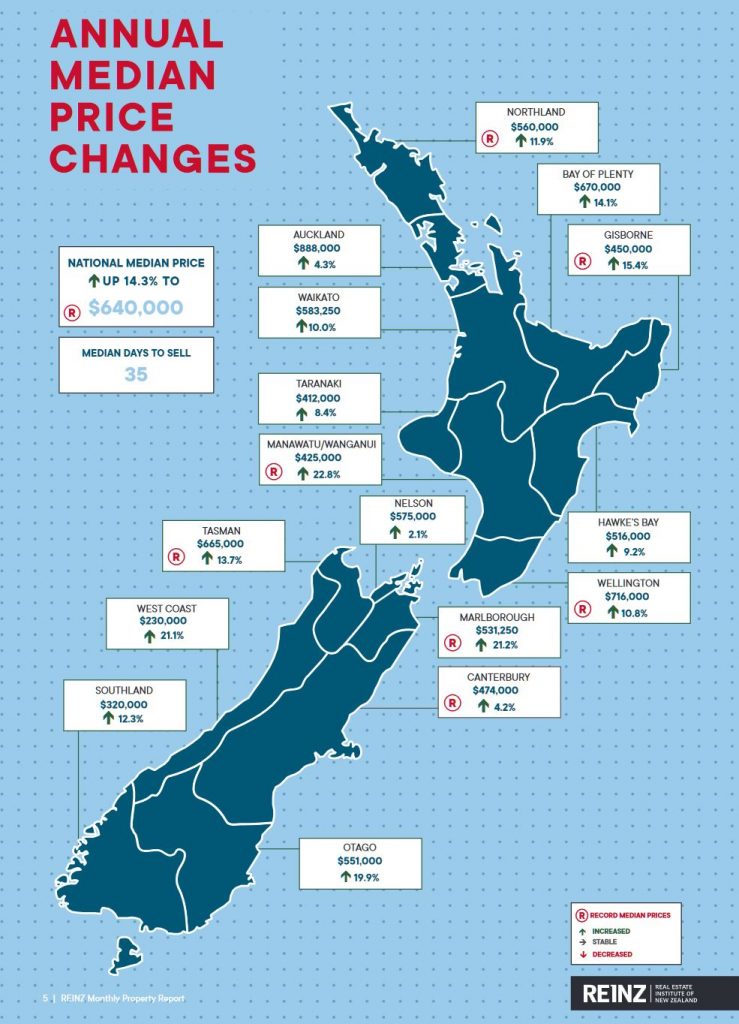

Median house prices across New Zealand increased by 14.3% in February to a new record median price of $640,000, up from $560,000 in February 2019. This was the largest percentage increase in 53 months according to the latest data from the Real Estate Institute of New Zealand (REINZ).

The number of properties sold in February across New Zealand increased by 9.2% from the same time last year (from 6,132 to 6,694) making it the highest number of properties sold in the month of February in 4 years.

For New Zealand excluding Auckland, the

number of properties sold decreased by a marginal -0.3% when compared to the

same time last year (from 4,742 to 4,726) – 16 fewer properties.

In Auckland, the number of properties sold in February increased by 41.6% year-on-year (from 1,390 to 1,968) – the highest number of residential properties sold in the month of February in 5 years.

The REINZ House Price Index for New

Zealand, which measures the changing value of property in the market, increased

8.7% year-on-year to 3,013 – a new record high.

The HPI for New Zealand excluding Auckland

increased 10.2% from February 2019 to 2,995 another new record high.

The Auckland HPI increased by 6.9%

year-on-year to 3,035 – the highest annual percentage increase in 35 months and

the first time the Auckland region crossed the 3,000 mark.

In February the median number of days to sell a property nationally decreased by 12 days from 47 to 35 when compared to February 2019 – the lowest days to sell for the month of February in 13 years.

The total number of properties available for sale nationally decreased by -22.3% in February to 20,875 down from 26,850 in February 2019 – a decrease of 5,975 properties compared to 12 months ago and the lowest level of inventory for the month of February ever. However, this was an uplift on January’s figure of 19,488.

