The REINZ published their August 2019 report, which says the number of residential properties sold across New Zealand in August decreased by -6.1% from the same time last year to 5,959 (down from 6,346), the lowest level of sales for 7 months.

For New Zealand excluding Auckland, the number of properties sold decreased by -6.9% when compared to the same time last year (to 4,198 down from 4,509).

In Auckland, the number of properties sold in August decreased by -4.1% year-on-year (to 1,761 down from 1,837) the lowest in 4 months.

Breaking this down showed volumes actually only fell in Auckland City (-14.0%), North Shore City (-13.0%) and Manukau City (-5.4%). Whereas they increased by 43.0% in Papakura District, 16.2% in Franklin District, 13.8% in Rodney District and 0.4% in Waitakere City showing how mixed the Auckland region is.

Median house prices across New Zealand increased by 5.5% in August to $580,000, up from $550,000 in August 2018. These results are in line with the REINZ House Price Index (HPI) which saw property values increase 2.9% annually.

Median price increases for New Zealand excluding Auckland were even stronger, increasing by 9.5% to new record high of $498,000, up from $455,000 in August last year.

Median house prices in Auckland fell by -3.5% to $820,000 – down from $850,000 at the same time last year.

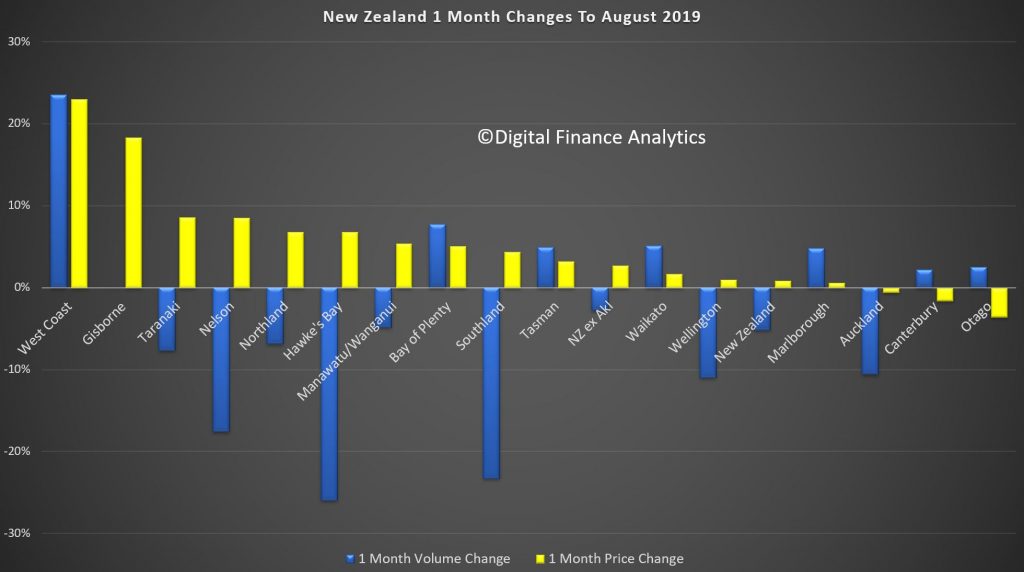

Here are the un-adjusted movements over the past month, sorted by price changes.

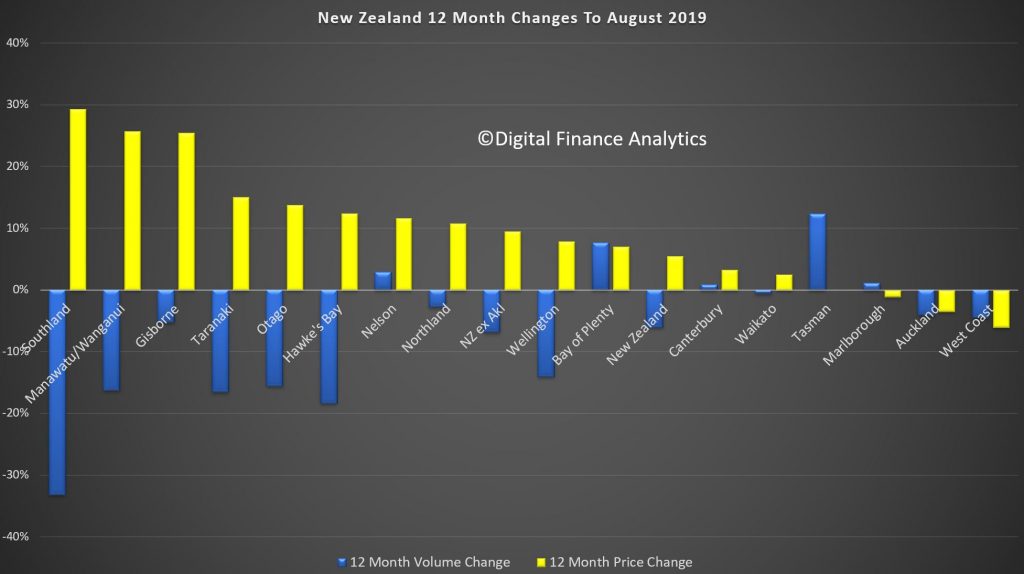

And here are the same compared with 12 months ago.

