ANZ says it will explore the possibility of an initial public offering (IPO) of

ordinary shares in UDC Finance as part of a range of strategic options for UDC’s future.

A wholly-owned subsidiary of ANZ Bank New Zealand, UDC is New Zealand’s leading asset finance company funding plant equipment, vehicles and machinery.

ANZ New Zealand CEO David Hisco said: “We have been looking at strategic options for UDC’s future for some time as part of ANZ’s strategy to simplify the bank and improve capital efficiency.

“While UDC is continuing to perform well and there is no immediate requirement to make decisions, after last year’s planned sale to HNA did not proceed it makes sense to keep examining a broad range of options for UDC’s future.

“This will include exploring whether, subject to market conditions, an IPO would be in the interests of UDC’s staff and customers, and ANZ shareholders.

“The range of strategic options we have for UDC, including approaches we have received regarding the business and the option of retaining it, will take a number of months to examine before any decision is made. In the meantime, it will continue to be business as usual for UDC,” Mr Hisco said.

The Chinese government has appointed a new head of its central bank. Yi Gang, currently the deputy governor of the People’s Bank of China, will take over the leadership from Zhou Xiaochuan, who had been in the position since 2002.

A US-trained economist, Yi received his doctorate in economics from the University of Illinois in 1986. He was a professor at Peking University in China following various academic positions in the US, before joining China’s central bank in 1997. Yi is known in academia for his expertise on inflation and price instability.

Yi developed his technocratic career exclusively within the headquarters of the central bank, taking up various leading positions in areas of monetary policy, exchange rate policy, and foreign reserve management. He then became the right-hand man of Zhou, who dominated Beijing’s economic policy-making for a record 15 years.

However Yi’s governorship came as a surprise, given the widely circulated rumours of other powerful contenders, such as Liu He, now announced as a vice premier of China, and Guo Shuqing, the chairman of China Banking Regulatory Commission.

But the appointment makes sense if the reshuffle of president Xi Jinping’s economic team is taken into account, as like-minded liberals lining up in key positions. Yi will actually work directly under Liu, who also trained in the US, ensuring that the government keeps in close consultation with the central bank while the bank does not stray politically.

Problems the new governor will have to confront

Now that the jockeying for the top position at the central bank is over, the new governor is bound to carry on Zhou’s liberal legacy and to tackle some of the more daunting challenges the Chinese economy faces.

First up is the need to further strengthen the central bank, which has been given extra duties in financial legislation and regulation in the latest round of administrative streamlining announced at the People’s Congress. After all, the authority of the central bank in government circles over the last two decades has largely hinged on the bank playing an indispensable role in providing professional expertise.

A distressed financial system could trigger a systemic economic collapse. To reign in this possibility, Yi will have to work closely with authorities in the State Council, China’s cabinet, to contain the risks to a manageable scale.

The bank will have to walk a fine line here. It must contain the shadow banking sector, which is largely beyond the radar of the authorities. At the same time it has to make sure such tightening does not choke financial innovations embodied by the burgeoning internet finance and fintech.

Equally, if not more important, the financial reforms must be taken to facilitate China’s grand economic transition. In the short to medium term, this entails a further aligning of China’s interest rates to China’s market levels.

They also need to bring its exchange rates in line with international market levels, open its financial markets in a gradual and orderly fashion, and push for the use of the Chinese currency in the global market. This is an ambitious project initiated by Zhou with the goal of seeing the renminbi’s international status on par with the greenback.

A more open and liberal financial system in China is of course good news for the world economy as well because central banks need to work together to address increasingly divergent policy priorities among advanced and emerging economies.

Whether or not Yi becomes the next “Mr RMB” (as Zhou is often dubbed), he needs to be the “Dr Reformer” at this critical stage of both the Chinese and global economy.

Author: Hui Feng, Future Fellow and Senior Research Fellow, Griffith University

The Royal Commission into Financial Services Misconduct, yesterday spent time with ANZ, and examined their expenses validation and verification processes, especially when applications were made via the broker channel.

Astonishingly, it appears that the bank may ignore the expense data from the broker as submitted (so the Commission asked why they capture the data at all!). Household Expenditure Measure (HEMs) figured in the discussion, as a test which was used by the bank in the assessment process. It will be interesting to see if the Commission views this approach is compliant with their responsible lending obligations.

