Australian retail turnover rose 0.2 per cent in September 2019, seasonally adjusted, according to the latest Australian Bureau of Statistics (ABS) Retail Trade figures. In line with our expectations, and continuing to show the pressure on households, and the limited impact of the tax cuts, and even lower interest rates.

This follows a 0.4 per cent rise in August 2019.

Rises were seen in other retailing (0.8 per cent), cafes, restaurants and takeaway services (0.6 per cent), and food retailing (0.1 per cent). These rises were slightly offset by a fall in clothing, footwear and personal accessory retailing (-0.5 per cent) and department stores (-0.2 per cent). Household goods (0.0 per cent) was relatively unchanged.

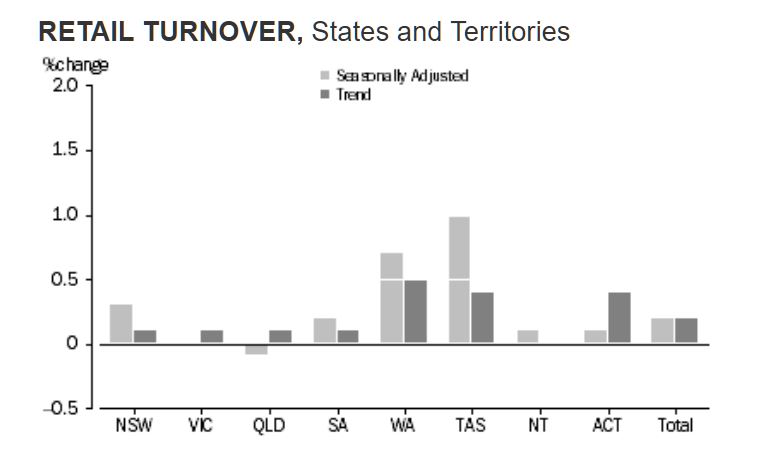

In seasonally adjusted terms, there were rises in New South Wales (0.3 per cent), Western Australia (0.7 per cent), Tasmania (1.0 per cent), South Australia (0.2 per cent), the Australian Capital Territory (0.1 per cent), and the Northern Territory (0.1 per cent). Victoria (0.0 per cent ) was relatively unchanged. Queensland (-0.1 per cent) fell in seasonally adjusted terms in September 2019.

The trend estimate for Australian retail turnover rose 0.2 per cent in September 2019, following a rise of 0.2 per cent in August 2019. Compared to September 2018, the trend estimate rose 2.4 per cent.

Online retail turnover contributed 6.3 per cent to total retail turnover in original terms in September 2019. In September 2018 online retail turnover contributed 5.6 per cent to total retail.

Quarterly volumes fall 0.1 per cent

For the September quarter 2019, there was a fall of 0.1 per cent in seasonally adjusted volume terms. This follows a rise of 0.1 per cent in the June quarter 2019.

The quarterly fall in volumes was led by cafes, restaurants and takeaway food services (-1.0 per cent), and department stores (-0.1 per cent). Food retailing (0.0 per cent) was relatively unchanged. Household goods (0.9 per cent), other retailing (0.3 per cent), and clothing, footwear and personal accessories retailing (0.3 per cent) rose in seasonally adjusted volume terms.

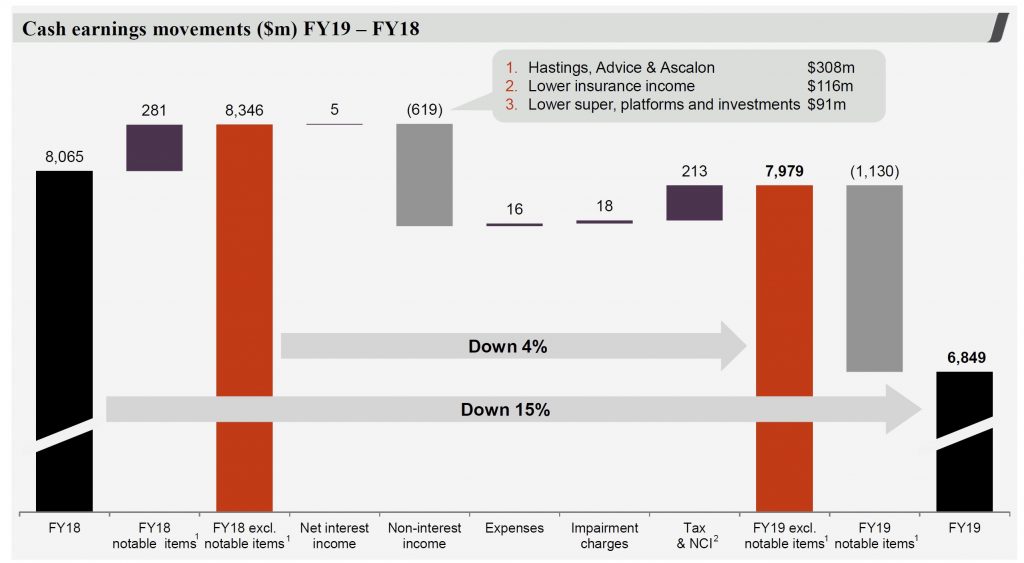

What ever way you look at the 2019 results, out today, Westpac had a bad year in a low growth, low interest rate, high customer remediation environment. Their statutory net profit was $6,784 million, down 16%, while cash earnings were $6,849 million, down 15%.