In order to support the continuous functioning of financial markets through the provision of liquidity, the Bank of Canada announced two measures on Thursday.

First, acting as fiscal agent, the Bank

will broaden the scope of the current Government of Canada bond buyback

program. This is intended to add market liquidity and support price

discovery. Until further notice, buybacks will extend across all

benchmark maturity sectors and will be conducted at least weekly.

Regular weekly operations will be conducted on a switch basis. Cash

buybacks will be conducted following nominal bond auctions.

The first operation will be a $500 million

switch operation in the 30-year sector held on Monday March 16.

Additional program details are forthcoming, including the timing of the

first operation.

Second, to proactively support interbank

funding, the Bank of Canada will temporarily add new Term Repo

operations with terms of 6 and 12 months. These operations will occur

bi-weekly starting with the first operation on Tuesday, 17 March 2020.

Details of the first Term Repo operation are as follows:

Amount

Auction Date

Settlement Date

Term (Days)

Maturity Date

$4 billion

17 March 2020

19 March 2020

168

3 September 2020

$3 billion

17 March 2020

19 March 2020

350

4 March 2021

Regular 1-month and 3-month Term Repo

operations will remain in effect but could change with regards to size,

frequency and term depending on prevailing market conditions.

Term Repo terms and conditions remain in effect. The results of the 6- and 12-month operations will be announced on the Bank’s web site by Market Notice.

The Bank of Canada continues to closely

monitor global market developments and remains committed to providing

liquidity as required to support the functioning of the Canadian

financial system.

Westpac confirmed it has been hit with another class action relating to the AUSTRAC scandal. Via Financial Standard.

The

class action, brought by Johnson Winter & Slattery, has been filed

on behalf of certain shareholders who acquired interest in Westpac

securities or equity swap confirmations between 2013 and 2019.

“The

claim relates to market disclosure issues connected to Westpac’s

monitoring of financial crime over the relevant period and matter which

are the subject of the AUSTRAC proceedings,” Westpac told the ASX.

“The claim does not identify the amount of any damages sought.”

Westpac said it will be defending the claim, as it has said for the other class actions filed against it.

Prior to this proceeding being filed, Westpac said it expects around $80 million in additional expenses in FY20 as part of its response plan to the AUSTRAC scandal.

The bank is facing 23 million alleged breaches of anti-money laundering and counter-terrorism laws brought on by AUSTRAC.

The

regulator alleges, amongst other things, Westpac failed to

appropriately assess the online money laundering and terrorism financing

risks associated with the movement of money into and out of Australia

through correspondent banking relationships.

The bank is also facing class actions from US-based law firm Rosen Law on behalf of purchasers of Westpac shares between November 2015 and November 2019, as well as another Australia-based class action lodged by Phi Finney McDonald.

Property insider Edwin Almeida and I discuss the thorny issue of running open houses in the current environment. What precautions should we take? And how will it impact property listings?

The current structure of finance and its interlock with society based on debt creation and financialisation is not working effectively – as the current market gyrations indicate, and as we face into an extensional crisis. So far the solutions are to grow debt more, cut rates and let Central Banks build their balance sheets (and buy assets from Government bonds and beyond). But there comes a point where we need to think more deeply about what is happening and what needs to change. So in coming days, I will be featuring some of the different alternative approaches.

One approach which I have been examining is called Economic Democracy. There was an excellent post from The Conversation a few months back, which is now more relevant than ever. Andrew Cumbers, Professor of Regional Political Economy, University of Glasgow writes:

We need to fundamentally fix the way we run our economies and hand economic power back to the people. I believe this can – and must – be done through a concept called economic democracy. As I outline in a forthcoming book, The Case for Economic Democracy, it is key to transitioning toward a more socially just and ecologically sustainable system.

In the past, people have tended to think

about the idea of economic democracy in quite a restricted sense. They

have focused on developing the collective voice of employees through

trade unions and collective bargaining. Or concentrated on cooperative

or employee ownership policies. While these remain important, my colleagues and I argue that an expanded definition is needed, one that forces us to think afresh about how we might radically democratise the economy as a whole.

