Australia’s trend unemployment rate increased in July 2019 to 5.3 per cent, from 5.2 per cent in June, according to the latest information released by the Australian Bureau of Statistics (ABS).

ABS Chief Economist Bruce Hockman said: “Australia’s trend unemployment rate increased to 5.3 per cent in July 2019, the same level as this time last year.”

“The trend participation rate increased further to 66.1 per cent, while employment growth continues to show strength,” added Mr Hockman.

Employment and hours

In July 2019, trend monthly employment increased by around 24,600 persons. Full-time employment increased by 15,100 persons and part-time employment increased by 9,600 persons.

Over the past year, trend employment increased by 339,200 persons (2.7 per cent) which was above the average annual growth over the past 20 years (2.0 per cent).

The trend monthly hours worked increased by less than 0.1 per cent in

July 2019 and by 1.8 per cent over the past year. This was slightly

above the 20 year average year-on-year growth of 1.7 per cent.

Underemployment and underutilisation

The trend monthly underemployment rate remained steady at 8.4 per cent

in July with no changes over the past year. The trend underutilisation

rate decreased by 0.1 percentage points over the year.

States and territories trend unemployment rate

The trend unemployment rate remained steady in most states and

territories, except for South Australia (up 0.2 percentage points) and

Queensland and Northern Territory (up 0.1 percentage points).

Over the year, unemployment rates fell in New South Wales, Victoria,

Western Australia and the Australian Capital Territory, and increased in

Queensland, South Australia, Tasmania and the Northern Territory.

Australians are still confused about what goes into their

credit report, despite it being an important record of their credit health,

according to research by consumer education website, CreditSmart.

The CreditSmart survey found that nearly three quarters of

Australians assume their credit score is included in their credit report. One

in five mistakenly believe that marital status, income, insurance claims and

even traffic fines form part of their credit report.

Commenting on the findings, Geri Cremin, Credit Reporting

Expert at CreditSmart, said: “If you are applying

for a credit card, a personal loan or even applying to change your mobile phone

provider, your credit report can make or break your application.

Your credit report is a snapshot of your credit history and

current credit health – so lenders do look at your credit report, and you

should too.”

“Your credit report is a way for lenders to see how you

handle the credit you currently have and assess whether the credit you’re

applying for is right for you. Better still, a good credit report might open

the door to better deals.”

Who’s accessing your credit report?

How credit reports are used is also unclear to many

Australians. The majority of consumers know their credit report can be checked

when they apply for a home loan, however:

Less than 50% are aware that it can also be checked when taking out a new mobile phone contract or opening a new gas or electricity account.

Four in ten also wrongly believe their credit report is checked when applying to rent a property.

30% believe that their credit report is checked when they take out home insurance.

13% also think that a future employer checks their credit report when they apply for a job.

“By law, your credit report can only be accessed by others

in limited circumstances. For example, your credit report can’t be accessed by

a real estate agent when you apply to rent a house, an insurer when you apply

for car or home insurance or by a potential employer when you apply for a job,”

added Ms Cremin.

Aussies love credit, but feel it’s getting

harder to access

CreditSmart’s research showed that Australians are

enthusiastic users of credit, with three quarters (76%) currently using some

form of credit product.

Credit cards (56%), home loans (29%), vehicle finance

(12%), Buy Now Pay Later services (12%) and personal loans (12%) were the most

popular types of products used by Australian consumers who responded to the

CreditSmart survey.

The survey also found that four in 10 Australians think it

is harder to get credit now than it was 12 months ago. They say the reasons

are:

lenders doing tighter credit checks (57%)

tougher regulation around credit (54%) and

lenders looking at bank statements and daily expenses more closely (41%)

declining property market (22%)

“As Australians feel credit is getting harder to access,

it’s important to take charge of your individual credit health. A great first

step is to check your credit report – understand what’s on it and get on top of

your monthly repayments. Lenders look to your credit health to determine your

attractiveness as a customer, so it is important to know where your credit

health stands,” Ms Cremin said.

“We recommend checking your credit report annually and

really treat it as an asset that will help you access the right credit if and

when you need it.”

So, what is included in my credit report?

At a minimum, your credit report will include identifying

information about you, such as your name, birth date, address and employment

history.

