An important post from Macrobusiness (MB) by the excellent Leith van Onselen which opens the can of worms which is the RBA’s Committed Liquidity Facility (a.k.a. Bank Safety Net or Unofficial Government Guarantee). Its all about the RBA’s version of QE!

He says:

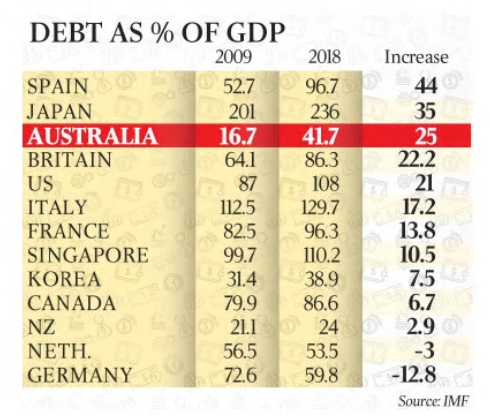

Figures from the International Monetary Fund (IMF) show that Australian government debt has risen faster than most other developed nations, increasing from 16.7% of GDP to an expected 41.7% this year – a jump of 25 percentage points. From The Australian:

The IMF report comes as Scott Morrison prepares to unveil next month’s budget, which will recycle improved company tax flows into personal income tax cuts while taking on more debt to finance infrastructure development. The Treasurer argues that the government is no longer borrowing to finance daily running costs but just to cover infrastructure and defence investments.

The mid-year budget update in December showed gross debt peaking at $591 billion in 2019-20, having hit $500bn in 2016-17. Gross debt stood at $319bn when the Coalition took office in 2013.

The IMF predicts this year will be the peak for Australian gross debt at 41.7 per cent of GDP, before a decline to 32.2 per cent over the next five years…

Although the IMF projects that Australia’s federal and state budgets will be back in surplus by 2020, it says there will be a continuing need to raise funds to roll over debts as they mature.

We think the projected return to surplus by 2020 is wishful thinking, given:

Commodity prices will likely fall, draining company profits, national income, and company tax revenue;

The housing downturn will dampen consumer spending, jobs and growth, draining company and personal income tax revenue; and

We are likely to see tax cuts offered from both sides in the upcoming federal election campaign.

Regardless, there is another important question that is rarely asked outside of MB: why is the Reserve Bank of Australia (RBA) persisting with the Committed Liquidity Facility (CLF) when there is now so much government debt on issue?

The CLF was established in late-2011 in order to meet the Basel III liquidity reforms. Below is the RBA’s explanation of the CLF [my emphasis]:

The facility, which is required because of the limited amount of government debt in Australia, is designed to ensure that participating authorised deposit-taking institutions (ADIs) have enough access to liquidity to respond to an acute stress scenario, as specified under the liquidity standard…

The CLF will enable participating ADIs to access a pre-specified amount of liquidity by entering into repurchase agreements of eligible securities outside the Reserve Bank’s normal market operations. To secure the Reserve Bank’s commitment, ADIs will be required to pay ongoing fees. The Reserve Bank’s commitment is contingent on the ADI having positive net worth in the opinion of the Bank, having consulted with APRA.

The facility will be at the discretion of the Reserve Bank. To be eligible for the facility, an ADI must first have received approval from APRA to meet part of its liquidity requirements through this facility. The facility can only be used to meet that part of the liquidity requirement agreed with APRA. APRA may also ask ADIs to confirm as much as 12 months in advance the extent to which they will be relying on a commitment from the Bank to meet their LCR requirement.

The Fee

In return for providing commitments under the CLF, the Bank will charge a fee of 15 basis points per annum, based on the size of the commitment. The fee will apply to both drawn and undrawn commitments and must be paid monthly in advance. The fee may be varied by the Bank at its sole discretion, provided it gives three months notice of any change…

Interest Rate

For the CLF, the Bank will purchase securities under repo at an interest rate set 25 basis points above the Board’s target for the cash rate, in line with the current arrangements for the overnight repo facility.

In light of the federal budget deficit projected to balloon out to nearly $600 billion, the question for the RBA is: shouldn’t the CLF be unwound and the banks instead be required to hold government bonds, as initially required under Basel III?

Bonds on issue are roughly triple that of when the CLF was first announced, so surely the RBA should amend the liquidity rules so that Australia’s ADIs are forced to purchase government bonds, so that the size of the CLF requirement decreases?

The most likely reason is because the RBA wants to keep open the option of bailing-out the banks. As noted by Deep T:

When there is capital flight due to official interest rate decreases, the RBA could and would step in and fund the banks’ funding shortfall from a loss of international investors using the Committed Liquidity Facility at rates below the banks’ international funding rates. The CLF used in these circumstances would be a form of quantitive easing and would have a dampening effect on mortgage rates by subsidising bank borrowing rates but could never be a lasting solution and only have limited effect in the long term. So yes, high cost international funding by the banks can easily be replaced by cheap RBA funding through a form of QE or money printing subsidising bank profits and banker bonuses.

The fact of the matter is the CLF represents another subsidy to the banks. The cost of the CLF is very low – i.e. 15bps pa – compared to the alternative. The CLF allows ADIs to originate mortgage assets and create RMBS rather than buying government bonds. The net spread on mortgage assets or RMBS compared to government bonds is much greater than 15bps pa, thus representing a significant direct subsidy to the banks.

MB reader, Jim, nicely dissected the lunacy of the CLF in a comment in 2016:

You’ve missed the real beauty of the CLF, and APS210

So the banks are forced to hold ‘as much as possible’ qualifying Tier 1 securities to meet their APS210 requirements. But… even with the large commonwealth government deficit, there still isn’t enough CGS to go round (CGS and TCorp bonds only qualify for Tier 1 securities under APS210).

