On 19 March, the Haut Conseil de la Stabilité Financière (HCSF), the French macroprudential authority, announced it would increase banks’ countercyclical capital buffer on their exposures to French counterparties to 0.50% from 0.25% by no later than 2 April 2020.

The increase, the first since the HCSF established the buffer in June 2018 to stem the potential for excessive credit growth, raises banks’ capital requirements, a credit positive, says Moody’s.

The countercyclical capital buffer was introduced with Articles 136-140 of the European Union’s (EU) Capital Requirement Directive IV (CRD IV) to build up extra capital in boom periods and pre-empt the credit risks that accumulate during economic upswings. The buffer applies to all French, EU and European economic area banks’ that have exposures to French counterparties.

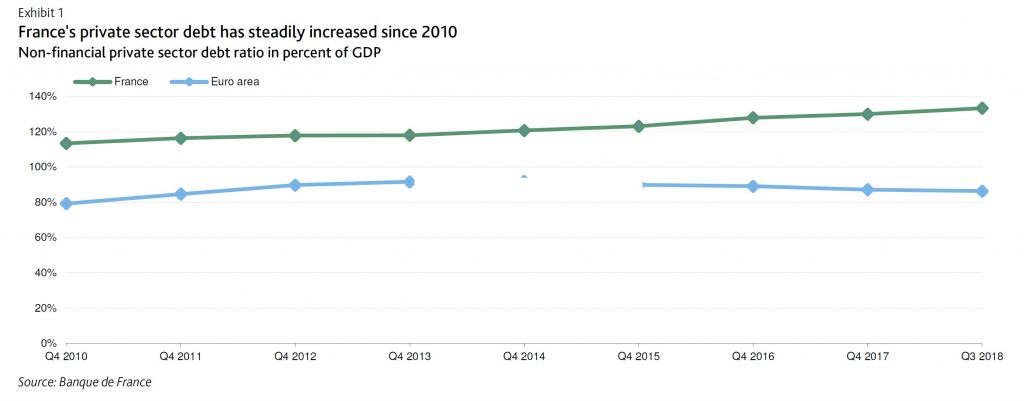

Last Monday’s increase aims to dampen continuing credit growth : non-financial private sector debt increased to 133.3% of GDP as of third-quarter 2018 (one of the highest levels in the EU) from 131.0% as of first-quarter 2018 and 113.4% at year-end 2010.

Since 2016 credit to corporates and households has increased at a 4%-6% annual rate amid relaxed lending standards (especially on housing loans with higher loan-to-value ratios and longer maturities), rising house prices and increasing leveraged buyout transactions (up 3.6% in February 2019 compared to February 2018). Moreover corporate debt issuance also drove the increase in indebtedness, in particular at large corporates, which prompted the HCSF to express some concern.

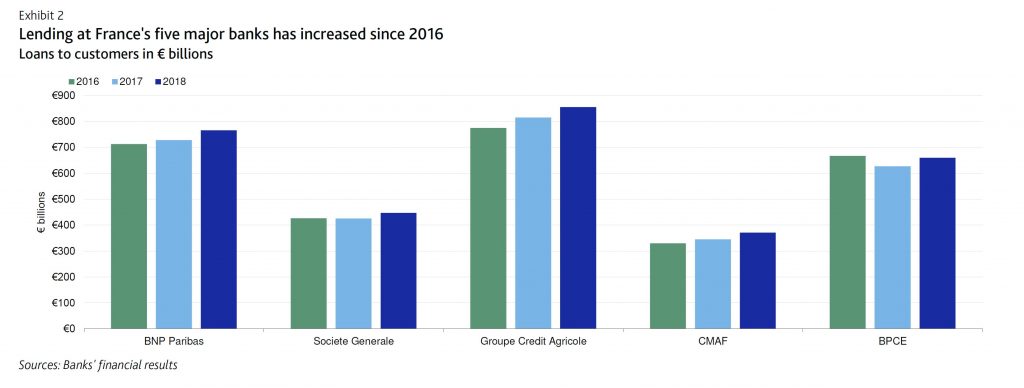

Total lending (domestic and international) among France’s five major banks – BNP Paribas, Societe Generale, Credit Agricole S.A., Banque Federative du Credit Mutuel, BPCE – grew 5.6% year over year as of year-end 2018, with bank loans to SMEs growing a robust +6.3% for the same period.

