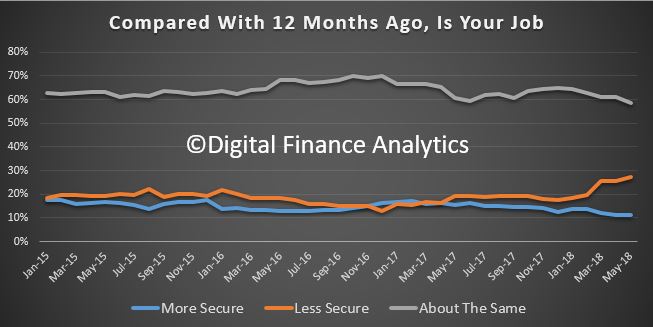

The latest Digital Financial Analytics Household Financial Confidence Security Index for May 2018 is released today. The index tests households attitudes to their finances, based on our 52,000 rolling household survey.

The index dropped to 90.2, down from 91.7 last month. This is below the neutral setting of 100.

Property-related sentiment is hitting hard, especially in New South Wales and Victoria where price falls are most evident. In Western Australia and South Australia, the index hardly moved compared with last month, and in Queensland it slid just a tad.

Looking across our property segments, those not in the property game, and renting or living continue to languish. But we also are tracking falls among property investors, reflecting difficulty in obtain finance, higher interest rates, and falling property prices, and now, also those who are owner occupiers. Both of these property owning segments slid again, mirroring falls in property prices, and the slowing auction clearance rates. That said, those owning property are still relatively more confident about their finances, compared with renters, so the property effect continues.

Across the age bands, those aged 40-50 were a little more confident, reflecting recent stock market progress, especially among those without mortgages (yes, some have paid down their loans completely), while levels of employment remain pretty good. But for younger households the budget pressure on them remains severe, especially those paying rent, or mortgages. Those entering the retirement phase, 60+ continue to wrestle with outstanding mortgages (many hold these loans into retirement now) and also lower returns from deposits.

We can examine the moving parts within the index, to get a sense of what is driving the results. First we look at job security. Something appears to be happening here, as the proportion feeling less secure is rising, up 1.7% compared with last month. There was also a fall by 2.4% of those reporting no change in sentiment compared with last month. Below the hood, it appears that more are involved in multiple part-time jobs, and becoming swept up in the gig economy. Zero-hours contracts appear to be on the rise in some industry sectors. So, while the number of jobs created may be north of one million as the Government often says, we question the quality of these jobs, and their security. Our index reveals another perspective.

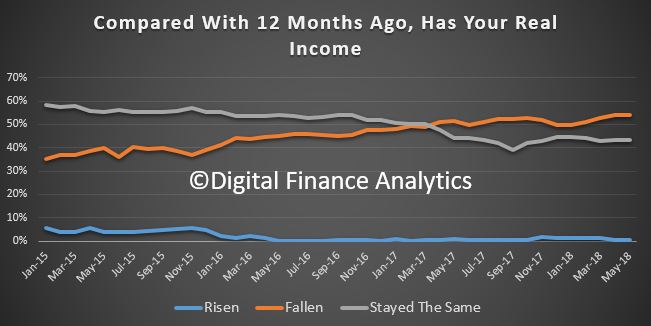

This may also help to explain the fall in real income (after inflation) many households are experiencing. 54% of households said their incomes had fallen in the past year, and only a small fraction report a rise. 43% say there has been no change since June 2016. There are a number of drivers here, but the main one is simply no, or low pay rises, adjustments to overtime rates, and lower returns from bank deposits. Many older households rely on income from savings and this in under pressure with the current low interest rates, and banks trimming their deposit rates too boot.

On the other hand, the costs of living continue higher. Nearly 81% of households say their costs are higher than a year ago, up 2% on last month. The litany of rising categories includes electricity, fuel, health care costs, school fees and child care costs. But households are also reporting higher costs at the supermarket, and a tendency to eat in, rather than out, to keep costs under control. More also turning to credit cards, or pulling equity from their properties to keep the household afloat.

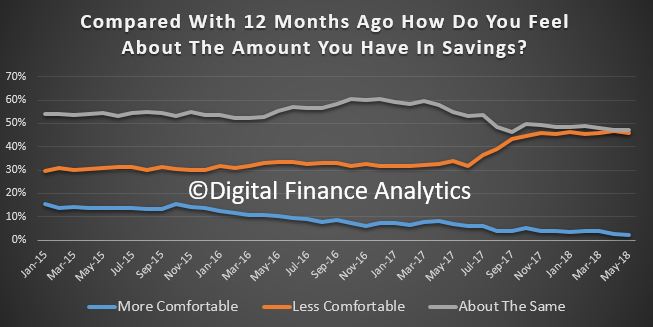

On the savings front, more are concerned about the amount they have for emergencies. Just 2% are more comfortable compared with last month, while 46% are less comfortable, up 1% on last month. The interest rates offered on bank deposits continue to fall, and this is impacting many who rely on a regular savings generated income. Those who are in the stock market are a little more positive, but the recent crash in bank shares following the revelations from the Royal Commission, and other adverse events, translates to lower confidence. Its worth remembering that nearly half of dividends paid last year came from the financial sector.

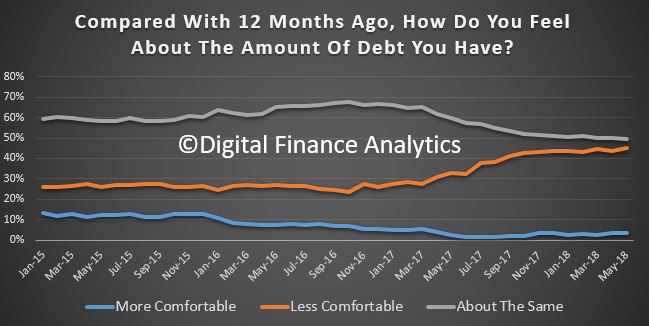

Households continue to feel the pressure from debt. 45% of households are less comfortable with the debt they owe, up 0.6% from last month. Around 49% remain the same as a year ago, and 3% are more comfortable. The drivers relate to larger mortgages, and higher real mortgage rates (despite some refinancing to gain a lower rate); the inability to get mortgage funding due to tighter lending standards, and a rise in equity withdrawals and some areas of personal credit. While personal credit balances overall are falling, personal debt is concentrated in households with larger mortgages and here it is rising. Payday lending is also on the rise. In addition, households are concerned about the prospect of higher interest rates ahead. Many are stuck in the debt machine.

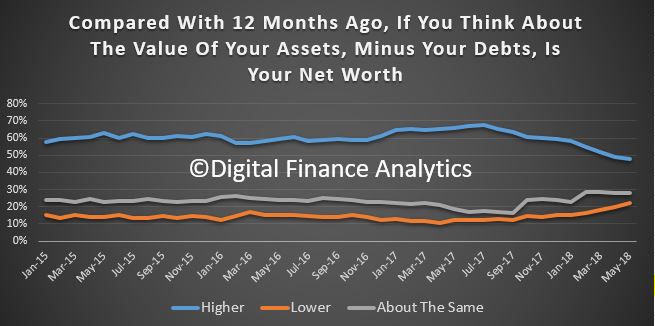

Finally, and putting the data together, we look at net worth – defined as assets less loans outstanding. 47% of households say their net worth has improved over the past year, down 4% on last month, as property values slide and household debt rises. 22% reported their net worth was lower, up 2% compared with last month and 28% said there was no change in the past year.

So, the pressures on household finances are clearly visible in these results, and bearing in mind the expected continued fall in home prices, and the prospect of interest rate hike, plus flat incomes, we expect the trend to continue to weaken in the months ahead.

This is certainty a different read compared with the recent headlines of jobs and GDP growth, and it shows the disconnection between the top-line narrative, and the real experiences of households across the country.

Whilst banks have reduced their investor mortgage interest rates to attract new borrowers, we believe there will also be more pressure on mortgage interest rates as funding costs rise, and lower rates on deposits as banks trim these rates to protect their net margins. In the last reporting round, the banks were highlighting pressure on their margins as the back-book pricing benefit from last year ebbs away.

By way of background, these results are derived from our household surveys, averaged across Australia. We have 52,000 households in our sample at any one time. We include detailed questions covering various aspects of a household’s financial footprint. The index measures how households are feeling about their financial health. To calculate the index we ask questions which cover a number of different dimensions. We start by asking households how confident they are feeling about their job security, whether their real income has risen or fallen in the past year, their view on their costs of living over the same period, whether they have increased their loans and other outstanding debts including credit cards and whether they are saving more than last year. Finally we ask about their overall change in net worth over the past 12 months – by net worth we mean net assets less outstanding debts.

Our research on the liveability of regional cities in Victoria has identified an important element: liveability in these areas requires fast, reliable and frequent rail connections to capital cities.

People living in regional areas still need access to capital cities. The reasons include employment, education, medical services, shopping, arts, culture and visits to family and friends.

Regional Victorians who lack access to reliable rail services remain deprived of non-car travel options. This forces them to drive and that adds to traffic congestion in our capital cities. Car dependency is costly for health and wealth.

Regional rail is important both to meet the needs arising from predicted population increases across regional areas and to manage the rapid population growth and sprawl of our capital cities. Australia’s population is predicted to increase by 45 million by 2100 and our cities are already expanding rapidly. We need to start thinking about where these extra people are going to live.

At present, most people (more than 80%) in Australia live in capital cities. However, as populations grow, more people will start moving to regional areas. This means we need to pay more attention to the liveability of regional Australia as well as capital cities.

Wherever they live, people need transport to get to employment, education, shops and services, and to socialise with friends, family and community members. Furthermore, our research has found that having close access to a range of these things is associated with better health and well-being. Good access to frequent, reliable and fast transport is not a luxury. It is a critical factor influencing liveability and is described as a social determinant of health – one of the conditions (where we live, learn, work and play) that influence our health.

Liveable places promote health and well-being among the people who live there. However, they also require transport options, including public transport such as trains, buses, trams as well as walking and cycling. In regional areas expansive distances make it hard to get by without a private vehicle.

A good example of this is Mitchell Shire. It begins at the northern edge of metropolitan Melbourne and extends to the regional town of Seymour in northeastern Victoria.