It begs the question more broadly, are mortgages held by the banks supported by appropriate expense calculations? Some are saying that up to 40% of loans on book may have issues.

We also note that the “mortgage power” type calculators available on bank web sites to give an indication of a borrowers ability to get a mortgage, on average now gives a mortgage figure some 20% lower than a couple of years back.

So, many borrowers would not now get the mortgage they did then. Think about the implications for existing borrowers seeking to refinance, or to move from interest only loans to principal and interest loans!

There was also more data on lower auction clearance rates. Plus predicted falls in home prices, from Moody’s.

When you overlay the Commission findings, with the sales trends (deep discounts are now a feature of current sales, see above), it seems to me home prices are set for more falls in the months ahead.

We discussed this in our latest video blog.

More broadly, the Commission shows the massive repair job the banks have to do on their reputations and culture. No wonder their share prices are down. Of more significance are the structural risks to the economy, as households continue to struggle with over-committed budgets thanks to lax lending. This is unlikely to end well.

The purpose of the Commission was to remove uncertainty from the banking sector, but as it goes about its business, in fact the levels of concern are rising. It has royally back-fired!

But there is a good chance that customer outcomes will be enhanced as the consequences are digested. This would be an excellent outcome. But not an intended one.

CBA’s new CEO Matt Comyn has written to staff as the the blow touch is applied by the inquiry.

This week the Royal Commission into Misconduct in Banking, Insurance and Superannuation commenced hearings in Melbourne.

From the outset, we said that we were absolutely determined to be cooperative and open with the Commission. Unfortunately, as we heard on Tuesday, our first submissions did not meet the Commission’s expectations. This was never our intention and we will resubmit our information as soon as possible and ensure we have fully met the requests of the Commission. We will work to make sure this doesn’t happen again.

There will be cases highlighted next week where customers have been treated unfairly by us. In many cases, our actions have had a significant impact on the financial and emotional wellbeing of our customers. This is unacceptable.

Where we have made mistakes we must and will take responsibility for them, we will make things right for our customers, and not repeat the same mistakes. We will exceed our regulatory and compliance obligations, and enhance the financial wellbeing of every single customer we serve.

Together, we will make our bank better, and one we can all continue to be proud of.”

As reported in the Business Insider, Moody’s Investor Services thinks there will be further declines to come, suggesting that Sydney prices will suffer a “correction” in the year ahead.

“Incomes in NSW have increased faster than the national average and underpin some of the recent gains in home values,” Moody’s says, pointing to the chart below. “However, housing values have risen even faster and are overvalued relative to equilibrium value. Therefore, Moody’s Analytics expects a correction across NSW.”

Preliminary auction clearance rates soften as the number of auctions surges to the second busiest week so far this year.

There were 3,097 homes taken to auction across the combined capital cities this week, making it the second busiest week of the year so far, with preliminary results showing a 67.5 per cent success rate. In comparison, 1,764 auctions were held last week and the final clearance rate came in at 63.3 per cent. Over the same week last year, auction volumes were lower with 2,916 homes going under the hammer across the combined capital cities, although the clearance rate was a stronger 74.1 per cent.

In Melbourne, a preliminary auction clearance rate of 68.9 per cent was recorded across 1,656 auctions this week, down from 70.8 per cent across just 453 auctions last week. Over the same week last year, 1,441 homes were taken to auction across the city, returning a clearance rate of 77.0 per cent.

Sydney was host to 1,055 auctions this week, with preliminary results showing a 67.8 per cent success rate, up from 62.2 per cent across 974 auctions last week. This time last year, the clearance rate was a stronger 76.8 per cent across 1,001 auctions.

Excluding Tasmania, where all 3 reported auctions were successful, Adelaide recorded the highest preliminary clearance rate this week (69.7 per cent).

Looking at auction volumes, Perth was the only city to see a slight fall in the number of homes taken to auction this week, while all other cities increased week-on-week.

