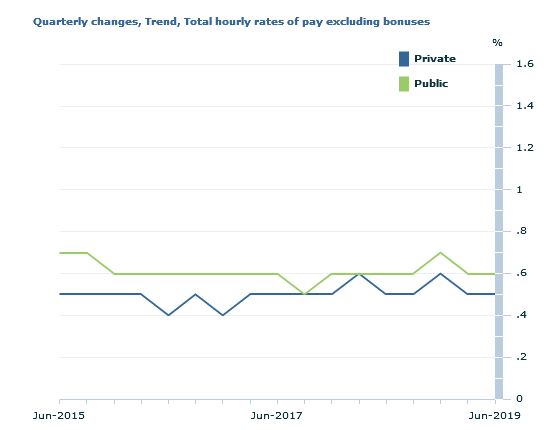

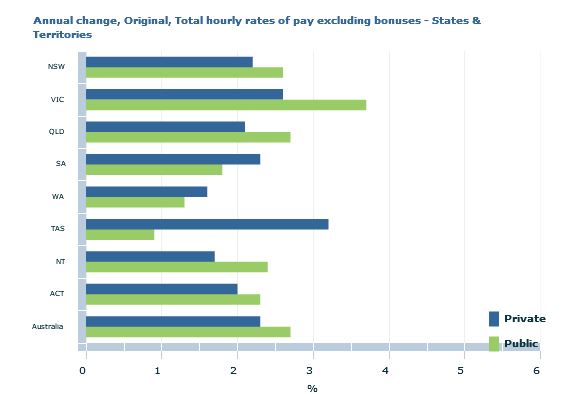

The trend Wage Price Index (WPI) rose 0.5 per cent in the June quarter 2019 and 2.3 per cent through the year, according to figures released today by the Australian Bureau of Statistics (ABS). These are lower than projected in the budget, and highlights the stresses in the economy. Without one-off factors the numbers would be even lower.

Seasonally adjusted private sector wage growth was 0.5 per cent, while public sector wage growth was 0.8 per cent in the June quarter 2019.

ABS Chief Economist, Bruce Hockman said: “Wage growth continues at a

steady rate in the Australian economy on the back of strong public

sector growth over the quarter. The most significant contribution to

wage growth this quarter came from the public sector component of the

health care and social assistance industry, where a number of large

increases were recorded in Victoria under a plan to ensure wage parity

with other states.”

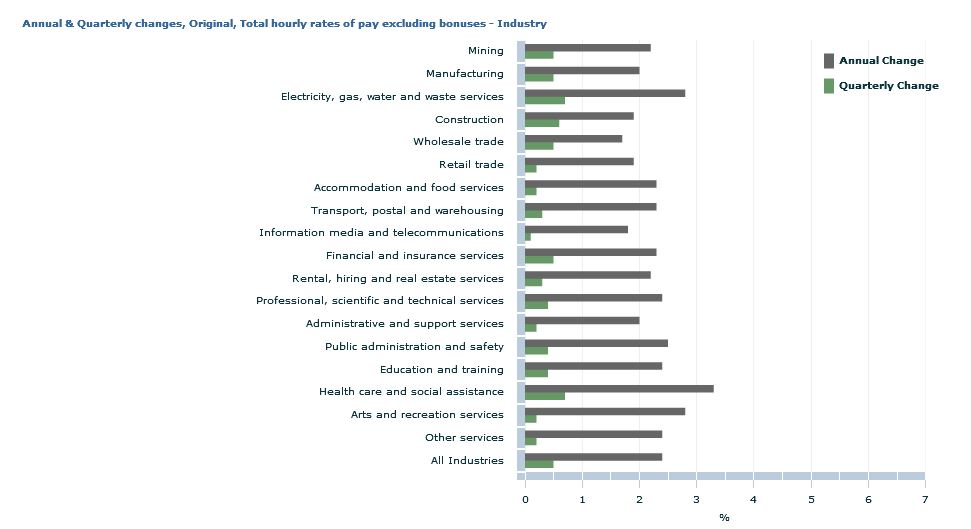

In original terms, annual wages growth to the June quarter 2019 by industry ranged from 1.7 per cent for wholesale trade to 3.3 per cent for health care and social assistance.

Western Australia recorded the lowest through the year wage

growth of 1.6 per cent while Victoria recorded the highest of 2.9 per

cent.

