Commonwealth Bank (CBA) announces it has reached an in-principle agreement with the Australian Securities and Investments Commission (ASIC) to settle the legal proceedings in relation to claims of manipulation of the Bank Bill Swap Rate (BBSW).

As part of the in-principle settlement, CBA will acknowledge that, in the course of trading on the BBSW market in Australia on five occasions between February and June 2012, CBA attempted to engage in unconscionable conduct in breach of the ASIC Act. CBA will also acknowledge it did not have adequate policies and systems in place to monitor the trading and communications of its staff in order to prevent that conduct from occurring.

Subject to Federal Court approval of the settlement, CBA has agreed to pay a $5 million penalty, a payment of $15 million to a financial consumer protection fund and a $5 million payment towards ASIC’s costs of the litigation and its investigation. The impact of this settlement will be reflected in CBA’s 2018 Financial Year results.

CBA has also agreed to enter into an enforceable undertaking with ASIC, under which an independent expert will be appointed to review controls, policies, training and monitoring in relation to its BBSW business.

CBA and ASIC will make an application to the Federal Court for approval of the settlement

ASIC has welcomed the authorisation by the Minister for Revenue and Financial Services of the operator of the new single external dispute resolution (EDR) scheme for consumer and small business complaints: the Australian Financial Complaints Authority (AFCA).

AFCA will be able to deal with complaints about financial firms including banks, credit providers, insurance companies and brokers, financial advisers, managed investment schemes and superannuation trustees. It will operate significantly higher monetary and compensation limits for consumer and small business complainants, as well as provide enhanced access to free dispute resolution for primary producers. ASIC will oversee the operation of AFCA and receive reports including about systemic issues and serious contraventions by financial firms.

AFCA will replace the two existing ASIC approved EDR schemes – the Financial Ombudsman Scheme (FOS) and the Credit and Investments Ombudsman (CIO) – and the statutory Superannuation Complaints Tribunal (SCT).

Joining AFCA

All financial firms that are required to have a dispute resolution system to deal with complaints from consumers and small businesses must become members of AFCA by 21 September 2018. This includes trustees of regulated superannuation funds who are currently subject to the SCT.

ASIC will work closely with AFCA, FOS, CIO and the SCT to monitor membership compliance to ensure that consumers and small businesses retain effective access to EDR throughout the transition period. Some of the transition arrangements may differ depending on which EDR scheme a firm is currently a member of. This is set out below.

FOS and CIO members

FOS and CIO are making arrangements to transition to the new authorised operator: AFC Limited, which will then operate FOS and CIO until all outstanding complaints are finalised.

Existing members of FOS and CIO must become members of AFCA by 21 September 2018. They must also retain their existing membership of the FOS or CIO scheme until further notice.

Consumers will be able to lodge complaints with FOS and CIO up to and including 31 October 2018. AFCA then commences on 1 November 2018 and from that date complaints can be lodged with it. Complaints made to the FOS and CIO schemes before 1 November 2018 and which remain unresolved at that date will be dealt with by AFCA under the Rules/Terms of Reference that applied when the complaint was originally made.

Financial firm members must keep paying fees to the FOS and CIO schemes as and when they fall due.

If any FOS or CIO member has any questions about the transition to the new AFCA scheme or about their ongoing membership obligations, they should contact their current scheme for information in the first instance.

Superannuation trustees

Superannuation members and other eligible complainants will be able to lodge complaints with the SCT up to and including 31 October 2018.

The SCT will continue to operate beyond 1 November 2018 to resolve the complaints it has on hand at that date. Superannuation trustees will need to continue to deal with any existing complaints they have with the SCT.

Superannuation trustees will also need to ensure that they have joined the AFCA scheme by 21 September 2018. Superannuation trustees will then deal with the AFCA scheme in relation to complaints lodged with it on or after 1 November 2018.

Complaints that have been lodged with the SCT before 1 November 2018 will not be able to be transferred to AFCA.

The Treasury has put together a fact sheet to assist people who have already lodged a complaint with SCT, or who are thinking about making a complaint in the future. The fact sheet may be accessed here

ASIC recently consulted on changes to its policy guidance about oversight of AFCA. As part of this process ASIC sought feedback about the need for disclosure relief for financial firms in relation to the EDR changes. We will announce our position on this soon.