In August the median number of days to sell a property nationally increased by 2 days from 37 to 39 when compared to August last year. However, this was down 1 day on last month’s figure of 40 days.

For New Zealand excluding Auckland, the median days to sell increased by 2 days from 35 to 37.

Auckland also saw the median number of days to sell a property increase by 2 days from 42 to 44 when compared to the same time last year.

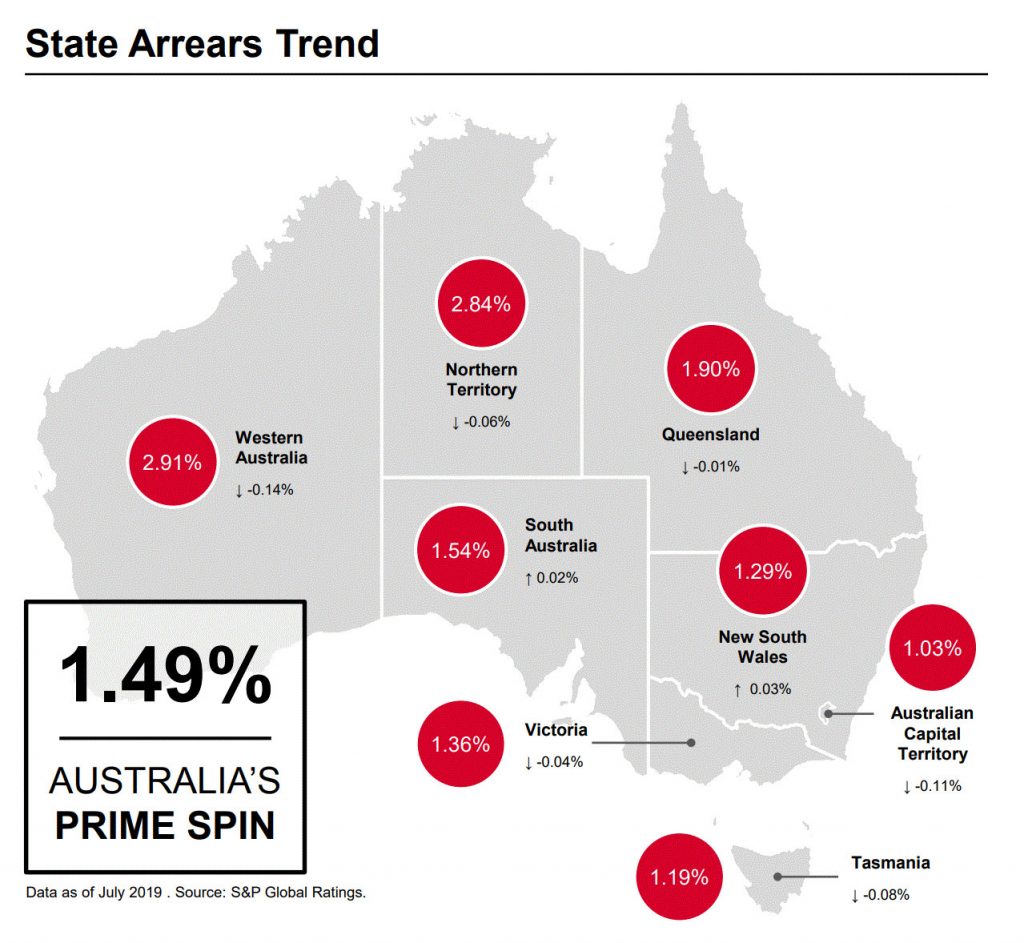

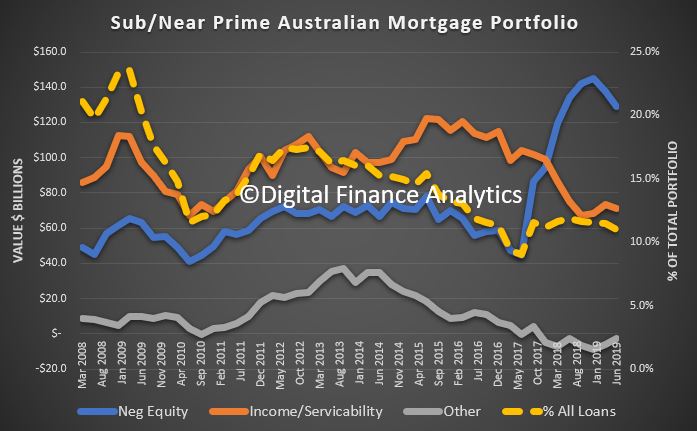

Australian prime home loan arrears fell in July in all states except NSW and South Australia, but they remain above their five-year average, new data from Standard & Poor’s has shown, via The Adviser.

