ASIC says Commonwealth Bank of Australia (CBA) has entered into a court enforceable undertaking with ASIC in relation to their bank bill trading business and their participation in the setting of the Bank Bill Swap Rate (BBSW), a key benchmark and reference interest rate in the Australian financial system.

As part of the undertaking, CBA will pay $15 million to be applied to the benefit of the community and $5 million towards ASIC’s investigation and legal costs.

As part of the undertaking, CBA will pay $15 million to be applied to the benefit of the community and $5 million towards ASIC’s investigation and legal costs.

CBA will also engage an independent expert to assess changes CBA has made (and will make) to its policies, procedures, systems, controls, training, guidance and framework for the monitoring and supervision of employees and trading in Prime Bank Bills.

On 21 June 2018, the Federal Court in Melbourne imposed pecuniary penalties totalling $5 million on CBA for attempting to engage in unconscionable conduct in relation to BBSW. CBA admitted to attempting to seek to affect where BBSW set on five occasions in the period 31 January 2012 to 15 June 2012.

CBA also admitted that it failed to do all things necessary to ensure that they provided financial services honestly and fairly and that its traders were adequately trained.

Justice Beach of the Federal Court noted the terms of the court enforceable undertaking and, in imposing the pecuniary penalty of $5 million, stated ‘…that sum together with the other payments all totalling $25 million should be an adequate denouncement of and deterrence against the unacceptable trading behaviour of individuals within CBA that ought to have known better and a bank that ought to have better supervised its personnel.’

Background

ASIC commenced legal proceedings in the Federal Court against CBA on 30 January 2018 (refer:18-024MR), alleging that on three specific occasions between 31 January 2012 and October 2012, CBA traded in a manner that was unconscionable and created an artificial price and a false appearance with respect to the market for certain financial products that were priced or valued off BBSW.

This followed proceedings in the Federal Court against the Australia and New Zealand Banking Group (ANZ) on 4 March 2016 (refer: 16-060MR), against the Westpac Banking Corporation (Westpac) on 5 April 2016 (refer: 16-110MR) and against National Australia Bank (NAB) on 7 June 2016 (refer: 16-183MR).

On 10 November 2017, the Federal Court made declarations that each of ANZ and NAB had attempted to engage in unconscionable conduct in attempting to seek to change where the BBSW set on certain dates and that each bank failed to do all things necessary to ensure that they provided financial services honestly and fairly. The Federal Court imposed pecuniary penalties of $10 million on each bank.

On 20 November 2017, ASIC accepted enforceable undertakings from ANZ and NAB which provides for both banks to take certain steps and to pay $20 million to be applied to the benefit of the community, and that each will pay $20 million towards ASIC’s investigation and other costs (refer: 17-393MR).

On 24 May 2018, the Federal Court found that Westpac engaged in unconscionable conduct under s12CC of the Australian Securities and Investments Commission Act 2001 (Cth) by its involvement in setting BBSW on four occasions (refer: 18-151MR). A further hearing of this proceeding on penalty and relief will be held on 12 October 2018.

In July 2015, ASIC published Report 440, which addresses the potential manipulation of financial benchmarks and related conduct issues.

The Government has recently introduced legislation to implement financial benchmark regulatory reform and ASIC has consulted on proposed financial benchmark rules.

On 21 May 2018, the new BBSW methodology commenced (refer: 18-144MR). The new BBSW methodology calculates the benchmark directly from market transactions during a longer rate-set window and involves a larger number of participants. This means that the benchmark is anchored to real transactions at traded prices.

If there is a breach of the undertaking entered into by CBA, then under the ASIC Act, ASIC can apply for orders from the court to enforce compliance.