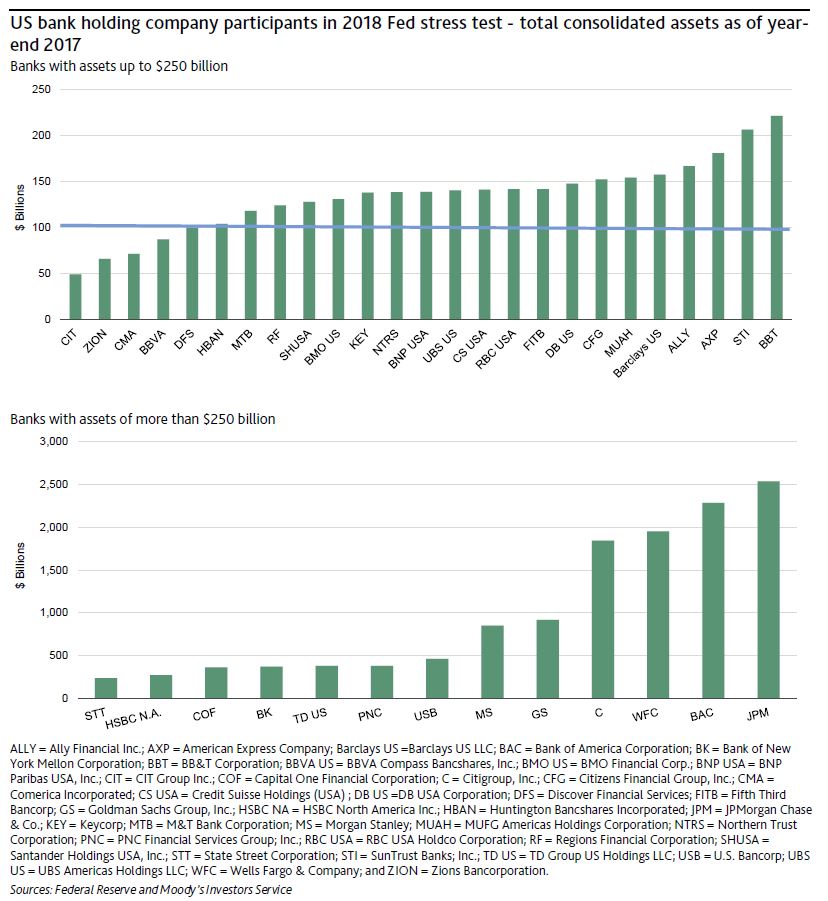

Last Wednesday, the US Senate passed the Economic Growth, Regulatory Relief, and Consumer Protection Act. A key component of this bill increases the asset threshold for a bank to be designated a systemically important financial institution (SIFI) to $250 billion of total consolidated assets from $50 billion, the threshold defined in the Dodd-Frank Act of 2010.

For US banks with assets of less than $250 billion, the higher asset threshold for SIFI designation is likely to lead to a relaxation of risk governance and encourage more aggressive capital management, a credit-negative outcome.

SIFI banks are subject to the enhanced prudential standards of the US Federal Reserve (Fed). The regulatory oversight of SIFIs is greater than for other banks, and SIFIs participate in the Fed’s annual Dodd-Frank Act stress test (DFAST) and the Comprehensive Capital Analysis and Review (CCAR), which evaluate banks’ capital adequacy under stress scenarios. Furthermore, transparency will decline with fewer participants in the public comparative assessment the stress tests provide.

In 2018, the 38 bank holding companies shown in the exhibit below are subject to the Fed’s annual capital stress test. Passage of the bill into law would immediately exempt four banks with less than $100 billion of assets from the Fed’s enhanced prudential standards, which includes the stress test and living will requirements. These banks will have the most leeway in relaxing risk governance practices and managing their capital.

The 21 banks at the right of the top exhibit that have assets of $100-$250 billion1 could become exempt from enhanced prudential standards 18 months after passage of the bill into law. However, the Fed will have the authority to apply enhanced oversight to any bank holding company of this asset size and will still conduct periodic stress tests. In the 18 months after passage into law, it will be up to the Fed to develop a more tailored enhanced oversight regime for the $100-$250 billion asset group. The Fed also could continue to apply the same enhanced prudential standards. Therefore, it is difficult to assess the potential for their easier risk governance practices until more about the regulatory oversight is known.

