Nice piece from ABC’s Michael Janda.

The big controversy this week was whether Gen Ys should forgo some smashed avo to save up for a house.

The commentariat took Bernard’s advice to millennials with more than a grain of salt — he was demolished on the statistical evidence by Greg Jericho and a raft of other analysts.

Yet, the demographer’s opinion also sparked articles on how Gen Y could get into the housing market.

I think the better question to ask is why the hell anyone in Gen Y would want to buy a house right now?

As a member of Gen Y living in the nation’s most expensive city it’s a question I’ve asked myself many times and, aside from two very fleeting periods in late-2008 and around 2012, it’s been hard to find a good reason to buy.

So if your baby boomer parents are hassling you about rushing into the market to avoid being locked out forever, here are a few responses you can shoot back while you sit down, eat your smashed avo, sip your latte and relax.

1. Australian real estate has never been more expensive

A recent study by global investment bank UBS, using a method developed by a branch of the US Federal Reserve, showed Australian house prices were about 7 per cent above previous peaks in 2003, 2007 and 2010.

What goes up tends to go down, and after each of those peaks house prices tended to stagnate or fall slightly.

And while global real estate markets have been going crazy on low interest rates, Australia has been more insane than just about anywhere else, perhaps excluding Canada, New Zealand and Hong Kong.

The folks at Demographia, who do an annual property study comparing markets across eight nations, found that Sydney was the world’s second most expensive city relative to income after Hong Kong, with prices 12.2 times typical annual earnings.

Don’t smirk too much if you live outside the Harbour City though, with Melbourne equal fourth and the other three capitals with populations over a million rated “severely unaffordable” for the twelth year in a row, plus plenty of regional areas in that category.

To back up those private sector measures, this is the ABS chart of capital city home prices since 2003. How many other things can you think of that have almost doubled in price over the past 13 years? Certainly not most people’s pay packets.

2. We do not have a property shortage and are heading for a glut

But prices have jumped because we have a terrible housing shortage, I hear the property spruikers respond.

Except we don’t.

If we did, it wasn’t nationwide and it wasn’t severe, as I showed in this analysis of ABS population growth and dwelling completion figures last year.

Even in those locations where we might have had a shortage it will soon be replaced by a glut.

According to analysts at Citi, Brisbane is already in a unit glut, Melbourne is on the way and some areas of Sydney are too.

Citi is not alone, with analysts at UBS, Westpac, Morgan Stanley, BIS Shrapnel, Deloitte-Access Economics and even the Reserve Bank, amongst others, warning of an apartment glut.

And when you get a glut prices usually fall, with fairly conservative analysts warning of a 15-20 per cent drop.

So why buy now when you can get more choice and cheaper prices later?

3. We are in one of the world’s biggest property bubbles

See above.

Seriously, prices are at record highs in Australia’s two biggest cities, and many other areas, in absolute terms, relative to incomes, relative to rents, relative to just about any other measure you care to name.

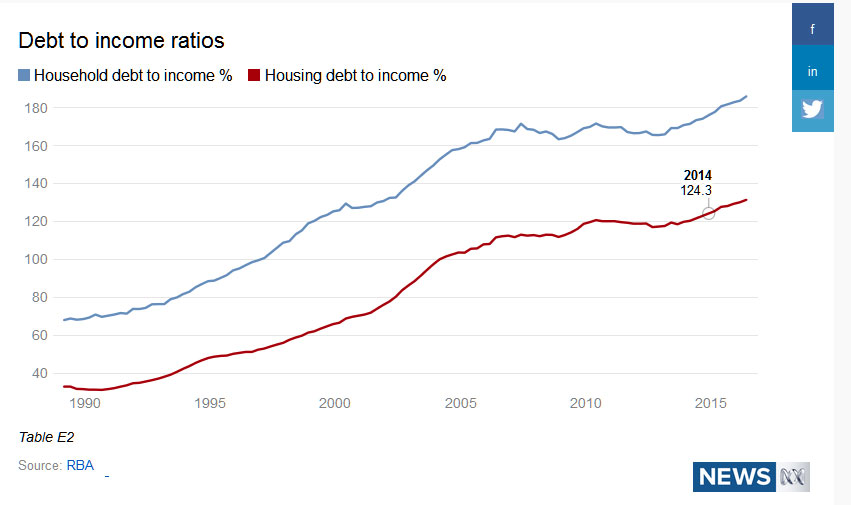

At the same time, household debt, and especially housing debt, is at a record high.

