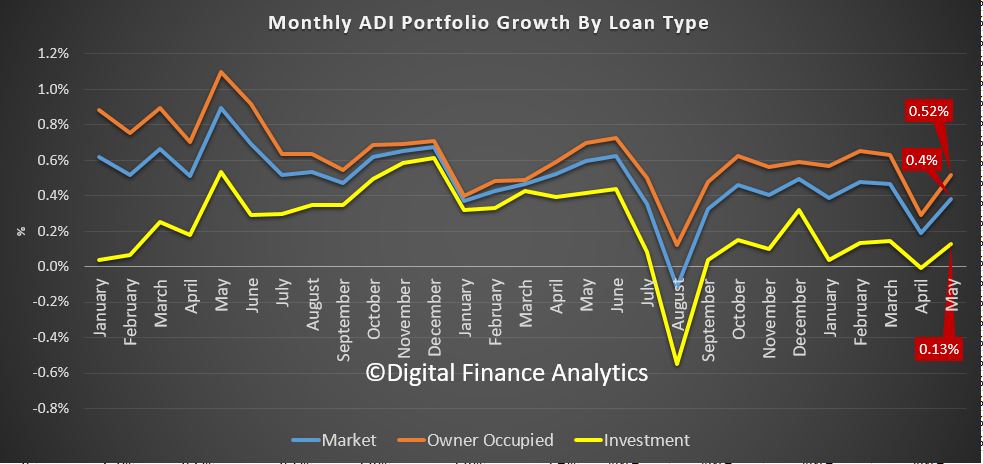

APRA has released their monthly banking statistics to end May 2018. After last months drop, we were waiting to see whether the loosening announced by APRA would show up, and yes, this month there was a rise in both the growth of owner occupied and investment lending!

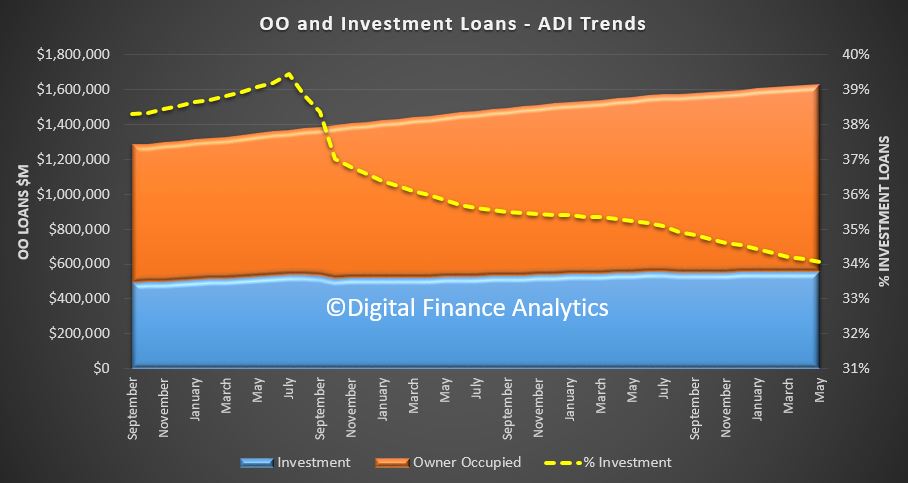

Total portfolio balances rose by 0.38% to $1.63 trillion, which would translate to be a 4.6% annualised growth rate, well above inflation and wages growth if this rate continued. Thus household debt still grows ever larger (a ratio of 188.6 household debt to income according to the RBA, last December), despite being at record and risky levels.

Within that, owner occupied loans rose 0.52% in the month to $1.08 trillion, up $5.5 billion while investment lending rose just 0.13% to $555 billion, up $712 million. Or in annualised terms, owner occupied loans are growing at 6.2% while investment loans are growing at 1.5%. Investment loans now make up 34.06% of all loans, which is still very high but falling.

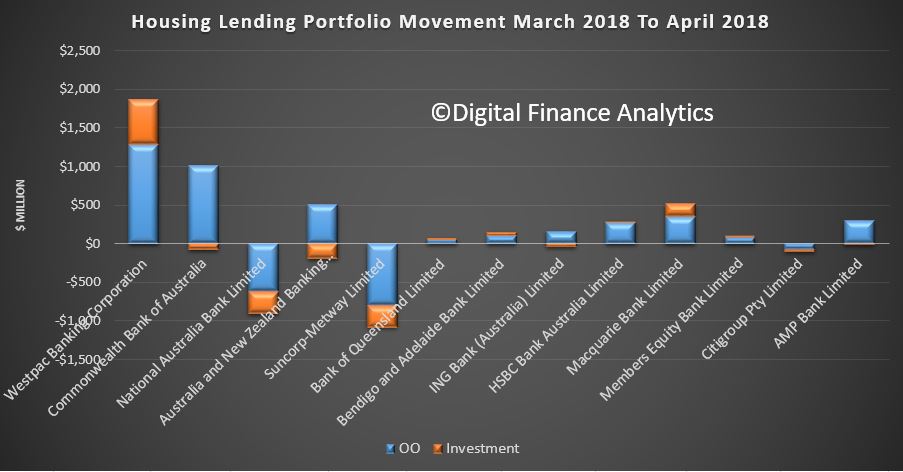

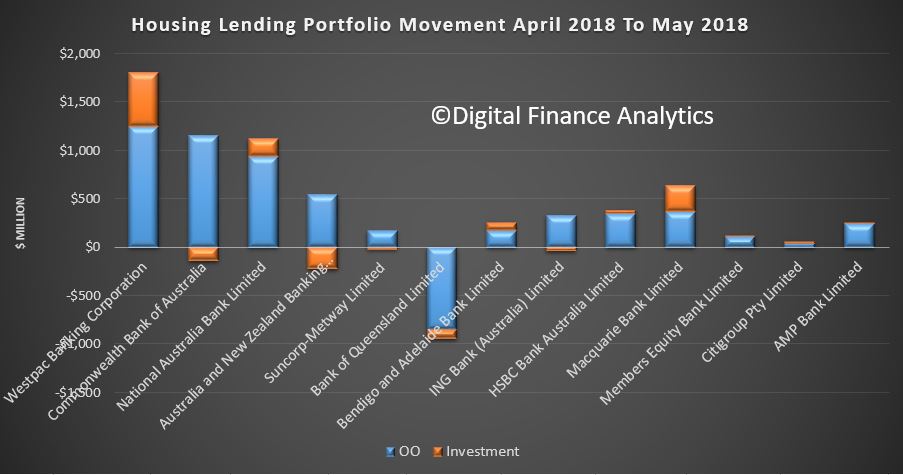

Turning to the individual lenders, there is little to be seen at the total portfolio level, with CBA leading the owner occupied lending, and Westpac the investment side of the ledger.

However, the individual portfolios within the lenders are more interesting, with Westpac still leading the way in investment lending portfolio growth, alongside Macquarie and NAB. However CBA and ANZ both saw their investor portfolio balances fall, while still expanding their owner occupied portfolios. Bank of Queensland dropped their balances in both owner occupied and investment lending this month. Clearly different strategies are in play.

Later we will get the RBA numbers, and we will see what the total market trends look like. We suspect non-banks will be growing faster than ADIs.

But overall, this appears to show a willingness to continue to let debt run higher to support home prices, so we are still on the same debt exposed path, should interest rates rise further, as is likely, as we discussed recently. Sound of can being kicked down the road once again!

In summary the total profits were up 9.1% compared with a year ago, total assets grew 3% over the same period, the capital base grew 5.8%, the capital adequacy rose 0.4 percentage points and the liquidity coverage ratio rose 8.3 percentage points.

So superficially, all the ratios suggest a tightly run ship. But it is worth looking in more detail at these statistics, because as we will see below the waterline, things look less pristine.

First, there were 148 Authorised Depository Institutions (ADI’s) a.k.a banks at the end of March.

Endeavour Mutual Bank Ltd changed its name from Select Encompass Credit Union Ltd, with effect from 9 February 2018.

Gateway Bank Ltd changed its name from Gateway Credit Union Ltd, with effect from 1 March 2018.

My Credit Union Limited had its authority to carry on banking business in Australia revoked, with effect from 1 March 2018.

So the net number rose by 1 from December 2017.

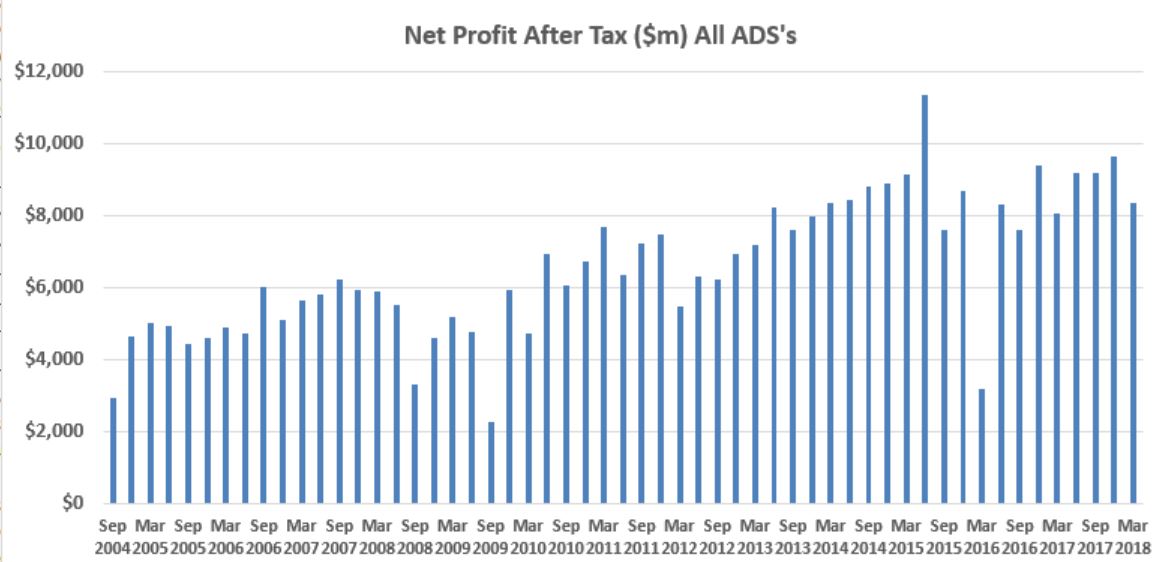

In terms of overall performance, APRA says that the net profit after tax for all ADIs was $36.4 billion for the year ending 31 March 2018. This is an increase of $3.0 billion or 9.1 per cent on the year ending 31 March 2017.

