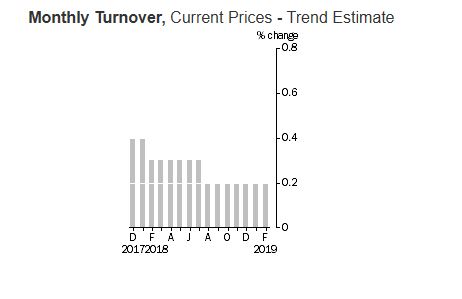

The trend estimate rose 0.2% in February 2019. This follows a rise of 0.2% in January 2019, and a rise of 0.2% in December 2018. This a more reliable indicator. Compared to February 2018, the trend estimate rose 2.9 per cent, and is higher than average wages growth.

ABS Director of Quarterly Economy Wide Surveys, Ben Faulkner said: “There were improved results across most industries with rises in food retailing (0.8 per cent), department stores (3.5 per cent), household goods retailing (1.1 per cent) and clothing, footwear and personal accessory retailing (1.6 per cent). Other retailing (0.0 per cent) and cafes, restaurant and takeaway services (0.0 per cent) were relatively unchanged. The rise this month follows subdued results in December 2018 (-0.4 per cent) and January 2019 (0.1 per cent).”

In seasonally adjusted terms, there were rises in Queensland (1.4 per cent), New South Wales (0.6 per cent), Victoria (0.8 per cent), Western Australia (0.6 per cent), South Australia (0.7 per cent), the Australian Capital Territory (1.7 per cent) and the Northern Territory (1.4 per cent). There was a fall in Tasmania (-0.7 per cent).

The trend estimate for Australian retail turnover rose 0.2 per cent in February 2019, following a 0.2 per cent rise in January 2019. Compared to February 2018, the trend estimate rose 2.9 per cent.

Online retail turnover contributed 5.6 per cent to total retail turnover in original terms in February 2019, which is unchanged from January 2019. In February 2018, online retail turnover contributed 5.1 per cent to total retail.

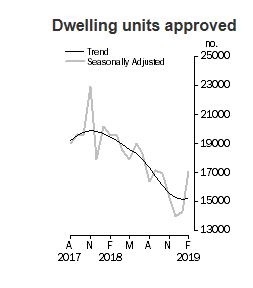

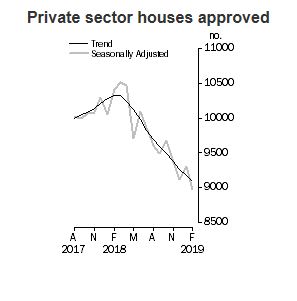

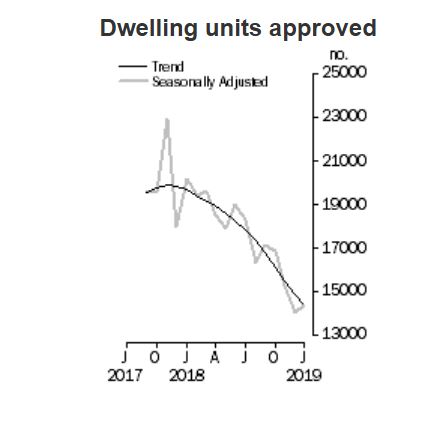

A rise in building approvals for apartments and townhouses has driven a 0.4 per cent increase in the total number of dwellings approved in Australia in February 2019, in trend terms, according to data released by the Australian Bureau of Statistics (ABS) today.

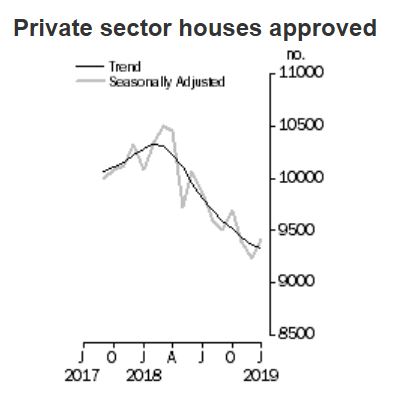

“Building approvals for private dwellings excluding houses rose 2.6 per cent in February.” said Justin Lokhorst, Director of Construction Statistics at the ABS. “Meanwhile, private houses fell a further 0.8 per cent”.

