Home prices are horribly high in Australia. I think we can all agree on that point. But what is really driving this? “Classic” economic theory is that supply and demand of property drives prices, so factors such a number of builds, population and migration, and planning controls are all to blame. Indeed, a recent paper from the RBA peddled the line, as does the property and real estate sector. State and Federal Governments also talk this up.

But, there is another factor which is, according to our simulations, is much more directly impacting home prices and affordability. That is availability of credit. And this is contentious, because classic economists (including those residing in most central banks) tend to argue that credit growth is a zero sum gain, in that if there is a loan on one side of the ledger, there is a creditor on the other side of the fence, so the net impact is zero.

Worse still, classic theory suggests that banks are limited in what they can lend by the availability of deposits. Neither of these statements is true, and it fundamentally changes the banking and banking supervision game.

Back in 2014 I discussed this, based on an insight from the Bank of England. Their Quarterly Bulletin (2014 Q1), was revolutionary and has the potential to rewrite economics. “Money Creation in the Modern Economy” turns things on their head, because rather than the normal assumption that money starts with deposits to banks, who lend them on at a turn, they argue that money is created mainly by commercial banks making loans; the demand for deposits follows. Rather than banks receiving deposits when households save and then lending them out, bank lending creates deposits.

More recently the Bank of Norway confirmed this, and said “The bank does not transfer the money from someone else’s bank account or from a vault full of money. The money lent to you by the bank has been created by the bank itself – out of nothing: fiat – let it become.”.

And even the arch conservative German Bundesbank said in 2017 recently “this means that banks can create book money just by making an accounting entry: according to the Bundesbank’s economists, “this refutes a popular misconception that banks act simply as intermediaries at the time of lending – ie that banks can only grant credit using funds placed with them previously as deposits by other customers“.

Therefore the only limit on the amount of credit is peoples ability to service the loans – eventually.

With that in mind, we have built a scenario model, based on our core market model, which allows us to test the relationship between home prices, and a series of drivers, including population, migration, planning restrictions, the cash rate, income, tax incentives and credit. We are looking at national averages here, and we have smoothed the data from RBA and ABS to bring the trends out.

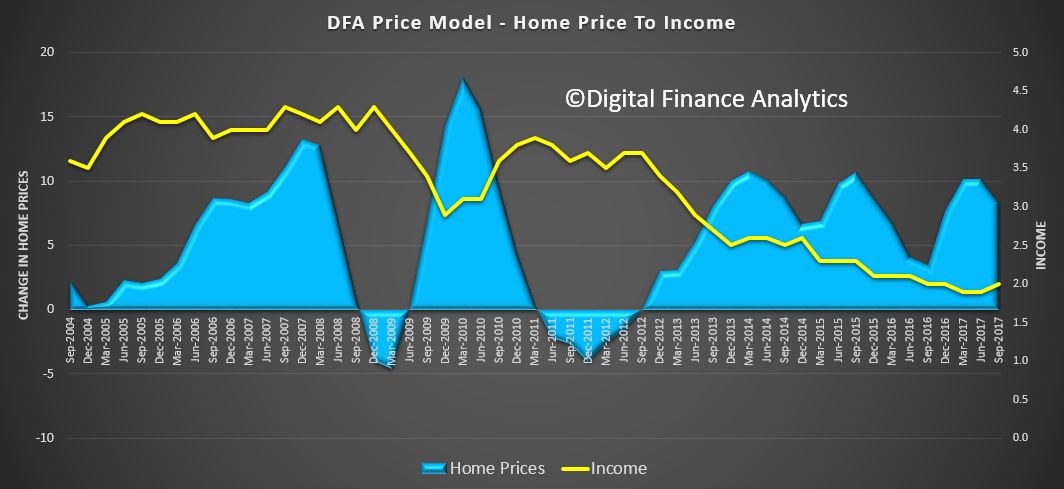

So first, lets walk through some of the relativity mapping. First we look at home prices relative to income growth. The blue area tracks changes in home prices since 2004, and the yellow line is the change in income. Most striking is that income growth and home prices are running in opposite directions, and have been especially since 2013. So income growth is not correlated to home price growth.

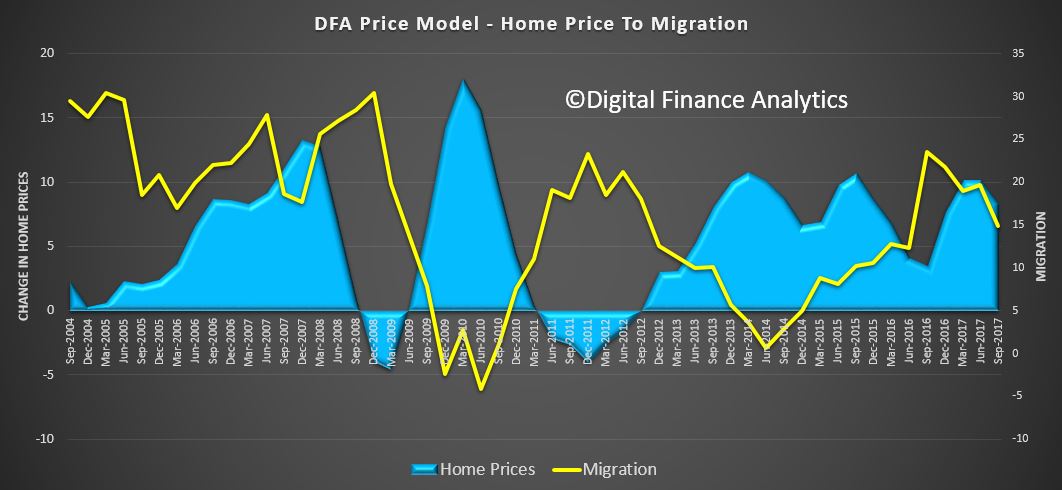

Next we look at home prices relative to migration and once again there is little alignment between home price growth and migration rates, this despite up to two thirds of population growth being fed from migration in recent years.