The chairwoman and CEO of AMP have resigned after the company admitted to charging for advice never provided and lying to clients and regulators. But no banking CEOs have been toppled despite the Financial Services Royal Commission unearthing instances of fraud, bribery, impersonating customers, failures to report misconduct to regulators and other poor behaviour.

Similar conduct in the United States has resulted in bank executives and directors being forced to resign. That this is not happening in Australia shows how the Australian Securities and Investments Commission (ASIC) and the Australian Prudential Regulation Authority (APRA) aren’t using their full powers to take action on the banks’ bad behaviour.

APRA already has the power under the Banking Act to remove someone from a bank board and install its own nominee. The recently enacted Banking Executive Accountability Regime has given APRA more power to remove directors and install new ones.

So ASIC and APRA are not bedevilled by a lack of power, but by a lack of willpower.

In 1998 the Wallis Inquiry hived off the consumer protection and market conduct functions from the Australian Competition and Consumer Commission (ACCC) and gave these to ASIC. Professor Ian Harper, a member of the inquiry, now concedes that may have been an error.

The ACCC is an excellent regulator, with a long history of being a tough cop. Handing the consumer protection and market conduct function back to the ACCC is a step that federal Treasurer Scott Morrison should take now.

Indeed, Matt Comyn, who was responsible for this division from 2012 onwards, has been promoted to Commonwealth Bank CEO. Former CEO Ian Narev has been permitted to sail off into the sunset with bonuses intact.

Despite United States authorities being widely regarded as weak in standing up to their banks, American CEOs are being held accountable.

Take the example of John Stumpf, chairman and CEO of Wells Fargo, the biggest retail bank in the US. Under his direction Wells Fargo staff had been opening multiple accounts for clients, with neither their knowledge nor their consent, and then charged account-keeping fees.

No one is suggesting Stumpf knew about the fraud, or that Comyn knew that CBA was charging fees for advice to dead people. But Stumpf’s misstep caused his departure. Why is no one suggesting Comyn must go?

This is the true state of the Australian financial sector: bank executives and CEOs who could be facing criminal charges, and should have resigned, don’t even acknowledge the buck stops with them.

Regulatory failure

And if there is any doubt about the need to get cracking, here is the knockout blow: UBS has downgraded Westpac shares because the royal commission revealed that the percentage of “liar loans” in the bank’s A$400 billion loan book may be much higher than stated, or even than Westpac itself is aware of.

This is the culmination of ten years of cowboy behaviour in a financial system that now resembles the Wild West.

This is what happens when compliance culture breaks down, which in turn is a function of regulatory oversight and enforcement. Put differently, our regulators have failed to act for so long that the problem is assuming systemic proportions.

What will be interesting to see is whether the APRA inquiry is another whitewash. I half suspect that if it failed to excoriate CBA it would look pretty silly.

Let’s hope the panellists understand that. But if they don’t, then they must be called out.

Author: Andrew Schmulow, Senior Lecturer, Faculty of Law, University of Western Australia

The Royal Commission into Financial Services Misconduct has now uncovered evidence of poor industry practice from both the lending camp, including from mortgage brokers, and the financial advice camp. In both cases their forensic analysis revealed cases of consumers being put in the wrong products, charged for services they never received and on fee structures which were hardly transparent.

In addition, some advisers and brokers were restricted by the product portfolios available via their organisations, and ties back to the big banks and other large players were often not adequately disclosed.

But here’s the thing. There are two distinct flavours of regulation in play, despite both being within ASIC’s bailiwick. I believe it is time to move to a unified common set of regulatory standards to cover both credit and wealth domains.