Among the states and territories, total dwelling approvals rose in February in New South Wales (3.1 per cent) and Western Australia (2.0 per cent), in trend terms. Falls were recorded in the Northern Territory (6.5 per cent), the Australian Capital Territory (6.3 per cent), Queensland (2.0 per cent), South Australia (1.1 per cent) and Victoria (0.8 per cent). Tasmania was flat.

Declines in approvals for private houses were recorded in New South Wales (2.0 per cent), Victoria (1.1 per cent) and Queensland (0.8 per cent), while increases were recorded in South Australia (2.0 per cent) and Western Australia (0.5 per cent).

In seasonally adjusted terms, total dwellings rose by 19.1 per cent in February, largely driven by rises in Victoria (37.3 per cent) and New South Wales (25.2 per cent). Private dwellings excluding houses rose 64.6 per cent, while private houses decreased by 3.6 per cent.

The value of total building approved rose 1.3 per cent in February, in trend terms. The value of non-residential building rose 1.9 per cent, while residential building increased 0.8 per cent.

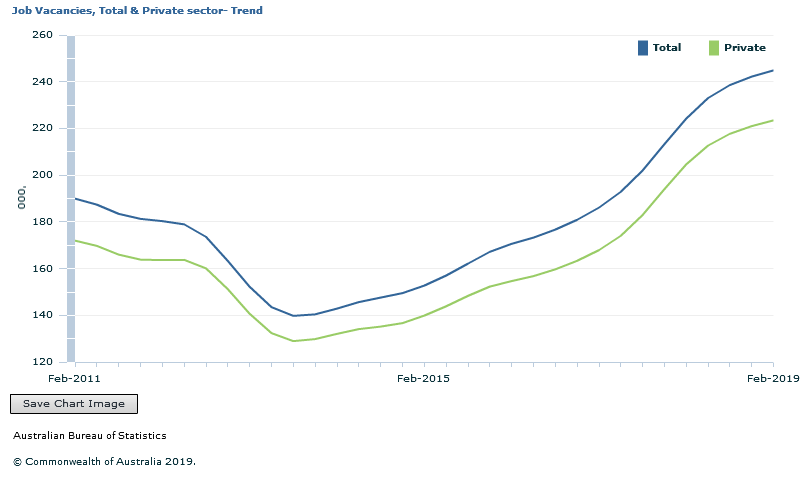

The number of job vacancies in Australia increased by 1.1 per cent over the February 2019 quarter, according to new trend figures from the Australian Bureau of Statistics.

Bruce Hockman, Chief Economist at the ABS, said that job vacancies continued to grow but at a slower rate than in 2018.

“Growth in the quarterly trend measure of job vacancies eased further to 1.1 per cent, which was well below the 5.2 per cent seen a year ago,” Mr Hockman said.

“This was consistent with the recent slowing in other economic indicators.”

Over the year, job vacancies increased by 9.2 per cent, with private sector vacancies increasing by 9.2 per cent and public sector vacancies by 9.4 per cent.

The seasonally adjusted number of job vacancies increased by 1.4 per cent over the February 2019 quarter.

In original series terms, New South Wales contributed the most to the growth in vacancies over the year, with health care and social assistance, and construction the two leading industries.

Australia’s trend unemployment rate remained steady in February 2019 at 5.0 per cent, from a revised January 2019 figure, according to the latest information released by the Australian Bureau of Statistics (ABS).

But there are signs of changes ahead. Have we reached the floor?

ABS Chief Economist Bruce Hockman said: “The trend unemployment rate declined 0.5 percentage points over the year, from 5.5 per cent to 5.0 per cent. The pace of decline slowed in recent months, which was consistent with the slowdown seen in recent Job Vacancies and GDP numbers.” Employment and hours

In February 2019, trend monthly employment increased by 20,600 persons. Full-time employment increased by 12,300 persons and part-time employment increased by 8,200 persons.

Over the past year, trend employment increased by 290,700 persons (2.3 per cent) which was above the average annual growth over the past 20 years (2.0 per cent).

