances have already been cut, as banks try to protect their margins. Whilst mortgage interest rates are often discussed, the poor old saver continues to get a bad deal, yet this does not get much attention. I have always been surprised more is not made of this.

This takes us to the Bail-In question. I won’t go over the arguments again, you can watch my separate video on this.

But two points. First, there is a theoretical government backed deposit guarantee up to $250,000 (as we record this), but it needs to be activated by the Government, on an individual bank basis, so it is not in force today. Second, APRA says deposits will not be bailed-in, despite the fact the APRA now has the power to grab “other instruments” to assist in a bank restructure, and in New Zealand, deposits are definitely up for grabs. The situation in Australia, in my view is deliberately vague. Deposit bail-in could have been expressly excluded, but were not. The $250k guarantee is per financial entity, so you may be able to spread your risks by sharing deposits across multiple separate Australian based banks. Local subsidiaries of international banks are also included provided they are licenced locally. The $250,000 would cover all deposits, including term accounts, so it is not a limit by account, but by banking relationship. Also check if you are using an overseas bank, as they may not be guaranteed. It is worth asking now. Get it in writing.

Money held in superannuation funds will probably be placed with various market investments such as shares and bonds and some cash. But unless your funds are held in a separate self-managed superannuation account, the $250,000 deposit account guarantee would not apply. And it is worth checking with your bank if you have a self-managed deposit account to ensure it is.

Obviously market investments like shares and bonds will react to poor market conditions. We have seen market crashes of 25% or more in the past, and investments may well fall. There are no guarantees. Superfund balances can and will fall, but they will still take their management fees.

Some advocate placing money in Bitcoin or other cyber currencies, because they have decentralised block-chain records which mean Governments cannot get their hands on the funds placed there. While that may be true, values are very volatile, and I regard such Cyber investments as purely speculative and risky. Not really a core or secure option in my view.

What about gold or silver? Well, at least you hold something physical and in the past in crisis, these commodities have retained more value. But then you have the storage risk, and the liquidity risk. If you wanted to realise value later you need to find a buyer, and pricing is not certain. This is also true of ETF’s, and prices may fall.

So, should you hold cash, in notes? Surprisingly, it appears more funds are indeed being held in this form (for example in the UK, never has so much been held in notes – so the Bank of England is looking at removing the fifty-pound note. This is partly to reduce the size of the black economy, and partly to reduce the floats people hold. One point to bear in mind is that there is physical risk – notes burn for example, and you get no interest on notes held, but at least there is less chance of losing more value if the notes are safe.

And that’s the point, there are no easy answer to the question what should I do. It really does depend on your risk appetite, and whether you are most concerned about safeguarding the current value of what you have, or whether you are looking for future capital growth. Generally, I think it is true that risks are reduced by spreading savings and investments across multiple options, but then there is a trade off as complexity costs.

Now, turning to the question of what is different this time, with regards to property prices. In a word availability of credit. In the last decade or so, property prices have moved up and down, but the banks have been willing – very willing – to lend. This has driven prices higher and so many who bought a few years back are sitting on paper profits.

But the tightening of credit which we are seeing now will force prices lower, turn investors away, and as some are also forced to sell, this additional feedback loop will also force prices lower again. If you add in the lower number of foreign buyers, I cannot see a scenario where prices take off again anytime soon. My base case is a drop of 15-20% over the next couple of years. But I could be wrong.

A final point. Many households do not have a handle on their household budgets, so as I keep saying, it is worth drawing up a budget so you can see where the money is coming and going. You may be surprised. Then you can actively manage and prioritise your spending. This is the first critical step to getting to grips with your finances.

Also banks have a legal responsibility to assist in cases of hardship, so if you are in financial difficulty, it is worth talking to them.

So in conclusion, there are no easy answers to this conundrum. Which is why the level of uncertainly is currently so high, and I cannot see this settling down anytime soon.

The preliminary results from Domain are in. Looks like sales volumes held up. The same week last year was Easter, so ignore the comparisons. But final settlements are likely to end up close to last week, once all the data is in.

In the second part of our series on the anatomy of the property auction results, we dive deeper into the numbers.

We compared data from CoreLogic and Domain, two of the players who report auction clearance rates. We summarised the research in our latest video blog.

In each case, there is an interim step, where both Domain and CoreLogic adjust to a lower number of actual auctions on the day. Domain calls them “the number of reported auctions” and CoreLogic “CoreLogic Auctions”.

So, this takes us to two questions. First how are the figures collated and second, what adjustment are made between the listed auctions and final figures?