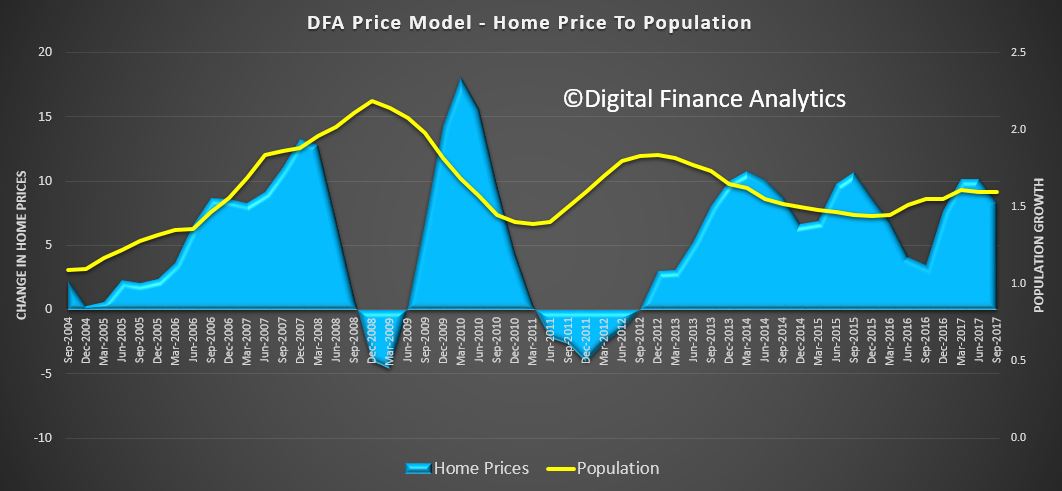

The relationship between overall population growth and home prices is equally disconnected. For example the rate of growth slowed from 2012 onward when we have had a large run up in home prices.

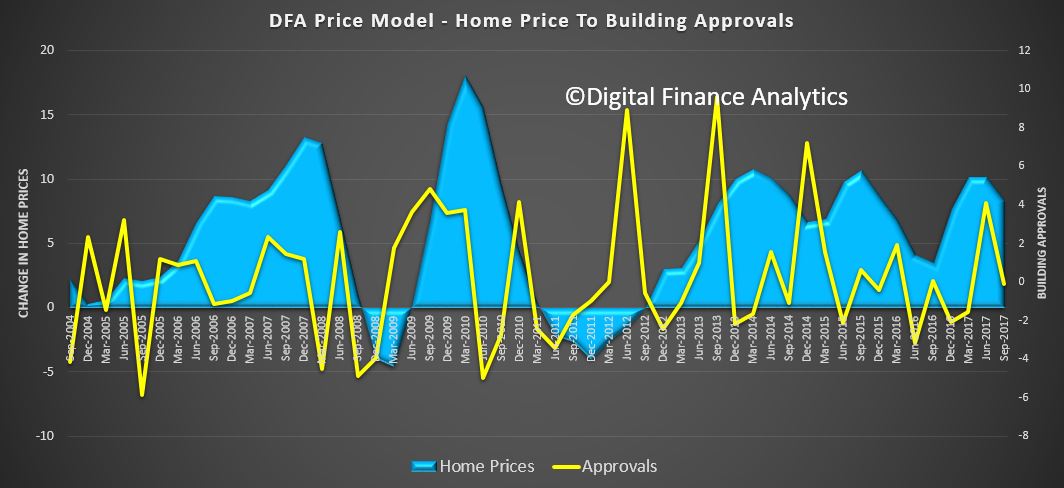

We then turned to building approvals, and even adjusting for the delay between approvals and commencements, there is little correlation.

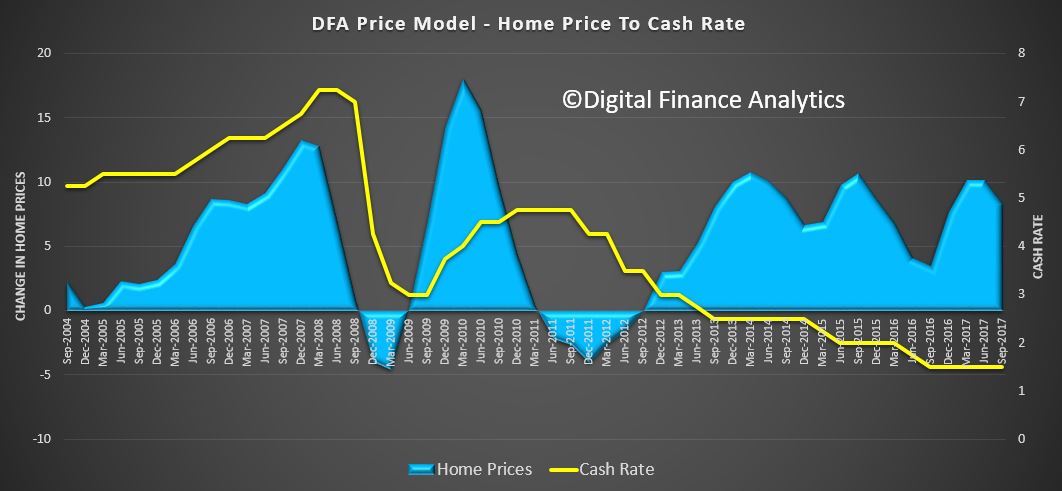

Up next is the RBA cash rate. Here we see an inverse linkage, in that as interest rates are cut, home prices expand. This also suggests that should rates rise, home prices will fall.

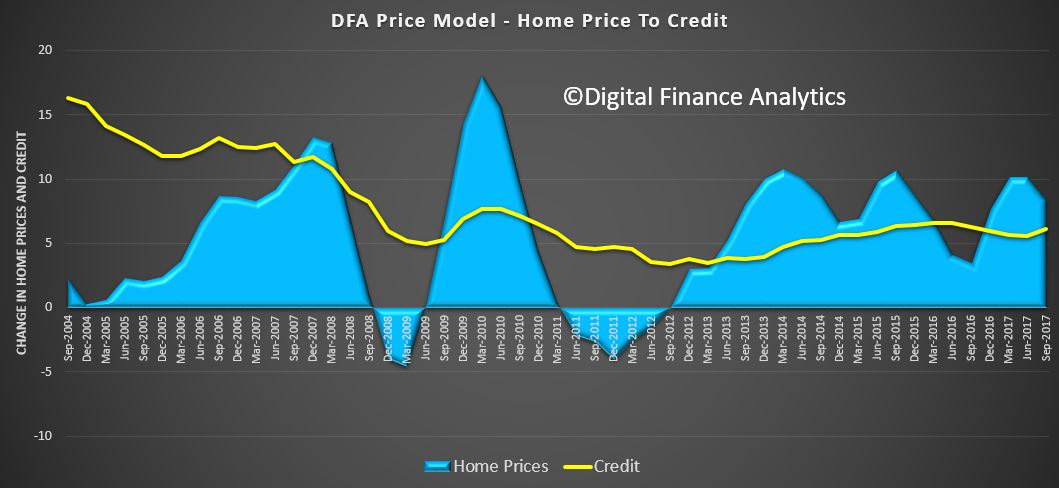

And here is the reason. The correlation between home prices and credit availability are clear to see. As credit rose from 2012 onward, home prices did too. It also suggests that if credit availability is tightened, we should expect prices to fall – take note, given the current tighter underwriting standards now in force. This is why I predict ongoing falls in property prices.