Additionally, France’s credit-to-GDP gap (measuring the difference between the credit-to-GDP ratio and its long-term trend) was 2.7 percentage points in fourth-quarter 2018, versus the euro area average of negative 12.4 percentage points at the same time.

The HCSF’s decision will be submitted to the ECB on a non-objection basis and will be adopted before 2 April 2019 for an effective implementation of this requirement a year later (April 2020).

The 2018 decision to set a CCyB at 0.25 % has not resulted in a more moderate lending growth at French banks hence the decision to tighten it at 0.50%. It remains to be seen whether or not a higher capital add-on will be successful in materially curbing lending at banks. If not successful the official sector may consider tightening the 0.5 % CCyB once again.

We assign a one-notch downward adjustment for credit conditions in France’s macro profile, which reflects the macro- risks faced by banks, to account for the material growth of private sector indebtedness in France since 2015 and the risk that a too rapid rise in corporate and household debt could eventually increase the vulnerability of borrowers to an economic downturn.

Many European have imposed much higher countercyclical capital buffers, up to 2.5% (for example, Sweden). The growing use of CCyBs in European countries – 11 countries have resorted to this prudential measure – points to a potential accumulation of excessive credit risk throughout the region.

APRA’s Pat Brennan, Executive General Manager, Policy and Advice Division spoke at the 2019 KangaNews Debt Capital Markets Summit, Sydney

Bank capital (and liquidity) is the core of financial resilience, hence capital ratios are key indicators of financial strength. Bank boards, investors and regulators pay very close attention to these, the headline ratios and the underlying drivers, for reasons that are very obvious to this audience.

Reflecting the importance of financial strength,

APRA is in the process of updating the entire prudential framework for

capital in the banking industry. This began in 2014 with the Financial

System Inquiry recommendation for APRA to set requirements such that

Australian bank capital ratios are “unquestionably strong”, and

substantial progress has been made against this objective. More recently

at the end of 2017, the Basel Committee on Banking Supervision

finalised most of the post-global financial crisis (GFC) reforms,

finishing off in January of this year with the release of the final

market risk capital framework. In 2018 APRA began the public

consultation process as we sought to synthesise these two key drivers,

as well as introducing a variety of features that are specific to the

Australian industry.

Today I will provide an update on APRA’s

approach to risk-based capital requirements, then loss-absorbing

capacity (LAC), and then provide an update on what policy developments

APRA is working on behind the capital headlines.

Risk-based capital

A 10-year post-GFC capital build is near completion with

unquestionably strong capital ratios already attained by most banks.

Stress tests undertaken by both APRA and the IMF in recent years have

also found banks remaining above regulatory minimum requirements in very

severe stress scenarios.

While the overall amount of capital

that needs to be held by Australian banks has already been set in the

unquestionably strong benchmarks announced in July 2017, the allocation

of the precise amount of capital attributable to each source of risk is

being worked through as part of the revisions to the capital framework.

In February last year, APRA released an initial discussion paper that

proposed a number of revisions to the credit risk, operational risk and

market risk frameworks, including the adoption of a capital floor, which

will limit the capital benefit banks that use the internal

ratings-based approach (IRB) can obtain relative to those that use the

standardised approaches. These proposals focus primarily on improving

the risk sensitivity of the capital framework.

In August last

year, APRA also released a discussion paper on improving the

transparency, comparability and flexibility of the capital framework in

areas where APRA’s methodology is more conservative than minimum

international requirements. The proposals in that paper complement the

revisions to the capital framework by seeking to ensure that the capital

strength of Australian banks is appropriately understood by market

participants.

APRA expects to soon release its response to

revised capital requirements for credit risk and operational risk. In

relation to the former, the next phase of consultation will focus on the

treatment of residential mortgages for all banks, and other amendments

to the standardised approach to credit risk. Later this year, APRA will

release its full response to the revised credit risk requirements for

the IRB approach and its response to improving transparency,

comparability and flexibility. The outcome of this may lead to

significant presentational and calculation changes to a number of

prudential standards, although these would not affect the quantum of

capital required.

This stream of work is a multi-year process and

is likely to involve further rounds of consultation and quantitative

impact studies to enable APRA to assess the impact and better calibrate

the proposed changes. Given the need for extensive consultation, the

revised prudential standards are likely to be finalised in late 2020,

and are intended to commence in early 2022, consistent with the

international timetable agreed at the Basel Committee.