In FY19 and FY18, the Group raised provisions called “notable items” of $1,130m which relate to Customer remediation Provisions of $958 million (after tax) in FY19, $281 million in FY18.

The majority of the provisions relate to remediation programs for:

Ongoing advice service fees associated with the Group’s salaried financial planners and authorised representatives

Refunds for certain customers that had interest only loans that did not automatically switch, when required, to principal and interest loans

Refunds to certain business customers who were provided with business loans where they should have been provided with loans covered by the National Consumer Credit Protection Act

Other items as part of our get it right, put it right initiative Wealth reset In March 2019, the Group announced its decision to reset its Wealth business. In FY19, provisions for restructuring and transition costs were $241 million (after tax $172 million)

Cash earnings per share was 198.2 cents, down 16%. Westpac’s return on equity (ROE) was 10.75%, down 225 bps. The Final fully franked dividend is 80 cents per share, down 15% from 94 cents per share.

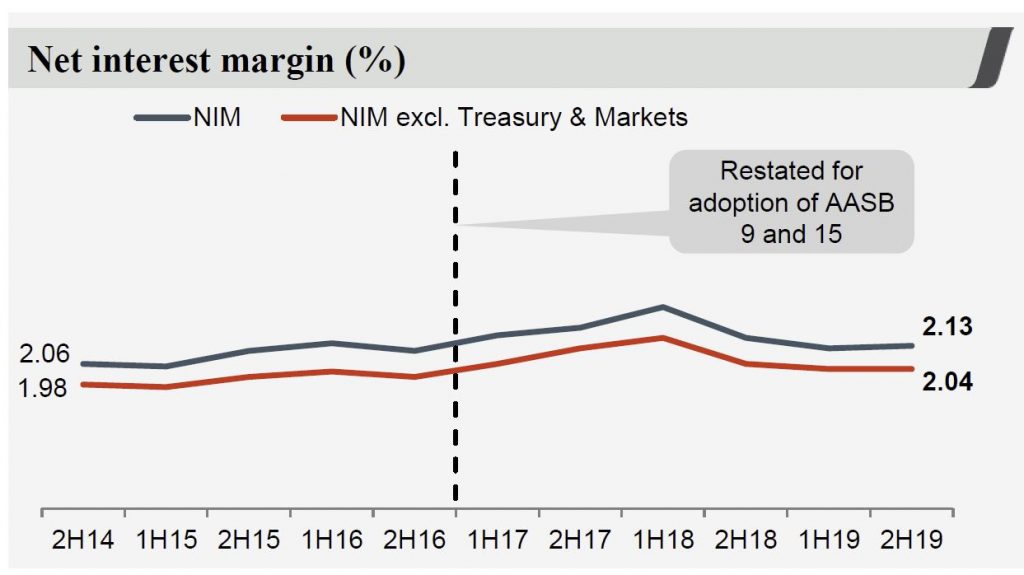

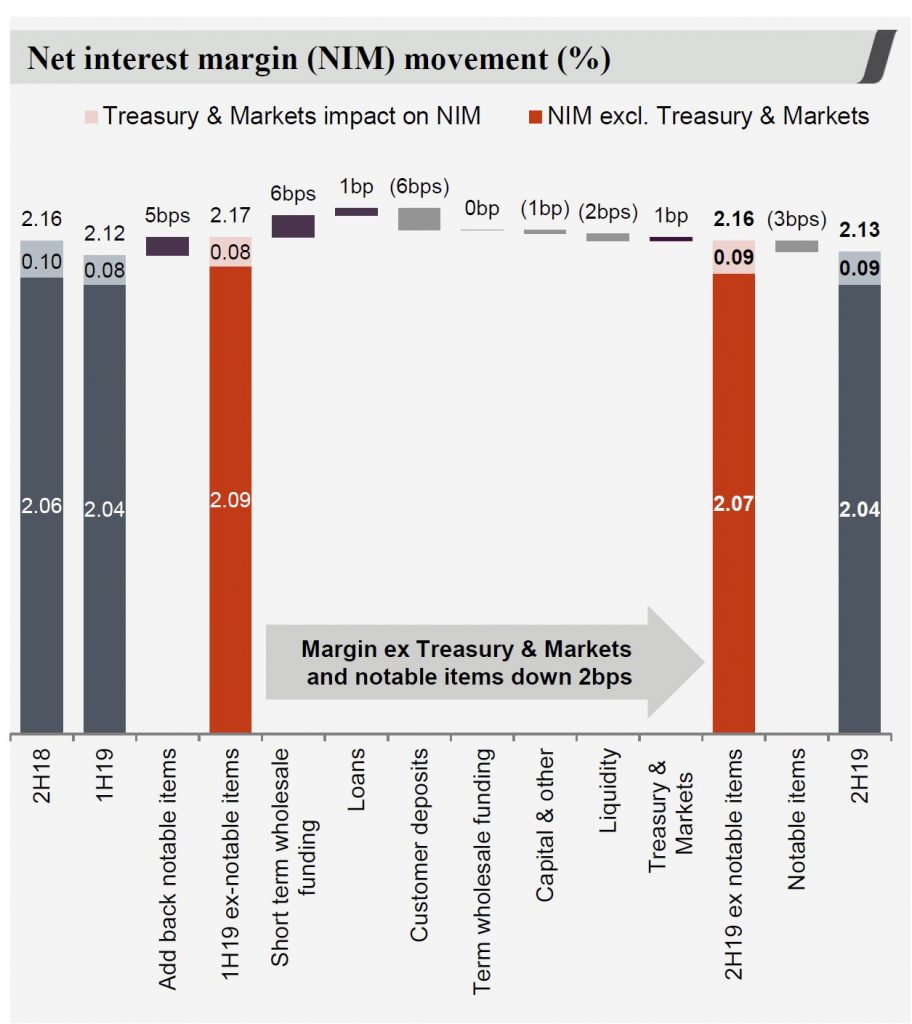

Their net interest margin was 2.12%, down 10 bps

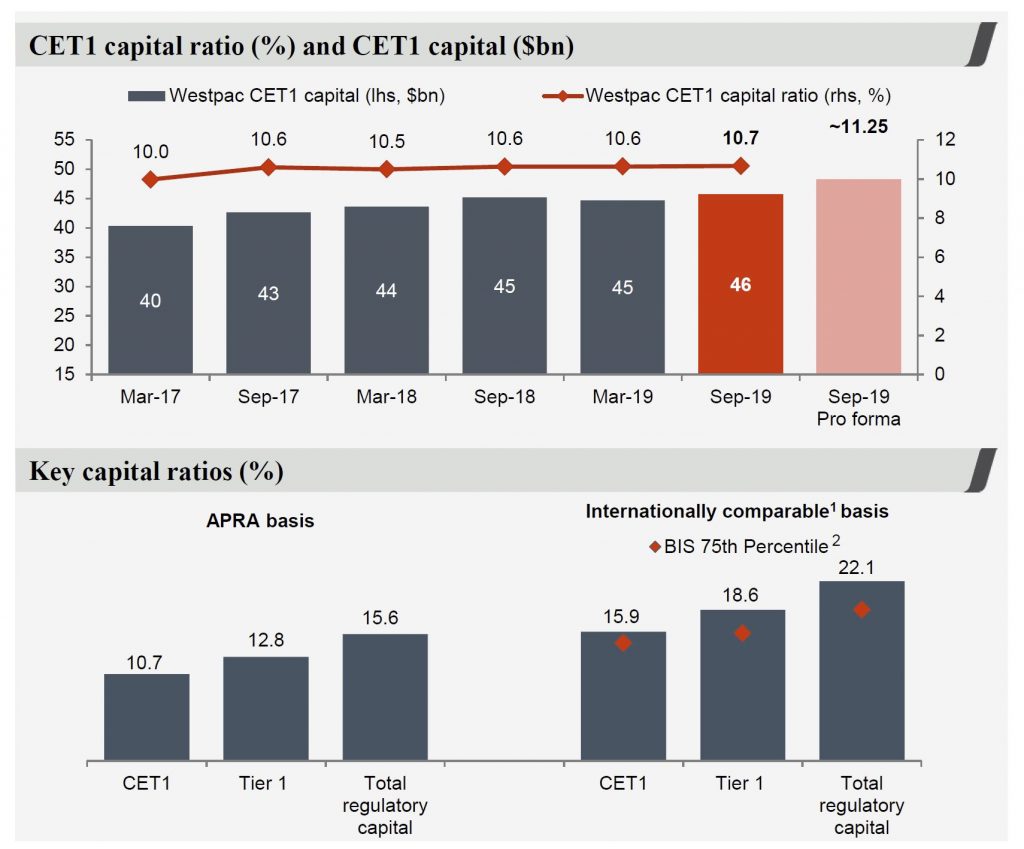

Their common equity Tier 1 (CET1) capital ratio was 10.7%, still above APRA’s unquestionably strong benchmark.

