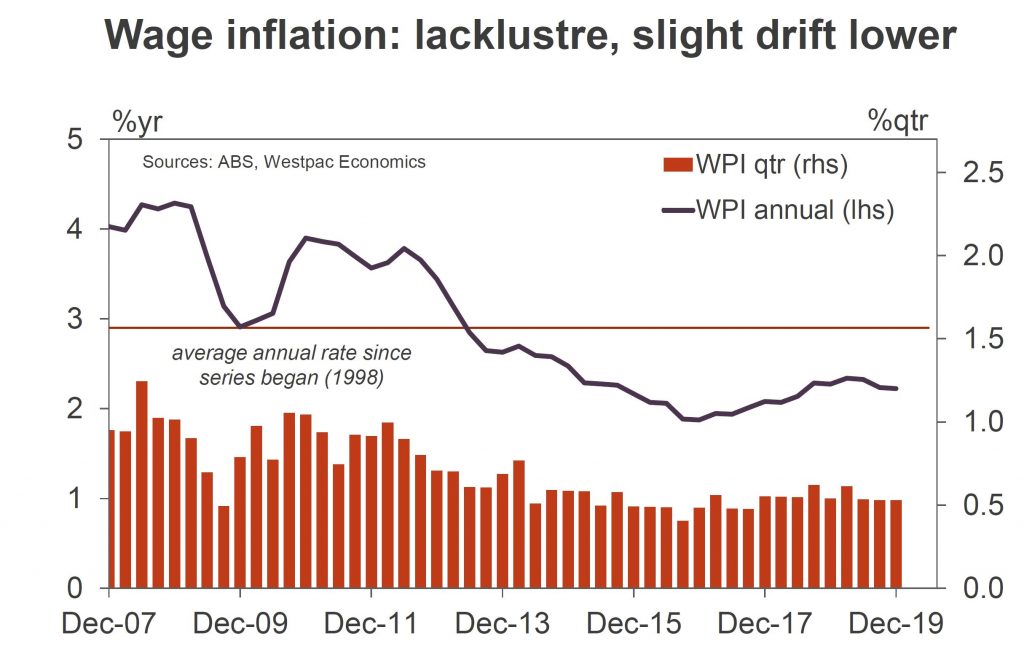

ABS Chief Economist, Bruce Hockman stated

“The seasonally adjusted quarterly rise of 0.5 per cent extended the

period of moderate growth observed throughout 2019, and was influenced

by the relative stability of the labour underutilisation rate. Annually,

both private and public sector wages rose 2.2 per cent; this was the

lowest public sector growth rate since the commencement of the index in

December quarter 1997.”

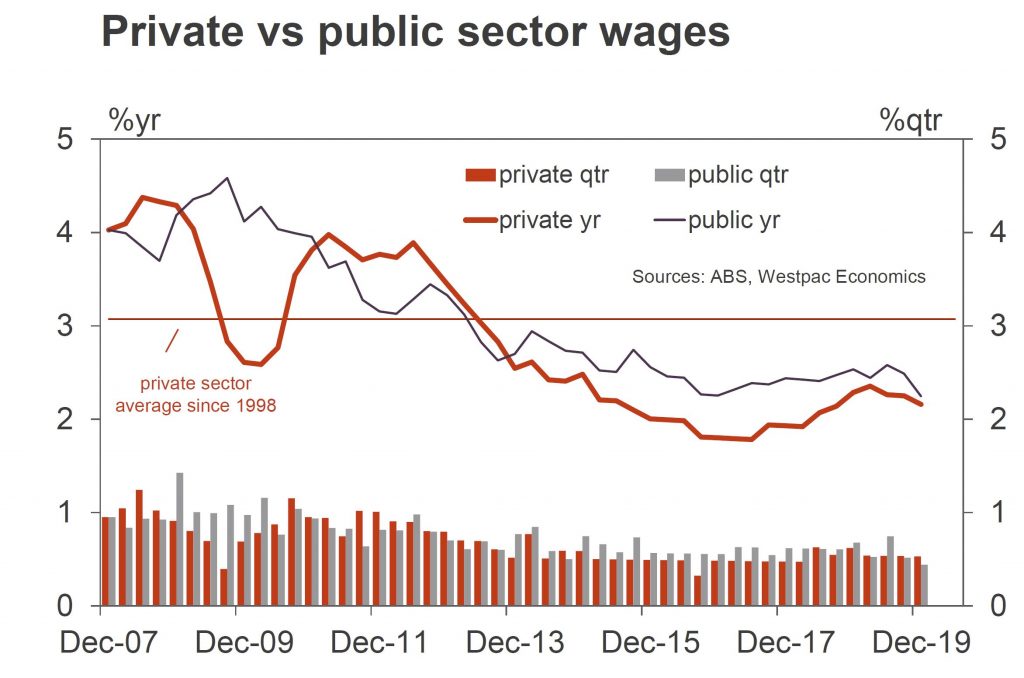

For the first time since 2012, private

sector wages grew at a faster rate than the public sector (0.5 compared

to 0.4 per cent), in original terms.

Across industries, annual wage growth

in 2019 ranged from 1.6 per cent for the information media and

telecommunication services industry to 3.1 per cent for the health care

and social assistance industry.

Victoria recorded the highest through

the year growth of 2.7 per cent, while Western Australia recorded the

lowest for the sixth consecutive quarter (1.7 per cent)

Members commenced their discussion of the global economy by noting the International Monetary

Fund’s forecast for global growth to pick up in 2020 and 2021. The easing in trade tensions

between

the United States and China, and ongoing stimulus delivered by central banks, had supported a

modest

improvement in the growth outlook for a number of economies. Global manufacturing and trade

indicators,

notably export orders, had continued to show signs of stabilising in late 2019. Inflation had

remained

low and below most central banks’ targets. Members also discussed the coronavirus outbreak,

which

was a new source of uncertainty regarding the global outlook.

In China, a range of activity indicators had picked up in the December quarter, which suggested

that

targeted fiscal and monetary easing had been working to stabilise economic conditions. In east

Asia, the

growth outlook had been supported by signs of a turnaround in the global electronics cycle and

more

stimulatory fiscal and monetary policies in some economies in the region. On the other hand, the

outlook

for output growth in India had been revised lower given the broad-based slowing in economic

activity

there.

In major advanced economies, indicators for manufacturing and services activity had ticked up

slightly

and tight labour markets had supported growth in consumption. In the United States, lower

interest rates

had supported a pick-up in residential investment. Business investment intentions had

stabilised.