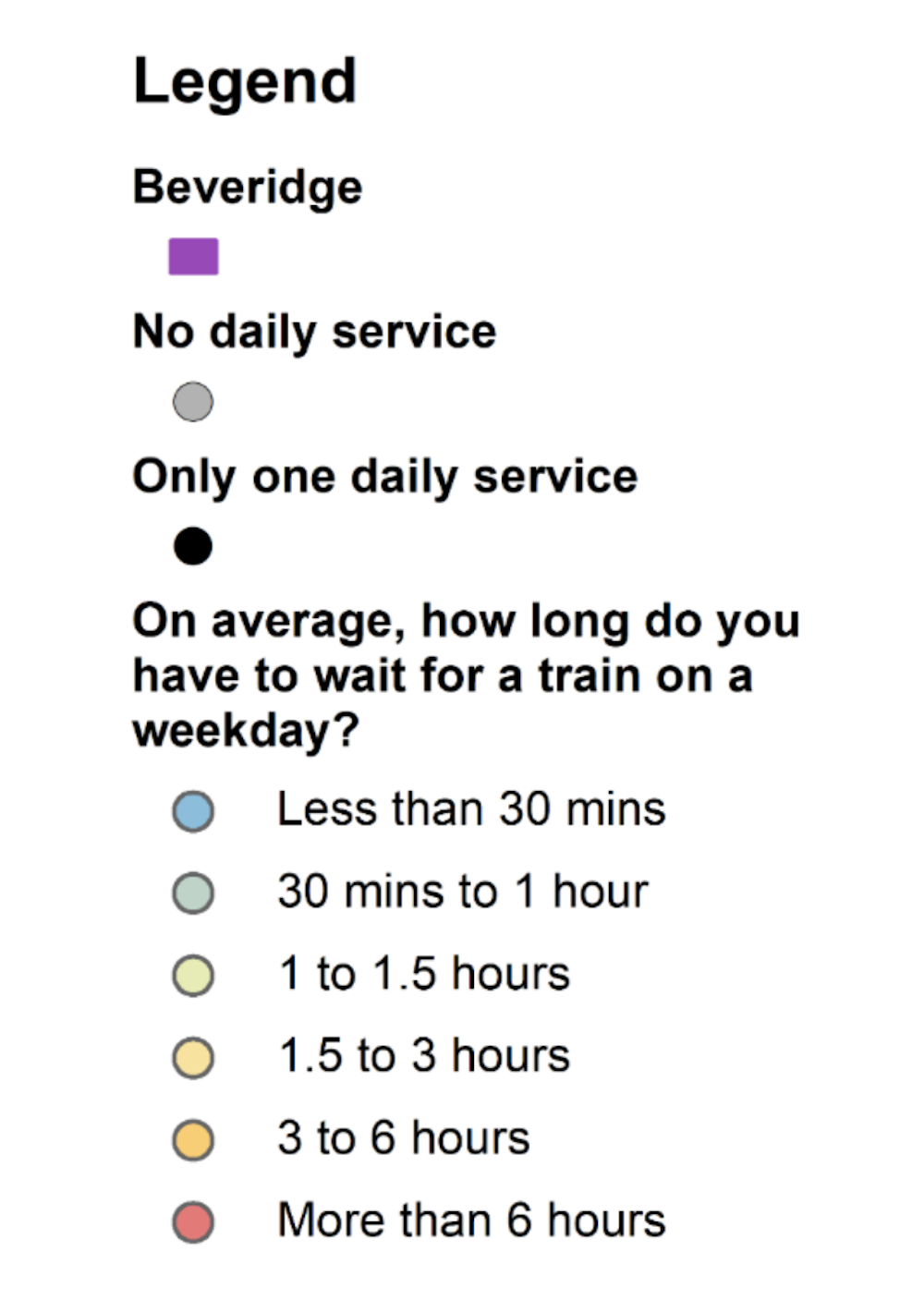

To understand the current regional rail services (and liveability) for areas like Beveridge we produced the summary map below.

Wait times between 6am and 9pm for regional train routes with a daily service on weekdays. Calculated using Public Transit Victoria data from April 12 to June 10, 2018.Author provided

Developers’ signs in the Beveridge area are advertising “40 minutes to the city” along the Hume Highway. Perhaps they are including a helicopter in their house and land packages. Based on current regional rail options, residents must drive to their nearest station 10-15 minutes away, wait for a train – services depart at intervals of 34-105 minutes – and then travel up to an hour to the city during peak hour.

Alternatively, these developments might be encouraging car use as the main means of transport. In that case, Google Maps suggests peak-hour travel from Beveridge to the Melbourne central business district takes between one and two hours on a weekday. Again, as well as being associated with poor health outcomes, long commutes by car will increase traffic congestion along the route and in the city.

Regional rail services are highly uneven

The map above also suggests that some areas of regional Victoria are doing better than others in terms of regional rail connections to Melbourne.

Consider the examples of Bendigo and Shepparton in central and north-eastern Victoria. Shepparton is a large regional centre, with an economy established in health services and agriculture. Its population is projected to grow to 315,000 people by 2046.

Shepparton Council planning is guided by a liveability framework, a 30-year plan and has recently completed a liveability assessment. However, Shepparton’s economic and social development is restricted by only four train services to Melbourne per day compared to Bendigo’s 27 services.

Car dependency, transport planning and urban design are critical social determinants of health that also need to be considered in creating liveable, well-connected communities in regional areas. We need to act now if we are to learn from the liveability lessons of our capital cities and avoid repeating the mistakes.

Authors: Melanie Davern, Senior Research Fellow, Healthy Liveable Cities Group, Centre for Urban Research, RMIT University; Carl Higgs, Research Officer, Centre for Urban Research, RMIT University; Claire Boulange, Postdoctoral Research Fellow, Centre for Urban Research, RMIT University

Jonathan Arundel; Senior Research Fellow, Healthy Liveable Cities Group, Centre for Urban Research, RMIT University; Lucy Gunn, Research Fellow, Centre for Urban Research, RMIT University; Rebecca Roberts, GIS Analyst, Centre for Urban Studies, RMIT University

ASIC is warning consumers about companies that claim they can fix a poor credit rating. ASIC is running a month-long campaign, with other Commonwealth, state and territory agencies, to help consumers understand that by using credit repair and debt management firms they may end up paying high fees.

Consumers should be aware these companies often fail to fix credit and debt issues, which can leave people in a worse financial situation.

ASIC Deputy Chair, Peter Kell said consumers may not realise that free services exist to help them fix credit reports or resolve their debt problems, such as the National Debt Helpline.

‘Consumers experiencing money or debt problems don’t need to put themselves under further financial stress by paying high fees to firms providing credit repair and debt solution services’, Mr Kell said.

‘If people are having difficulty obtaining loans because of an incorrect default listing on their credit report, there are actions they can take that are free of charge to have it corrected.

‘If you think you have had a credit default wrongly listed against you, contact the creditor and ask for it to be removed. If you aren’t satisfied with the response you receive you can contact the relevant dispute resolution service for help’, added Mr Kell.

People experiencing debt problems can seek free help and guidance from financial counsellors and the National Debt Helpline on 1800 007 007 or go to ndh.org.au.

In 2016, an ASIC report[1] found debt management firms:

were offering services where fees and costs were not well explained;

often required payments be made before services were provided;

sometimes used high-pressure sales techniques.

Mr Kell suggested consumers can consider alternative services like financial counselling before engaging a debt solutions firm.

Consumers should be aware that lenders will review their credit report when they apply for credit or a loan and they should check their credit history details are correct. Consumers are entitled to obtain one free copy of their credit report each year from a credit reporting agency.

ASIC is the lead Australian Government agency for financial literacy, consistent with its strategic priority and statutory objective to promote confident and informed consumers and investors. ASIC’s financial capability program includes:

leading the National Financial Literacy Strategy;

providing consumer information via ASIC’s MoneySmart; and

delivering ASIC’s MoneySmart Teaching program.

The National Financial Literacy Strategy, led and coordinated by ASIC, is a framework to guide policies, program and activities that aim to strengthen Australians’ financial capability.

In addition to ASIC, other agencies involved in the campaign include the Australian Competition & Consumer Commission (ACCC), Consumer Affairs Victoria, NSW Fair Trading and the Queensland Office of Fair Trading.

The Federal Court recently found, in proceedings brought by ASIC, that credit repair business Malouf Group Enterprises Pty Ltd and its director Jordan Francis Malouf breached the Australian Consumer Law by making false and misleading representations and engaging in unconscionable conduct. In addition to penalties imposed by the Court, the Malouf Group will pay $1.1 million to consumers (refer: 18-114MR).

Free financial services available to consumers

Financial Counselling

Financial counselling is a free service offered by community organisations, community legal centres and some government agencies. Financial counsellors can help consumers solve their money problems.

National Debt Helpline

The free hotline – 1800 007 007 – is open from 9:30am to 4.30pm, Monday to Friday (opening hours can differ in different states) to help consumers struggling with debt. Consumers can visit the National Debt Helpline website for information and resources.

The Department of Agriculture runs a Rural Financial Counselling Service to support primary producers, fishermen and small rural businesses that are suffering financial hardship, for further details call 1800 686 175.

ASIC’s MoneySmart website provides a financial counsellor online search tool to locate a financial counsellor near you.

External Dispute Resolution (EDR) services

A credit repair company may offer to contact an External Dispute Resolution (EDR) service to resolve a consumer case. The company could charge a fee, even though those services are free and are designed to be easy for people to use. Consumers can save time and money by contacting an Ombudsman directly, rather than going through a credit repair company.

FOS handles complaints about banking, credit, loans and debt collection, life insurance, superannuation, financial planning, insurance broking, stockbroking, investments, managed funds, timeshares, general insurance, finance and mortgage broking. They do not deal with complaints about compulsory third party, private health, public liability and workers’ compensation insurance.

CIO handles complaints about credit unions, building societies, non-bank lenders, mortgage and finance brokers, financial planners, lenders and debt collectors, credit licensees and credit representatives.

Other dispute resolution services

Energy, water and telecommunication ombudsman services provide free advice and conciliation services for consumers with complaints about providers in those industries.

Does the Coalition’s tax plan favour high earners over those with lower incomes?

Depending whom you listen to, the tax cuts, unveiled in last month’s federal budget, lead to either a flatter, more regressive tax system under which low-income earners will be even worse off relative to high earners, or the opposite, with a progressive outcome. It can’t be both.

While there are tax cuts proposed from July this year, the most substantial cuts are planned for 2022-23 and then 2024-25. As this is several years away, it becomes tricky to analyse their likely impact.

The main issue is wage inflation, which in turn leads to “bracket creep”. We tend to think about the change in terms of what it means for today’s incomes, but that’s not realistic. An annual income today of A$80,000 will be around A$110,000 by 2027-28 if the government’s wage projections prove to be accurate.

Using our model of the Australian tax and welfare system, PolicyMod, we projected the incomes of each person in the 20,000 families in the underlying model survey data (the Australian Bureau of Statistics’ Survey of Income and Housing 2015-16).

We did this for each year until 2028-29, using the federal budget’s wage assumptions. We then used this to forecast the outcome of the proposed tax cuts, and compared it with the effects of maintaining current tax rates.