Woolworths Holdings announced yesterday it will book an impairment of $437.4 million against David Jones, reducing the valuation of the department chain to about $965 million. This write down is the second since 2018. Woolworths Holdings bought the prestigious network of stores in 2014 for $2.1 billion.

A Woolworths spokeswoman said

This writedown reflects sustained and unprecedented economic pressures and structural changes in the Australian market. The retail sector in Australia is currently in recession, and the Australian economy has slowed to its weakest level since the global financial crisis in 2009

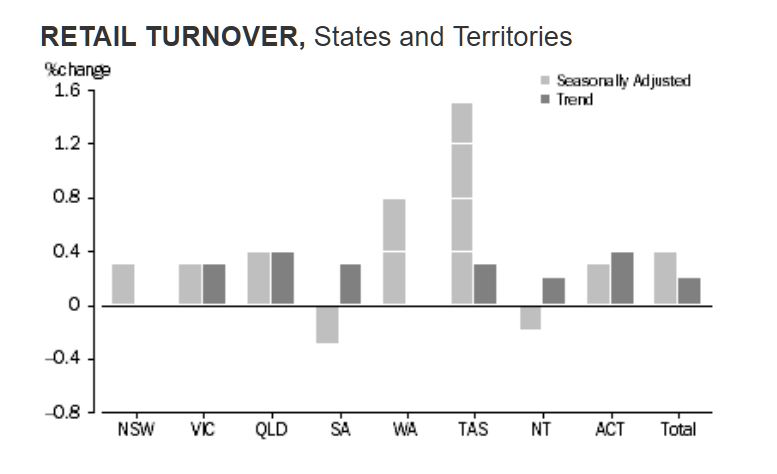

Today the ABS said the trend estimate for Australian turnover rose 0.2% in June 2019. This follows a rise of 0.2% in May 2019 and a rise of 0.2% in April 2019. The seasonally adjusted estimate for Australian turnover rose 0.4% in June 2019. This follows a rise of 0.1% in May 2019 and a fall of 0.1% in April 2019. The original estimate for Australian turnover fell 1.5% in June 2019. The original estimate for chains and other larger retailers fell 0.1% in June 2019. The original estimate for smaller retailers fell 4.6% in June 2019.

The following states and territories rose in trend terms in June 2019:

Victoria (0.3%), Queensland (0.4%), South Australia (0.3%), the

Australian Capital Territory (0.4%), Tasmania (0.3%), and the Northern

Territory (0.2%). New South Wales (0.0%), and Western Australia (0.0%)

were relatively unchanged in trend terms in June 2019.

FOOD RETAILING

In current prices, the trend estimate for Food retailing rose 0.1% in

June 2019. The seasonally adjusted estimate rose 0.1%. By industry

subgroup, the trend estimate rose for Supermarkets and grocery stores

(0.1%), was relatively unchanged for Liquor retailing (0.0%), and fell

for Other specialised food retailing(-0.4%). The seasonally adjusted

estimate rose for Supermarkets and grocery stores (0.5%), and fell for

Other specialised food retailing (-3.8%), and Liquor retailing (-0.1%).

HOUSEHOLD GOODS RETAILING

In current prices, the trend estimate for Household goods rose 0.2% in June 2019. The seasonally adjusted estimate rose 0.2%. By industry subgroup, the trend estimate rose for Electrical and electronic goods retailing (0.4%), and Furniture, floor coverings, houseware and textile goods retailing (0.3%), and fell for Hardware, building and garden supplies retailing (-0.2%).

CLOTHING, FOOTWEAR AND PERSONAL ACCESSORY RETAILING

In current prices, the trend estimate for Clothing, footwear and personal accessory retailing rose 0.6% in June 2019. The seasonally adjusted estimate rose 2.0%. By industry subgroup, the trend estimate rose for Clothing retailing (0.5%), and Footwear and other personal accessory retailing (0.5%).

DEPARTMENT STORES

In current prices, the trend estimate for Department stores rose 0.2% in June 2019. The seasonally adjusted estimate fell 0.6%.

OTHER RETAILING

In current prices, the trend estimate for Other retailing rose 0.4% in June 2019. The seasonally adjusted estimate rose 0.6%. By industry subgroup, the trend estimate rose for Other retailing n.e.c. (0.4%), Pharmaceutical, cosmetic and toiletry goods retailing (0.4%), and Other recreational goods retailing (0.2%), and was relatively unchanged (0.0%) for Newspaper and book retailing.