Japanese economic activity had slowed as expected following the increase in the consumption tax

in

October 2019, but the fiscal stimulus that had been announced was expected to support growth. In

the

euro area, survey indicators of conditions in the manufacturing sector appeared to have bottomed

out,

but investment had remained weak.

The progress in addressing the US–China trade and technology disputes had alleviated an

important downside risk to global growth. However, given the nature of the ‘phase one’

deal and the potential for tensions to re-escalate, this risk had not been eliminated.

Members discussed the coronavirus outbreak, noting that it was a new source of uncertainty for

the

global economy. With the situation still evolving, members observed that it was too early to

determine

the extent to which growth in China would be affected or the nature of the international

spillovers. It

was noted that previous outbreaks of new viruses had had significant but short-lived negative

effects on

economic growth in the economies at the centre of the outbreak. Members observed that it was

difficult

to know how representative these earlier episodes could be. China now accounted for a much

larger share

of the global economy and was more closely integrated, including with Australia, than in 2003 at

the

time of the SARS outbreak. The economic effects would depend crucially on the persistence of the

outbreak and measures taken to contain its spread.

Some commodity prices, notably for industrial metals, iron ore and oil, had fallen on concerns

that the

coronavirus outbreak would disrupt production in China and reduce Chinese commodity demand in

the near

term. By contrast, rural prices had been little changed.

Domestic Economic Conditions

The Australian economy had grown modestly in the September quarter. While growth in public demand

and

exports had been relatively strong, growth in household spending and investment had remained

weak. The

output of the farm sector had also subtracted from growth over the preceding year, reflecting

the

effects of ongoing drought conditions. Members noted that the recent bushfires had devastated

some

regional communities and that this was expected to have reduced GDP growth over the December and

March

quarters. The effects of the coronavirus outbreak were also expected to subtract from growth in

exports

over the first half of 2020.

Overall, economic growth was expected to be weaker in the near term than had been forecast three

months

earlier, partly because of the effects of the bushfires and the coronavirus outbreak. However,

GDP

growth was still expected to pick up over the forecast period, supported by accommodative

monetary

policy, a pick-up in mining investment, and recoveries in dwelling investment and consumption.

The

recovery from the bushfires was expected to add to growth in the second half of 2020. The

central

forecast for growth remained unchanged since November, at 2¾ per cent over 2020

and

around 3 per cent over 2021.

An increase in mining investment was expected in the near term and a turnaround in dwelling

investment

was likely to have occurred by the end of 2019. However, the recovery in consumption was less

certain

and more consequential for overall demand. There was also uncertainty around estimates of the

effects of

the bushfires and the coronavirus outbreak: it was difficult to assess potential indirect

effects on

activity from these events and relevant data were yet to be published.

Household consumption had been lower than expected in the September quarter despite strong growth

in

household disposable income, supported by the receipt of tax offset payments and lower interest

payments

following the recent reductions in the cash rate. Information from the ABS retail sales release

and the

Bank’s liaison program had suggested that retail sales volumes were likely to have grown

only

modestly in the December quarter; although nominal retail sales had increased strongly in the

month of

November, much of this increase was likely to have been purchases brought forward to take

advantage of

‘Black Friday’ sales. Measures of consumer sentiment had declined over recent

months, but

consumers’ views on their personal financial situation, which historically have had a

stronger link

to consumption, had been little changed.

Members noted that a number of factors had contributed to the slowdown in consumption growth

since

mid 2018. The downturn in the housing market had reduced households’ wealth, and the

extended

period of weak growth in household income had probably lowered expectations of future income

growth.

Members observed that the prolonged period of slow growth in income was expected to continue to

weigh on

consumption over coming quarters. Furthermore, recent data had suggested that households were

directing

more income to saving and reducing their debt.

Looking ahead, the Bank’s forecast was for growth in consumption to increase gradually,

sustained

by moderate growth in household disposable income and the recovery in the housing market. Growth

in

housing prices had picked up in most capital cities and parts of regional Australia over recent

months.

Prices had increased very strongly in Sydney and Melbourne in recent months. Higher housing

prices and

the associated increase in housing turnover were expected to support consumption and dwelling

investment.

Dwelling investment had continued to decline in the September quarter, however, and was expected

to

decline further in the near term. Nonetheless, leading indicators were consistent with the

forecast of a

trough in dwelling investment towards the end of 2020, followed by a recovery through 2021.

Private

residential building approvals had increased in the December quarter. Contacts in the Bank’s

business liaison program had reported an increase in sales of new homes and greenfield land in

recent

months.

Business investment declined in the September quarter, with both mining and non-mining investment

weaker than expected as at November. Mining investment had been considerably lower

because

work on new liquefied natural gas plants had continued to wind down. Information from business

liaison

contacts and the recent ABS capital expenditure survey continued to support the view that mining

investment was passing through a trough. Non-mining investment was expected to be subdued in the

near

term, but then to increase modestly, consistent with the expected pick-up in domestic activity.

Public

investment had been stronger than expected in the September quarter and information from

government

budgets had suggested public spending would continue to support growth in the near term,

including

through funding of initiatives for bushfire recovery and drought relief.

The unemployment rate had declined slightly to 5.1 per cent in December. Employment

growth

had moderated in the December quarter, but had remained at 2.1 per cent over the year.

All the

growth in the quarter had been in part-time employment. The Bank’s forecast of employment

growth

had been revised downwards for the first half of 2020, reflecting the overall signal from

leading

indicators and the downward revision to forecast GDP growth in the near term. The unemployment

rate was

expected to remain in the 5–5¼ per cent range for some time before

declining to

around 4¾ per cent in 2021, as GDP and employment growth picked up.

Members noted that the inflation data for the December quarter had been in line with

expectations.

Headline CPI inflation had been 0.6 per cent in the quarter and 1.8 per cent

over

2019. Trimmed mean inflation had been 0.4 per cent in the quarter and 1.6 per cent

over 2019. Housing inflation had continued to be a significant drag on overall inflation,

with little

change in rents both in the quarter and over the year. New dwelling prices had risen in the

December

quarter following earlier declines because smaller discounts had been offered by developers.

Inflationary pressures were expected to remain subdued. Underlying and headline inflation were

expected

to increase a little to around 2 per cent over the following couple of years as spare

capacity

in the economy declined. Wages growth was expected to be largely unchanged over the following

couple of

years because mild upward pressure on growth in the wage price index would likely be offset by

downward

pressure from the increase in the superannuation guarantee from mid 2021.

