We are now in the end game of a massive experiment, which is clearly failing. That experiment, cooked up by central banks, and with support from Government meant that interest rates and mortgage rates dropped, lending criteria loosened, and home prices shot up dramatically. The final phase of the up was through COVID when quantitative easing again drove debt higher, whilst luring households into a false sense of security – remember not rate rises til 2024?

But now, it’s all coming unglued as rates are rising, and the debt burden is becoming overbearing. Take Canada for example – based on a recent EBC report. They say that sky-rocketing home prices earlier in the pandemic raised the bar by several notches for Canadian buyers. But the spike in interest rates since March served a crushing blow in parts of the country.

http://www.martinnorth.com/

Go to the Walk The World Universe at https://walktheworld.com.au/

Today’s post is brought to you by Ribbon Property Consultants.

People are leaving NSW for other states, driven by the failure of housing and planning policy and ultra-lose lending. The consequences are significant in terms of younger households exiting, while the burden of providing adequate support for older Australians is rising fast.

This mess will create massive problems in the years ahead.

http://www.martinnorth.com/

Go to the Walk The World Universe at https://walktheworld.com.au/

Today’s post is brought to you by Ribbon Property Consultants.

If you are buying your home in Sydney’s contentious market, you do not need to stand alone. This is the time you need to have Edwin from Ribbon Property Consultants standing along side you.

Buying property, is both challenging and adversarial. The vendor has a professional on their side.

Emotions run high – price discovery and price transparency are hard to find – then there is the wasted time and financial investment you make.

Edwin understands your needs. So why not engage a licensed professional to stand alongside you. With RPC you know you have: experience, knowledge, and master negotiators, looking after your best interest.

Shoot Ribbon an email on info@ribbonproperty.com.au & use promo code: DFA-WTW/MARTIN to receive your 10% DISCOUNT OFFER.

A replay of an investment podcast as Nucleus Wealth’s Chief Investment Officer Damien Klassen and Senior Financial Adviser Samuel Kerr, with guest Martin North of @WalkTheWorldDFA, as they discuss property rate cut that nobody noticed.

Agenda:

● The percentage of GDP that this year’s rake hikes have consumed ● Discount rates on standard variable rates ● Fake standard variable rates?

Find us on social media: https://twitter.com/NucleusWealth https://www.instagram.com/nucleus_wea… https://www.facebook.com/NucleusWealth https://www.linkedin.com/company/nucl…

Nucleus Wealth is an Australian Investment & Superannuation fund that can help you reach your financial goals through transparent, low-cost, ethically tailored portfolios. To find out more head to https://nucleuswealth.com/

The information on this podcast contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management. Nucleus Wealth is a business name of Nucleus Wealth Management Pty Ltd (ABN 54 614 386 266 ) and is a Corporate Authorised Representative of Nucleus Advice Pty Ltd – AFSL 515796

This is an edited version of a live discussion with Cameron who recently republished his book from 2017 Game of Mates: How favours bleed the nation as Rigged “How Networks Of Powerful Mates Rip Off Everyday Australians”.

This book will open your eyes to how Australia really works. It’s not good news, but you need to know it.’ – Ross Gittins

‘You’ll be shocked at how far the Mates have their hand in your pocket.’ – Nicholas Gruen

Australia has become one of the most unequal societies in the Western world, when just a generation ago it was one of the most equal. This is the story of how networks of Mates have come to dominate business and government, robbing ordinary Australians.

Every hour you work, thirty minutes of it goes to line the Mates’ pockets rather than your own. Mates in big corporations, industry groups, government departments, the halls of parliament and the media skew the system to suit each other. Corporations dodge taxes, so you pay more. You pay more for your house and higher interest rates on your mortgage, more for your medicines and transport, and more for your children’s education and insurance, because the Mates take a cut.

Rigged uncovers the pattern of political favours, grey gifts and information-sharing that has been allowed to build up over two decades. Drawing on extensive economic research, it exposes the Game of Mates as nothing less than cronyism on a grand scale across Australia and how we have fallen behind other countries in combating it.

We also discuss housing policy and economics in general.