Which is why the RBA invented the CLF. The CLF allows, no, it requires the banks to:

– hold their own securitised bonds on their balance sheet to qualify as ‘liquid assets’

– buy each other’s bonds to qualify as ‘liquid assets’

So, ANZ, CBA, NAB and WBC each have around $50bn of their own off balance sheet mortgages sitting back on their balance sheet to protect them against a ‘liquidity event’. Then they each have around $10bn each of each other’s bonds, so NAB holds around $50bn of WBC/ANZ/CBA bonds etc.

And if / when the liquidity shit hits the fan (e.g. foreigners stop buying the bank’s bonds), the banks can swap them into the RBA for a 15bps fee.

So the RBA will be forced to sit on about half a trillion dollars of Aussie bank paper ($100bn each plus a little more for CBA and WBC, plus Suncorp, Bendigo etc). Just think what THAT would do to your graph of yellow lines – more than double it in an instance.

So the CLF is not about government debt, its about bank debt, and how the RBA has bent over forward for the banks. Having worked in treasury at a Big 4, the CLF is the biggest joke under the sun – a guaranteed way to print money for the banks. This is why the fixed income desks at banks are always the best paying – those guys are paid to buy and hold bank bonds under APS210 requirements.

Do an investigation on how much REAL systemic debt is sitting in the banking system – the RBA has made itself lender of last resort to over $500bn worth of debt.

The bottom line is that with the stock of outstanding Commonwealth debt now so large (and still growing), the rationale for maintaining the CLF has evaporated. But don’t expect any action from the RBA, which wants to maintain the capability of bailing-out the banks via its own form of quantitative easing.

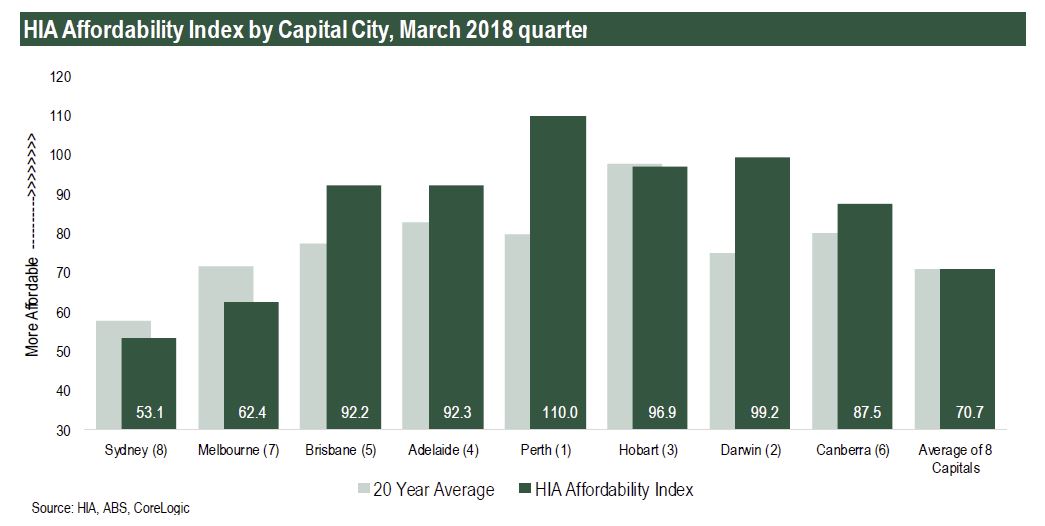

“Affordability improved in most of Australia’s capital cities during the first three months of 2018 as house price pressures eased,” commented Shane Garrett, HIA Senior Economist.

This does not necessarily take account of the now tighter, and becoming even tighter lending standards now in play. In any case, in most centres, affordability is still well below the long term averages.

HIA’s Affordability Index is calculated for each of the eight capital cities and regional areas on a quarterly basis and takes into account latest dwelling prices, mortgage interest rates and wage developments. The results are published and analysed in the HIA Affordability Report.

“Affordability in Sydney improved by 1.9 per cent as a result of the reduction in dwelling prices over the past six months, while in Melbourne the outcome was largely unchanged as price growth remains solid.

“Across the eight capital cities overall, affordability improved slightly (+0.2 per cent) during the March 2018 quarter. The improvement was held back by strong home price growth in a limited number of markets including Melbourne and Hobart.”

“Current interest rate settings continue to benefit affordability. The RBA’s official cash rate is at a record low and hasn’t been moved in over 20 months – an unprecedented period of stability.

“Even though we have started to move in the right direction, housing affordability remains very challenging in the larger capital cities. The root cause of the problem is that the cost of producing new houses and apartments is still too high.

“Governments need to focus on solutions involving lower land costs, a more nimble planning system and a lighter taxation burden on new home building,” concluded Mr Garrett.

Australian Finance Group Limited announced that it has entered into a binding agreement to make a strategic investment of 30.4% (fully diluted) of Think Tank Group Pty Ltd (“Thinktank”) for $10.9 million in cash consideration. In connection with the investment, AFG will distribute a white label Commercial Property product through its network of brokers.

Thinktank operates primarily as a small ticket (sub $3m) commercial property lender and was established in 2005. Thinktank operates nationally and has a loan book in excess of $750 million. It has established itself as a viable and competitive non-major commercial property lender in a sector that has been bereft of competition and choice for too long.