Members noted that the risks around the wage and price inflation forecasts were evenly balanced.

Wages

growth could pick up faster than expected if labour market conditions tightened by more than

expected.

The increase in the superannuation guarantee in 2021 was forecast to constrain wages growth for

some

wage earners, although the timing and extent of this was uncertain and broader measures of

earnings

growth could be expected to be boosted a little. Domestic inflationary pressures would depend on

a range

of factors, including how fast the economy recovered from the soft patch over the preceding

year, the

persistence of the effect of the drought on food prices, and developments in the housing market.

Financial Markets

Members noted that developments in global financial markets had reflected evolving perceptions of

key

risks.

Up until mid January, concerns over global downside risks had eased following stabilisation in a

range

of forward-looking indicators of growth, the passage of the ‘phase one’ US–China

trade deal and improved prospects for an orderly Brexit. In response, long-term government bond

yields

and equity prices had risen. The US dollar and Japanese yen had depreciated a little, while

the

Chinese renminbi had appreciated. There had also been renewed capital flows into emerging

markets.

However, since then these moves in financial markets had been partly reversed as market

participants

became concerned about the potential effect of the coronavirus on the prospects for global

economic

growth. In particular, government bond yields had declined noticeably to be back at very low

levels. In

Australia, the 10-year government bond yield had declined in line with movements abroad, to

below

1 per cent. Also, the US dollar and Japanese yen had appreciated, while the

Chinese

renminbi had depreciated. The Australian dollar had also depreciated to be around its lowest

level since

2009.

Overall, global financial conditions remained accommodative, in part because of ongoing stimulus

delivered by central banks. After some easing of monetary policies in 2019, central banks in the

major

advanced economies had indicated that their current policy settings were likely to remain

appropriate

for some time. Central banks in the United States, Europe and Japan had recently left policy

settings

unchanged, noting that some downside risks had receded for the time being. However, they had

also

signalled that they were prepared to ease policy further if necessary, and markets were

expecting some

further easing in the United States, the United Kingdom and Canada in the year ahead. In China,

the

central bank had recently implemented targeted measures to support economic growth, including by

providing additional liquidity to the financial system.

Corporate financing conditions had generally remained favourable, including in Australia. Credit

spreads were at low levels and global equity prices had been higher over recent months,

notwithstanding

the volatility associated with the coronavirus outbreak. Members noted that equity market

valuations

were high relative to earnings in a number of economies, which could be explained partly by low

long-term bond yields keeping overall discount rates low relative to history.

Domestically, the reductions in the cash rate in 2019 had seen bank funding costs and lending

rates

reach historic lows. The major banks were estimated to be paying interest of 25 basis

points or

less on a little over one-quarter of their deposit funding. Around 60 basis points of the

75 basis point reduction in the cash rate since mid 2019 had been passed through to

standard

variable mortgage rates. However, the actual rates that households were paying on their

outstanding

variable-rate loans had declined by more than this, with the average rate declining by almost

70 basis points over the same period. This additional decline reflected strong competition

among

lenders for high-quality borrowers and households continuing to switch from (more expensive)

interest-only loans. If this were to continue, by around mid 2020 the average rate paid on

outstanding variable-rate mortgages would have declined by around 75 basis points since May

2019.

Households’ total mortgage payments increased in the December quarter, with a rise in

principal

and excess payments more than offsetting the decline in interest payments. Members discussed

whether

this increase reflected a change in behaviour by households and the potential for it to persist.

They

noted that some households were likely to be repaying their debts faster in response to low

growth of

their incomes and the earlier fall in housing prices. The process of balance sheet adjustment

had been

facilitated in part by the reductions in the cash rate as well as by the higher tax refunds for

low- and

middle-income earners, both of which had boosted disposable incomes.

Consistent with stronger conditions in some established housing markets, housing loan commitments

had

continued to rise. That had been driven largely by owner-occupiers, and growth in credit

extended to

owner-occupiers had increased to 5½ per cent on a six-months-ended annualised

basis in

December. Despite accommodative funding conditions for large businesses, growth in business debt

had

slowed over the six months to December.

Financial market pricing at the time of the meeting suggested that market participants expected a

further 25 basis point cut in the cash rate by mid 2020.

Before turning to the policy decision, members reviewed the policy and academic discussions

taking

place around the world regarding the operation of macroeconomic policy and monetary policy

frameworks in

an environment where interest rates are low because of structural factors. These discussions

focused on

a range of issues, including: the appropriate level and specification of inflation targets; the

cases

for and against more aggressive monetary policy easing when policy interest rates are near the

effective

lower bound; the role of forward guidance and strategies for lowering long-term interest rates

and their

potential side-effects; and the role of fiscal policy. Members also reviewed the international

discussions regarding possible changes in the monetary transmission mechanism at low interest

rates.

Considerations for Monetary Policy

In considering the policy decision, members observed that the outlook for the global economy

remained

reasonable, with signs that the slowdown in global growth was coming to an end. The progress in

addressing the US–China trade and technology disputes had reduced but not eliminated an

important

downside risk to global growth. The coronavirus outbreak was a new source of uncertainty. While

it was

too early to tell what the overall effect would be, the outbreak presented a material near-term

risk to

the economic outlook for China and for international trade flows, and thereby the Australian

economy.

Global financial conditions remained positive. This partly owed to ongoing stimulus delivered by

central banks, and financial market participants expected some further monetary easing in some

economies. Long-term government bond yields were back at very low levels, including in

Australia.

Borrowing rates for households and businesses were at historically low levels, and there was

strong

competition among lenders for borrowers of high credit quality. Conditions in some established

housing

markets had strengthened, and mortgage loan commitments had also picked up. The Australian

dollar had

depreciated to be around its lowest level since 2009.

The outlook for the Australian economy was for growth to improve, supported by a turnaround in

mining

investment and, further out, dwelling investment and consumption. In the short term, the effects

of the

bushfires were temporarily weighing on domestic growth, but the recovery was likely to reverse

the

negative effects on GDP by the end of the year. The forecast recovery in consumption growth

remained a

key uncertainty for the outlook. Consumption had been weak, as households had been gradually

adjusting

their spending to the protracted period of slow growth in incomes and to the fall in housing

prices.

Although housing prices had been rebounding nationally, it was too soon to see the response to

this in

household spending, and it was unclear for how long the period of balance sheet adjustment would

continue.