Loss-absorbing capacity and recapitalisation

Our work on building loss-absorbing and recapitalisation capacity

to deal with a bank failure or near-failure has been moving on a very

different timeline to risk-based capital, and deliberately so. The 2014

Financial System Inquiry recommended introducing LAC requirements in

Australia (which was consistent with APRA’s intent), adding that

international practices were still emerging at that time, and APRA

should follow these developments.

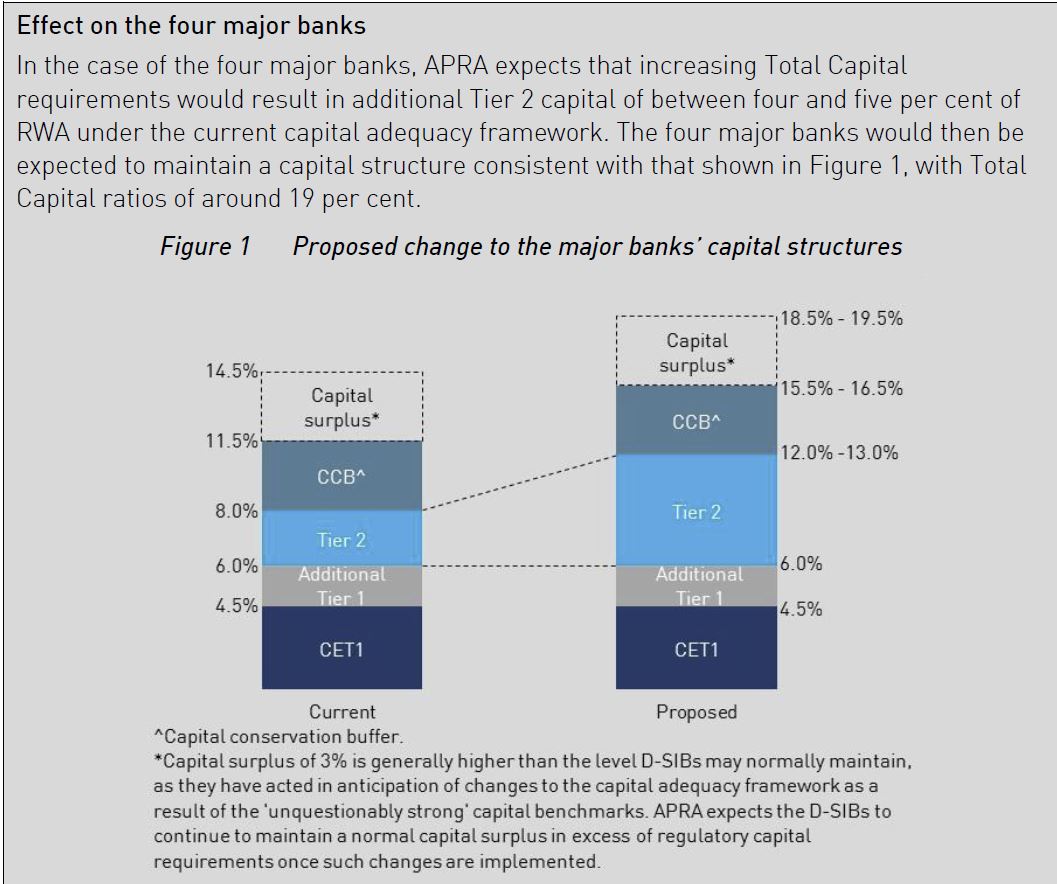

In November last year, APRA released the discussion paper Increasing the loss-absorbing capacity of authorised deposit-taking institutions to support orderly resolution.

In this paper we proposed increasing the Total Capital Requirement of

the major banks by between 4 and 5 per cent of risk-weighted assets,

with the expectation this would be mostly met through the increased

issuance of Tier 2 instruments. APRA intentionally proposed a simple

approach of using existing, well-understood capital instruments, given

they have been proven to work for their intended purpose – that is they

recapitalise a bank when needed.

Whilst APRA is still considering

submissions received and gathering additional information, and as such

we have not yet made any decisions on the proposals, I will offer a few

observations. The response we have received has been somewhat mixed. We

have been given clear feedback in a number of submissions that the

quantum of Tier 2 targeted, particularly at the higher end of the

calibration range consulted on, will test the likely bounds of investor

capacity. Submissions therefore challenged whether that calibration is

sustainable over time given debt markets will continue to experience

occasional periods of difficult issuance conditions. Some submissions

also questioned whether there are lower cost options to achieve the same

level of recapitalisation capacity, accepting these options are more

complex. On the other hand we have also received feedback from some

parties that using existing, proven capital instruments is a very good

idea.