Dr Cameron K. Murray is a Research Fellow in the Henry Halloran Trust at the University of Sydney and an economist specialising in property and urban development, environmental economics, rent-seeking and corruption. Professor Paul Frijters teaches at the London School of Economics and was previously Professor of Health Economics at the University of Queensland.

http://www.martinnorth.com/

Go to the Walk The World Universe at https://walktheworld.com.au/

Join me for a live discussion with Cameron who recently republished his book from 2017 Game of Mates: How favours bleed the nation as Rigged “How Networks Of Powerful Mates Rip Off Everyday Australians”.

You can ask a question live!

This book will open your eyes to how Australia really works. It’s not good news, but you need to know it.’ – Ross Gittins

‘You’ll be shocked at how far the Mates have their hand in your pocket.’ – Nicholas Gruen

Australia has become one of the most unequal societies in the Western world, when just a generation ago it was one of the most equal. This is the story of how networks of Mates have come to dominate business and government, robbing ordinary Australians.

Every hour you work, thirty minutes of it goes to line the Mates’ pockets rather than your own. Mates in big corporations, industry groups, government departments, the halls of parliament and the media skew the system to suit each other. Corporations dodge taxes, so you pay more. You pay more for your house and higher interest rates on your mortgage, more for your medicines and transport, and more for your children’s education and insurance, because the Mates take a cut.

Rigged uncovers the pattern of political favours, grey gifts and information-sharing that has been allowed to build up over two decades. Drawing on extensive economic research, it exposes the Game of Mates as nothing less than cronyism on a grand scale across Australia and how we have fallen behind other countries in combating it.

We also discuss housing policy and economics in general.

Dr Cameron K. Murray is a Research Fellow in the Henry Halloran Trust at the University of Sydney and an economist specialising in property and urban development, environmental economics, rent-seeking and corruption. Professor Paul Frijters teaches at the London School of Economics and was previously Professor of Health Economics at the University of Queensland.

Go to the Walk The World Universe at https://walktheworld.com.au/

Another outing with our property insider Edwin Almeida, as we look at the latest in the rental sector, the latest listing numbers, and the latest from our We-Chat chatters…

