I caught up with Steve from Canstar to discuss the latest mortgage rate moves, and how this is playing out across households and banks. With the expectation that rates might well go higher still, what can be done?

On 4 March, the Federal Reserve Board (Fed) finalized changes to its capital rules for US banks with assets greater than $100 billion. Via Moody’s.

The final changes increase the flexibility banks have to payout capital more aggressively and will likely give bank management greater leeway to reduce the size of their management buffers and operate with capital ratios closer to the minimum levels required.

The final version establishes a stress capital buffer (SCB) that incorporates the Fed’s stress test results into its regulatory Pillar 1 capital requirements for these banks. Originally proposed in April 2018, the final rule includes a number of changes that weaken the original, making it credit negative for all US banks covered by the rule.

The Fed’s impact analysis of the final rule suggests that in aggregate the Common Equity Tier 1 (CET1) capital requirements at the affected US banks could decline up to $59 billion: $6 billion at the eight US global systemically important banks (G-SIBs) and $35 billion at the rest. Since most banks currently hold a management buffer above existing requirements, the affected banks could actually cut their CET1 capital by twice this amount and still comply with the final rule. The CET1 capital reduction could be $40 billion (a 5% decline) at the G-SIBs, $50 billion (a 21% decline) at other banks with $250 billion or more in assets, and $35 billion (a 16% decline) at banks with assets between $100 and $250 billion.

Consistent with the proposal, the final rule integrates stress testing into the Fed’s regulatory capital requirements by replacing the capital conservation buffer, which is currently 2.5%, with the SCB. The SCB will be the higher of either 2.5%, or the difference between the starting and minimum projected CET1 capital ratio under the severely adverse scenario of the Fed’s Dodd-Frank Act Stress Test (DFAST) plus four quarters of planned common stock dividends.

Starting in October 2020, if a bank’s risk-based capital ratios fall below the aggregate of the minimum capital requirement plus the SCB, the relevant G-SIB surcharge, and the countercyclical capital buffer (if any), restrictions would apply to capital payouts and certain discretionary bonus payments. As in the proposal, the final rule changes the current annual Comprehensive Capital Analysis and Review (CCAR) and DFAST process.

The final rule eliminates the assumption that a bank’s balance sheet and risk-weighted assets will grow under the stress scenarios, eliminates the Fed ability to object on quantitative grounds to a bank’s capital plan, and removes the 30% dividend payout ratio as a threshold for heightened scrutiny of a bank’s capital plan. Both the flat balance sheet assumption and the requirement that banks hold capital for only four quarters of dividends rather than for the full amount of planned payouts over the stress test horizon lower capital requirements versus the current stress testing regime.

The decrease is only partially offset for G-SIBs by the first-time inclusion of the G-SIB surcharge within the Fed’s stress test.

The final rule is weaker than the original proposal for several reasons. Under the proposal, banks would not have been allowed to pay out capital in excess of their approved capital plans without Fed prior approval. In the final rule, banks can in most cases make payouts in excess of amounts in their capital plan, provided the payout is otherwise consistent with the payout limitations in the final rule.

Additionally, the final rule modifies payout limitations to allow firms with an SCB in excess of 2.5% to pay a greater portion of their dividends and management bonuses and to repurchase shares for a period of time after capital ratios fall below the requirement. And in the final rule, the SCB, unlike the DFAST capital requirements, will not incorporate material business plan changes, such as those resulting from a merger or acquisition. As a result, such actions will only affect a bank’s capital ratio once the action has occurred.

The final rule also excludes the originally proposed stress leverage buffer requirement, which would not have been a binding constraint for most banks. Its elimination from the final rule removes this requirement as a potential backstop. And without the stress leverage buffer, the still pending proposal to modify the supplementary leverage ratio for the eight G-SIBs by tying it more closely to the G-SIB surcharge could further weaken the ability of the leverage ratio to serve as a backstop requirement and would also be credit negative.

The Australian Prudential Regulation Authority (APRA) has released a strengthened prudential standard aimed at mitigating contagion risk within banking groups. The new rules will come in from 1 January 2021. Until then the 100 or so such operations within a small number of ADIs will remain obscured, with potential higher risks exposure in a down turn.