It doesn’t take a genius to figure out why Australian home prices are so high.

The deregulation of the banking system and lower interest rates allowed people to borrow more money, which meant they could keep bidding up the price of homes.

Why is that a bubble?

Basically because you can’t just keep increasing your borrowing faster than your income is growing indefinitely — eventually, even with low interest rates, you simply won’t be able to keep up with the repayments. Ask Greece how this works.

Australia is especially vulnerable since a lot of the money we have borrowed for housing comes from overseas (we’re talking hundreds of billions of dollars here) and if they suddenly stop lending us any more … again, ask Greece.

But you don’t need to take my word for it, ask the OECD, the IMF and the central bank for central bankers, the BIS.

4. Inflation is not going to help you pay off your massive debt

Remember how I said earlier that low interest rates have helped people borrow more money?

Well there’s a big downside to that, explained expertly by Fairfax economics writer Peter Martin.

Basically, rates are low because inflation is low. Inflation is low because wage growth is slow. Slow wage growth means that the size of your repayments don’t shrink much relative to your pay packet over the decades it takes to pay off a home loan.

This is in contrast to most of the baby boomers. Yes they had to put up with peak mortgage interest rates of 17 per cent for a while, but inflation was also much higher which meant the real size of their debt and repayments fell over the life of the loan.

(Not to mention that the initial size of their loans was generally much lower relative to their incomes than it is now).

This was something Glenn Stevens actually warned about in a relatively obscure talk to the Real Estate Institute of Australia when he was an assistant governor of the Reserve Bank in 1997.

5. Interest rates are more likely to rise than fall

There’s more bad news. If inflation does pick up over the medium and longer term, then an inflation-targeting Reserve Bank will have to lift interest rates in response.

While you can get a sub-4 per cent interest rate on many home loans now, more typical interest rates would be around 6.3 per cent, which is the average discount variable rate over the past 12 years.

Most home loans now are for 25 to 30 years, so there’s a fair bet you’ll see rates rise at least a couple of percentage points.

Can you afford that? If not, I wouldn’t even think of buying. In fact, under the bank regulator’s new tighter rules, your financial institution shouldn’t give you a loan.

6. The dangers of negative equity

If you believe that we are in an overvalued housing market, then a key danger you should think about is negative equity.

This is where you owe more to the bank on you home loan than your house or flat is worth.

Provided you can afford the loan it doesn’t have to be a disaster, as you can often ride out a fall in prices by not selling and wait for an eventual recovery.

But it could be a long wait and, in the meantime, you are effectively locked into your home and mortgage because if you sold you couldn’t pay back the bank and you’d be bankrupt.

This has other effects on your life.

For example, if you buy a home with your partner and then have relationship problems it becomes very hard to split up when you can’t sell your property. Think about it, who stays there? Does that person pay rent? You have to stay in touch to manage the property even if you now hate each other. Not good.

7. Rents are relatively cheap … and falling

If you don’t own a home, and don’t live with your folks, you’re probably renting.

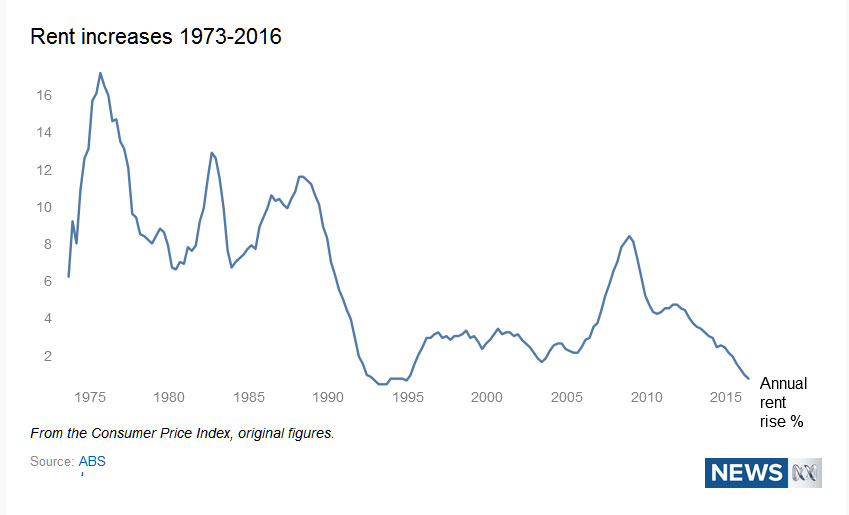

While rents feel, and are, expensive in many Australian cities, the fact is that rents are around the lowest they’ve ever been relative to purchase prices – what analysts call the “rental yield”.