Our results are remarkably similar to the forecasts of Treasurer Scott Morrison. He has projected a total tax cut between 2018-19 and 2028-29 of A$143 billion, whereas our model puts this figure at A$140 billion.

Whose tax is being cut?

Who will actually receive these tax cuts, and will they really benefit? Our modelling shows around 50% of the adult population pays income tax in a given year. So clearly the benefit goes to the top half of the taxable income distribution.

What’s more, if the tax cuts are only returning bracket creep for many taxpayers, then they are not really tax “benefits”, because they will not make those people better off in real terms.

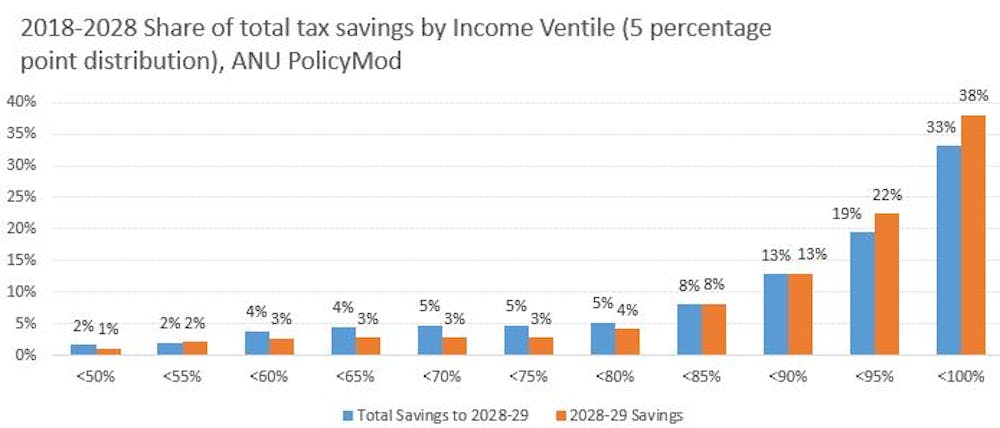

This is clearly shown in the chart below, where the bottom 50% of taxable income individuals will have a negligible share of tax savings. Around 33% of total savings between 2018-19 and 2028-29 go to people in the top 5% of incomes. In 2028-29 it is 38%.

If this were the end of the story, we might conclude that the tax cuts are grossly unfair. But it’s not quite as simple as that, because people with the highest taxable incomes are not necessarily the “wealthiest” people.

A more reasonable test considers whether the income tax cuts are real or “imagined”. If they are real, average tax rates should be lower. The fairness of the tax cuts can then be judged by the share of the tax burden across the income distribution.

If high earners are paying a larger share of tax than low and middle earners, then we have a more progressive tax system. A less progressive system, in contrast, is a flatter system – although not necessarily a totally flat income tax rate.But determining whether the proposals are progressive or regressive still doesn’t fully answer the question of whether they are “fair”.

Fair tax hikes for all?

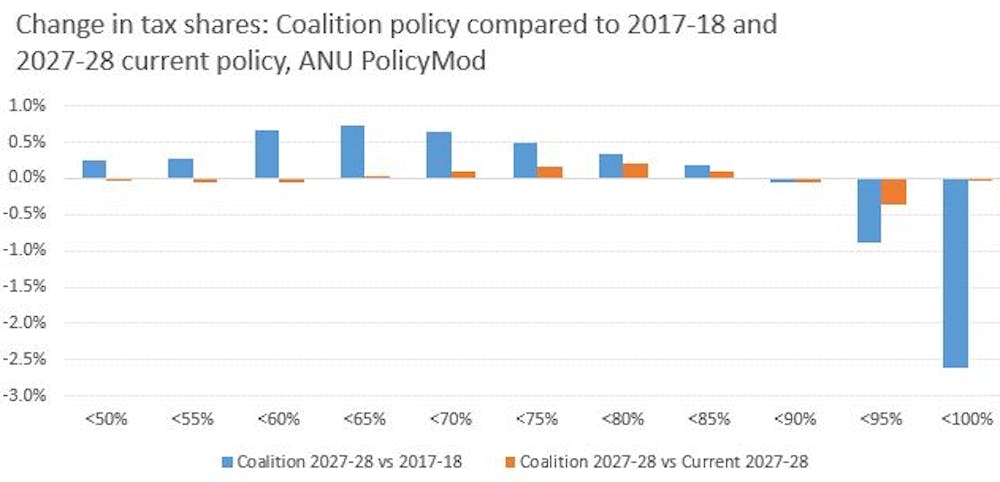

The chart below shows that tax rates will increase for all income groups, although they will rise more slowly if the Coalition’s tax plan is delivered. Crucially, higher earners will feel this difference most keenly. By 2027-28, the top 5% of earners average tax rate will be 2.1 percentage points lower than under the current regime, whereas for the bottom 50% the difference is just 0.2%.

Another way of looking at progressivity is to consider the share of tax paid. The chart below shows that under the current policy trajectory, higher-income groups pay a lower share of tax in future years compared with 2017-18. This occurs naturally due to bracket creep, which tends to impact low- and middle-income people more than those with very high incomes.

In the current financial year the top 10% of earners pay 58% of personal income tax. By 2027-28 this is projected to fall to 54.8% if the tax regime remains unchanged. Under the Coalition’s tax plan it is only marginally lower still, at 54.3%.

Anyway, it is purely hypothetical to extrapolate the current tax regime as far ahead as 2027-28. It is highly likely that future governments will change the tax code for a range of reasons, including overcoming bracket creep.

Note also that some “low-income” people may live in high-income households. However, our earlier analysis looking at households rather than individual earners also suggests that the Coalition’s tax proposal is marginally less progressive than the current system.

The chart below shows that the Coalition’s tax policy will have only a limited impact on the tax shares at different income levels by 2027-28. Perhaps a more relevant comparison is with the current tax shares for 2017-18, where a clearer pattern emerges of low- and middle-income earners paying a larger share of taxation.

The upshot is that the Coalition’s policy only partly overcomes bracket creep, with taxes still set to increase overall in the long term. The proposed policy does slightly more to overcome bracket creep for higher-income individuals. But it also locks in a higher tax share for those on low and middle incomes, and a lower share of the tax burden for higher earners.

On that basis, the proposals will lead to a slightly less progressive income tax regime than the one we currently have. But it will still be a long way short of a flat tax, and pretty much everyone looks set to be paying more income tax a decade from now.

Authors: Ben Phillips, Associate Professor, Centre for Social Research and Methods, Australian National University; Matthew Gray, Director, ANU Centre for Social Research and Methods, Australian National University

From Guest Blogger Alex Petrovic – currently working as finance content contributor.

Australia’s gig economy has been on the rise for a number of years, and new data by the Australian Bureau of Statistics (ABS) reveals that the number of workers considered to be part of this economy is still growing. From Deliveroo to Uber and Upwork, people are increasingly turning to jobs that offer a better work-life balance.

But what does this mean for gig economy workers seeking a home loan? With more Australians becoming self-employed, demand from these borrowers is set to increase, and lenders will need to adapt to meet their needs.

The rise of the gig economy

Gig economy work is growing around the world, not just in Australia. With the spread of mobile internet connectivity and platform websites such as 99designs, Airtasker, and Freelancer, people can now work from anywhere they like, whether that’s at home or from their local café.

It’s an attractive option for many people who are seeking a better work-life balance, yet doing short spells of contract work or completing work for a range of employers can make things more challenging when it comes to securing a home loan.

The difficulty of securing a home loan

Following the global financial crisis, self-employed borrowers faced even more significant challenges securing a mortgage. When you’re your own boss, income isn’t always steady, and without a history of up to three years’ worth of accounts or payslips, it can be far more difficult to obtain verification.

Banks became far less willing to lend to those they regarded as being riskier than your more traditional borrower with a standard income. For a potential borrower with enough savings and income to pay their deposit and keep up with repayments, being refused merely for having a non-standard income can be incredibly frustrating.

While self-employment has been on the rise for some time, securing a home loan is still proving difficult for many Australians. In fact, a recent survey revealed that one in five have been turned down for a loan, and of these, 26% were declined because they were self-employed or working part-time.

What is perhaps more worrying, is that more than half of those who were declined for a loan at a bank were not aware that other options are available. Non-bank lenders can help sole traders when it comes to securing a mortgage. By assessing applications on a case-by-case basis and having a more flexible approach to the type of documentation they can use to conduct their lending assessments, they may be able to help where other lenders cannot.

This flexibility isn’t just about giving borrowers other options; using documentation such as accountant letters, bank statements, and business activity statements can actually provide lenders with a more current picture than some traditional forms of documentation might.

While some may have concerns that these types of lenders will charge much higher interest rates, what you’ll find is that they actually offer very competitive rates. For example, the lowest interest rate from Commonwealth bank is 3.79%, although rates do vary depending on the loan to valuation ratio (LVR).

Time for a change

What the larger financial institutions have done is essentially create a void by only focusing on one type of customer. Old style policies must be adapted to suit newer generations and those working in the gig economy.

Banks should follow the lead of non-bank lenders, who offer a more flexible approach and look at the whole picture of an individual’s circumstance to gain a better understanding of potential borrowers. There is no need to loosen lending criteria; it’s about staying current and helping this underserviced market find a solution that meets their needs.

