According to the Bank of England, climate change creates risks to both the safety and soundness of individual firms and to the stability of the financial system. These risks are already starting to crystallise, and have the potential to increase substantially in the future. There is a pressing need for central banks, regulators and financial firms to accelerate their capacity to assess and manage these risks.

So, the Bank of England has published a discussion paper which sets out its proposed framework for the 2021 Biennial Exploratory Scenario (‘BES’) exercise.

The objective of the BES is to

test the resilience of the largest banks and insurers (‘firms’) to the

physical and transition risks associated with different possible climate

scenarios, and the financial system’s exposure more broadly to

climate-related risk.

They say, conducting a climate stress test poses distinct challenges compared to conventional macrofinancial or insurance stress tests. To ensure it is effective in light of these challenges, the Bank is using this discussion paper to consult relevant stakeholders on the design of the exercise. This includes financial firms, climate scientists, economists, other industry experts, and informed stakeholder groups.

Whilst climate-related risks will materialise over decades, actions today will affect the size of those future risks. It is therefore important that firms, and other stakeholders such as the Bank, continue to develop innovative approaches to measure climate-related risks before it is too late to ensure resilience to them. The BES will use exploratory scenarios to size these future risks and to explore how firms might respond to them materialising, rather than testing firms’ capital adequacy.

The key features of the BES are:

Multiple Scenarios that cover climate as well as macro-variables: to test the resilience of the UK’s financial system against the physical and transition risks in three distinct climate scenarios. These range from taking early, late and no additional policy action to meet global climate goals.

Broader participation: both banks and insurers are exposed to climate-related risks, and the action of one will spill over to affect the other. For insurers, this exercise builds on the scenarios developed for this year’s insurance stress test.

Longer time horizon: is needed as climate-related risks crystallise over a much longer timeframe than conventional risks. The BES proposes a modelling horizon of 30 years. This is because climate change, and the policies to mitigate it, will occur over a much longer timeframe than the normal horizon for stress testing. To make these scenarios credible and tractable, the Bank proposes that the BES examine firms’ resilience using fixed balance sheets, focusing on sizing the risks and the scale of business model adjustment required to respond to these risks, rather than testing the adequacy of firms’ capital to absorb those risks.

Counterparty-level modelling: a bottom up, granular analysis of counterparties’ business models split by geographies and sectors is proposed to accurately capture the exposure to climate-related risks.

Output: the Bank will disclose aggregate results of the financial sector’s resilience to climate-related risk rather than individual firms.

The Governor Mark Carney said: “The BES is

a pioneering exercise, which builds on the considerable progress in

addressing climate related risks that has already been made by firms,

central banks and regulators. Climate change will affect the value of

virtually every financial asset; the BES will help ensure the core of

our financial system is resilient to those changes.”

Sarah Breeden the Executive Director

sponsor for climate change said “None of us can know exactly how climate

change will unfold, but we do know that it will create risks to the

financial system. I am excited that this ground-breaking exercise will

for the first time allow us to quantify this risk and so determine the

actions we need to take today if we are to minimise these future risks.”

The Bank is consulting on the design of the exercise and welcomes feedback on the feasibility and the robustness of these proposals from firms, their counterparties, climate scientists, economists and other industry experts by 18 March 2020. The final BES framework will be published in the second half of 2020 and the results of the exercise will be published in 2021.

The Banks concludes, there are many challenges involved in designing such an exercise and this proposal seeks to balance various trade-offs. These include providing a comprehensive description of the potential risks while also creating a tractable exercise for firms, and providing sufficient detail in the scenarios to allow results to be aggregated consistently while also providing scope for firms to assess the risks in a granular way.

I discuss the latest with Formafist in Canada and we compare the two markets in terms of property and the broader economy. How has 2019 been and what is 2020 looking like? Some amazing parallels, and stark differences….

This segment covers the Canadian market, and the other half of the discussion, covering the Australian market is available on Daniel’s channel here:

What’s been happening to house prices and sales volumes over 2019, what’s changed in the year

What’s happened to foreign buyers?