More importantly, it includes:

A list of any applications you’ve made for credit over the last five years – regardless of whether your application was approved or not. This information is listed as an “enquiry” by the credit provider you applied to and it includes the type of credit you applied for.

A breakdown of your current credit accounts such as your home loan or credit card.

Up to 24 months of repayment history – which shows your monthly repayment behaviour on financial credit accounts (phone or utility companies do not report repayment history, so your telco and utility repayments won’t be on your credit report).

Any defaults listed by a credit provider on financial loans as well as telco and utility accounts. A default can occur if you miss your payment of at least $150 by at least 60 days. A default stays on your credit report for 5 years.

Consistent with the DFA surveys on household financial confidence the latest survey via ME Bank says:

Australian households are feeling overall worse about their net

wealth, jobs, income and living expenses with further significant

residential property price falls over the past six months and a

weakening labour market, ME’s latest Household Financial Comfort Report has revealed.

Consulting Economist for ME, Jeff Oughton, said that despite

remaining a little above the report’s seven-year average, financial

comfort across most of the 11 drivers that make up the Index fell, with

net wealth in particular seeing the largest drop, falling 3% to 5.54 out

of 10 during the six months to June 2019.

“The financial comfort of Australian households eased over the past

six months, with a significant fall seen in comfort with wealth. Despite

lower mortgage loan rates, expected cuts in personal income tax and

higher local and global equity prices, this is largely a consequence of

continued decreases in the value of residential property in many parts

of Australia,” said Oughton.

“Comfort with wealth would have fallen much more if it wasn’t for

record bond prices and rebounding share markets as well as the

Government’s retention of negative gearing on investment properties and

cash refunds for franking credits that saw household comfort with

investments increase.”

Financial comfort with investments (in financial assets, such as

shares and super, and property) was the only driver across the index to

improve (up only 1%), but was largely accrued by households with high

incomes. Households with incomes of $200k+ per annum and large

superannuation balances (above $1 million) reported increases to overall

financial comfort by 10% to 7.45 and 11% to 8.3, respectively, during

the six months to June 2019.

A weakening labour market and subdued income growth weigh on comfort

Financial comfort among households also eased as a consequence of a

weakening job market, which resulted in subdued wage growth, falling

comfort with income and high levels of both underemployment and job

insecurity.

In particular, financial comfort among working Australians

significantly deteriorated, with full-time workers recording a 3%

decrease to 5.86, part-time workers decreasing 4% to 5.1, casual workers

decreasing 1% to 5.02 and self-employed workers down 3% to 5.57.

Oughton said: “It’s clear from the latest Report that there are

increased concerns around job availability and underemployment. The

number of workers who felt it would be difficult to find a new job

increased by 16 percent to over 1 in 2 employees, which is the highest

recorded since late 2016.”

In June 2019, 35% of part-time and casual workers said they would

prefer to work more hours – seeking an additional 23 hours per week.

Meanwhile, 26% of all workers said they felt insecure in their current

job.

Households’ comfort with their incomes also fell by 1% to 5.69 in the

latest survey. Only 36% of Australian households reported an increase

in their annual income during 2018/19, falling 2 points from December

2018, and there were fewer income gains recorded across households in

general. Higher income households also continued to be much more likely

to report increased incomes during the past year.

Living costs and a lack of savings are household’s biggest financial ‘worries’

In net terms of the greatest financial ‘worries’ and ‘positives’,

cost of necessities was the most commonly cited worry in ME’s latest

report, nominated by 44% of households. This was followed by worries

about level of cash savings on hand (34%), ability to maintain lifestyle

in retirement (31%) and impact of legislative change (19%).

Looking more closely at savings, Oughton said that overall, comfort

with cash savings remained steady at 5.09 during the six months to June.

“Since the latest Federal Budget was announced, households, on

average, have slightly increased their precautionary savings. However,

this saving behaviour was predominantly among those with a smaller

amount of cash savings, and in contrast, those 10% of households

reportedly spending more than their monthly income are overspending by

more each month (up 18% in dollar terms).”

Oughton also noted that about 40% of households continued to spend all their monthly income.

When asked about retirement, the anticipated standard of living in

retirement has eased, falling 1% to 5.2, and notwithstanding a rise in

the comfort of households expecting to self-fund their retirements (up

to 7% to 7.31).