AFG Chief Executive Officer David Bailey explained the decision: “Our strategic investment in Thinktank represents the next evolutionary step for AFG to diversify its earnings base. The ongoing success of AFG Home Loans and the introduction of AFG Business are important contributors to the future growth of AFG. It makes sense to participate further in an asset class that we are comfortable with – both directly through the white label opportunity and indirectly through our shareholding to generate further earnings for AFG.

“The opportunity to blend Thinktank’s commercial property lending expertise with our own distribution and securitisation capability will benefit both businesses. It will also enable us to deliver further competition and choice to the small to medium enterprise (SME) market place at a time when it is most needed. AFG aims to bring the same disciplines to this white label proposition as we have successfully demonstrated with our own residential white label programme,” added Mr Bailey.

Thinktank CEO, Jonathan Street, commented: “The agreement reached with AFG marks a further significant step forward for our business and serves to further enhance our capacity to best service the finance needs of borrowers over the breadth of the Australian commercial property market.

In coming together, we see considerable opportunity to not only combine our efforts to great effect across the AFG network but equally in extending the same emerging advantages and benefits to our wider base of aggregation and broker relationships.”

Investment highlights:

Investment of 30.4% (fully diluted) of Thinktank Group Pty Ltd (“Thinktank”) for $10.9 million in cash consideration

Addition of a white label commercial property mortgage to AFG’s product offering with a strategic alignment with AFG’s commercial broking platform, AFG Business

Opportunity to increase Thinktank’s penetration of the market through AFG’s 2,900 strong broker network

Thinktank is expected to achieve profit after tax in FY18 of approximately $3.2 million

AFG has the right to appoint two directors to the Thinktank board and they will take up those positions immediately

Completion is expected to occur today following the transfer and confirmed receipt of consideration.

More evidence of the rising costs of funds as ME Bank says it has lifted its standard variable rate on existing owner-occupier principal and interest mortgages, effective today, 19 April 2018.

ME’s standard variable rate for existing owner-occupier principal-and-interest borrowers with an LVR of 80% or less, will increase by 6 basis points to 5.09% p.a. (comparison rate 5.11% p.a.^).

Variable rates for existing investor principal-and-interest borrowers will increase by 11 basis points, while rates for existing interest-only borrowers will increase by 16 basis points.

ME CEO Mr Jamie McPhee said the changes are in response to increasing funding costs and increased compliance costs.

“Funding costs have been steadily increasing over the last few months primarily due to rising US interest rates that have flowed through to higher short-term interest rates in Australia.

“In addition, ME continues to transition its funding mix to ensure the requirements of the Net Stable Funding Ratio will be met, and this is also increasing our funding costs.

“At the same time, industry reforms and increasing regulatory obligations are increasing our compliance costs.

“Despite these increases ME’s standard variable home loan for owner-occupier principal-and-interest borrowers with LVR 80% or less, is still lower than the major banks as it has been since ME became a bank in 2001. In addition ME also continues to offer some of the highest deposit rates in the market.

“This was not an easy decision, but rising costs have forced us to reset prices to maintain a balance between borrowers, depositors and our industry super fund shareholders and their members, all while ensuring we continue to grow and provide a genuine long-term banking alternative,” McPhee said.

“We will continue to assess market conditions and make changes to prices to maintain this balance if necessary.”

More hikes will follow, across the industry together with reductions in rates paid on deposits as the fallout of the Royal Commission and higher international funding costs take their toll.

The 10-year US Bond rate is moving higher again, following some slight fall earlier in April. Have no doubt, funding cost pressure will continue to rise.

^Home loan comparison rates calculated on a loan of $150,000 for a term of 25 years, repaid monthly.

The Reserve Bank hosted a roundtable discussion on small business finance today, along with the Australian Banking Association and the Council of Small Business Australia. The roundtable was chaired by Philip Lowe, Governor of the Reserve Bank.

Small businesses are very important for the economy. They generate significant employment growth, drive innovation and boost competition in markets. Access to external finance is an important issue for many small businesses, particularly when they are looking to expand.

Our own SME survey highlights the problems SME’s face in getting finance in the face of the banks focus on mortgage lending. The latest edition of our report reveals that more than half of small business owners are not getting the financial assistance they require from lenders in Australia to grow their businesses.

The aim of the roundtable was to provide a forum for the discussion of small business lending in Australia. The participants included entrepreneurs from the Reserve Bank’s Small Business Finance Advisory Panel along with representatives from financial institutions, government and the financial regulators.

The challenges faced by small businesses when borrowing were discussed. The entrepreneurs highlighted a number of issues, including:

access to lending for start-ups

the heavy reliance on secured lending and the role of housing collateral and personal guarantees in lending

the loan application process, including the administrative burden

the ability to compare products across lenders and to switch lenders.

The participants discussed a range of ideas for addressing these challenges. Financial institutions shared their perspectives and discussed some of the steps that are being taken to address concerns of small business. The roundtable heard some suggestions about how to improve the accessibility of information for small businesses about their financing options. The roundtable also heard from the Australian Prudential Regulation Authority regarding the proposed revisions to the bank capital framework that relate to small business lending.

The roundtable discussed some other policy initiatives that are currently underway, including the introduction of comprehensive credit reporting and open banking. Participants agreed that these initiatives could help to improve access to finance, and the Reserve Bank will continue to monitor developments closely.

Background

The Small Business Finance Advisory Panel was established by the Reserve Bank in 1993 and meets annually to discuss issues relating to the provision of finance, as well as the broader economic environment for small businesses. The panel provides valuable information to the Reserve Bank on the financial and economic conditions faced by small businesses in Australia.