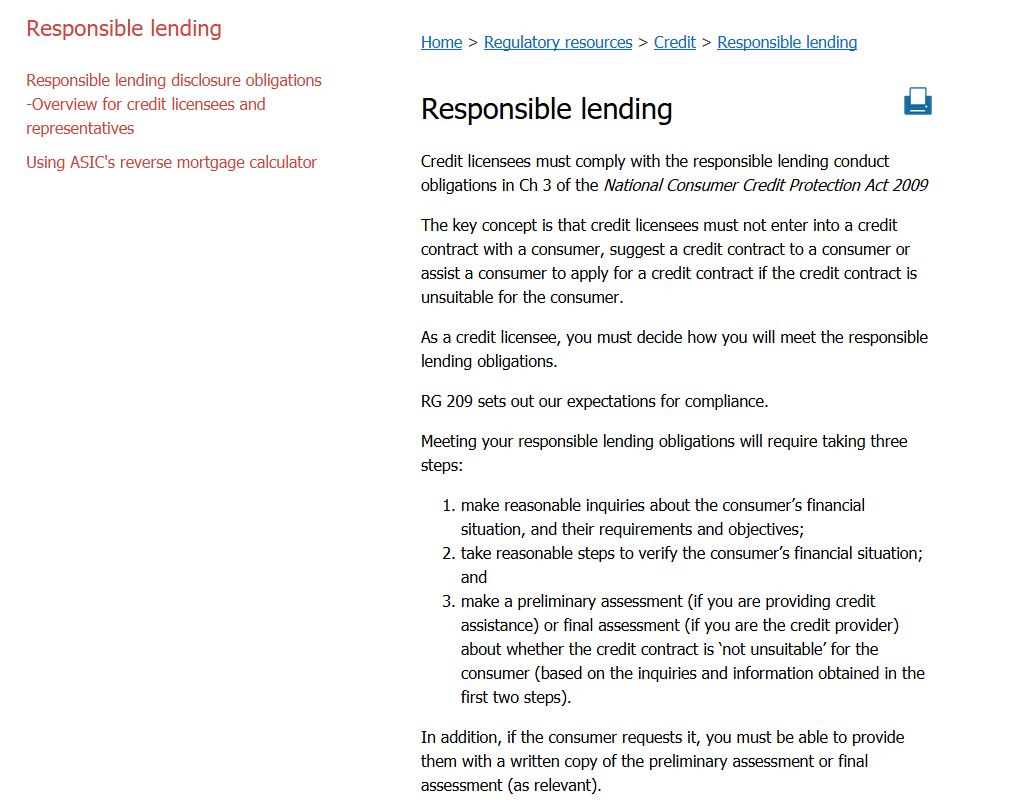

Lending and credit are based on ASIC’s regulations for responsible lending, which requires both a lender, and intermediary – like a broker – to ensure the loan is “not unsuitable”.

This looking at the purpose of the loan, making an assessment of the ability of the consumer to repay, and ensuring it is fit for purpose. What warrants as appropriate steps depends on the nature of the transaction and og the individual capabilities of the customers involved, so it is “scalable”. But that said, they are not obliged to act in the best interests of their client, and fee disclosure is at best rudimentary. Trailing commissions for example are not disclosed. The precise meaning and definition of what is suitable is still subject to case law. But overall, this is weak protection, and as we have seen from the Commission has failed to protect many borrowers. There is nothing here about the best or most appropriate product and it does not include any reference to whole of market analysis. Just, at best “Not Unsuitable”.