What’s happening to Investors?

Any news on building construction, quality, new approvals?

How about the broader economy, and interest rates?

Biggest surprise of the year

Looking ahead, thoughts on next year,

Will home prices, and volumes go up or down, (what might determine that)

Will interest rates be cut or raised by central banks?

What’s the biggest thing to watch for… in each market…

In this trimmed high quality recording of our live event, we discuss the latest financial and property data, examine our latest scenarios, and discuss the trends ahead. We also answer a range of questions posed by our viewers live. The unedited original stream with live chat, is available to view (starting at 0:30) below:

AMP Financial Planning Pty Ltd (AMPFP) ceased providing managed discretionary account (MDA) services on 10 December 2019 following the imposition of tailored licence conditions by ASIC.

In March 2019, following a surveillance of

AMPFP’s MDA services and advice business, ASIC granted AMPFP’s

application to vary its Australian financial services (AFS) licence to

provide MDA services, subject to some tailored licence conditions (19-078MR).

The tailored conditions formalised commitments made by AMPFP, in

response to ASIC’s concerns, to improve monitoring and supervision of

its discretionary investment services and related financial advice.

Under the tailored licence conditions, a

Senior Executive of AMPFP was required to provide an acceptable

attestation to ASIC by 30 September 2019 confirming that AMPFP had

complied with and was complying with the tailored conditions. This was

to ensure that all of the required improvements to monitoring and

supervision practices had been implemented and were operating

effectively.

AMPFP did not provide ASIC with an acceptable attestation in relation to its provision of MDA services. The attestation provided by AMPFP had exceptions and ASIC informed AMPFP that the attestation was not acceptable to it, and AMPFP ceased providing MDA services in accordance with its licence conditions.

Background

MDAs create particular risks for retail

clients because when a client enters into a contract with an MDA

provider, they give the provider authority to make investment decisions

on their behalf on an ongoing basis without seeking the client’s prior

approval.

The risks increase if the person

recommending the MDA service and making or influencing the investment

decisions are the same because the clients may not be receiving

impartial advice about the decision to enter into or remain in the MDA

service. ASIC expects AFS licensees to consider the risks involved with

the financial advice and investment activities of their representatives

in their monitoring and supervision practices.

The Federal Reserve Board and Federal Deposit Insurance Corporation announced Tuesday that they did not find any “deficiencies,” which are weaknesses that could result in additional prudential requirements if not corrected, in the resolution plans of the largest and most complex domestic banks. However, plans from six of the eight banks had “shortcomings,” which are weaknesses that raise questions about the feasibility of a firm’s plan, but are not as severe as a deficiency. Plans to address the shortcomings are due to the agencies by March 31, 2020.

Resolution plans, commonly known as living

wills, describe a bank’s strategy for rapid and orderly resolution

under bankruptcy in the event of material financial distress or failure.

In the plans of Bank of America, Bank of

New York Mellon, Citigroup, Morgan Stanley, State Street, and Wells

Fargo, the agencies found shortcomings related to the ability of the

firms to reliably produce, in stressed conditions, data needed to

execute their resolution strategy. Examples include measures of capital

and liquidity at relevant subsidiaries. The agencies did not find

shortcomings in the plans from Goldman Sachs and J.P. Morgan Chase.

The firms will receive feedback letters, which will be publicly available on the Board’s website.

For the six firms whose plans have shortcomings, the letter details the

specific weaknesses and the actions required. Overall, the letters note

that each firm made significant progress in enhancing its resolvability

and developing resolution-related capabilities but all firms will need

to continue to make progress in certain areas.

To that end, the letters confirm the

agencies expect to focus on testing the resolution capabilities of the

firms when reviewing their next plans. Resolving a large bank would be

challenging and unprecedented, and the agencies expect the firms to

remain vigilant as markets change and as firms’ activities, structures,

and risk profiles change.