Furthermore, of all 11 components that make up the financial comfort

index, Australians still felt the least comfortable with their ability

to cope with a financial emergency, which fell slightly by 1% to only

4.77 out of 10. Indeed, 20% of households said they didn’t think they

could raise $3,000 in an emergency.

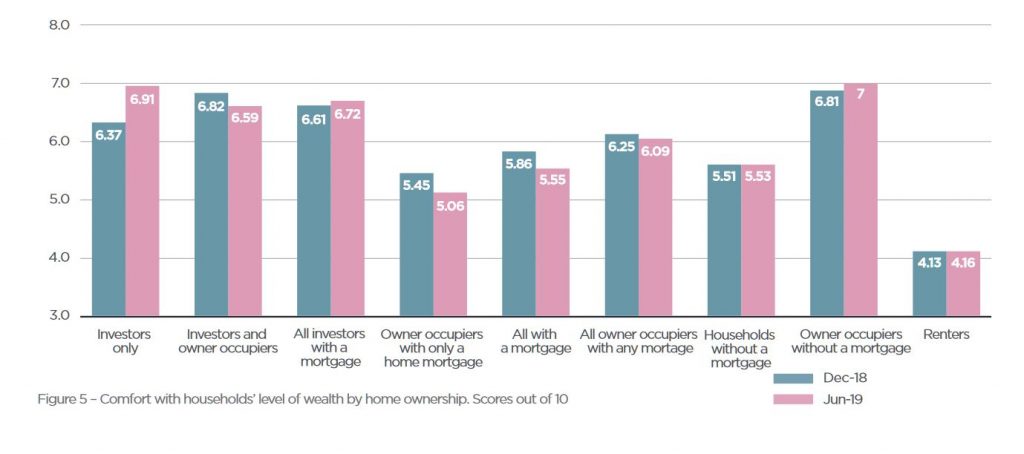

Residential property price correction a drag, but most households increasingly optimistic for 2019/20

While the residential property price correction has negatively

impacted wealth, comfort by housing tenure has been mixed over the past

six months. The Report reveals that comfort has lessened among both

homeowners with a mortgage and renters, which could be attributed to

tightening in the availability of credit, continued housing

unaffordability, and high housing debt and rental payment stress. In

contrast, comfort has risen amongst those who own their home outright

and geared property investors post-Federal election, with negative

gearing retained on investment properties.

Oughton said: “It’s evident that despite the latest monetary policy

changes, there remains high levels of housing debt worry and actual

payment stress among Australians.”

“The number of households contributing more than 30% of their

disposable income towards paying off a mortgage has remained steady at

about 43%, while the corresponding figure for renters has risen to 62% –

partly reversing the improvement reported in the previous two surveys.”

In contrast to the actual fall in dwelling prices during the past 12

months, the majority of households living in their homes and investment

property investors are feeling even more positive than six months ago

about the 12-month outlook for dwelling prices.

In fact, over 41% of households living in their homes expect their

dwelling prices to rise during 2019/20, while only 11% expect the value

of their home to fall (including only 3% who are expecting a large

fall).

However, the expectations of higher home values amongst

owner-occupiers varies significantly across major capital cities, with a

significant rise in Brisbane (46%), Sydney (45%) and Melbourne (42%) –

in comparison to Perth (25%).

Investors are relatively more optimistic than owner-occupiers, albeit

less so than six months ago: 46% of investors expect the value of their

investment properties to rise during the next 12 months, while only 9%

anticipate a fall (including 2% who anticipate a large fall). Investors

in Sydney are the most optimistic about property values (with 54% of

investors expecting rises and only 6% expecting a fall), followed by

investors in Brisbane (50%) and in Melbourne (44%).

Oughton summarised the key winners and losers from ME’s 16th Household Financial Comfort Report:

Winners:

Households not reliant on the government aged pension in their retirement

Households with super balances (greater than $1 million) – financial comfort up 11% to 8.3

Young and middle-aged singles/couples with no children

Geared investors in residential property markets – financial comfort up 8% to 6.9