The trend monthly hours worked increased by 0.1 per cent in February 2019 and by 1.9 per cent over the past year. This was slightly above the 20 year average year-on-year growth of 1.7 per cent.

Underemployment and underutilisation

The trend monthly underemployment rate decreased by less than 0.1 percentage points to 8.1 per cent in February and by 0.4 percentage points over the year. The trend underutilisation rate decreased less than 0.1 percentage points to 13.1 per cent, and by 0.9 percentage points over the year.

States and territories trend unemployment rate

The trend unemployment rate increased in Tasmania, decreased in Queensland, and remained steady in all other states and territories. Seasonally adjusted data

The seasonally adjusted unemployment rate decreased 0.1 percentage point to 4.9 per cent in February 2019, while the participation rate fell 0.2 percentage points to 65.6 per cent. The seasonally adjusted number of persons employed increased by 4,600.

The net movement of employed in both trend and seasonally adjusted terms is underpinned by around 300,000 people entering and leaving employment in the month.

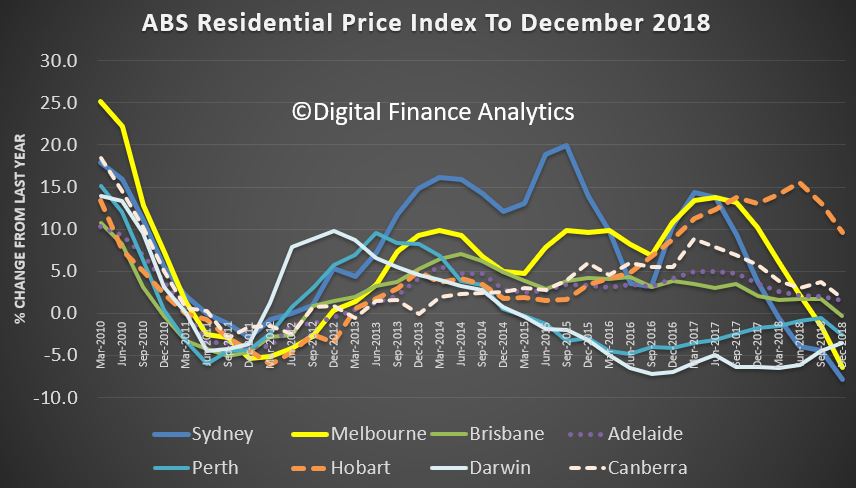

Residential property prices fell 2.4 per cent in the December quarter 2018, according to figures released today by the Australian Bureau of Statistics (ABS). The total value of Australia’s 10.3 million residential dwellings fell by $133.1 billion to $6.7 trillion. The mean price of dwellings in Australia is now $651,100, and falling.

Plus the number of home transfers complete are trending down as sales volumes decline, and stock rises.

Chief Economist for the ABS, Bruce Hockman said: “Australia’s two largest cities continue to lead the fall in property prices. These falls follow a period of solid growth, where prices in Sydney rose 68 per cent and Melbourne rose 54 per cent, over the five years to December quarter 2017.”

Sydney property prices fell 3.7 per cent in the December quarter 2018 and have continued to fall since September quarter 2017, while Melbourne property prices recorded the fourth consecutive quarter of falls (-2.4 per cent).

Here are the annual trends. Hobart and Canberra are still in poisitve territory (but falling).

Mr. Hockman said: “While property prices are falling in most capital cities, a tightening in credit supply and reduced demand from investors and owner occupiers have had a more pronounced effect on the larger property markets of Sydney and Melbourne.”

Through the year growth in residential property prices fell 5.1 per cent in the December quarter 2018. Falls were recorded in Sydney (-7.8 per cent), Melbourne (-6.4 per cent), Darwin (-3.5 per cent), Perth (-2.5 per cent) and Brisbane (-0.3 per cent).

We also see continuing falls in the number of home transfers (the end result of sales). The last quarter of 2018 is still preliminary, but the trends are pretty clear now. Falls in Melbourne appear the most significant.

But Sydney is not far behind.

Other states also appear weaker (even Hobart, Adelaide and Canberra). Expect more home price falls ahead.