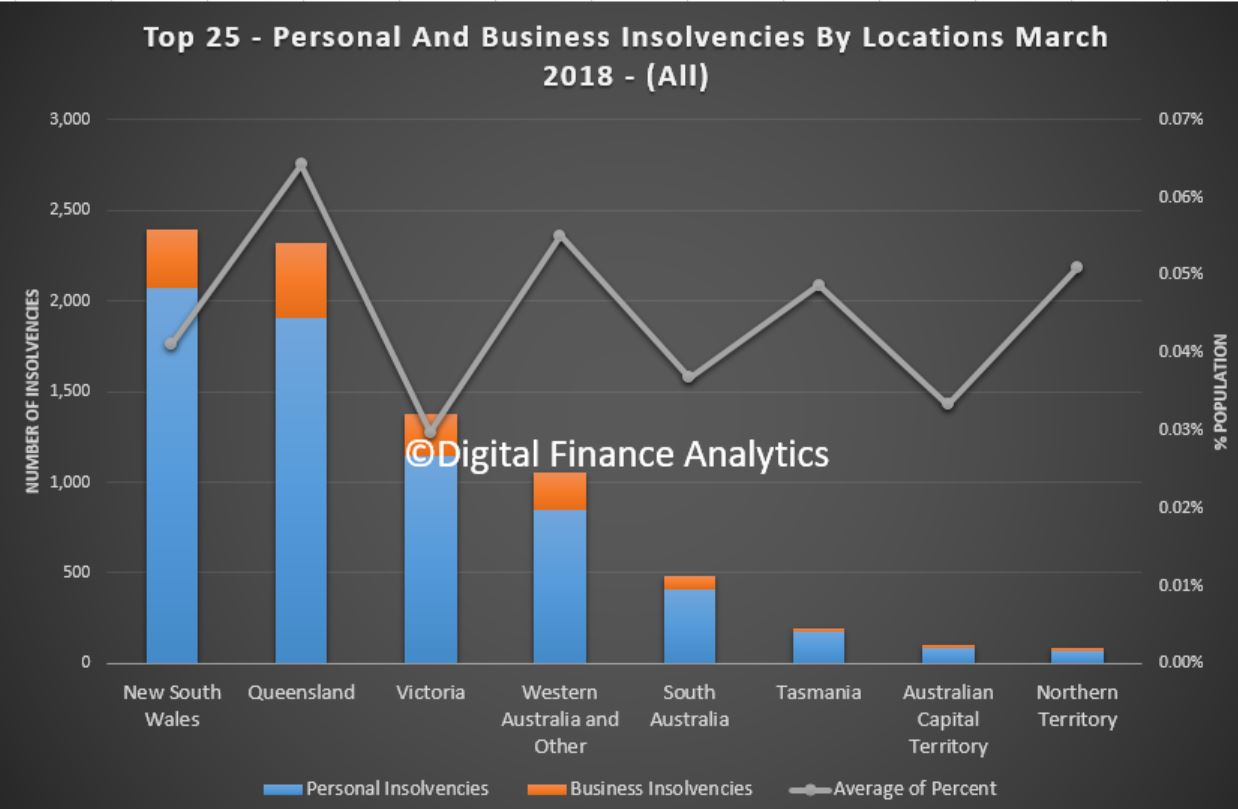

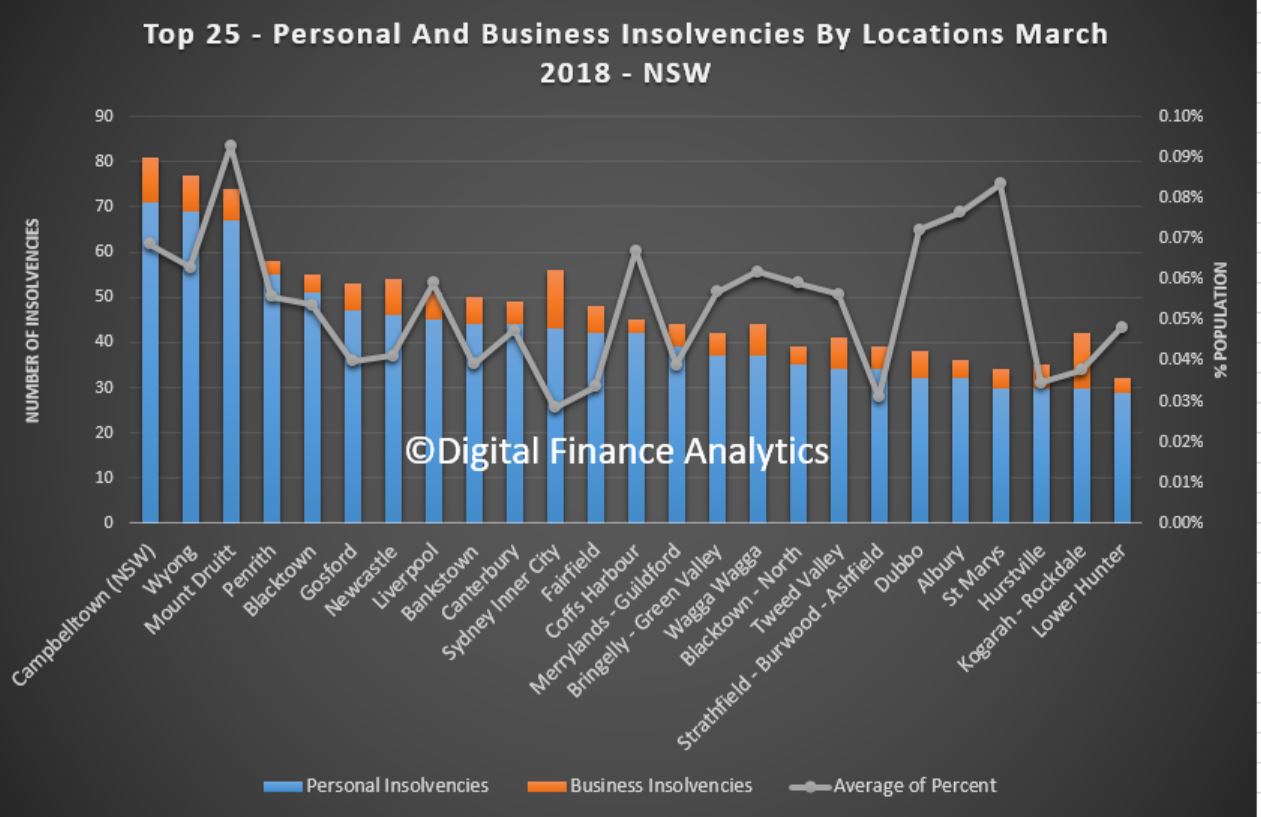

By state, NSW leads the way with 2,073 personal insolvencies and 322 business insolvencies. Queensland has 1,908 personal insolvencies and 410 business insolvencies and has the highest proportion of the population across the states in trouble.

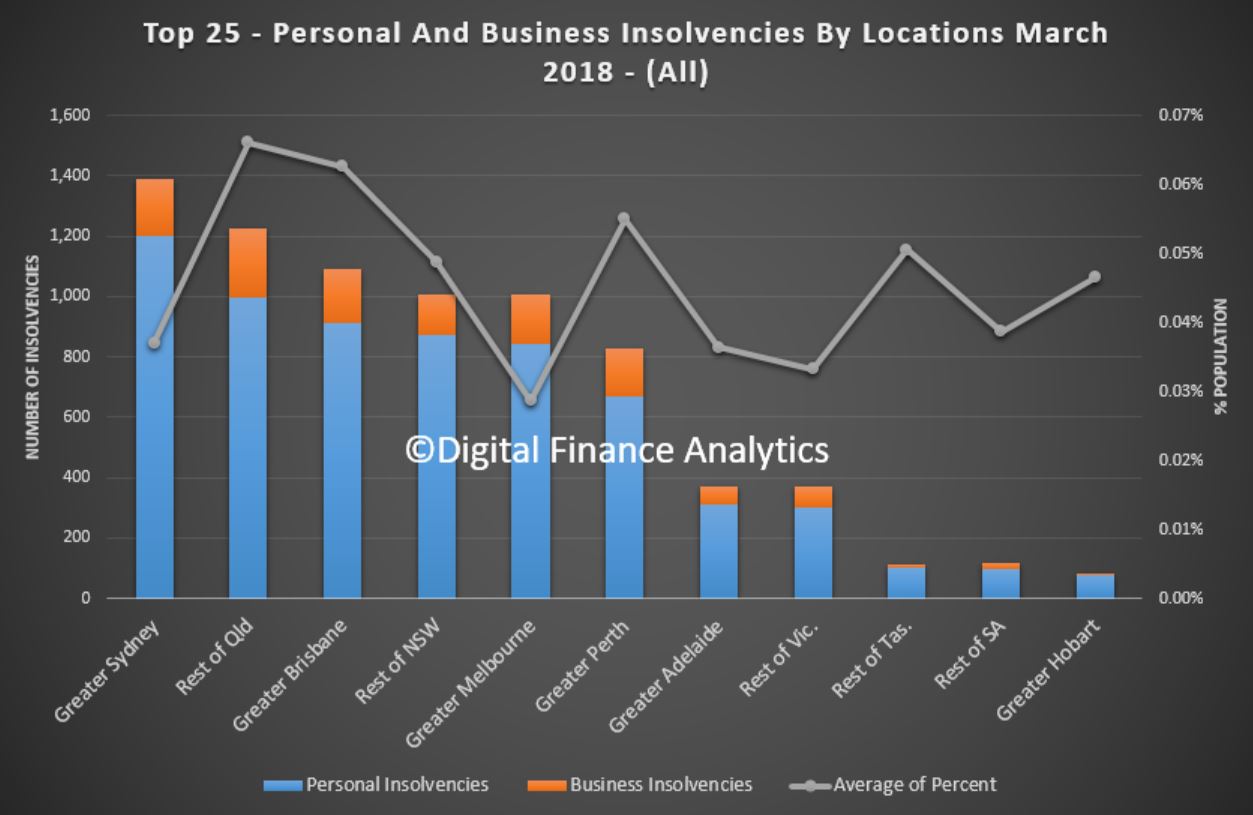

Drilling down, we see the Greater Sydney and the Rest of Queensland lead they way, followed by Brisbane.

