The ABA says that in a first for the industry, retail banks in Australia will be required to sign up to the new Banking Code of Practice as a condition of membership to the Australian Banking Association.

Anything which improves the cultural norms of banking should be welcomed, but this is very little and very late – and could be interpreted as a reaction to the Royal Commission evidence in the past few days.

Acting ethically is certainly helpful, but banks should be putting the interests of their customers first and foremost. This can build trust, one brick at a time. All the evidence shows that do this, customers win, and benefits also flow to shareholders thanks to greater customer loyalty and brand value. We need cultural reform from within the banks and the rate of reform needs to be accelerated significantly.

This is what the ABA has said.

The new Code, currently awaiting ASIC approval, has been completely rewritten and updated to better meet community standards and will be binding and enforceable.

CEO of the Australian Banking Association Anna Bligh said the new Code, now to become a requirement of ABA membership, was a significant ramp up of the industry’s efforts to improve conduct and culture.

“In the past it was up to each individual bank if they wanted to sign up however this new customer focussed Code will become compulsory for all ABA members with a retail presence,” Ms Bligh said.

“This new code will be binding, forming part of relevant customer contracts, enforceable by law and will be monitored by an independent body.

“Australians expect their banks to operate in an ethical and appropriate way when they apply for a credit card, home, small business loan or other financial product.

“While there is much work still to be done, Australia’s banks are serious about genuine reform which addresses conduct and culture, with the Banking Code of Practice a cornerstone of these efforts.

“The industry is committed to genuine reform which will rebuild trust with the Australian community, with the new Code an important step in the right direction.

“Once approved by ASIC, the Code will deliver changes across the board with plain English contracts for small business, no more unsolicited offers to increase credit card limits, greater transparency around fees and customers having an ability to cancel a card online – just to name a few,” she said.

Finalised and lodged with ASIC in December the new Code outlined important changes for individuals and small businesses, including:

Plain English contracts

Ending unsolicited offers of credit card increases

The mandated ability for customers to cancel a credit card online

Improved transparency around fees by telling customers about service fees immediately before they occur.

Bank who have signed up are required to include in its contracts a statement that the Code applies, which in turn is a legally enforceable document. This new industry code will have the force of the law. There will be a 12 month implementation period for the Code once ASIC has given its approval.

In addition, an independent body, the Banking Code Compliance Committee (BCCC) will monitor and oversee compliance with the code. The committee has power to investigate breaches of the Code and apply sanctions if necessary.

Samsung Pay is a secure and easy-to-use mobile payment service that allows users to add credit and debit cards from participating financial institutions, and loyalty cards from participating merchants.

NAB Executive General Manager of Consumer Lending, Angus Gilfillan, said Samsung Pay complements the bank’s mobile payments service, NAB Pay, which customers can already use on compatible Samsung and other Android devices.

“We are continuing to invest in giving our customers the best digital payments experience,” Mr Gilfillan said.

“We know Australians increasingly want to pay for their purchases quickly and conveniently. The growth in ‘tap and pay’, and take up of NAB Pay since we launched it two years ago, has been remarkable.

“By adding Samsung Pay, we’re giving our customers more choice in digital wallets.”

NAB customers can also use Samsung, Fitbit, and Garmin smartwatches to make contactless payments, and NAB will also be adding Google Pay to its suite of mobile payment services very soon.

“We see the highest number of NAB Pay transactions being made at supermarkets, restaurants, and at takeaway venues – which is exactly when you want to be able to make quick and easy payments,” Mr Gilfillan said.

Samsung Electronics Australia’s Head of Products and Services, Mark Hodgson, says Samsung is thrilled to be able to provide the Samsung Pay experience to even more Australians.

“Our partnership with NAB builds on our commitment to providing a simple and secure digital wallet experience to every Australian using a Samsung smartphone or wearable. We believe our collaboration with partners like NAB will help further enhance our mobile experience, and we look forward to evolving the portfolio further over the upcoming year.”

NAB also announced last year that it is working with the Commonwealth Bank of Australia and Westpac to build Beem It, a free app enabling anyone to make an instant payment using their smartphone, and to request payment from someone who owes them money or to split a bill.

“We are continually looking at all options to provide our customers with access to safe and secure ways to make digital payments.”

“From our own mobile banking app and NAB Pay, to a range of other payment platforms and services, we’re investing in solutions to help our customers use and manage their money. We’re very pleased to be launching Samsung Pay to our customers now,” Mr Gilfillan said.