The Reserve Bank has previously hosted discussions on small business finance issues, including a Small Business Finance Roundtable in 2012 and a Conference on Small Business Conditions and Finance in 2015.

The Australian Banking Association, along with the Australian Council of Small business, representatives for member Banks and other stakeholders were also in attendance to bring their own perspective on the issues and to answer questions. The event was agreed to and organised at the end of last year.

Australian Banking Association CEO Anna Bligh said that the Roundtable was an important opportunity for Australia’s banks to listen first hand to the needs of small business.

“Small business is the engine room of the Australian economy, accounting for more than 40% of all jobs or around 4.7 million people,” Ms Bligh said.

“This Roundtable was an important step in building the relationship between banks, small businesses and their representatives.

“Banks are working hard to better understand the needs of business, their challenges and how they can work with them to help them achieve their goals,” she said.

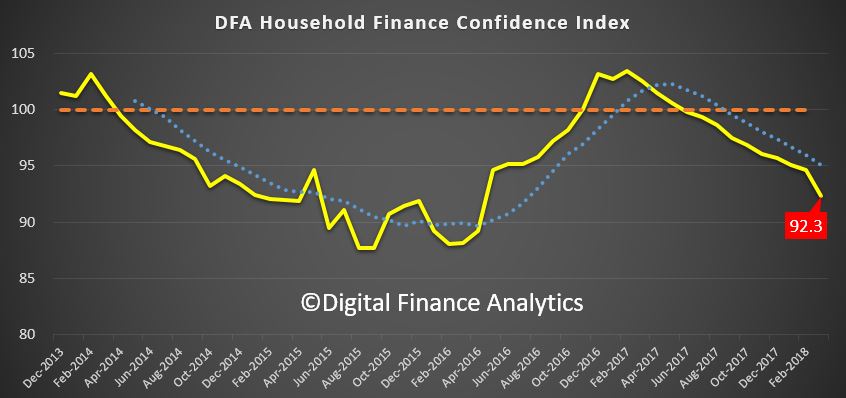

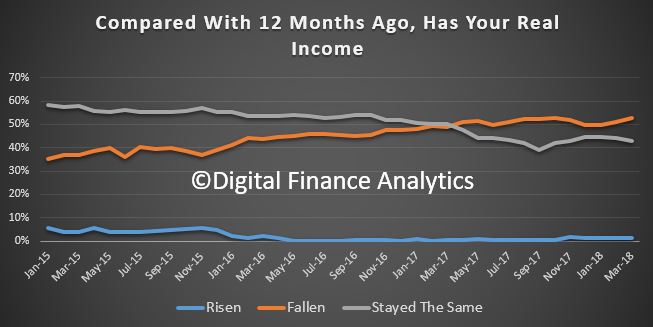

The latest Digital Finance Analytics Household Finance Confidence Index for March 2018 shows a further slide in confidence compared with the previous month.

The current score is 92.3, down from 94. 6 in February, and it has continued to drop since October 2016. The trend is firmly lower.

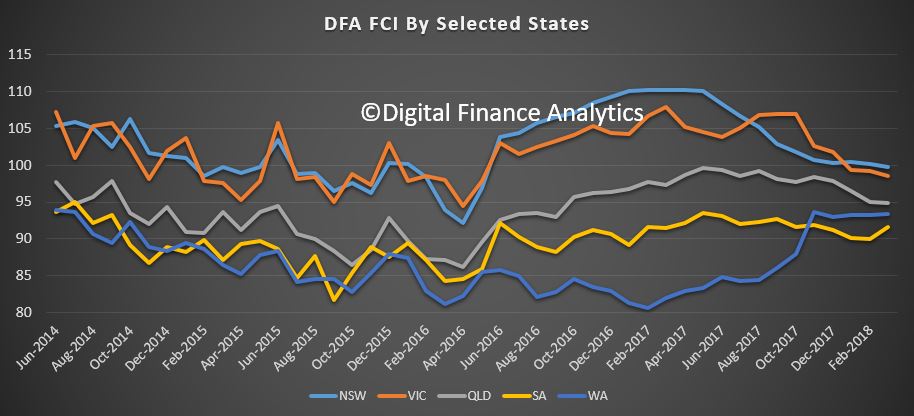

Across the states, confidence is continuing to fall in NSW and VIC, was little changes in SA and QLD, but rose in WA.

Across the age bands, there were falls in all age groups.

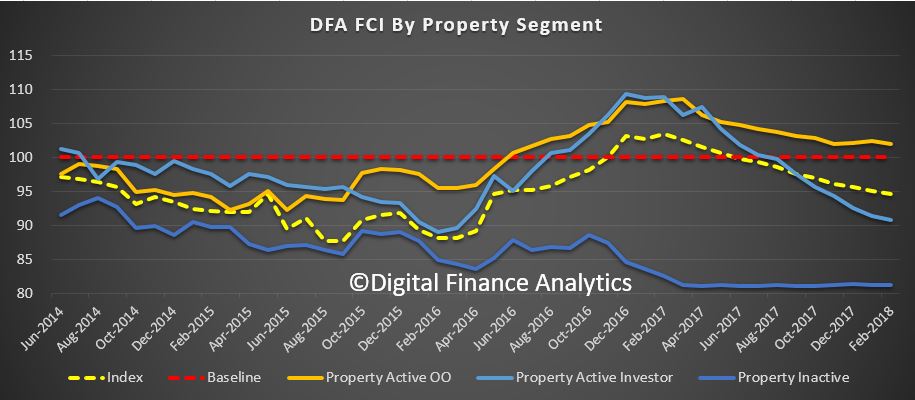

Turning to the property-based segmentation, owner occupied householders remain the most confident, while property investors continue to become more concerned about the market. Those who are property inactive – renting, or living with parents or friends remain the least confident. Nevertheless those who are property owners remain more confident relative to property inactive households.