This was because of a nice hike in mortgage margins, in reaction to the regulator’s intervention in the investor mortgage sector, and a significant drop in overall provisions. But top line revenue growth slowed and margins have started to tighten. As a result, profits were lower this quarter compared with the prior three quarters.

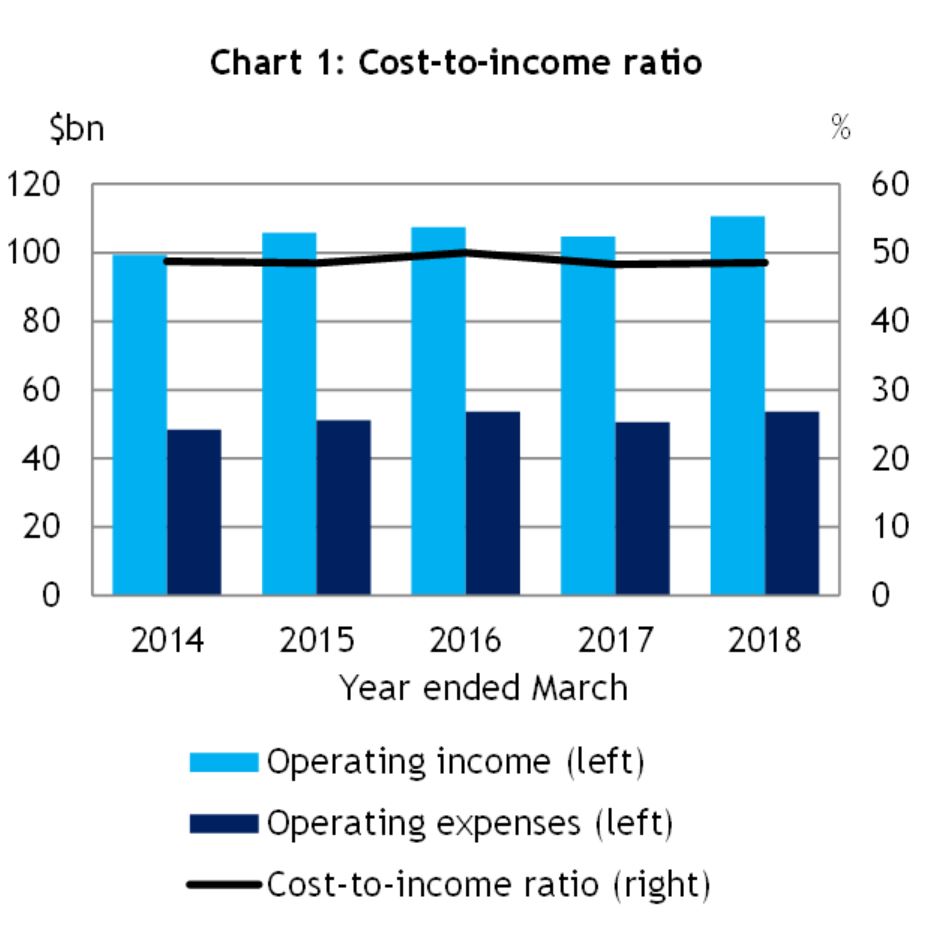

The cost-to-income ratio for all ADIs was 48.5 per cent for the year ending 31 March 2018, compared to 48.2 per cent for the year ending 31 March 2017. In other words, the costs of the business grew faster than income.

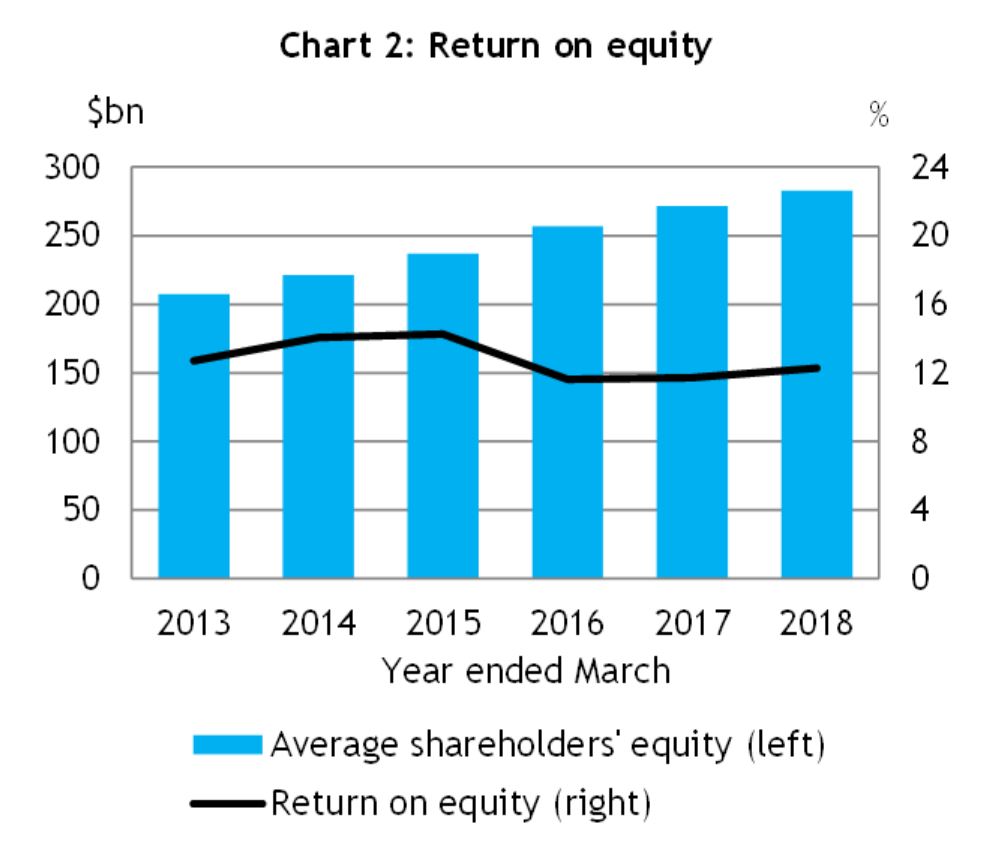

The return on equity for all ADIs increased to 12.3 per cent for the year ending 31 March 2018, compared to 11.7 per cent for the year ending 31 March 2017. We suspect this increase will not be repeated in the coming year.

That said an ROE of 12.3 per cent would still put the banking sector near the top of both Australian companies and global banks, reflecting a lack of true competition and some poor practices as laid bare by the Royal Commission. The quest for profit growth from some players has proved to be at the cost of customers. If banks do become more customer focussed, it is possible ROE’s will fall, and one-off penalties and fees (for example CBA, ANZ) will also hit returns.

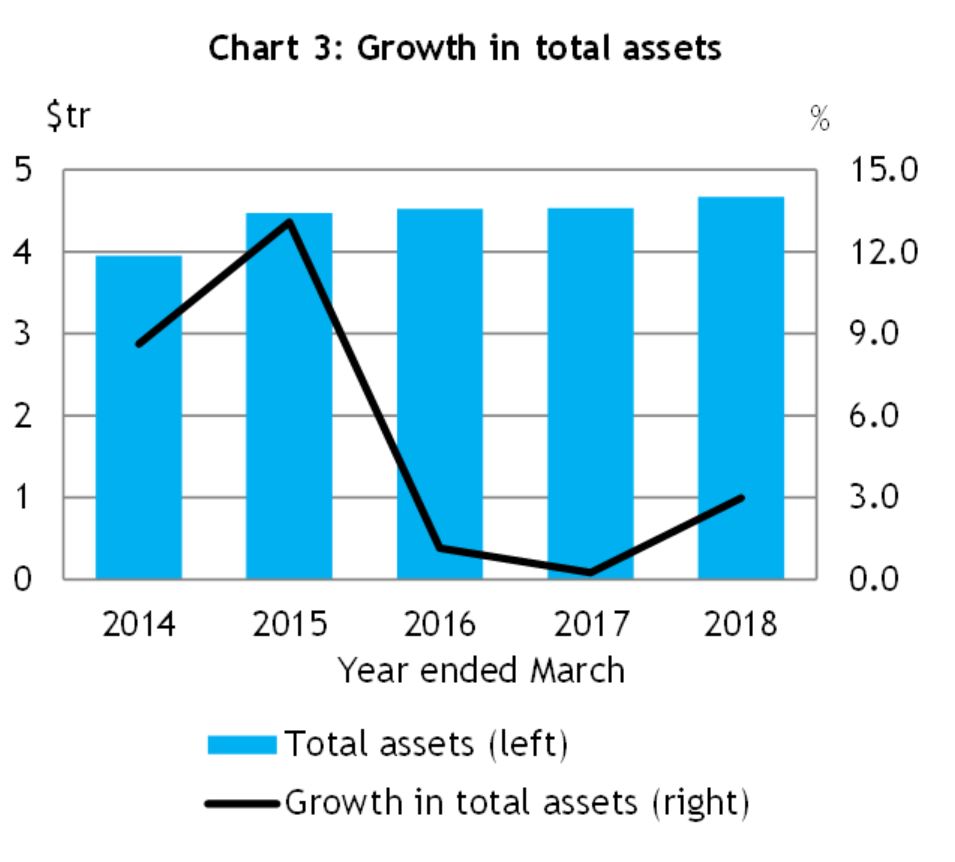

The total assets for all ADIs was $4.67 trillion at 31 March 2018. This is an increase of $135.9 billion (3.0 per cent) on 31 March 2017 and was largely driven by mortgages which grew strongly over the period.