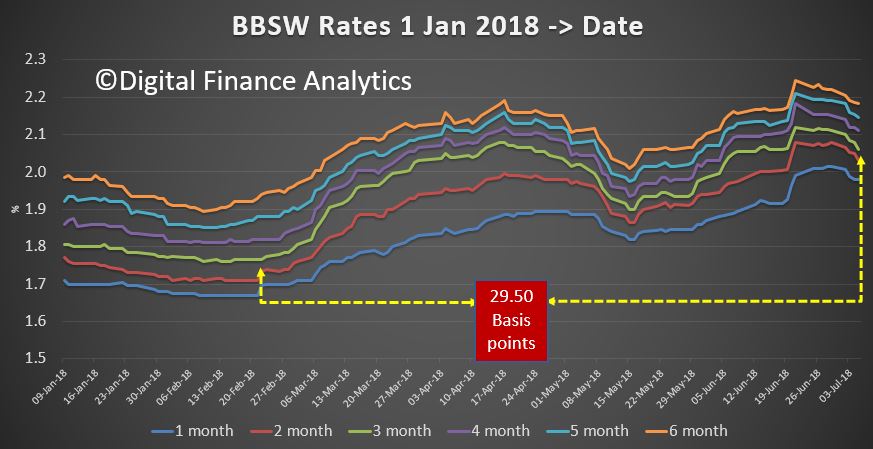

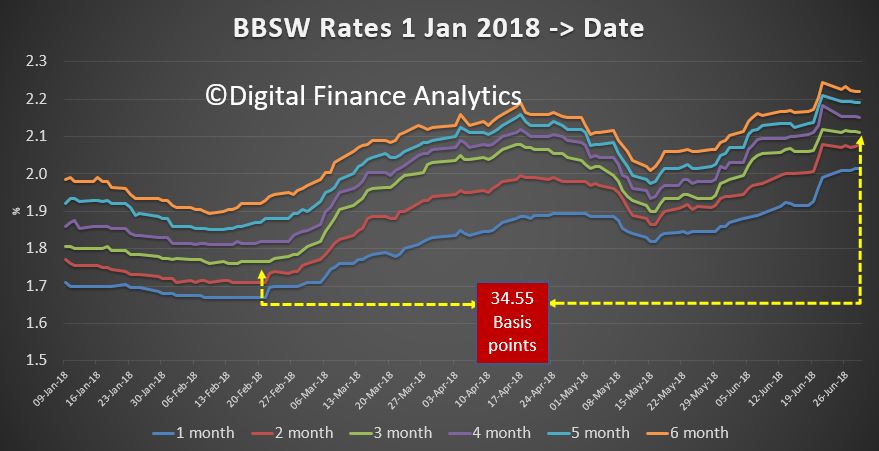

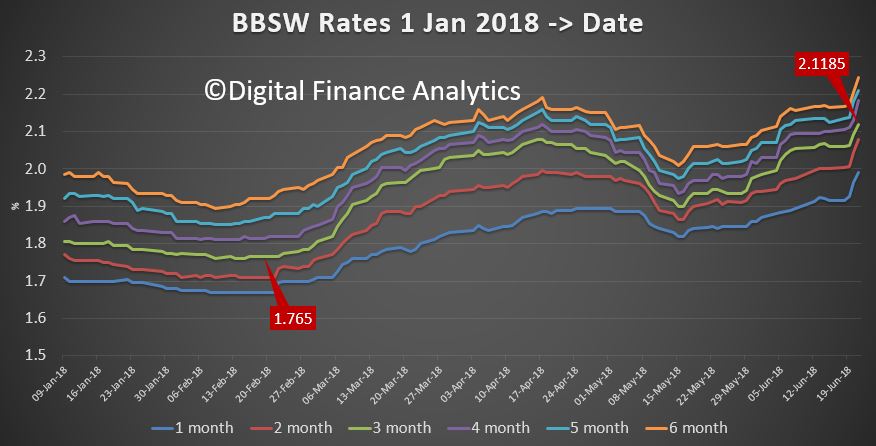

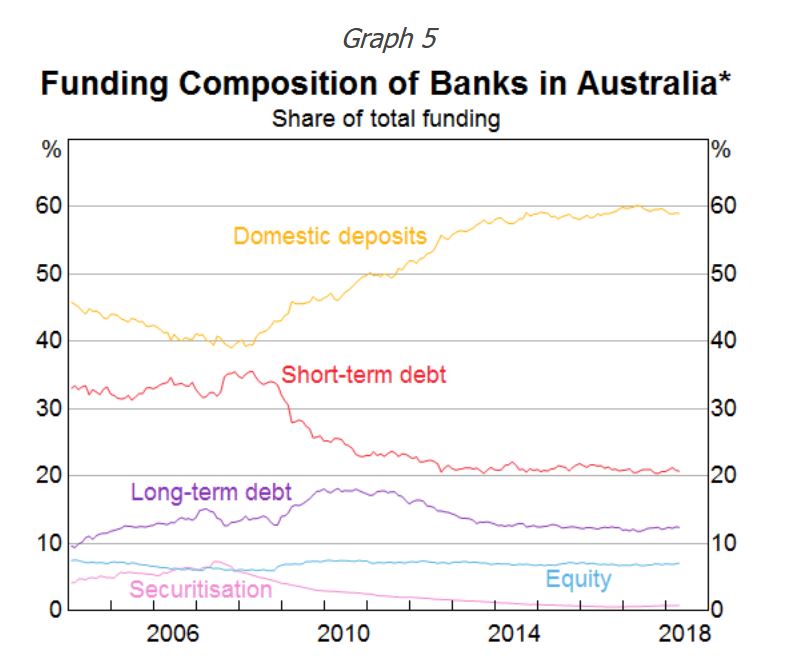

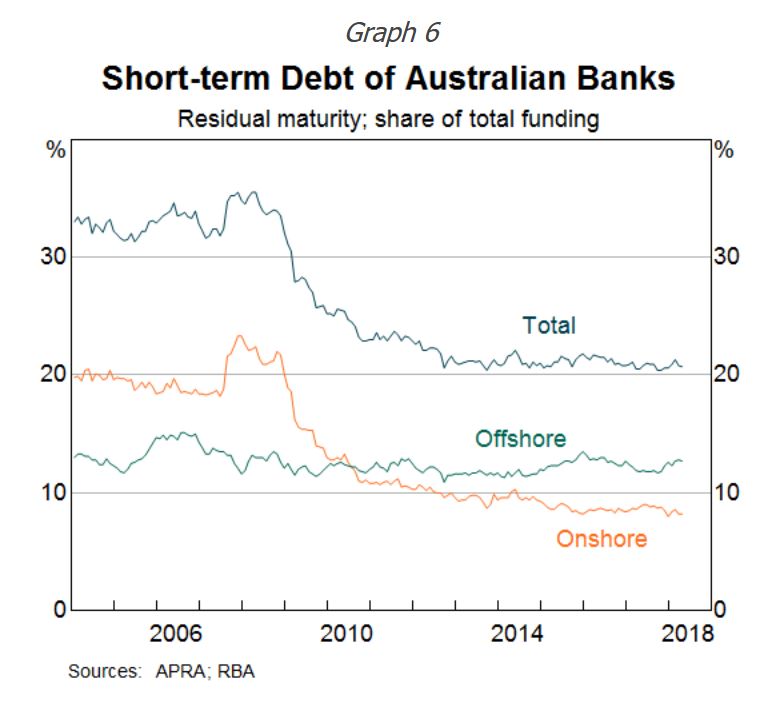

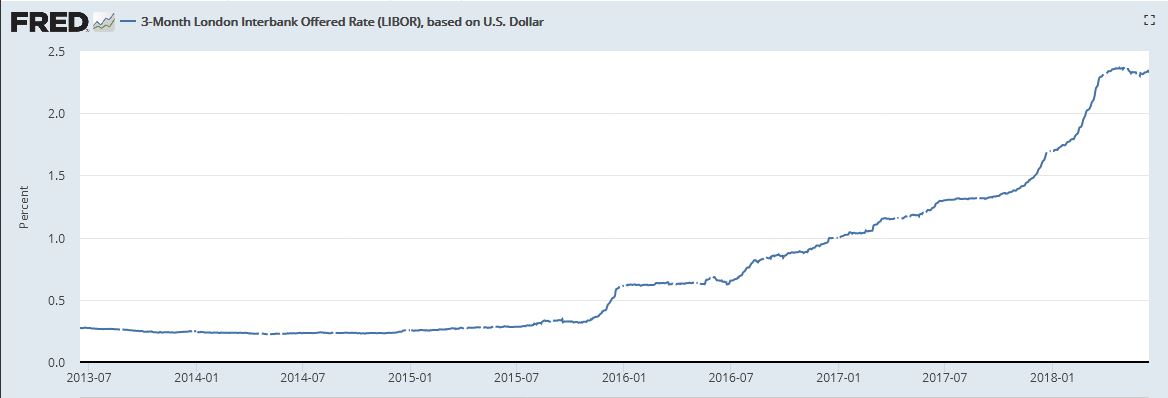