Such complex group structures could potentially make it difficult for APRA to resolve an ADI quickly and protect depositors’ savings in the unlikely event of a bank failure.

The updated Prudential Standard APS 222 Associations with Related Entities (APS 222) will further reduce the risk of problems in one part of a corporate group having a detrimental impact on an authorised deposit-taking institution (ADI).

Deputy Chair John Lonsdale said APRA began consulting last July on proposed changes to APS 222 to incorporate some of the lessons learned from the global financial crisis.

“Concessions in the existing framework led to some ADIs establishing operations in foreign jurisdictions, which are managed and funded within the domestic bank.

“APRA has only limited visibility of these operations, which also fall outside the purview of foreign regulators. They complicate operating structures and there is no certainty their assets would be available to an ADI if it were to enter resolution. There are currently around 100 such operations within a small number of ADIs.

“Additionally, if an ADI were to fully utilise some of the limits within the existing framework, they would be exposed to excessive levels of contagion risk,” Mr Lonsdale said.

APRA received submissions from 10 stakeholders to its consultation; most supported updating the requirements, however some raised concerns about the complexity of implementing certain proposed changes.

Responding to the consultation, APRA confirmed that APS 222 will be updated to include:

a broader definition of related entities that includes board directors and substantial shareholders;

revised limits on the extent to which ADIs can be exposed to related entities;

minimum requirements for ADIs to assess contagion risk; and

removing the eligibility of ADIs’ overseas subsidiaries to be regulated under APRA’s Extended Licensed Entity framework.

Additionally, APRA will require ADIs to

regularly assess and report on their exposure to step-in risk – the likelihood

that they may need to “step in” to support an entity to which they are not

directly related.

Mr Lonsdale said the stronger APS 222 will enhance the prudential safety of

ADIs and reinforce financial system stability.

“As we saw during the global financial crisis, deficiencies in governance or

internal controls in one part of a corporate group can quickly spread and cause

financial or reputational damage to an ADI. Furthermore, complex group

structures could potentially make it difficult for APRA to resolve an ADI

quickly and protect depositors’ savings in the unlikely event of a bank

failure.

“By updating and strengthening the requirements of APS 222, APRA will ensure

ADIs are better able to monitor, manage and control contagion risk within their

organisations.

“While aspects of the revised standard will have a material impact on some

ADIs, we have adjusted our original proposals in some areas to make the

requirements less burdensome. We are open to considering appropriate transition

arrangements on a case-by-case basis where specific entities request it,” Mr

Lonsdale said.

The new APS 222 will come into effect from 1 January 2021.

APRA’s report released today highlights the gaps which still exist across our financial firms, following the CBA analysis. Worryingly, despite firms’ boards and management teams being aware of the risk and accountability deficits which exist, some are not addressing them appropriately. Indeed, in some organsiations, there is still limited visibility of potential non-financial risks.

The Final Report of the Prudential Inquiry into the CBA found that continued financial success dulled the institution’s senses to signals that might have otherwise alerted the Board and senior executives to a deterioration in the bank’s risk profile. This was particularly evident in relation to the management of non-financial risks.

The Prudential Inquiry also found a number of prominent cultural themes; there was a widespread sense of complacency, a reactive stance in dealing with risks, insularity and not learning from experiences and mistakes, and an overly collegial and collaborative working environment that lessened constructive criticism, timely decision-making and a focus on outcomes.

The Final Report listed 35 recommendations focussing on five key levers of change:

more rigorous board and executive committee governance of non-financial risks;

exacting accountability standards reinforced by remuneration practices;

a substantial upgrading of the authority and capability of the operational risk management and compliance functions;

injection of the “should we” question in relation to all dealings with and decisions on customers; and

cultural change that moves the dial from reactive and complacent to empowered, challenging and striving for best practice in risk identification and remediation.