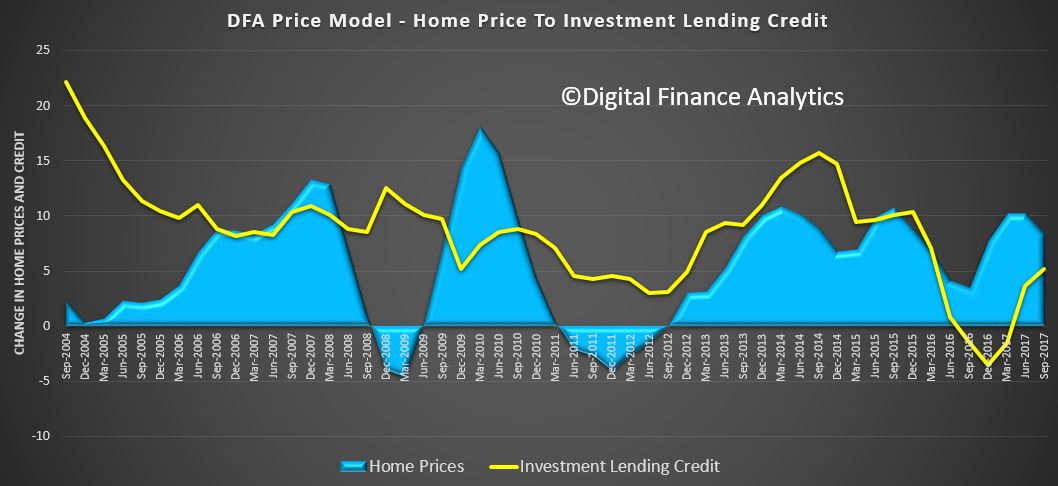

And more specifically, credit for property investment is even more strongly correlated. As we know investors are attracted by the capital growth, and also the capital gains and negative gearing tax breaks available.

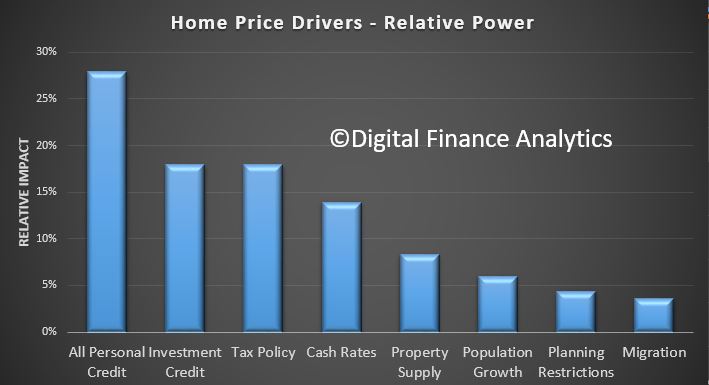

So then, we rolled all these factors into our overall model, and examined the relative influence of each on home prices. The four most powerful levers in terms of home prices is first overall growth in personal credit, including mortgages and other loans at 27% of total impact. Investment lending contributed a further 18%, followed by tax policy for investment property at 17% and the cash rate at 14%. The other factors, the ones which are spoken about the most, property supply, population growth, planning restrictions and migration, together make up just 22% of total impact. Or in other words, without addressing the credit elephant in the room, tax policy and interest rates, the chances of taming prices is low.

So now I can quote the recent Grattan report again, but with renewed vigour. “…much of the debate has focused on policies that are unlikely to make a real difference. Unless governments own up to the real problems, and start explaining the policy changes that will make a real difference, Australia’s housing affordability woes are likely to get worse”.

And the greatest of these is credit policy, which has for years allowed banks to magic money from thin air, to lend to borrowers, to drive up home prices, to inflate the banks balance sheet, to lend more to drive prices higher – repeat ad nauseam! Totally unproductive, and in fact it sucks the air out of the real economy and money directly out of punters wages, but make bankers and their shareholders richer.

One final point the GDP calculation we use in Australia is flattered by housing growth (triggered by credit growth). The second driver of GDP growth is population growth. But in real terms neither of these are really creating true economic growth.

To solve the property equation, and the economic future of the country, we have to address credit. But then again, I refer to the fact that most economists still think credit is unimportant in macroeconomic terms!

The alternative is to continue to let credit grow well above wages, and lift the already heavy debt burden even higher. Current settings are doing just that, as more households have come to believe the only way is to borrow ever more. But, that is, ultimately unsustainable, and why there will be an economic correction in Australia, and quite soon.

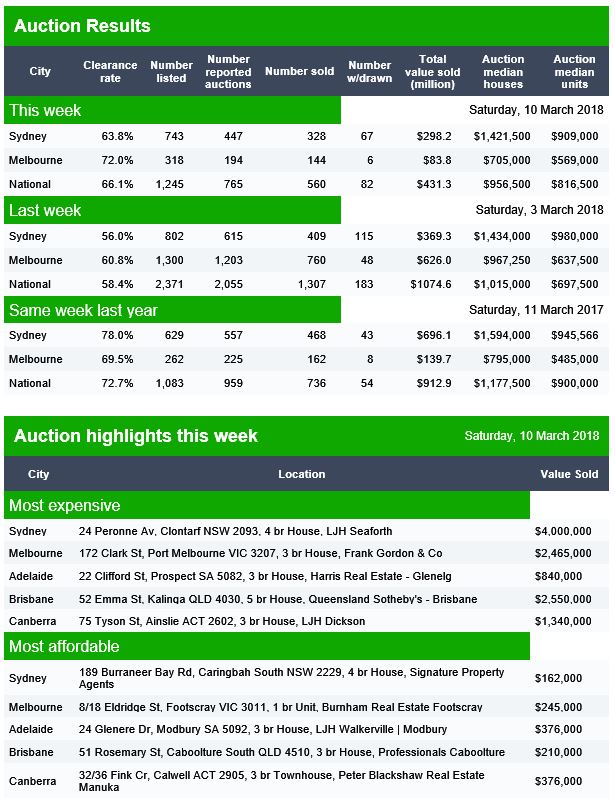

Domain published their preliminary results for today, and both volumes and clearance rates are down – partly thanks to the long week end in some states. But even allowing for this, the rates are lower than this time last year. The final results will of course settle lower as normal.