The agencies also announced on Tuesday

that Bank of America, Goldman Sachs, Morgan Stanley, and Wells Fargo had

successfully addressed prior shortcomings identified by the agencies in

their December 2017 resolution plan review.

Bank of Ireland has caved in to public pressure following a public outcry over its plans to heavily restrict cash transactions in its branches, via Irish Independent.

The bank came in for sustained criticism

after the Irish Independent revealed yesterday that it plans to restrict

over-the-counter cash withdrawals to a minimum of €700 and cash

lodgements to a minimum of €3,000 in an effort to push customers towards

using ATMs and self-service machines.

However, after criticism from Finance

Minister Michael Noonan, as well as groups representing consumers,

farmers, older people, rural dwellers and bank workers, the bank

conceded that what it called “vulnerable” customers could continue to

get cash and make withdrawals of smaller amounts of money at branch

counters.

The changes prompted fears of a renewed

bout of bank branch closures and staff lay-offs in the wake of the

bank’s move to severely restrict counter-based cash transactions.

Mr Noonan described the changes as

“surprising and unnecessary”, adding that he expects the bank to “fully

honour” its commitment to “vulnerable customers”.

Bank of Ireland said it would continue to

allow older customers and those unfamiliar with technology to make cash

transactions over the counter.

“Bank of Ireland would like to confirm

that vulnerable customers, together with those elderly customers who are

not comfortable using self-service channels or other technology

solutions, will be assisted by branch staff to use the available

in-branch services.”

However, other banks are now expected to

follow the lead of Bank of Ireland by moving to set strict limits on

over-the-counter cash handling.

It comes after around 200 bank branches

were closed, mainly in rural areas, during the financial collapse, with

at least 10,000 retail bank staff laid-off.

Banks including Bank of Scotland, Danske, ACC and Irish Nationwide have already closed, limiting banking options for customers.

Now there are concerns that the move by

Bank of Ireland to effectively become a cashless bank will prompt more

branch shut-downs and redundancies.

Deputy chairman of the Consumers

Association Michael Kilcoyne said other banks were set to mirror Bank of

Ireland and discourage customers from withdrawing and lodging cash over

the counter.

This would make branches in rural areas less viable, he warned.

“The implications of the Bank of Ireland

move are very severe. If it gets away with this it will get rid of more

staff and close branches.

“This will be a further blow for rural Ireland,” he said.

Mr Kilcoyne predicted that AIB, Ulster Bank and Permanent TSB would make similar moves to curtail cash handling.

And banking union IBOA said it is seeking a

meeting with Bank of Ireland boss Richie Boucher over concerns the

changes would mean more job losses.

The Irish Farmers’ Association said the

changes would cause great difficulty for some farmers who are not

familiar with the bank’s online system.

Age Action accused the bank of ignoring the needs of older people by setting high limits on over-the-counter transactions.

ASIC has commenced civil penalty

proceedings in the Federal Court against National Australia Bank Limited

(NAB) and seeks findings of several thousand contraventions of the ASIC

Act and the Corporations Act.

ASIC alleges that from December 2013 to February 2019, NAB:

engaged in Fees for No Service Conduct by

failing to provide ongoing financial planning services to a large

number of customers while charging fees to those customers;

failed to issue, or issued defective, fee

disclosure statements (FDSs). ASIC alleges that the defective FDSs

contained false or misleading representations in that they did not

accurately describe the fees the customer paid and/or the services the

customer actually received. The provision of the defective or

out-of-time FDSs terminated the ongoing fee arrangements between NAB and

its customers and it is ASIC’s case that consequently NAB was not

lawfully entitled to continue to charge the fees;

failed to establish and maintain compliance systems and processes to detect and prevent these failures; and

contravened its overarching obligations

as an Australian Financial Services licence holder to act efficiently,

honestly and fairly.

It is also ASIC’s case that NAB engaged in

unconscionable conduct from at least May 2018 by continuing to charge

ongoing service fees to certain customers when it knew that it had not

delivered the services and had issued defective FDSs or at least knew

that there was a real risk that it had engaged in this conduct. However,

NAB did not stop charging fees to its customers until 4 February 2019.