In the debate about what is the best form of LAC, many

submissions concentrated on its form and understandably referred to the

variety of international approaches that have emerged. Submissions

offered informative perspectives on the relative merits of differing

forms of LAC from a capacity and efficiency perspective. Few, however,

reflected on the differing objectives and structures that have

influenced the divergence of international approaches.

Now is a good time to reflect that in many jurisdictions the chosen LAC approach was in direct response to their own, painful, lived experience through the GFC; with the reality of “Too Big to Fail” meaning authorities were faced with no choice but to bail-out troubled banks. In some jurisdictions this has led to a stated policy approach with the express, singular objective to never again require taxpayers to fund a bank bail-out. On the other hand, in other jurisdictions, including Australia, the objective is to protect the community from the potentially devastating broader impacts of financial crises. This is done firstly by reducing the probability of failure; and secondly by establishing sufficient recapitalisation capacity such that, should a failure or near-failure occur, the overall cost is minimised. This is consistent with the Financial System Inquiry recommendation that stated recapitalisation capacity should be “sufficient to facilitate the orderly resolution of Australian authorised deposit-taking institutions and minimise taxpayer support.”

These differing objectives guide

policy choices. Differing legislative and regulatory frameworks, and

institutional and corporate structures, around the globe also guide

choices and have played a role in influencing the divergence of

approaches adopted.

So for now we are thinking through options

and gathering additional information. APRA would still prefer a solution

that is on the side of simplicity, though at the same time we clearly

want to arrive at an approach that will work over time.

Whenever

APRA consults on a policy we undertake a genuine consultation process

and, for major policy such as this, it is an extensive process and all

submissions are carefully considered. In this case we have benefitted

from a high level of engagement with a broad range of stakeholders,

broader than is usually the case for APRA consultations, reflecting this

is new territory. At this point I cannot say when we will make public

our findings from the consultation, but given some years ago we

intentionally adopted the position of a follower of international

developments, we are now motivated to work through the considerations as

swiftly as possible.

Following finalisation of the LAC framework

APRA will build out other aspects of the prudential framework for

recovery and resolution.

And now, what is behind the headlines?

Without diminishing their importance, there is plenty that capital

ratios do not tell you. They don’t tell you how well a bank is run: if

its approach to risk management is sound, whether there is good

governance, and whether stakeholder interests are appropriately

balanced. Capital is no panacea as financial strength alone cannot

adequately mitigate against poor risk management or weak governance.

These are fundamental concerns for a prudential regulator. Capital

standards, including unquestionably strong benchmarks, are set on the

basis of at least sound risk management and governance being in place,

and so APRA has an ongoing supervisory and policy focus on non-financial

risks and drivers.

Cyber-risk, remuneration, accountability,

governance, risk management, recovery and resolution – these will

naturally become the greater part of APRA’s policy focus for the

forthcoming years. We are not lowering policy intensity on financial

risk and capital, but we are complementing and adding to this by

strengthening the prudential framework for non-financial risk.

Here is a quick overview of what to expect:

Late last year, APRA released the final version of Prudential Standard CPS 234 Information security,

which provides a clear set of requirements and expectations covering

information security, including cyber risk. We will very shortly be

supplementing this with a detailed practice guide.

In the next

quarter we will release for consultation an updated prudential standard

on remuneration. This follows the April 2018 Information Paper Remuneration practices at large financial institutions,

which reported on a thematic review APRA conducted where we found that

practices were not as robust as they should be. We have also learnt a

great deal from the CBA Prudential Inquiry and of course the Royal

Commission. The new standard will be stronger and be primarily focused

on outcomes. This will include that performance assessment must reflect

consideration of all relevant contributions to performance, including

risk management; banks will need to be transparent with APRA on how

remuneration decisions are made; and variable remuneration must be truly

variable in practice.

We will also have a significant focus on

governance and accountability. An extension of the Banking Executive

Accountability Regime (BEAR) to cover other prudentially regulated

industries has been a consideration since BEAR was first envisaged –

APRA has consistently supported this extension as the prudential

principles of BEAR apply equally across industries. Following the Royal

Commission, the BEAR extension will go even further, with a parallel

conduct accountability regime to be administered by ASIC. This is an

important development and APRA and ASIC will work closely to ensure the

parallel regimes work optimally. APRA will refresh its Governance and

Fit and Proper standards to not only more closely complement the

accountability regime, but to strengthen standards more generally; again

this will be in light of what we have learned through our supervisory

activity, through the CBA Prudential Inquiry and the findings of the

Royal Commission.