The unemployment rate had declined a little to 5.1 per cent and was expected to remain

around

this level for some time before declining further to a little below 5 per cent as

economic

growth picked up. Wages growth was expected to be largely unchanged over the following couple of

years.

Members agreed that a further gradual lift in wages growth would be a welcome development and

was needed

for inflation to be sustainably within the 2–3 per cent target range.

In the December quarter, CPI inflation had been broadly as expected at 1.8 per cent

over the

year. Inflationary pressures had remained subdued, held down by flat housing-related costs.

Inflation

was expected to increase gradually to 2 per cent over the following couple of years,

in

response to some tightening in labour market conditions.

Given this outlook, members considered how best to respond.

Members reviewed the case for a further reduction in the cash rate at the present meeting. This

case

rested largely on the only gradual progress towards the Bank’s inflation and unemployment

goals.

Lower interest rates could speed progress towards the Bank’s goals and make it more assured

in the

face of the current uncertainties. In considering this case, the Board took into account that

interest

rates had already been reduced to a low level and that there are long and variable lags in the

transmission of monetary policy. The Board also recognised that the incremental benefits of

further

interest rate reductions needed to be weighed against the risks associated with very low

interest rates.

Internationally, concerns had been raised about the effect of very low interest rates on

resource

allocation in the economy and their effect on the confidence of some people in the community,

notably

those reliant on savings to finance their consumption. A further reduction in interest rates

could also

encourage additional borrowing at a time when there was already a strong upswing in the housing

market.

The Board concluded that the cash rate should be held steady at this meeting. Members agreed that

it

was reasonable to expect that an extended period of low interest rates would be required in

Australia to

reach full employment and achieve the inflation target. The Board would continue to monitor

developments

carefully, including in the labour market, and remained prepared to ease monetary policy further

if

needed to support sustainable growth in the economy, full employment and the achievement of the

inflation target over time.

The Decision

The Board decided to leave the cash rate unchanged at 0.75 per cent.

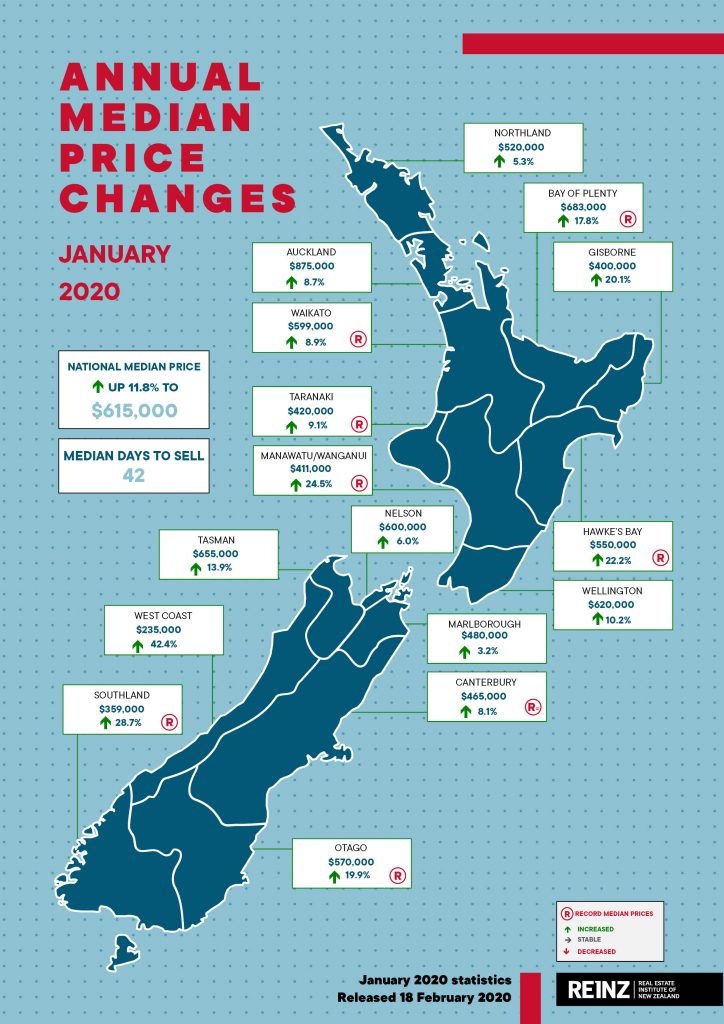

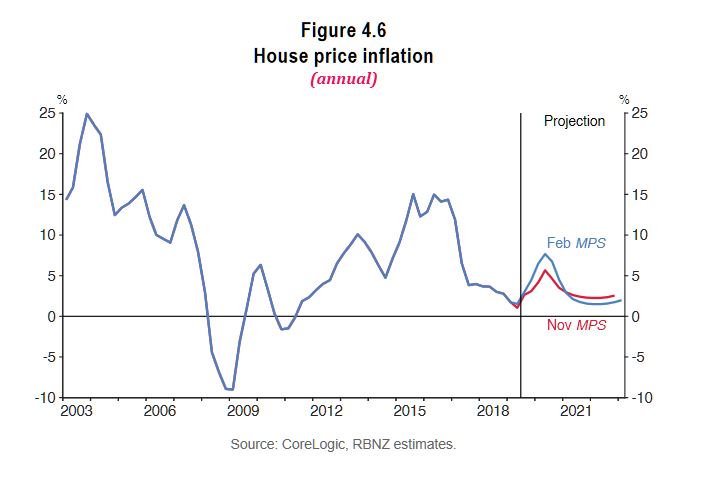

REINZ has released their January 2020 residential report today, and they reported the busiest January in 4 years. The annual average rise across New Zealand was 7%, with Auckland at 4.4% and other areas up 9.1%. Auckland is actually now among the faster-rising regions. Prices in Canterbury are rising, although to date this has been slower than many other regions.

In January the median number of days to sell a property nationally decreased by 6 days from 48 to 42 when compared to January 2019 – the lowest days to sell for the month of January in 3 years.

Low interest rates and lighter regulation are driving the market. Over 2019, the RBNZ cut the OCR from 1.75 percent to 1 percent and they indicate that the OCR will remain at 1 percent for some time. In response, household debt continues to rise. Lower debt servicing costs enables higher household spending on consumption, although returns from savings will be lower as well.

Over the past year New Zealand construction activity has ramped up substantially while net migration has steadily declined. The cancellation of earlier plans to introduce a capital gains tax has also helped to drive the market.