Even if you exclude the “one-offs”, cash earnings were $7,979 million, down 4% and the ROE at 12.52%, is down 94 bps.

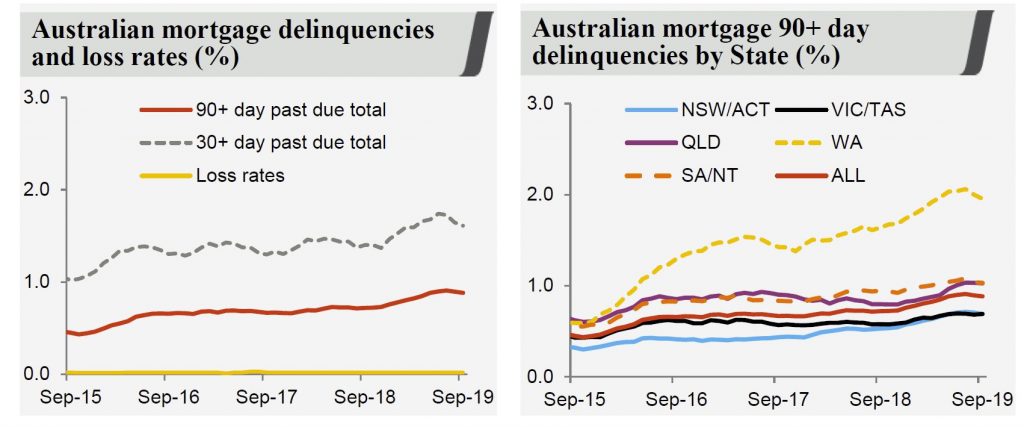

Westpac said credit quality remains sound and impairment charges remain low at 11 basis points of loans. Nevertheless, they have seen a rise in 90 day mortgage delinquencies over the year, in part due to low wage growth and slowing economic activity. A number of factors are evident:

Existing 90+ day borrowers remaining in collections for longer due mainly to weak housing market activity in most of FY19 –

A greater proportion of P&I loans in the portfolio (70% of portfolio at 30 September 2019)

NSW/ACT delinquencies rose 6bps in 2H19 (16bps higher over FY19) to 69bps at 30 September 2019 (NSW/ACT represents 41% of the portfolio)–

Seasoning of the RAMS portfolio, as this portfolio has a higher delinquency profile