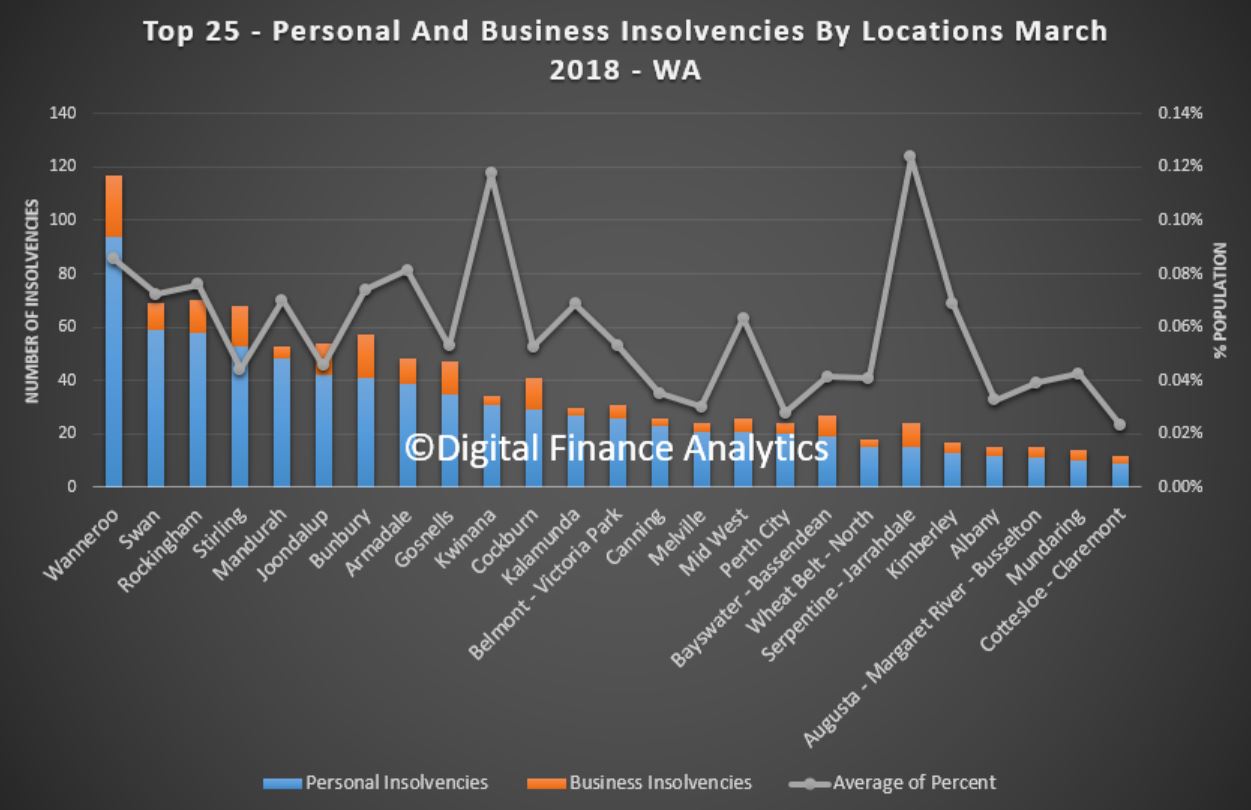

We can then look across the main states by location. WA’s worst location is Wanneroo, followed by Swan and Rockingham (aligns with our mortgage stress analysis by the way).

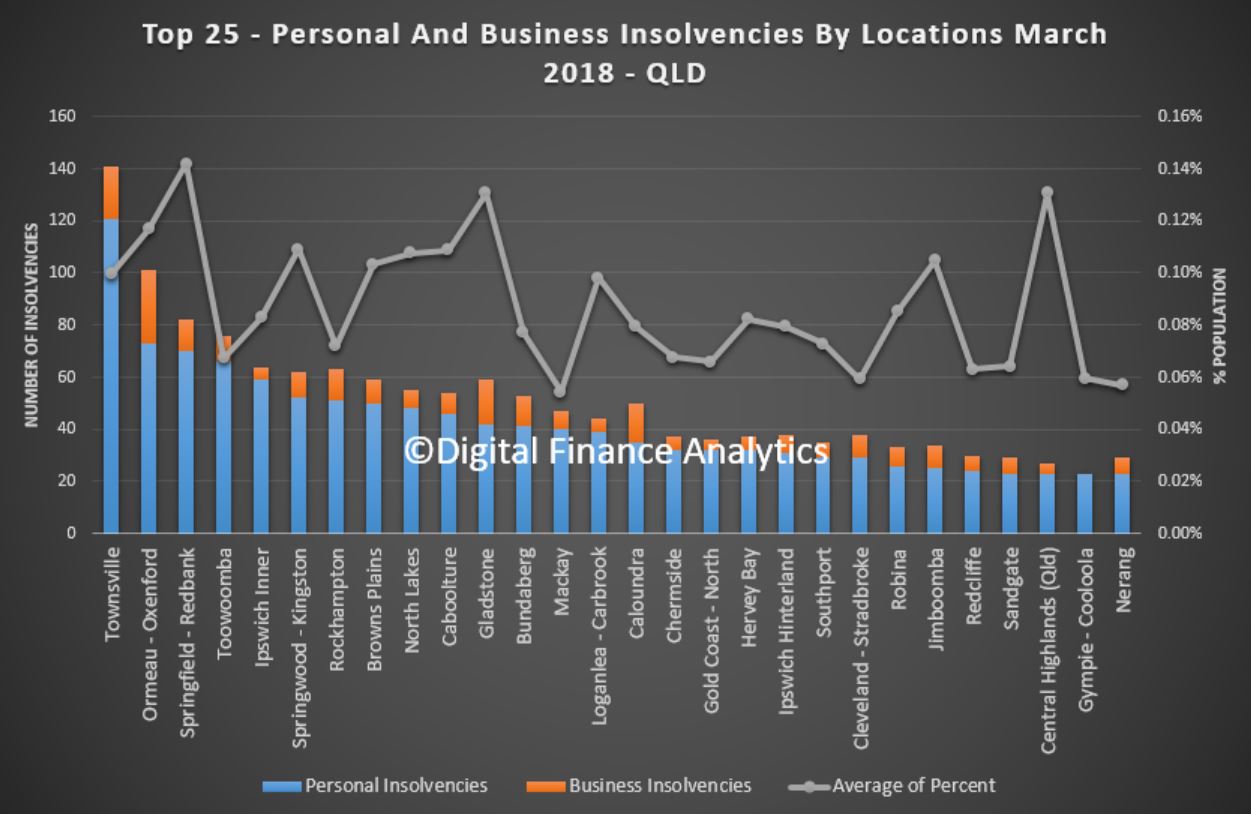

In Queensland, Townsville and Ormeau – Oxenford lead the way.

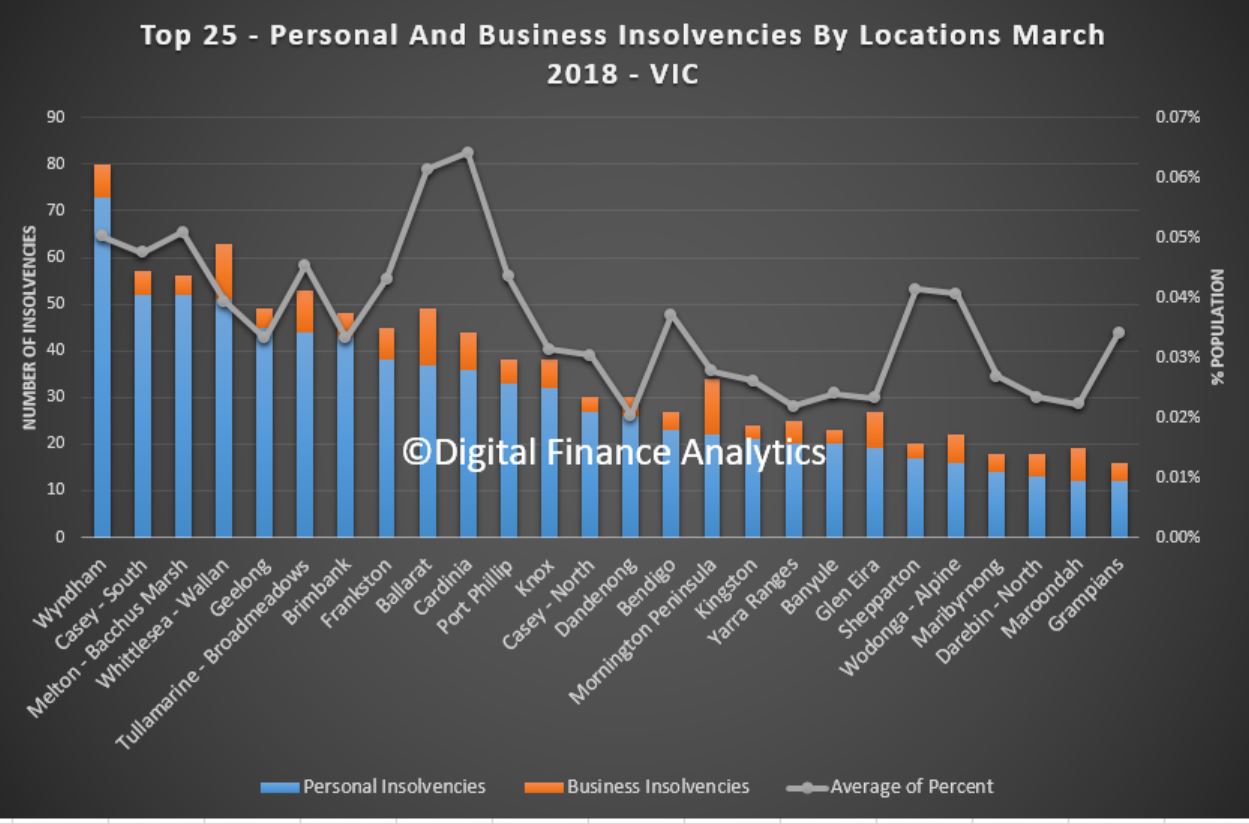

In Victoria Wyndham and Casey – South are the highest counts.

And in NSW, Campbelltown, Wyong, Mount Druitt and Penrith are the leaders – again close correlation with our mortgage stress analysis.

The point to make is insovencies do vary considerably by geography, as does the mix of business and personal insolvencies.

Welcome to our latest summary of finance and property news to the 26th May 2018 with a distinctively Australian flavour.

Watch the video, listen to the podcast, or read the transcript.

I had a number of interesting discussions with people who follow our analysis of the property market this past week. One in particular which stood out was from Melbourne who told me that in February 2017 he decided to sell his home, and got an indication it would sell conservatively for 1.3 million dollars. After a delay he took it to auction in August 2017 and struggled to see $1.25 million. But that property is now worth $1.15m a $150,000 drop from Feb 2017 to May 2018 or 11%. He also told me that back in 2017 he could have got a mortgage of $980,000, but now, on the same financial basis he can only access $670,000 today.

That in a nutshell is what is happening in the major markets, with people’s mortgage borrowing power being curtailed, and as a result home prices are falling. And they will fall further.

We had a bevy of analysts revising down their forecasts for future home prices this week. It is tricky to determine the extent of any fall ahead, and most predictions will of course be wrong. But the more significant factor in play is the significant change in the atmospherics around the housing sector. More are going negative. And when the largest lender in Australia signals they expect a fall, even a mild one, this is significant.

Recently Morgan Stanley said it is predicting property prices could fall by about 8% in 2018, and lending by more than a third. Morgan Stanley suggests there’ll not only be further price weakness in the months ahead, but also the likelihood of renewed softening in building approvals. It says these two factors will likely weigh on household consumption and building activity, seeing Australian economic growth decelerate, rather than accelerate, this year.

CBA has also gone negative on housing, now forecasting a mild correction. Gareth Aird, senior economist at CBA says that Australian residential property prices have fallen over the past six months. Additional declines appear likely over the next 1½ years due to a further tightening in lending standards, a continued lift in supply, potentially higher mortgage rates and more rational price expectations from would-be buyers. But he says a hard landing, however, looks unlikely and “is not our central scenario”.

We discussed this analysis in more detail in our recent release “Another Bank Goes Negative On Housing” which is still available. And remember CBA is the largest mortgage lender for owner occupied loans. Until recently they were bullish on prices, so this reversal is significant.