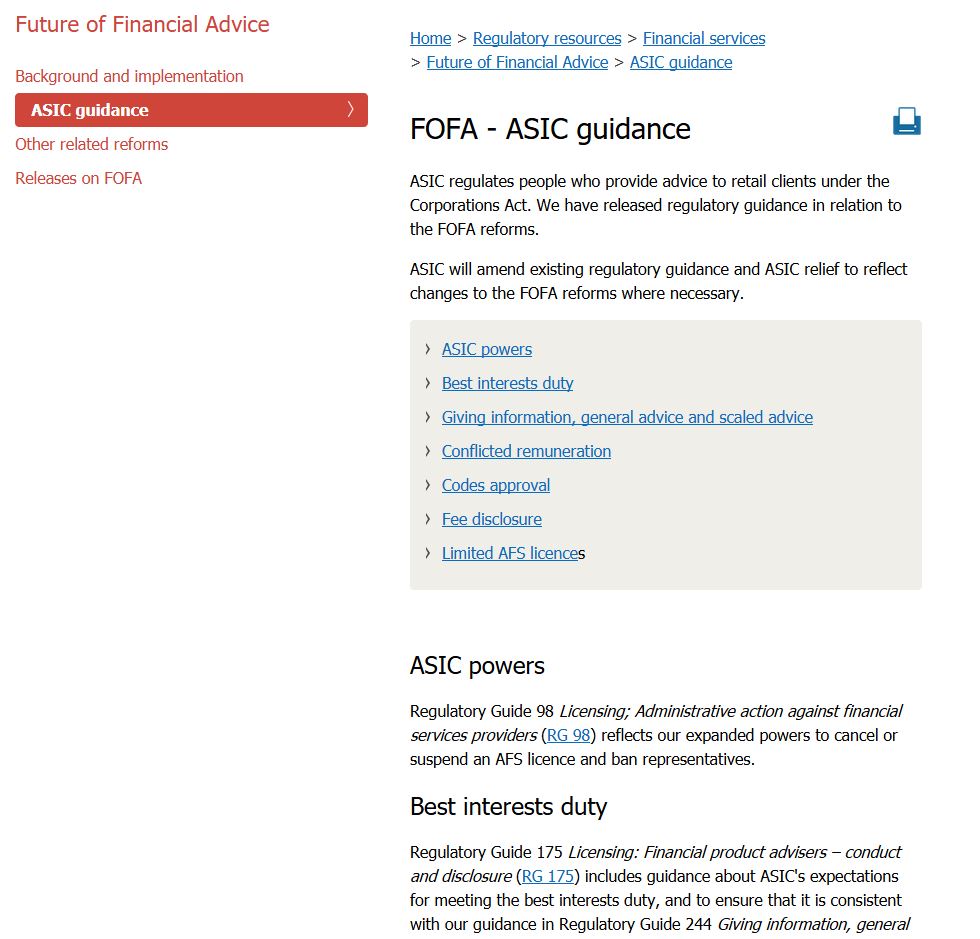

On the financial advice side of the house, as is being explored by the Commission currently, under the FOFA rules, advisers must work in the best interests of their clients, disclose remuneration, and their relationship with product manufacturers if appropriate.

This is a whole different set of rules, again regulated by ASIC. Note again, this does not include finding the best product, or providing whole of market advice. So the rules are slightly stronger, but still incomplete.

Now consider this scenario. I am a property investor who is seeking a mortgage as part of a strategy to build wealth. I will need a life insurance policy also. Who do I talk to? A mortgage broker can assist me with finding a mortgage, but cannot help with life insurance. But if I go and talk to a financial adviser unless they are also a mortgage broker, they cannot assist with the mortgage. And if I find an adviser qualified in both regimes, which rules do they work under?

And that’s the point. The regulations, which by the way are an accident of history in that the responsible lending laws evolved from earlier state legislation, get in the way of providing holistic unified advice. A consumer has both credit AND other wealth management requirements as part of a single issue. Indeed, there are trade-offs, for example between holding more or less investment properties, versus investing in other market related investment products. Indeed, it is feasible to wrap property investments into an overall wealth strategy.

So I suggest that now is the time to create a new unified set of rules to apply to all financial advisers, whether they are advising on credit or wealth products. They should be crafted around best interests of their clients, and should mean offering whole of market advice. That means creating an advice plan which spans both investments and lending. The plan should be based on a fee for service, and the advisers’ remuneration should not be in any way linked to a commission or revenue flow from the products they suggest.

Indeed, we should break apart the advice element from the product sale, and application. I suggest that individual product application could be completed by the adviser as part of a fee for service, but they should not receive any additional remuneration related to successful product sales.

This also has implications for ASIC, as it would reshape the advice landscape, but potentially could both simplify the regulatory regime, and strengthen the protection for customers, and help facilitate better customer outcomes. Down the track, advisers would require one set of qualifications, and would be become more recognised professionals.

I believe the current chaotic regulatory environments, which were crafted to appease the finance industry, are in appropriate and the time has come to create a single unified set of regulations. This would assist customers, but would also help the industry on its journey towards professionalism.

In a statement issued today, Treasurer Scott Morrison said the reform will represent the “most significant increases in maximum civil penalties in twenty years”.

These increases are right, as before the financial impact of poor behaviour was very low However, do not be misled, changing penalties will not address the fundamental cultural, structural and economic issues which have combined to deliver a finance sector which is simply not fit for purpose.

We need a removal of incentives from the advice sector (mortgage brokers included). Actually we need unified regulation across credit and wealth sectors (the current two regimes are an accident of history).

We need structural separate and disaggregation of our financial conglomerates. We need a realignment of interests to focus on the customer – which by the way is not at odds with shareholder returns, as customer focus builds franchise value and returns in the long term.