We can look at the various drivers which underpin the finance confidence index.

We start with job security. This month, there was a rise 6% in households who are less confident about their job security compared with last month, up to 25.8%. Those who felt more secure fell by 1.5% to 12.1% while 61% saw no change. Availability of work was a primary concern, but the security concerns were more around job terms and conditions, and the requirement to work unsocial hours and weekends.

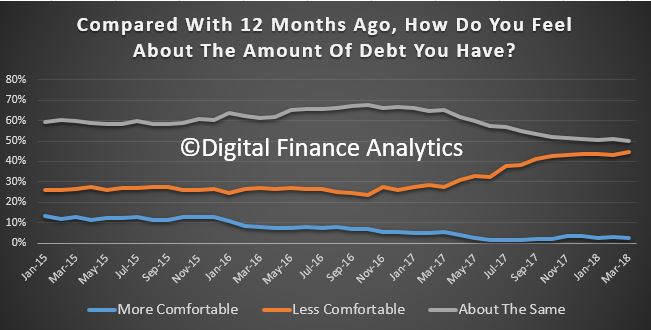

Turning to concerns about levels of debt, 44.5% of households were more concerned about their outstanding loans, up 1.5% from last month. Under 3% of households were more comfortable with the debt they hold. 49% reported no change this month. Those who were more concerned about debt highlighted concerns about higher interest rates, and the ability to service their current loans in a flat income environment.

52% of households reported their incomes had fallen in the past month, in real terms. This is up 1.5% this month. Just over 1% of households reported a pay rise, and 43% reported no change in real incomes. More households comprise of members who are working multiple jobs to maintain income.

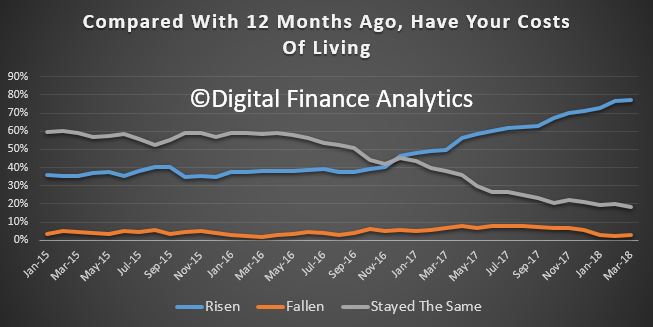

In contrast, cost of living continues to rise faster than incomes for many households. 77% of households said their costs had indeed risen, up slightly from last month. 18% of households said costs had stayed the same and 3% said costs had fallen. Households said the costs of electricity, petrol, school fees and child care costs all hit home. Health care costs, and especially the costs of private health care cover also figured in their responses. More households are seriously considering terminating their health insurance cover due to the rising expense.

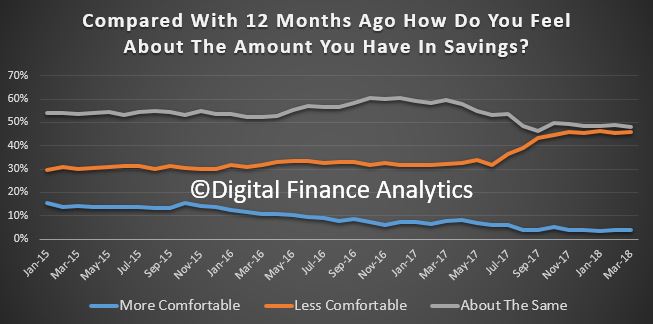

Turning to savings, 46% of households were less comfortable with their savings a rise of 1.5% compared with last month. 4% were more comfortable. 50% were about the same. There were ongoing concerns about further falls in interest rates on deposit accounts, and the need to continue to raid savings to support ongoing household budgets.

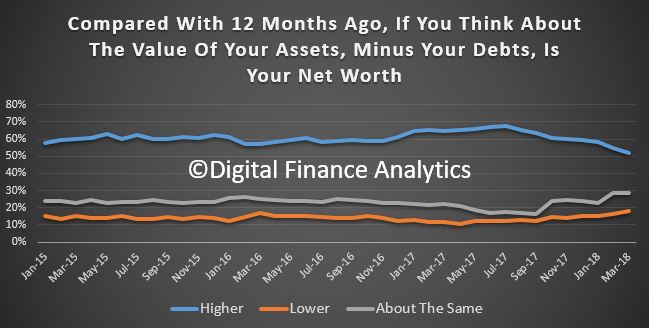

Finally, we look at household overall net worth. Despite the volatility seen in the financial markets, the main concern captured in answers to this question related to potential falls in property values. 52% said their total net worth was higher, down 3% from last month. 18% said their net worth was lower, a rise of 2% compared with last month. 28% remained the same. Both those with higher levels of education, and males tended to report more of a rise in net worth. Women were considerable more concerned about the current trajectory of home prices, and the risks relating to future falls. Households in regional centres remained more concerned about their net worth, not least because in many areas home prices have risen less strongly in recent years.

So in conclusion, based on the latest results, we see little on the horizon to suggest that household financial confidence will improve. We expect wages growth to remain contained, and home prices to slide, while costs of living pressures continue to grow. There will also be more pressure on mortgage interest rates as funding costs rise, and lower rates on deposits as banks trim these rates to protect their net margins.