And UBS, who called the top of the market earlier than most, says macroprudential tightening ‘phase 3’, is a ‘game changer’ that will materially further tighten credit ahead, with higher living expense assumptions & debt to-income limits cutting borrowing capacity ~30-40%. Indeed, they says, housing is already weakening more quickly than our bearish view, with home loans dropping by ~10% since Aug-17, before the full Royal Commission impact. We have shifted our base case towards our ‘credit tightening scenario’, where home loans falls ~20%, credit growth drops to ~flat, prices fall persistently, & the RBA holds for longer. This coupled with record housing supply in coming years & a slump in foreign buyers sees us downgrade our house price outlook to fall 5%+ over the next year; below our prior 0 to -3% y/y. They conclude that housing activity will correct & prices to fall; still with downside risk: We still expect commencements, activity & prices to have an ongoing ‘downturn’ until at least 2019 – with downside risk from a ‘credit crunch’ scenario amid regulatory tightening & the Royal Commission. But housing should not ‘crash’ without (unexpected) RBA rate hikes or higher unemployment. So that’s ok then…

CoreLogic added some colour to the question of home prices by assessing home price growth across each decile, which confirms that values have fallen fastest at the premium end of the market. The broad trend findings in the CoreLogic May Decile Report showed that values have been falling on an annual basis across the 10th decile (the premium end of the market), while all other valuation deciles enjoyed positive (albeit restrained) growth over the twelve months to April 2018. National dwelling values were 0.2% higher over the 12 months to April 2018 – the slowest annual rate of growth since values fell -0.3% over the 12 months to October 2012. Analysing deeper at a decile level, it was only the most expensive 10% of properties that recorded a fall in values over the year (-4.3%) and all other sectors recorded annual growth greater than 0.2%.

In Sydney the most expensive decile, have fallen 7.2% over the past year, while in Melbourne the same decile fell just 2.4%. In contract the cheapest 10% of houses rose 1.5% in Sydney, and 11.9% in Melbourne over the past year. This is thanks partly to first home buyer stamp duty concessions implemented by both state governments from 1 July 2017. But be warned, if Perth is any guide, the top of the market falls first, but other sectors soon follow. This is one reason why we continue to hold the view prices will drop further than many analysts are predicting.

The credit tightening is real, borrowing power is being reduced, and investors are voting with their feet. We continue to see investors planning to exit the market before prices fall further. If you want further evidence, look no further than the latest auction clearance rates. CoreLogic says the combined capital city auction market continues to soften throughout 2018; while volumes have remained relatively steady over each of the last 3 weeks the weighted average clearance rate has continued to decline. Last week, the combined capitals returned a final auction clearance rate at a record year-to-date low of 56.8 per cent, the last time clearance rates were tracking at a similar level was in early 2013. With 2,100 homes taken to auction last week almost half of these failed to sell, over the same period last year the clearance rate was a much higher 73.1 per cent across 2,824 auctions.

In Melbourne, the final auction clearance rate increased last week across a slightly lower volume of auctions, with 62 per cent of the 1,033 auctions reported as selling, up on the previous week when the final clearance rate across the city dropped below 60 per cent (59.8 per cent- 1,099 auctions).

Sydney’s final auction clearance rate fell to 54 per cent last week, the lowest recorded since late 2017, with 672 homes taken to auction which was lower than the week prior when 787 auctions were held and a higher 57.5 per cent cleared.

Across the remaining auction markets, Adelaide was the only capital city to see a rise in clearance rate last week with volumes also increasing across the city.

This trend is set to continue with CoreLogic currently tracking 2,164 auctions, increasing slightly on last week’s final figures which saw 2,100 auctions held. Sydney is expected to see the most notable difference in volumes this week; increasing by 15 per cent on last week with a total of 775 homes scheduled for auction. Australia’s other largest auction market Melbourne is set to host 1,064 auctions this week, remaining somewhat consistent on the 1,033 auctions held last week at final results. In any case there are doubts about the auction stats, as we discussed in “Auction Results Under the Microscope”.

Across the smaller auction markets, Tasmania is the only other auction market to see a rise in week-on-week volumes, with Adelaide and Perth down more than 30 per cent on last week, while Brisbane and Canberra’s volumes are down to a lesser degree.

When compared to activity last year, both volumes and clearance rates were tracking considerably higher, with 2,885 auctions held on this same week one year ago when the success rate of auctions were tracking consistently above the 70 per cent mark throughout the first half of 2017; a much different trend to what we are currently seeing.

All the indicators are for more falls.

As the property market rotates, and demand slackens, property developers with a stock of newly built, or under construction dwellings – mostly high-rise apartments are trying tactics from deep discounting, cash bribes, or 100% mortgages to persuade people to buy. Remember there are around 200,000 units coming on stream over the next year or two and demand is falling. So we were interested to see (thanks to a tip off from our community) a WA initiative which was recently announced by Apartments WA – “Backed by the foundations of the BGC Group – Western Australia’s largest residential home builder and largest private company, we make your buying journey a seamless process from finding you the right apartment, assisting with obtaining finance, right through to settlement and key handover”.

I have been following the latest rounds of hearings at the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry, which is exploring lending for small businesses.

It’s been quite dramatic, with stories of business owners with impossible dreams, walking into commercial ventures which had a limited chance of success. The banks on the stand appear to have made procedural mistakes, and when things go wrong often went for the jugular to cover their losses. This included relying on guarantees even if it meant selling the guarantors property, and the case studies included sad stories of people losing their homes. This included a disabled pensioner, blind and riddled with medical problems; her daughter, a budding small business operator. Or an ambitious woman trying her hand at running a pie shop with the hope of retiring early.

But the way the story is presented is only half the story. Yes, the banks failed in their duties on occasions, but on the other hand many businesses need finance if they are to start, and banks want to lend. What is really going wrong?

My theory is there small businesses are not get access to the advice they need to make a balanced assessment as to the viability of their operation. By default, they assume if the bank provides funding then the business must be viable – but this is not necessarily so. The bank is only concerned with protecting their loan, and ensuring they can cover the risk of loss – this is not the same as considering the business in the round. We discussed this analysis in more detail in our recent release “The Problem With Small Business Lending”. And remember about 53 per cent of the nation’s 2.2 million small to medium businesses need finance to continue trading.

The Australian Financial Review reported on our recent research on the Bank of Mum and Dad funding business start-ups. More than 33,000 business owners are estimated to have seed finance – or ongoing financial support – from loans that are secured with their parents’ home, analysis of home ownership and borrowing numbers reveals. The average cash injection is about $56,000 but loans typically range from few hundred dollars to more than $1 million, the analysis reveals. But while the number of parents providing direct cash support to their siblings’ business is increasing there has been a big fall in the number willing to put their houses on the line. That’s because of increased understanding that a lender could foreclose if there a default, which means parents’ best intentions risk the threat of homelessness by prodigal sons or daughters, according to financial advisers. said the number of parents guaranteeing a loan with their homes has fallen by about 8 per cent in the past year. This is because of the greater focus on financial advice and a better understanding of the risks involved with a guarantee, plus thanks to the strong rises in property there is more equity in a property.

Next, we look at the latest from the US where the adjustments to the Dodd-Frank Act (DFA) – sound familiar?) are expected to be signed into law next week. The changes ease the capital and regulatory requirements for smaller institutions and custody banks by raising the systemic threshold to $250 billion from $50 billion for enhanced prudential standards (EPS), reduce stress testing requirements and modify applicability of proprietary trading rules (the Volcker Rule). The legislation reduces regulations for U.S. small to mid-size banks in particular, while only providing de-minimis regulatory relief to the largest U.S. banks. The change to the systemic threshold reduces the number of banks subject to heightened regulatory oversight to 12 from 38. Regulators will still have discretion to apply EPS to banks with $100 billion-$250 billion in assets. Banks above $250 billion in assets would not see much benefit from the legislation.

Fitch Ratings says stress testing has provided discipline for banks and is an important risk governance practice that is considered in its rating analysis. The elimination or meaningful reduction of stress testing would likely have negative ratings implications. And this at a time when debt is very high.

Moody’s says the return of a 3% 10-year Treasury yield is making itself known in the housing industry. Markets have already priced in a loss of housing activity to the highest mortgage yields since 2011. They conclude that just as it is overly presumptuous to predict the nearness of a 4% 10-year Treasury yield, it is premature to declare an impending top for the benchmark Treasury yield. Thus far in 2018, the 11% drop by the PHLX index of housing-sector share prices differs drastically from the accompanying 3% rise by the market value of U.S. common stock. In addition, the CDS spreads of housing-related issuers show a median increase of 78 bp for 2018-to-date, which is greater than the overall market’s increase of roughly 23 bp. Finally, 2018-to-date’s -1.97% return from high-yield bonds is worse than the -0.13% return from the U.S.’ overall high-yield bond market. Despite the lowest unemployment rate since 2000, the sum of new and existing home sales dipped by 0.7% year-over-year during January-April 2018. All this shows the impact on the housing sector as rates rise.

The highest effective 30-year mortgage yield in seven years has depressed applications for mortgage refinancings. For the week-ended May 18, the MBA’s effective 30-year mortgage yield reached 5.01% for its highest reading since the 5.04% of April 15, 2011. The effective 30-year mortgage yield’s latest fourweek average of 4.95% was up by 63 bp from the 4.32% of a year earlier. March 2018’s 7% yearly drop by the NAR’s index of home affordability showed that the growth of after tax income was not rapid enough to overcome the combination of higher home prices and costlier mortgage yields. March incurred the 17th consecutive yearly decline by the home affordability index. The moving three-month average of home affordability now trails its current cycle high of the span-ended January 2013 by 23%.

And according to the latest from The St.Louis Fed On The Economy Blog, individuals who were in financial distress five years ago were about twice as likely to be in financial distress today when compared with an average individual. They argued that financial distress is not only quite widespread but is also very persistent. They show that the share of households with past financial distress increased from approximately 6.6 percent in 1998 to 12.2 percent in 2016. They conclude that households that have encountered an episode of financial distress in the past are 1.5 times more likely to delay payment today, compared to average households.

Why is this US data relevant to us? Well first, the debt levels in the US are significantly lower than here as home prices relative to income are lower there. We have more households in financial difficulty as a result. Second, the higher rates are likely to impact local funding costs here, which will put pressure on local banks funding costs, and third, higher rates will further tighten credit availability, and as in the US, this is likely to impact the construction sector – so expect to see more unnatural acts to try to attract buyers into a falling market – to which I reply, caveat emptor – let the buyer beware!