Brisbane cleared 57% of 91 listed, Adelaide 73% of 58 and Canberra 76% of 35 listed.

The AFR is reporting that Deposit Power, which which provided interim finance to property buyers, has closed its doors leaving an estimated 10,000 residential, commercial and property investors in the lurch about the fate of nearly $300 million worth of deposits.

This is after the collapse of New Zealand’s CBL’s insurance, which was an issuer and guarantor of deposit bonds.which provided interim finance to property buyers, has closed its doors after the collapse of New Zealand’s CBL’s insurance, which was an issuer and guarantor of deposit bonds.

Deposit Power had links with most of the major property broker networks, including Mortgage Choice and Connective, and major banks through their broker networks.

There are fears that the status of existing deals – which used the deposit bonds as a form of bridging finance for up to 48 months – could be jeopardised by the collapse of the insurance company.

Worried mortgage brokers, who recommended the products to clients, are seeking advice on whether clients need to buy other cover, or secure additional or replacement financial risk bonds.

It could mean unspecified risks, uncertainty and deal delays for tens of thousands of counter parties, financiers and their representatives, including lawyers and other brokers.

Reforming negative gearing could save the federal government A$1.7 billion without hurting “mum and dad investors”, according to our new modelling, by focusing tax deductions on investors with smaller property portfolios and removing them for richer investors.

Combined with changes to capital gains tax, reforming negative gearing could make the Australian housing market more sustainable and equitable.

Negative gearing allows investors to claim a tax deduction if their rental income is less than their expenses. It cost the federal government A$3.04 billion in 2013-14, according to our calculations.

Our report also confirms that negative gearing and the capital gains tax discount incentivise housing investors to take on debt. This potentially makes the housing market less stable and crowds out first home buyers.

According to Treasury modelling, the Labor Party’s plan to limit negative gearing deductions on newly acquired rental housing would put relatively modest downward pressure on house prices. Preliminary research from Melbourne University has found that eliminating negative gearing would result in an increase in home ownership.

But using data on the distribution of property and incomes makes it possible to differentiate between poorer and wealthier investors, allowing the government to target reforms to cushion the blow for investors on lower incomes.

Targeted negative gearing reform

In our example, investors in the bottom half of the income and property distributions could be allowed to claim tax deductions for all allowable rental expenses. Those in the 51st–75th income percentiles could deduct 50% of those expenses, while negative gearing would be eliminated for those in the top 25% of incomes.

Our modelling of this scenario shows this would save the federal government A$1.7 billion, or 57.3% of the current cost to the budget, each year. If negative gearing deductions were limited based on property values, the saving would be A$1.5 billion (or 48.3%).

Given this reform would be less likely to hurt poorer investors, they would be less likely to withdraw from the rental market than if negative gearing was eliminated. This would also mitigate the impact of negative gearing reform on renters.

Our modelling does not focus on the impact negative gearing reform might have on the housing market, house prices, rents, or how investors might respond, but our modelling does show the impact of changing who can claim negative gearing deductions, as well as capping it at different levels.

Home owners who also own at least one rental property receive the highest capital gains tax benefits. Our analysis showed this group has an average property portfolio valued at over A$730,000.

These home owners also have an average taxable income of A$82,000 per person, which is more than 250% of the average taxable income of renters (A$31,000).

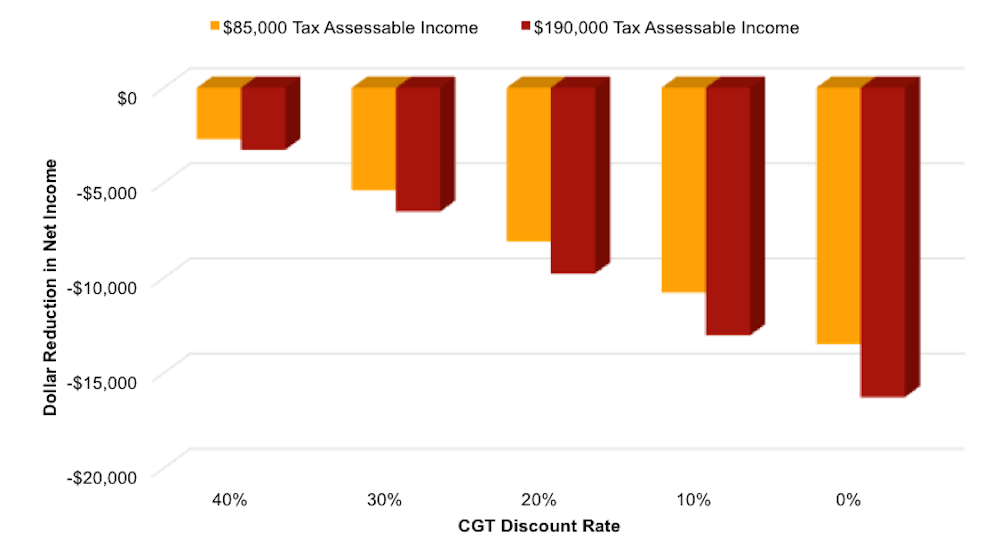

We modelled some alternative capital gains tax scenarios reducing the discount – which would increase the tax payable on net capital gains. Our calculations show that reducing the discount would lead to higher income earners paying more capital gains tax.

This would reduce the difference between the tax payable by higher and lower income rental investors, and therefore reduce inequities in the current system.