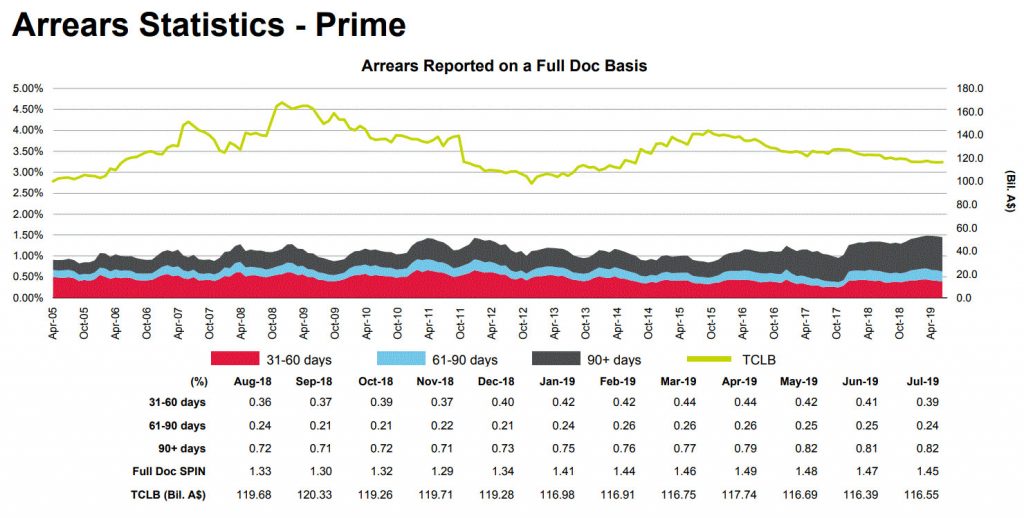

The Standard & Poor’s Performance Index (SPIN) for Australian prime mortgages dropped to 1.49 per cent in July 2019, down from 1.51 per cent a month earlier, S&P Global Ratings’ recent RMBS Arrears Statistics: Australia report showed.

According to the data, which measures

the weighted average of residential mortgage loans that are more than

30 days past due in publicly and privately rated Australian RMBS

transactions, prime arrears typically drop in spring and are expected to

decline during the third quarter of the year.

However, while the arrears index dropped month-on-month, the data showed that arrears were 11 basis points higher than they were in July 2018 and remain above their five-year average of 1.25 per cent.

Looking at arrears on a national

level, arrears improved in six states and territories, with NSW and

South Australia showing an uptick in arrears.

NSW saw an increase to 1.29 per cent, while South Australia saw arrears rise to 1.54 per cent in July 2019.

Western Australia recorded the largest drop in arrears during July, with the rate decreasing 14 basis points to 2.91 per cent.

According to S&P, the majority of

this improvement was for loans 30-60 days in arrears. Loans more than

90 days in arrears, however, continued to increase in the western state.

Owner-occupier arrears improved in July, falling by 3 basis points to 1.71 per cent.

However, investor arrears remained mostly unchanged in July, falling by 1 basis point to 1.46 per cent from the previous month.

According to S&P, this partly reflects the “generally tighter lending conditions for investors in the current environment”.

“We expect arrears to continue to

decline as the recent rate cuts filter through. These improvements are

likely to be seen in the earlier arrears categories, which are more

sensitive to interest-rate movements. We expect longer-dated arrears to

remain elevated in a softer economic environment,” S&P analysts

stated.

“Recent rises in housing finance

approvals could bolster refinancing conditions, which started to improve

in July, rising 5.4 per cent in seasonally adjusted terms. This will

help to stabilize arrears and prepayment rates if the current momentum

continues because refinancing is a common way for borrowers to

self-manage their way out of arrears.”

RBA on the rising arrears rate

The level of mortgages past due has been noted in recent months, with the Reserve Bank of Australia’s head of financial stability, Jonathan Kearns, noting in June

that the number of people in arrears on their home loans had reached

the highest level recorded since the global financial crisis.

In an address to the 2019 Property

Leaders’ Summit in Australia in June, Mr Kearns discussed the factors

contributing to the continual rise in home loan arrears.

Mr Kearns claimed that “cyclical

upswings” in arrears were attributable to weak economic conditions,

which include falling or stagnant wages and softness in the housing

market – which may inhibit some borrowers from selling their property to

ease their mortgage burden.

The head of financial stability also

acknowledged that tighter lending standards can conversely impact a

borrower’s ability to meet their mortgage repayments, pointing to

previous restrictions on interest-only lending, which prevented

borrowers from rolling over the interest-only period.

Mr Kearns also conceded that tighter serviceability measures may prevent distressed borrowers from refinancing their loan, cited by S&P as one of the factors contributing to the rise in delinquencies.

However, Mr Kearns pointed to

internal data collected by the Reserve Bank, which suggested that the

application of tighter lending standards has been “effective” in

improving credit quality.