Go to the Walk The World Universe at https://walktheworld.com.au/

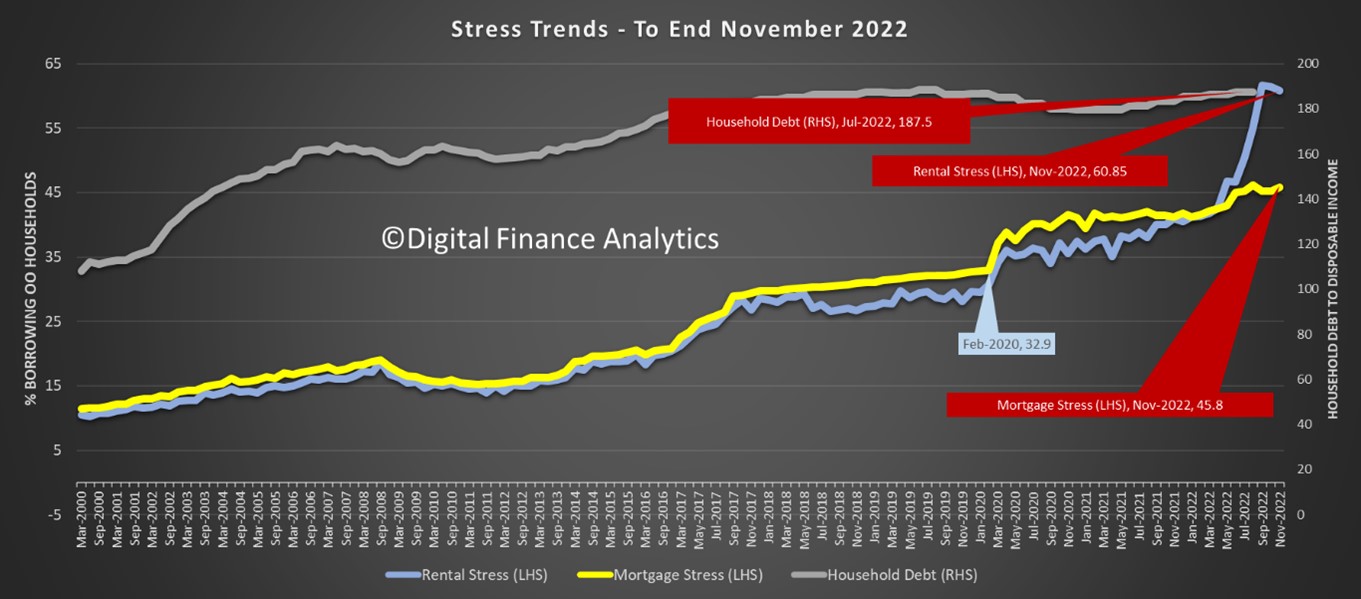

In our final update of the year, we incorporate the latest from our surveys as we assess the impact higher interest rates are having on households across the country, based on our rolling 52,000 omnibus survey.

And the news is not good, in that both mortgage stress and rental stress – defined in terms of cash-flow in and out, continues to grow, following the eighth rate hike from the RBA, which was promptly passed on to households by way of higher mortgage rates, (though not reflected to the same extent in higher deposit account rates I might add). There was also a continued rise in average rents, thanks to intense competition, lower supply and leveraged investors. All this set against an average inflation rate expected to hit eight per cent soon.

There are many different definitions out there (from 30% of income, or taxable income; through to underwriting metrics) but we define stress in CASH FLOW terms. If households have more outgoings (excluding one off discretionary items) than income, we define them as stressed. If they have a mortgage, they are in mortgage stress; if renting then rental stress.

Investors with cash flow pressures are identified as stressed investors. We also aggregate the data to estimate total financial stress. Each expressed as a % of households, and count. The latter is the best measure in our view.

This month, more than 1.75 million households with an owner-occupied mortgage, or 45.8% of borrowers register as stressed, while more than 1.88 million renting households, or 60.85% are stressed. And the household debt to income remains very high, as reported by the RBA.

Analysis By State

In this slide, we highlight in yellow where the proportion of households in stress rose compared with last month, blue means a fall, and no highlight means no change. Tasmania and South Australia are now vying for top spot, both with more than half of household in a negative cash flow situation. WA and Victoria follow on, then NSW and the other states.