NAB’s Mobile Banking App includes a range of world-leading features to help customers have more control over their cards. Features include the ability to switch on or off online transactions, overseas card usage, and ATM withdrawals, and to block, unblock, and replace a card that may have been lost.

The app also includes real-time alerts and merchant information, providing customers more information about their transactions straight away, and a range of options to help them know more about and manage their repayments and accounts.

But research suggests the very organisational structure of banks makes it difficult to hold directors and senior executives criminally responsible for systemic misconduct.

The way corporations are arranged, how decision-making is delegated, and information is gathered and distributed, appears to fragment and diffuse individual responsibility.

This makes it hard to establish criminal culpability (the standard of proof is “beyond a reasonable doubt”), even if directors and executives remain in control of processes and are paid bonuses based on organisational performance.

Certain clauses in commercial contracts and the structuring of corporate groups across multiple jurisdictions can also be used to frustrate investigations.

In cases where corporate criminality can be more directly tied to decisions by executives or directors, subsidiaries (or internal divisions) can be dissolved or sold.

A senior ANZ executive admitted to the Royal Commission that the bank has no process to verify income and expenditure statements in loan applications.

This is despite laws requiring lenders to take reasonable steps to establish borrowers’ ability to service loans.

Moreover, this was not an oversight but a deliberate decision to substitute regulatory requirements for less rigorous internal practices.

Decoupling occurs when corporations say publicly that they follow the law, and even create policies to tick regulatory boxes, but then do something entirely different as a matter of standard practice.

With existing corporate governance structures in place decoupling is extremely difficult to detect from the outside. It takes active oversight by regulators, internal whistleblowing or public inquiries with coercive powers to gather evidence to identify it.

Certain types of (re)organisation also enable systemic misconduct because they diffuse responsibility and diminish individual culpability.

These include sub-contracting, the use of consultants, creation of subsidiaries and transnational structures, relocating work to low transparency jurisdictions, and the use of franchising systems, dealer networks and agents.

These decisions about organisational structure are made at the board or senior executive levels.

Implications for the Royal Commission

The banks have publicly asserted that their boards are focused on ensuring good corporate governance, and that they have the structure (explicit policies, clear lines of reporting/delegation) to ensure regulatory compliance.

But what has emerged at the Royal Commission shows these structures either don’t exist or don’t function as they should.

Although Australia has stronglaws to jail company directors for policies that facilitate systemic misconduct, this rarely occurs.

The lack of prosecutions, convictions and commuting of jail time embolden other senior executives and help them rationalise away the seriousness and impact of similar conduct.

There are a number of factors that the Royal Commission and federal government should address to prevent future systemic misconduct, beyond just creating a temporary lull before a return to business as usual.

Australian companies only have one board and that is at the heart of the problem. While all board directors are responsible for the management and governance of corporations, in practice they delegate authority to executive directors who then operate with wide discretion. This includes enacting policy and reorganising the corporation in ways that diffuse accountability and criminal culpability.

While all corporate governance systems have their weaknesses, in two-tiered boards, executive directors are overseen by supervisory boards who appoint their own auditors. These kinds of boards constrain executive director discretion, making decoupling more difficult.

In addition to changing the governance of organisations, regulators must be given more resources, greater powers to collect evidence and explicit directions to mount investigations before and not after the systemic misconduct has been identified.

The use of consultants and the rapid expansion of their business model which bundles accounting, audit and legal services together presents is another threat to accountability and transparency. It is also an obstacle to investigating and successfully prosecuting systemic corporate misconduct.

Andrew Linden, Sessional/ PhD (Management) Candidate, School of Management, RMIT University; Warren Staples, Senior Lecturer in Management, RMIT University

The New Zealand Government’s New Policy Targets Agreement requires monetary policy to be conducted so that it contributes to supporting maximum levels of sustainable employment within the economy.

The new focus on employment outcomes is an outcome of Phase 1 of the Review of the Reserve Bank Act 1989, which the Coalition Government announced in November 2017.

“The Reserve Bank Act is nearly 30 years old. While the single focus on price stability has generally served New Zealand well, there have been significant changes to the New Zealand economy and to monetary policy practices since it was enacted,” Grant Robertson said.

“The importance of monetary policy as a tool to support the real, productive, economy has been evolving and will be recognised in New Zealand law by adding employment outcomes alongside price stability as a dual mandate for the Reserve Bank, as seen in countries like the United States, Australia and Norway.

“Work on legislation to codify a dual mandate is underway. In the meantime, the new PTA will ensure the conduct of monetary policy in maintaining price stability will also contribute to employment outcomes.”