In this respect, I argue that there are

three critical interlocking pillars to economic democracy: individual

economic rights, diverse forms of democratic collective ownership of

companies, and the need for greater public participation in economic

decision-making.

There is plenty of mainstream media commentary about a global crisis of liberal democracy, the deepening divide between elites and citizens, and the opportunism of faux “outsiders” such as Trump and Johnson (themselves from wealthy elites). But there is seldom much discussion of the underlying economic fundamentals.

A common feature of disaffected voters is

anger toward the excesses of economic globalisation, which was pursued

by centre-left and centre-right politicians of the 1990s. The theory ran

that reducing the restrictions on business and finance operating across

borders – and, in the EU’s case, a single market with freedom of

movement for both business and workers – would be good for us all.

But that has not been the experience for

many. The collapse of well paid and unionised industrial jobs in Europe

and North America, and the shift of work to China and other developing

countries, has fuelled a reaction against globalisation.

Or at least against globalisation in its neoliberal, free trade

variant. Economic nationalists such as Trump and Victor Orban in

Hungary, have capitalised on this reaction.

This has fuelled a sense of alienation and

loss of control among ordinary people. The threat posed to work by

further automation is likely to further depress everyday life, adding grist to the mill of populists.

Brexit and the broader rise of right-wing

populism show the limitations of democracy under the existing

capitalist system. Politically, voters are asked every few years to

choose from a limited range of options and then leave everything else in

the hands of their political representatives.

In economic terms, people have a

diminishing sense of control over the key activities and events that

shape their lives. The proliferation of zero hours contracts and casual

work, and the decline of stable permanent employment have disconnected many from secure jobs and incomes.

In the workplace itself, employees have little say over their companies’ decision-making process. Trade unions are in retreat and what limited collective bargaining we have is under attack in most large developed economies.

There is still a tradition of cooperatives and employee-owned

enterprises nominally committed to democratic practice (though often

sadly lacking in reality). But even these are marginal to the dominant

corporate and privatised economy.

In short, ordinary citizens have very

little say in how the capitalist economy works. This applies at the

macro level – how the economy as a whole functions, who controls it and

makes the key decisions on investment, what to produce, how and what to

tax, what to regulate and what is produced. And it applies at the

individual level of accessing economic resources to lead decent lives,

in a way that is fair to others and sustainable in caring for the planet

and future generations. Both are critical matters of concern.

This is the backdrop for understanding the

growing popularity of alternative economic policies that seek to give

workers and citizens real power and control over their livelihoods. In

the UK, the Labour party’s policies to reverse privatisation and create

new more democratic forms of public ownership are massively popular. A recent opinion poll

by the right-wing Legatum Institute think tank found 83% of respondents

favoured nationalisation of water companies, 77% for electricity and

gas, and 76% for train services.

Even in the US, where there is traditional

hostility to ideas seen as “socialist”, public opinion appears to be

shifting. A poll carried out by Washington-based think tank the Democracy Collaborative

discovered that 55% of people supported the idea of employee ownership

funds, while only 20% were opposed. The idea that workers should have

the first right to buy their companies when they comes up for sale had

69% support.

But what should this look like in

practice? Unlike older visions of economic democracy that started with

class or the collective, my starting point is the individual. We should

all have the right to participate in a democratic society on equal

terms.

Nobel Prize winning economist Amartya Sen has emphasised

that individual economic freedom is only possible where citizens have

the resources, competence and capability to flourish. Rather than the

restricted choice of whatever the market is offering, it is important to

create a sense of economic citizenship, one that provides all people

with the resources and capability to make meaningful life choices.

An important mechanism for doing this is

to provide everyone with a universal basic income that would cover their

essential living requirements: food, shelter and clothing. This idea

has provoked plenty of controversy with enthusiasts and detractors on

the left and right.

Right wing proponents, such as Milton Friedman, support it because they think it could allow governments to cut welfare services elsewhere. Others reject it for creating indolence and dependency.

If everyone was given an income, why would anybody turn up for work?

Many trade unionists and social democrats don’t like the idea because

they think it would shift focus away from workplace rights and public services, allowing further attacks from the right.