In the sphere of risk management, APRA will in the near future release for consultation a materially updated Prudential Standard APS 220 Credit Quality that

we will also rename to Credit Risk Management. Given credit is the most

material risk of the Australian banking sector we expect this will get

plenty of attention. On a slightly longer time frame, we are developing

an overarching operational risk standard and will consider changes to Prudential Standards CPS 220 Risk Management as our work of non-financial risk progresses.

In

conclusion, APRA has a comprehensive policy agenda both on bank capital

and non-financial risk. On the latter, this will draw on our

supervisory experience, the CBA prudential inquiry, the findings of the

Royal Commission and international developments. The Australian banking

system is well capitalised and APRA is supplementing that financial

strength by ensuring strong risk management and sound governance

practices are in place across the full spectrum of risks that banks

face.

A spike in market volatility during fourth quarter 2018 dragged down overall capital markets results for the five major U.S. trading banks including: Bank of America Corporation (BAC), Citigroup, Inc. (C), The Goldman Sachs Group (GS), JPMorgan Chase & Co. (JPM) and Morgan Stanley (MS), according to the latest report from Fitch Ratings.

“Market

volatility can be a boost to trading revenues; however, too much

volatility in fixed income sales outweighed strength in equity trading

and advisory revenues this quarter,” said Julie Solar, senior director,

Fitch Ratings. “Too little volatility results in fewer trading

opportunities, but too much keeps investors on the side lines.”

Total

debt underwriting revenues fell 24% from the year-ago period,

reflecting volatility, particularly impacting the high-yield market.

Fitch expects that some volume was financed directly by commercial

banks, which reported very strong commercial and industrial loan

(C&I loan) growth trends in 4Q18.

However, despite a

challenging final six weeks of the year, record earnings during the

first part of the year contributed to the highest full-year results

since 2009. Capital markets revenues for the five banks included in this

report totalled $107 billion in 2018, approximately 4% higher than in

2017, aided mainly by a significant increase in equity sales and trading

revenues.

M&A activity in 4Q18 increased a considerable 37%

versus last year, buoyed by a significant rise in M&A completions

and continued strength from the technology and healthcare sectors.

Several banks noted that deal pipelines remain strong, although down on a

linked-quarter basis.

“Even with a strong backlog of deals,

continued volatility and market sentiment could impact banks’ ability to

bring transactions to market, and the IPO pipeline may also feel an

impact from the prolonged government shutdown as the SEC was unable to

review pending IPOs for several weeks. 2019 is off to a strong start and

the first quarter is typically the strongest of the year, but it is

unclear how investment banking revenues could be impacted,” added Solar.

The Basel III leverage ratio standard comprises a 3% minimum level

that banks must meet at all times, a buffer for global

systemically-important banks and a set of public disclosure

requirements. For the purpose of disclosure requirements, banks must

report the leverage ratio on a quarter-end basis or, subject to approval

by national supervisors, report a measure based on averaging (eg using

an average of exposure amounts based on daily or month-end values).

Heightened volatility in various segments of money and derivatives

markets around key reference dates (eg quarter-end) has alerted the

Basel Committee to potential regulatory arbitrage by banks. A particular

concern is “window-dressing”, in the form of temporary reductions of

transaction volumes in key financial markets around reference dates

resulting in the reporting and public disclosure of elevated leverage

ratios. In this regard, the Committee published a newsletter in

October 2018 in which it indicated that window-dressing by banks is

unacceptable, as it undermines the intended policy objectives of the

leverage ratio requirement and risks disrupting the operations of

financial markets.

This consultative document seeks comments on revisions to leverage

ratio Pillar 3 disclosure requirements to include, in addition to current requirements,

mandatory disclosure of the leverage ratio exposure measure amounts of

securities financing transactions, derivatives replacement cost and

central bank reserves as calculated using daily averages over the

reporting quarter.

The Committee welcomes comments on all aspects of the consultative document here by Wednesday 13 March 2019

The Reserve Bank of New Zealand has released a discussion paper in which they consult on proposals to lift the capital held by banks in New Zealand.

The expected effect on banks’ capital is an increase of between 20 and 60 percent. This represents about 70 percent of the banking sector’s expected profits over the five-year transition period. They expect only a minor impact on borrowing rates for customers.