A Bill will be introduced to Parliament in the coming months to implement Cabinet’s decisions on recommendations from Phase 1 of the Review. As well as legislating for the dual mandate, this will include the creation of a committee for monetary policy decisions.

“Currently, the Governor of the Reserve Bank has sole authority for monetary policy decisions under the Act. While clear institutional accountability was important for establishing the credibility of the inflation-targeting system when the Act was introduced, there has been greater recognition in recent decades of the benefits of committee decision-making structures,” Grant Robertson said.

“In practice, the Reserve Bank’s decision-making practices for monetary policy have adapted to reflect this, with an internal Governing Committee collectively making decisions on monetary policy. However, the Act has not been updated accordingly.”

The Government has agreed a range of five to seven voting members for a Monetary Policy Committee (MPC) for decision-making. The majority of members will be Reserve Bank internal staff, and a minority will be external members. The Reserve Bank Governor will be the chair.

“It is my intention that the first committee of seven members would have four internal, and three external members. Treasury will also have a non-voting observer on the MPC to provide information on fiscal policy,” Grant Robertson said.

The MPC is expected to begin operation in 2019 following passage of amending legislation. There will be a full Select Committee process for the legislation.

Reserve Bank Governor-Designate, Adrian Orr, said that the PTA recognises the importance of monetary policy to the wellbeing of all New Zealanders.

“The PTA appropriately retains the Reserve Bank’s focus on a price stability objective. The Bank’s annual consumer price inflation target remains at 1 to 3 percent, with the ongoing focus on the mid-point of 2 percent.

“Price stability offers enduring benefits for New Zealanders’ living standards, especially for those on low and fixed incomes. It guards against the erosion of the value of our money and savings, and the misallocation of investment.”

Mr Orr said that the PTA also recognises the role of monetary policy in contributing to supporting maximum sustainable employment, as will be captured formally in an amendment Bill in coming months.

“This PTA provides a bridge in that direction under the constraints of the current Act. The Reserve Bank’s flexible inflation targeting regime has long included employment and output variability in its deliberations on interest rate decisions. What this PTA does is make it an explicit expectation that the Bank accounts for that consideration transparently. Maximum sustainable employment is determined by a wide range of economic factors beyond monetary policy.”

Mr Orr said that he welcomes the intention to use a monetary policy committee decision-making group, including both Bank staff and a minority of external members.

“Legislating for this committee will give a strong basis for the Bank’s use of a committee decision-making process. Widening the committee to include external members also brings the benefit of diversity and challenge in our thinking, while enhancing the transparency of decision-making and flow of information.”

Phase 2 of the Review is being scoped. It will focus on the Reserve Bank’s financial stability role and broader governance reform. Announcements on the final scope will be made by mid-2018 and subsequent policy work will commence in the second half of 2018.

State-owned power networks have spent up to A$20 billion more than was needed on the electricity grid, and households and businesses in New South Wales, Queensland and Tasmania are paying for it in sky-high power bills.

A new Grattan Institute report, Down to the Wire, shows that electricity customers in these states would be paying A$100-A$400 less each year if the overspend had not happened.

The problem is that state governments, worried about blackouts and growing demand for electricity, encouraged the networks to spend more in the mid-2000s. But the networks overdid it, and now consumers are paying for a grid that is underused, overvalued, or both.

Why we built too much

The grid includes high-voltage transmission lines that carry electricity over large distances, as well as low-voltage poles and wires that connect to homes and businesses. Networks are built to cope with those times of highest demand for electricity. Yet the growth in the value of network assets has far exceeded growth in customer numbers, total demand, or even peak demand.

Demand for electricity did grow rapidly in the early 2000s, but since then it has slowed substantially as more and more households have installed solar panels, and appliances have become more energy efficient. Networks may have overbuilt because they expected that demand would continue to grow.

Yet the overbuilding has occurred almost exclusively in the public networks. Why would government ownership lead to such high costs?

There are two main reasons. First, investment in electricity networks boosts state government revenues because public networks pay a fee to the state to neutralise their lower borrowing costs (as well as the dividend they pay to the state as the owner). Second, a government-owned business might come under political pressure to prioritise goals such as reliability or job creation over cost.

Of course governments worry about reliability – they cop the blame if anything goes wrong. In 2005, the NSW and Queensland governments required their network businesses to build excessive back-up infrastructure to protect against even the most unlikely events. Reliability did improve a bit in some networks, but at significant cost: on average, customers got an extra 45 minutes of electricity a year at a cost of A$270 each.