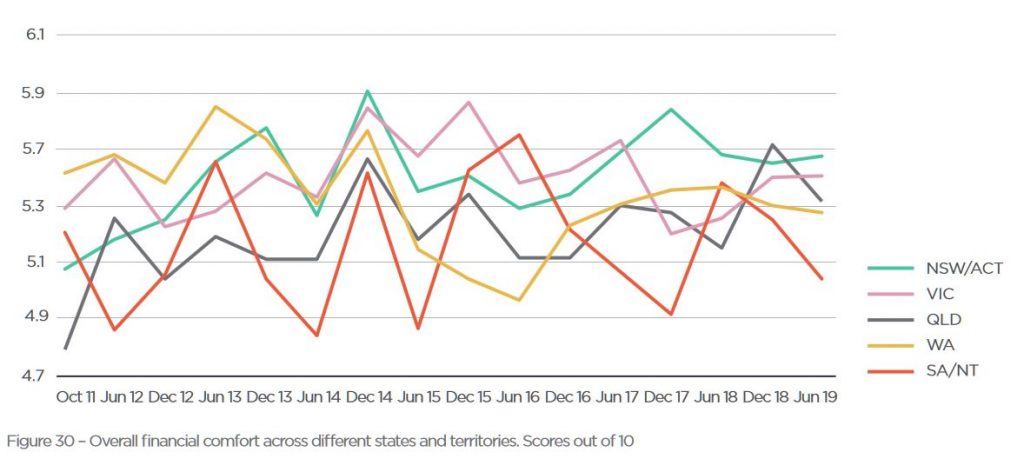

NSW/ACT and VIC – the highest levels of financial comfort was found in NSW/ACT (5.64), followed by Victoria (5.55)

Losers:

QLD, TAS and SA/NT – overall comfort fell in these states

Brisbane, Perth and Adelaide residents – comfort in these cities

dropped to match the low levels of comfort reported in regional

Australia

Working Australians – comfort significantly deteriorated among

workers, with full-time workers recording a 3% decrease to 5.86,

part-time workers decreasing 4% to 5.1, casual workers decreasing 1% to

5.02 and self-employed workers down 3% to 5.57

WA workers – this state reported as being the most difficult job

market, with over 60% expecting it would be difficult to get a new job

in WA

Renters – rental payment stress was reported by 62% of renters, up 11 points during the six months to June 2019.

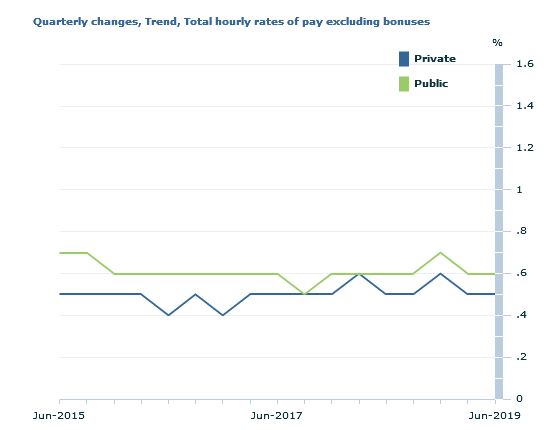

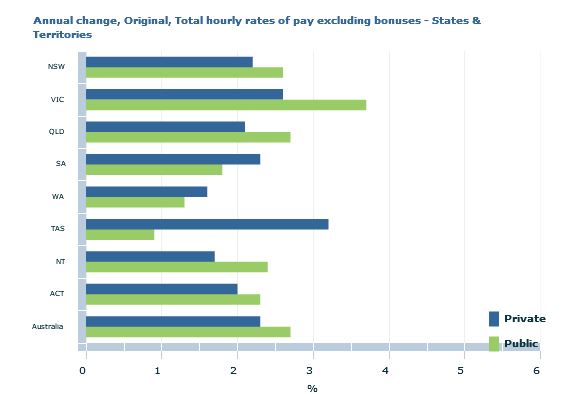

The trend Wage Price Index (WPI) rose 0.5 per cent in the June quarter 2019 and 2.3 per cent through the year, according to figures released today by the Australian Bureau of Statistics (ABS). These are lower than projected in the budget, and highlights the stresses in the economy. Without one-off factors the numbers would be even lower.

Seasonally adjusted private sector wage growth was 0.5 per cent, while public sector wage growth was 0.8 per cent in the June quarter 2019.

ABS Chief Economist, Bruce Hockman said: “Wage growth continues at a

steady rate in the Australian economy on the back of strong public

sector growth over the quarter. The most significant contribution to

wage growth this quarter came from the public sector component of the

health care and social assistance industry, where a number of large

increases were recorded in Victoria under a plan to ensure wage parity

with other states.”