If many of these banks are no longer required to participate in the public stress tests, it would reduce transparency. The quantitative results of DFAST and CCAR provide a relative rank ordering of stress capital resilience under a common set of assumptions. The loss of such transparency is credit negative.

For the largest banks, those with more than $250 billion in assets that remain SIFIs, there are no changes in the Fed’s supervision. The bill also specifies that foreign banking organizations with consolidated assets of $100 billion or more are still subject to enhanced prudential standards and intermediate holding company requirements.

In order to become law, the bill must also be passed by the US House of Representatives and signed by the president. This year’s annual Fed stress test will proceed as usual with submissions by the banks due 5 April, with results announced in June.

The Australian Prudential Regulation Authority (APRA) today announced that it has granted approval to ING Bank (Australia) Limited to begin using its internal models to determine its regulatory capital requirements for credit and market risk, commencing from the quarter ended 30 June 2018.

ING is the first authorised deposit-taking institution (ADI) to be accredited since APRA revised the accreditation process in 2015. Consistent with suggestions from the 2014 Financial System Inquiry, APRA’s changes were intended to make the process more accessible for ADIs to achieve accreditation, without weakening the overall standards that advanced accreditation requires.

APRA continues to engage with other ADIs seeking accreditation to use internal models for calculating regulatory capital requirements.

The Reserve Bank of Australia should follow the example of other central banks and be clearer about when and how rates will change, called “forward guidance”, to make its policy more effective.

At the moment the RBA follows an approach to implement monetary policy known as inflation targeting. This means it has a numerical target for inflation (an average 2-3% inflation over the medium term) and a framework to achieve that target (how it thinks monetary policy affects the economy, and how it communicates policy decisions).

Australia’s cash rate is at a historical low of 1.5%. So if there’s any adverse shock to our economy (for example, a large correction in house prices), the RBA would have little room to reduce the cash rate before getting to 0% – the zero lower bound on nominal interest rates.

At that point, you can’t cut rates anymore. Research shows economic shocks can have a more severe impact on economic activity when the policy rate is at, or near, zero.

Instead the RBA should be more explicit about the conditions that would lead to a rate change. Research shows this has stimulated economic recovery before.

How rates work at the moment

To understand forward guidance it helps to understand conventional thinking about monetary policy. The RBA controls inflation by adjusting the cash rate, which is the interest rate on overnight loans in the interbank market.

Changes in the cash rate change longer-term interest rates in the economy. These then influence households’ and businesses’ spending and investment plans. These decisions also determine demand and inflation.

For example, suppose inflation is below target. A cut in the cash rate reduces longer-term interest rates, which encourages people to buy goods and services (falls in long-term deposit rates and government bonds reduce the incentive to save) and invest (commercial and mortgage loans are cheaper). Rising demand sends prices up, which brings inflation back to target.

As with other central banks around the world, the RBA also explains the rationale for its policy decisions. For example, in the Statement of Monetary Policy, released four times a year, the bank sets out its assessment of current domestic and international economic conditions, along with an outlook for Australian inflation and output growth.

The purpose of these announcements is to enhance the credibility of the inflation target. If people trust the RBA will implement policy to achieve the inflation target, they will make plans around what they spend and how they price goods and services based on this. This makes inflation easier to control.

How being clearer about rates helps

While the RBA might not be able to influence the current cash rate, it can still influence longer-term rates by making announcements about its future policy decisions. Long-term interest rates usually change depending on what people expect of future cash rate changes.

So if monetary policy can influence these expectations, it can move long-term rates.

Of course, words are cheap. To make these declarations credible the RBA would need to communicate its plans for the future cash-rate, with modelling and forecasts justifying those plans.

Economists could then judge whether the RBA is meeting its objective through good luck or good policy. If it’s through good policy, it enhances the RBA’s credibility and, in a virtuous circle, this gives the bank policy more influence over expectations.

A prominent example of forward guidance comes from the United States’ central bank, the Federal Reserve. In December 2008, when the federal funds rate (the US equivalent of the Australian cash rate) was first at the zero lower bound, the Federal Reserve announced:

The committee anticipates that weak economic conditions are likely to warrant exceptionally low levels of the federal funds rate for some time.