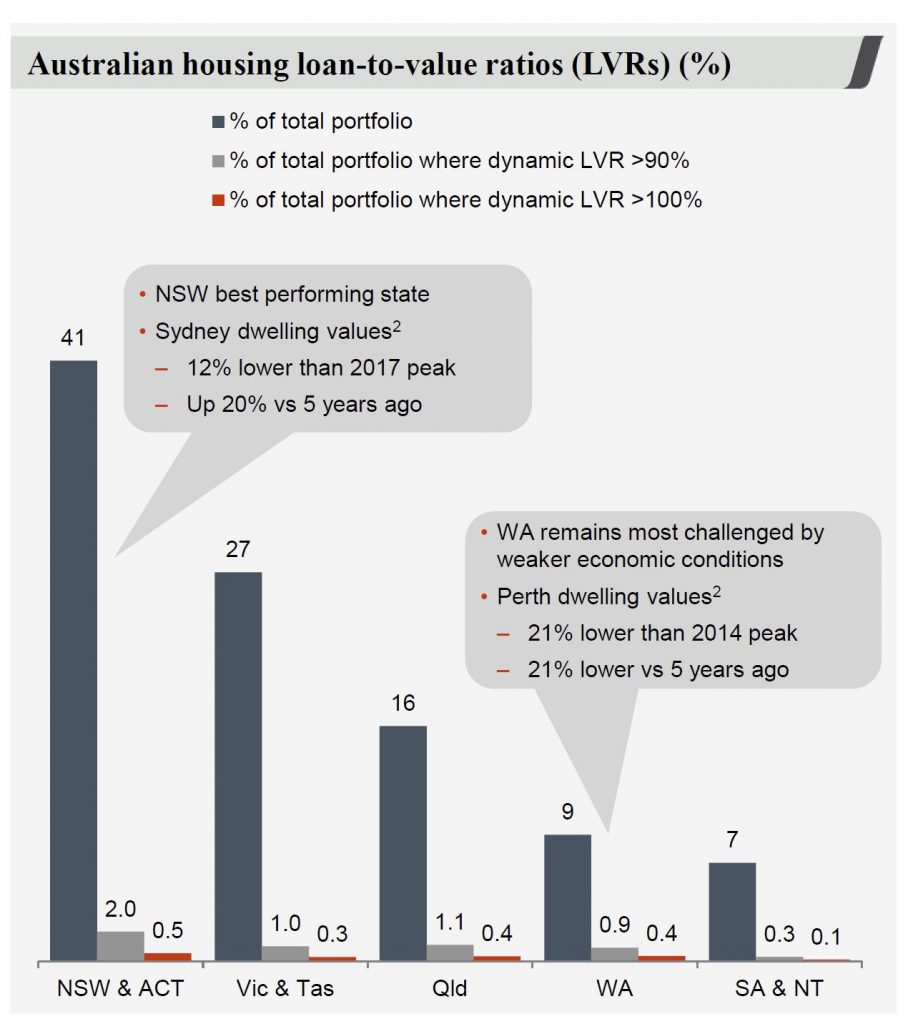

70% of Australian home loan customers are ahead on their repayments including offset accounts. Australian properties in possession increased over the year by 162 to 558. Properties in possession continue to be mostly in WA and Qld. Loss rates are 3 basis points. In their “stressed” scenarios losses would rise to ~57 basis points.

They say negative equity remains low based on dynamic calculations using Australian Property Monitors data. Not clear at what level data is applied.

Looking at the segments:

Consumer cash earnings were $3,288, 4% lower due to a decline in non-interest income and increased impairment charges. Mortgage lending increased 1% and deposits rose 2%. Net interest margin was down 3bps due to lower mortgage spreads from increased competition and lower interest only lending.

Business cash earnings were $2,431 and performance was impacted by notable items ($270 million after tax). Excluding these items, cash earnings were $60 million or 2% lower from a reduction in non-interest income and higher regulatory related costs. Deposits rose by 3% over the year. Non-interest income was down 11%, mainly due to provisions as well as lower wealth income from new platform pricing and product mix changes.

Westpac Institutional Bank cash earnings was $1,014. Lower cash earnings were primarily due to a $78 million movement in derivative valuation adjustments, no contribution from Hastings and a $62 million turnaround in impairment charges. (2019 impairment charge of $46 million). In FY18, Hastings contributed $203 million to non-interest income, $158 million to expenses and $29 million to tax.

Westpac New Zealand was the brighter spot, with cash earnings ($NZ) of 1,042 3 (12) Cash earnings growth was supported by a gain on the sale of Paymark and a $10 million impairment benefit. Loans increased 5% with growth evenly spread across mortgage and business lending, while deposits also grew 4%. RBNZ gaave their NZ IRB model the tick today, after 18 months remediation!

The CEO Brian Hartzer said:

We expect system credit growth in the year to September 2020 to lift from 2.7% this year to 3%. That will be largely driven by housing where we expect a lift from 3.1% to 3.5%, although business credit growth is expected to slow somewhat from 3.3% to 3%.

By my calculations, that would not be sufficient to reverse Westpac’s decline.

Westpac New Zealand Limited (Westpac) has retained its

accreditation as an internal models bank following completion of an extensive

remediation process required by the Reserve Bank.

In 2017 the Reserve Bank

required Westpac to undertake an independent review of its compliance with

internal models obligations. The review found that Westpac was using a number

of unapproved models and that it had materially failed to meet requirements around

model governance, processes, and documentation.

The Reserve Bank imposed a

precautionary capital overlay in light of the regulatory breaches, and gave

Westpac 18 months to remedy the failures or risk losing its accreditation as an

internal models bank.

Deputy Governor Geoff

Bascand says that following the remediation process, Westpac is now operating

with peer-leading processes, capabilities and risk models in a number of areas.

“Westpac has taken the

findings of the independent review as an opportunity to make meaningful

improvements to its risk management, and we commend it for its co-operative and

constructive engagement in working with Reserve Bank over the remediation

period.

“The changes that Westpac

has made to its internal processes, governance and resourcing, as well as a

suite of new credit risk models for which it has sought approval, have given us

confidence in its capital modelling and compliance and satisfied us that it now

meets the internal models bank standard.

“Looking forward, we will continue

to hold all internal model banks to the same high standards.”

Internal models banks are

accredited by the Reserve Bank to use approved models to calculate their

regulatory capital requirements. Accreditation is earned through maintaining

high risk management standards, and comes with stringent responsibilities for

the bank’s directors and management.

Banks are required to

maintain a minimum amount of capital, which is determined relative to the risk

of each bank’s business. The way that risk is measured is important for

ensuring that each bank has an appropriate level of capital to absorb large and

unexpected losses.