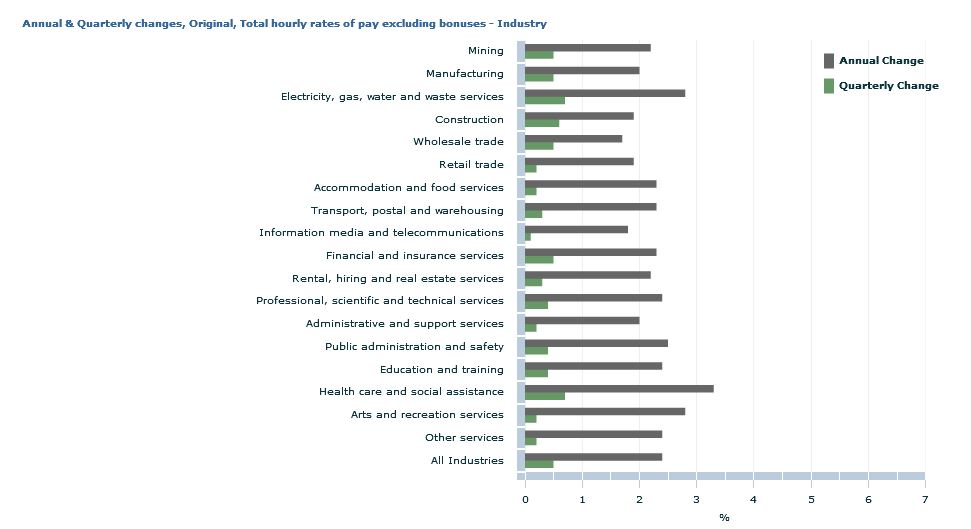

In original terms, annual wages growth to the June quarter 2019 by industry ranged from 1.7 per cent for wholesale trade to 3.3 per cent for health care and social assistance.

Western Australia recorded the lowest through the year wage

growth of 1.6 per cent while Victoria recorded the highest of 2.9 per

cent.

Facebook Inc. has been paying hundreds of outside contractors to

transcribe clips of audio from users of its services, according to

people with knowledge of the work.

The

work has rattled the contract employees, who are not told where the

audio was recorded or how it was obtained — only to transcribe it, said

the people, who requested anonymity for fear of losing their jobs.

They’re hearing Facebook users’ conversations, sometimes with vulgar

content, but do not know why Facebook needs them transcribed, the people

said.

Facebook confirmed that it had been transcribing users’ audio and said it will no longer do so, following scrutiny into other companies. “Much like Apple and Google, we paused human review of audio more than a week ago,” the company said Tuesday. The company said the users who were affected chose the option in Facebook’s Messenger app to have their voice chats transcribed. The contractors were checking whether Facebook’s artificial intelligence correctly interpreted the messages, which were anonymized.

The social networking giant, which just completed a $5 billion settlement

with the U.S. Federal Trade Commission after a probe of its privacy

practices, has long denied that it collects audio from users to inform

ads or help determine what people see in their news feeds. Chief

Executive Officer Mark Zuckerberg denied the idea directly in

Congressional testimony

NAB’s update today reported an unaudited statutory net profit of $1.70 billion in the third quarter 2019, and unaudited cash earnings of $1.65 billion. This is a 1% rise in cash earnings compared with 3Q18.

They said that revenue was up 1%, thanks to a rise in SME lending and slightly higher group margins. Net interests margins increased mainly due to lower short-term wholesale funding costs. Expenses were flat, with efficiencies offsetting high compliance and risk costs.