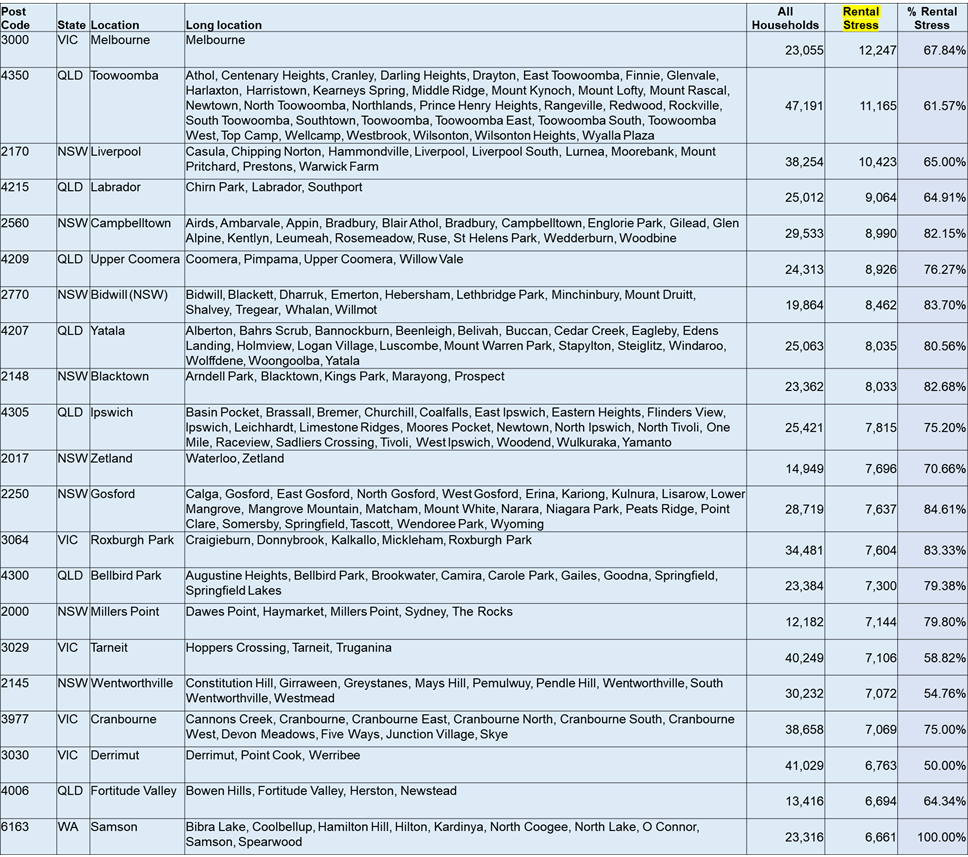

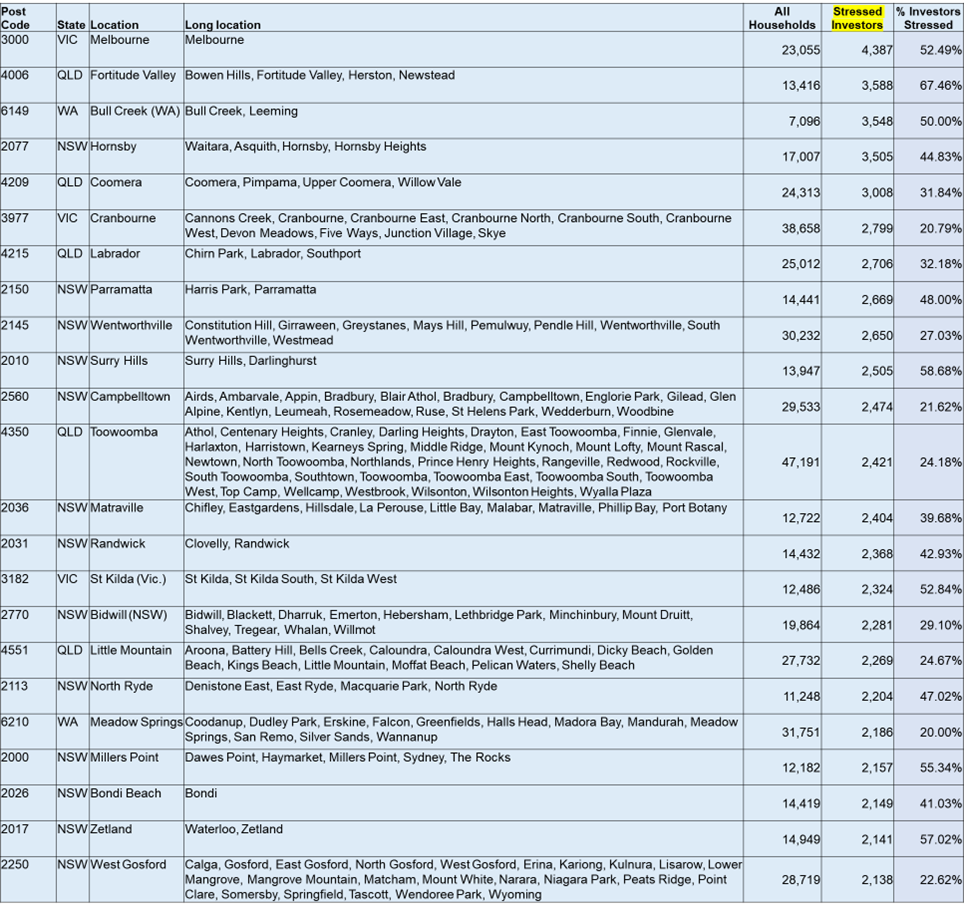

Rental stress is most significant in NSW, ACT and QLD. Investor stress is highest in NSW, because many investors are over-geared and experiencing significant rate hikes. Overall financial stress (an aggregated measure reveals that the state with the highest proportion of household in financial stress is the ACT.

