The monthly ABS housing finance data was released today for August. In a way, nothing new here, as first time buyers continue to be squeezed out, and investors dominate. The trend estimate for the total value of dwelling finance commitments excluding alterations and additions rose 0.3%. Investment housing commitments rose 0.9% while owner occupied housing commitments fell 0.1%. In seasonally adjusted terms, the total value of dwelling finance commitments excluding alterations and additions fell 1.2%.

In trend terms, the number of commitments for owner occupied housing finance fell 0.2% in August 2014. In trend terms, the number of commitments for the purchase of established dwellings fell 0.3% and the number of commitments for the construction of dwellings fell 0.2%, while the number of commitments for the purchase of new dwellings rose 1.7%. In original terms, the number of first home buyer commitments as a percentage of total owner occupied housing finance commitments fell to 11.8% in August 2014 from 12.2% in July 2014.

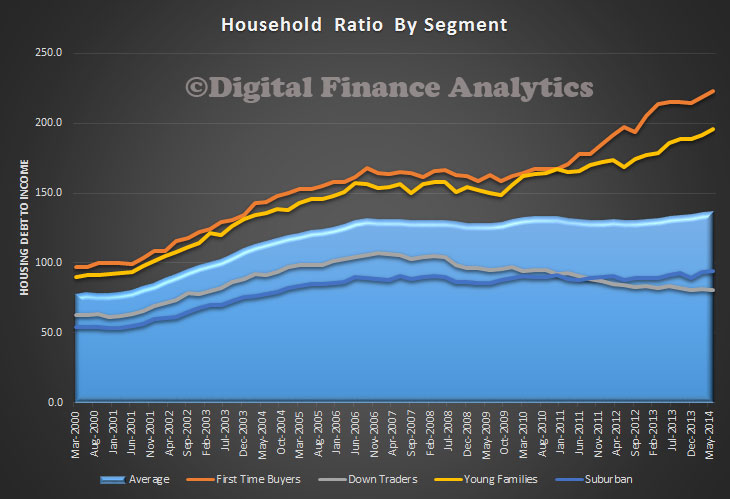

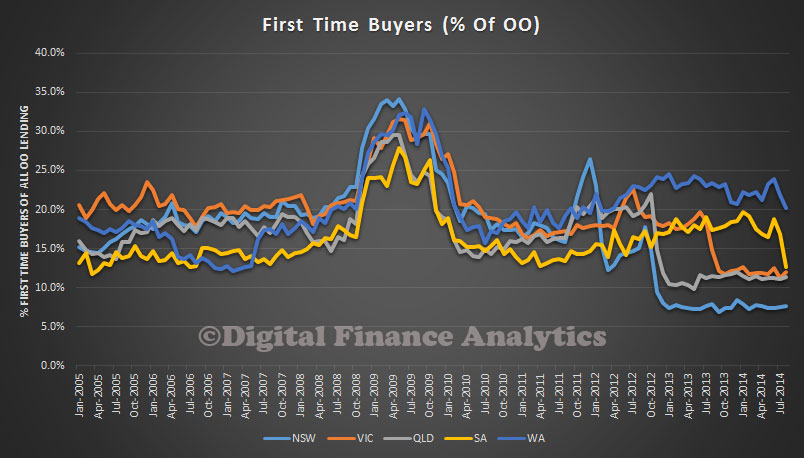

Looking at the first time buyer data, we see they are lowest in NSW and VIC (where the investment market is hottest), but we also see down trends in WA and SA. This confirms our surveys that first time buyers cannot compete.

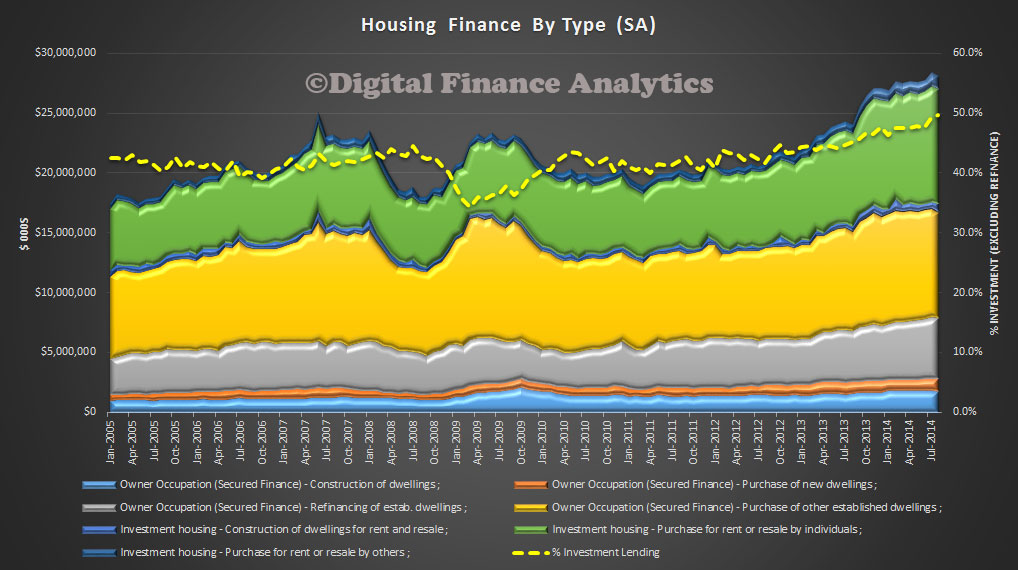

Looking at investment lending we see that nearly 50% of all lending in August (if you exclude refinance) was for investment purposes.

Looking at investment lending we see that nearly 50% of all lending in August (if you exclude refinance) was for investment purposes.