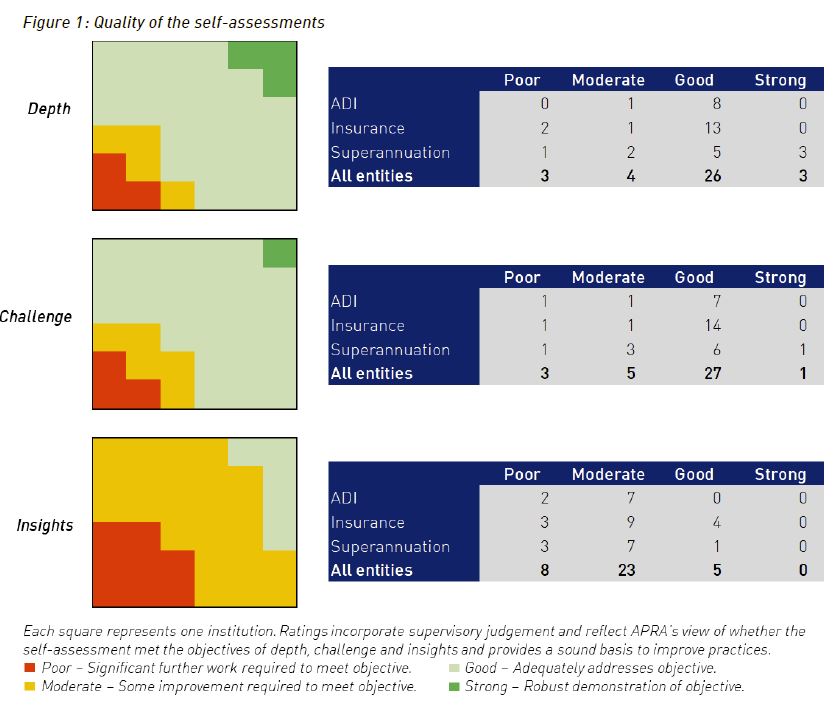

In releasing the Final Report, APRA noted that all regulated financial institutions would benefit from conducting a self-assessment to gauge whether similar issues might exist in their institutions. APRA subsequently wrote to the chairs of 36 institutions requesting a board endorsed written self-assessment of the effectiveness of their own governance, accountability and culture practices. APRA received all of these assessments by mid-December 2018.

APRA’s request for institutions to conduct the self-assessments was intentionally not prescriptive. Boards were asked to determine an approach to the assessment which would provide them with a comprehensive understanding of the effectiveness of governance, accountability and culture, and enable them to form a view as to the extent the ‘tone from the top’ is permeating through and across the institution. As a result, the structure, methodology and format each institution took to completing the self-assessment was considered an important indicator of how seriously boards approached the task.

APRA set three principles that it expected the self-assessments to reflect:

Depth – to enable the board to gain assurance that appropriate governance, accountability and culture are embedded in practices and behaviours, and enforced within the various levels and across the group-wide operations;

Challenge – either independent or self-challenge, to provide the board with fresh perspectives on the strength of governance, accountability and culture (e.g. the assessment should not only reflect the view of the risk function); and

Insights – to inform the board of areas requiring attention and improvement, and how better practice can be achieved.

Emerging themes

While the self-assessments exhibited considerable variation in the number and severity of findings, four themes emerged across all industries:

non-financial risk management requires improvement. This was evidenced through a range of issues identified by institutions, including resource gaps (particularly in the compliance function), blurred roles and responsibilities for risk, and insufficient monitoring and oversight. Institutions acknowledged that historical underinvestment in risk management systems and tools has also contributed to ineffective controls and processes.

accountabilities are not always clear, cascaded, and effectively enforced. Institutions noted that, while senior executive accountabilities are fairly well defined within frameworks, there is less clarity or common understanding of responsibilities at lower levels, and points of handover where risks, controls and processes cut across divisions. This is further undermined by weaknesses in remuneration frameworks and inconsistent application of consequence management.

acknowledged weaknesses are well known and some have been long-standing. The majority of self-assessment findings were reported to be already known to boards and senior leadership. Nevertheless, some issues have been allowed to persist over time, with competing priorities, resource and funding constraints typically cited as the basis for acceptance of slower progress. It was observed that these issues are often only prioritised when there is regulatory scrutiny or after adverse events.

risk culture is not well understood, and therefore may not be reinforcing the desired behaviours. Institutions are putting considerable effort into assessing risk culture, but many continue to face difficulties in measuring, analysing, and understanding culture (and sub-cultures across the institution). It is therefore unclear if these institutions can accurately determine whether their culture is effectively reinforcing desired behaviours (or identify how it would need to be changed to do so).