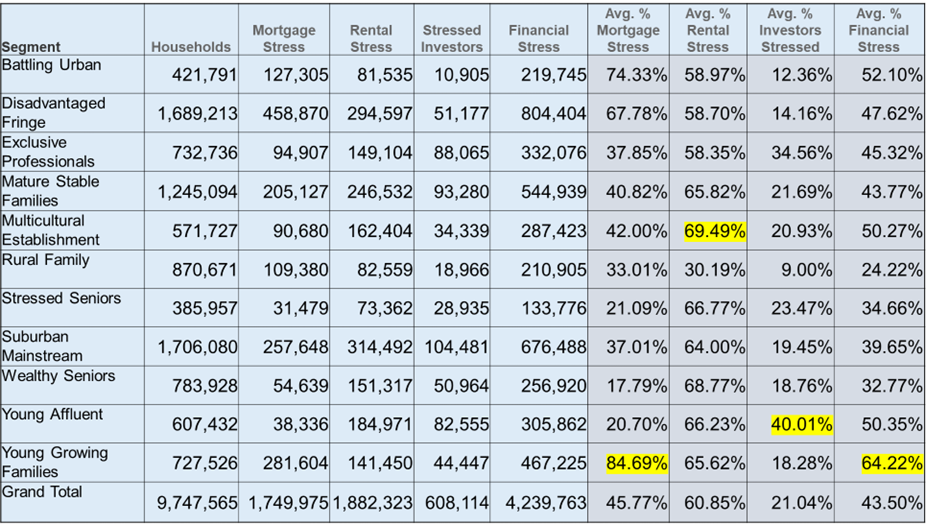

Analysis By Cohort

We analyse our data by different household segments or cohorts, as this provides an important lens to understand what is playing out across the country.

Mortgage stress is highest among Young Growing Families (which include many First Time Buyers) at 84.69%. We see also large counts of those on the Urban Fringe, as well as some more affluent households exposed. Rental stress is highest among first generation migrants at 69.49%. Investor stress is highest among Young Affluent households and overall financial stress is highest among Young Growing Families.

Whilst we continue to see stress building in the high growth suburbs, where many purchasers entered the market when mortgage rates were around 2%, we continue to see pockets of stress across different areas, including some which would generally be regarded as more affluent. Many households in these regions have large mortgages.

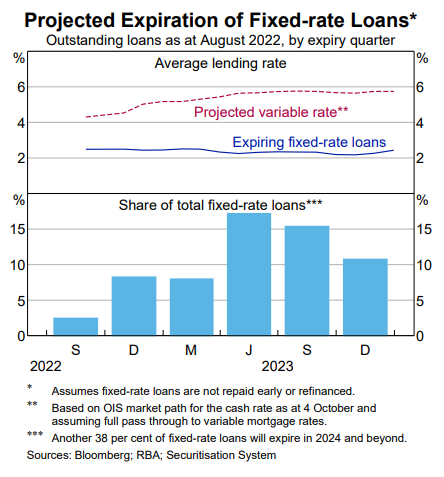

It is worth reflecting on the fact that about one quarter of mortgage holders have so far been insulated from mortgage rate rises because they are on fix term loans. However, many of these are due to reset next year, as the RBA showed in a recent report.

The expectation is that rates will still be high through 2023, and that mortgage delinquencies will rise, at the same time a property prices continue to slide. This is a perfect storm.