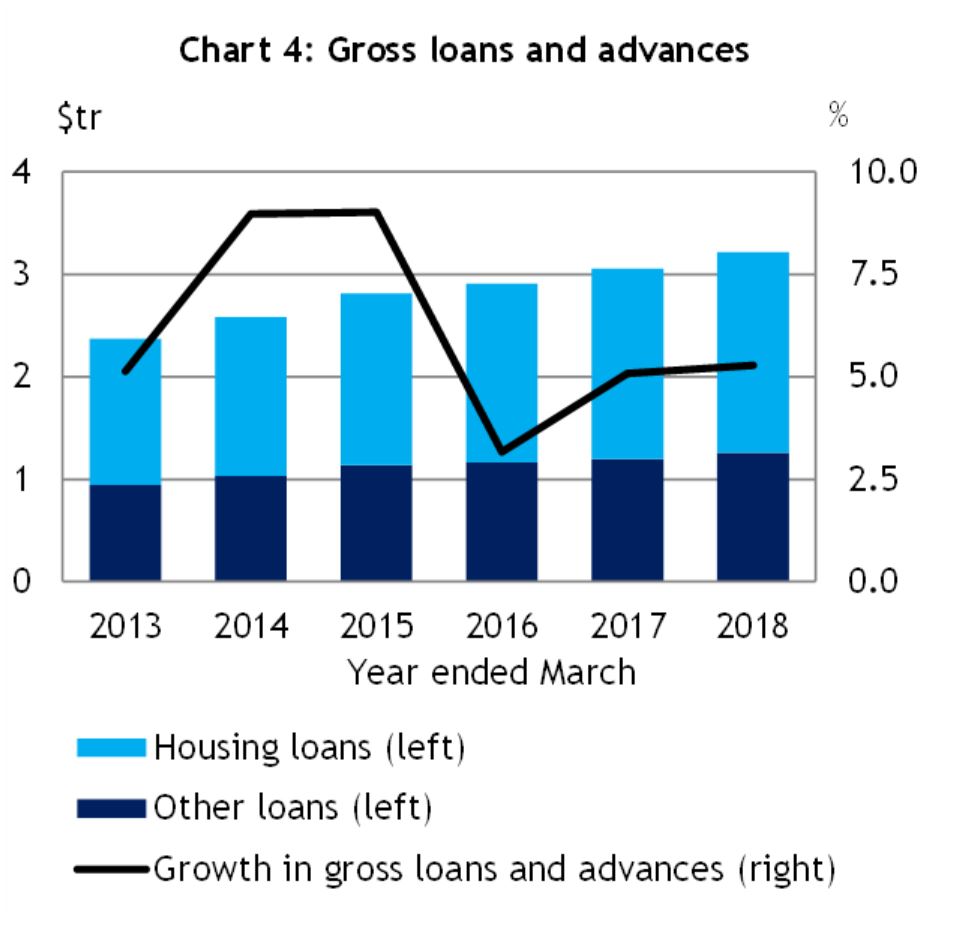

The total gross loans and advances for all ADIs was $3.22 trillion as at 31 March 2018. This is an increase of $161.4 billion (5.3 per cent) on 31 March 2017.

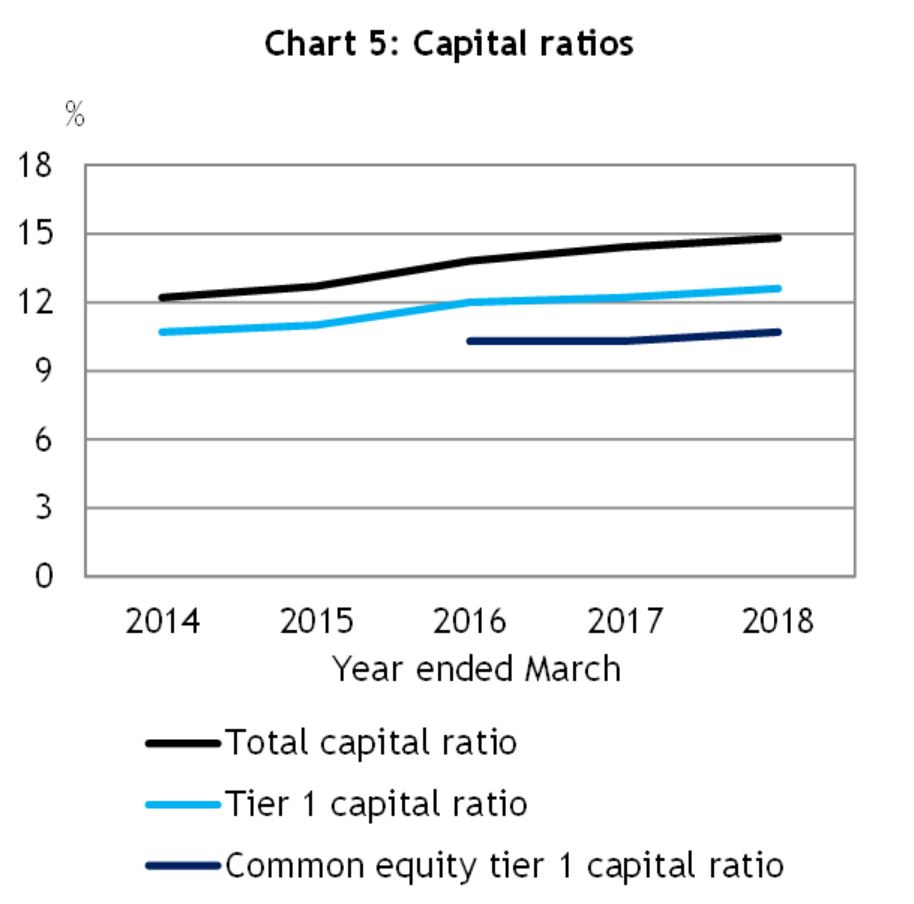

The total capital ratio for all ADIs was 14.8 per cent at 31 March 2018 , an increase from 14.4 per cent on 31 March 2017. This is a reflection of higher APRA targets. The common equity tier 1 ratio for all ADIs was 10.7 per cent at 31 March 2018, an increase from 10.3 per cent on 31 March 2017.

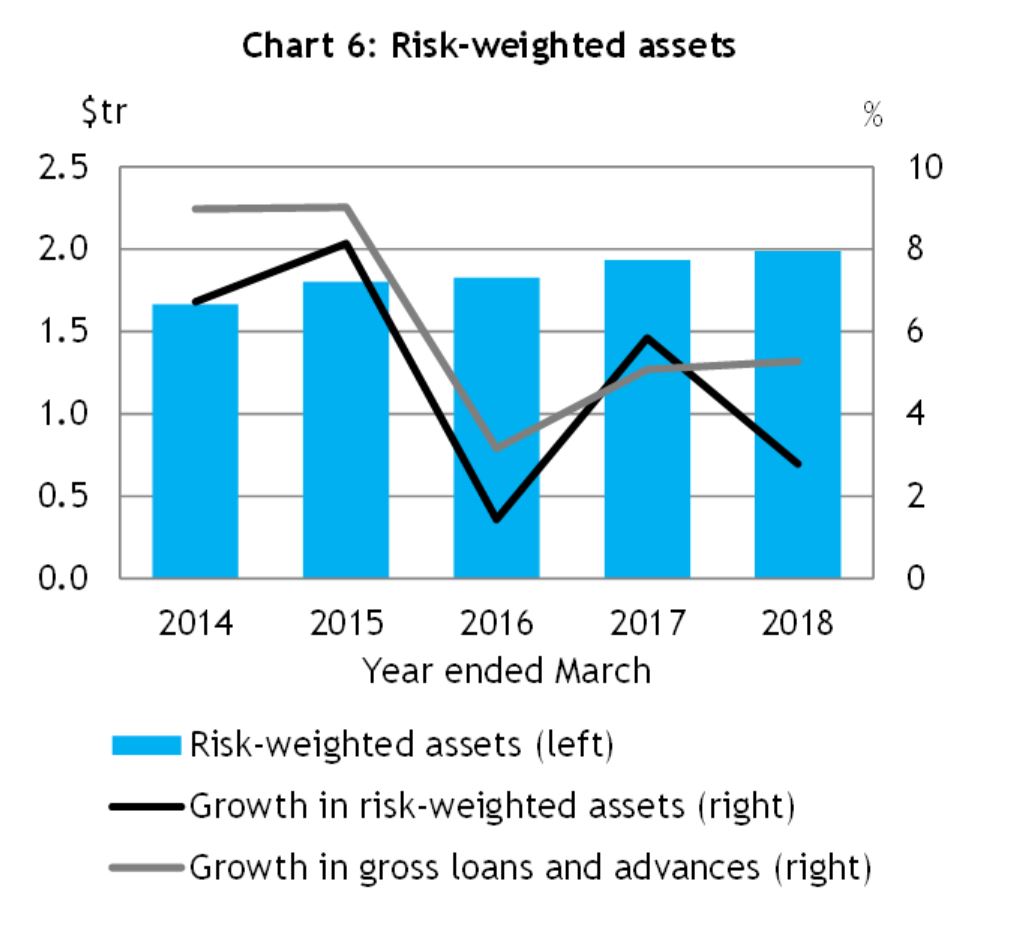

The risk-weighted assets (RWA) for all ADIs was $1.99 trillion at 31 March 2018, an increase of $53.9 billion (2.8 per cent) on 31 March 2017.