While the self-assessments contained some in-depth self-reflection and

acknowledgement by institutions of issues within their organisations,

the assessments relating to the effectiveness of boards and senior

leadership were notably less critical. Many self-assessments noted that

the institution is generally well governed, with a respected and

suitably challenging board, strong executive leadership teams and a good

tone from the top, although at the same time acknowledging weaknesses

spanning most or all chapters of the Final Report. This raises the

question of whether boards and senior management have a potential blind

spot when it comes to assessing their own effectiveness.

Fitch Ratings has affirmed the ratings of Australia’s four major banking groups: Australia and New Zealand Banking Group Limited (ANZ), Commonwealth Bank of Australia (CBA), National Australia Bank Limited (NAB) and Westpac Banking Corporation (WBC). At the same time it has revised the outlook on NAB’s Long-Term Issuer Default Rating to Negative from Stable. The Outlook on CBA’s Long-Term Issuer Default Rating remains Negative, while it is Stable for ANZ and WBC.

The

rating review focuses on the Australian-domiciled entities within each

group and therefore does not encompass their overseas subsidiaries.

NAB

The revision of the rating Outlook to Negative reflects the risk that NAB’s focus on remediating issues and changing culture means its ongoing operations may not receive sufficient management time, resulting in a weakening of NAB’s earnings relative to peers. Management changes may make this task more difficult in the short-term. The affirmation of NAB’s ratings reflects Fitch’s expectation that the bank will maintain its strong company profile in the short-term, which in turn supports its sound financial profile.

The Royal Commission into Misconduct in

the Banking, Superannuation and Financial Services Industry and NAB’s

self-assessment on governance, accountability and culture identified

shortcomings within its management of operational and compliance risks,

culture and governance. These were not aligned to what Fitch had

previously incorporated into its ratings and resulted in a revision to

our score for management and strategy, which also remains on negative

outlook. NAB continues to have robust risk and reporting controls around

other risks, including credit, market and liquidity risk, as reflected

by its conservative underwriting standards and very high degree of

asset-quality stability.

Fitch expects NAB’s asset quality and

loan losses to display a very high degree of stability through business

cycles, but could be more volatile than that of some domestic peers due

to NAB’s greater business and corporate exposure.

Capitalisation

and leverage are maintained with solid buffers over regulatory minimums,

but ratios are at the lower end of those of domestic peers. However,

these are likely to trend towards domestic-peer levels as NAB progresses

towards meeting the Australian Prudential Regulation Authority’s

“unquestionably strong” capital requirements by the 1 January 2020

implementation date. Additional capital requirements should be met in an

orderly fashion given the bank’s strong market position and capital

flexibility, with its capital position likely to be bolstered by the

announced partial conversion of its NAB convertible preference shares

into ordinary equity and slower forecast loan growth. The bank’s

earnings and profitability are moderately variable over economic cycles

and it remains reliant on offshore wholesale funding. Sound liquidity

management provides some offset to this risk.

ANZ

The affirmation of ANZ’s ratings reflects the bank’s strong company profile and simple business model in its home markets of Australia and New Zealand, which support its financial profile. The bank’s strong market share across most products provides a higher degree of pricing power relative to smaller peers and allows it to generate strong and consistent operating returns through the cycle.

Australian

household debt is still high relative to international peers, meaning

households are susceptible to a sharp increase in interest rates or

rising unemployment. The risk of external shocks also remains prominent

in light of the geopolitical environment and potential impact on global

growth. However, none of these scenarios are in Fitch’s base case.