For New Zealand excluding Auckland, the number of properties sold increased by 0.9% when compared to the same time last year (from 3,279 to 3,308) – also the highest for the month of January in 4 years.

In Auckland, the number of properties sold in January increased by 9.7% year-on-year (from 1,180 to 1,295) – the highest number of residential properties sold in the month of January since January 2016.

Sales in Auckland were the highest for the month of January in four years, with particularly strong uplifts in sales volumes in North Shore City (+29.0%), Waitakere City (+28.6%) and Rodney District (+21.1%).

Regions outside Auckland with the highest percentage increase in annual sales volumes during January were: • Nelson: +42.6% (from 54 to 77 – 23 more houses) • Manawatu/Wanganui: +15.3% (from 281 to 324 – 43 more houses) – the highest for the month of January in 3 years • Bay of Plenty: +11.5% (from 340 to 379 – 39 more houses) – the highest for the month of January in 4 years • Marlborough: +11.3% (from 62 to 69 – 7 more houses). Regions with the largest decrease in annual sales volumes during January were: • Tasman: -29.3% (from 58 to 41 – 17 fewer houses) – the lowest since January 2017 • Southland: -27.2% (from 151 to 110 – 41 fewer houses) – the lowest for the month of January in 6 years • Otago: -17.1% (from 269 to 223 – 46 fewer houses) – the lowest for the month of January in 9 years.

In the recent Reserve Bank NZ Monetary Policy Statement, they indicated that over the medium term, annual house price inflation is expected to slow as net immigration moderates, residential construction activity remains high, and the effects of past lower mortgage rates fade.

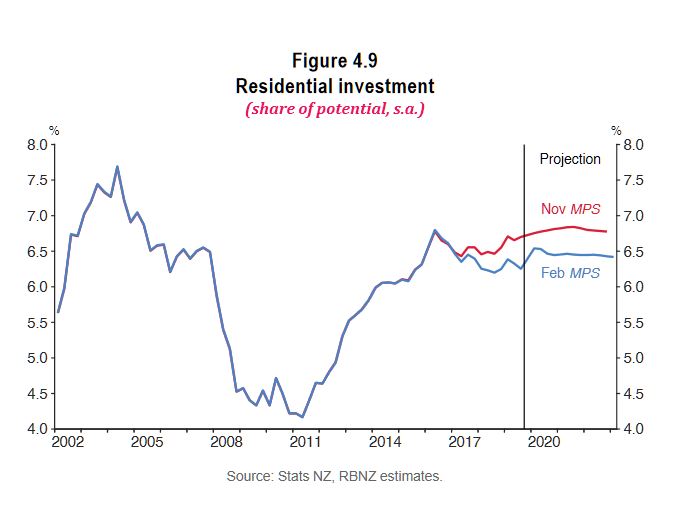

However, they expect residential investment growth is expected to pick up over the next six months, in line with recent high levels of residential building consent issuance. That said, residential investment is forecast to decline very gradually as a share of GDP later in the projection period, reflecting ongoing capacity constraints in the construction sector.

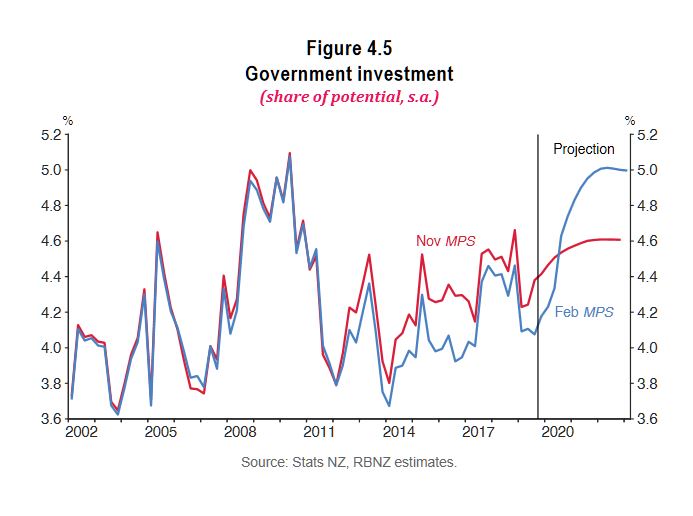

In December 2019, the Government announced a substantial investment package of $12bn, equivalent to around 4 percent of annual nominal GDP. The Treasury forecasts that $8.1bn will be spent between June 2020 and June 2024, mainly on infrastructure projects

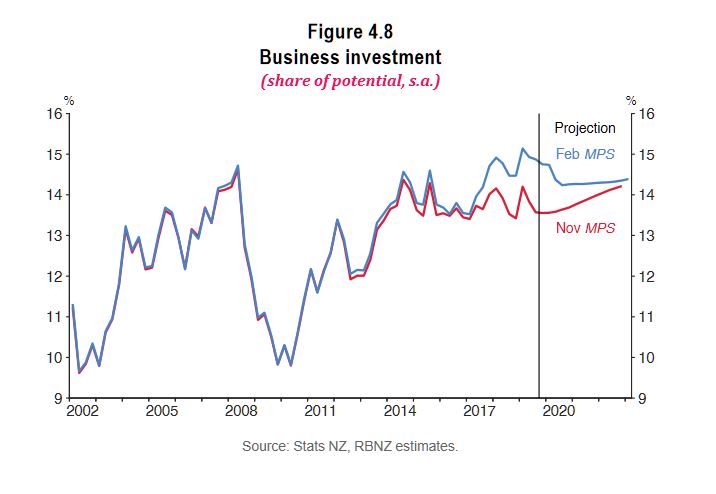

Which is probably just as well, given that business investment is forecast to fall ahead.

We discuss our submission to the Senate Inquiry into funding for the SME sector. The proposed bill will provide incentives for the big banks, but do little to address the real issues. We offer an alternative approach, using data from our SME surveys.

We are pleased to offer our submission for consideration.

The Bill as proposed will do little to address the underlying SME funding

issues we have in Australia, despite benefitting the incumbent major investors

through their equity shares. It might play well from a “we are doing something

for SME’s” perspective, but in reality, it will do little.

To address the real problem of SME funding, we recommend

a FinTech style structure, as already proven in the UK and elsewhere across

Europe. This would enable the allocated funds to reach more businesses, but

more importantly also facilitate a transformation of lending to the SME sector

in Australia, including driving incumbents to lift their game.