The Reserve Bank will amend

Westpac’s conditions of registration from 31 December to remove the two

percentage point overlay applying to its minimum capital requirements.

As a condition of retaining

its accreditation Westpac will need to satisfy several ongoing requirements,

which it has committed to resolving, Mr Bascand says.

It would be nice if the “facts” being thrown around in the debate over the Cashless Debit Card were peer-reviewed, or even just evidence-based. Via The Conversation.

Instead, there are anecdotes. And it’s these that are being used to justify the government’s decision to spend A$128.8 million

over four years continuing the existing trial of the cashless debit

card in five sites in Western Australia, Queensland and South Australia

and extending it to Cape York and all of the Northern Territory.

The cashless card was recommended to Prime Minister Tony Abbott in a report from mining billionaire Andrew Forrest in 2014. He initially called it the “Healthy Welfare Card”.

It wasn’t a new idea. Some A$1 billion dollars had already been spent

on income management programs in the past, many of which had failed to meet their stated objectives.

The biggest was the Basics Card introduced as part of the 2007 Northern Territory Emergency Response (the “Intervention”) which was only made possible through the suspension of the Racial Discrimination Act.

Research published by the Australian Research Council funded Life Course Centre of Excellence found its introduction was correlated with negative impacts on children, including reductions in birth weight and school attendance.

It points to several possible explanations, including increased

stress on mothers, disrupted financial arrangements within households,

and confusion about how to access funds.

The government has not addressed these serious issues. Instead, it

now seeks to place those who have been left on the basics card for over

ten years now, on to the cashless debit card.

What was ‘Basics’ has become ‘Indue’

The 2016 Indue Cashless Debit Card.

indue.com.au

The “Indue” Cashless Debit Card trials underway since 2016 direct 80% of each payment to the card (Forrest asked for 100%)

where it can only be spent on things such as food, clothes, health

items and hygiene products. Purchases of alcohol and withdrawals of cash

are not permitted.

The trials are compulsorily for everyone living in the trial sites

receiving a disability, parenting, carer, unemployment or youth

allowance payment.

My own research in the East Kimberley found it makes those people’s lives harder.

Those targeted are a broad group needing support for a broad range of

reasons, yet all are treated as if they have issues with alcohol or

drugs or gambling.

Most of the people on it do indeed have a common problem: that is

trying to survive on meagre payments in remote environments with a

chronically low supply of jobs.

Of all the claims made for the card, the least believable is that it gets its users into jobs.

What it does do is limit access to cash needed for day to day-to-day

living. It makes it hard to buy second-hand goods, transport and (at

some outlets) food, and can make living more expensive.

For anyone actually struggling with addiction, it can’t substitute for treatment, a concern raised by medical specialists.

While the government says the trials have been community-led, in

reality consultation has been limited to a small group of people not

subject to the card.

When leaders in the East Kimberley who had agreed to the card withdrew their support, the government continued with the trial.

Profiting from the Cashless Debit Card has been Indue, a private company whose deputy chairman up until 2013 is now the present President of the National Party, Larry Anthony.

Indue’s involvement is helping to create a two tiered banking system

in which most people have a choice of financial providers, but those

subject to the card are restricted to one, which provides a very

different product to the others.

Indue is also not a member of the Australian Banking Association, and

so is not bound by the consumer protection provisions of its Banking Code of Practice.

The inquiry is due to report next week. Given the expensive and harmful consequences of the trial, it ought to find the extension is not justified. There are better ways to spend $128.8 million that would actually help vulnerable Australians.

Author: Elise Klein (OAM), Senior Lecturer in Development Studies, University of Melbourne