State governments should take responsibility

Successive state governments in NSW, Queensland and Tasmania are responsible for overinvesting in their networks and, in NSW and Queensland, for setting reliability standards too high.

State governments can’t turn back the clock but they can still fix the mistakes of the past. And they should, because if they don’t, consumers will be paying for decades to come.

Households and businesses that can afford to buy solar panels and batteries will reduce their reliance on the grid. Meanwhile, those left behind – including the most vulnerable Australians – will be stuck with the burden of paying for the grid.

In Down to the Wire we recommend that where network businesses are still in government hands, the government should write down the value of the assets. This would mean governments forgoing future revenue in favour of lower electricity bills. For recently privatised businesses in NSW, a write-down could create more issues than it solves, so in those cases the state government should refund consumers the difference through a rebate.

At a time when governments are concerned about energy affordability, NSW, Queensland and Tasmania have a real opportunity to do something about it. They should seize it.

How to prevent this happening again

There will always be pressure to spend more. At the moment, concerns about South Australia’s reliability could very well lead to further investment in network infrastructure.

Policymakers must also deal with the risk that, in future, parts of the network may no longer be needed. The grid may need to be reconfigured as new technologies emerge, some communities go off-grid, and new energy sources arise in new locations.

For now, consumers bear this risk: they are locked into paying for assets whether or not they are needed. In future, the risk should be shared between consumers and businesses; this would encourage businesses to avoid overbuilding in the first place and instead consider alternative solutions.

With the focus on reliability right now, governments are at risk of repeating mistakes of the past. The truth is that Australia already has a very reliable grid.

On average across the National Electricity Market, consumers experience less than two-and-a-half hours in unplanned outages per year. Reducing that by a few minutes of supply each year is very expensive. Politicians typically value reliability more than consumers, but ultimately it is consumers who foot the bill.

State governments now have an opportunity to reset the clock – to pay off the mistakes of the past and let consumers guide choices about our future grid.

Author: Kate Griffiths, Senior Associate, Grattan Institute

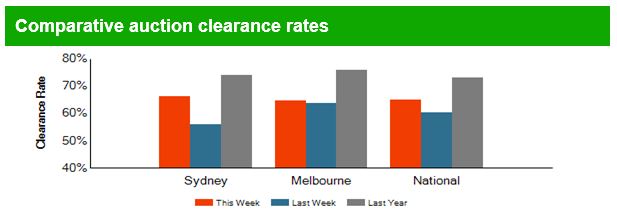

Brisbane cleared 49% of 137 scheduled auctions. Adelaide cleared 65% of 106 scheduled and Canberra 74% of 81 scheduled auctions.

Last week settled gain significantly lower, so expect the same again. And consider the gap between the number listed 3,143 and the number “reported auctions” 2,160.

You could easily argue the true picture is 1,484 (number sold) / 3,143 (number listed) giving a preliminary result of 47% clearance. Would that give a truer picture?

Today we examine the recent Financial Market Earthquakes and ask, are these indicators of more trouble ahead?

Welcome to the Property Imperative Weekly to 24th March 2018. Watch the video or read the transcript.

In this week’s review of property and finance news we start with the recent market movements and consider the impact locally.

The Dow 30 has come back, slumping more than 1,100 points between Thursday and Friday, and ending the week in correction territory – meaning down more than 10% from its recent high.

The volatility index – the VIX which shows the perceived risks in the financial markets also rose, up 6.5% just yesterday to 24.8, not yet at the giddy heights it hit in February, but way higher than we have seen for a long time – so perceived risks are higher.

And the Aussie Dollar slipped against the US$ to below 77 cents from above 80, and it is likely to drift lower ahead, which may help our export trade, but will likely lead to higher costs for imports, which in turn will put pressure on inflation and the RBA to lift the cash rate. The local stock market was also down, significantly. Here is a plot of the S&P ASX 100 for the past year or so. We are back to levels last seen in October 2017. Expect more uncertainty ahead.

So, let’s look at the factors driving these market gyrations. First of course U.S. President Donald Trump’s signed an executive memorandum, imposing tariffs on up to $50 billion in Chinese imports and in response the Dow slumped more than 700 points on Thursday. There was a swift response from Beijing, who released a dossier of potential retaliation targets on 128 U.S. products. Targets include wine, fresh fruit, dried fruit and nuts, steel pipes, modified ethanol, and ginseng, all of which could see a 15% duty, while a 25% tariff could be imposed on U.S. pork and recycled aluminium goods. We also heard Australia’s exemptions from tariffs may only be temporary.