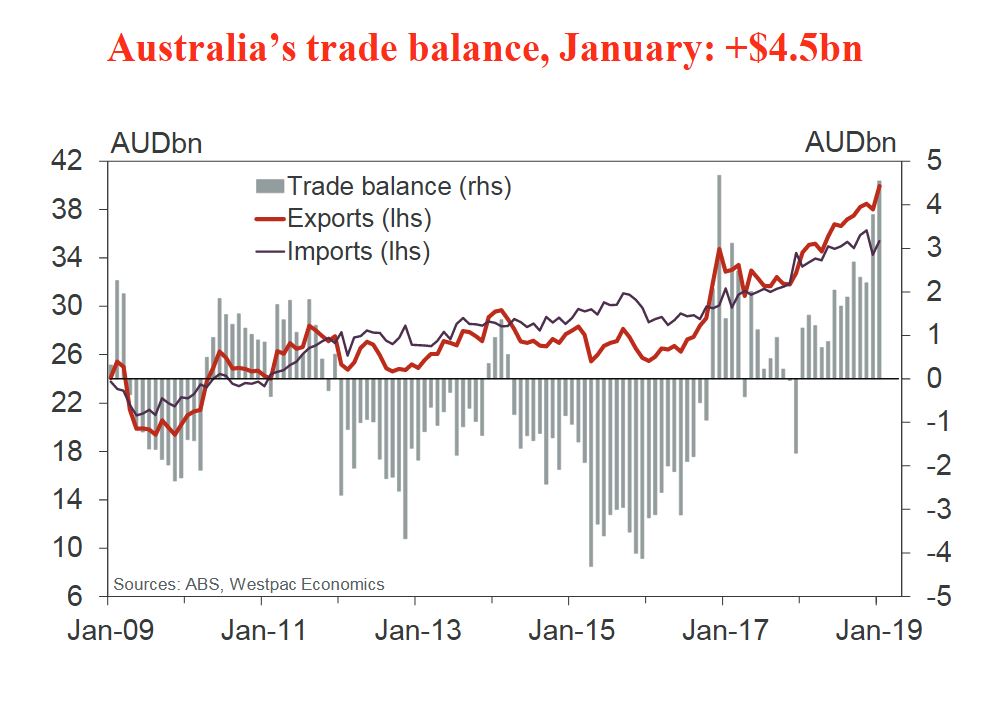

The ABS released the latest trade data to end January 2019. The surplus jumped to $4.5bn which is the second highest on record. The largest was $4.7bn surplus in December 2016.

Westpac highlighted that the January outcome was a $0.8bn improvement on December and exceeded expectations (market median $2.75bn and Westpac $3.1bn).

Imports did rebound in the month, +3.3%, following a 5.5% fall last month (vs a forecast +4%).

Exports were much stronger than anticipated, increasing by 5.0%, up $1.9bn (vs a forecast +2.2%).

Export strength was largely centred on a sharp rebound in gold off a low base, up 174% (Westpac expected a 75% rebound).

In dollar terms, gold accounted for $1.4bn of the $1.9bn increase in total exports in the month.

Coal exports rose 6%, following a couple of softer months, and metal ores increased by 3.4%, boosted by the higher iron ore price. But rural exports have been more resilient over the past couple of months – however the drought in NSW and surrounds remains a considerable headwind.

Metal ores and coal both advanced in January, up a combined $0.6bn.

The trade surplus widened in 2018 and in to 2019 on higher export earnings, boosted by rising commodity prices.

Notably, commodity prices have surprised to the high side in part due to supply disruptions having an amplified impact in a market where supply and demand are in relatively tight balance.

The $4.5bn surplus for January compares with a Q4 monthly average of $2.8bn.

The surplus for Q1 as a whole is expected to be a material improvement on that in Q4, with export volumes forecast to rise (following a disappointing second half of 2018) and on a likely further increase in the terms of trade.