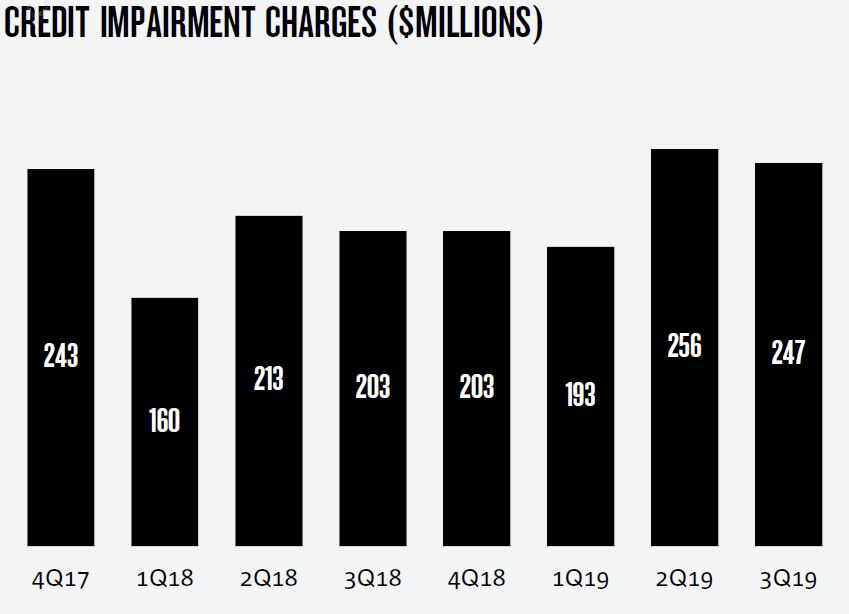

They reported that credit impairment charges increased 10% to $247 million compared to 1H19 quarterly average. The ratio of collective provisions to credit risk weighted assets increased 2 basis points to 96 basis points from March to June.

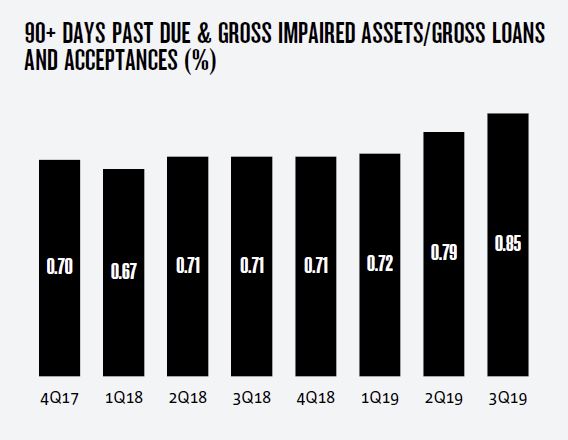

The ratio of 90+ days past due and gross impaired assets to gross loans and acceptances increased from 0.79% to 0.85%, largely due to rising Australian mortgage delinquencies.

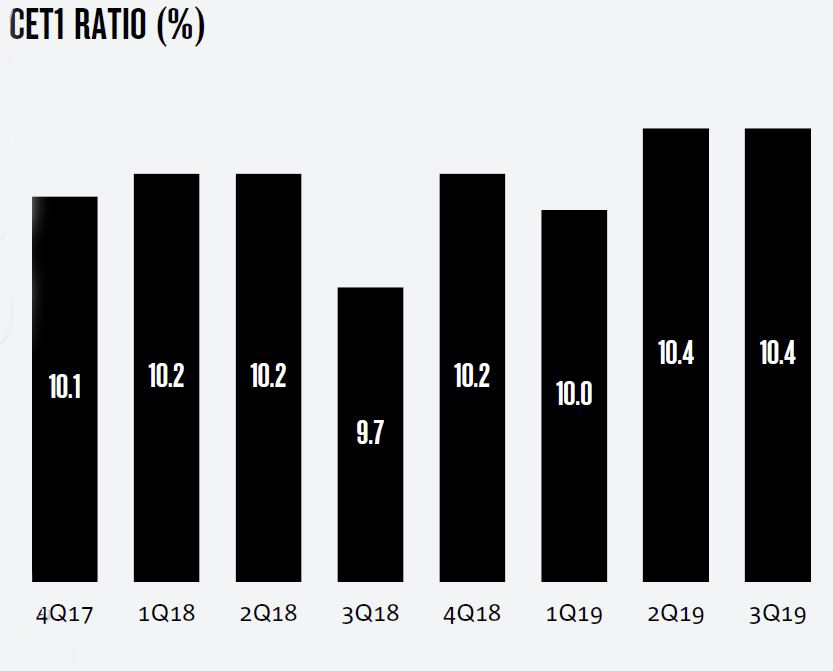

CET1 remains at 10.4%, the APRA leverage ratio is 5.4%, the liquidity ratio (LCR) quarterly average was 128% and the net stable funding ratio (NSFR) was 113%.

The New Zealand Council of Financial Regulators (CoFR) has announced a new vision for New Zealand’s economic wellbeing and has welcomed the addition of the Commerce Commission to the forum.