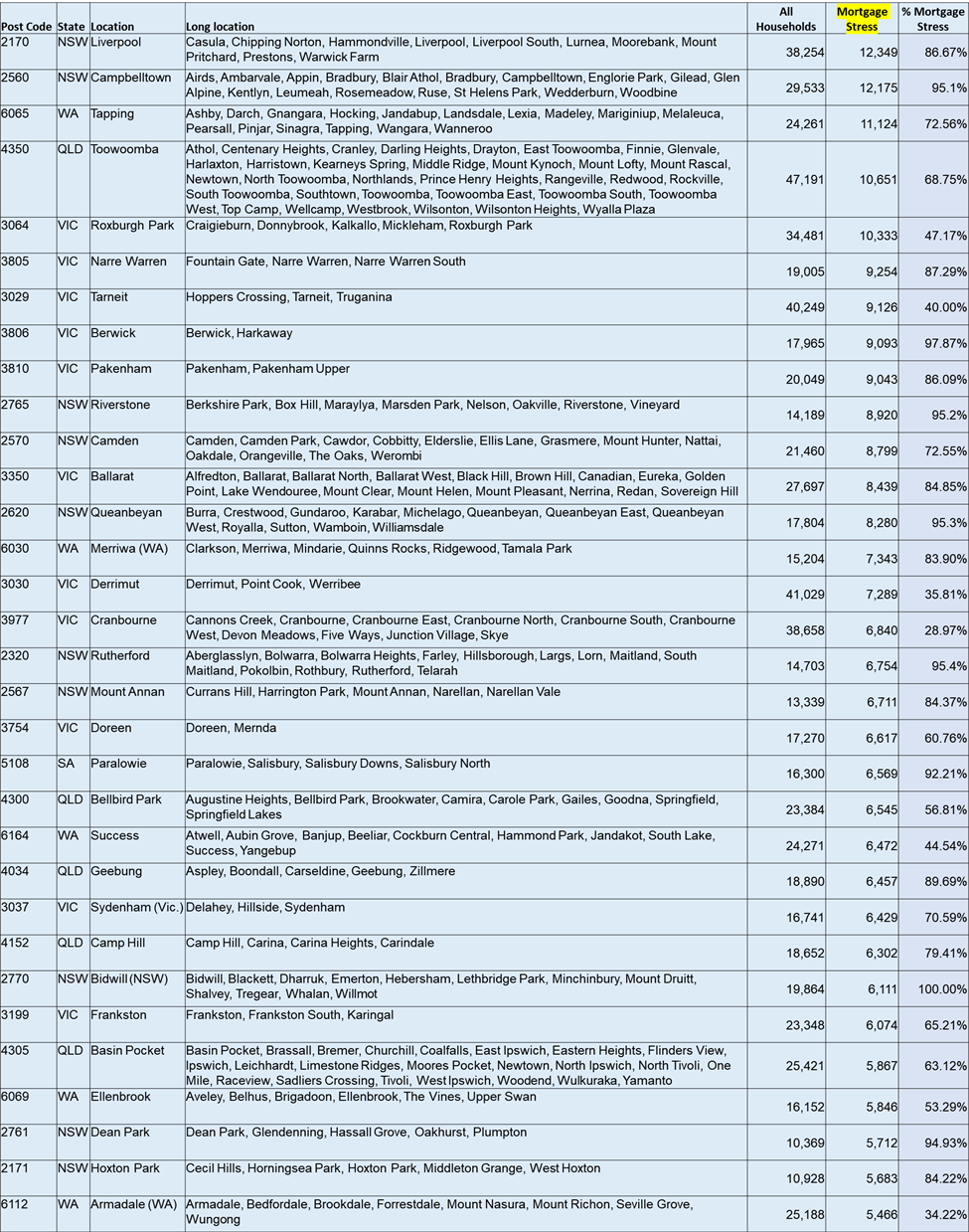

Post Code Analysis

We list the top post codes in each category, based on the COUNT of households.

Conclusions

We do not expect things to ease ahead, as interest rate rises continue to work though, and rental costs rise. Inflation is running hotter than expected, and the RBA still expects a peak around 8% but also staying high through 2023. As a result, households need to get to grips with their cash flow and prioritise important payments, such as mortgage and rental payments, over other perhaps less critical payments.

Households under mortgage pressure would do well to talk to their bank who do run hardship schemes designed to assist in times of crisis.

We also recommend the Government Debt Help Line on 1800 007 007 for people seeking unbiased free advice.

Finally, real wages growth remains below inflation, so households must consider the scenario where true incomes continue to shrink in real terms. As a result, stress levels will remain high for some time yet.

My latest Friday afternoon chat with Journalist Tarric Brooker, as we walk through the key charts as we come to the end of 2022. So, what might 2023 look like?

Go to the Walk The World Universe at https://walktheworld.com.au/