The more substantive research suggests

little evidence that labour market participation falls when UBI is

introduced, although some people take the opportunity to reduce hours

for positive reasons such as spending more time with family and

volunteering. Meanwhile, the biggest positives tend to be improvements

in the physical and mental health of participants and the greater

likelihood of young people staying on for longer in education.

In response to fears on the left, UBI

should not be viewed as a standalone policy but rather part of a

progressive agenda of fairer taxation, living wage rates, reducing working hours and strengthening employment rights. Framed this way, the idea has much appeal in providing people with real choices.

It would also change the balance of power

in the labour market. Rather than coercing people into poorly paid and

inhumane forms of work, employers would also be forced to make work more

attractive and rewarding.

Democratic collective ownership

Under a proper economic democracy, the

individual should also have ownership rights and control over the work

they do and how it is used. Under capitalism, once we enter employment,

we effectively sell the right to own and control our labour to

employers. The workplace becomes a managerial dictatorship.

Many thinkers since the 19th century, from Karl Marxto liberals

such as John Stuart Mill, have recognised that this is unjust. People

have a basic right to control their labour and any benefits that accrue

from it, whether that’s in the form of income or profit.

Work is a social activity, not an

individual one. It involves interaction and cooperation with others.

Recognising this, my second pillar of economic democracy is collective,

diverse and democratic forms of ownership. This is very different to the

existing dominance of shareholder capitalism, where companies are privately controlled and largely subject to the whims of the market.

Similarly, while plans to take privatised

utilities back into public ownership are important, these entities need

to be run along much more democratic lines than in the past. Many older

and existing forms of public ownership have been too removed from public control,

run by elite officials or boards composed of private sector interests

rather than giving the public themselves a role in decision-making. The

BBC is a good example of this, set up as a corporation on behalf of the

pubic, who in reality have little say over how it is run.

As well as providing democratic

participation for workers, it’s also important to include users of

public services in the way they are run. There are different ways of

achieving this and plenty of good examples from around the world of how happens in practice.

For example, when the French city of

Montpelier de-privatised its water system, taking it back into public

ownership in 2016, it set up a water observatory, a citizens forum with

the power to scrutinise and hold the new public enterprise to account. It also drew 30% of its board from civil society organisations.

Another interesting example of a more

hybrid form of democratic public ownership comes from Costa Rica. Here,

the country’s third largest bank, the Banco Popular is a public enterprise that is legally owned by the country’s workers, with 1.2 million members (20% of the total population).

To own a share, a worker needs to have had

a savings account with the bank for one year. The key governing body of

the bank is a democratic assembly of 290 elected representatives, which

determines the bank’s strategic direction. A quarter of the bank’s

revenues fund social projects and it has played an increasingly

important role in the country’s rapid expansion of renewable energy,

including financing the first Latin American energy supplier to become

carbon neutral.

Beyond public services, other forms of

democratic collective ownership (such as employee ownership, cooperative

or mutual societies) could play a greater role across the economy. The

Mondragon network of worker cooperatives in Spain’s Basque country is

inspirational for many because of its intense democratic ethos across

its workforce of more than 70,000. Workers in every cooperative have an

annual general assembly. On the basis of one member one vote, the

assembly approves the business plan and budget, and elects a governing

council (the board of directors).

Key ingredients in Mondragon’s continued success

include having its own bank, lots of cooperation across its network,

collective knowledge sharing and an emphasis upon lifelong learning

alongside job security. These are measures of public effectiveness and

social value that contrast strongly with the short-term, profit

maximisation mantra of privately-owned firms.

Part of the wider appeal of Mondragon is

the sense that its model can be transplanted elsewhere to create whole

ecosystems of worker-owned enterprises at the local and regional level.

These could stimulate interesting new initiatives that build the wealth

of communities in post-industrial places, from Cleveland in the US to

Preston in the UK.

Public participation and deliberation

Beyond extending economic rights to the

individual and at the business level, my third pillar requires greater

public participation and engagement at the macro level of the economy as

a whole. This would involve the public becoming more involved in

decisions about spending in the wider economy.

One well-researched phenomenon, for example, is the idea of participatory budgeting.

This is where governments devote a proportion of their budget directly

to citizens groups who are brought together in a series of deliberative

exercises to decide on investment priorities.