Some other factors also weighed on the market. Crude oil prices rose more than 5.5% this week as following an unexpected draw in U.S. crude supplies and rising geopolitical tensions in the middle east. Crude settled 2.5% higher on Friday after the Saudi Energy Minister said OPEC and non-OPEC members could extend production cuts into 2019 to reduce global oil inventories. Here is the plot of Brent Oil futures which tells the story.

Bitcoins promising rally faded again. Earlier Bitcoin rallied from a low of $7,240 to a high of $9175.20 thanks to easing fears that the G20 meeting Monday would encourage a crackdown on cryptocurrencies. Finance ministers and central bankers from the world’s 20 largest economies only called on regulators to “continue their monitoring of crypto-assets” and stopped short of any specific action to regulate cryptocurrencies. So Bitcoin rose 2% over the past seven days, Ripple XRP fell 8.93%and Ethereum fell 14.20%. Crypto currencies remain highly speculative. I am still working on my more detailed post, as the ground keeps shifting.

Gold prices enjoyed one of their best weeks in more than a month buoyed by a flight-to-safety as investors opted for a safe-haven thanks to the events we have discussed. However, the futures data shows many traders continued to slash their bullish bets on gold. So it may not go much higher. So there may be no relief here.

Then there was the Federal Reserve statement, which despite hiking rates by 0.25%, failed to add a fourth rate hike to its monetary policy projections and also scaled back its labour market expectations. Some argued that the Fed’s decision to raise its growth rate but keep its outlook on inflation relatively unchanged was dovish. Growth is expected to run at 3%, but core inflation is forecast for 2019 and 2020 at 2.10%. They did, however, signal a faster pace of monetary policy tightening, upping its outlook on rates for both 2019 and 2020. You can watch our separate video blog on this. The “dots” chart also shows more to come, up to 8 lifts over two years, which would take the Fed rate to above 3%. The supporting data shows the economy is running “hot” and inflation is expected to rise further. This will have global impact. The era of low interest rates in ending. The QE experiment is also over, but the debt legacy will last a generation.

All this will have a significant impact on rates in the financial markets, putting more pressure on borrowing companies in the US, and the costs of Government debt. US mortgage interest rates rose again, a precursor to higher rates down the track.

Moodys’ said this week, that the U.S.’ still relatively low personal savings rate questions how easily consumers will absorb recent and any forthcoming price hikes. Moreover, the recent slide by Moody’s industrial metals price index amid dollar exchange rate weakness hints of a levelling off of global business activity.

The flow on effect of rate rises is already hitting the local banks in Australia. To underscore that here is a plot of the A$ Bill/OIS Swap rate, a critical benchmark for bank funding. In fact, looking over the past month, the difference, or spread has grown by around 20 basis points, and is independent from any expectation of an RBA rate change. The BBSW is the reference point used to set interest rates on most business loans, and also flows through to personal lending rates and mortgages.

As a result, there is increasing margin pressure on the banks. In the round, you can assume a 10 basis point rise in the spread will translate to a one basis point loss of margin, unless banks reduce yields on deposit accounts, or lift mortgage rates. Individual banks ae placed differently, with ANZ most insulated, thanks to their recent capital initiatives, and Suncorp the most exposed.

In fact, Suncorp already announced that Variable Owner Occupier Principal and Interest rates will rise by 5 basis points. Variable Investor Principal and Interest rates will increase by 8 basis points, and Variable Interest Only rates increase go up by 12 basis points. In addition, their variable Small Business rates will increase by 15 basis points and their business Line of Credit rates will increase by 25 basis points. Expect more ahead from other lenders. The key takeaway is that funding costs in Australia are going up at a time when the RBA is stuck in neutral. It highlights how what happens with rates and in money markets overseas, and particularly in the US, can have repercussions here – repercussions that many are possibly unprepared for.

Locally, the latest Australian Bureau of Statistics showed that home prices to December 2017 fell in Sydney over the past quarter, along with Darwin. Other centres saw a rise, but the rotation is in hand. Overall, the price index for residential properties for the weighted average of the eight capital cities rose 1.0% in the December quarter 2017. The index rose 5.0% through the year to the December quarter 2017.

The capital city residential property price indexes rose in Melbourne (+2.6%), Perth (+1.1%), Brisbane (+0.9%), Hobart (+3.9%), Canberra (+1.7%) and Adelaide (+0.6%) and fell in Sydney (-0.1%) and Darwin (-1.5%). You can watch our separate video on this, where we also covered in more detail the January 2018 mortgage default data from Standard & Poor’s. It increased to 1.30% from 1.07% in December. No area was exempt from the increase with loans in arrears by more than 30 days increasing in January in every state and territory. Western Australia remains the home of the nation’s highest arrears, where loans in arrears more than 30 days rose to 2.44% in January from 2.08% in December, reaching a new record high. Conversely, New South Wales continues to have the lowest arrears among the more populous states at 0.98% in January. Moody’s is now expecting a 10% correction in some home prices this year.