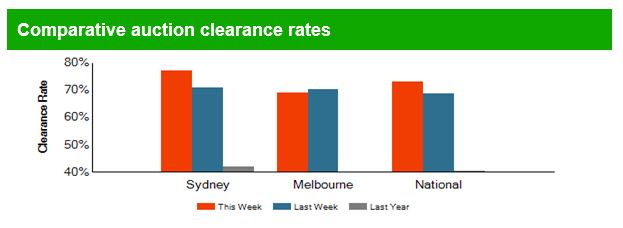

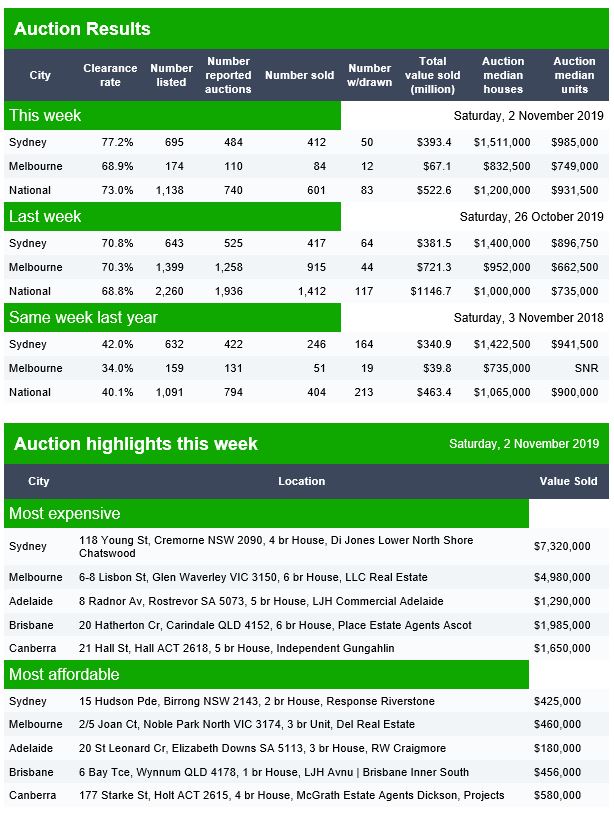

Domain released their preliminary results for today.

The latest data continues the story of high clearance rates, though on relatively low volumes (and the weekend before the big race on Tuesday), hence low counts in Melbourne.

Canberra listed 66 auctions, reported 50 and sold 42, with 2 withdrawn and 8 passed in, giving a Domain clearance of 81%

Brisbane listed 121 auctions, reported 54 with 32 sold and 11 withdrawn and 22 passed in, giving a Domain clearance of 49%.

Adelaide listed 82, reported 42, sold 31 with 8 withdrawn and 11 passed in, giving a Domain clearance of 62%

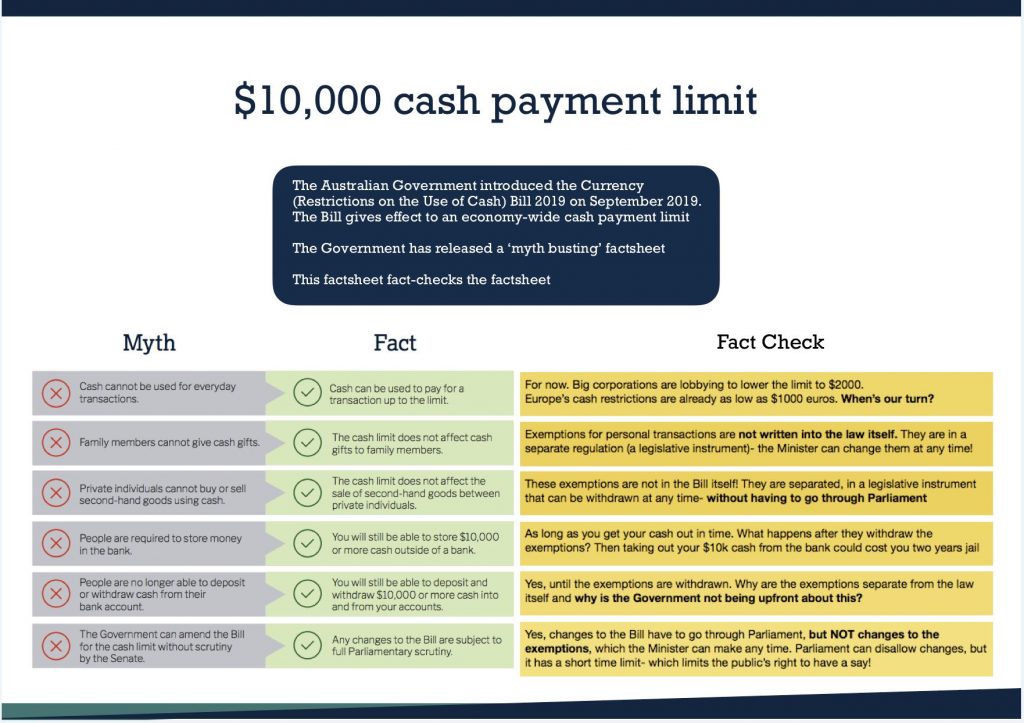

There is still time to make a submission, and stop this from becoming law. Our civil liberties depend on it.

Here’s how you make a submission: email economics.sen@aph.gov.au

Address to: Senate Standing Committees on Economics, PO Box 6100, Parliament House, Canberra ACT 2600

Some points to consider:

Civil liberties – cash is legal tender and you have the right to privacy and to not use a bank; you don’t want government and banks to “monitor and measure” everything you do.

Practical benefits of cash – power supplies and communications technology not always reliable; instant settlement of payments so can be better for commerce, good for discounts etc; whatever else.

