The RBA published a paper on “The Value of Payment Instruments: Estimating Willingness to Pay and Consumer Surplus” by Tai Lam and Crystal Ossolinski. This paper draws on a survey of consumers’ willingness to pay surcharges to use debit cards and credit cards, rather than cash. Just as the price a consumer is willing to pay for a good or service is indicative of the value he/she places on that item, the willingness to pay a surcharge to use a payment method reflects that method’s value to that consumer, relative to any alternatives.

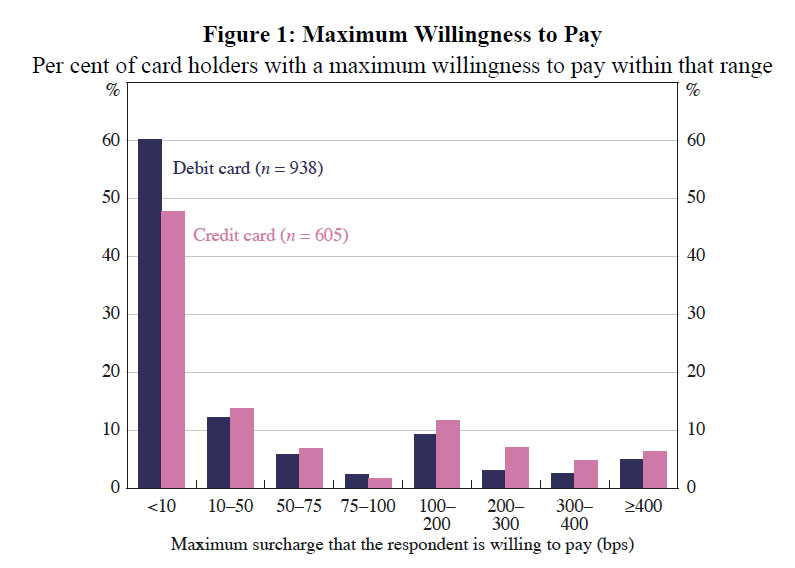

They find a wide dispersion in the willingness to pay for the use of cards. Around 60 per cent of consumers are unwilling to pay a 0.1 per cent surcharge, which suggests that for these individuals, the net benefits of cards are very small or that cash is actually preferred. At the other end of the distribution, some individuals (around 5 per cent) are willing to pay more than a 4 per cent surcharge, indicating they place a substantial value on paying using cards.

On average, consumers have a higher willingness to pay for the use of credit cards than debit cards. This difference can be viewed as the additional value placed on the non-payment functions – rewards and the interest-free period – of credit cards. They estimate that on average credit card holders place a value of 0.6 basis points on every 1 basis point of effective rewards rebate.

On average, consumers have a higher willingness to pay for the use of credit cards than debit cards. This difference can be viewed as the additional value placed on the non-payment functions – rewards and the interest-free period – of credit cards. They estimate that on average credit card holders place a value of 0.6 basis points on every 1 basis point of effective rewards rebate.

Based on the survey data and information on the costs to merchants of accepting payment methods, they predict the mix of cash, debit card and credit card payments chosen by consumers under different levels of surcharging and explore the implications for the efficiency of the payments system. In particular, the consumer surplus in a scenario where merchants do not surcharge and the costs of all payment methods are built into retail prices can be compared with that where merchants surcharge based on payment costs and retail prices are correspondingly lower. Their findings suggest that cost-based surcharging leads to some consumers switching to less costly payment methods, resulting in greater efficiency of the payment system and an increase in consumer surplus of 13 basis points per transaction.