Mr Kearns said at the time that he expected the overall arrears rate to continue rising, but he claimed the trend would not pose a significant threat to financial stability.

“To the extent that we can point to

drivers of the rise in arrears, while the economic outlook remains

reasonable and household income growth is expected to pick up, the

influence of at least some other drivers may not reverse course sharply

in the near future, and so the arrears rate could continue to edge

higher for a bit longer,” he said.

“But with overall strong lending

standards, so long as unemployment remains low, arrears rates should not

rise to levels that pose a risk to the financial system or cause great

harm to the household sector.”

The Reserve Bank of New Zealand (RBNZ) and Financial Markets

Authority (FMA) today released their findings on life insurers’ responses to

the joint Conduct and Culture Review.

Overall, the regulators were

disappointed by the responses. Significant work is still needed to address the

issues of weak governance and ineffective management of conduct risk,

identified in the regulators’ report earlier this year.

Rob Everett, FMA Chief

Executive, said: “While we’re disappointed, we’re not surprised as the

responses confirm what we found in our original review. It’s clear that

progress has been slow and not as far-reaching as required.

Some providers have started

work to identify the customer and conduct issues they face, others have not

provided any detail on this.”

Sixteen life insurers were

asked to provide work plans outlining the steps they will take to improve their

existing processes and address the regulators’ findings and recommendations.

There was wide variance in

the comprehensiveness and maturity of the plans provided.

Adrian Orr, Reserve Bank

Governor, said, “We’re disappointed the industry’s response has been

underwhelming. The sector has failed to demonstrate the necessary urgency and

prioritisation, around investment in systems, to provide effective governance

and monitoring of conduct risk.”

There was also a wide

variance in the quality and depth of the systematic review of policyholders and

products. Some did not complete this exercise and others did not provide data

on the number of policyholders affected or the estimated cost of remediation

activities. Insurers that completed the exercise identified at least 75,000

customer issues requiring remediation, with a value of at least $1.4 million.

Some of the new issues identified included:

Overcharging of premiums and benefits not being updated due to system errors, human errors and under-reporting of deaths

Poor customer conversations overlooking eligibility criteria and poor post-sale communications, which lead to declined claims and underpayment of benefits

Poor value products were identified, where premiums charged were not fair value for the cover provided.

Sales incentives and

commissions

The FMA and RBNZ committed

to report back on staff incentives and commissions for intermediaries. Previous

reports by the FMA reflected the concerns with conflicted conduct associated

with high up-front commissions and other forms of incentives, (like overseas

trips) paid to advisers.

Although some insurers have

committed to removing sales incentives for employees and their managers, not

all committed to removing or altering indirect sales incentives.

Those providers that have

removed sales incentives for employees don’t typically use external advisers to

distribute products. Providers using external advisers told the regulators that

changing long-held business arrangements and distribution models is difficult

and will take time to implement.

Mr Everett said, “We’re

ready to work with life insurers to ensure they prioritise their focus on

serving the needs of their customers, while at the same time balancing the need

to remunerate advisers for the important work they do to help these customers.

But we do not think high up-front commissions create confidence that insurers

and advisers are acting in the best interests of customers.”

Mr Orr said, “Good

governance within insurance firms requires the effective management of conflicts

of interest. We need to see much better systems and controls in place to manage

the inherent conflicts where advisers or sales staff are offered incentives to

sell or replace insurance policies.”

Next steps

Those companies that have

not undertaken comprehensive systematic reviews of policyholders and products

have been asked to complete further reviews of their systems to identify

issues, and to develop mature plans to respond and remediate any of their

findings. These plans must be completed by December 2019.

The FMA and RBNZ will

continue to monitor how the insurers are responding to recommendations and

implementing their work plans. Life insurers are currently not legally required

to become more customer-focused and the FMA and RBNZ found that the sector has

a weak appetite for change.

Deficiencies in some of the

plans received, and some insurers’ lack of commitment to implementing the

regulators’ recommendations, further demonstrates the need for additional

obligations to be included in the regulation of conduct of life insurers.

“This is a bit controversial, we know that,” deputy prime minister Michael McCormick told the National Party’s federal council, which on the weekend voted for a national roll-out of cashless debit cards for anyone younger than 35 on the dole or receiving parenting payments. From The Conversation.

The Nationals have joined the chorus within the federal government proclaiming the cards a huge success.

The Minister for Families and Social Services, Anne Ruston, has even gone so far as to claim welfare recipients are “singing its praises”.

Really?

Both McCormick and Ruston have proclaimed success based on the most

recent trial of cashless welfare in Queensland. This trial began barely

six months ago, and the independent evaluation by the Future of Employment and Skills Research Centre at the University of Adelaide is ongoing.

A more complex story emerges out of my research into lived

experiences of the first cashless debit card trial, which began in

Ceduna, South Australia, in March 2016

I spent about three months in the town of Ceduna between mid 2017 and the end of 2018 talking to people about life on the card.