Excuses for the law are false. Eliminating the black economy is a lie and won’t work: Australia’s black economy is small and shrinking, and cash restrictions have not reduced black economies in Europe, in fact the opposite.

Restricting cash won’t stop tax evasion, because the majority of evasion is done by large corporations and bank, assisted by the Big Four accounting firms – who want this ban. As Andrew Wilkie said, the government has enough laws to crack down on money laundering and the black economy – use them.

Real reason is to trap Australians in banks. This is explicit from the IMF: Cashing In: How to Make Negative Interest Rates Work. Won’t be able to escape negative interest rates, or bail-in.

Finally, government’s reassurances are fake, not guarantees. Treasury issued a fact sheet, which Melissa Harrison quickly refuted: exemptions aren’t contained in the legislation, just in the regulation that is easily changed.

The US Consumer Financial Protection Bureau, Federal Reserve Board, and Office of the Comptroller of the Currency today announced that the threshold for exempting loans from special appraisal requirements for higher-priced mortgage loans during 2020 will increase from $26,700 to $27,200.

The threshold amount will be effective January 1, 2020, and is based

on the annual percentage increase in the Consumer Price Index for Urban

Wage Earners and Clerical Workers (CPI-W) as of June 1, 2019.

The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010

amended the Truth in Lending Act to add special appraisal requirements

for higher-priced mortgage loans, including a requirement that creditors

obtain a written appraisal based on a physical visit to the home’s

interior before making a higher-priced mortgage loan. The rules

implementing these requirements contain an exemption for loans of

$25,000 or less and also provide that the exemption threshold will be

adjusted annually to reflect increases in the CPI-W. If there is no

annual percentage increase in the CPI-W, the agencies will not adjust

this exemption threshold from the prior year. However, in years

following a year in which the exemption threshold was not adjusted, the

threshold is calculated by applying the annual percentage change in

CPI-W to the dollar amount that would have resulted, after rounding, if

the decreases and any subsequent increases in the CPI-W had been taken

into account.

Australians in dispute with their

bank, insurance provider, super fund, or other financial firms have lodged

73,000 complaints with the financial sector’s new ombudsman and have been

awarded $185 million in compensation, in the first 12 months of its operation.

The Australian Financial Complaints Authority (AFCA) is celebrating 12 months since it opened its doors as the nation’s one-stop-shop for complaints about financial firms, replacing three former external dispute resolution schemes.

People made 73,272 complaints to

AFCA between 1 November 2018 and 31 October 2019. This represents a 40 percent

increase in complaints received compared to AFCA’s predecessor schemes, which

in the 2017/18 financial year received a combined total of 52,232 complaints.

Of the complaints made, 56,420 have

been resolved with the majority resolved in 60 days or less.

Research conducted in July this

year showed that just three percent of Australians knew about AFCA. Yet,

despite the need to raise awareness, Australians are making nearly 200

complaints a day.

AFCA Chief Executive Officer and

Chief Ombudsman David Locke said AFCA was a fair, free and independent service

that was fast becoming valued by the public and its members for its approach to

dispute resolution.

“Every day we continue to hear from

people who are dissatisfied with the way their financial firm has handled their

complaint. These matters have not been resolved internally by financial firms

and so the individual then brings their complaint to AFCA,” Mr Locke said.

“We take our commitment to fairness

and independence very seriously, and where possible we encourage the financial

firm and complainant to resolve the matter among themselves. The statistics

show that this happened with 70 percent of all claims resolved in the past 12

months.

“Still, the increase in complaint

numbers we are witnessing at AFCA indicates that there is still work to be done

by firms to improve their practices and restore public faith in financial

firms. AFCA will continue to focus on member engagement to help firms to

enhance their own internal dispute resolution procedures.”

Mr Locke said he was proud of the

significant milestones that AFCA and its people had achieved in its first year

of operation.

“Establishing AFCA as a new

organisation and handling a 40 percent increase in complaints was never going

to be easy and we are still improving the way we operate,” he said.

“I am very proud of the AFCA team

and what has been achieved so far. I am fortunate to work with a great team of

people who are professional, passionate about fairness and independence, and

who care about our customers.

“AFCA has also been in a major growth

phase of staff to meet demand and has launched the first leg of a national

roadshow to promote its service across the country.

“The Financial Fairness Roadshow

has been a great success. So far we’ve been to 26 locations across Tasmania,

Victoria, the ACT and regional New South Wales, where we’ve spoken with more

than 7,000 people.

“We plan to tour the rest of the

country in the first half of 2020.”

Mr Locke said AFCA had also hosted

forums for small business, consumer advocates and AFCA members in 10 locations

coinciding with the Roadshow’s itinerary.