The new vision aims to contribute to maximising New Zealand’s sustainable economic wellbeing through responsive and coordinated financial system regulation, and allows for a longer term view that more effectively recognises the specific responsibilities of each agency.

CoFR works to identify and respond to issues of cross-agency relevance. CoFR’s members are the Reserve Bank, Financial Markets Authority, the Treasury, Ministry of Business, Innovation and Employment, and now the Commerce Commission. Responsibility for chairing CoFR alternates between the Reserve Bank Governor and the FMA Chief Executive.

The Reserve Bank’s Governor, Adrian Orr, said: “We recognise our responsibility for joint stewardship (te hunga tiaki) of a healthy and efficient financial system that benefits all New Zealanders.”

The Financial Markets Authority’s Chief Executive, Rob Everett, said: “The Council was instrumental in launching the recent conduct and culture review of New Zealand’s banks and life insurers. This illustrated the importance and benefits of regulators working together to tackle issues that span across the financial markets’ regulatory system. Ensuring a coordinated response to such issues will help to build confidence in the regulation of New Zealand’s financial markets.”

Mr Orr says, “Bringing the Commerce Commission on board with its consumer credit focus is a welcomed addition to this forum.”

CoFR meets quarterly to discuss financial markets regulatory issues, risks and priorities, and is attended by the heads of each agency. The existence of CoFR does not derogate from the existing statutory rights and responsibilities of the respective authorities. The most recent meeting occurred yesterday.

Its main objectives are to:

Develop a collective view on longer-term strategic priorities for the financial system;

Identify and monitor important issues, risks and gaps in the financial system that may impinge upon achievement of member agencies’ regulatory objectives;

Agree collaborative responses to issues that require cross-agency involvement and put in place appropriate mechanisms to deliver them.

About the Council of

Financial Regulators

The Council of Financial Regulators (CoFR) has been operating since 2011 as a

forum for agencies with responsibility for financial sector regulation. CoFR is

comprised of the Reserve Bank, Financial Markets Authority, the Treasury,

Ministry of Business, Innovation and Employment, and recently the Commerce

Commission as a forum to share information, identify issues and develop

coordinated responses to issues that may require cross-agency involvement.

CoFR agreed to a financial markets regulatory charter in 2016, which sets out

how we operate our shared ownership of regulatory functions in this area. MBIE

developed the charter as a management tool to set expectations and provide an

overview of the regulatory system. The new vision seeks to build on this

charter.

CoFR formally meets quarterly to discuss financial markets regulatory issues,

risks and priorities. It comprises senior leaders from each agency and from

time to time, CoFR may invite representation from other regulatory agencies and

public authorities, as required.

Australian businesses are more aware than ever of the growth opportunities offered by Asia, but most are struggling to convert these opportunities into revenue outcomes. Groundbreaking research launched today by Asialink Business, sponsored by Commonwealth Bank of Australia, reveals that while awareness and interest in Asian markets — including China — is at a high, many businesses are struggling to activate the opportunities to deliver financial returns.

“Asia’s emerging middle class continue to offer huge growth potential for

Australian businesses of all sizes. By 2030, emerging Asian economies will have

middleclass markets that are more than AUD$20 trillion bigger than they are

today — yet for Australian businesses, while Asia is now firmly on their radar,

many are not activating these opportunities, especially small and medium

enterprises.

“The Asialink Business Commonwealth Bank of Australia survey

demonstrates that the ‘top performers’ all share common strengths, including

employing a highly Asia capable team, customising products to keep-up with

changing local tastes, and investing in an on-the-ground presence in Asia,” Asialink

Business CEO,Mukund Narayanamurti, says.

Released today, the Activating Asia report and Asialink Business

Commonwealth Bank of Australia survey results find that while 80% of Australian

businesses include Asia to some extent in their corporate strategy, most are

failing to generate significant revenue from these markets: More than half of

the organisations (54.7%) surveyed generate less than 5% of their revenue from

Asia.

CBA Head of Asian Business Banking, Jonathan Yeung says:

“The business opportunities that exist in Asia are well known and well versed.

But while many Australians businesses are including Asia as part of their

strategy, we know that majority of these organisations don’t optimise their

operations to maximise revenue streams.