According to latest figures released by the Australian Bureau of Statistics (ABS), the seasonally adjusted unemployment rate increased to 5.6 per cent and the labour force participation rate increased by less than 0.1 percentage points to 65.7 per cent. The number of persons employed increased by 18,000 in February 2018. So no hints of any wage rises soon, as it is generally held that 5% unemployment would lead to higher wages – though even then, I am less convinced.

The latest final auction clearance results from CoreLogic, published last Thursday showed the final auction clearance rate across the combined capital cities rose to 66 per cent across a total of 3,136 auctions last week; making it the second busiest week for auctions this year, compared with 63.3 per cent the previous week, and still well down from 74.1 per cent a year ago. Although Melbourne recorded its busiest week for auctions so far this year with a total of 1,653 homes taken to auction, the final auction clearance rate across the city fell to 68.7 per cent, down from the 70.8 per cent over the week prior. In Sydney, the final auction clearance rate increased to 64.8 per cent last week, from 62.2 per cent the week prior. Across the smaller auction markets, clearance rates improved in Brisbane, Perth and Tasmania, while Adelaide and Canberra both returned a lower success rate over the week. They say Geelong was the best performing non-capital city region last week, with 86.1 per cent of the 56 auctions successful. However, the Gold Coast region was host to the highest number of auctions (60). This week they are expecting a high 3,689 planned auctions today, so we will see where the numbers end up. I am still digging into the clearance rate question, and should be able to post on this soon. But remember that number, 3,689, because the baseline seems to shift when the results arrive.

As interest rates rise, in a flat income environment, we expect the problems in the property and mortgage sector to show, which is why our forward default projections are higher ahead. We will update that data again at the end of the month. Household Financial Confidence also drifted lower again as we reported. It fell to 94.6 in February, down from 95.1 the previous month. This is in stark contrast to improved levels of business confidence as some have reported. Our latest video blog covered the results.

Finally, The Royal Commission of course took a lot of air time this week, and I did a separate piece on the outcomes yesterday, so I won’t repeat myself. But suffice it to say, we think the volume of unsuitable mortgage loans out there is clearly higher than the lenders want to admit. Mortgage Broking will also get a shake out as we discussed on the ABC this week. And that’s before they touch on the wealth management sector!

We think there are a broader range of challenges for bankers, and their customers, as I discussed at the Customer Owned Banking Association conference this week. There is a separate video available, in which you can hear about what the future of banking will look like and the importance of customer centricity. In short, more disruption ahead, but also significant opportunity, if you know where to look. I also make the point that ever more regulation is a poor substitute for the right cultural values. At the end of the day, a CEO’s overriding responsibility is to define the right cultural values for the organisation, and the major banks have been found wanting. A quest for profit at any cost will ultimately destroy a business if in the process it harms customers, and encourages fraud and deceit. You simply cannot assume banks will do the right thing, unless the underlying corporate values are set right. Remember Greenspans testimony after the GFC, when he said “I made a mistake in presuming that the self-interests of organisations, specifically banks and others, were such that they were best capable of protecting their own shareholders and their equity in the firms.”

Continued increases in shadow-banking regulation should be a net positive for system-wide stability and liquidity if maintained over the medium term, says Fitch Ratings.

Overall shadow-banking asset levels have remained manageable. However, more rapid growth in certain regions and activities is expected to attract additional regulatory scrutiny, given the potential indirect effects of market interconnectedness and/or asset price volatility on the overall financial system.

Shadow-banking assets were $45 trillion, as of YE16, or 13.2% of total global financial assets, according to the Financial Stability Board (FSB). This marked an increase of 7.6% over the previous year. In the US, shadow-banking assets remained relatively stable at $14.1 trillion, as of YE16, or 31.6% of total global shadow-banking assets. Conversely, China’s shadow-banking assets increased to $7 trillion, rising from 1.4% of total global shadow-banking assets in 2010 to 15.5% at YE16, a 40.1% CAGR on an exchange rate-adjusted basis, according the to the FSB. Euroarea shadow-banking assets were $10.1 trillion, as of YE16, falling to 22.4% of total global shadow-banking assets from 27.3% in 2010.