They say “Banks currently get the vast majority of their money by borrowing it (usually over 90 percent), with the rest coming from owners (usually less than 10 percent). The Reserve Bank is proposing to change this balance by requiring banks to use more of their own money. This proposal is consistent with steps taken by other banking regulators after the Global Financial Crisis”.

Banks currently get the vast majority of their money by borrowing it (usually over 90 percent), with the rest coming from owners (usually less than 10 percent). The Reserve Bank is proposing to change this balance by requiring banks to use more of their own money. This proposal is consistent with steps taken by other banking regulators after the Global Financial Crisis.

If banks increase their capital, they will be more resilient to economic shocks and downturns, which will strengthen New Zealand’s banking system and economy.

Because the level of a bank’s capital can have an impact on the interest rate it charges on its loans, it is possible that higher capital requirements could make it more expensive for New Zealanders to borrow money from a bank. While we certainly take this into account, we think this impact should be minimal.

Another potential impact is that bank owners would earn less from their investment in the bank. While we agree that this is likely to be the case, we believe this cost would be more than offset by the benefits of a safer banking system for all.

The key changes are:

Limit the extent to which capital requirements differ between the Internal Ratings-Based approach (IRB) and the Standardised approach, by re-calibrating the IRB approach and applying a floor linked to the Standardised outcomes. This reflects one of the principles of the Capital Review: where there are multiple methods for determining capital requirements, outcomes should not vary unduly between methods. In essence, there should be as level a playing field as possible, both between IRB banks and between IRB and Standardised banks;

These proposals are expected to raise risk-weighted assets (RWA) for the four IRB-accredited banks to approximately 90 percent of what would be calculated under the Standardised approach;

Set a Tier 1 capital requirement (consisting of a minimum requirement of 6 percent and prudential capital buffer of 9-10 percent) equal to 16 percent of RWA for banks deemed systemically important, and 15 percent for all other banks;

Assign 1.5 percentage points of the proposed prudential capital buffer requirements to a countercyclical component, which could be temporarily reduced to 0 percent during periods of exceptional stress;

Assign 1 percentage point of the proposed prudential capital buffer requirement to D-SIB buffer, to be applied to banks deemed to be systemically important;

Retain the current Tier 2 capital requirement of 2 percent of RWA, but raise the question of whether Tier 2 should remain in the capital framework; and

Staged transition of the different components of the revised framework over the coming years.