Ceduna is located on the north-west coast of Eyre Peninsula, South Australia.

www.shutterstock.com

All communities are diverse and people’s experiences diverge. Some

liked the card, or had come to accept it, others were caught up dealing

with far more significant problems.

But I talked to people who found the card “an insult”. They told me

it made them feel “targeted” and “punished”. They talked of degradation

and defiance. They also told me the card didn’t work.

As for the the claim by both Ruston (and her ministerial predecessor Paul Fletcher)

that the card empowers people to “demonstrate responsibility”, the

opposite was true. In the words of June*, an Indigenous grandmother,

foster carer and talented artist: “It has taken responsibility away from

me. It’s treating me like a little kid again.”

Indigenous testing grounds

Ceduna, in the far west of South Australia, was the first of four

sites chosen to trial cashless debit cards. The second was in the East

Kimberley

The location of these two trial sites meant early trial participants

have been predominately Indigenous. I am of the view that Indigenous

communities are being used as testing grounds for new technologies and

controversial measures.

The BasicsCard, introduced in 2007.

AAP

In the first two trial sites, income support recipients younger than

65 have just 20% of their payment deposited into their bank account. The

remaining 80% goes on to their debit card, which cannot be used at any

alcohol or gambling outlet across the nation. Nor can they be used to

withdraw cash.

The lead-grey cashless debit card is similar but different to the

lime-green BasicsCard, introduced as part of the 2007 Northern Territory

National Emergency Response (the “Intervention”). The use of the

BasicsCard as an “income management” tool was extended to non-Indigenous

people in the Northern Territory in 2010, and to other states in 2012.

The BasicsCard generally quarantines 50% of a social security

recipient’s income so that it cannot be spent on alcohol, gambling,

tobacco or pornography. BasicsCard holders need to shop at approved

stores. In contrast, the cashless debit card, administered by financial

services company Indue, can theoretically be used wherever there are Eftpos facilities.

Shame and humiliation

My research wasn’t based on collecting statistics but “hanging out”

and getting to know people. I came to see the stigma associated with the

“grey card” sometimes resonated with past experiences.

Robert*, for example, told me about growing up on a mission and then

suddenly finding himself as “one little blackfella” in a large high

school. He was acutely sensitive to the “smirks” and judgements of

others whenever he used the grey card to pay for things.

Pete* left high school after a couple of weeks to join an itinerant

rural workforce that has since vanished. After decades of manual work,

finding himself unemployed due to ill health was devastating enough.

Being issued the grey card compounded his humiliation.

Others voiced their belief the grey card was designed to induce

shame. But they refused that shame, expressing instead a defiant belief

in the legitimacy of their need for support.

The welfare system often defines people by the one thing they are not

currently doing – waged employment. But many people I spent time with

in fact laboured constantly: it just wasn’t recognised as work. People

like June*, for example, looked after sick kin, the elderly and

children. Yet the grey card treated them as dependents.

I heard about ways of getting around the card’s restrictions. As one

acquaintance put it: “Drunks gonna drink!” One strategy involved

exchanging temporary use of the card for cash. With terms that nearly

always disadvantage the card holder, it has the potential to make life

tougher for people living in hardship.

The evaluation of the Ceduna trial for the Department of Social Services

was more positive, noting that alcohol drinkers and gamblers reported

doing so less frequently. But it also noted no reduction in crime

statistics related to alcohol consumption, illegal drug use or gambling.

And the Australian National Audit office was so critical of the

government’s evaluation it concluded

that it was difficult to ascertain “whether there had been a reduction

in social harm” as a result of the card’s introduction.

Which makes simplistic claims about the card’s success look a bit rich.

Author: Eve Vincent, Senior Lecturer, Macquarie University

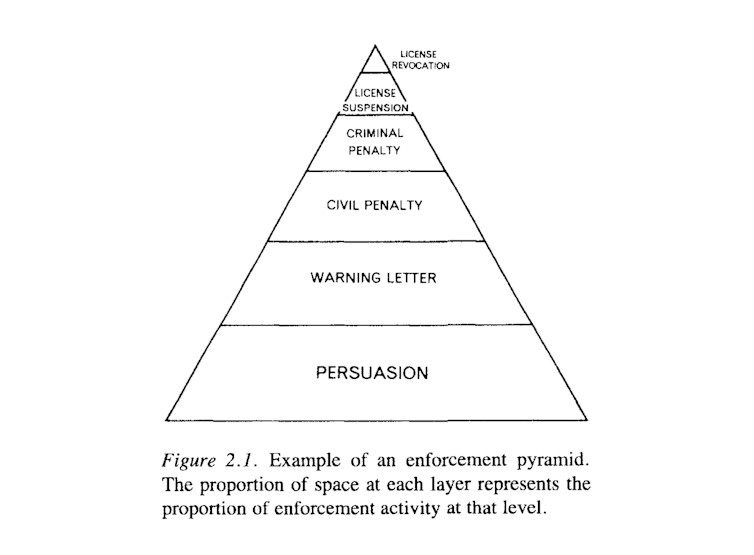

British health-care conglomerate Bupa runs more nursing homes in Australia than anyone else. We now know its record in meeting basic standards of care is also worse than any other provider. Via The Conversation.