Author provided

Our modelling shows benefits of negative gearing are skewed towards more affluent investors in middle age and in full-time employment. Investors aged over 55 or who aren’t in the labour market (those who are unemployed, retired or not working) benefit the least from negative gearing.

We need to change the way we tax housing to create a more equitable and sustainable housing market. But this needs to be done (and communicated to investors) in a way that limits the risk of a shock to the market if investors exit the housing market.

Policymakers have been reluctant to change the fundamental settings of the tax system, but our modelling shows it can be done in a way that limits the impact on poorer investors.

The main limitation on this reform is behavioural, determining how investors will react to the effects of tax changes. Housing reform is complex, involving a range of market factors as well as the tax drivers.

Authors: Helen Hodgson, Associate Professor, Curtin Law School and Curtin Business School, Curtin University; Alan Duncan, Director, Bankwest Curtin Economics Centre and Bankwest Research Chair in Economic Policy, Curtin University; John Minas, Lecturer, Griffith University; Rachel Ong, Professor of Economics, School of Economics and Finance, Curtin University

Once taken for granted by the mainstream, home ownership is increasingly precarious. At the margins, which are wide, it is as if a whole new form of tenure has emerged.

Whatever the drivers, significant and lasting shifts are shaking the foundations of home ownership. The effects are far-reaching and could undermine both the financial and wider well-being of all Australian households.

Over the course of 100 years, Australians became accustomed to smooth housing pathways from leaving the parental home to owning their house outright. However, not only did the 2008-09 global financial crisis (GFC) underline the risk of dropping out along the way, but more recent Australian evidence has shown that the old pathways have been displaced by more uncertain routes that waver between owning and renting.

The Household, Income and Labour Dynamics in Australia (HILDA) Survey indicates that, during the first decade of the new millennium, 1.9 million spells of home ownership ended with a move into renting (one-fifth of all home ownership spells that were ongoing in that period). It also shows that among those who dropped out, nearly two-thirds had returned to owning by 2010. Astonishingly, some 7% “churned” in and out of ownership more than once. Many households no longer either own or rent; they hover between sectors in a “third” way.

The drivers of this transformation include an ongoing imperative to own, vying with the factors that oppose this – rising divorce rates, soaring house prices, growing mortgage debt, insecure employment and other circumstances that make it difficult to meet home ownership’s outlays.

Those who use the family home as an “ATM” are at added risk. This relatively new way of juggling mortgage payments, savings and pressing spending needs makes some styles of owner occupation more marginal – as the tendency is to borrow up, rather than pay down, mortgage debts over the life course.

A retirement incomes system under threat

Since its inception, the means-tested age pension system has been set at a low fixed amount. Retired Australians could nevertheless get by provided they achieved outright home ownership soon enough. The low housing costs associated with outright ownership in older age were effectively a central plank of Australian social policy.

Moreover, developments in the Australian housing system could undermine a second retirement incomes pillar – the superannuation guarantee. An important goal of the superannuation guarantee is financial independence in old age. But if superannuation pay-outs are used to repay mortgage debts on retirement, reliance on age pensions will grow rather than recede.

Such policy interest is not surprising. Housing wealth dominates the asset portfolios of the majority of Australian households, boosted by soaring house prices. If home owners can be encouraged or even compelled to draw on their housing assets to fund spending needs in retirement, this will ease fiscal pressures in an era of population ageing.

However, the welfare role of home ownership is already important in the earlier stages of life cycles. Financial products are increasingly being used to release housing equity in pre-retirement years. This adds to the debt overhang as retirement age approaches. It also increases exposure to credit and investment risks that could undermine stability in housing markets.

A gender equity issue

A commonly overlooked angle relates to gender equity. Australian women own less wealth than men, and they also hold more housing-centric asset portfolios.

Hence, women are more exposed to housing market instability associated with precarious home ownership. Single women are especially vulnerable to investment risk when they seek to realise their assets.

A neglected economic lever

Housing and mortgage markets played a central role in the GFC. Today, it is widely agreed that resilient housing and mortgage markets are important for overall economic and financial stability. There are also concerns that the post-GFC debt overhang is a drag on economic growth.

However, the policy stance in the wake of the GFC has been “business as usual”. There has been very little real innovation in the world of housing finance or mortgage contract design in recent years. This might change if housing were steered from the periphery to a more central place in national economic debates.

Forward-looking policy response is needed

Growing numbers of Australians clearly face an uncertain future in a changing housing system. The traditional tenure divide has been displaced by unprecedented fluidity as people juggle with costs, benefits, assets and debts “in between” renting and owning.

This expanding arena is strangely neglected by policy instruments and financial products. Politicians cling to an outdated vision of linear housing careers that does little to meet the needs of “at risk” home owners, locked-out renters, or churners caught between the two.

The hazards of a destabilising home ownership sector are wide-ranging, rippling well beyond the realm of housing. Part of the answer is a new drive for sustainability, based on a housing system for Australia that is more inclusive and less tenure-bound.

Author: Rachel Ong, Professor of Economics, School of Economics and Finance, Curtin University; Gavin Wood, Emeritus Professor of Housing and Housing Studies, RMIT University; Susan Smith,

Honorary Professor of Geography, University of Cambridge

More confirmation of lower auction clearance rates, this time from CoreLogic. But also, note that quite a few properties listed for sale never came to auction! So you could say the real results are even worse.

CoreLogic says there were 2,980 homes taken to auction across the combined capital cities this week, returning a preliminary auction clearance rate of 65.9 per cent, while last week, 3,313 auctions were held and the final clearance rate came in at 66.8 per cent.

Over the same week last year, auction volumes were slightly lower with 2,907 homes going under the hammer across the combined capital cities, although the clearance rate was a stronger 74.6 per cent.

If we look at results by property type, units outperformed the house market this week with 67.6 per cent of units selling at auction, while 65.1 per cent of houses sold across the combined capital cities.

In Melbourne, Australia’s largest auction market, a preliminary auction clearance rate of 67.3 per cent was recorded across 1,523 auctions this week, down from 70.6 per cent across 1,606 auctions last week. One year ago, the clearance rate was a stronger 78.4 per cent across 1,459 auctions. There were 1,044 auctions held in Sydney this week returning a preliminary auction clearance rate of 66.9 per cent, compared to 65.1 per cent across 1,259 last week, and 76.0 per cent across 950 auctions one year ago.