ASIC is seeking declarations, pecuniary

penalties and compliance orders from the Federal Court to prevent

similar contraventions occurring in the future.

‘Fees for No Service

misconduct has been widespread and is subject to ongoing ASIC regulatory

responses including investigations and enforcement actions. This

widespread misconduct was examined in some detail by the Financial

Services Royal Commission. ASIC views these instances of misconduct as

systematic failures, unfair to customers including those that are more

vulnerable.

‘When the Fees for No Service

misconduct is coupled with Fees Disclosure Statements inadequacies or

failings, customers are potentially placed in a more disadvantageous

position. The customer may not therefore have been provided with the

opportunity to know whether they have received the services for which

they have paid or the amount of fees charged to them’ said ASIC Deputy

Chair Daniel Crennan QC.

The maximum civil penalty for contraventions alleged against NAB are:

$250,000 per contravention for breaches

of s962P (charging ongoing fees after the termination of an ongoing fee

arrangement) and s962S (failing to provide a timely FDS);

$1.7 to $2.1 million maximum penalty

(depending on the time period) per contravention for breaches of s12CB

(unconscionable conduct) and s12DB (false or misleading

representations).

NAB received more than $650 million in

ongoing service fees from 2009 to 2018. NAB has stated that it has

provisioned more than $2 billion for Fee for No Service remediation

across all of its advice licensees.

Background

Fees for No Service conduct and

remediation of that conduct by NAB and other licensees was examined as

part of the Financial Services Royal Commission. ASIC has been

monitoring NAB’s (and other licensees’) remediation of its fees for no

service failures with the last update on its progress provided on 11

March 2019 (19-051MR).

On 28 November 2019, ASIC released Report 636 – compliance with the fee disclosure statement and renewal notice obligations (19-325MR).

As noted by Report 636, FDSs are intended

to help customers understand what services they have paid for, what

services they have received and how much those services cost, and to

enable them to make more informed decisions about whether their ongoing

fee arrangements with their adviser should continue. Not issuing or

issuing late or defective FDSs deprive customers of an opportunity to

make those important decisions.

ASIC’s action against NAB falls within

ASIC’s Wealth Management Major Financial Institutions Portfolio. The

Portfolio focuses on the financial services conduct of Australia’s

largest financial institutions (NAB, Westpac, CBA, ANZ, Macquarie and

AMP) with respect to credit and retail lending, financial advice, fees

for no service, superannuation trustees, insurance, unfair contract

terms and other licensee obligations, and other conduct arising from the

Financial Services Royal

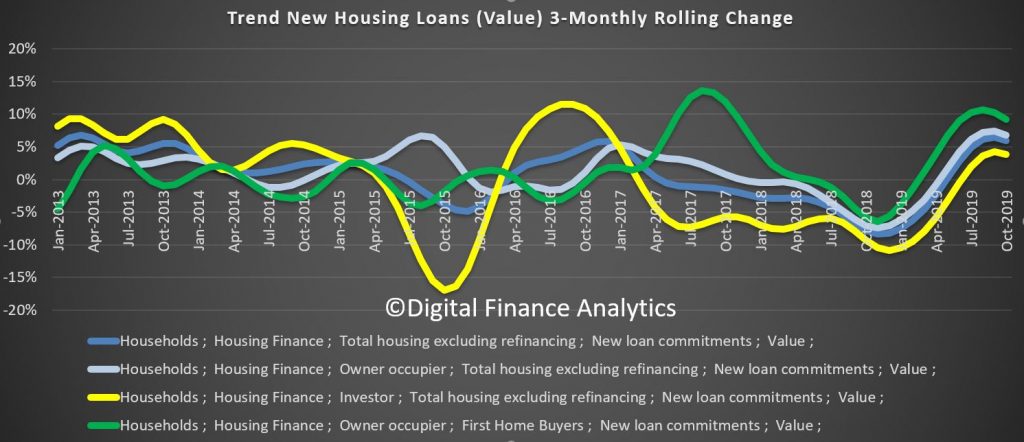

The ABS released their new data series today on loan flows. This includes some enhancements on the old data, though mostly back to July 2019 only, as well as some of the previously reported series. It will take some time to examine these in detail, but here is my first take.