This is more than a now familiar story of a corporation putting

shareholders before customers. It is also about another abysmal design

failure in regulation.

Health care is meant to be one of our most regulated sectors. In this

case, Bupa’s facilities were inspected and certified by the Aged Care

Quality and Safety Commission.

The regulator’s inspectors found 45 of Bupa’s 72 nursing homes

failed health and safety standards. In 22 homes the health and safety

of residents was deemed at “serious risk”. Thirteen homes were

“sanctioned” – with government funding being withheld and the homes

banned from taking new residents.

Yet none of this appears to have spurred Bupa’s management into action, according to media reports.

Flurries of inspection reports and written warnings over months and

years only underlined that the regulatory tiger, even if it had teeth,

had a very soft bite.

Responsive regulation

We have seen examples of equally insipid regulation in other areas.

In the building sector, for example, a range of regulatory flaws

including outsourced building certification have led to shoddily built and dangerous apartment construction.

In the financial sector, the banking royal commission castigated the

industry regulators – the Australian Securities and Investments

Commission and the Australian Prudential Regulatory Authority – for

their unwillingness to enforce rules.

“The conduct regulator, ASIC, rarely went to court to seek public denunciation of and punishment for misconduct,” noted royal commissioner Ken Hayne. “The prudential regulator, APRA, never went to court.”

This failure is due to more than individual agency shortcomings. It’s

an unintended consequence of the design of “responsive regulation” –

the system that has superseded command-and-control regulation over the

past three decades.

Responsive regulation was popularised by Australian sociologist John

Braithwaite and American law professor Ian Ayres in the early 1990s. It

was intended to overcome the pitfalls of the command-and-control model,

which involved regulators employing large numbers of inspectors to look

for non-compliance.

From about the 1970s it had become increasingly evident this model

wasn’t working. It was also very expensive. Consider, for example, the

cost of having fire and health and safety inspectors visit every single

building site, particularly when most builders were doing the right

thing. The cost and intrusiveness of the system fuelled calls to do away

with regulation .

Too big to fail

Ayers and Braithwaite saw their model as a way forward.

“Responsive regulation is not a clearly defined program or a set of prescriptions

concerning the best way to regulate,” they explained. “On the contrary, the best strategy is shown to depend on context, regulatory culture and history.”

Responsive regulation assumes that in most cases the enterprises

being regulated are interested in compliance and will respond to

light-touch directives. It assumes that often compliance failures are

due to ignorance or inadequate procedures. Its approach is to give

parties a chance to amend their ways.

But there’s a potentially huge flaw in the responsive regulation

model. What happens when an organisation is so large it is deemed too

big to fail, or deems itself so?

This seems to have been the case with a number of financial companies

whose misdeeds were exposed by the banking royal commission. It seems

it might have been the case with Bupa.

In such cases, because of the timidity of the regulator or the

confidence of the enterprise, the warnings might just go on and on. The

company continues to book its profits – which may well eclipse any

penalty it might have to pay if crunch time does ever come.

Markets have their limits

This design flaw highlights a more fundamental problem with

governments positioning themselves as rule makers and leaving the rest

to the “market”.

Markets are designed to facilitate exchange on the basis of profits.

The profit motive means market participants look for the lowest-cost

option. In aged care this means paying the lowest possible wages,

possibly to unqualified staff, and cutting corners to cut costs.

Markets are very useful for increasing individual choices and

efficiently allocating resources, but they are not suited to every task.

They fail when factors other than profit ought to be considered.

We therefore need to think about the design of regulatory systems more holistically, as part of a broader social process.

The pioneers of responsive regulation certainly understood this. They

emphasised flexibility, taking into account context, culture and

history.

What those three things now tell us, given widespread regulatory failure across industries, is that government should not resist stepping in to provide important public services where the private sector cannot or will not do so at an acceptable level. Nor should it be afraid to act through empowered regulators, with ressources and powers to fulfil their mandates.