“Through our research, we’ve charted a practical roadmap for Australian

businesses to build the specific skills, knowledge and networks they need to

succeed and capitalise on the opportunities in the region. We are excited to

launch the Activating Asia report, the latest report in our Asia

Capability research partnership with Asialink Business.”

Drawing on a unique survey of businesses across diverse sectors of the

economy, and backed by practical case studies and interviews, Activating

Asia reveals three key lessons for succeeding in Asia’s competitive

markets:

Asia capable staff are critical: Businesses that succeed in the region are more likely to actively seek staff with language or in-country experience. For example, businesses that always mention Asian language capabilities or Asia experience in job ads earn, on average, more than 5 times the revenue from Asia than those that never mention these skills.

Keep up with customers’ fast changing preferences: Businesses that tailor and adjust their product or service and marketing earn, on average, more than 8 times the revenue from Asian markets than those that sell the same offering using the same marketing.

Technology is a complement, not a substitute for being on the ground 33 per cent of Australian businesses that earn more than 5 per cent of their revenues from Asia undertook in-country visits at least once a month – more than double that of businesses earning less than 5 per cent of revenues from Asian markets.

Professional services businesses feature in the top performers — of those

businesses that generate more than 50% of their revenue from Asia, 26% are

professional services firms, followed closely by private education and training

organisations at 25%.

The study also reveals that overall business sentiment towards Asia is

positive. Despite the ongoing China-US trade tensions, China

continues as the most attractive market for Australian Businesses. Nearly half

of participating businesses (44%) report an active interest or existing

presence in China. Australian businesses also have significant interest in the

opportunities presented by the ten ASEAN economies in Southeast Asia collectively

ranking as the second most popular market for Australian organisations.

To actualise the diverse opportunities across the region, Activating

Asia calls on Australian businesses to invest in building Asia

capabilities and embed an Asia capable mindset into long-term business

planning.

The key question now is will the banks revert to their previous practices of doing little to validate household spending patterns as part of the mortgage assessment processes. Some are already saying “buy now” with renewed vigour.

The Royal Commission revealed last year that some lenders ignored household expense data favouring the automated HEM decisioning. But on the basis of the finding, they are now in the clear.

Banks of course need mortgage lending to grow to enable their profits to rise, and in recent times that has been a problem. New lending momentum has been pretty slow.

HEM standards were tightened in July, meaning that the minimum spending benchmarks were lifted especially for households on higher incomes. Some banks have been asking for painful detail and history in lieu of using HEM, and this has slowed lending decisions but around half of loans are still approved by HEM.

We also need to link this with the APRA loosening of the interest rate hurdle which gives lenders flexibility on their decisioning (within limits).

ASIC is currently taking evidence from the industry on potential changes to responsible lending, and has said we should expect some revisions by years end. Plus they have previously stated that even if they lost the Westpac case, they would still insist that while HEM is a useful too it is not necessary and sufficient to meet their requirements.

The trouble is the original ASIC guidelines were vague, and the “non-unsuitable” formulation left significant ambiguity. This needs to be changed.

The way through this is to use debt to income ratios, something which has been in place in the UK and NZ for some time, as we know the risks of loss are greater when the Debt To Income ratios are higher.

But then the question will become, how prescriptive should the regulators be, and of course in the current weakening economic environment there will be an attempt to push lending harder.

So, my expectation is there will be some loosening of underwriting standards (which is bad) while the Banks can assume class actions relating to responsible lending will be unlikely to proceed.

I expect households will be required to certify the accuracy of their expenses, but that banks once they have that protection will be will to lending within the HEM framework.

So the bottom line is, yes, I expect more credit will be offered, the question is will households lap it up – leading to rises in prices (as credit growth and home price growth are linked), or will the weak wages growth, high costs of living and home price momentum (or lack of it) reduce demand.

The finance and real estate sector will be spinning hard to try and entice people into the market. Just remember we have the biggest debt bomb ticking away.

But the banks are also on notice now.

Amidst the court proceedings with ASIC, Westpac updated its group

credit policies “to enhance the way [it] captures customer living

expenses, commitments, and verify documentation.”

A Westpac spokesperson said, “We recognise sometimes it can be

difficult for customers to provide a complete picture of their expenses

and the enhancement of our expense categories means our staff and

brokers have the opportunity to prompt customers to remind them about

particular expenses they may have forgotten.”