CAFES, RESTAURANTS AND TAKEAWAY FOOD SERVICES

In current prices, the trend estimate for Cafes, restaurants and takeaway food services rose 0.2% in June 2019. The seasonally adjusted estimate rose 0.5%. By industry subgroup, the trend estimate rose for Cafes, restaurants and catering services (0.2%), and Takeaway food services (0.1%).

Online retail turnover contributed 6.1 per cent to total retail turnover in original terms in June 2019. In June 2018 online retail turnover contributed 5.7 per cent to total retail.

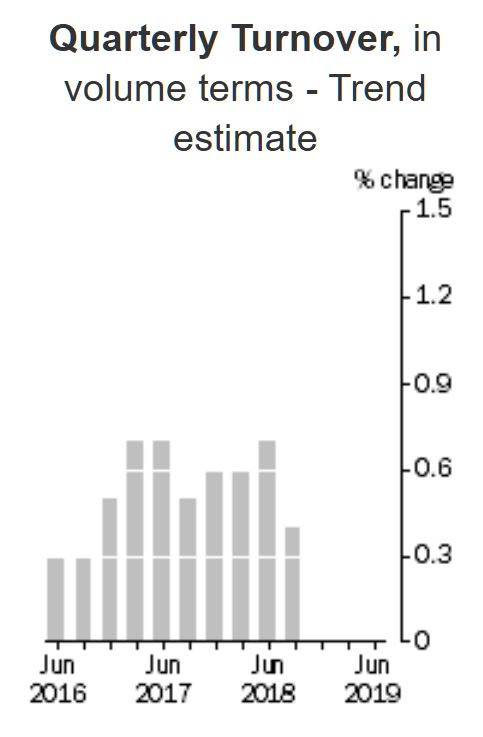

For the June quarter 2019, there was a rise of 0.2 per cent in seasonally adjusted volume terms. This follows a fall of 0.1 per cent in the March quarter 2019. The quarterly rise in volumes was led by Department stores (1.4 per cent), Cafes, restaurants and takeaway food services (0.5 per cent), Clothing, footwear and personal accessory retailing (0.7 per cent), Other retailing (0.4 per cent), and Household goods retailing (0.1 per cent). Food retailing (-0.4 per cent) fell in seasonally adjusted volume terms.

Nab’s online retail tells the same story:

The NAB Online Retail Sales Index contracted (-1.6%) in June on a

month-on-month, seasonally adjusted basis. This follows from a rebound

in May (3.4% mom, s.a).

In year-on-year terms, the NAB Online Retail Sales Index remains

positive, albeit barely, up 0.5% (y/y, s.a.) in June. However, this

result is compared to June 2018, and it is worth noting that the period

January to September 2018 was one of the strongest growth periods in the

NAB online retail sales index history.

After a strong May result, June data shows sales for three of the

eight online retail categories contracting in month-on-month growth

terms. The largest sales category, homewares and appliances (-7.1% mom,

s.a.), was a key contributor to the headline result given its relative

weight in the index. Media, and to a lesser extent, grocery and liquor,

were the two other categories to contract in the month. The smallest

sales category, takeaway food, recorded the fastest growth in the month.

For more detail, see Charts 3, 5, 7 & 8 below.

In month-on-month terms, all states and territories except WA (2.4%

mom, s.a.) and ACT (4.5%) recorded a contraction in sales growth.

Tasmania (-6.4%) led the monthly decline in sales growth.

In June, spend growth in metro areas was higher, at 0.4% (mom,

s.a.), relative to regional (-3.1%). WA metro areas went against the

broader result to record the highest online retail spend growth (+5.4%)

in the month. The above mentioned state contraction in online retail

sales for Tasmania was associated with a larger contraction in metro

area sales, along with a smaller contraction in regional, albeit with

sales for the latter also falling last month. See Charts 15 and 16 for

more detail.

While contracting, at -1.6%, domestic online retailers performed

better in month-on-month terms relative to international competitors

(-1.9% mom, s.a.). In year-on-year terms, from our series, considerable

weakness in international online sales remains. See charts 13 and 14,

and table 3 for category growth and share.

We estimate that in the 12 months to June, Australians spent $29.32

billion on online retail, a level that is just over 9% of the

traditional bricks and mortar retail sector (May 2019, Australian Bureau

of Statistics), and about 12.7% higher than the 12 months to June 2018.

We review the latest data from the RBA, APRA and ABS, plus higher mortgage delinquencies and the new bill to clamp down on cash transactions. A lot to talk about!