Author: Author: Benedict Sheehy, Associate professor, University of Canberra

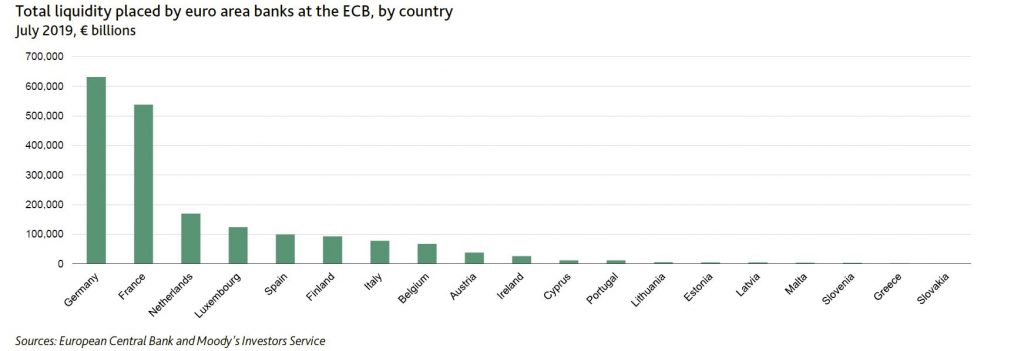

On 12 September, the European Central Bank (ECB) announced that it will introduce a two-tier system for banks’ reserve remuneration, exempting a portion of deposits in excess of the minimum reserve requirement from the negative deposit facility rate and giving that portion a 0% rate instead. The introduction of the tiering system on banks’ excess liquidity placed at the central bank is credit positive, says Moody’s.

This is because it will reduce the cost of holding liquidity at the ECB, providing a partial offset. They expect that the tiering mechanism will be particularly positive for banks with material excess liquidity.

The announcement comes as the ECB’s Governing Council

announced that it would maintain its accommodative monetary policy stance given

slowing economic conditions in Europe, persistent downside risks of global

trade tensions and muted inflationary pressures. As a result, the ECB

relaunched its Asset Purchase Programme and lowered the rate on the deposit

facility by 10 basis points to negative 0.50% from negative 0.40%.

The tiering system on banks’ excess liquidity will moderate

the negative effect of persistent low rates on banks in the euro area.

The two-tier system will exempt from negative interest a

maximum volume of six times the banks’ minimum reserve requirement, therefore

paid at 0%. The minimum reserve requirement and the non-exempted portion of the

excess reserves will be charged 0.5%.

The tiering system will apply to all banks and start at the

end of October 2019.

Since the aggregated minimum reserve requirement is currently €132 billion, approximately €786 billion (six times the aggregated minimum requirement) would be exempt from negative rates. The remaining reserves and deposit facility would be subject to the new deposit rate of negative 50 basis points, providing a net annual benefit to the euro area’s banks of about €2 billion relative to the status quo of negative 40 basis points on the full balance of €1.9 trillion liquidity placed at the ECB, equivalent to 0.8% of EU banks’ annual net interest income.

In 2018, Moody’s estimate that banks’ €1.8 trillion of total liquidity placed at the central bank at a rate of negative 0.40% cost around €7 billion. This compares with US banks, whose deposits placed with the US Federal Reserve in 2018, remunerated at a rate of 2.35%, represented a revenue of around €40 billion.

The introduction of a two-tier system for banks’ reserve

remuneration will be particularly positive for German and French banks, whose liquidity

holdings exceed the most their reserve requirements and account for more than

60% of the total liquidity placed at the ECB. The tiering mechanism that the

ECB has introduced is similar to the mechanism implemented by Switzerland’s

central bank, which also set exemption thresholds for deposit rates as a

multiple of banks’ minimum reserve requirements.

Southern European banks will benefit to a lesser extent

because they do not hold large amounts of excess reserves at central banks.

However, they will continue benefiting from the third series

of targeted longer-term refinancing operations (TLTRO III). The ECB in June

2019 announced that banks could access two years of funding at 10 basis points

above the ECB’s refinancing rate of 0%. On 12 September, the ECB removed the

10-basis-point surcharge and announced that TLTRO funding would extend to

maturities of three years instead of two, conditions that will be particularly

favourable for banking systems with large outstanding repayments from previous

TLTRO programmes, such as those in Italy and Spain.

Non-bank lender Pepper Money has launched mortgage lending operations in New Zealand, offering advisers in New Zealand the technology and tools to write its prime, near-prime and specialist loans. Via The Adviser.

Following more

than a year of consultation with advisers and intermediaries, lending

partners, regulators and borrowers, Pepper Money has today (16

September) opened its business in New Zealand.

This builds on the international reach of the non-bank lending group, which already operates in Australia, the UK, Spain, Ireland and Asia.

New Zealand-born Aaron Milburn,

Pepper Money’s director of sales and distribution in Australia, will

head up the New Zealand business from today. His new job title will be director of sales and distribution for Australia and New Zealand.

Speaking to The Adviser about the new

business, Mr Milburn said that Pepper Money will primarily distribute

through the third-party channel, as it does in Australia.

Mr Milburn added that while while the

company may look to launch mortgages directly in future, “the initial

plan – and for the foreseeable future – is to utilise the adviser

network over there”.

He explained: “We will initially

distribute through the adviser network in NZ through all of the major

aggregators that operate in New Zealand.

“Pepper’s business is 95 per cent

driven through brokers in Australia and in the UK, and we see no need to

change that model as we enter NZ.”

He continued: “We think that advisers

do a wonderful job in New Zealand, and we would like to continue to

support that area of distribution as we enter NZ, as we do in

Australia.”

Mr Milburn told The Adviser that his

first priority in his expanded role will be to launch the suite of

products in New Zealand and “deliver what advisers have been asking for

at our various feedback sessions and study tours”.