So if you compare the $3.22 trillion assets with the $1.99 trillion weighted assets for capital purposes, you can see the impact of lower risk weights for some asset types.

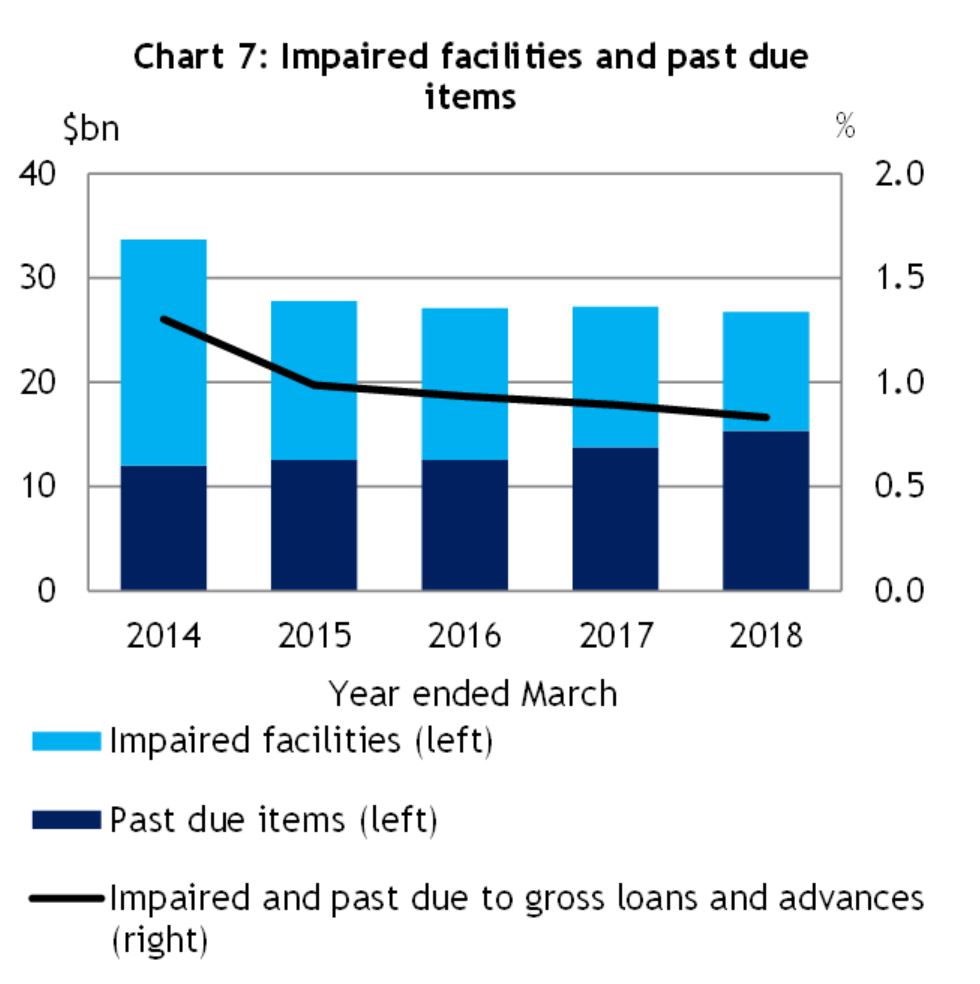

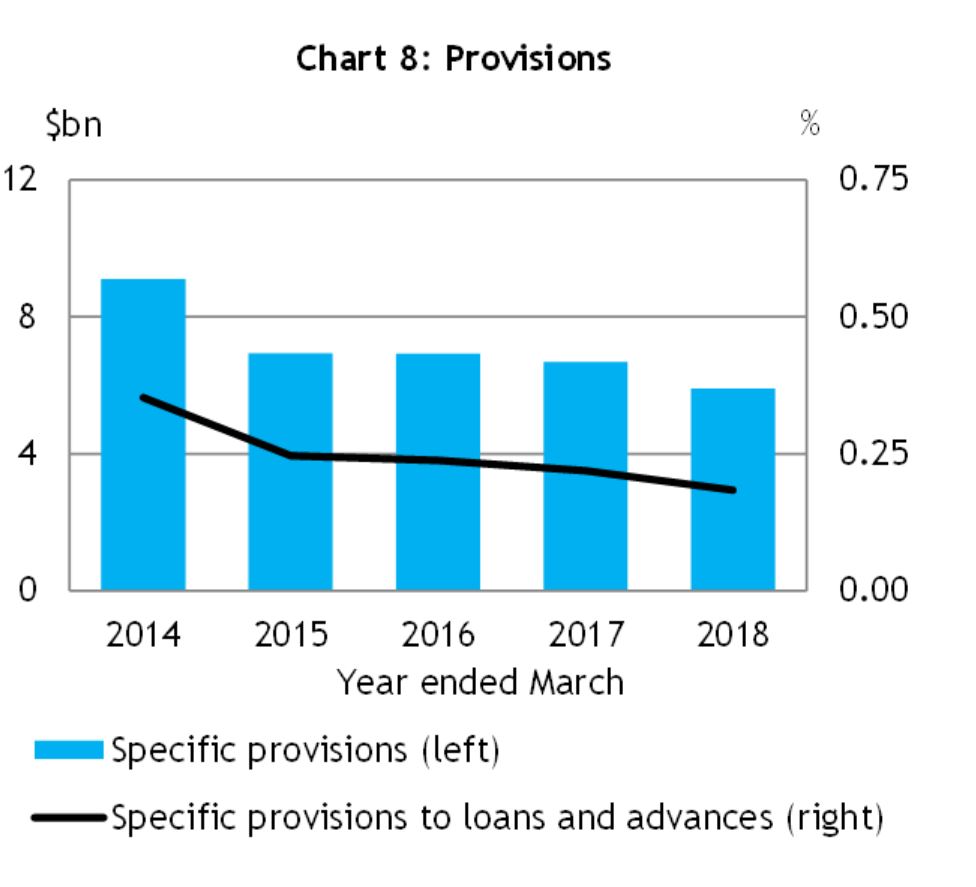

Looking at impairments for all ADIs we see that impaired facilities were $11.4 billion as at 31 March 2018. This is a decrease of $2.1 billion (15.7 per cent) on 31 March 2017.

Past due items were $15.4 billion as at 31 March 2018. This is an increase of $1.6 billion (11.5 per cent) on 31 March 2017. Rising 90 day delinquencies for mortgage loans was the main reason for the uplift, despite commercial loans performing a little better. Expect more delinquencies ahead, as indicated by our mortgage stress analysis. See our post “Mortgage Stress On the Rise”

That said, impaired facilities and past due items as a proportion of gross loans and advances was 0.83 per cent at 31 March 2018, a decrease from 0.89 per cent at 31 March 2017 and specific provisions were $5.9 billion at 31 March 2018. This is a decrease of $0.8 billion (11.7 per cent) on 31 March 2017. In addition, specific provisions as a proportion of gross loans and advances was 0.18 per cent at 31 March 2018, a decrease from 0.22 per cent at 31 March 2017.

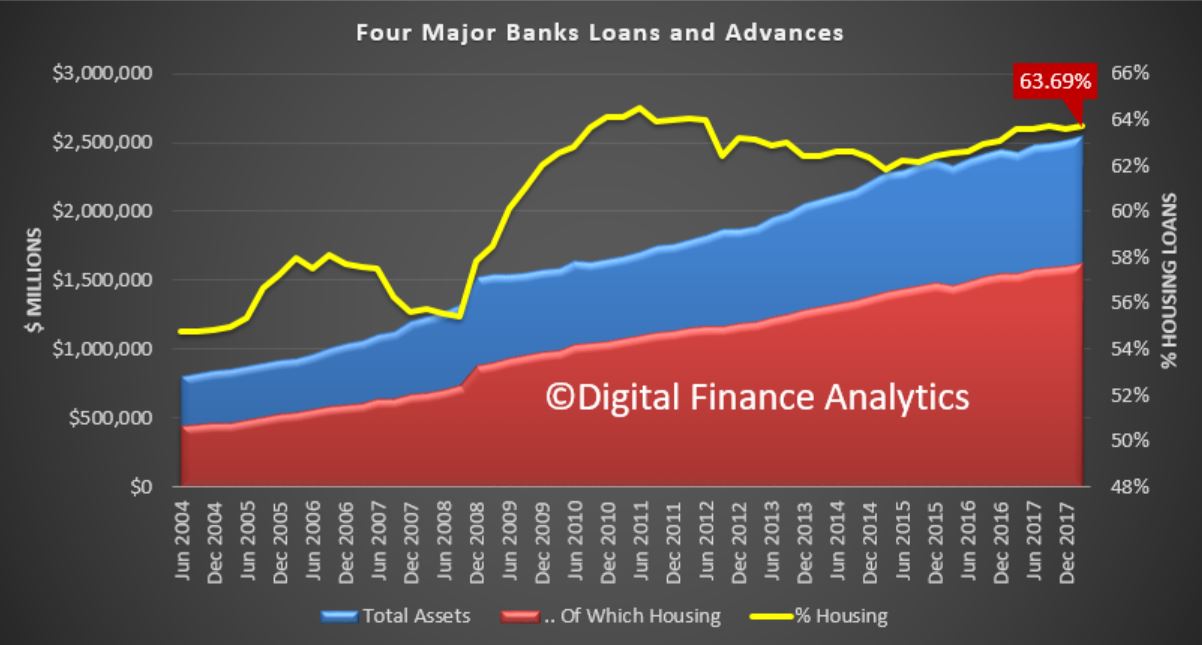

But there were two really important observations in the data, when we look at just the big four. The first is that total loans and advances by the four majors reached $2.55 trillion dollars, a record, and 63.69% of all loans were for housing lending. Not since 2012 has this been such a high proportion, its previous peak was 64.48% in the Jun 2011 quarter. The proportion of investor loans fell slightly, thanks to the recent tightening, but owner occupied lending by the big four remained strong. Think about it, nearly 64% of all loans are property related, so consider what a significant fall in prices would mean for them.