By way of background, these results are derived from our household surveys, averaged across Australia. We have 52,000 households in our sample at any one time. We include detailed questions covering various aspects of a household’s financial footprint. The index measures how households are feeling about their financial health. To calculate the index we ask questions which cover a number of different dimensions. We start by asking households how confident they are feeling about their job security, whether their real income has risen or fallen in the past year, their view on their costs of living over the same period, whether they have increased their loans and other outstanding debts including credit cards and whether they are saving more than last year. Finally we ask about their overall change in net worth over the past 12 months – by net worth we mean net assets less outstanding debts.

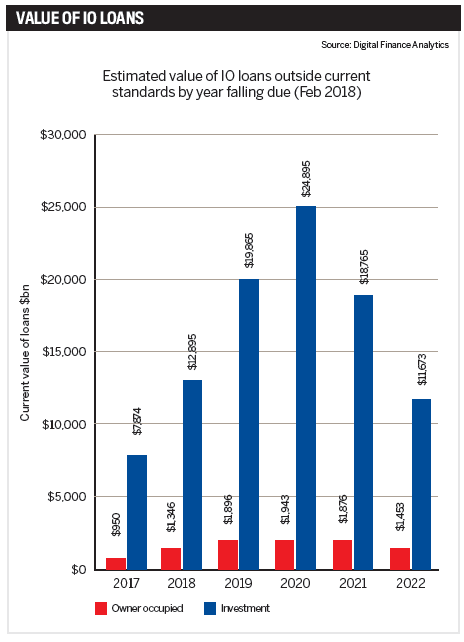

Interest only loans are rarely out of the news. Following ASIC’s interim review the September quarter posted a knee-jerk 44.8% decline in new IO loans and lending practices are now firmly in the regulator’s crosshairs. APRA and RBA have already clamped down and further scrutiny is expected during the royal commission.

The regulators aren’t the only ones concerned. In February, assistant governor Michele Bullock delivered a speech on mortgage stress in which she highlighted a “large proportion of interest-only loans are due to expire between 2018 and 2022”.

That large proportion is, in fact, almost every IO loan written between 2013 and 2016, and subsequent analysis of IO property fixed-term lending by Digital Finance Analytics has calculated the total number at 220,000, with values upwards of $100bn.

These loans originate from before the reviews of 2015 and 2017, and in the coming year the fixed terms on 14% of them will face a reset outside of current lending criteria. By 2020, the value of loans due for renegotiation is expected to reach $27bn.

While there are many options open to these borrowers, Bullock calls it an “area to watch”, saying many could find themselves in financial stress.

“Some homeowners may not realise they are fast approaching the end of their five-year term and, if they do nothing, their lender will automatically roll them onto a P&I loan that could be challenging for them to support,” says Zippy Loans’ principal broker Louisa Sanghera.

“Combine this scenario with a slowing of the property market and clients may not have the buffer of equity to soften the blow.”

To the customer, interest-only is an attractive proposition for a number of reasons, from freeing up cash to tax incentives. Additionally, investors have widely financed rental property investments on an IO basis while paying down their owner-occupied P&I loan. Executive director of The Local Loan Company, Ray Hair, observes that it’s a decades-long trend, one that has taken place right under the radar of regulators and banks.

To date, availability has largely driven demand for IO, but with many borrowers now preparing to face the consequences of their honeymoon financial planning, a mounting collection of horror stories could change that.

“Whenever regulators initiate corrective action in a market there is an initial period of over correction, however the pendulum generally swings back to a position of equilibrium. Sadly, this is of little comfort to those caught out by the overnight changes in policy, increased interest rates and institutional disregard for the personal cost,” says Hair.

“Expect to see some very angry investors looking for a lender, broker or adviser to blame, and pay compensation” Ray Hair, The Local Loan Company

Major lenders are preparing their broker networks for further changes to lending criteria, and are actively assessing the terms of loans due to expire to 2022. But with many below the cap and borrowers looking for IO products, the call to return to business as (almost) usual has been too strong to resist.

“We have seen several major lenders loosen the reigns and cut the rates for interest-only loans again, likely because they are sitting below the cap and are looking to add more interest-only loans to their books. It will be interesting to observe whether other lenders follow and how this plays out in terms of consumer behaviour,” says Uno Home Loans CEO Vincent Turner.

The mortgage crunch

In January, UNSW professor of economics Richard Holden published a sobering observation of Australia’s relationship with high-LVR and IO loans. In it he reported Australian banks lend an average 25% more than their US counterparts and that these loans are poorly structured and sometimes based on falsified or inaccurate household finances.

A decade ago, US banks learned this lesson the hard way, when five-year adjustable rate mortgages could not be refinanced and the fallout triggered a chain reaction that dragged most of the globe into recession.

In Australia, IO lending has comprised as much as 40% of the loan book at the major banks, and a particularly large share of property investors choose IO. The number of new IO loans is in overall decline, $156bn borrowed in 2015 to $135.5bn in 2017, but their share is still significant. In the owner-occupier market they count for one in four loans, and in the investor market it’s two in three.

“Interest-only loans in Australia typically have a five-year horizon and to date have often been refinanced. If this stops then repayments will soar, adding to mortgage stress, delinquencies, and eventually foreclosures,” Holden told Australian Broker at the time.

“It’s our professional and ethical obligation to look after the best interests of our clients and help them plan strategies” Louisa Sanghera, Zippy Loans

A teacher at the University of Chicago when the US housing market crashed, he added, “The high proportion is similar to the high proportion of adjustable rate mortgages in the US circa 2007.”

So how scared should people be? According to Hair, a lot of people “should be very afraid”, although he says dynamic lending policies, a banking sector unwilling to lose market share and strength in non-bank lenders will dampen some impact.