The

ongoing execution of ANZ’s simplification strategy supports the rating,

as it is likely to reduce complexity, provide greater focus on key

markets and improve the bank’s overall risk appetite. The focus on

remediating and rectifying issues identified in various inquiries,

including the royal commission, means there is a risk that the bank’s

ongoing operations do not receive sufficient management focus, resulting

in a weakening of its credit profile.

ANZ’s asset quality is

likely to deteriorate modestly in 2019. Earning pressure should continue

due to more modest loan growth, continued pressure on net-interest

margins, rising funding costs, a probable rise in impairment charges and

further remediation and compliance costs. ANZ maintains solid buffers

over regulatory capital minimums and its common equity Tier 1 (CET1)

capital ratio was the highest of Australia’s major banks as of September

2018. These buffers are likely to trend toward domestic-peer levels as

asset sales are completed and capital returned to shareholders. There is

a reliance on offshore wholesale funding, similar to other Australian

major banks, but liquidity is managed well.

CBA

The affirmation of CBA’s ratings reflects Fitch’s expectation that the bank will maintain its strong company profile in the short-term, which in turn supports its sound financial profile. The Negative Outlook reflects challenges in remediating shortcomings in operational and compliance risk management that contributed to a number of conduct and compliance issues over more than a decade. Management’s focus may be diverted from ongoing operations when rectifying these shortcomings and increased compliance costs might manifest in weaker earnings, particularly in relation to domestic peers.

CBA’s remediation of these

shortcomings is on track, but the process is only at an early stage and

is complex. There have been significant changes in the last two years to

the bank’s management and board, who appear committed to rectifying the

outstanding issues. The group is also in the process of exiting its

life insurance and wealth management operations, which may also distract

management from core operations. Successful completion of the

remediation and asset divestments without a significant erosion of the

bank’s franchise would support the current ratings. The remaining

operations after the asset divestments will focus on traditional banking

operations in Australia and New Zealand.

CBA retains a

market-leading position in Australian retail banking despite these

issues and has invested heavily in technology to combat the looming

threat of digital disruptors. The group continues to maintain

peer-leading profitability, while asset quality is sound and capital has

continued to improve. There is a reliance on offshore wholesale

funding, similar to the other Australian major banks, but liquidity is

managed well.

WBC

WBC’s strong company profile supports its ratings. The bank’s market share provides it with some pricing power relative to smaller peers in Australia and New Zealand and allows it to generate strong and consistent operating returns through the cycle, although in the short-term, we expect these to be affected by a challenging operating environment. In addition, WBC has been less affected by conduct-related issues than its domestic major-bank peers, meaning earnings may come under less pressure than for peers despite weaker system growth prospects. Nevertheless, WBC may still be susceptible to legal action from regulators and customers.

Partly

offsetting the risks from high household debt is WBC’s loan

underwriting, which Fitch believes is conservative in the global

context. WBC has progressively tightened its underwriting for mortgages

and commercial exposures, particularly property development, over recent

years. This was driven in part by the regulator, mainly in relation to

mortgages. The bank’s loan book is highly collateralised and we expect

its asset quality to remain a strength relative to that of international

peers, although loan impairments could rise modestly in 2019 from the

current low levels.

WBC is unlikely to have difficulties to

achieving “unquestionably strong” capital targets set by the regulator

before the 2020 deadline – its CET1 capital ratio was already above the

minimum at end-September 2018. Offshore wholesale funding reliance

remains a weakness relative to many similarly rated international peers,

although satisfactory liquidity management and diversification of

funding helps offset some of this risk.