Finally, the latest data from S&P Global Ratings using their Mortgage Performance Index (SPIN) to March 2018 shows a rise in arrears – they increased to 1.18% in March from 1.16% in February and there was a significant hike in 90+ defaults. WA and NT continue their upward trends, both above 2% and rising. Home loan delinquencies fell in New South Wales, Queensland, South Australia, and the Australian Capital Territory in March. Of note, mortgage arrears in South Australia appear to have turned a corner; the state’s March 2018 arrears of 1.35% are well down from a peak of 1.81% in January 2017. This reflects a general improvement in economic conditions in South Australia, in line with national trends. Western Australia remained the state with the nation’s highest arrears, sitting at 2.37% in March.

But S&P says say arrears more than 90 days past due made up around 60% of total arrears in March 2018, up from 34% a decade earlier. This shift partly reflects a change in the reporting of arrears for loans in hardship that came in response to regulatory guidelines. Even accounting for this, however, there has been a persistent rise in this arrears category, though the level of arrears overall remains low. And I recall Wayne Byers recent comment to the effect that at these low interest rates, defaults should be lower!

The pressure on households is set to continue. The crunch is getting nearer.

The employment and wage data from the ABS last week was not flash, with job growth momentum easing, unemployment higher and wages growth continuing at glacial speed.

So its worth asking what is really going on under the hood. To do that we have looked at ABS data over the last decade to drill into the detail. And frankly its not pretty.

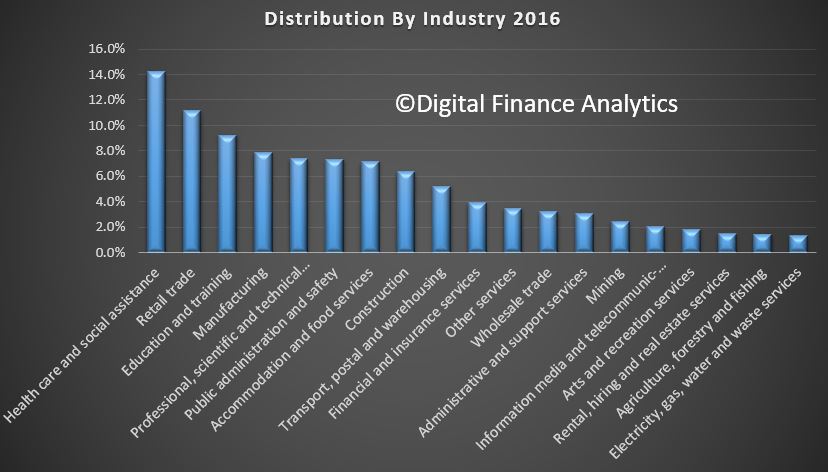

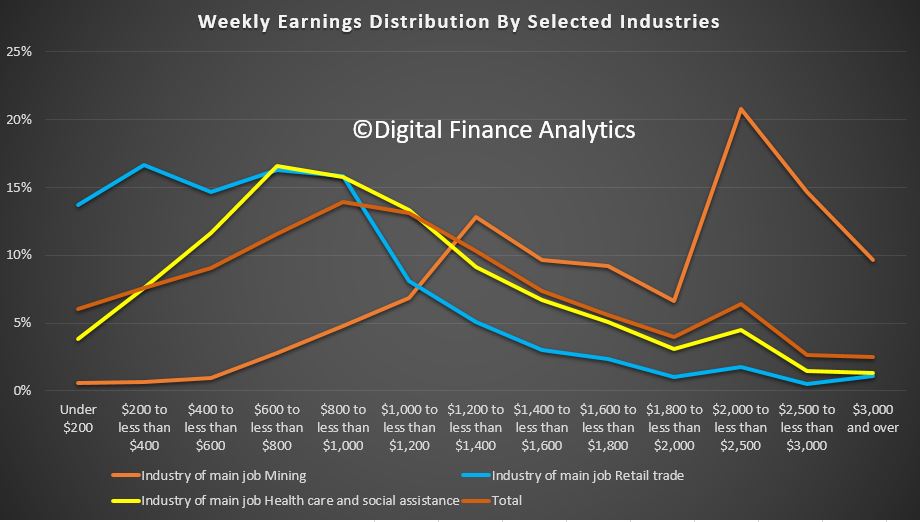

First we looked at employment across the industry sectors. Health care leads the way now at 14.2%, in terms of the number of people employed, followed by retail at 11.1%, education and training at 9.2% and manufacturing at 7.9%. For comparison purposes, about 12 % of the U.S. workforce is employed in the health care sector.

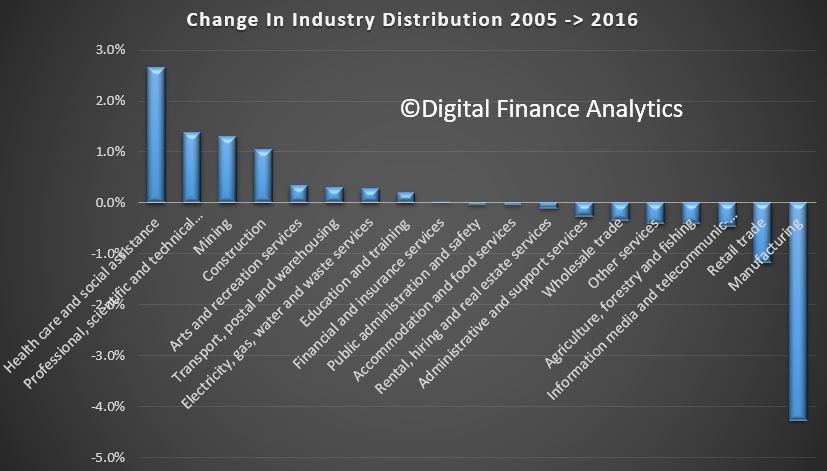

Then we compared the relative distribution by industry groups now, and back in 2005. Over that decade or so there has been a considerable shift in industry distribution.

The fastest growing sector in Health care, which have expanded relatively by 2.7%. The next largest growth sector was Professional and Technical Services at 1.4% and Mining at 1.3%. Construction grew relatively by 1.1%. At the other end of the spectrum, Manufacturing fell by a massive 4.3%, followed by Retail down 1.2% and information technology and media down 0.5%.

Or in other words, relativity more people are working in the health care sector than a decade ago. Drilling further into the data we also see a significant rise in the number of females working in this sector, as well as significant growth in part-time employment in the sector.

The final piece of analysis looks at relative weekly income across specific industry sectors. More than half of all people working in retail earn less than $600 a week. More than half of people in the healthcare sector earn less than $800 a week. Half the average of all industry sectors earns less than $1,000 a week, whilst half of those in the resource and mining sector earn more than $1,800 a week. So Retail and Health care sectors are intrinsically low paid.

Now lets put that together. All this goes some way to explain the shifts in employment and income. The health care sector has been an important generator of jobs in recent years, and health care is expected to continue to expand employment in coming years, but the jobs will continue to shift to low-paying support occupations reflecting changing demographics and greater demand. About 40 percent of the sector’s workers are not directly involved in treating a patient; instead, they work in jobs such as office or administrative work and food preparation. Others are working in health support occupations like home care and personal assistance. These jobs are paid significant less than care practitioners.

But, the health care sector is more labour intensive than other sectors, such as manufacturing, and this translates into a relatively lower share of output. So growth in health care does not guarantee broad-based prosperity because beyond the high pay of health care practitioners, the health care jobs in highest demand pay lower-than-average wages.

In fact the truth is the growth in jobs are in sectors which are service industries, and these to not really create new value, they simply circulate money in the system , perhaps from superannuation savings to pay for medical care.

Thus the growth in jobs in not assisting overall economic growth, and the lower average wages is depressing overall wage growth. Workers in the health care sector are also less likely to press hard for pay rises.

So the bottom line is we have a structural problem in the economy, where more people are doing important work helping those needing health care assistance, but the overall economic contribution impact is net negative, hence the low GDP growth and wages growth. Or in other words, more jobs are not necessarily good or well paid jobs. And that’s a structural problem, given the current demographic shifts. Welcome to the bed pan economy.

Even though house prices have risen substantially over recent decades, housing costs as a share of income have barely shifted in over 20 years. Costs relative to disposable income for housing are largely unchanged, at 17% since 1993, although there has been some increase since 2000.

There is no agreed measure for defining housing affordability, but just looking at house prices can be deceptive. Australian households are roughly equally split between purchasing, renting or owning their house outright.

There is no doubt that house prices increased substantially over recent decades. According to CoreLogic over the past 20 years the median house price in Australia increased from A$140,000 in December 1997 to A$540,000 by December 2017 – an annual increase of 7%. Relative to disposable income this represents a 68% increase over the 20-year period.

Australian households are roughly equally split between purchasing, renting or owning their house outright. Highly inflated house prices are more concerning to people wishing to move from renting to purchasing a house (mostly potential first home buyers).

Housing affordability looks very different when we look at actual housing costs relative to income, rather than just house prices. Housing costs increased substantially between 1984 and 1993.

This was a combination of weak income growth and strong increases in housing costs, particularly mortgages with interest rates increasing sharply over this period. Since peaking in 1993 costs remained relatively stable with rents increasing modestly over the past 10 years, while mortgage costs declined.

Overall, actual housing costs relative to income have remained stable since 1993 at around 16% of disposable income.

We split households into five equal groups from lowest 20% of disposable income up to highest 20%, after adjusting for type of family and household size. Clearly, low-income households spend a lot more on housing relative to their income than higher-income households. The share of housing costs for the lowest income quintile has increased in recent years but is not substantially different from longer term averages.

All other income groups have increased their share of spending relative to income since 1984. Since 1993 the changes have been mixed with the lowest income households and highest income households both spending less as a share of income, while the middle income categories have increased their spending, albeit modestly.

Housing was much more affordable in 1984 with average housing costs at just 11.3% of disposable income.

A number of important changes have occurred over the past 25 years. Interest rates are much lower, living standards have increased substantially for low, middle and high income families and savings rates have also increased – implying that housing costs are increasingly a larger share of expenditure.

Another common measure of housing affordability is housing stress. We use the “30/40” stress rule – a household paying more than 30% of their disposable income on housing costs and also in the bottom 40% of the income distribution.

Using this housing stress measure, we see a significant increase in renter stress, firstly between 1984 and 1993 and then from 2007. Mortgage stress is largely unchanged since 1988 following an increase between 1984 and 1988.

Housing stress rates are similar for major states. The highest rate is in Queensland with 13.5% of households in stress whereas the combined ACT and NT region has the lowest stress rate at 8.1%, thanks to relatively high incomes. The NSW rate is lower than both Victoria and Queensland.

Home ownership rates in Australia have slowly declined since 1984 from around 72% to around 68% by 2015-16. Ownership rates of households headed by people aged under 35 dropped from 50% in the 1980s to around 35% in 2015-16. Households headed by people aged 35 to 49 have experienced a similar percentage point decline but from a higher base.