So far, this has only occurred at the

local level. But the results are overwhelmingly positive, both in

engaging citizens and in making more socially progressive investment

choices. Brazil, beginning with the southern city of Porto Alegre in the

late 1980s, has been a pioneer of the concept.

Regional assemblies of residents were set

up across the city to vote on priorities, which were then fed into

city-level planning. Participatory budgeting then spread throughout

Brazil with over 120 cities adopting it in the 1990s and 2000s. The idea

has also spread widely across the world. There are currently over 250 schemes in the US, with Chicago and New York being important centres.

Brazil led the way with participatory budgeting.

Shutterstock

Advocates of participatory budgets point

to how they increase the involvement of women and lower income groups in

democratic processes. When sustained over a longer time period, they

reduce corruption, improve transparency and public engagement, and

create better institutions that involve citizens more regularly into

governance processes. The evidence also suggests

that they lead to greater spending on health and education in poorer

areas of cities, significantly reduce infant mortality and are linked to

the growth of civil society organisations.

Struggling for economic democracy

There remain powerful vested interests

that will mobilise against more radical initiatives to democratise the

economy. Commercial interests have powerful resources to protect the

status quo. They can fashion superficial media narratives, that have

been notably successful in protecting fossil fuels and undermining efforts to tackle climate change.

But, if we are to confront the major

economic, social and ecological crises that face us, these interests

must be overcome to create a very different kind of global economy. This

needs democratic mechanisms that rebalance economic resources and

decision-making away from the rich and powerful toward the pursuit of

the common good, while safeguarding the planet for future generations.

As the examples here demonstrate, these ideas are not unworkable utopias

but existing forms of democratic economy.

The Dow plunged to its biggest-one day

percentage loss since October 1987 as fears the spread of the novel

coronavirus will pick up pace and usher in a global recession

overshadowed the Federal Reserve’s bold new stimulus measures to calm

funding markets.

The Dow Jones Industrial Average

fell nearly 10%, or 2,352 points, it worst one-day percentage drop

since Black Monday when it lost 22.6%. It was the fourth-largest

percentage drop for the blue chip index in history, rivaling those seen

in 1929.

The rout on Wall Street for the second-straight day comes as investors upped their bearish bets on stocks despite the Federal Reserve unveiling $1.5 trillion in fresh liquidity to combat “temporary disruptions” in funding markets.

The short-term pause in selling following the Fed announcement proved short-lived as investor sentiment on stocks continued to be swayed by the latest updates on the spread of Covid-19, which has killed nearly 5,000 people, with infections topping 133,000 worldwide.

In the U.S., where infections are feared

to increase in the coming weeks, state-wide bans on large gatherings to

limit the virus impact continued, with New York announcing announce a

ban on gatherings of 500 or more people.

The Fed’s announcement was unprecedented:

The Open Market Trading Desk (the

Desk) at the Federal Reserve Bank of New York has released a new

monthly schedule of Treasury securities operations and has updated the

current monthly schedule of repurchase agreement (repo) operations.

Pursuant to instruction from the Chair in consultation with the FOMC,

adjustments have been made to these schedules to address temporary

disruptions in Treasury financing markets. The Treasury securities

operation schedule includes a change in the maturity composition of

purchases to support functioning in the market for U.S. Treasury

securities. Term repo operations in large size have been added to

enhance functioning of secured U.S. dollar funding markets.

As a part of its $60 billion reserve

management purchases for the monthly period beginning March 13, 2020

and continuing through April 13, 2020, the Desk will conduct purchases

across a range of maturities to roughly match the maturity composition

of Treasury securities outstanding. Specifically, the Desk plans to

distribute reserve management purchases across eleven sectors,

including nominal coupons, bills, Treasury Inflation-Protected

Securities, and Floating Rate Notes. The distribution of purchases

across sectors will be the same distribution as the Desk uses to

reinvest principal payments from the Federal Reserve’s holdings of

agency debt and agency MBS in Treasury securities. The first such

purchases will begin tomorrow, March 13, 2020.