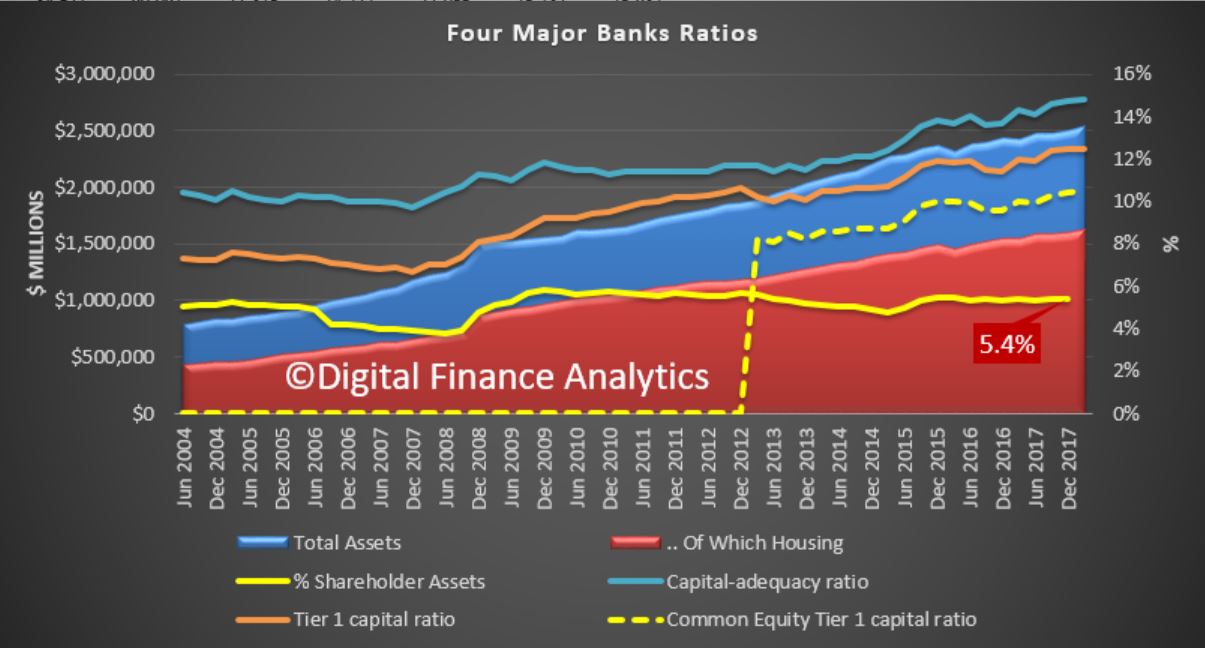

The second observation relates to the critical banking ratios. We all know that APRA has been pushing the capital rations and the newer CET1 (from January 2013) higher, and these are all rising, with the CET1 sitting, on an APRA basis at 10.5%, the highest its been.

However, if you look at the ratio of shareholder capital, it is sitting at a miserly 5.4% of all loans. In other words for every $100 invested in the loans made by an investor, they only have $5.40 at risk. This is, in extremis, the heart of the banking business, and this explains why shareholder returns are so high from the banking sector. These are highly leveraged businesses and if their risk and loan underwriting standards are not correctly calibrated it can go wrong very quickly. By the way the smaller banks and mutual have much lower leverage ratios, so they are simply less risky.

Banking is a risk business, but we see here laid bare, who is really taking the risks while the shareholders are doing very nicely thank-you!

We will delve into the detail later, but three charts tell the story, looking across the market of ADI’s with more than $1 billion of loans.

;

First, the number of loans being approved outside current serviceability standards has lifted to around 5% of all new loans. This reflects tighter controls in the banks, so they narrowed the serviceability aperture. But is also suggests that some loans are still getting funded under questionable parameters. Remember loan underwriting standards continue to tighten, so this will be an important measure to watch ahead.

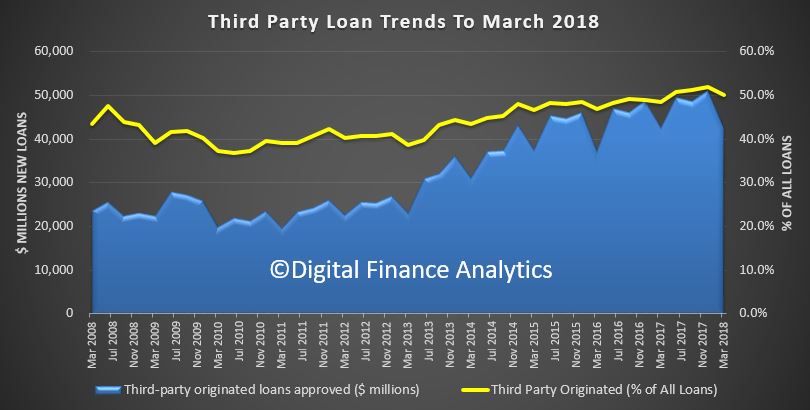

Second, the volume and share of loans via brokers, having reach a peak last year look to be falling, reflecting first lower absolute volumes of new loans, and second a preference by the banks to use their own channels. We will be watching the mix by channel in the months ahead, our thesis is mortgage brokers are going to have to work a lot harder down the track!

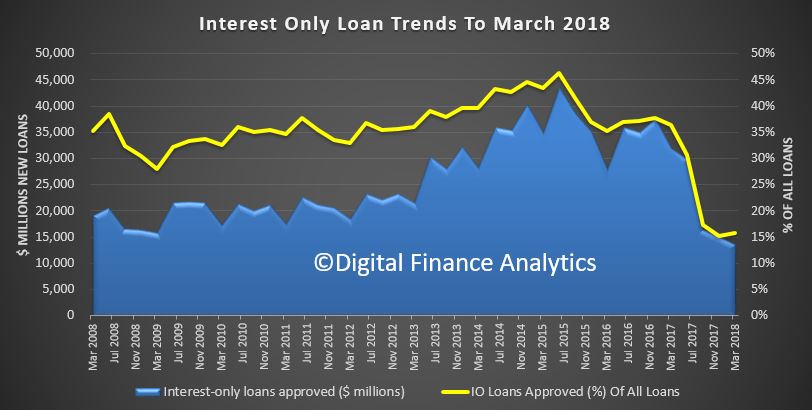

And third, the doozy, the share of interest only new loans have fallen to 15% of loans, and the value written in also down. So the APRA inspired intervention (better late then never) is hitting home. Again we need to watch whether there is a rebound as settings are tweaked to try and keep home prices falling further.

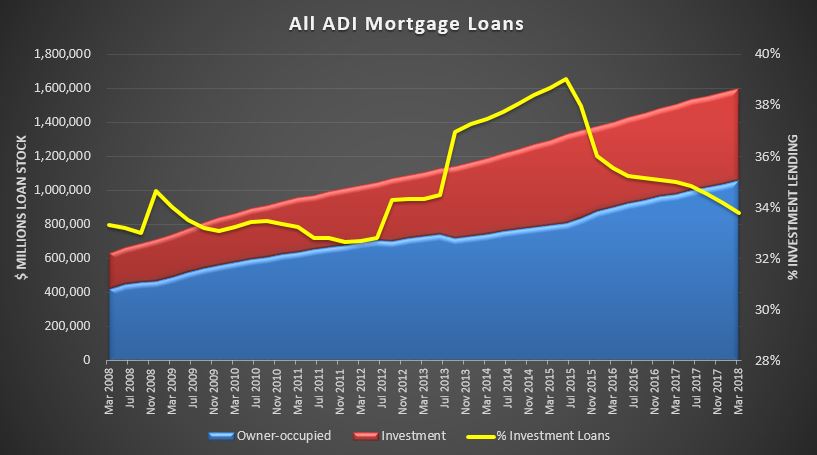

OK, I lied, there is a fourth slide. Despite all the tightening, the total balances grew again in March to $1.6 trillion, despite investment loans falling to 33.8% of the portfolio. So lets be clear, household debt is still rising, with investment loans rising 0.4% in the quarter and owner occupied loans rising by 2%. Or over the past year, 2.6% and 8% respectively. Still too hot in the current climate, in my view. So more tightening is needed, and I suspect a harder Debt to Income hurdle of 6% is where it will bite.

The enhanced focus on mortgage lending serviceability means that a consideration of the loan to income ratio or LTI is ever more important.