Across the smaller auction markets, preliminary results show that Canberra was the best performing in terms of clearance rate with a 70.8 per cent success rate.

Overall volumes and clearance rates remain below those from a year ago. Volume remains higher in Melbourne. The final results will settle lower as normal.

Brisbane cleared 56% of 107 scheduled auctions, Adelaide, 63% of 84 scheduled and Canberra 66% of 77 scheduled auctions.

How far will home prices fall? Welcome to the Property Imperative weekly to 3rd March 2018.

Yet another big big week in property and finance for us to review today. Watch the video or read the transcript.

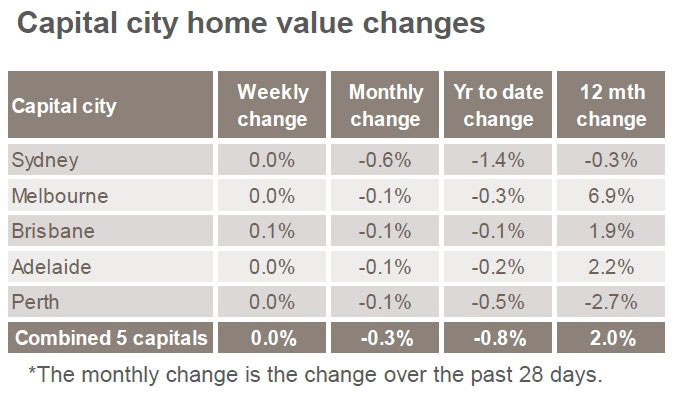

We start with the latest home price data from CoreLogic. Prices continue to soften. On an annual basis, prices are down 0.5% in Sydney, 2.7% in Perth and 7.4% in Darwin. They were higher over the year in Melbourne, up 6.9%, Brisbane 1.8%, Adelaide 2.2% and Hobart a massive 13.1%. But be beware, these are average figures, and there are considerable variations across locations within regions and across property types. The bigger falls are being seen at the top end of the market.

Over the three months to February, Adelaide was up 0.1% and Hobart 3.2%. These were the only capital cities in which values rose. Sydney, which has been the strongest market for value growth over recent years, saw the largest fall in values over the three-month period, down -2.4%. Sydney was followed by Darwin, which has been persistently weak over recent years, and saw values fall by a further -2.0% over the quarter.

Finally, CoreLogic says month-on-month falls were generally mild but broad based. Over the month, values fell across every capital city except Hobart (+0.7%) and Adelaide (steady), with the largest monthly decline recorded across Darwin (-0.9%) and Sydney (-0.6%). Values were lower in Melbourne (-0.1%), Brisbane (-0.1%), Perth (-0.2%), and Canberra (-0.3%).

The reason for the falls are pretty plain to see. Demand is substantially off, especially from investors, as mortgage underwriting standards are tightening. So it was interesting to hear APRA chairman Wayne Byres’s testimony in front of the Senate Economics Legislation Committee. I discussed this with Ross Greenwood on 2GB. During the session he said that the 10% cap on banks’ lending to housing investors imposed in December 2014 was “probably reaching the end of its useful life” as lending standards have improved. Essentially it had become redundant. But the other policy, a limit of more than 30% of lending interest only will stay in place. This more recent additional intervention, dating from March 2017, will stay for now, despite it being a temporary measure. The 30% cap is based on the flow of new lending in a particular quarter, relative to the total flow of new lending in that quarter. This all points to tighter mortgage lending standards ahead, but still does not address the risks in the back book. The mortgage underwriting screws are much tighter now – our surveys show that about a quarter or people seeking a mortgage now cannot get one due to the newly imposed limits on income, expenses and serviceability.

During the sessions, Senator Lee Rhiannon asked APRA about mortgage fraud. This was to my mind the most significant part.

Yet even now, more than 10% of new loans are being funded at a loan to income of more than 6 times. And whilst the volume of interest only loans has fallen to 20% of new loans, well below the 30% limit, it seems small ADI’s are lending faster than the majors. And we know the non-banks are going gang busters.

Now the HIA said their Housing Affordability Index saw a small improvement of 0.2 per cent during the December 2017 quarter indicating that affordability challenges have eased thanks to softer home prices in Sydney where they are now slightly lower than they were a year ago. This makes home purchase a little more accessible, particularly for First Home Buyers they said. But they failed to mention the now tighter lending standards which more than negates any small improvement in their index.

The impact of this tightening came through in the latest data on housing finance from both the RBA and APRA. I made a separate video on this if you want the gory details. The RBA said that in January owner occupied lending rose 0.6%, or 8% over the past year to $1.14 trillion. Investment lending rose 0.2% or 3% over the past year to $587 billion and comprises 34% of all housing lending. They changed the way they report the data this month. It changes the trend reporting significantly. Since mid-2015 the bank has been writing back perceived loan reclassifications which pushed the investor loans higher and the owner occupied loans lower. They have now reversed this policy, so the flow of investment loans is lower (and more in line with the data from APRA on bank portfolios). Investor loans are suddenly 2% lower. Magically! Once again, this highlights the rubbery nature of the data on lending in Australia. What with data problems in the banks, and at the RBA, we really do not have a good chart and compass. It just happens to be the biggest threat to financial stability but never mind.

The latest APRA Monthly Banking Statistics to January 2018 tells an interesting tale. Total loans from ADI’s rose by $6.1 billion in the month, up 0.4%. Within that loans for owner occupation rose 0.57%, up $5.96 billion to $1.05 trillion, while loans for investment purposes rose 0.04% or $210 million. 34.4% of loans in the portfolio are for investment purposes. So the rotation away from investment loans continues, and overall lending momentum is slowing a little (but still represents an annual growth rate of nearly 5%, still well above inflation or income at 1.9%!). Looking at the lender portfolio, we see some significant divergence in strategy. Westpac is still driving investment loans the hardest, while CBA and ANZ portfolios have falling in total value, with lower new acquisitions and switching. Bank of Queensland and Macquarie are also lifting investment lending.

Now searching questions are being asked about Lax Mortgage Lending, and the risks the banks are sitting on at the moment. While better lending controls will help ahead, we have a significant problem now, with many households facing financial difficulty. First there is the issue of basic cash flow, as incomes remain contained, costs of living rise, and mortgage payments still need to be met. We estimate 51,500 households risk default in the year ahead, a small but growing problem. We will release the February mortgage stress data on Monday, so look out for that.