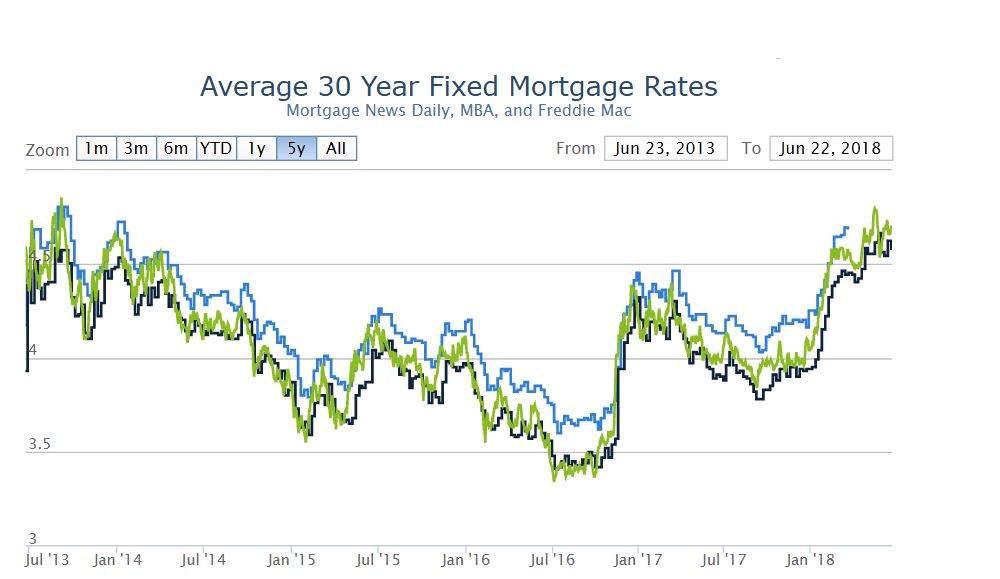

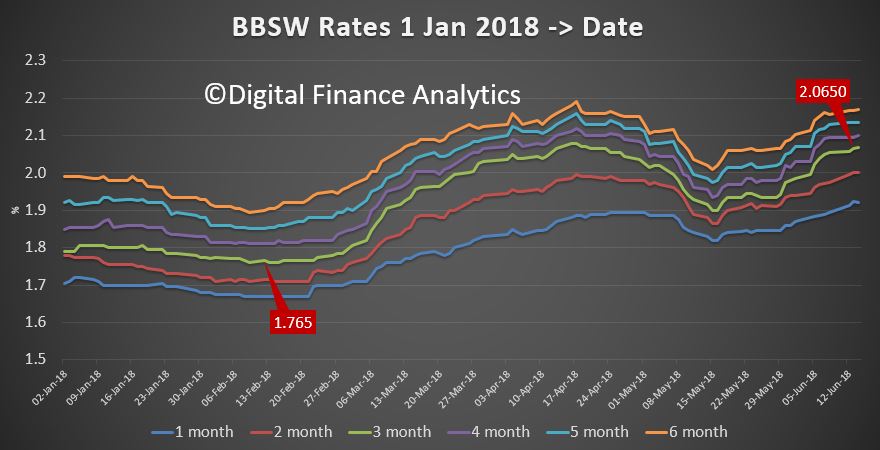

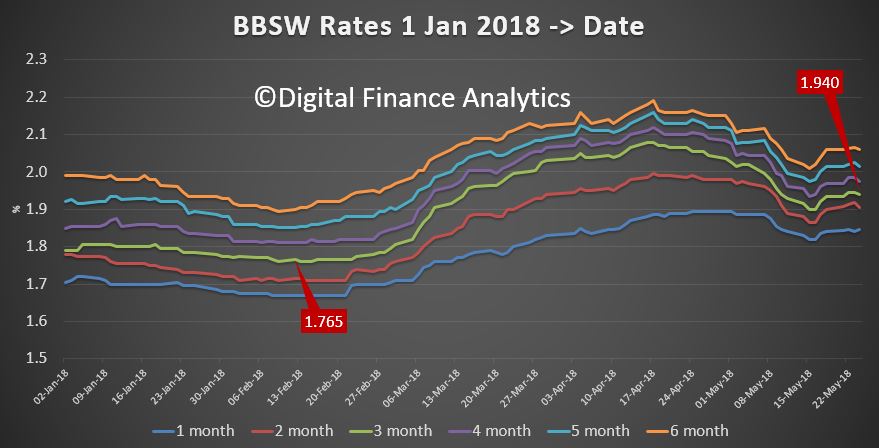

So does this mean the risk of mortgage rate hikes have also abated from the majors?

So does this mean the risk of mortgage rate hikes have also abated from the majors? This additional funding is required to support continued mortgage loan growth.

This additional funding is required to support continued mortgage loan growth.