New loan flows rose through the past few months, though the rate of growth slowed in October.

More focus on owner occupied loans than investor loans as expected. First time buyers also remain active, mainly for owner occupation purchase.

New loan commitments for housing rose by 2.0 per cent, seasonally adjusted, in October according to new data released today by the Australian Bureau of Statistics (ABS) in its Lending Indicators publication (previously called Lending to Households and Businesses).

ABS Chief Economist, Bruce Hockman, said: “New loan commitments for housing showed further strength in October, with the series up 15.2 per cent on the most recent trough in May 2019. Recent growth continues to be driven by new commitments for owner occupier housing, which rose 2.2 per cent in October, the fifth consecutive monthly increase.”

The data released today for the first time is based on new and improved data from the Economic and Financial Statistics collection.

“The new collection provides a more contemporary view of a changing economy. It also provides more information on investment lending, including new information on first home owners who are investors,” Mr Hockman said.

Previously published levels have changed with the data in the new publication presented on a consistent basis. An information paper released by the Australian Bureau of Statistics last week explains the impacts of the changes.

The number of loan commitments to owner occupier first home buyers rose 1.4 per cent in October, accounting for 29.9 per cent of new housing loan commitments to owner occupiers.

Personal finance fixed term loan commitments rose 3.1 per cent in October following a 0.8 per cent fall in September and were down 0.4 per cent on October 2018.

In trend terms, the value of new loan commitments to businesses for construction rose 1.2 per cent in October, while new loan commitments to businesses for the purchase of property fell 2.2 per cent.

RBA’s minutes out today. Clear signals of more action next year, despite the perceived gentle turning point.

Financial Markets

Members noted that interest rates were very low around the world, with a number of central banks

having

eased monetary policy over recent months in response to downside risks to the global economy and

subdued

inflation. Market expectations for further policy easing by central banks had been scaled back

over

previous months, with concerns about the downside risks receding a little. The US Federal

Reserve had

indicated that any further reduction in the federal funds rate would require a material change

in the

economic outlook. Reflecting these developments, market pricing had pointed to a narrowing in

the degree

of uncertainty around the expected path for the federal funds rate. Globally, long-term

government bond

yields had remained at very low levels, but had risen slightly in recent months as the prospects

for

further easing in monetary policy had diminished.

Financing conditions for corporations remained very accommodative. Robust demand for corporate

debt had

seen spreads narrow between corporate bond yields and government benchmarks. US equity prices

had risen

to new highs over the prior month, and had increased significantly since the start of the year

relative

to corporate earnings. Australian equity prices had also increased over the month, with the ASX

200 returning to the highs reached in July.

Foreign exchange rates had been little changed over the previous month. The People’s Bank of

China

had continued to implement targeted easing measures to support financing conditions, while

remaining

conscious of the need to contain financial stability risks. More broadly in emerging markets,

central

banks had eased monetary policy in recent months. However, political unrest remained a source of

volatility for certain markets.

Members discussed the transmission mechanisms for monetary policy in Australia through financial

markets. They noted that the reductions in the cash rate this year had been transmitted to

broader

financial conditions in ways that were consistent with the historical experience. Government

bond yields

had declined across the yield curve by more than 1 percentage point over the year, which

had flowed

through to lower funding costs across the economy. The Australian dollar had depreciated by

around

6 per cent on a trade-weighted basis over the previous year and remained at the lower

end of

its range over recent times. The depreciation reflected the reduction in the interest

differential

between Australia and the major advanced economies, and had occurred despite an increase in the

terms of

trade over this period.