Domain says their data comes from Australian Property Monitors (APM). APM is of course part of the Domain Group which is a subsidiary of Fairfax Media Limited. APM publishes auction activity results for the Sydney, Melbourne, Brisbane and Adelaide capital cities every Saturday evening, providing a snapshot of how demand and supply in the auction market is behaving and as a leading indicator for the overall property market. (Auction activity for the other capital cities is also monitored and made available by mid week)

APM adopts the Australian Bureau of Statistics geographic definition for capital cities, referred to as the Statistical Division (SD).

APM publishes Auction Clearance Rates (ACR) on the Saturday evening, based on the majority sample collected on that day, for release across various publications on the Sunday, while the process of collecting results continues throughout the week.

When reporting auction activity, APM monitors the following five key elements that can occur to properties listed for auction. These are;

a) Sold prior to auction;

b) Sold at auction (under the hammer)

c) Passed in

d) Withdrawn from auction, or

e) Sold after auction

Including some or all of these five elements of auction activity in the calculation used will affect the reported clearance rate.

APM’s definition of the reported clearance rate calculation is defined as: Sold at auction plus sold prior, over all reported plus withdrawn.

On the “top-line” of the clearance rate calculation, APM considers only those properties sold either prior or during the auction to be “sold at auction”.

On the “bottom-line”, APM includes all reported auctions (including properties passed in), and any listed auctions withdrawn prior to the scheduled auction time.

APM includes withdrawn auctions in the calculation to prevent any bias in the clearance rate caused by properties being withdrawn due to expectations it may not sell or fail to achieve an expected price. It’s still counted as no sale.

I also examined in detail the weekly listings of property sold, each transaction is coded in line with the APM method. I also saw a small number of what appeared to be duplicate transactions across weeks, but not a significant number so I think we can lay to rest the idea that the results may be being inflated by duplicating the same results across multiple weeks.

Turning to CoreLogic, I spoke with Tim Lawless their research guru. This is what he told me:

Our auction data is collected directly from the industry, via a variety of channels including our call centre based in Adelaide, results which are pushed through from agents via our app or portal, or via direct data feeds from agency groups. Each week we publish three sets of clearance rates: Saturday night, Sunday morning (CoreLogic media release) and final results on Thursday morning. The collection of auction results progressively improves across each release as we receive more results from the industry. By the time we finalise our collection on Wednesday afternoon, on average, we collect 90% of auction results.

There has been some discussion that auction results which are not reported each week must also be unsuccessful auctions intentionally withheld by the agent. There may be an element of this – real estate agents aren’t obliged to provide us with their results, however each week it is generally the same agents who choose not to provide their auction results to us.

Regardless, we publish our results with full transparency, showing the number of auctions, together with the number of results collected segmented by successful auctions (sold before, at or prior to auction) and unsuccessful results (unsold, vendor bid, withdrawn). For those that believe the clearance rate should be adjusted lower based on unreported auctions, it’s pretty easy to do so… however the direction of the trend would be very similar, just a lower clearance rate.

For a long time there has been discussion around whether auction results are accurate or not. As a data aggregator and analytics provider, it’s in our best interest to publish results that are as accurate as possible; we have no interest in talking the market up or down.

Thanks Tim.

My take out of that is there may be some holding back of failed sales by some agents, but there is no way to triangulate the quantum of the problem, and there is no mandatory reporting of results. So the data must be seen as a best endeavours exercise. Tim also makes an excellent point that the trends really tell the tale.

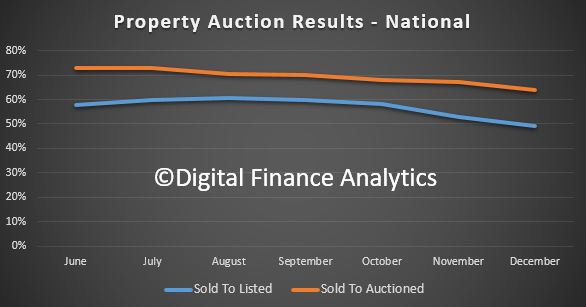

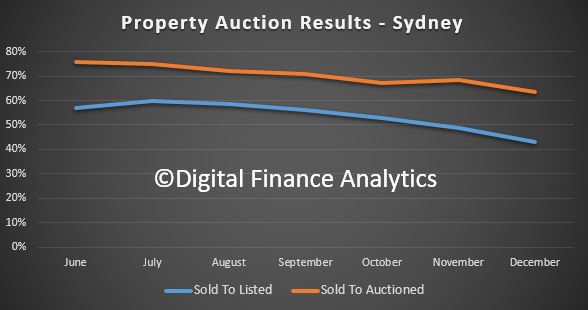

So, one final piece of the puzzle is some analysis we have done of the results, using both the percentage of all listings and sold property. I have charted the monthly trends for the second half of last year.