Today, March 12, 2020, the Desk will

offer $500 billion in a three-month repo operation at 1:30 pm ET that

will settle on March 13, 2020. Tomorrow, the Desk will further offer

$500 billion in a three-month repo operation and $500 billion in a

one-month repo operation for same day settlement. Three-month and

one-month repo operations for $500 billion will be offered on a weekly

basis for the remainder of the monthly schedule. The Desk will

continue to offer at least $175 billion in daily overnight repo

operations and at least $45 billion in two-week term repo operations

twice per week over this period.

These changes are being made to address highly unusual disruptions in Treasury financing markets associated with the coronavirus outbreak. Reserve management purchases into the second quarter will continue to be conducted with this maturity allocation. The terms of operations will be adjusted as needed to foster smooth Treasury market functioning and efficient and effective policy implementation.

Detailed information on the schedule of Treasury purchases is provided on the Treasury Securities Operational Details page.

Detailed information on the schedule and parameters of term and

overnight repo operations are provided on the Repurchase Agreement

Operational Details page.

Given the current market gyrations, we are going to examine the latest critical data each day, because a week is a long time in politics but a lifetime on the markets at the moment…

Several UK mortgage lenders have announced loan repayment holidays to support homeowners affected by coronavirus. Via Homes and Property

Royal Bank of Scotland said it will defer mortgage payments for up to three months to affected borrowers.

The state-backed bank is 62 per cent owned

by the taxpayer and has announced the emergency measures to support

customers who might lose their jobs or see their income decline if they

cannot work due to illness or lockdown.

A spokeswoman for RBS said: “We are monitoring the potential impact of coronavirus

across all our customers to ensure we can support them appropriately

through any period of disruption. We have a strong track record in

working with our customers who are affected by disruption outside of

their control.”

TSB also said borrowers could have mortgage repayment holidays for up to two months.

UK Finance said all its members were

putting measures in place to support borrowers affected by the virus.

Stephen Jones, the industry body’s chief executive said: “All providers

are ready and able to offer support to their customers who are impacted

directly or indirectly by COVID-19, which could include offering or

increasing an overdraft or allowing repayment relief for loan or

mortgage repayments: asking for help early is key.

“We would encourage customers who think

they may be affected to contact their provider as soon as possible to

discuss the support available to them.”

Miles Robinson, head of mortgages

at online broker Trussle, said: “Self-employed and gig economy workers

might be concerned about their income becoming more unstable, at least

temporarily, which may affect their ability to pay the bills at the end

of the month.

“The good news is that mortgage lenders

don’t live under a rock. They know that coronavirus is causing severe

uncertainty. They’re also aware that as a result of the outbreak, some

customers might be unable to make their monthly mortgage repayments.”

UK lenders adopted similar measures in the 2009 recession.

President Trump is suspending flights from Europe for the next 30 days because of the virus, a decision likely to ripple throughout the global economy. The president said such travel restrictions would apply to “trade and cargo,” but the White House later clarified that goods from Europe would still be able to enter the country. Via The Hill.

Trump said he will

“soon be taking emergency action [to] provide financial relief …

targeted for workers who are ill, quarantined, or caring for others due

to coronavirus,” without specifying how he would do so.

The

president also said he would instruct the Small Business Administration

to extend low-interest loans to businesses in coronavirus hot spots to

overcome steep declines in activity, and would ask Congress to approve a

temporary payroll tax suspension that has fallen flat among lawmakers.

Trump

also did not address a several issues that Democrats consider essential

to any coronavirus aid plan, including provisions to expand

unemployment insurance and ensure that low-income children don’t miss

meals due to school closures. The House is set to vote on a bill with

those measures and others, including federal paid sick leave, on

Thursday in a bid to force the Senate to pass the legislation quickly.

More than 1,000 cases of coronavirus have now hit the U.S.

Earlier, President Trump insisted the U.S. is not suffering through a financial crisis in an Oval Office address to the country about the coronavirus outbreak on Wednesday.

“This is not a financial crisis. This is just a temporary moment of time that we will overcome together as a nation,” Trump said.

Dow Jones industrial average futures plunged after Trump’s address, projecting a loss of more than 800 points when markets open on Thursday.