The recent reductions in the cash rate had been reflected in reduced funding costs for banks, and

had

flowed through to lower borrowing rates for households. Average variable mortgage rates had

declined by

around 65 basis points since the middle of the year, as competition for high-quality

borrowers had

remained strong and households continued to switch away from interest-only loans towards

principal-and-interest loans at lower interest rates. These trends were expected to continue.

Consistent with lower mortgage interest rates and improved conditions in some housing markets,

housing

loan commitments had been increasing over the preceding few months, particularly for

owner-occupiers.

Growth in credit extended to owner-occupiers had also increased a little in recent months, while

lending

to investors had still been declining.

Members noted that data from lenders and information from liaison suggested that only a small

share of

borrowers had actively adjusted their scheduled mortgage payments following the reductions in

interest

rates. This was consistent with historical experience in the months immediately following a

reduction in

the cash rate. However, the available data indicated that, even over the longer term, as

interest rates

had declined borrowers had not been paying down their home loans more quickly than in the past.

Mortgage

payments as a share of aggregate household income had remained steady over recent years,

although were

slightly lower than in the first half of the decade.

Interest rates on loans to businesses had also declined to historically low levels. Despite the

accommodative funding conditions for large businesses, growth in business debt had slowed,

suggesting

that demand for finance had softened. Lending to small businesses had been little changed over

the

preceding year, and access to finance for small businesses remained restricted.

Financial market pricing implied that market participants were expecting a further 25 basis

point

reduction in the cash rate by mid 2020.

Members discussed longer-term developments in the banking sector, including the strengthening of

prudential requirements and the opportunities and challenges presented by advances in

technology.

Increased capital and liquidity after the financial crisis had made banks safer, but had also

raised the

relative attractiveness of some forms of market-based finance. Members discussed how advances in

technology opened up new opportunities for banks, while also introducing potential new

competitors.

International Economic Conditions

Members observed that there had been little change in the global outlook over the previous month,

but

that some of the downside risks had receded. The near-term uncertainty around US trade policy

had

diminished because some of the previously planned tariff increases had been postponed and there

was some

prospect of an initial agreement between the United States and China. In addition, a ‘hard

Brexit’ was assessed to be less likely.

Weak trade outcomes had continued to restrain growth in output, particularly for export-oriented

economies. Survey indicators of manufacturing activity and export orders had stabilised,

although they

remained at low levels. Surveyed conditions in the services sector had declined as weaker

external

demand conditions had spilled over to sectors other than manufacturing. Members noted that even

though

geopolitical tensions had lessened recently, ongoing uncertainty had adversely affected the

confidence

and spending decisions of businesses. In the euro area, investment indicators had remained weak

and

business confidence had declined further since September. In the United States, consumer

spending had

been solid and employment growth had strengthened. Recently, some survey measures of

manufacturing and

services activity had increased a little, although industrial production and surveyed investment

intentions had declined further in recent months.

Slower growth in China and India, largely unrelated to trade tensions, had also continued to be a

feature of the recent pattern of global growth. In China, indicators of activity had been weaker

in

October. The real levels of retail sales and fixed asset investment had declined in October and

the

output of a broad range of industrial products had remained subdued. Members noted that, in

response to

slowing growth, Chinese authorities had eased minimum equity capital requirements for a variety

of

infrastructure projects (including port, road, rail, logistics and ecological protection

projects). In

India, the extended monsoon season had exacerbated existing weakness in the economy.

Inflation remained low in the major advanced economies and was below target despite tight labour

markets and higher wages growth. Members observed that inflation had generally declined in Asia.

In

China, although headline consumer price inflation had increased, reflecting higher pork and

other meat

prices, core consumer price inflation had remained broadly unchanged at a relatively low rate.

Movements in commodity prices had been mixed since the previous meeting. The announcement of

further

measures to support steel-intensive economic activity in China had supported iron ore prices. At

the

same time, reports of a tightening in coal import controls in China had weighed on coking and

thermal

coal prices. Base metals prices had generally been lower since the previous meeting. Supply

developments

had continued to support the prices of some rural commodities.

Domestic Economic Conditions

A number of indicators suggested that growth in Australia had continued at a moderate pace since

the

middle of the year.