This transformational play would demonstrate the

Governments active support for the SME sector, but also lead to broader and

deeper change, to the benefit of the local economy.

Introduction

Digital Finance Analytics is a boutique research and

advisory firm which curates a rolling 52,000 firm survey each year, with ~4,000

new firms added each month. The survey is a telephone omnibus and is executed

on our behalf by a reputable service bureau. It is statistically accurate

across the country.

We design the questions, and analyse the results using our

Core Market Model. The survey has seen running for more than 15 years. We have

several clients who subscribe to our data services, as well as those to receive

copies of the free summaries. Clients include several financial services

companies, FinTechs and Government agencies, within Australia and beyond.

We hold information about their business structure, banking

relationships and financial profile, as well as their digital behaviour. This

provides a multi-factorial basis for our underlying segmentation[i],

which has proved to be both stable, and insightful over time.

There is tremendous diversity in the SME sector, and as a

result one size certainly does not fit all. We believe strong segmentation is

essential to be able to translate strategy into effectively action. We focus on

what we call “the voice of the customer”.

This enabled us to develop models and descriptors for each

of the clusters. Businesses are placed within the model descriptions in a

best-fit manner. We believe that the results should be judged largely on the

interpretability and usefulness of results, not whether the clusters are “true”

or “false”.

When these stable segments are cross-linked with our

research, we can compare the different needs and opportunities across the

groups, and we can prepare segment specific treatment plans for each.

The custom segmentation we use is well distributed by count

across the business community. Growing business and Cash Strapped Sole Traders

are the two largest groups. As expected, the count of Large Established Firms

is the lowest.

In the light of our research, we have reviewed the

provisions of the proposed legislation and wish to make three major points.

SME’s Are Indeed an Essential Part of Our Economy.

The small and medium business sector (SME) is a critical

growth engine for the economy, with more than 3 million businesses offering

employment for more than 7 million Australians. The characteristics of these

businesses are varied from newly founded part-time entities, through to

businesses employing up to 100 people and with a turnover of up to $10 million

each year. More than 77% have a turnover of less than $500,000 each year. 91.3%

have an annual turnover of less than $2 million each year. So, one size does

not fit all.

The largest industry segment is Construction (17%), followed

by Professional, Scientific and Technical (12.5%) and Rental, Hiring and Real

Estate Services (11.5%). Financial Services (9%) and Agribusiness (8.25%) are

the next two. Note that Mining accounts for only 0.4% of all SME’s.

Nearly half of all businesses have been trading for less

than 4 years. Cash Strapped Sole Traders are most likely to fail (55% in 5

years), followed by Cash Strapped Sole Traders and Stable Subcontractors. The

highest failure rates are found in Transport, Financial Services, Real Estate

and Construction.

Most SME’s are true small businesses and one quarter of

SME’s have a sales turnover off less than $50,000 each year, and more than half

have a turnover of less than $150,000 per annum. Most low turnover businesses

are unincorporated. Those businesses with larger turnovers are more likely to

be formed as a company.

Looking at the state distribution, 60% of businesses are in

NSW and VIC.

Funding Is Indeed A Growing Problem for SME’s.

We have detected an increasing problem where more businesses

are unable obtain suitable finance to enable them to grow and invest in their

businesses. Underlying this is the fact

that demand from households and businesses for services from the SME sector is

waning as the broader economy falters. SME’s are the canary in the economic

coalmine!

For many segments, the need for working capital is the main

issue, and the main cause of this need relates to delayed payments. This is

particularly a concern among some smaller businesses. The average debtor days

is still elevated, with 45% of firms reporting an average settlement time from

invoicing of 50-60 days. There were minor variations across the states. Debts from Large Corporates and Government

entities are both taking longer to settle due to “enhanced” cash flow

management techniques.

The average number of banking relationships varies across

the segments. Larger and more complex businesses are likely to spread their

relationships. Others, in need of funding, will also try to access facilities

from many sources, and so have more complex relationships.

Satisfaction with banking services remains in the doldrums,

with around half of all businesses dissatisfied, or very dissatisfied with

their bank, and only 17% very satisfied.

The satisfaction rating did vary by segment, with more established

firms who do not need to borrow the more satisfied, while newer smaller firms,

seeking to borrow, the least satisfied. For them access to credit was a

significant issue.

Compliance and price were the two most significant causes of

dissatisfaction, though only 5% said obtaining funding was the root cause of

their concerns. When asked about their propensity to switch lenders, 61% said

they would consider moving. However, when we examined their length of time with

existing banking relationships, many are rusted on long term. The inertia, and

the gap between intent to switch and switching is explained by a combination of

time constraints, complexity of switching and lack of available alternatives.

Again, this footprint varies by segment.

We continue to see the rise of FinTech lenders operating in

Australia. Around 23% of SME’s have applied, and a further 10% say they will

apply for funding. Overall awareness is rising, although there are some

concerns about the true costs of borrowing from this source.

Many lenders are reluctant to lend to the sector, require

security (mortgage over property for example) and funding is expensive. Banks

prefer to lend to households as opposed to businesses, partly because of the

relative capital ratio costs and lower risk profiles.

Some businesses are turning to the growing FinTech sector,

where unsecured finance is available, at a price, but getting funding through

these channels can be expensive because of lack of true competition and high

demand.

Finally, we agree with the proposition that Australia

currently lacks a patient capital market for small and medium enterprises. But this is not the main issue blocking the

growth of the sector. Access to straightforward credit is.

But the Proposed Bill Is Targeting the Wrong SME Segments

We understand the fund will invest between $5 million to $15

million in small and medium enterprises that have a turnover of between $2

million and $100 million, where they can demonstrate three years of revenue

growth and a clear vision to expand.

Established Australian businesses will be eligible to apply

for equity capital investments between $5 million and $15 million.

Small-business owners will not have to give up control for this investment.

The Business Growth Fund’s investment stake will range from

10 to 40 per cent, setting a balance between business owners keeping control of

their business and providing enough incentives for investors. Initially, the

Business Growth Fund could support 10 investments per year, with the aim to

increase to 30 per year as the fund develops. Banks and superannuation

contributions could enable the fund to grow to $500 million.

Our research indicates that this particular segment is

small, can already obtain funding for such expansion (many would fit within our

“Business In Transition” segment), and as a result we do not believe many would

be prepared to give up such a large stake in their growing businesses. It seems

this is more orientated to offer investors and the financial sector a return,

than being shaped best to provide support for those small businesses which need

assistance the most. The small number of transactions envisaged will also not

assist many businesses, and the target is clearly not the bulk of those with

real funding needs.