The downward trend in ownership rates for younger households has been ongoing since 1988. Surprisingly, the house price boom between 1999 and 2005 in Australia does not appear to have made a significant difference to pre-existing trends.

However, home ownership trends are complex, and are likely driven by a range of factors such as interest rates, higher rents in the 1980s, broader societal changes such as people marrying and having children later in life and a higher divorce rates. Another possibility is a shift away from home ownership, with younger people preferring the flexibility that renting offers.

Overall, housing costs in Australia have been relatively stable as a share of disposable income since the early 1990s. This average does mask problems for low-income renters who are paying an increasing share of their income on housing costs, and rent stress levels have also increased over the long term.

Changed economic circumstances provide risks for housing affordability. Were interest rates or unemployment to increase sharply there would be risks to households and flow on effects to the broader economy.

House prices have indeed increased sharply since the late 1990s, well above incomes or inflation. This poses a problem for those wishing to move from the rental market to owning a home as higher house prices imply larger deposits.

While elevated house prices are a concern, the more pressing social problem for Australia remains the lack of affordable rental housing for lower-income families that is close to jobs and services in our capital cities. This has been an ongoing problem in Australia for a number of decades. An ageing population with potentially lower home ownership rates will add to this problem in future years

Author: Ben Phillips, Associate Professor, Centre for Social Research and Methods, Australian National University

Macquarie Group is consolidating its private bank and private wealth businesses to concentrate its growth strategy on high net-worth (HNW) clients, a move it expects to affect advisers.

This underscore the transition in wealth management, as players morph their businesses in the light of the “best interest” requirement, and the fact the providing such advice is costly, and cannot be done en masse. So the focus will be on HNW investors.

HNW clients are already the exclusive focus of Macquarie’s private bank. They are also a substantial proportion of its private wealth business.

The announcement was made by Macquarie’s Banking and Financial Services group (BFS), which also looks after retail banking activities. The gearing towards HNW investors in the bank’s private wealth and banking business will have no impact on BFS’s retail banking strategy which includes home lending, deposits and credit card solutions for consumer clients.

Macquarie head of wealth management Bill Marynissen said concentrating on one client segment will enable it to deliver better on a comprehensive and tailored wealth and banking offering that can take clients from wealth accumulation stages through to retirement.

“Focusing on attracting high net-worth clients is a logical evolution of our private client business and we believe it is a space in which we can be a market leader,” Marynissen said.

“We have carefully assessed growth opportunities in the high net-worth segment against the strong fundamentals of our business. These include a deep understanding of the high net-worth segment, our wealth and banking expertise and suite of solutions, and the capacity to build on our existing digital capabilities.”

Australia has more than 1.2 million adults with wealth of $1.3 million or more, ranking it among the top 10 countries globally for HNW individuals. The segment swelled 7.4% or by 80,000 adults since 2011.

Many advisers will be impacted by the decision to concentrate the focus of the combined private bank and private wealth businesses to HNW clients, according to Macquarie’s wealth management division.

“Macquarie is supporting these advisers in a number of ways, including by facilitating discussions with other firms and assisting with their transition,” the bank said.

Property-related sentiment is hitting hard, especially in New South Wales and Victoria where price falls are most evident. In Western Australia and South Australia, the index hardly moved compared with last month, and in Queensland it slid just a tad.

Property-related sentiment is hitting hard, especially in New South Wales and Victoria where price falls are most evident. In Western Australia and South Australia, the index hardly moved compared with last month, and in Queensland it slid just a tad. Looking across our property segments, those not in the property game, and renting or living continue to languish. But we also are tracking falls among property investors, reflecting difficulty in obtain finance, higher interest rates, and falling property prices, and now, also those who are owner occupiers. Both of these property owning segments slid again, mirroring falls in property prices, and the slowing auction clearance rates. That said, those owning property are still relatively more confident about their finances, compared with renters, so the property effect continues.

Looking across our property segments, those not in the property game, and renting or living continue to languish. But we also are tracking falls among property investors, reflecting difficulty in obtain finance, higher interest rates, and falling property prices, and now, also those who are owner occupiers. Both of these property owning segments slid again, mirroring falls in property prices, and the slowing auction clearance rates. That said, those owning property are still relatively more confident about their finances, compared with renters, so the property effect continues. Across the age bands, those aged 40-50 were a little more confident, reflecting recent stock market progress, especially among those without mortgages (yes, some have paid down their loans completely), while levels of employment remain pretty good. But for younger households the budget pressure on them remains severe, especially those paying rent, or mortgages. Those entering the retirement phase, 60+ continue to wrestle with outstanding mortgages (many hold these loans into retirement now) and also lower returns from deposits.

Across the age bands, those aged 40-50 were a little more confident, reflecting recent stock market progress, especially among those without mortgages (yes, some have paid down their loans completely), while levels of employment remain pretty good. But for younger households the budget pressure on them remains severe, especially those paying rent, or mortgages. Those entering the retirement phase, 60+ continue to wrestle with outstanding mortgages (many hold these loans into retirement now) and also lower returns from deposits. We can examine the moving parts within the index, to get a sense of what is driving the results. First we look at job security. Something appears to be happening here, as the proportion feeling less secure is rising, up 1.7% compared with last month. There was also a fall by 2.4% of those reporting no change in sentiment compared with last month. Below the hood, it appears that more are involved in multiple part-time jobs, and becoming swept up in the gig economy. Zero-hours contracts appear to be on the rise in some industry sectors. So, while the number of jobs created may be north of one million as the Government often says, we question the quality of these jobs, and their security. Our index reveals another perspective.

We can examine the moving parts within the index, to get a sense of what is driving the results. First we look at job security. Something appears to be happening here, as the proportion feeling less secure is rising, up 1.7% compared with last month. There was also a fall by 2.4% of those reporting no change in sentiment compared with last month. Below the hood, it appears that more are involved in multiple part-time jobs, and becoming swept up in the gig economy. Zero-hours contracts appear to be on the rise in some industry sectors. So, while the number of jobs created may be north of one million as the Government often says, we question the quality of these jobs, and their security. Our index reveals another perspective. This may also help to explain the fall in real income (after inflation) many households are experiencing. 54% of households said their incomes had fallen in the past year, and only a small fraction report a rise. 43% say there has been no change since June 2016. There are a number of drivers here, but the main one is simply no, or low pay rises, adjustments to overtime rates, and lower returns from bank deposits. Many older households rely on income from savings and this in under pressure with the current low interest rates, and banks trimming their deposit rates too boot.

This may also help to explain the fall in real income (after inflation) many households are experiencing. 54% of households said their incomes had fallen in the past year, and only a small fraction report a rise. 43% say there has been no change since June 2016. There are a number of drivers here, but the main one is simply no, or low pay rises, adjustments to overtime rates, and lower returns from bank deposits. Many older households rely on income from savings and this in under pressure with the current low interest rates, and banks trimming their deposit rates too boot. On the other hand, the costs of living continue higher. Nearly 81% of households say their costs are higher than a year ago, up 2% on last month. The litany of rising categories includes electricity, fuel, health care costs, school fees and child care costs. But households are also reporting higher costs at the supermarket, and a tendency to eat in, rather than out, to keep costs under control. More also turning to credit cards, or pulling equity from their properties to keep the household afloat.

On the other hand, the costs of living continue higher. Nearly 81% of households say their costs are higher than a year ago, up 2% on last month. The litany of rising categories includes electricity, fuel, health care costs, school fees and child care costs. But households are also reporting higher costs at the supermarket, and a tendency to eat in, rather than out, to keep costs under control. More also turning to credit cards, or pulling equity from their properties to keep the household afloat. On the savings front, more are concerned about the amount they have for emergencies. Just 2% are more comfortable compared with last month, while 46% are less comfortable, up 1% on last month. The interest rates offered on bank deposits continue to fall, and this is impacting many who rely on a regular savings generated income. Those who are in the stock market are a little more positive, but the recent crash in bank shares following the revelations from the Royal Commission, and other adverse events, translates to lower confidence. Its worth remembering that nearly half of dividends paid last year came from the financial sector.

On the savings front, more are concerned about the amount they have for emergencies. Just 2% are more comfortable compared with last month, while 46% are less comfortable, up 1% on last month. The interest rates offered on bank deposits continue to fall, and this is impacting many who rely on a regular savings generated income. Those who are in the stock market are a little more positive, but the recent crash in bank shares following the revelations from the Royal Commission, and other adverse events, translates to lower confidence. Its worth remembering that nearly half of dividends paid last year came from the financial sector. Households continue to feel the pressure from debt. 45% of households are less comfortable with the debt they owe, up 0.6% from last month. Around 49% remain the same as a year ago, and 3% are more comfortable. The drivers relate to larger mortgages, and higher real mortgage rates (despite some refinancing to gain a lower rate); the inability to get mortgage funding due to tighter lending standards, and a rise in equity withdrawals and some areas of personal credit. While personal credit balances overall are falling, personal debt is concentrated in households with larger mortgages and here it is rising. Payday lending is also on the rise. In addition, households are concerned about the prospect of higher interest rates ahead. Many are stuck in the debt machine.

Households continue to feel the pressure from debt. 45% of households are less comfortable with the debt they owe, up 0.6% from last month. Around 49% remain the same as a year ago, and 3% are more comfortable. The drivers relate to larger mortgages, and higher real mortgage rates (despite some refinancing to gain a lower rate); the inability to get mortgage funding due to tighter lending standards, and a rise in equity withdrawals and some areas of personal credit. While personal credit balances overall are falling, personal debt is concentrated in households with larger mortgages and here it is rising. Payday lending is also on the rise. In addition, households are concerned about the prospect of higher interest rates ahead. Many are stuck in the debt machine. Finally, and putting the data together, we look at net worth – defined as assets less loans outstanding. 47% of households say their net worth has improved over the past year, down 4% on last month, as property values slide and household debt rises. 22% reported their net worth was lower, up 2% compared with last month and 28% said there was no change in the past year.

Finally, and putting the data together, we look at net worth – defined as assets less loans outstanding. 47% of households say their net worth has improved over the past year, down 4% on last month, as property values slide and household debt rises. 22% reported their net worth was lower, up 2% compared with last month and 28% said there was no change in the past year. So, the pressures on household finances are clearly visible in these results, and bearing in mind the expected continued fall in home prices, and the prospect of interest rate hike, plus flat incomes, we expect the trend to continue to weaken in the months ahead.

So, the pressures on household finances are clearly visible in these results, and bearing in mind the expected continued fall in home prices, and the prospect of interest rate hike, plus flat incomes, we expect the trend to continue to weaken in the months ahead.