In the UK, where LTI calculations are the norm, the Bank of England first introduced limits on high LTI mortgages in 2014. These measures meant that no more than 15 per cent of mortgages issued should exceed a loan-to-income ratio of 4.5. The actions were not retrospective and few British lenders were impacted by the curbs.

The UK’s 4.5 LTI cap on 85 per cent of new lending is still in place. In June last year, Bank of England governor Mark Carney announced that the 4.5 ratio “insurance measures” will become “structural features of the UK housing market.

Last month, APRA, the prudential regulator announced that it would remove its 10 per cent benchmark on investor loan growth for banks that could confirm that their policies and practices meet a range of expectations.

But one of APRA’s expectations for banks is a commitment to develop

internal risk appetite limits on the proportion of new lending at very high debt-to-income levels (where debt is greater than six times a borrower’s income) and policy limits on maximum debt-to-income levels for individual borrowers.

So, it should be of no surprise to note that the Commonwealth Bank of Australia has announced that it has brought in its new debt-to-income measurement for borrowers.

CBA, who is the largest owner occupied mortgage lender in Australia has disclosed that it will now “monitor” loan applications with a debt-to-income ratio higher than 4.5 and will also bring in a new e-learning requirement for brokers that have not settled a CBA loan for more than a year. Applications with a DTI higher than 7.0 will be subject to a manual credit approval check.

The new measure will reportedly help the bank get a clearer picture of what its book looks like and to understand trends. Speaking of the decision, Daniel Huggins, CBA’s executive general manager, home buying, said:

At the Commonwealth Bank, we constantly review and monitor our home loan processes and policies to ensure we are maintaining our prudent lending standards and meeting our customers’ home buying needs. Our decision to implement a new debt-to-income measure is just another example of our ongoing commitment to responsible lending and meeting our regulatory commitments.

Last year, NAB introduced an LTI ratio calculation of 8 for all home loan applications. In February, this year, it was reduced to 7 a still generous 7 times.

The bank said at the time.

NAB is committed to lending responsibly and ensuring our customers can meet their home loan repayments today and into the future.

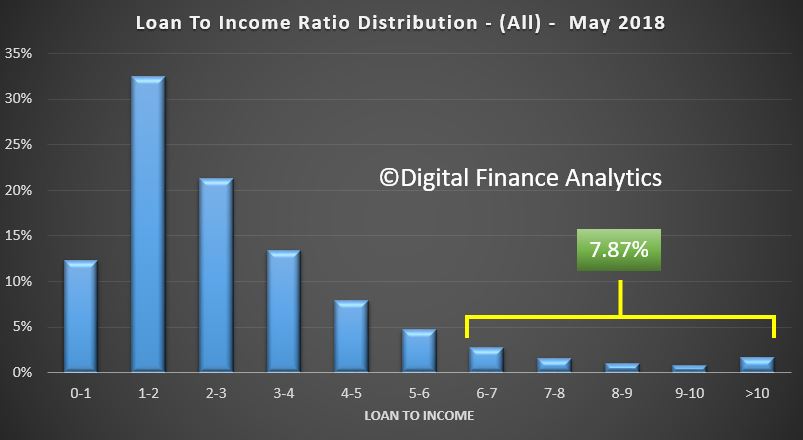

Now we have been looking at the current portfolio view of all mortgages in Australia from an LTI perspective using data from our core market model. This is based on our rolling survey of 52,000 households each year.

The relative distribution across the LTI bands highlights relative risks in the system.

We took a cut off of 6 times, in line with the APRA guidelines. On an all portfolio basis, across the country around 7.9% of all loans have a current loan to income ratio of 6 times or more. This is based on current loan values and current incomes, not those considered at the inception of the loan.

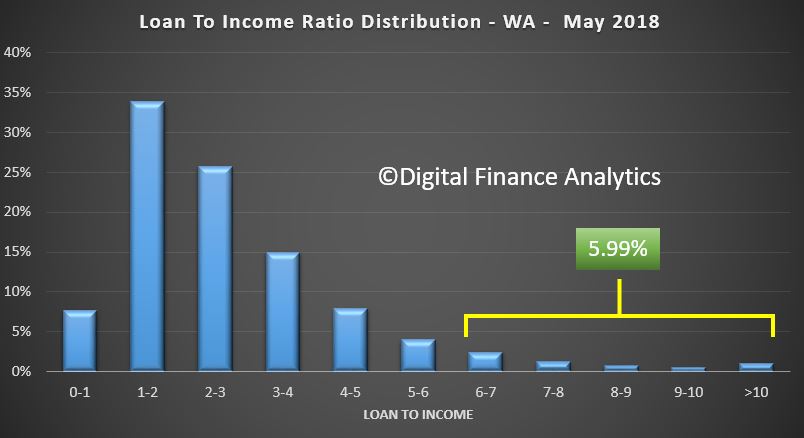

But there are some significant state variations, for example, loans in Western Australia have 6% of loans with an LTI of 6 or above. In the west the proportion is rising as incomes remain constrained, despite loans growing a little. This is thanks partly to capital being released via refinancing.

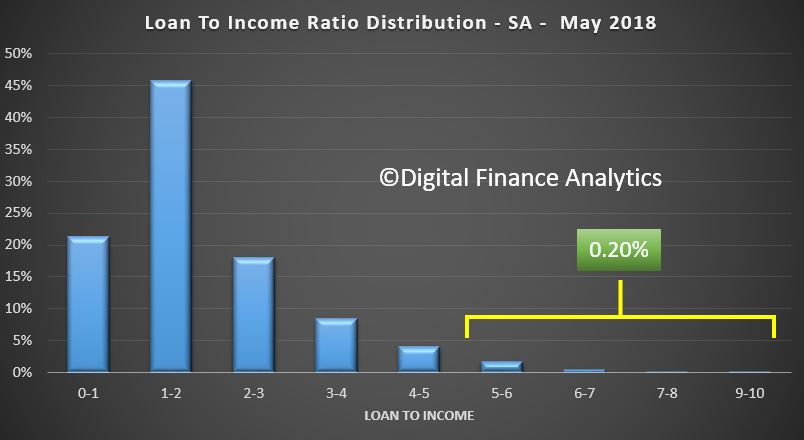

In South Australia, only a very small proportion of loans have a loan to income of 6 times or more.

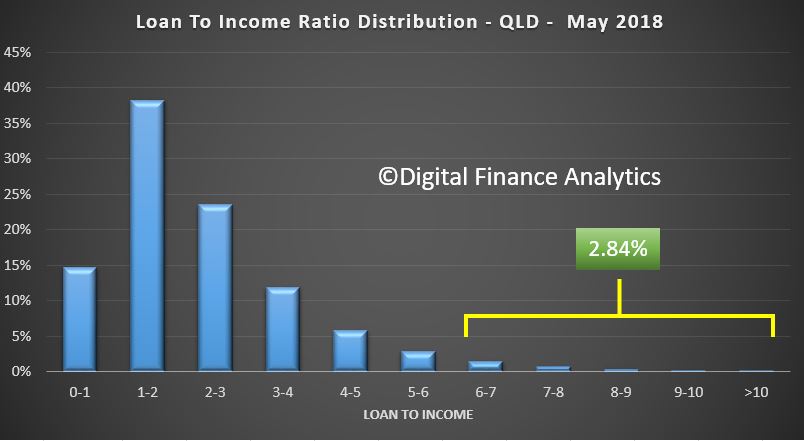

In Queensland, the total proportion above 6 times is 2.8%.

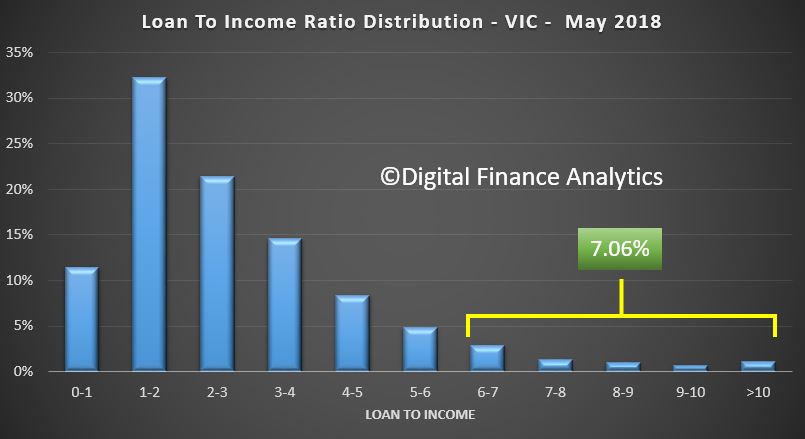

However things get more interesting in the eastern states, with 7.1% of households in Victoria holding a loan to income ratio of 6 times or higher.

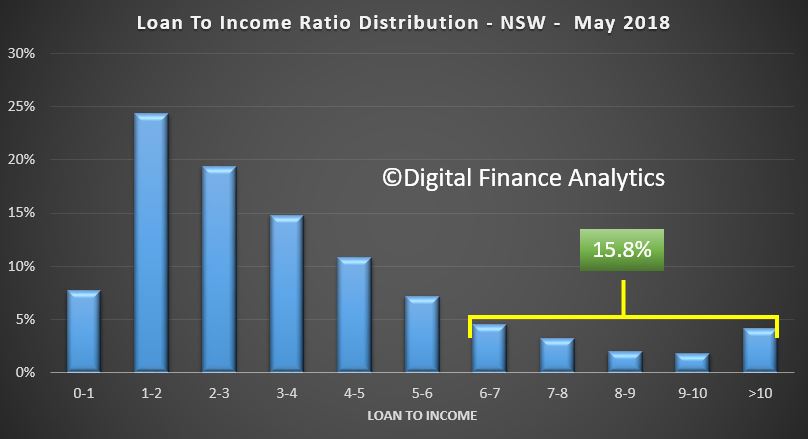

But the prize goes to New South Wales with a massive 15.8% of households currently holding loans with a loan to income ratio of 6 or more. This is of course explained by the high prices, big mortgages, and lose lending standards.