Thus, we cannot support the current proposal (which we also

note is imprecise in terms of the assessment processes, return hurdles and

other matters). Our view is that the current proposal appears rushed, and too

high-level. But our main point is, it is targeting the wrong SME’s.

We Think There Is A Better Option

We believe there is a better option to assist SME’s in their

growth agenda. The truth is there is a dearth of financing available from

existing major players. Their risk and capital ratios mean they prefer to lend

to households for mortgage purposes, then to small business. As interest rates

fall, this pressure is being exacerbated.

We think a better model would be to provide funding via the

emerging Fintech sector, by either providing funding to flow to existing FinTech’s,

or by creating a new Government backed marketplace where FinTech’s and SME’s

can transact.

There are good examples of such models[ii].

For example, in the UK, the main contenders are Tide (focused solely on SMEs,

small or medium-sized companies) and Starling (which has retail accounts as

well). In France, the big player is Qonto. In Germany, there’s Penta and Hufsy

(which is based in Denmark). In Norway, Aprila. For “micro-businesses” of 1-10

people, there’s Holvi in Finland, Coconut, Anna and CountingUp in the UK, and

Shine in France.

Tide now claims over 1.4% of the UK’s SMEs as clients (up

from 1% in December 2018), and is gunning for 8% market share by 2023, aided by

a £60m UK government grant.

Meanwhile, Starling has 46,000 SME members, up from 30,000

in March, with £100m from the same government grant to develop its business

banking offering.

Qonto in France has grown from 15,000 small business

customers to 40,000 in the past year, and is expanding into Germany, Spain and

Italy this year. Finnish startup Holvi, which was bought by Spanish bank BBVA

in 2016, claims 150,000 customers and is expanding into France, Italy, the

Netherlands, Ireland and Belgium.

There is a lot of space for growth because the European

market — with 24.5m SMEs — is still extremely dominated by the big lenders. In

the UK, for example, four big banks have a 90% share of SME banking.

This was an intentional strategy from the UK Government to

disrupt the inadequate SME sector. And in response the incumbents have been

forced to respond and are now upping their game and starting their own

digital-focused business banks as well to compete. In November 2018, NatWest

launched Mettle. Santander’s “start-up” small business bank, Asto, also

launched in the UK late 2018 Meanwhile, HSBC is building its own small business

bank start-up, known internally as Project Iceberg.

In addition, the cost of funding to SME’s has dropped and

the Fintech sector has developed, supported by the core injection of UK

Government funding.

These digital plays cover a wide range of services which

SME’s need, as well as basic payments, transactions and lending. And they are

tending to create a marketplace where businesses and service providers and

lenders can interact. This is transformational.

The SME experience has been significant, with easier access

to funding, faster decisions, and the resultant rebalancing of the industry has

lifted mainstream lenders too. If a similar model was replicate here, the SME

sector would win. Australia would win.

Conclusion

The point to make, is rather than a thin deal flow

targeting larger SME’s which really do not need assistance, a revised strategy

could facilitate transformation of finance to SME sector. Thus, the planned investment

could be made by the Australian Government, but leading to more productive

outcomes. If we were to replicate a UK model, we think it should be the current

inflight Fintech-based approach, rather than one which favours incumbents, and

which does not deal with the core issues Australian SMEs face.

Thus, we recommend that the current proposed Bill is

withdrawn, and the strategy redeveloped to take account of the emerging Fintech

scene

Martin North

Principal

Digital Finance Analytics

9th February 2020

[i] Our

partitional clustering approach means that the segments are defined using multi-factor

cluster analysis and split into non-overlapping tribes, rather than in a

hierarchical tree. To achieve this, we developed a proprietary scoring system

based on Lloyd’s algorithm, (also known as Voronoi iteration) for grouping data

points into a given number of categories. This is often referred to as k-means

clustering. The modelling is iterated sufficiently to enable adequate

separation between clusters, as determined by Lloyds’s algorithm.

We will be running our latest live show tomorrow 20:00 Sydney on 18th February. Join us live, to ask a question, or send one in beforehand via the DFA blog

Economist John Adams and Analyst Martin North reflect on last week’s Canberra visit when John had 14 (yes 14) meetings about the Cash Restrictions Bill. But John also came away with some more disturbing conclusions about our politicians.

The current popular view is that in response to the Covid-19 problem, the central bank will stimulate, and this will support the local, and therefore global economy. One reason why markets are sanguine.

There is just one problem with this. China’s Global Times (one external voice of the Government) headed a piece “China should get ready for belt-tightening following virus outbreak”. Maybe China will not stimulate the economy by rolling out another massive monetary stimulus. This is potentially a game changer.

With the Chinese economy taking a major hit from the outbreak of the novel coronavirus pneumonia (COVID-19), the central government appears to pursue fiscal austerity as part of the efforts to pull through the difficult times.

While it is generally expected that fiscal stimulus and monetary easing will undoubtedly be the two main tools of central authorities for alleviating downward pressure on the economy and for maintaining macroeconomic stability, given the past experience and the financial risks currently facing China, a flood of spending programs seems no longer on the financial regulators’ list of choices for stimulating the economy.

“China will face decreased fiscal revenues and increased expenditures for some time to come, and the fiscal operation will maintain a state of ‘tight balance.’, Chinese Finance Minister Liu Kun wrote in an article published on Qiushi, a magazine affiliated with the Communist Party of China Central Committee. In this situation, it won’t be feasible to adopt a proactive fiscal policy by expanding the fiscal expenditure scale. I, and instead, policies and capital must be used in a more effective, precise and targeted way,” Liu said. Chinese Finance Minister Liu Kun wrote in an article published on Qiushi, a magazine affiliated with the Communist Party of China Central Committee.

Liu’s article sent a clear signal that China would not stimulate the economy by rolling out another massive monetary stimulus.

Due to the major impact of the coronavirus outbreak on businesses across the country, the Ministry of Finance has already made it clear that it would continue to reduce the tax burden on enterprises, which will undoubtedly weigh down the already slowing fiscal income. And a potential decrease in fiscal revenues directly points to the limited room for splashing out on unnecessary programs. China’s fiscal revenues grew 3.8 percent in 2019, the slowest growth since 1987, while fiscal expenditures during the same year gained 8.1 percent compared with the previous year, outpacing economic growth.