We need cultural reform and new values from our finance sector leaders. (Executive Pay should come under the spot light).

We need a reform of the regulatory structure in Australia, because they are captured at the moment at least by group think, and their interests are aligned too closely to the finance sector. This must include ASIC, APRA, RBA and ACCC. All have bits of the finance puzzle, but no one is seriously accountable.

But there is a more fundamental issue. We have relied on overblown credit, and superannuation sectors, as a proxy for high quality economic growth. This inflated housing and lifted household debt.

We need a fundamental economic reset, because reforming financial services alone won’t solve our underlying issues.

Here are the changes:

The government will increase penalties under the Corporations Act to:

“For individuals: (i) 10 years’ imprisonment; and/or (ii) the larger of $945,000 OR three times the benefits;

For corporations: (i) the larger of $9.45 million OR (ii) three times benefits OR 10% of annual turnover.

“The Government will expand the range of contraventions subject to civil penalties, and also increase the maximum civil penalty amounts that can be imposed by courts, to the maximum of:

the greater of $1.05 million (for individuals, from $200,000) and $10.5 million (for corporations, from $1 million); or

three times the benefit gained or loss avoided; or

10% of the annual turnover (for corporations).

“In addition, ASIC will be able to seek additional remedies to strip wrongdoers of profits illegally obtained, or losses avoided from contraventions resulting in civil penalty proceedings.”

ASIC says it has has accepted an enforceable undertaking (EU) from Commonwealth Financial Planning Limited (CFPL) and BW Financial Advice Limited (BWFA), both wholly owned subsidiaries of the Commonwealth Bank of Australia (CBA).

ASIC found that CFPL and BWFA failed to provide, or failed to locate evidence regarding the provision of, annual reviews to approximately 31,500 ‘Ongoing Service’ customers in the period from July 2007 to June 2015 (for CFPL) and from November 2010 to June 2015 (for BWFA).

The EU requires, among other things:

CFPL and BWFA to pay a community benefit payment of $3 million in total;

CFPL to provide an attestation from senior management setting out the material changes that have been made to CFPL’s compliance systems and processes in response to the misconduct; and

CFPL to provide further attestations from senior management, supported by an expert report, that:

CFPL’s compliance systems and processes are now reasonably adequate to track CFPL’s contractual obligations to its Ongoing Service clients; and

CFPL has taken reasonable steps to identify and remediate its Ongoing Service customers to whom CFPL did not provide annual reviews in the period from July 2015 to January 2018.

As BWFA ceased trading in October 2016, CFPL is the focus of the compliance improvements required under the EU.

ASIC Deputy Chair Peter Kell said, ‘Our report into Fees For No Service in October 2016 identified the major financial institutions’ systemic failures in this area, and called for fair compensation to be paid to customers who did not receive the advice reviews that they were promised and paid for.

‘This enforceable undertaking follows on from the earlier enforceable undertaking accepted by ASIC in relation to ANZ’s fees for no service conduct. These failures show that all too often the financial institutions prioritised revenue and fee generation over the delivery of advice and services paid for by their customers.’

In addition to the EU, CFPL and BWFA have also agreed to compensate approximately 31,500 affected customers in the period from July 2007 to June 2015 (for CFPL) and from November 2010 to June 2015 (for BWFA). The compensation program is nearing completion and as at 28 February 2018, CFPL and BWFA have paid or offered to pay approximately $88 million (plus interest) to these customers (with the total compensation estimated at $88.6 million (plus interest)).

Background

The EU follows an ASIC investigation into CFPL and BWFA in relation to their fees for no service conduct concerning various Ongoing Service packages which were offered to CFPL and BWFA financial planning customers for an annual fee. A key component of those packages from about 2004 (for CFPL) and from 2010 (for BWFA) was the provision of an annual review of the customer’s financial plan.

As a result of the investigation, ASIC was concerned that:

CFPL and BWFA either did not provide, or have not identified evidence regarding the provision of, annual reviews to approximately 31,500 Ongoing Service customers who had paid for those reviews;

CFPL and BWFA did not have adequate systems and processes in place for tracking their Ongoing Service customers and ensuring that annual reviews were provided to them;

senior management were aware from at least mid-2012 that a relatively small number of CFPL Ongoing Service customers who were not assigned to an active adviser may not have received an annual review, and that there was a potential risk of a broader ‘fees for no service’ issue in relation to other Ongoing Service customers, but CFPL did not notify ASIC of the issue until July 2014; and

CFPL and BWFA failed to comply with section 912A(1)(a) of the Corporations Act which provides that a financial services licensee must do all things necessary to ensure that the financial services covered by the licence are provided efficiently, honestly and fairly, and a condition of their respective Australian financial services licence.