Members discussed survey measures of business confidence and conditions, and consumer sentiment.

Business confidence had been below average and below its recent high levels in 2017 and early

2018, with

the decline broadly based across industries. In contrast, survey measures of current business

conditions

had remained around average in recent months. Members noted that, historically, business

conditions had

been a better indicator of current economic activity than measures of business confidence,

although its

main advantage was timeliness rather than adding information not present in other indicators.

Growth in household disposable income had been weak over recent years, in both nominal and real

terms.

Members noted the importance of income growth as a key driver of consumption growth, although

the

earlier downturn in the housing market had also had a noticeable effect. The recent recovery in

the

established housing market was expected to be positive for consumption growth in the period

ahead.

Retailers in the Bank’s liaison program had suggested that nominal year-ended sales growth

had been

little changed in October and November.

Households’ expectations about future economic conditions had declined significantly since

June.

Members noted that the prolonged period of slow income growth had affected both consumer

sentiment and

growth in household consumption. Members observed that the decline in sentiment had coincided

with an

increasingly negative tone in news coverage of the economy. Notwithstanding this, households’

assessment of their own financial situation relative to a year earlier had remained broadly

steady and

somewhat above average. Historically, households’ assessments of their own finances

generally have

mattered more for household consumption decisions than their expectations about future economic

conditions.

Conditions in established housing markets had continued to strengthen over the previous month.

Housing

prices had increased further in Melbourne and Sydney and this experience had been broadly based

across

both cities. Growth in housing prices had increased in Brisbane, Adelaide and regional areas,

and

housing prices had increased in Perth for the first time in two years. Non-price indicators had

also

pointed to a strengthening of conditions in the established housing market: auction clearance

rates had

remained high in Sydney and Melbourne, and auction volumes had picked up, albeit from a very low

base.

By contrast, conditions in the new housing construction market had remained subdued. Residential

construction activity was expected to continue to contract for several quarters, despite

conditions in

established housing markets having strengthened. Although there had been tentative signs of an

improvement in conditions in some of the earlier stages of building activity, most indicators

had

remained weak, and most developer contacts in the liaison program were yet to report increased

sales of

new housing.

Business investment appeared to have eased in the September quarter. Information from the ABS

Capital

Expenditure (Capex) survey and preliminary non-residential construction data suggested that

non-mining

investment had decreased in the quarter, led by a marked decline in machinery & equipment

investment. The Capex survey had provided the fourth estimate of investment intentions for 2019/20. Non-mining investment in 2019/20 was

expected to be weaker than previously envisaged, while the survey continued to suggest that

mining

investment would contribute to growth over time, as firms invested to sustain – and in

some

instances expand – production.

Conditions in the labour market and wages data had shown little change since earlier in the year.

The

unemployment rate had remained around 5¼ per cent in October. Employment had

declined by

19,000 in October as both full-time and part-time employment had declined. This had

followed a

sustained period of stronger-than-expected employment growth, which had remained at 2 per cent

over the year despite the most recent monthly decline. The employment-to-population ratio and

the

participation rate had both remained at high levels. Over the previous few months, measures of

the

number of job advertisements had not changed much and firms’ near-term hiring intentions

had

remained broadly stable. Employment intentions among the Bank’s liaison contacts had

generally been

moderate, but had been weakest for firms exposed to residential construction.

The wage price index (WPI) had increased by 0.5 per cent in the September quarter, to

be

2.2 per cent higher in year-ended terms, which was broadly as had been expected.

Private

sector wages growth had been 2.2 per cent in year-ended terms, and had levelled out in

recent

quarters following its gentle upward trend of the previous couple of years. This was consistent

with

information from liaison that a larger share of firms expected wages growth to be stable (rather

than

increasing) in the year ahead compared with a year or so earlier. Growth in the private sector

WPI

measure including bonuses and commissions had risen to 3 per cent in year-ended terms,

which

was the highest rate of growth since late 2012. This was consistent with information from

liaison

indicating that firms had been using temporary measures to retain and reward employees rather

than

permanent wage increases. Public sector wages growth had slowed in the September quarter

following the

one-off boost from the large wage outcome for Victorian nurses and midwives in the June quarter.