Of the $45 trillion of global shadow-banking assets at YE16, 72% were held by collective investment vehicles, such as open-end fixed income, money market, and credit hedge funds, which largely drove asset growth for the last five years. The inherent redemption risk of these vehicles could pressure asset prices in the event of runs, particularly if material leverage is employed.

Globally, banks continue to have modest direct exposure to Other Financial Intermediaries (OFIs), the FSB’s broad measure of shadow-banking activity, both in lending and borrowing. At YE16, aggregate funding and credit interconnectedness between banks and OFIs approximated pre-crisis (2003-2006) levels after several years of decline. Banks’ claims on OFI assets were $6.3 trillion, or 5.6% of total bank assets, while funding from OFIs was $5.9 trillion, or 5.4% of total funding. That said, given the level of broader interconnectedness between banks and shadow-bank participants, and the potential for regulatory arbitrage to be employed by market participants, global regulatory scrutiny is expected to continue.

China’s regulators have responded to rapid shadow-banking growth with increased oversight, particularly on wealth management and trust products, the origination, of which, have begun to level off after years of growth. The increased regulation is aimed at improved transparency and disclosure in order to reduce contagion risks within the system, rather than reducing the scale of shadow banking, which could disrupt the stability and liquidity of the financial system. We believe the Chinese government will continue to focus on regulation as long as it does not materially hamper GDP and economic growth.

China’s shadow-banking sector is more systemic and complex than other more developed markets, with the extent of interconnectivity and risk, creating significant potential risk for Chinese banks. Unlike the US, where non-banks tend to be the dominant shadow-banking participants, banks are a key component in China’s shadow-banking ecosystem. While the shadow-banking products in China may be less complex than in the US, the evolving implicit/explicit guarantees in China make it more difficult to pinpoint who bears the ultimate investment risk. Smaller Chinese banks, relying on the interbank market and shadow banking for liquidity, may see rising funding costs as a result of increased regulation, while larger banks with stronger deposit franchises may be relatively better insulated than smaller, less capitalized peers.

The first round of hearings at the Royal Commission into Financial Services Misconduct closed out after two weeks of frankly amazing evidence. Their live streaming of the hearings was well worth watching. Of the 2,386 submissions received so far 69% related to banking alone!

The case study approach looked at issues across residential mortgages, car finance, credit cards, add-on insurance products, credit offers and account administration. We discuss the findings so far. Watch the video or read the transcript.

The litany of potential breaches of both the law, company policy and regulatory guides were pretty relentless, with evidence from various bank customers as well as representatives from ANZ, CBA, NAB and Westpac, plus others. It looks to me as if many of these breaches will possibly force the banks to pay sizeable remediation costs and penalties. Weirdly, NAB who was first up, probably came out the least damaged, despite the focus on their Introducer program. Their own whistleblower programme brought the issues of fraud inside the bank and beyond to light.

Some of the other players were clearly caught out trying to avoid scrutiny, and seeking to bend the rules systematically to maximise profitability, despite the severe impact on customers. They also tried to blame systems, or brokers, or executional issues. It was pretty damming. We should expect extra remediation costs and even fines together with a heightened risk of further individual or group actions. It is not over yet.

A number of industry practices will be changed, centred on responsible lending, including a further tightening of lending standards and so credit will be harder to get – this will continue to drive credit growth, especially for housing, lower still.

In the final session, in addition to legal breaches, there was also discussion of what conduct below community standards and expectations might mean. The case study approach brought the issues to the fore.

Specific areas included mortgage broking where we think it is likely remuneration models will change, with a focus on fees rather than commissions, and this will shake up the industry. Insiders are already saying this could reduce competition, but we do not agree. Also take note that the banks tended to blame the brokers and aggregators, but they ALL have responsible lending obligations, and they cannot outsource them.

If there is a move towards meeting customer best interest as opposed to not unsuitable, this could lead to a consolidation of brokers and financial planners, something which makes sense, in that a mortgage, or wealth building is part of the same continuum, and credit is not somehow other – the two regimes are an accident of history because the credit laws evolved separately from individual state laws. They should be merged, in the best interests of customers.

But now to those unknown unknowns. I do not think the poor behaviour resides only in the large players which were examined. Arguably, it is endemic across smaller banks and non-banks too. In fact, many smaller players are very active broker users. This means that the proportion of loans held by customers which are unsuitable is considerable. We must not let this become a big bank, or broker bashing exercise. We need structural and comprehensive reform across the board.