This analysis provides some insights into the pressures on households, as this higher multiples are indicative of larger payments being made to service the loan.

Thus we conclude the most severe issues will be found in NSW, where of course house prices are now firmly on the slide.

We will publish our latest mortgage stress data, to the end of May early next week. Finally, consider this, when I was a banker, the rule of thumb was 3 times one income plus 1 time the second. How the world has changed!

APRA has released their monthly banking statistics for ADI’s to April 2018. And now we are really seeing the tighter lending standards biting. In fact, Westpac apart, all the majors have reduced their investor property lending.

APRA reports for each lender the net total balance outstanding at the end of each month and by looking at the trends we see the net of loan roll offs and new loans. This is important, as we will see.

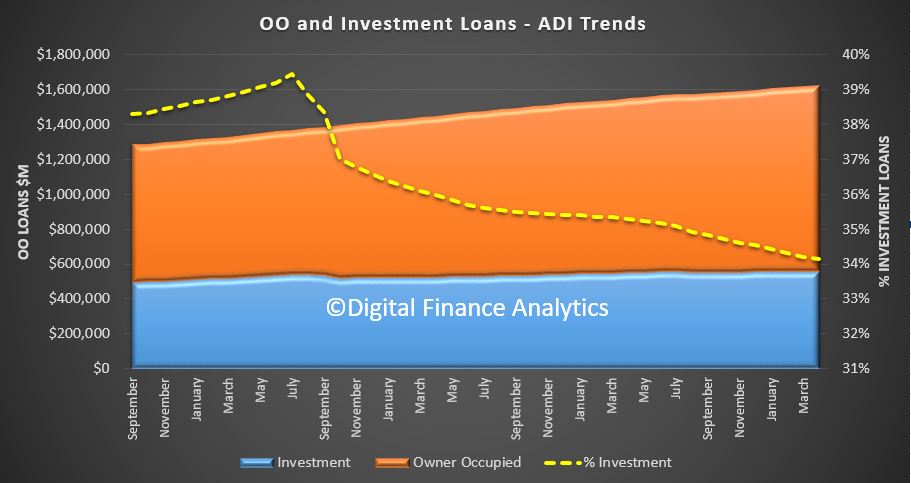

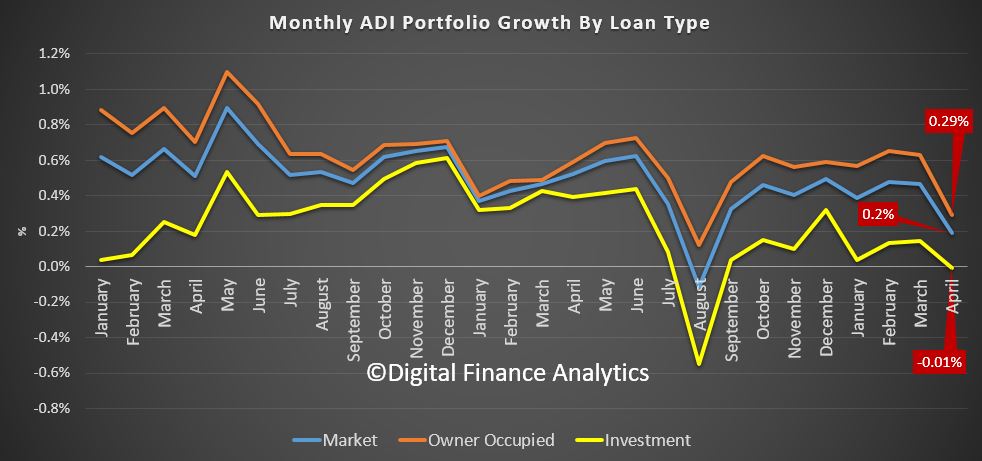

At the aggregate level, total lending for mortgages from ADI’s rose 0.2% in the month, up $3.0 billion to $1.62 trillion. Within that owner occupied loans grew by 0.29% or $3.1 billion to $1.07 trillion while investment loans fell slightly, down 0.01% of $42 million. As a result the relative share of investment loans fell to 34.14%.

The trend movement highlights the significance of the fall (the August 2017 point is an outlier thanks to reclassification), this is the weakest result for years. At an aggregate level, over 12 months this would translate to a rise of just 2.3%, significantly down from the 5-6% range of recent months.

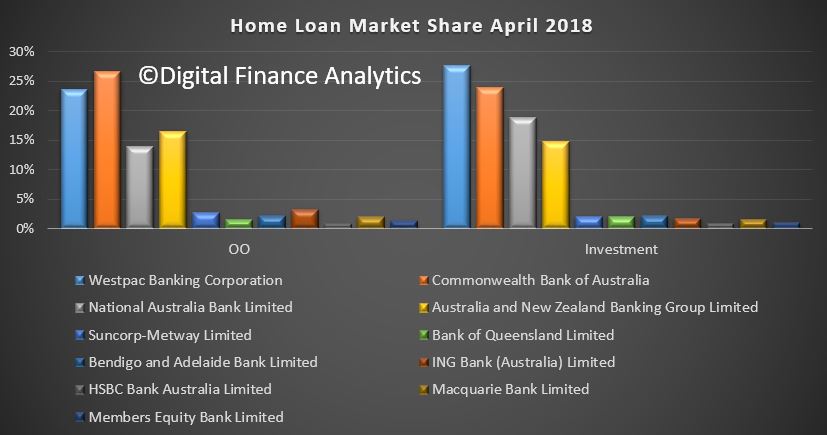

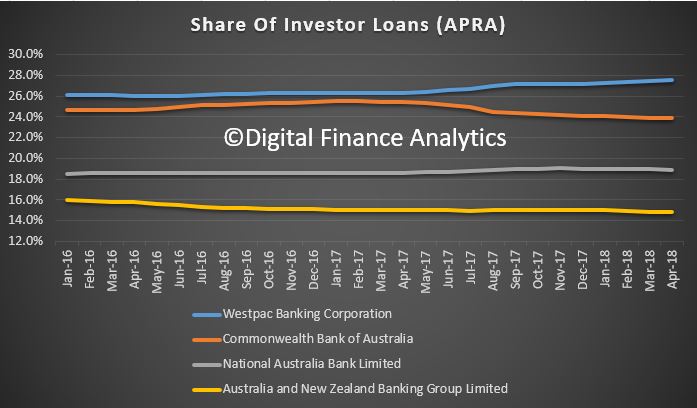

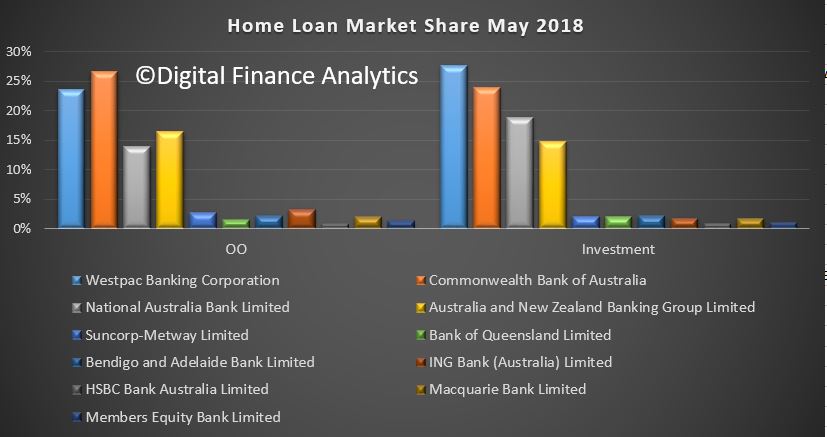

Turning to the individual market shares, at the aggregate level there was little change, other than Westpac’s share of investor loans grew to 27.6%, up from 26.1% in January 2016

Here is the trends from the big four. Westpac has continued to increase share of investor loans. CBA has fallen away the most significantly.

There has been almost no shift in owner occupied loan shares.

The monthly changes in value tell the story, with Westpac and Macquarie growing the value of their portfolios, across both owner occupied and investment lending. We see falls in net investor lending elsewhere.

We conclude that Westpac executed a different strategy in terms of mortgage origination compared with its competitors. They may be offering selective discounts to attract particular types of business, or they may have different lending standards, or both.

It is quite possible we will see other lenders trying to compete relative to Westpac in the investment loan domain ahead, as lending growth is needed to sustain profitability. But demand is also falling, so we expect lending momentum to continue to weaken, with the consequential impact on home prices and bank profitability. We are entering credit crunch territory!

When I last addressed this Committee, I outlined some of the many ways APRA is accountable to both the Parliament and the Australian people. These measures are crucial for APRA to maintain the trust of industry and the public as we aim to fulfil our mandate as a prudential regulator, promoting financial safety and thereby protecting the interests of bank depositors, insurance policyholders and superannuation members.

The core of APRA’s mission is safety and soundness. Clearly, some of the revelations emerging from the Royal Commission have been disturbing and go to the heart of whether financial institutions treat their customers fairly. However, while institutions have a great deal of work to do to restore trust, I want to emphasise that Australians can be reassured that the industry is financially sound, and that the financial system is stable. That reflects considerable policy reform and hands-on supervision, over a long period of time, designed to build strength and resilience. We don’t know when the next period of adversity will arrive or what will trigger it, but when it does arrive we need to have done what we could to strengthen the financial system so that it can continue to provide its essential services to the Australian community when they are needed most.