Considerations for Monetary Policy

Turning to the policy decision, members noted that there had been little change in the economic

outlook

since the previous meeting. Globally, financial market conditions had been more positive, as

market

participants’ concerns about downside risks had receded a little and a number of central

banks had

eased monetary policy. There were also signs of stabilisation in several recent economic

indicators,

particularly for the manufacturing industry.

Domestically, after a soft patch in the second half of 2018, the Australian economy appeared to

have

reached a gentle turning point. GDP growth in the September quarter was expected to have

continued at a

similar pace since the beginning of the year. Most of the partial data preceding release of the

national

accounts had been in line with expectations, although non-mining investment had been weaker and

public

spending a little stronger. The outlook for growth in output continued to be supported by lower

interest

rates, the recent tax cuts, high levels of spending on infrastructure, a pick-up in the housing

market

and the improved outlook in the resources sector. However, members noted that weak growth in

household

income continued to present a downside risk to consumer spending, and that a low appetite for

risk could

be constraining businesses’ willingness to invest. The drought in many parts of Australia

was

another source of uncertainty for the outlook.

Members observed that labour market conditions had been broadly unchanged since earlier in the

year.

While this outcome had largely been in line with forecasts, it remained an area to monitor, both

because

an improving labour market was important for its own sake and also because a tightening in the

labour

market would put upward pressure on wages growth and inflation. It was noted that the current

rate of

wages growth was not consistent with inflation being sustainably within the target range, unless

productivity growth was extraordinarily weak, nor was it consistent with consumption growth

returning to

trend.

Members discussed the transmission to the economy of the interest rate reductions since the

middle of

the year. They noted in particular that the available evidence suggested that more stimulatory

monetary

policy had been working through the usual channels of lower bond yields, a depreciation of the

exchange

rate and lower interest rates on mortgages. There had also been an effect on housing prices,

increased

housing turnover in the established market and some early signs of a stabilisation in housing

construction activity. The upturn in the housing market was a positive development for the

economy in

the near term, but could become a source of concern if borrowing were to run too quickly ahead

of income

growth.

Members also discussed community concerns about the effect of lower interest rates on confidence,

noting the decline in business confidence and consumer sentiment this year. This decline had

coincided

with heightened economic uncertainty globally, a period of softer growth in the Australian

economy and

weakness in household income growth, and the Board had responded to these factors in preceding

months.

While members recognised the negative confidence effects for some parts of the community arising

from

lower interest rates, they judged that the impact of these effects was unlikely to outweigh the

stimulus

to the economy from lower interest rates.

In assessing the evidence, members noted that monetary policy had long and variable lags and that

indebted consumers may take some time before increasing their spending in response to a decline

in their

mortgage interest payments. More generally, the persistently low growth in household incomes

continued

to be a source of concern for the consumption outlook. Economic growth and the unemployment rate

remained broadly consistent with the forecasts, but members agreed that it would be concerning

if there

were a deterioration in the outlook. As in other countries, there was no real concern of

inflation

rising quickly.

The Board concluded that the most appropriate approach would be to maintain the current stance of

monetary policy and to continue to assess the evidence of how the easing in monetary policy was

affecting the economy. Members agreed that it would be important to reassess the economic

outlook in

February 2020, when the Bank would prepare updated forecasts. As part of their deliberations,

members

noted that the Board had the ability to provide further stimulus to the economy, if required.

Members

also agreed that it was reasonable to expect that an extended period of low interest rates would

be

required in Australia to reach full employment and achieve the inflation target. The Board would

continue to monitor developments, including in the labour market, and was prepared to ease

monetary

policy further if needed to support sustainable growth in the economy, full employment and the

achievement of the inflation target over time.

The Decision

The Board decided to leave the cash rate unchanged at 0.75 per cent.