According to the director of sales and distribution for Australia and New Zealand, this largely focuses around filling a “significant

gap in the near-prime space in New Zealand, where families are

potentially paying too much or have been in the wrong products due to a

lack of choice” and providing advisers with supporting tools to help

deliver these products.

He explained: “We had advisers in New

Zealand contacting Pepper asking us to go over there and really inject

some competition into the market and make it easier for advisers and,

ultimately, Kiwi families to realise their goals.”

Pepper Money will therefore also offer advisers the Pepper Product Selector (PPS)

tool in New Zealand, which will enable brokers to “get indicative

offers for their customers in under two minutes”, as well as a “fully

online integrated submission platform for brokers,” the marketing

toolkit, the social media toolkit and the Pepper Insights Roadshow.

Pepper Money to pay trail

Notably, while the majority of lenders in New

Zealand went through a “no trail” period starting in 2006 (when

payments went from 0.65 of a percentage point in upfront commission plus

0.20 of a percentage point in trail commission to an average of 0.85 of

a percentage point in upfront only), several lenders have begun returning to trail commission to reduce instances of churn.

According to Mr Milburn, Pepper Money in New Zealand will be offering advisers an upfront and trail commission.

He told The Adviser: “Overwhelmingly, the feedback was that an upfront and trail model was preferred.

“A number of banks have either

re-implemented trail in NZ or are looking to in the near future, so we

took the opportunity to put trail back into the New Zealand market with

our products.”

Mr Milburn concluded that the new operation in New Zealand would build on the practice and service offerings built in Australia.

He said: “We will continue to deliver

the level of service and solutions that we do today and continue to

really focus on that technology improvement side of things.

“We want to make it easier and faster

for brokers to provide solutions for their customers and help build

their brand out in the community and the focus will continue in the back

end of 2019 to 2020.”

The current low interest rate environment could impact the ability of smaller banks to compete against the major institutions, APRA chair Wayne Byres has cautioned, via InvestorDaily.

In an address to the European Australian Business Council in Melbourne, Mr Byres spoke on financial stability and the challenges ahead for the banking system.

The return on equity (RoE) of the Australian major banks has certainly declined but has not fallen below 10 per cent, even during the GFC, and is now in the order of 12 per cent; for large global European banks, RoE was negative at the height of the crisis, and has struggled to get much above 5 per cent since then.

Reflecting this, the price-to-book (PTB) ratio of the Australian majors averages around 1.5x, and capital is readily available; for large European banks, PTB has typically been in the order of 0.5x and new capital is therefore expensive.

In 2018, a decade after the crisis, the four Australian majors were ranked in the top 35 banks in the world by market capitalisation. Europe, despite a much larger banking system and population, only had four banks in the top 35.

All four Australian major banks enjoy AA credit ratings, and ready access to funding; very few European banks (without explicit government support) enjoy similar ratings.

He compared the experience of the Australian

market to Europe, noting local banks are having to get used to low

interest rates, as opposed to their weathered overseas counterparts.

In

Europe, where the continent’s GDP fell more than 5 per cent at the

height of the global financial crisis and didn’t make it back to 2008

levels for another five years as well as unemployment rising to 11 per

cent and only just recovering, he noted the environment has been tough.

“For

European banks, of course, it is nothing new – Europe has operated with

its interest rate on the ECB’s main refinancing operations at 1 per

cent or below since late 2011, and zero since early 2016,” Mr Byres

said.

“In

that regard, the European experience illustrates some of the challenges

potentially ahead for Australian banks. A very low interest rate

environment will see margins squeezed, adding to the headwinds from slow

lending growth.

“Profitability, and therefore capital generation,

will come under more pressure. And given their different funding

profiles, these trends may well impact smaller banks more forcefully

than larger ones, reducing the ability of the former to apply

competitive pressure to the latter. But to be clear, neither group will

welcome further rate reductions.”

He reflected on the market

around 2014-15, when APRA was concerned the banks were not responding

prudently to the environment of high house prices, high household debt,

low rates and subdued income growth.

“Speculative activity was increasingly prominent,” Mr Byres said.

“Such

an environment would, one might think, see prudent bankers trimming

their sails and battening down the hatches. Instead, intense competitive

pressures across the industry saw a tendency for standards go by the

wayside – for lenders, it was full steam ahead.”

APRA and ASIC worked to drive standards to more prudent levels, while ASIC focused on responsible lending.

“However,

it is worth remembering that the original risks we were concerned about

in 2014 – high prices, high debt, low interest rates and subdued income

growth – have not gone away, and in some cases increased,” Mr Byres

said.

“When it comes to the supply of credit, it would therefore

be unwise for lending standards to be allowed to erode again as a means

of generating lending growth. And on the demand side, it would be

unhelpful if recent (and prospective) interest rate reductions led to a

resurgence in speculative activity.”

Property expert Joe Wilkes and I discuss failed market intervention – and whether we should leave the market to be the market … rather than foist more debt on households.