Translated, the Fed anticipated keeping the federal funds rate at zero for a considerable time. This communication was meant to influence the public’s expectations about the future course of US monetary policy, and to have consumers and businesses expect an expansionary monetary policy for some time.

During the recovery, the Fed refined its communication strategy to become more explicit about the economic circumstances that would lead to a change in policy. For example, in June 2013, the committee that sets rates anticipated that:

…this exceptionally low range for the federal funds rate will be appropriate at least as long as the unemployment rate remains above 6-½%.

This type of announcement gives people more information about the strategy the Fed will take with rates, rather than simply providing forecasts about what it expects future economic conditions to be like (which doesn’t need to have any information about policy strategy).

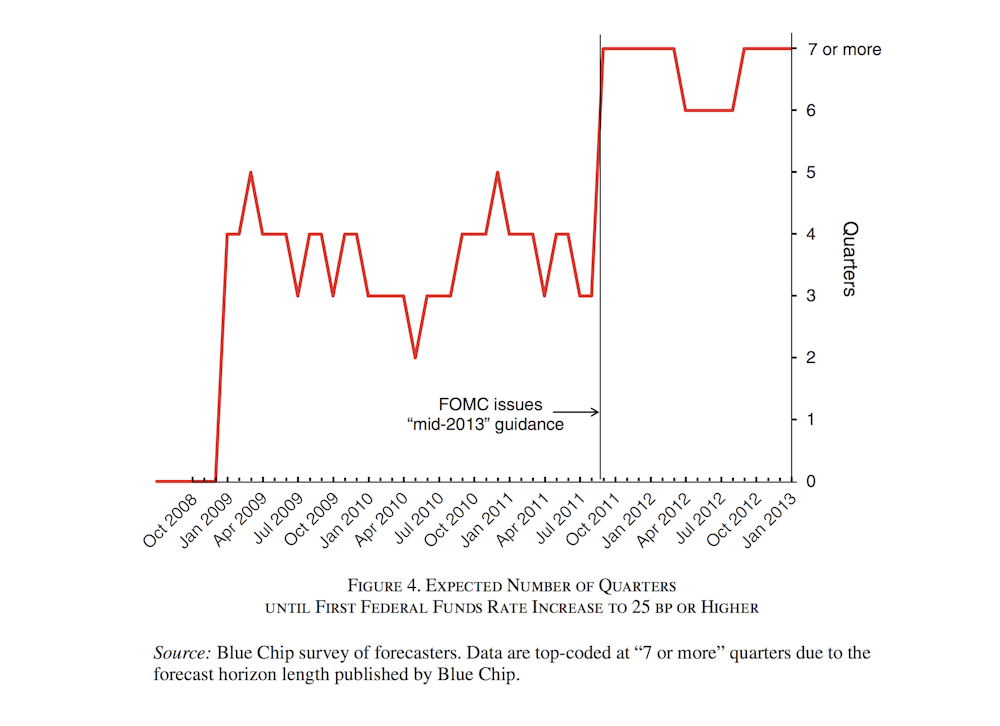

Recent evidence confirms this had an impact on businesses’ expectations. Right after the June 2013 announcement by the Federal Reserve, there was an increase in the number of quarters until businesses expected the US policy rate to increase above 25 basis points.

FOMC= Federal Open Market Committee (which sets rates)Swanson and Williams: the zero bound and interest rates, Author provided

Other research also suggests forward guidance influenced private sector expectations and stimulated the economic recovery after the global financial crisis.

At the moment, the RBA doesn’t produce statements about future monetary policy and how this would change if the economic environment changed. But the bank could do this.

The RBA has the luxury to develop its communications policy during a time of economic calm, unlike the Federal Reserve, which was forced to experiment with new policies during the worst recession since the Great Depression.

If the RBA waits until a future crisis, it would limit the power forward guidance could have in our economy.