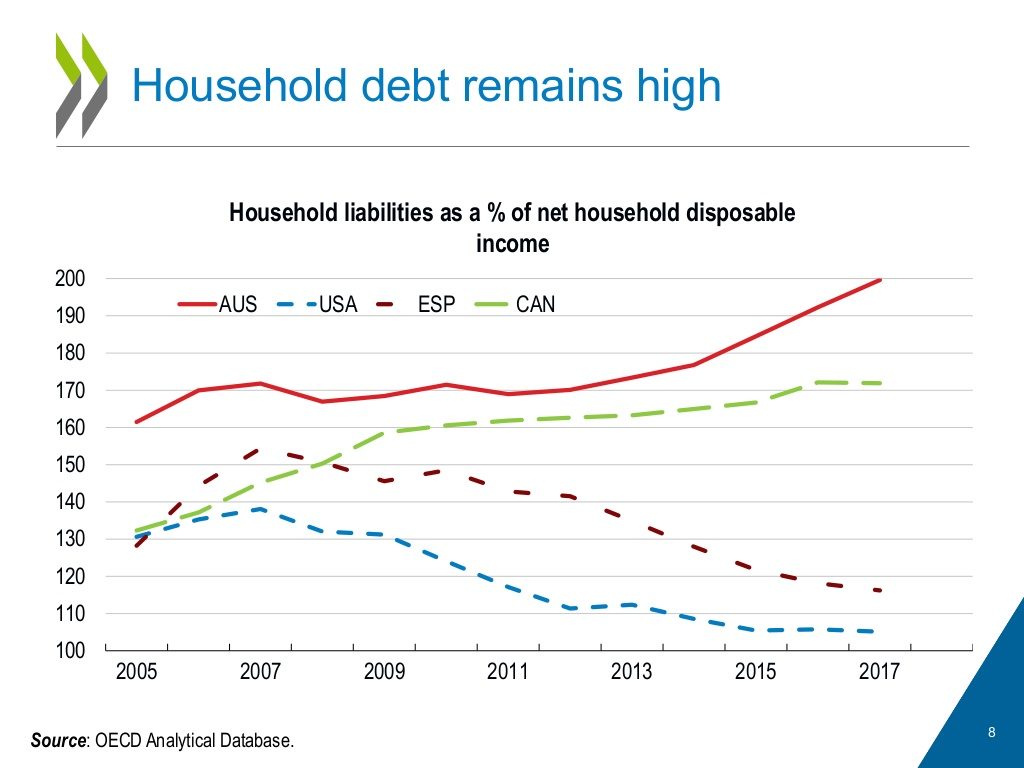

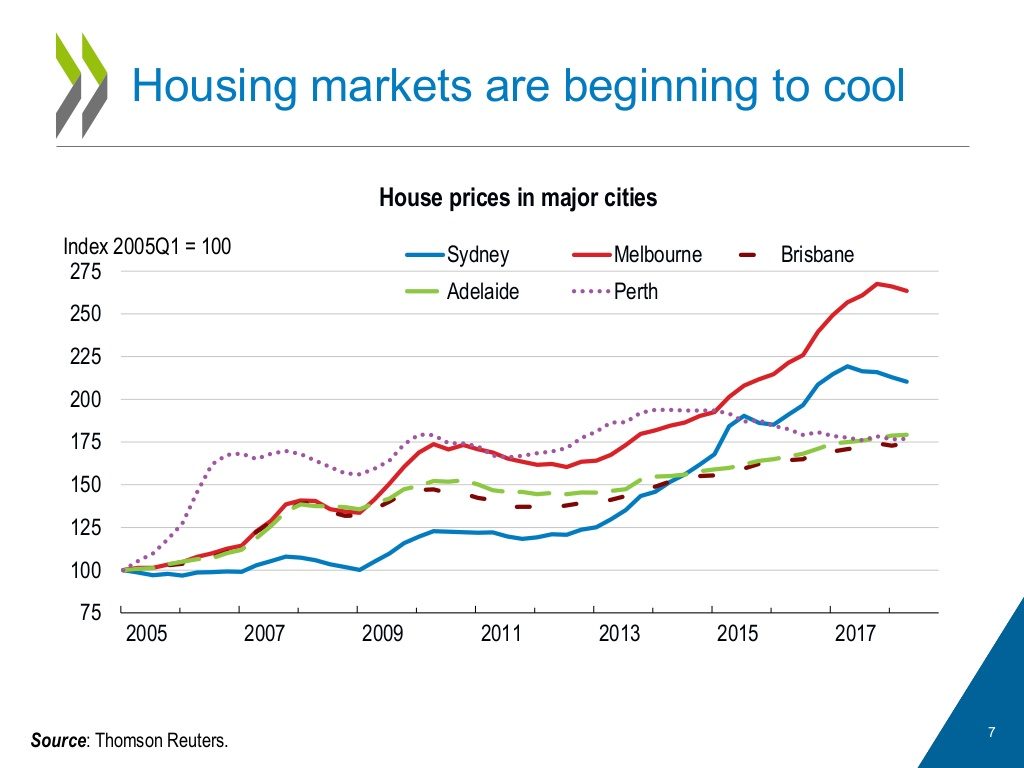

The OECD says Australia’s housing market is a source of vulnerability. Prices have more than doubled in real terms since the early 2000s and household debt has surged. The market has started to cool over the last year, with prices falling most notably in Melbourne and Sydney. So far, data point to a soft landing without substantial consequence for the overall economy. Nevertheless, risk of a hard landing remains.

To date the decrease in house prices has been gradual. Prudential

measures taken by the Australian authorities restricting certain types

of housing credit have played a role. So too has a pick-up in new

housing supply and construction activity remains elevated. Furthermore,

some evidence suggests that Australia’s house prices have not been

hugely overvalued; the IMF has estimated that as of Q3 2017 prices were

above equilibrium by only between 5 and 15% (Heilbling andLi, 2018).

Several features of Australian financing limit the risk of financial

fall-out from a house-price correction. Banks are well capitalised and

their liquidity position is sound. Indebtedness is concentrated in

middle- and high-income households, and data indicate declining

financial stress in recent years, despite rising mortgage debt.

Moreover,many mortgage holders have accumulated substantial buffers of

advance payments(“mortgage prepayments”).

Nevertheless, risk of a macroeconomic downturn from the cooling

housing market remains. Not withstanding the estimates that Australia’s

market is not greatly overvalued, house prices could fall more

substantially. Should this happen, household consumption could weaken.

Households would cut their spending due to lower housing wealth and due

to increased economic uncertainty generated by downturn. Households