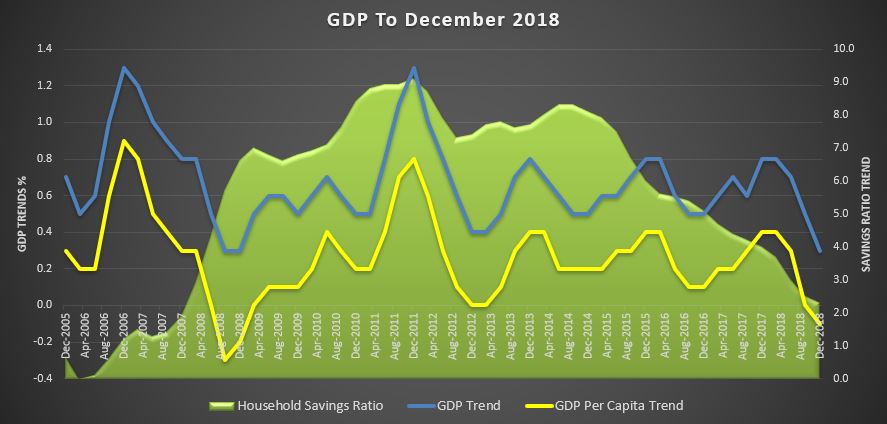

The Australian economy grew 0.2 per cent in seasonally adjusted chain volume terms in the December quarter 2018, according to figures released by the Australian Bureau of Statistics (ABS) today. But the heavy lifting was done by Government, leading to a 2.3% annual result. In seasonally adjusted terms we had two quarter falls in GDP per capita, so we are technically in recession on a per capital basis.

Actually the December data provided no major surprises as both the headline GDP and behaviour of consumers were broadly as anticipated. This is also true on housing, investment and public demand.

The trend data shows a fall in GDP, GDP per capital and in the savings ratio. Expect significant fiscal stimulus in the budget, and more after the election. This is an economy running of just a few cylinders.

New home building activity fell by 3.6 per cent during the final quarter of 2018 while home renovation activity declined by 3.1 per cent. Despite the softening at the end of 2018, activity was still higher than in the same quarter a year earlier.

Here is the ABS summary:

AUSTRALIAN ECONOMY GREW BY 0.2%

Australia’s gross domestic product (GDP) grew by 0.2% in the December quarter 2018, following a 0.3% rise in the September quarter. The Australian economy grew 2.3% through the year.

Government final consumption expenditure rose 1.8% in the December quarter 2018 and remains strong through the year at 5.6%. National non-defence (4.2%) was the main contributor to growth in the quarter, due to increases in social benefits to households from continued government spending on disability, health and aged care services. State and local government expenditure increased 1.1% driven by rises in non-employee expenses.

GOVERNMENT FINAL CONSUMPTION EXPENDITURE, Volume measures: Seasonally adjusted

SUSTAINED GROWTH IN INVESTMENT BY GENERAL GOVERNMENT

General government gross fixed capital formation increased 2.7% this quarter. The rise was driven by state and local general government (6.3%), with continued strength due to public infrastructure investment. This was offset by national general government, which fell 5.7% following defence purchases in the September quarter. Through the year general government gross fixed capital formation has risen 9.0%, again reflecting the high number of public infrastructure projects occurring across the country.

GENERAL GOVERNMENT GROSS FIXED CAPITAL FORMATION, Volume measures: Seasonally adjusted

BUILD UP IN INVENTORIES

Inventories held by business increased $685m in the December quarter 2018.

CHANGE IN INVENTORIES – Selected industries, Volume measures: Seasonally adjusted

GROWTH IN HOUSEHOLD CONSUMPTION SLOWS

Household final consumption expenditure increased 0.4% in the December quarter 2018, with through the year growth moderating to 2.0%. The growth in household consumption was driven by spending on health, clothing and footwear, and hotels, cafes and restaurants. There were falls in household spending for electricity, gas and other fuel, purchases of vehicles and furnishings and household equipment.

HOUSEHOLD FINAL CONSUMPTION EXPENDITURE, Volume measures: Seasonally adjusted

BROAD BASED GROWTH IN COMPENSATION OF EMPLOYEES

Compensation of Employee (COE) increased 0.9% in December quarter 2018 due to strength from both the private and public sector. Through the year COE increased 4.3% and with growth above its five year December average of 3.4% growth.

COMPENSATION OF EMPLOYEES, Current prices: Seasonally adjusted

HOUSEHOLD SAVING RATIO INCREASED MARGINALLY

The household saving ratio rose to 2.5% in the December quarter 2018. This slight pick up was due to modest growth in household disposable income alongside lower growth in household spending. The growth in gross disposable income was due to continued growth in compensation of employees as well as an increase in insurance claims received by households.