Both CFPL and BWFA have acknowledged in the EU that ASIC’s concerns were reasonably held.

The EU has been accepted by ASIC as part of ASIC’s Wealth Management Project to address systemic failures by financial institutions and advisers, over a number of years, to provide ongoing advice services to customers who paid fees to receive those services (commonly referred to by ASIC as Fees for No Service conduct). A report on ASIC’s work in this area was released in October 2016 (Report 499), and updated in May 2017 (17-145MR) and December 2017 (17-438MR).

ASIC says it has accepted an enforceable undertaking (EU) from Australia and New Zealand Banking Group Limited (ANZ) after an investigation found that ANZ had failed to provide documented annual reviews to more than 10,000 ‘Prime Access’ customers in the period from 2006 to 2013.

The EU requires ANZ, among other things, to:

pay a community benefit payment totalling $3 million

provide an audited attestation from ANZ senior management to provide ‘reasonable assurance’ that the bank has, since 2014, provided documented annual reviews to customers who were entitled to such reviews, and

provide further audited attestations from ANZ senior management as to the improvements that the bank has made to its compliance systems and processes, and that the design and implementation of those systems and processes will seek to ensure documented annual reviews are provided in accordance with the ANZ Prime Access package.

ASIC Deputy Chair Peter Kell said, ‘Our report into Fees For No Service in October 2016 identified the major financial institutions’ systemic failures in this area, which required affected customers to be fairly compensated and to be provided with the services that they have paid for.

‘ASIC considered it critically important that improved systems and procedures be put in place to ensure this breach of trust could not re-occur. This enforceable undertaking with ANZ will deliver on that commitment,’ he said.

In addition to the EU, ANZ has also agreed to compensate its Prime Access customers who, in the period from 2006 to 2013, did not receive the documented annual reviews that they were entitled to. The compensation program is nearing completion and as at 28 February 2018, ANZ has paid $46.81 million (including earnings) in compensation to these customers (with the total compensation estimated at $46.85 million).

Background

The EU follows an ASIC investigation into ANZ in relation to ANZ’s fees for no service conduct concerning the Prime Access service package which was offered to ANZ’s financial planning customers for an annual fee from 2003. A key component of the package was the provision of a documented annual review of the customer’s financial plan.

As a result of the investigation, ASIC was concerned that:

ANZ had failed to provide documented annual reviews to more than 10,000 Prime Access’ customers who had paid for those reviews

ANZ did not have adequate systems and processes in place to ensure that the ‘Prime Access Service, including the provision of documented annual reviews, was provided to Prime Access customers

from as early as 2008, ANZ Financial Planning was aware of a number of confirmed instances in which documented annual reviews had not been provided to Prime Access customers, and that there was a risk of a broader issue in relation to further Prime Access customers not being provided with documented annual reviews, but the conduct continued until 2013, and ANZ did not breach report the conduct to ASIC until August 2013, and

ANZ failed to comply with section 912A(1)(a) of the Corporations Act which provides that a financial services licensee must do all things necessary to ensure that the financial services covered by the licence are provided efficiently, honestly and fairly and a condition of its Australian Financial Services Licence.

ANZ acknowledged in the EU that ASIC’s concerns were reasonably held.

In ASIC’s post-draft submission to the Productivity Commission’s Inquiry into competition in the Australian financial system, the corporate regulator said it “support[ed] the Productivity Commission’s recognition of the importance of ASIC having a broad, proactive competition mandate”.

“An explicit and broad competition mandate for ASIC would ensure we have a clear basis to consider and promote competition in the financial system,” ASIC’s submission report said.

ASIC also acknowledged previous instances of “uncertainty” regarding “if and how ASIC could consider competition factors”, but pushed back against the idea of actually regulating competition.

“Having a broad competition mandate – to ensure we can appropriately incorporate competition considerations into our existing role as a market conduct regulator – would not make ASIC a competition regulator,” the submission report said.