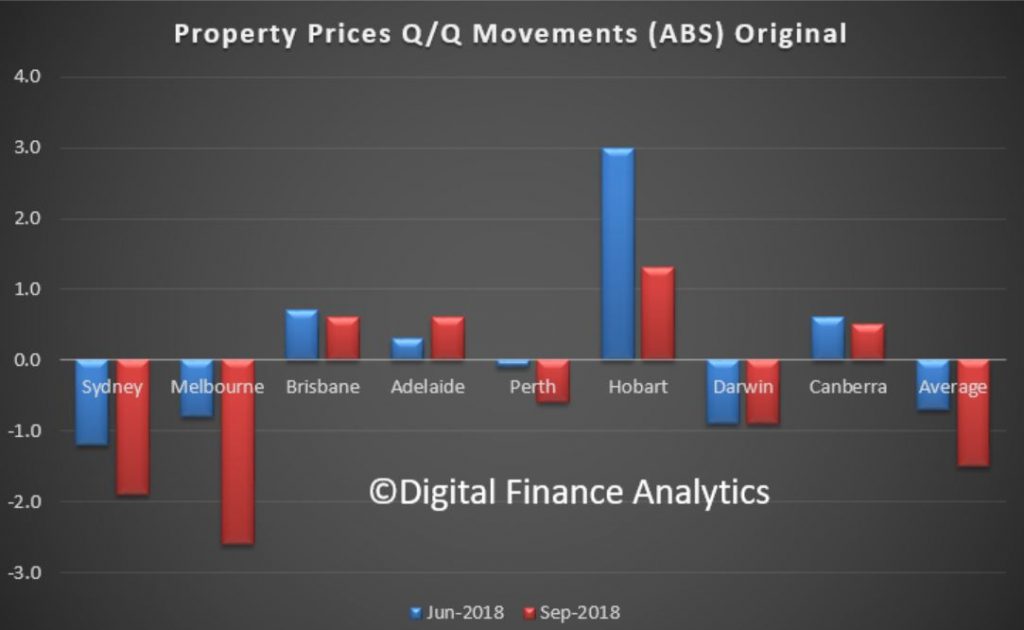

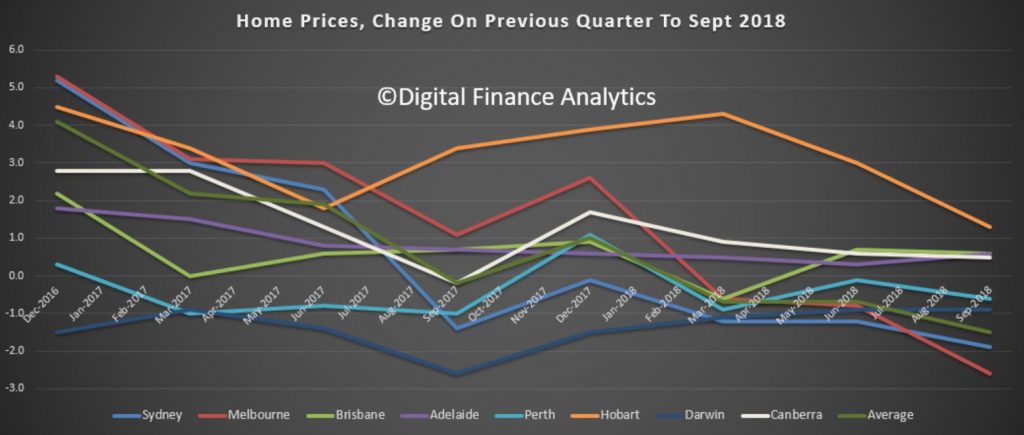

They said that the price index for residential properties for the weighted average of the eight capital cities fell 1.5% in the September quarter 2018. The index fell 1.9% through the year to the September quarter 2018.

The capital city residential property price indexes fell in Melbourne (-2.6%), Sydney (-1.9%), Perth (-0.6%) and Darwin (-0.9%), and rose in Brisbane (+0.6%), Adelaide (+0.6%), Hobart (+1.3%) and Canberra (+0.5%).

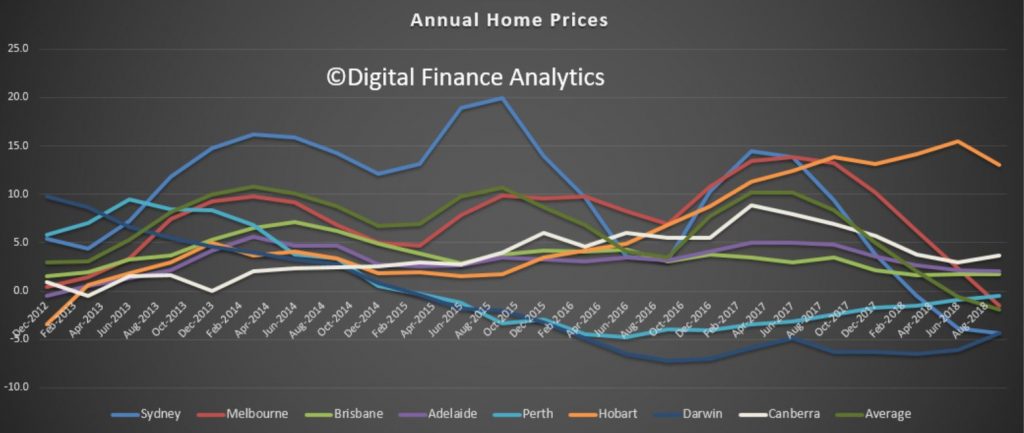

Annually, residential property prices fell in Sydney (-4.4%), Darwin (-4.4%), Melbourne (-1.5%), Perth (-0.5%) and rose in Hobart (+13.0%), Canberra (+3.7%), Adelaide (+2.0%) and Brisbane (+1.7%).

The total value of residential dwellings in Australia was $6,847,057.2m at the end of the September quarter 2018, falling $70,148.6m over the quarter.

The mean price of residential dwellings fell $9,700 to $675,000 and the number of residential dwellings rose by 40,900 to 10,143,700 in the September quarter 2018.

Of course these averages do not tell the true picture, because the movements are not uniform across a state. In some post codes now we are seeing falls of more than 20% from the previous peak, elsewhere prices are holding more steadily. However, given credit availability drives home prices, and credit is harder to come by, we should expect more falls ahead. Then the question becomes, is a soft landing feasible? I have to say that all the cycles I have examined never ended softly, so it would be a first, if it did happen.