Rent increases also haven’t been as low as they are now since the aftermath of the early-1990s recession.

Not only does this mean that you’re unlikely to be slugged by huge rent increases over the next few years while you save up some money to capitalise on a potential house price crash, it also is a sign such a crash may be coming.

You see, low rental growth is a sign of the property glut we talked about earlier.

Even though purchase prices are being bid up by investors, when they go to rent out these places they struggle to find people to fill them, so they discount their rents.

Landlords with existing tenants become reluctant to raise rents because they can find somewhere cheaper to go.

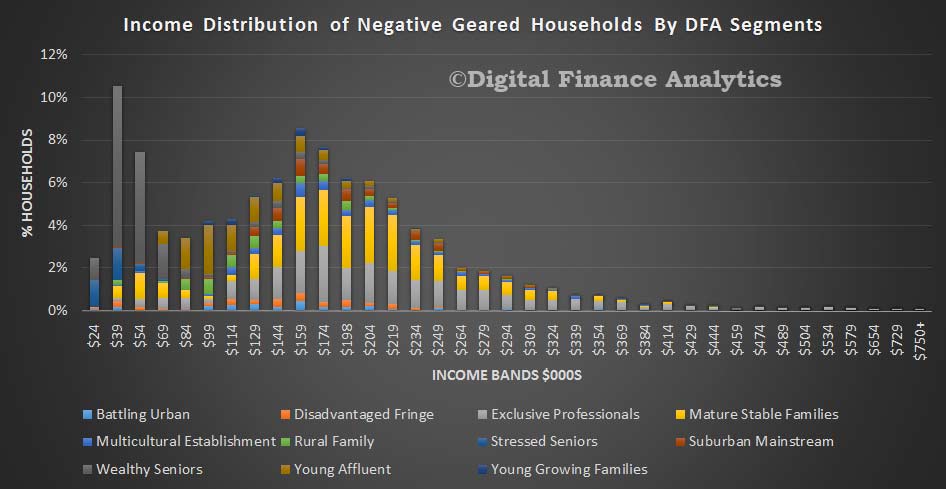

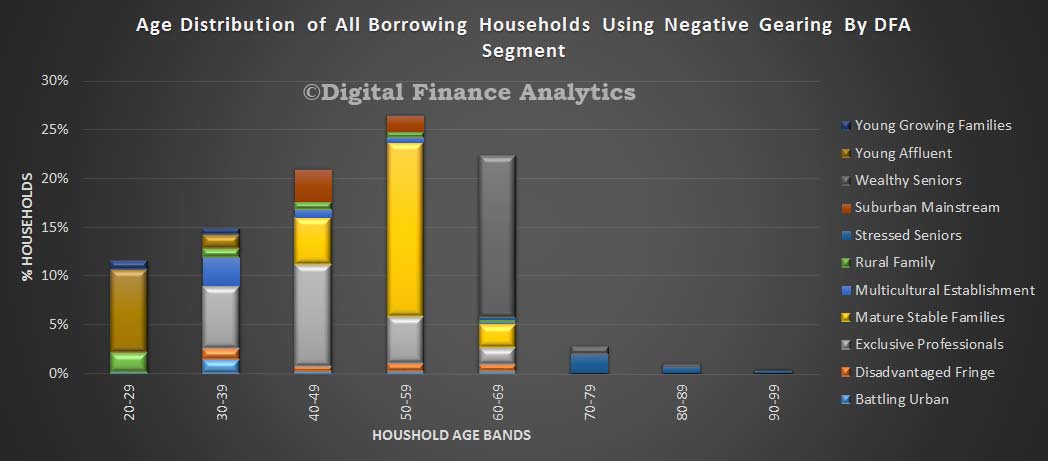

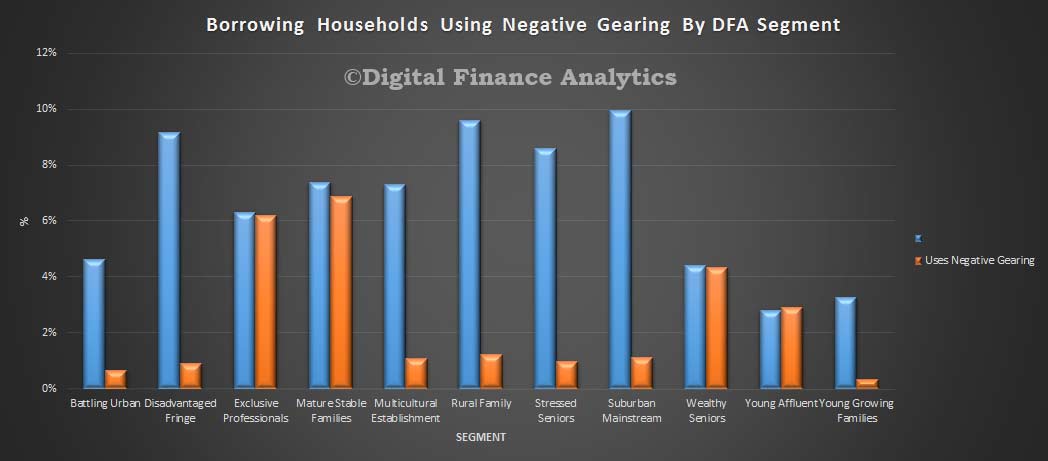

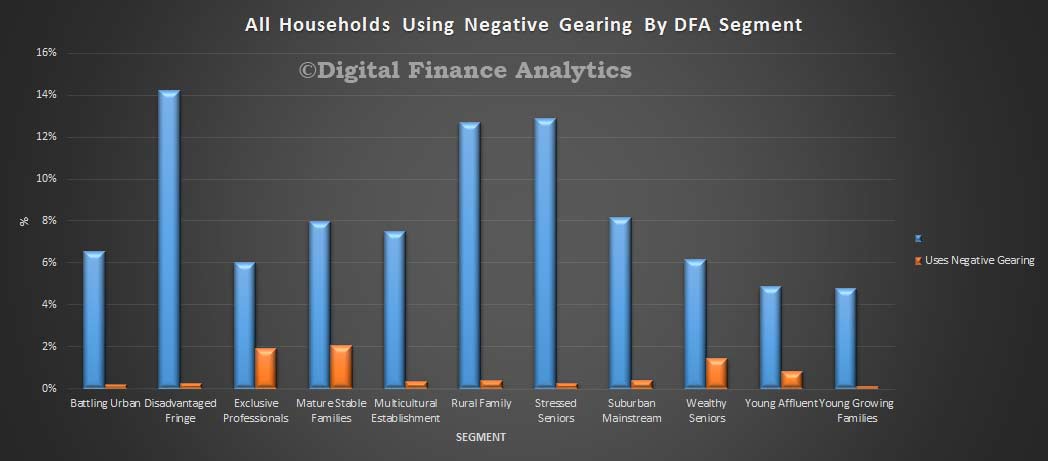

Even though the negative gearing tax break offsets some of these losses for landlords, if there’s no capital gain then they’re still losing dosh, and eventually they’ll sell.

8. Lifestyle

This is where it gets personal. What do you value in life? And I’m not just talking about smashed avo and lattes.

Where do you want to live? If it’s somewhere you can easily afford to rent but can’t afford to buy, then maybe renting for a bit longer while you save is a smart option.

Do you want to keep travelling? Have kids? Change jobs or career down the track?

Remember, a mortgage is often for 25-30 years and selling a home is potentially a lot more complicated and expensive than exiting a lease.

It’s something best done when you have a pretty good idea about where you want to live and prefer stability over flexibility.

Oh, and don’t forget about the negative equity trap that can lock you into keeping a home you don’t want anymore.

There’s plenty of people in Perth, Darwin, and regional Queensland and Western Australia that are learning all about this the hard way.