“We would not have a role in enforcing competition laws – for example, regulating corporate transactions from a competition perspective or monopolies, bringing abuse of market power cases, or regulating pricing and access regimes.”

The regulator added that it supported the co-operation of different regulators in tackling competition issues and the value of learning from each other.

However, ASIC pointed out that each regulator had its own specified area of expertise and “therefore best placed to assess how competition should be weighed and balanced within its area”.

“While we appreciate the Productivity Commission’s concern to ensure that all regulators give appropriate consideration to the competition impacts of their decisions, we are not sure that the role of the competition champion, as envisioned in the draft report, is necessarily the best option to achieve that goal,” the submission report said.

Furthermore, ASIC highlighted the “significant role” of the Australian Competition and Consumer Commission as a regulator of competition “for the entire economy”, as well as its role as a “competition advocate”.

“We acknowledge and support the ACCC’s establishment of its Financial Services Unit, and the role it plays in the financial sector,” the submission report said.

“ASIC maintains a strong working relationship with the ACCC, and welcomes the ACCC’s views and input, including in our work to encourage positive consumer outcomes through effective competition.”

ASIC has today released a report setting out the details of the changes made by the big four banks to remove unfair terms from their small business loan contracts of up to $1 million.

The report, Unfair contract terms and small business loans (REP 565), provides more detailed guidance to bank and non-bank lenders about compliance with the unfair contract terms laws as they relate to small business.

The report follows the announcement in August 2017 that the big four banks had committed to improving terms of their small business loans following work with ASIC and the Australian Small Business and Family Enterprise Ombudsman (ASBFEO). (See 17-287MR).

ASIC Deputy Chair Peter Kell said, ‘The UCT report provides further guidance to help banks and other lenders ensure that their small business loans are fair, and do not breach the rules prohibiting unfair contract terms.’

The report:

Identifies the types of terms in loan contracts that raise concerns under the law

Provides details about the specific changes that have been made by the banks to ensure compliance with the law

Provides general guidance to lenders with small business borrowers to help them assess whether loan contracts meet the requirements under the unfair contract terms law

‘ASIC will review small business lending contracts across the market. There are no excuses for failure to comply with the UCT laws, and we will consider all regulatory options available to us if we identify lenders whose unfair contracts break the law.’

ASIC will monitor the four banks’ use of the clauses to ensure they are not applied or relied on in an unfair way. ASIC will also examine other lenders’ loan contracts to ensure that their contracts do not contain terms that raise concerns under the unfair contract terms law.

ASIC and ASBFEO will continue work together to ensure small business loan contracts comply with the unfair contract terms law.

Unfair contract terms protections were extended to small business from 12 November 2016.

ASIC and the ASBFEO have been working with the big four banks to ensure their small business loan contracts meet the standards that are required by the unfair contract terms law (refer: 17-139MR).

Small business loans are defined as loans of up to $1 million that are provided in standard form contracts to small businesses employing fewer than 20 staff are covered by the legal protections.

In August 2017, ASIC and the ASBFEO welcomed the changes to small business loan contracts by the big four banks (refer 17-278MR) that have:

Ensured that the contract does not contain ‘entire agreement clauses’ which prevent a small business borrower from relying on statements by bank officers (e.g. about how bank discretions will be exercised)

Limited the operation of broad indemnification clauses

Addressed concerns about event of default clauses, including ‘material adverse change’ events of default and specific events of non-monetary default (e.g. misrepresentations by the borrower)

Limited the circumstances in which financial indicator covenants will be used in small business loans and when breach of a covenant will be considered an event of default

Limited their ability to unilaterally vary contracts to specific circumstances with appropriate advance notice.

As part of the in-principle settlement, CBA will acknowledge that, in the course of trading on the BBSW market in Australia on five occasions between February and June 2012, CBA attempted to engage in unconscionable conduct in breach of the ASIC Act. CBA will also acknowledge it did not have adequate policies and systems in place to monitor the trading and communications of its staff in order to prevent that conduct from occurring.

As part of the in-principle settlement, CBA will acknowledge that, in the course of trading on the BBSW market in Australia on five occasions between February and June 2012, CBA attempted to engage in unconscionable conduct in breach of the ASIC Act. CBA will also acknowledge it did not have adequate policies and systems in place to monitor the trading and communications of its staff in order to prevent that conduct from occurring.