would also reduce expenditures related to the purchase, sale and

maintenance of housing (such as spending on renovation and interior

decoration). Sustained decreases in house prices would also weaken

construction activity. Weakened aggregate demand could in turn lead to

losses on loans to businesses, putting stress on the financial sector.

The OECD’s 2018 Economic Survey of Australia

recommends authorities prepare contingency plans for a severe collapse

in the housing market. These should include the possibility of a crisis

situation in one or more financial institutions.

The Financial Stability Board (FSB), the Basel Committee on Banking Supervision (BCBS), the Committee on Payments and Market Infrastructures (CPMI) and the International Organization of Securities Commissions (IOSCO) has published their final report on Incentives to centrally clear over-the-counter (OTC) derivatives.

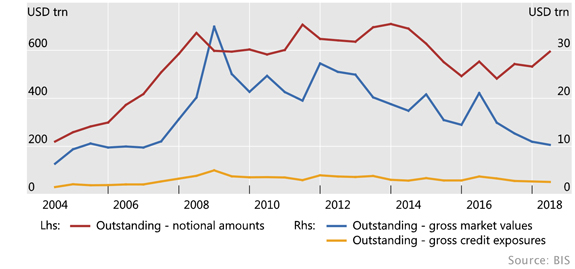

The total value of OTC derivatives was recently reported at US$595 Trillion, a massive number. The approach is been to allow the growth of these instruments, but to encourage central clearing rather than bi-lateral dealer arrangements to give greater visibility to the exposures involved. They propose capital incentives for centrally cleared transactions.

We discussed this in a recent video. This is a highly speculative market, and whilst shining more light on them may help, the more fundamental question which should be asked is why allow these to exist at all. The financial markets would be safer if they were limited to only underlying transactions, not speculative positions. At the moment, there is a risk that the derivatives markets could swamp, and bring down the normal banking system in a crisis, and that risk remains un-quantifiable. Another reason for structural separation.