Efrem Castelnuovo, Principal Research Fellow, Melbourne Institute of Applied Economic and Social Research, and Professor of Economics, Department of Economics, University of Melbourne;

Bruce Preston, Professor of Economics, University of Melbourne; Giovanni Pellegrino, Postdoctoral Research Fellow, University of Melbourne

Ten years ago the Australian government launched a National Partnership Agreement on Homelessness (NPAH). It injected A$800 million into homelessness services and A$300 million to build 600 new homes for people experiencing homelessness. It was later announced that another A$400 million would be available under the National Affordable Housing Agreement (NAHA) to build new housing and supported accommodation for the homeless. Total recurrent expenditure (at 2016-17 prices) on homelessness services has increased by 28.8%, from A$634.2 million in 2012-13 to A$817.4 million in 2016-17.

But despite this, the number of people experiencing homelessness and the rate of homelessness have both increased. Our research points to problems in the public housing system as one of the more important causes of these increases.

According to census figures released on Wednesday by the Australian Bureau of Statistics (ABS), the number of homeless people in Australia has risen by 14% to 116,427. The rate of homelessness has increased from 47.6 people per 10,000 of the population in 2011, to 49.8 per 10,000 now. (The ABS defines homelessness here.)

There is some good news: the numbers of Indigenous homeless and homeless children and youth (aged 12-18) have declined by 26%, 11% and 7% respectively since 2011. But on the downside, increases are particularly pronounced in New South Wales (where the homelessness rate rose by 27% and among people aged over 65 (by just over 30%) and overseas-born migrants (by 40%).

Why are we still going backwards?

Changes in Australian housing and welfare systems and wider social and economic developments appear to have more than offset any benefits from the NPAH and NAHA. Our research sheds some light on the role played by Australia’s housing system. Using the internationally recognised and unique Journeys Home longitudinal survey, we find that public housing is the most important factor in preventing homelessness among vulnerable people.

Public housing is particularly effective because it is affordable. It has also traditionally offered a long-term refuge for precariously housed people. This is because public housing leases provide the benefits of security of tenure commonly associated with home ownership.

It is perhaps no accident that NSW was one of the first states to introduce fixed-term tenancies in public housing. This eroded one of the major attributes of tenure, in a state that has seen relatively large increases in homelessness numbers.

The empirical evidence also suggests that community housing fails to provide the same protection for people at risk of homelessness. While community housing is affordable, the security of tenure is weaker, which may explain these findings.

Despite such evidence, the stock of public housing continued to decline between the 2011 and 2016 censuses. State government-initiated transfers of stock to the community housing sector accelerated this trend. In 2013 Australia had a public housing stock of 325,226 dwellings. This declined by 3.2% to 314,864 usable dwellings in 2017.

Where are the additional homeless coming from?

One of the more alarming changes is a sharp increase in the number of homeless people over 65. This partly reflects Australia’s ageing population. However, the increase is such that the elderly’s share of the total homelessness count has also risen.

Furthermore, our research suggests that this trend could become protracted. This is because the homeless elderly have much less chance of escaping into formal housing than younger people experiencing homelessness. We have little understanding of the reasons for this, but gaps in service provision to the aged could be partly responsible.

The other group who feature prominently among the homeless are overseas migrants. They now make up 46% of the homeless, despite representing just 28% of the Australian population. The number of homeless overseas-born migrants has soared by 40% since the 2011 Census, from 38,085 to 53,606 people.

It turns out that homeless overseas-born migrants are concentrated among those living in severely overcrowded dwellings – a little over half of those living in these conditions were born overseas. We know little about these homeless people. Discrimination could be a factor, though some characterise this group as students living in group households who should not be considered homeless. But this is speculation and further study is certainly required.

In view of the latest census results, it is clear to us that governments need to reassess their approach to what is turning into an intractable social problem.

We do not deny that situational factors, such as drug abuse, domestic violence and so forth, are important here. But equally, there is strong evidence that structural problems in our housing market are a significant cause of growth in the numbers of homeless people.

Until these problems are resolved, service provision and support will remain a band-aid masking deeper social and housing system issues.

Gavin Wood, Emeritus Professor of Housing and Housing Studies, RMIT University; Guy Johnson, Professor, Urban Housing and Homelessness, RMIT University; Juliet Watson, Lecturer, Urban Housing and Homelessness, RMIT University; Rosanna Scutella, Senior Research Fellow, Centre for Applied Social Research, RMIT University