Next we need to remember that half of all loans are originated in the banks themselves, and the same underwriting weaknesses are sure to reside there too – the banks will try to deflect attention beyond their boundaries, but they need to look inside too (and evidence suggests they prefer to look away!). Have no doubt, liar loans are found in loans written by bankers themselves. But the case studies in this sector are harder to find, for obvious reasons.

The same drivers are also apparent in the growing non-bank sector, where regulation is weaker. We need to look there too – including the car loans, and pay day loans, plus the strong growth in interest only mortgages by some players. APRA only now has new powers of oversight, but they are still pretty weak.

At its heart we need to rebalance the cultural norms in finance from profit at all costs, to serving the customer at all costs. The fact is, do that, put the customer first, and profitability follows. We discussed this in our recent Customer Owned Banking post.

Now, recalling the terms of reference of the Royal Commission, they will need to look beyond bank practice to think about completion, access to banking services and even the broader impact on the economy.

As we have argued, credit growth has been the engine of GDP growth, – the RBA has used this growth in credit to drive household consumption to replace mining investment. As lending practices are progressively tightened this has the potential to slow growth significantly at a time when rates are rising. We expect the rate of slowing to speed up ahead. I also think the confused roles of the regulators – ACCC, APRA, ASIC, RBA and The Council of Financial Regulators, where they all sit round the table (minus the ACCC) with The Treasury – are partly to blame. As the recent Productivity Commission review called out there needs to be change here too. But that is probably beyond the Commissions ambit, for now.

The bottom line is this, the economic outfall of the Royal Commission, even based on just round one will be significant. Credit growth may well slow. Bank share valuations will be hit (they have already fallen) and as the size of the costs of remediation emerge, this could get worse. But lending practices will not get fixed anytime soon. There is a long reform journey ahead.

And in three weeks, we are back, this time looking at financial planning and wealth management, the $2 trillion plus sector.

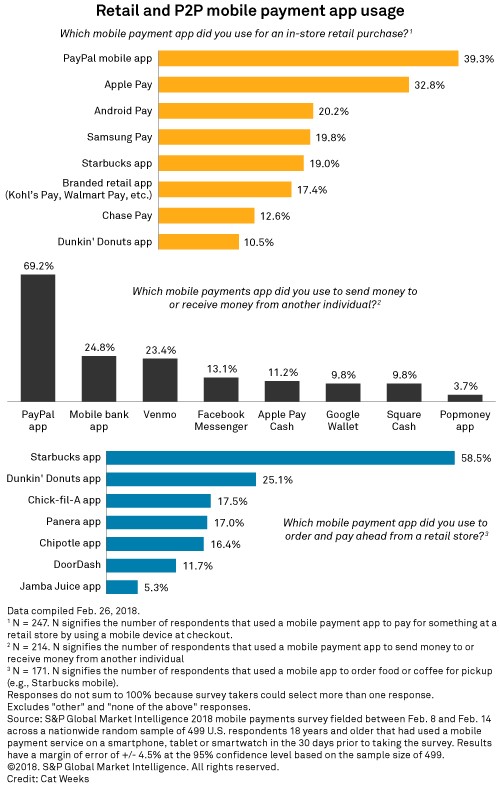

JPMorgan Chase & Co. has work to do if it wants Chase Pay to have the same kind of customer adoption as PayPal Holdings Inc.’s digital wallet, based on the results of a recent survey commissioned by S&P Global Market Intelligence.

About 39% of the individuals that used a mobile payment app to pay for an in-store retail purchase in the 30 days prior to taking the survey had used PayPal, versus 13% for Chase Pay.

This was one of several findings of the survey, which began with 904 respondents. Of those, 405 had not used a mobile payment app in the past 30 days, which gave us insight into why respondents would not want to use such services. The 499 that did use mobile payment services, meanwhile, yielded clues on what people do with their apps, such as the aforementioned in-store retail purchases.

Despite offering alternative services, Chase Pay recently partnered with PayPal, letting clients link their cards to their PayPal accounts through Chase Pay to access the PayPal wallet. This is not uncommon, as PayPal partners with other large banks and credit card issuers, such as Bank of America Corp. and Citigroup Inc., to link customer cards to their app. And as our survey data illustrated, respondents often used more than one wallet service.

PayPal also dominated in the survey question regarding person-to-person payments. Nearly 70% of those that had transferred money to an individual used PayPal, and the third most-used app was Venmo, which PayPal also owns.

Based on our survey, bank apps were slightly more popular than Venmo for person-to-person payments, with about 25% of respondents saying they had used a mobile bank app and about 23% saying they had used Venmo.