HOUSEHOLD SAVING RATIO, Current prices: Seasonally adjusted

Chief Economist for the ABS, Bruce Hockman, said: “Growth in the economy was subdued, reflecting soft household spending and a decline in dwelling investment. The approvals for dwelling construction indicate that the decline in dwelling investment will continue.”

Household spending grew by 0.4 per cent, reflecting a continuation of modest spending in recent quarters. Investment in dwellings fell 3.4 per cent.

Falls in private investment dampened growth in the quarter. This was consistent with the decline in construction industry value added, falling 1.9 per cent. Services industries supporting construction activity detracted from growth with professional scientific and technical services industry value added declining for the first time in three years. Mining investment fell in the quarter as significant projects transitioned from the construction to the production phase. This is reflected in oil and gas production, which grew 7.7 per cent.

Public demand sustained growth in the quarter. Public investment remained at high levels with State and Local government growth of 6.3 per cent reflecting continued work on a number of large infrastructure projects. Government final consumption expenditure grew 1.8 per cent, with ongoing expenditure in health, aged care and disability services. This investment translates to ongoing strength from the healthcare industry, which remains the largest contributor to economic growth.

Mr Hockman said “As the economy transitions out of the mining boom, investment has remained strong with major public works driving growth around Australia.”

Australia’s current account deficit in seasonally adjusted terms decreased $3,582 million in the December quarter 2018 to $7,203 million driven mainly by increased goods and services exports, according to latest figures from the Australian Bureau of Statistics (ABS).

Australia’s net foreign debt liability position increased $35.4 billion to $1,082.9 billion., up 3%.

More downward pressure on the GDP? It looks like the economy has lost considerable momentum over the second half of 2018, thanks to whats happening in housing and weak consumer spending.

The balance on goods and services surplus in the December quarter 2018 was $8,425 million, a rise of $2,661 million. Exports of goods and services rose $3,676 million (3 per cent) and imports of goods and services rose $1,015 million (1 per cent). The net primary income deficit narrowed by $848 million to $15,318 million in the December quarter 2018.

In volume terms, falling exports and rising imports resulted in an expectation for international trade to detract 0.2 percentage points from growth in the December quarter 2018 Gross Domestic Product. In seasonally adjusted chain volume terms, the balance on goods and services surplus decreased $781 million, narrowing the surplus to $1,241 million.

Australia’s net international investment position was a liability of $975.7 billion at 31 December 2018, an increase of $36.5 billion on the revised 30 September 2018 position of $939.1 billion.

Australia’s net foreign debt liability position increased $35.4

billion to $1,082.9 billion. Australia’s net foreign equity asset

position decreased $1.1 billion to $107.2 billion at 31 December 2018

The number of dwellings approved in Australia fell by 3.2 per cent in January 2019, in trend terms, according to data released by the Australian Bureau of Statistics (ABS) today.

“The trend for the total dwelling approvals series has steadily declined over the past year,” said Justin Lokhorst, Director of Construction Statistics at the ABS. “The series is now at its lowest level since May 2013.”

The decrease in January was driven by private sector dwellings excluding houses (e.g. townhouses and apartments), which fell 8.1 per cent in trend terms.

Private sector houses also declined, by 0.4 per cent.

Among the states and territories, total dwelling approvals fell in January in the Australian Capital Territory (19.8 per cent), the Northern Territory (8.0 per cent), Victoria (4.5 per cent), Queensland (3.9 per cent), New South Wales (2.3 per cent) and South Australia (0.8 per cent) in trend terms. Western Australia (2.2 per cent) and Tasmania (1.4 per cent) recorded increases.

Approvals for private sector houses fell 0.4 per cent in January in trend terms. Queensland (1.4 per cent), New South Wales (0.6 per cent) and Victoria (0.3 per cent) declined, while increases were recorded in South Australia (2.3 per cent) and Western Australia (0.2 per cent).