The central clearing of standardised OTC derivatives is a pillar of the G20 Leaders’ commitment to reform OTC derivatives markets in response to the global financial crisis. A number of post-crisis reforms are, directly or indirectly, relevant to incentives to centrally clear. The report by the Derivatives Assessment Team (DAT) evaluates how these reforms interact and how they could affect incentives.

The findings of this evaluation report will inform relevant standard-setting bodies and, if warranted, could provide a basis for fine-tuning post-crisis reforms, bearing in mind the original objectives of the reforms. This does not imply a scaling back of those reforms or an undermining of members’ commitment to implement them.

The report, one of the first two evaluations under the FSB framework for the post-implementation evaluation of the effects of G20 financial regulatory reforms, confirms the findings of the consultative document that:

The changes observed in OTC derivatives markets are consistent with the G20 Leaders’ objective of promoting central clearing as part of mitigating systemic risk and making derivatives markets safer.

The relevant post-crisis reforms, in particular the capital, margin and clearing reforms, taken together, appear to create an overall incentive, at least for dealers and larger and more active clients, to centrally clear OTC derivatives.

Non-regulatory factors, such as market liquidity, counterparty credit risk management and netting efficiencies, are also important and can interact with regulatory factors to affect incentives to centrally clear.

Some categories of clients have less strong incentives to use central clearing, and may have a lower degree of access to central clearing.

The provision of client clearing services is concentrated in a relatively small number of bank-affiliated clearing firms and this concentration may have implications for financial stability.

Some aspects of regulatory reform may not incentivise provision of client clearing services.

The analysis suggests that, overall, the reforms are achieving their goals of promoting central clearing, especially for the most systemic market participants. This is consistent with the goal of reducing complexity and improving transparency and standardisation in the OTC derivatives markets. Beyond the systemic core of the derivatives network of central counterparties (CCPs), dealers/clearing service providers and larger, more active clients, the incentives are less strong.

The DAT’s work suggests that the treatment of initial margin in the leverage ratio can be a disincentive for banks to offer or expand client clearing services. Bearing in mind the original objectives of the reform, additional analysis would be useful to further assess these effects.

In this regard, the Basel Committee on Banking Supervision issued on 18 October a public consultation setting out options for adjusting, or not, the leverage ratio treatment of client cleared derivatives.

The report also discusses the effects of clearing mandates and margin requirements for non-centrally cleared derivatives (particularly initial margin) in supporting incentives to centrally clear; and the treatment of client cleared trades in the framework for global systemically important banks.

The final responsibility for deciding whether and how to amend a particular standard or policy remains with the body that is responsible for issuing that standard or policy.

The BCBS, CPMI, FSB and IOSCO today also published an overview of responses to the consultation on this evaluation, which summarises the issues raised in the public consultation launched in August and sets out the main changes that have been made in the report to address them. The individual responses to the public consultation are available on the FSB website.

The five areas of post-crisis reforms to OTC derivatives markets agreed by the G20 are: trade reporting of OTC derivatives; central clearing of standardised OTC derivatives; exchange or electronic platform trading, where appropriate, of standardised OTC derivatives; higher capital requirements for non-centrally cleared derivatives; and initial and variation margin requirements for non-centrally cleared derivatives.

S&P Global Ratings has just come out with a significant comment on “some weaknesses in the effectiveness of regulation in the banking sector, and the conduct, governance, and risk appetite shown by Australian banks”. Finally!!

The negative rating outlooks on systemically-important Australian banks reflect pressures on the Australian sovereign creditworthiness (Commonwealth of Australia; AAA/Negative/A-1+) and a possible tempering of our current highly supportive opinion concerning the Australian government’s tendency to support banks.

During the past quarter, we revised our economic risk trend for the Australian banking industry to positive from stable. This reflects our expectation that the trend of an orderly unwinding of economic imbalances, including for high property prices and private sector indebtedness, should continue for at least the next year.

By contrast, we recently negatively revised our view of the Australian banking sector’s industry risk. In our view, developments over the past two years in the Australian banking sector, including information coming out of hearings at the ongoing Royal Commission, highlight some weaknesses in the effectiveness of regulation in the banking sector, and the conduct, governance, and risk appetite shown by Australian banks.

Blog")