Then there is the question of banks and brokers not doing sufficient due diligence on loan applications. This is something the Royal Commission will be looking at in the next couple of weeks. We worked with the ABC on a story, which aired this week, looking at the issues around poor lending. Its complex of course, because borrowers have to take some responsibility for the applications they made for credit, and need to be truthful. But both brokers and lenders have obligations to make sufficient inquiry into the applicant’s circumstances to ensure the loan is “not unsuitable” – which is nothing to do with the “best” mortgage by the way, it’s a much lower hurdle. But if a loan were deemed to be unsuitable, the courts may change the terms of the loan, or cancel the loan, meaning a borrower could leave a property without debt. An upcoming court case may clarify the law. But in the ABC piece, Brian Johnston, one of the best analysts in the business said this means it moves from being the borrowers problem to being the banks problem!

This also touches on the role of mortgage brokers, and whether their commission based remuneration might influence their loan recommendations, to the detriment of their customers, which is more than half the market. This is something which both ASIC and the Productivity Commission have been highlighting. Speaking at a CEDA event, Productivity Commission chairman Peter Harris said more than $2.4bn is now paid annually for mortgage broker services. The commission’s draft report released in early February says that based on ASIC’s findings, lenders pay brokers an upfront commission of $2,289 (0.62%) and a trail commission of $665 (0.18%) a year on an average new home loan of $369,000. He zeroed in on trailing commissions – which he said are worth $1bn per annum – and questioned their relevance.

The Banking Royal Commission says the first round of public hearings will be held in Melbourne at the Owen Dixon Commonwealth Law Courts Building at 305 William Street from Tuesday 13 March to Friday 23 March. They listed the range of matters they are exploring, from mortgages, brokers, cards, car finance, add-on insurance and account administration, with reference to specific banks, including NAB, CBA, ANZ, Westpac, Aussie, and Citi. Responsible lending is the theme.

Talking of mortgage brokers, another question to consider is the ownership relationship between a broker, their aggregator and the Bank. Not only are many brokers effectively directly employed by the big banks, but more have strong associations, these relationships are not adequately disclosed.

The New Daily did a good piece on showing these linkages, most of which are hard to spot. They said that Fans of Married at First Sight and My Kitchen Rules may have noticed over the past few days that popular property website realestate.com.au has started advertising a new product: home loans. But Realestate.com.au Home Loans is not an independent initiative. Far from it. It is a deal between Rupert Murdoch’s News Corp, which owns 61.6 per cent of realestate.com.au, and big-four bank NAB. Last June REA Group, the company behind the realestate.com.au website, signed what it called a “strategic mortgage broking partnership” with NAB. What REA Group is actually doing is piggy-backing on a mortgage broker called Choice Home Loans. In other words, while the branding may be realestate.com.au, the actual mortgage broking firm is Choice Home Loans. And who owns Choice Home Loans? NAB does. If you get conditional approval through realestate.com.au, it will be provided by NAB. However, getting conditional approval with NAB does not commit you to a NAB home loan. First, you could choose a realestate.com.au ‘white label’ loan. This is a loan that on the face of it looks like it is provided by realestate.com.au. But once again appearances are deceptive. REA Group does not have a mortgage lenders’ licence. So while these loans may be branded realestate.com.au, they are actually provided by a nationwide mortgage lender called Advantedge. And who owns Advantedge? NAB does. If you don’t fancy the realestate.com.au home loan, there are other choices. First, there is a range of NAB mortgages. And then, there is a list of mortgages from other providers – more than 30 of them, including big names like Westpac, ANZ, Commonwealth Bank, Macquarie, ING, ME, UBank – the list goes on. Oh, and by the way, that last bank mentioned – UBank – is also owned by NAB. All this highlights the hidden connections and the market power of the big banks. Like I said, these relationships are hard to spot!

Another little reported issue this week was the financial viability of Lenders Mortgage Insurers in Australia, those specialist insurers who cover mortgages over 80% loan to value. QBE Insurance reported their full year 2017 results today and reported a statutory 2017 net loss after tax of $1,249 million, which compares with a net profit after tax of $844 million in the prior year. This is a diverse and complex group, which is now seeking a path to rationalisation. They declared their Asia Pacific result “unacceptable” and said the strategy was to “narrow the focus and simplify back to core” with a focus on the reduction in poor performing segments. This begs the question. What is the status of their Lenders Mortgage Insurance (LMI) business? They reported a higher combined operating ratio consistent with a cyclical slowdown in the Australian mortgage insurance industry, higher claims and a lower cure rate. Very little detail was included in the results, but this aligns with similar experience at Genworth the listed monoline who reported a 26% drop in profit, and provides greater insight into the mortgage sector. Both LMI’s are experiencing similar stresses, with lower premium income, and higher claims. And this before the property market really slows, or interest rates rise! Begs the question, how secure are the external LMI’s? Another risk to consider.

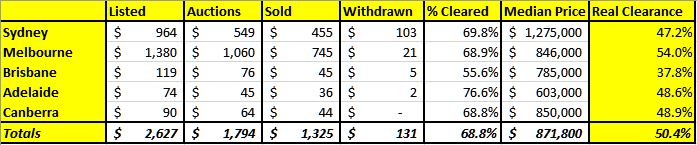

Last week’s auction preliminary results from Domain said nationally, so far from the 2,627 properties listed for auction, only 1,794 actually went for sale, and 1,325 properties sold. So the real clearance rate against those listed is 50.4%. Domain though calculates the clearance rate on those going to auction, less withdrawn sales over those sold. This give a higher measure of 68.8% nationally, which is still lower than a year ago. But, we ask, which is the real clearance rate?