Quoting the DFA data, he adds, “Unfortunately, there will be pain for highly leveraged borrowers with negative equity, as there has been in the past with an oversupply of apartments, restrictions on non-resident lending and the fall

in property values in mining-dependent regional towns.”

For Turner, the concerns are overstated on a macro level, and reasonable lead times for a switch are all most borrowers will need. However, he warns, “The bigger concern should always be unemployment that triggers substantial hardship, very quickly across a broad group of people, which has the effect of contagion.”

Hero or villain?

While there are many unknowns in how borrowers and lenders will cope with the switch to P&I, what is known is that brokers could find themselves very busy between now and 2022.

“It’s our professional and ethical obligation to look after the best interests of our clients and help them plan strategies that are sustainable and supportive of their personal financial goals,” says Sanghera, who predicts a “positive impact overall” for brokers.

At Zippy Loans active management of IO customers means the lender has very few of the loans on its books. Responding to the rises in interest rate charges over recent months, Zippy has contacted its IO clients to move them onto a workable P&I solution.

“Clients will need to consider a broader range of lending options to find a product that works for them and brokers are ideally placed to research these options on their behalf. I believe this will result in more people turning to brokers to navigate the ever-more complex market place and secure the right solution,” she adds.

Throughout this process, transparency will be key, as Turner notes, “Brokers who continue to push expensive interest-only loans will probably lose business to those who show their customers when P&I works and when IO is the better option. In most cases it isn’t.”

However, brokers will also be the bearers of bad news as some are forced to sell and, according to Hair, it’s likely a lot of disgruntled borrowers will pursue their brokers in the courts, as many have done before when things have not gone their way.

Advising brokers to keep “well documented notes” of original transactions and borrower objectives, as well as subsequent attempts to refinance, he says: “Brokers will be both the heroes and the villains in this pantomime.”

“Expect to see some very angry investors looking for a lender, broker or adviser to blame, and pay compensation, for the position they find themselves in,” he adds.

Is this Australia’s sub-prime crisis? From those in the industry it’s a unanimous no. However that doesn’t mean to say a significant number of borrowers won’t receive a harsh wake-up call.

“The bigger concern should always be unemployment that triggers substantial hardship … which has the effect of contagion” Richard Holden, UNSW

For Holden, the damage has already happened and recent measures are too little too late. Although he refers to tighter lending standards as “comforting”, he says the 30% cap is “about all that can be done” at this point.

Australia’s smaller lenders lack the resources to manage more of the IO debt burden, meaning a mass exodus of customers away from the majors is unlikely. That doesn’t mean to say the majors won’t step up to the potential competition. As Hair predicts,

this could bring some attractive offers for borrowers looking to switch or refinance.

For now, it’s all eyes on the interest rate. On the one hand, no change in the cash rate for 19 months has manufactured a level of stability, on the other it’s delayed the hangover. The IMF has already advised implementation of US-style signalling for potential hikes, although after the last month there is some way to go before reaching the 4% rate it expects to see by late 2019.

Regardless of what happens, some pockets of stress are expected.

Within the industry, brokers have a chance to step up and guide customers through the uncertainties, but the watchful eyes of the regulators will be on them.

A $100bn question remains: how wealthy is the average Australian borrower? Those writing the rulebook say wealthy enough to cover higher mortgage payments. Those who have seen the cycle play out elsewhere, say otherwise.

Canadian real estate prices are acting a little skittish. The Teranet–National Bank House Price Index, shows real estate prices stalled across the country. In addition, the index is making moves we haven’t seen outside of a recession.

Tera-What?

If you’re a regular reader, feel free to skip this. For those that don’t know, The Teranet-National Bank HPI is a different measure of real estate data, that relies on property registry information instead of sales. Many misinformed agents refer to this as a “delayed” measure, but that’s not the case. The use of registry data means that the information is “late” compared to the MLS, but it’s more accurate.

Using registry information means only completed sales are included. In contrast, the MLS uses just sales. In a hot market, few sales fall through, so the MLS is definitely a faster read. In a cooling market, sales can start to fall through, as some buyers look for a way out while prices drop. This is often not reflected in MLS data, since a transfer occurs 30 to 90 days after a sale. They each have their trade offs, and neither is better or worse than they other. If you’re really into housing data, it’s best to check both to get a real feel for the market.

Canadian Real Estate Prices Are Unchanged

Canadian real estate prices didn’t do a whole lot in March. The 11 City Composite index remained virtually unchanged compared to February. Prices are up 6.61% compared to the year before. National Bank analysts noted this is “the first time outside a recession when the March composite index was not up at least 0.2%” It was also the first time that only 4 out of the 11 markets saw an increase, outside of a recession. The unusual move is definitely worth noting from a macro perspective.

Toronto Real Estate Prices Are Flat

The Toronto real estate market has no idea what to do right now. The index showed prices remained flat from last month, and up 4.31% from last year. Prices are down 7.3% from the July peak when adjusted, and 7.9% when non-adjusted. This is the lowest pace of annual price growth since November 2013.

Funny thing to note is experts, including some bank executives, are saying the correction is over. Technically speaking, a correction hasn’t even begun according to this index. A correction is when prices fall more than 10% from peak, in less than a year, which we haven’t seen yet. If I didn’t know any better, it would appear that mortgage sellers bank executives are misinformed. How strange.

Vancouver Real Estate Prices Hit A New All-Time High

Vancouver real estate prices, driven entirely by condo appreciation, hit a new all-time high. Prices increased 0.5% from the month before, and are up 15.43% from the same month last year. Prices on the index showed monthly increases in 13 of the past 15 months. Teranet-National Bank analysts noted that gains are tapering, and this is “consistent with the Real Estate Board of Greater Vancouver.”