Here is the plot for Sydney. We see the clearance rates are declining, and the ratio of sold to listed is falling faster – suggesting that more properties are withdrawn (perhaps a sign of a fading market).

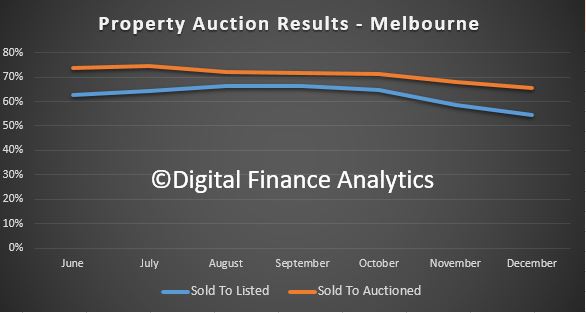

Compare this with Melbourne, where the momentum is also slowing, but the ratio of sold to listed is not so far below the sold to auctioned ratio – which suggests Melbourne is a little more buoyant (though is still slowing).

Finally, we can look at the national picture, which tells a similar story.

One final piece of the puzzle. If I then calculate the number sold properties compared with the transfer counts, which we discussed in a previous post, in the quarter to September 2017, the auctions comprised around 32% of all transfers made – allowing for an average 6-week delay in settling and completing the transaction. Looking back further, this ratio is pretty consistent. But in the December quarter, this shot up to 62% of transfers, which suggests that either there is now more false positives in the auction data, or the volume of non-auction sales has fallen. The former is, I think more likely than the latter, because in a falling market, I would expect a smaller number of auctions to run, compared with private sales. And we know that the listing volumes, and time in market, as well as discounts made to close a sale are all rising.

So, I think we need to be very careful when using the auction data. There is potential for agents to withhold negative results, but no one knows the extent of this. There is also some evidence of double counting, but only at the margin. Sydney looks the most suspicious.

In terms of the calculations, there are various tweaks made to the numbers and the two sources of data we looked at came out with different results. The trends are most telling, and the momentum was easing, up to the end of last year. We have not had enough normal weeks since January to trend the more recent weeks, and the ABS data will not be out for several weeks. We will revisit this later in the year

The most telling data is the mapping, or lack of it between the transaction data from the ABS and the auction results. This suggests to me there are more questions to ask. I have put some questions in to the ABS to dig further into their datasets, but I am still waiting for a reply. I will update you when I hear back. My suspicion is that ABS uses data feeds from CoreLogic, but the relevant page which outlines this, and the various terms report a missing page – 404 error – on the ABS site. Not good.

So here is the bottom line, be cautious with these numbers, and remember they have no statutory authority, may be contaminated with partial data, and of course the “marketing” use of the data may pull against the quest for accuracy, especially remembering Domain’s links to Fairfax and its property related businesses.

So, my conclusion is, we are without a really good chart and compass, here, just as we are with the RBA data series. More noise in the system!

The weighted average preliminary clearance rate rose across a higher volume of auctions this week with 1,813 homes taken to market returning a 65.3 per cent success rate. The higher activity this week comes of the back of the Easter period slowdown which saw only 670 auctions held across the capitals and a 64.8 per cent final auction clearance rate.

Overall results by property type, saw 70 per cent of units selling at auction this week, which was higher than the combined house result which returned a 63.4 per cent clearance rate.

Across Australia’s two largest cities, Melbourne recorded an increase in both auction volumes and clearance rate week-on-week, with 69.6 per cent of the 720 homes selling at auction this week, increasing on last week’s 65.5 per cent final clearance rate when a much lower 152 auctions were held. In Sydney, 775 auctions were held this week returning a 67.1 per cent preliminary clearance rate, down on the 67.9 per cent last week when 394 auctions were held across the city.

All of the remaining auction markets saw an increase in auction activity this week, however the performance was varied, with Adelaide recording the highest success rate of 59.7 per cent, while only 33.3 per cent of auctions cleared in Tasmania.

This Property Imperative Report is a distillation of our research in the finance and property market, using data from our household surveys and other public data. We provide weekly updates via our blog – the Property Imperative Weekly, but twice a year publish this report. This is volume 10.

This Property Imperative Report is a distillation of our research in the finance and property market, using data from our household surveys and other public data. We provide weekly updates via our blog – the Property Imperative Weekly, but twice a year publish this report. This is volume 10.

Finally, we can look at the national picture, which tells a similar story.

Finally, we can look at the national picture, which tells a similar story.