The importance of accountability has been one of our key themes this year, and was front and centre with the release in April of our review of executive remuneration practices in large financial institutions. Incentives and accountability can play an important role in driving positive outcomes such as growth, innovation and productivity, and also in deterring behaviours or decisions that produce poor risk-taking and damaging results. Our review found that while policies and processes existed within institutions to align remuneration with sound risk outcomes, their practical application was often weak. We have indicated that we are minded to strengthen the prudential framework to give better effect to the principles we want to see followed – less rewards based on narrow and mechanical shareholder metrics, and greater exercise of Board discretion to judge senior executive performance more holistically. But we have also urged institutions to push ahead with their own improvements, notwithstanding some investor opposition, in light of the long-term commercial benefits that can flow from better remuneration practices.

A lack of accountability for poor outcomes was a theme that also emerged in the Final Report of the Prudential Inquiry into the Commonwealth Bank of Australia, which was released earlier this month. The Report is clear and comprehensive, and provides a strong message – not just to CBA but to the entire financial services industry – about the importance of cultivating a robust risk culture, especially when it comes to non-financial risks. We are keen that the Report will be seen not just a road map for CBA, but a useful guide for all institutions in relation to strengthening governance, culture and accountability.

Residential mortgage lending is another area where APRA has been lifting industry standards. Although there remains more to do before we are ready to significantly dial back our supervisory intensity, there has been a lift in industry lending practices. As a result, last month we announced we would remove the 10 per cent investor growth benchmark for those lenders who could provide a range of assurances as to the quality of their lending standards and practices now and into the future.

Superannuation is an area where APRA consistently emphasises the need for trustees, regardless of size or ownership structure, to go beyond compliance with minimum regulatory requirements and aim to deliver the best possible outcomes for members. In this vein, we have just released the results of two thematic reviews of superannuation licensees; on board governance and the management of related parties. Both reviews noted improvements in industry practices in recent years, but also found more work was needed to address some longstanding weaknesses, including finding ways to bring fresh ideas, perspectives and skills onto trustee boards. Our post-implementation review of 2013’s Stronger Super reforms, launched last week, should also provide us additional insights on how the prudential framework is performing, and whether any adjustments would help to better achieve our objectives. Many of the findings in the Productivity Commission report into superannuation released this week are consistent with APRA’s approach to supervising RSE licensees. In particular, they align with APRA’s focus on enhancing the delivery of member outcomes through our engagement with trustees with “outlier” underperforming funds and products.

Technology is rapidly changing the way financial institutions operate. In all likelihood, the financial system will look very different in five years’ time relative to the way it looks today. Much of that change will bring benefits to the community, in the form of new competitors, products and ways of access. But it will also bring risks, and the accelerating threat of cyber-attacks to regulated entities has prompted APRA to recently propose its first prudential standard on information security. Industry consultation is ongoing, but we hope to implement the new cross-industry standard from 1 July next year. This is an issue which is only going to grow in importance.

Continuing to look ahead, APRA’s preparations are well advanced for the commencement of the Banking Executive Accountability Regime (BEAR), which will begin in just over a month. The BEAR largely strengthens APRA’s existing powers to identify and address the prudential risks arising from poor governance, weak culture, or ineffective risk management. However, I have made the point previously that while important, the BEAR alone will not remedy perceived weakness in financial sector accountability, and we have encouraged all regulated entities – not just ADIs – to use the new regime as a trigger to genuinely improve systems of governance, responsibility and accountability.

Finally, APRA is continuing to provide relevant information to the Royal Commission to help it in its inquiries. In addition, APRA and the Australian financial system more broadly, will be subject to intensive scrutiny from the International Monetary Fund in the weeks ahead as part of its 2018 Financial Sector Assessment Program (FSAP). The FSAP will examine in quite some detail financial sector vulnerabilities and the quality of regulatory oversight arrangements in Australia. As ever, APRA will fully cooperate with our international reviewers, and look forward to their report card, including any recommendations on how we could perform our role more effectively in the future.

With those opening remarks, we would now be happy to answer the Committee’s questions.

APRA has written to ADI’s saying that from the 5 May 2018, authorised deposit-taking institutions (ADIs) will be permitted to use the word ‘bank’ without restriction under the Banking Act.

Given the flack around the behaviour of the banks, and the Royal Commission, some may think twice about choosing to start using the term!

This is when changes to section 66 of the Banking Act 1959 , made as part of the Treasury Laws Amendment (Banking Measures No. 1) Act 2018, will take effect.

The terms ‘credit union’, ‘credit society’, credit co-operative’ and ‘building society’ will continue to be restricted terms. ADIs that are credit unions or building societies may continue to use those terms, as well as the restricted words bank, banker and banking, including as part of a corporate or business name.

The changes to the Banking Act also allow APRA to make a determination under section 66AA that an ADI or class of ADIs is not permitted to use the word bank (which would also apply to the words banker and banking). APRA will consider using this power in respect of ADIs that do not have the ordinary characteristics of banks (for example, purchased payment facilities), or otherwise in serious or unusual circumstances that warrant the making of a determination. We will consult any affected ADIs prior to making such a determination under section 66AA.

APRA will be revising its Guidelines for the Implementation of Section 66 of the Banking Act to reflect the recent legislative changes, and expects to publish these by mid-2018.

Many reporting standards make distinctions between bank and non-bank ADIs for reporting purposes. With the changes to section 66, this distinction may no longer be appropriate. APRA is currently considering this matter and will consult with industry on any proposed changes to reporting standards. In the interim, ADIs should continue to complete their reporting obligations as usual.

While an ADI will no longer need APRA approval to use the word bank, an ADI that intends to change its corporate or business name should notify its responsible supervisor of such changes.

On Tuesday, the Australian Prudential Regulation Authority (APRA) released the results of its prudential inquiry into Commonwealth Bank of Australia, which cited its concerns about the bank’s management of non-financial risks and made recommendations to address those issues. APRA also will apply a capital adjustment by adding AUD1 billion to CBA’s operational risk capital requirement until it is satisfied that CBA has addressed the recommendations. APRA’s inquiry results are credit negative for CBA because it exposes the bank to reputational damage and costs associated with addressing its shortcomings. Additionally, the capital adjustment will lower CBA’s Common Equity Tier 1 ratio to a pro forma 10.1% as of year-end 2017 from an actual 10.4%.

APRA’s report noted that CBA’s continued financial success negatively affected the bank’s ability to manage its operational, compliance and conduct risks. In particular, the report highlighted the board and its committees’ inadequate oversight of emerging non-financial risks; unclear accountabilities, starting with a lack of ownership of key risks; weaknesses in how issues, incidents and risks were identified and escalated and overly complex and bureaucratic decision-making processes. The report cited an operational risk-management framework that worked better on paper than in practice, supported by an immature and under-resourced compliance function. In addition, APRA criticized the bank’s remuneration framework, which before the prudential inquiry began in August 2017, had few consequences for senior management for poor risk management and compliance performance.

The report made 35 recommendations to strengthen the bank’s governance, accountability and culture, and gave the bank 60 days to provide a remedial action plan to APRA. An independent reviewer will be appointed to provide quarterly updates to APRA on CBA’s progress. The recommendations are focused on five key areas: more rigorous board- and executive-committee-level governance of non-financial risks; exacting accountability standards reinforced by remuneration practices; a substantial upgrade of the authority and capability of the operational risk management and compliance functions; questioning the appropriateness of all dealings with and decisions on customers; and cultural changes that aim for best practices in risk identification and remediation.

APRA began the inquiry after a number of incidents that have negatively affected the bank’s reputation. In August 2017, the Australian Transaction Reports and Analysis Centre began proceedings against CBA for non-compliance of the Anti-Money Laundering and Counter-Terrorism Financing Act. The same month, the Australian Securities and Investments Commission (ASIC) announced that CBA would refund more than 65,000 customers a total of approximately AUD10 million after selling them unsuitable consumer credit insurance. In March 2016, the bank’s life insurance business, CommInsure, was accused of deliberately avoiding or delaying paying claims to its customers (ASIC cleared CommInsure of any breaches of the law in March 2017). In 2014, CBA announced a review into the poor quality of advice and compliance breaches by its financial planning businesses.

The report comes against a backdrop of the ongoing Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry, which has identified conduct and culture challenges at some of Australia’s largest financial institutions. We note that the franchise dominance of Australia’s major banks and their exceptionally low credit costs during an extended period of low interest rates may have elevated the risk of complacency in their approach to operational and governance risks.

Within that, owner occupied loans rose 0.52% in the month to $1.08 trillion, up $5.5 billion while investment lending rose just 0.13% to $555 billion, up $712 million. Or in annualised terms, owner occupied loans are growing at 6.2% while investment loans are growing at 1.5%. Investment loans now make up 34.06% of all loans, which is still very high but falling.

Within that, owner occupied loans rose 0.52% in the month to $1.08 trillion, up $5.5 billion while investment lending rose just 0.13% to $555 billion, up $712 million. Or in annualised terms, owner occupied loans are growing at 6.2% while investment loans are growing at 1.5%. Investment loans now make up 34.06% of all loans, which is still very high but falling.

Later we will get the RBA numbers, and we will see what the total market trends look like. We suspect non-banks will be growing faster than ADIs.

Later we will get the RBA numbers, and we will see what the total market trends look like. We suspect non-banks will be growing faster than ADIs.