Montreal Real Estate Prices Drop 0.2%

The market brokerages have been attempting to rocket, appears to be a failure to launch. The index showed that prices declined 0.2% in March, and are up just 4.27% from the same month last year. Annual price increases peaked in December at just under 6%, and has been tapering ever since. Technically speaking, Montreal has yet to outperform the general Canadian market. Despite what you may have read in Montreal media.

Canadian real estate prices are acting unusual compared to movements typically made outside of a recession. However, they are moving in a typical real estate cycle. A gain as large as we’ve seen nationally, has never not been followed by a negative price movement. Try to act surprised when you see it. Bank economists will.

Today we take a look at the latest from the Royal Commission into Financial Service Misconduct, which recommenced its hearings yesterday again, with a focus on the Financial Planning Sector.

Financial Advisers provide advice on a range of areas of consumer finance, investing, superannuation, retirement planning, estate planning, risk management, insurance and taxation.

ASIC says between 20 and 40% of the Australian adult population use or have used a Financial Planner. That means that around 2.3 million Australians over 18 received advice. A number of issues have surfaced in recent years, including charging fees for no service, or advice not provided in full, the provision of inappropriate financial advice, as well as improper conduct by financial advisors and the misappropriation of customer’s funds.

There has been massive growth in the number of financial advisers, to more than 25,000 up 41% from 2009. 5,822 Financial Advice licences were issued in Australia to firms able to offer advice. What you may not know is that the top five players in Financial Advice in Australia are the big four banks and AMP, who together have nearly 48% of the $4.6 billion dollars in annual revenue. 30% of advisers work for one of the major banks and 44% work for the top 10 organisations by revenue, so it is very concentrated. Then there is a long tail of smaller organisations with 78% operating a firm with less than 10 advisors. The average advice licence covers 34 individuals operating under it.

There have been a number of significant scandals relating to the provision of financial advice in recent years.

Townsville based Storm Financial encourage investors to borrow against their home to invest in indexed share funds, in a “one size fits all model” of advice. Storm collapsed in 2009 will losses of more than $3 billion dollars. Around 3,000 of its 14,000 clients had suffered significant losses. Many of the investors were retired or about to retire, and with limited assets and income. Some lost their family homes or had to postpone their retirement. The founders were found to have caused or permitted inappropriate advice to be given and had breech their duty of care under the corporations’ act. Specifically, the one size fits all model of advice failed to take into account individual circumstances which led to devastating consequences for the individual investors. They had focused too much on the profitability of the business as opposed to the best interests of individual investors. ASIC worked with a number of major players for customers who had made investments through Storm. CBA undertook to make $136 million dollars in compensation to many CBA customers who borrowed from the bank to invest through Storm and who had suffered financial losses. This is in addition to $132 million CBA paid under the Storm resolution scheme. ASIC looked at settlements distributed by Macquarie Bank to Storm investors leading to a revised agreement where the bank agreed to pay $82.5 million by way of compensation and costs. Bank of Queensland agreed to pay $17 million as compensation for Storm related losses.

The second scandal involved Commonwealth Financial Planning Limited. A whistle-blower revealed allegations of misconduct within CFL to ASIC in 2010. It was suggested that some advisers were encouraging investors to invest in high risk, but profit generating products which were not appropriate. Some were even switching products without the client’s permission. This also included forging client signatures. When the GFC hit in 2008, thousands of CFL clients, many of whom were nearing or in retirement, lost significant amounts as a result of this misconduct. More than $22 million was paid to clients in compensation for receiving inappropriate financial advice from two financial planning advisers. Later it became evident the misconduct was more widespread so CBA implemented a second programme of compensation relating to advice from advisers. Their Open Advice programme had conducted more than 8,600 assessments, of which more than 2,500 required compensations to a total of $37.6 million has been offered.

So turning to the hearings. First up was Peter Kell from ASIC who described the “Fee for no service” problem.

The Future of Financial Advice reforms (FOFA) has tightened the rules, but the fees can be significant. And as we will see, some players simply took the fees to bolster their profits.

Next up was AMP, and we heard over the next day or so of more than 20 occasions when AMP failed in their duty to notify ASIC of a number of potential breaches.

Despite the fact AMP was aware of a range of issues they simply allowed the practices to continue. There was an absence of monitoring activities, what AMP said it was going to do to ASIC, e.g. training for staff in new procedures was different from what they actually did. The issues had been occurring since 2009, and AMP acknowledge that on at least 20 occasions they made false and misleading statements to ASIC about potential breeches.

Worse, the Royal Commission revealed today that AMP’s law firm, Clayton Utz, removed outgoing chief executive Craig Meller’s name from a draft of a critical report about the business.

So once again we see the cultural norms in financial services driving poor behaviour, which may bolster profits but at the expense of their customers, and an apparent willingness to avoid the issues with the regulators. This is shameful, but not surprising.

So we see mismanagement again, and failure of regulation.

We suspect we will see more of the same in the day ahead. Frankly I am not surprised because the cultural norms we see displayed here are precisely the same as were observed in the previous lending related hearings. The quantum of change required within our financial services organisations is profound and I also believe the scope of the Royal Commission should be expanded to include the role and function of our regulators.

Multiple failures are clearly costing households dear. But then the companies seem willing to cop the settlements, and move on, without root cause analysis and fixing the problem. This is not acceptable behaviour in my book and is well below community expectations.

He says:

He says:

.PNG)