Finally, there is a rising chorus demanding that APRA loosen their rules for mortgage lending in the face of slipping home prices. This despite the RBA’s recent comments about the risks in the system, especially relating to investor and interest only loans. But this is unlikely, and in fact more tightening, either by a rate rise, or macroprudential will be needed to contain the risks in the system. The latter is more likely. Some of this will come from the lenders directly. For example, last week ANZ said it will be regarding all interest-only loan renewals as credit critical event requiring full income verification from 5 March. If loans failed this assessment these loans would revert to P&I loans (with of course higher repayment terms). We are already seeing a number of forced switches, or forced sales thanks to the tighter IO rules more generally. We will release updated numbers next week. But, as ANZ has pointed out in a separate note from David Plank, Head of Australian Economics at ANZ; household leverage is still increasing, this despite a moderation in housing credit growth over the past year. Household debt continues to grow faster than disposable income. With household debt being close to double disposable income it will actually require the growth in household debt to slow well below that of income in order for the ratio of household debt to income to stabilise, let alone fall. In fact, he questions whether financial stability has really been improved so far, when interest rates are so very low.

So, nothing we have seen this week changes our view of more, and significant falls in property values ahead as mortgage lending is tightened further. This also shows that it is really credit supply and demand, not property supply and demand which is the critical controller of home price movements. Another reason to revisit the question of negative property gearing in my view.

According to CoreLogic, auction volumes surge past 3,000 for the first time this year returning a strong preliminary auction clearance rate of 70.5 per cent. Still well down on a year ago, despite higher volumes.

Auction volumes returned to higher levels this week across the combined capital cities with a total of 3,275 homes taken to auction; the higher volumes returned a strong preliminary auction clearance rate of 70.5 per cent. Last week 1,992 auctions were held across the capitals with 66.1 per cent clearing, while over the same week one year ago a 78.4 per cent clearance rate was recorded across a higher volume of auctions (3,301).

Results segregated into property type showed that units outperformed the house market this week, with 72.9 per cent of units selling at auction, while 69.5 per cent of houses sold across the combined capitals.

Melbourne returned a preliminary auction clearance rate of 71.7 per cent this week, which was higher than final figures from last week which saw 69.8 per cent of auctions clearing. Melbourne’s higher preliminary clearance rate was across a significantly higher volume of auctions week-on-week, with 1,610 held, up from last week’s 932 auctions. In Sydney, 1,221 homes were taken to auction this week, returning an equal highest preliminary result to Melbourne’s 71.7 per cent, increasing on last week’s final clearance rate of 67.8 per cent across a lower volume of auctions (737).

Across the smaller auctions markets, Adelaide was the best performing in terms of clearance rate with 75.9 per cent of the 107 auctions reporting as sold. While Perth returned the lowest preliminary auction clearance rate of 52.6 per cent.

Separately, they also showed no change in prices this past week.

The latest preliminary results are out from Domain. Nationally, so far from the 2,627 properties listed for auction, only 1,794 actually went for sale, and 1,325 properties sold.

So the real clearance rate against those listed is 50.4%. Domain though calculates the clearance rate on those going to auction, less withdrawn sales over those sold. This give a higher measure of 68.8% nationally, which is lower than a year ago. Across the country the median price was $871,800.

Here are the results by main locations, including our calculation of the true clearance rate. More were withdrawn in Sydney than the other states.

Next we look at home prices relative to migration and once again there is little alignment between home price growth and migration rates, this despite up to two thirds of population growth being fed from migration in recent years.

Next we look at home prices relative to migration and once again there is little alignment between home price growth and migration rates, this despite up to two thirds of population growth being fed from migration in recent years. The relationship between overall population growth and home prices is equally disconnected. For example the rate of growth slowed from 2012 onward when we have had a large run up in home prices.

The relationship between overall population growth and home prices is equally disconnected. For example the rate of growth slowed from 2012 onward when we have had a large run up in home prices. We then turned to building approvals, and even adjusting for the delay between approvals and commencements, there is little correlation.

We then turned to building approvals, and even adjusting for the delay between approvals and commencements, there is little correlation. Up next is the RBA cash rate. Here we see an inverse linkage, in that as interest rates are cut, home prices expand. This also suggests that should rates rise, home prices will fall.

Up next is the RBA cash rate. Here we see an inverse linkage, in that as interest rates are cut, home prices expand. This also suggests that should rates rise, home prices will fall. And here is the reason. The correlation between home prices and credit availability are clear to see. As credit rose from 2012 onward, home prices did too. It also suggests that if credit availability is tightened, we should expect prices to fall – take note, given the current tighter underwriting standards now in force. This is why I predict ongoing falls in property prices.

And here is the reason. The correlation between home prices and credit availability are clear to see. As credit rose from 2012 onward, home prices did too. It also suggests that if credit availability is tightened, we should expect prices to fall – take note, given the current tighter underwriting standards now in force. This is why I predict ongoing falls in property prices. And more specifically, credit for property investment is even more strongly correlated. As we know investors are attracted by the capital growth, and also the capital gains and negative gearing tax breaks available.

And more specifically, credit for property investment is even more strongly correlated. As we know investors are attracted by the capital growth, and also the capital gains and negative gearing tax breaks available. So then, we rolled all these factors into our overall model, and examined the relative influence of each on home prices. The four most powerful levers in terms of home prices is first overall growth in personal credit, including mortgages and other loans at 27% of total impact. Investment lending contributed a further 18%, followed by tax policy for investment property at 17% and the cash rate at 14%. The other factors, the ones which are spoken about the most, property supply, population growth, planning restrictions and migration, together make up just 22% of total impact. Or in other words, without addressing the credit elephant in the room, tax policy and interest rates, the chances of taming prices is low.

So then, we rolled all these factors into our overall model, and examined the relative influence of each on home prices. The four most powerful levers in terms of home prices is first overall growth in personal credit, including mortgages and other loans at 27% of total impact. Investment lending contributed a further 18%, followed by tax policy for investment property at 17% and the cash rate at 14%. The other factors, the ones which are spoken about the most, property supply, population growth, planning restrictions and migration, together make up just 22% of total impact. Or in other words, without addressing the credit elephant in the room, tax policy and interest rates, the chances of taming prices is low. So now I can quote the recent Grattan report again, but with renewed vigour. “…much of the debate has focused on policies that are unlikely to make a real difference. Unless governments own up to the real problems, and start explaining the policy changes that will make a real difference, Australia’s housing affordability woes are likely to get worse”.

So now I can quote the recent Grattan report again, but with renewed vigour. “…much of the debate has focused on policies that are unlikely to make a real difference. Unless governments own up to the real problems, and start explaining the policy changes that will make a real difference, Australia’s housing affordability woes are likely to get worse”.