Full show on the war on cash: https://youtu.be/770M2s6ZD8Y

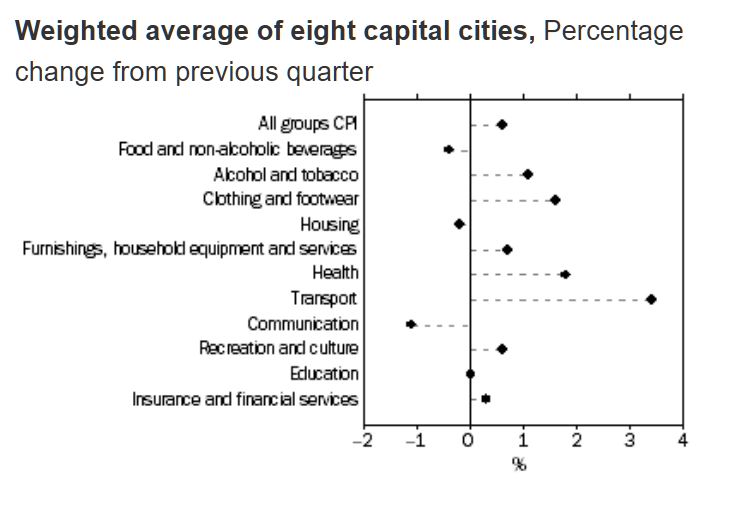

The Consumer Price Index (CPI) rose 0.6 per cent in the June quarter 2019, according to the latest Australian Bureau of Statistics (ABS) figures. This follows no movement (0.0 per cent) in the March quarter 2019.

All groups CPI seasonally adjusted rose 0.7%.

The trimmed mean rose 0.4%, following a rise of 0.3% in the March quarter 2019.

Over the twelve months to the June quarter 2019, the trimmed

mean rose 1.6%, following a rise of 1.6% over the twelve months to the

March quarter 2019.

The weighted median rose 0.4%, following a rise of 0.1% in the March quarter 2019.

Over the twelve months, the weighted median rose 1.2%,

following a revised rise of 1.4% over the twelve months to the March

quarter 2019.

The most significant price rises in the June quarter 2019 were automotive fuel (+10.2 per cent), medical and hospital services (+2.6 per cent), international holiday travel and accommodation (+2.7 per cent) and tobacco (+2.4 per cent).

Prices for fruit and vegetables (-2.8 per cent), domestic holiday travel and accommodation (-1.5 per cent) and electricity (-1.7 per cent) fell this quarter.

ABS Chief Economist, Bruce Hockman said: “Automotive fuel prices rose 10.2 per cent in the June quarter 2019. This rise had a significant impact on the CPI, contributing half of the 0.6 per cent rise this quarter. Automotive fuel prices returned to levels recorded in late 2018 after falling 8.7 per cent in the March quarter 2019.”

Inflation varied across the major centres. In Sydney we saw a large rise in fuel costs, putting the result in the range being experienced by Perth and Darwin.

Main Positive Contributors

Transport (+3.4%) driven by higher world oil prices and retail fuel

margins resulting in an increase in automotive fuel (+10.2%). Automotive

fuel rose in all capital cities this quarter, ranging from Canberra

(+1.7%) to Sydney (+11.8%).

Health (+1.8%) due to the cyclical increase in Private Health

Insurance premiums in the medical and hospital services (+2.6%) from 1

April. Medical and hospital services rose in all capital cities, ranging

from Canberra (+1.8%) to Adelaide (+3.8%).

Main Negative Contributors

Food and non-alcoholic beverages (-0.4%) driven by an improved

supply of fruit and vegetables with autumn/winter produce coming into

season, and bananas returning to normal prices following adverse

weather conditions in Queensland last quarter. Perth exhibited a smaller

fall than the other cities due to localised drought conditions

affecting fruit and vegetable supply.

Housing (-0.2%) driven by utilities (-1.0%), new dwelling

purchase for owner-occupiers (-0.2%), and continued weakness in rents

(0.0%). Utilities fell in all cities excluding Perth (0.0%) and Darwin

(+0.1%), ranging from Hobart (-0.1%) to Brisbane (-3.2%).

The CPI rose 1.6 per cent through the year to the June quarter 2019, after increasing 1.3 per cent through the year to the March quarter. Mr Hockman said: “Annual growth in the CPI continues to be subdued due to falls in a number of administered prices. Through the year, utility prices have fallen 0.2 per cent and child care has fallen 7.9 per cent following the introduction of the Child Care Subsidy package in July 2018.”

Blog")