Therefore, to maintain a “tight balance,” the Chinese economy will have to tighten its belt by curbing non-essential expenditures while expanding investment in a precise and targeted manner.

There has been a consensus call among economists and economic observers for the fiscal deficit ratio to break the 3 percent GDP mark temporarily so that more space could be given to fiscal expenditures to stabilize the economy amid the epidemic.

However, it should be noted that fiscal space constraint is not the key reason for belt-tightening. Past experience with massive stimulus already showed that a flood of investments could lead to many consequences like high levels of local government debts, and to the detriment of high-quality economic growth.

In 2019, China’s fiscal expenditures reached 23.9 trillion yuan ($3.4 trillion), of which only 3.5 trillion yuan was spent by the central government, and the rest by local governments.

In this sense, governments at all levels should be prepared for belt-tightening in the future to come.

This could have significant consequences for us all!

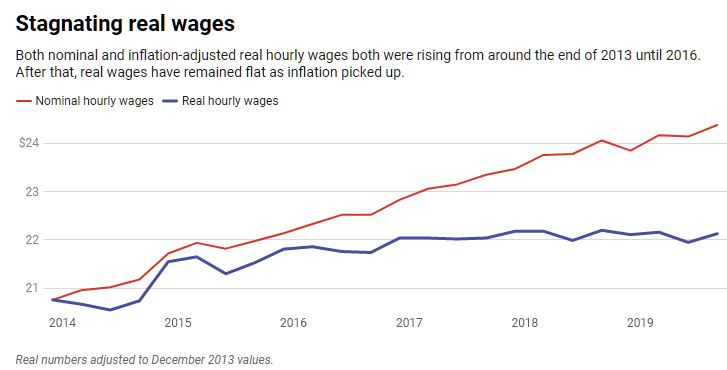

At first glance, the latest data – which came out on Feb. 7 – look pretty good. They show nominal hourly earnings rose 3.1% in January from a year earlier.

But the operative word here is nominal,

which means not adjusted for changes in the cost of living. Once you

factor in inflation, the picture changes drastically. And far from

representing a “blue collar boom” – as the president put it in his State of the Union address – the real, inflation-adjusted data show most U.S. workers have not benefited from the growing economy.

As an economist who studies wage data, I think it’s paramount that we take a step back and look at what the data really show.

Business journalists and financial markets

tend to focus on the monthly data. These figures are only reported in

nominal or current terms because the inflation data doesn’t come out

until later.

A more complete set of wage and pay data

is reported quarterly. The latest release came out in December for the

third quarter. These figures are not only adjusted for inflation but

also include fringe benefits, which account for just under a third of

total compensation.

At first blush, it makes sense to focus

primarily on the first set. Newer data is, well, newer, and market

participants and companies prefer the latest information when making

decisions about investments, hiring and so on.

But the effect of inflation means that the same US$1 bill buys less stuff over time as prices increase.

From December 2016 to September 2019, nominal wages rose 6.79% from $22.83 to $24.38. But after factoring in inflation, average wages barely budged, climbing just 0.42% in the period.

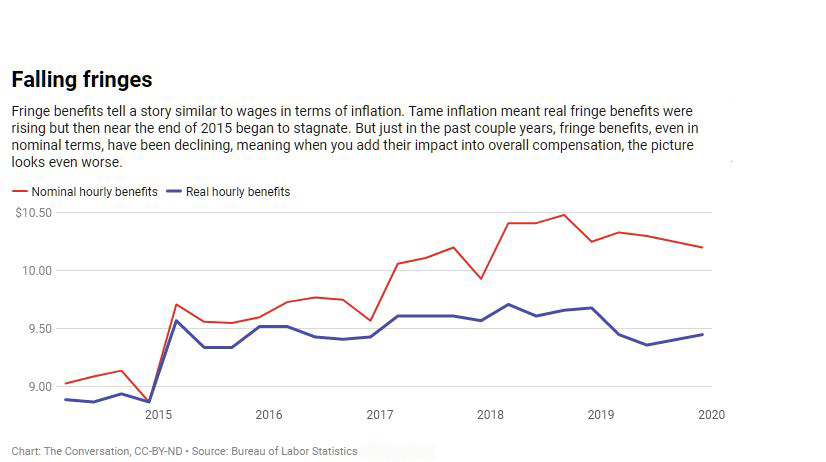

Incorporating fringe benefits into the picture adds another wrinkle.

The inflation-adjusted or real value of

fringe benefits, which include compensation that comes in the form of

health insurance, retirement and bonuses, declined 1.7% in the

three-year period.

Altogether, that means total real compensation slipped 0.22% from the end of 2016 to September 2019.

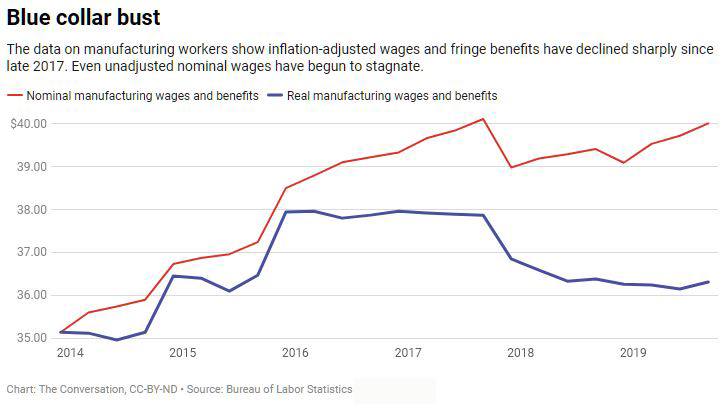

Of course, workers in different sectors

have fared differently. The Trump administration has singled out

manufacturing workers – who it says are the main beneficiaries of its

trade war and other policies intended to support the sector – as having

benefited from a “blue collar boom” in wages.

The nominal data for manufacturing workers

hardly support a boom but they do show an increase of 2.22% since

Donald Trump took office.

The adjusted data, however, make it look

more like a bust, with wages plunging 3.88% in the period. And, again,

the situation is worse when we add in fringe benefits, which brings the

decline to 4.33%.

So next time you read a story about a rise in pay, try to see if it reports the wage data in nominal or real terms, and if it includes fringe benefits too. If it’s only nominal wages, the numbers may mean a lot less than they seem.

Author: David Salkever, Professor Emeritus of Public Policy, University of Maryland, Baltimore County