In seasonally adjusted terms, total dwellings rose by 2.5 per cent in January, driven by rises in Western Australia (28.8 per cent), Tasmania (15.4 per cent) and New South Wales (12.0 per cent). Private dwellings excluding houses rose 2.7 per cent, while private houses also increased (by 2.1 per cent).

But as Westpac put it ” As a rule, January housing data should be taken with a large grain of salt – the low flows through the holiday period mean any month to month noise is amplified by seasonal adjustment”.

The value of total building approved fell 1.5 per cent in January, in trend terms, and has fallen for 14 months. The value of residential building fell 2.7 per cent, while non-residential building rose 0.4 per cent.

Australia’s trend unemployment rate remained steady in January 2019 at 5.1 per cent, from a revised December 2018 figure, according to the latest information released by the Australian Bureau of Statistics (ABS).

ABS Chief Economist Bruce Hockman said: “The unemployment rate has remained at 5.1 per cent for a second month, supported by strong participation in the labour force, at 65.7 per cent.” Employment and hours

In January 2019, trend monthly employment increased by 24,900 persons. Full-time employment increased by 16,800 persons and part-time employment increased by 8,100 persons.

Over the past year, trend employment increased by 295,500 persons (2.4 per cent) which was above the average annual growth over the past 20 years (2.0 per cent).

The trend employment to population ratio, which shows how employed the population is, rose to a 10 year high of 62.4 per cent.

“The 15-64 year old employment to population ratio reached a historical high of 74.1 per cent, with almost three of every four ‘working age’ Australians now employed”, Mr Hockman said.

The trend monthly hours worked increased by 0.1 per cent in January 2019 and by 1.6 per cent over the past year. This was slightly below the 20 year average year-on-year growth of 1.7 per cent.

The trend monthly underemployment rate remained steady at 8.3 per cent and decreased by 0.3 percentage points over the year. The trend underutilisation rate also remained steady at 13.3 per cent, and decreased by 0.7 percentage points over the past year.

States and territories

The trend unemployment rate increased in South Australia, Western Australia and Tasmania, decreased in New South Wales and Queensland, and remained steady in all other states and territories.

In January 2019, increases in trend employment were observed in most states and territories except Western Australia (down 1,700 persons),Tasmania (down 300 persons) and South Australia (down 200 persons). The largest increases were in New South Wales (up 11,200 persons), followed by Victoria (up 10,300 persons) and Queensland (up 3,500 persons).

Over the past year, increases in employment were observed in all states except Tasmania (down 1,400 persons). Both territories recorded falls in employment (the Northern Territory down 2,500 persons and the Australian Capital Territory down 2,300 persons). The largest increases were in New South Wales (up 133,900 persons), Victoria (up 118,800 persons) and Queensland (up 27,800 persons). The highest annual employment growth rates were in Victoria at 3.7%, followed by New South Wales at 3.4% and Queensland at 1.1%. New South Wales and Victoria were the only states to have a year-on-year growth rate in trend employment above their 20 year average. The monthly trend unemployment rate increased by 0.1 pts in Western Australia (6.6%) and Tasmania (6.2%). It increased by less than 0.1 pts in South Australia (6.0%) and the Northern Territory (5.0%). It remained unchanged in Victoria (4.5%) and the Australian Capital Territory (3.5%). It decreased by 0.1 pts in New South Wales (4.1%) and less than 0.1 pts in Queensland (6.1%).

The monthly trend underemployment rate increased in the Northern Territory (up 0.3 pts to 5.0%) and Victoria (up 0.1 pts to 8.2%). Decreases were seen in Tasmania (down 0.2 pts to 9.6%), Western Australia (down 0.1 pts to 9.2%) and the Australian Capital Territory (down 0.1 pts to 6.3%).

Increases to the trend participation rate were observed in the Northern Territory (up by 0.2 pts to 74.8%), South Australia (up by less than 0.1 pts to 62.8%), New South Wales (up by less than 0.1 pts to 65.1%) and Victoria (up by less than 0.1 pts to 65.9%). Decreases were observed in Tasmania (down 0.1 pts to 60.1%) and the Australian Capital Territory (down 0.1 pts to 69.6%). The monthly trend participation rate remained unchanged in Queensland (65.6%) and Western Australia (68.5%).