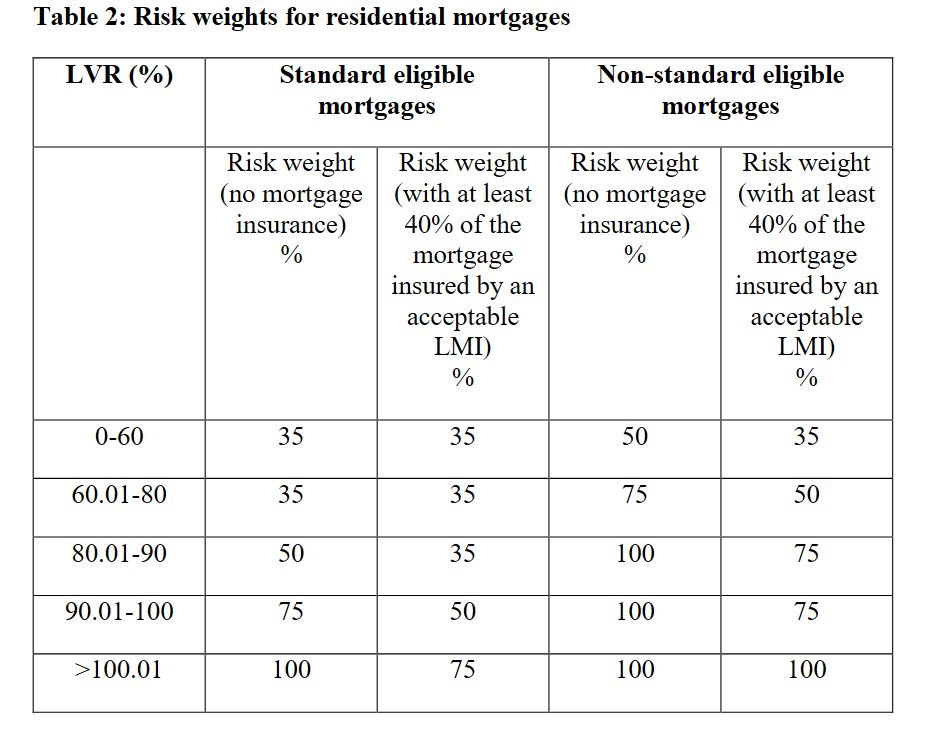

But there is another point to consider. Major banks use internal risk models to calculate the amount of capital they hold against mortgage loans. Other banks use more standard approaches.

The calculation is driven by a range of factors, but LVR is one element. Here is the APRA risk weights table. The point is a loan with an LVR at 80% has a risk weight of 50%, but the same loan at 90% LVR requires 75%, and 100% LVR 100% weighting. In other words, the capital doubles between 80 and 100% LVR!

At some point quite soon now banks will need to re-baseline their mortgage books. When property prices were rising, they would do this quite regularly to reduce the capital requirement. The reverse is also true.

The governing APRA document says “The ADI must also revalue any property offered as security for such loans when it becomes aware of a material change in the market value of property in an area or region”. Have banks started to revalue their portfolios and up their risk weights in the light of these falls? This is also, by the way, why economists attached to the major banks have an interest in playing down potential home price falls.

APRA says “the valuation may be based on the valuation at origination or, where relevant, on a subsequent formal revaluation by an independent accredited valuer. The determination of the appropriate risk weight is also dependent upon mortgage insurance provided by an acceptable lenders mortgage insurer (LMI)”. Of course many lenders now have access to Automated Valuation Models from players such as CoreLogic.

So now the question becomes, how much more capital will the banks have to put aside to take account of falling prices, who will bear the cost, and will APRA back down on its capital requirements which insist the banks hold more capital ahead? I expect more weakness in bank share prices as the impact of this hits home. As home prices fall further the impact will be magnified.

This is probably one of the most significant speeches on the issue, as it gets to the core thinking driving bank regulation. Essentially it is this. If there were to be a financial crisis, experience has shown the costs to the broader economy are substantial, and are born by society.

As a result, Orr argues that while a significant toolkit is available to lean against these risks, the cornerstone is lifting bank capital.

Note though that the toolkit includes under crisis management OBR – deposit bail-in!

As a result, the amount of capital required will be significantly higher.

Implicitly, this approach enables the financial system to continue to expand, to drive debt higher (as we saw in his recent post), with the financial stability risks offset by higher capital. But as we have said many times, this faith in ever great debt as a growth lever is deeply flawed. And those borrowing will be required to pay more, as higher capital costs!

Here is the speech in full.

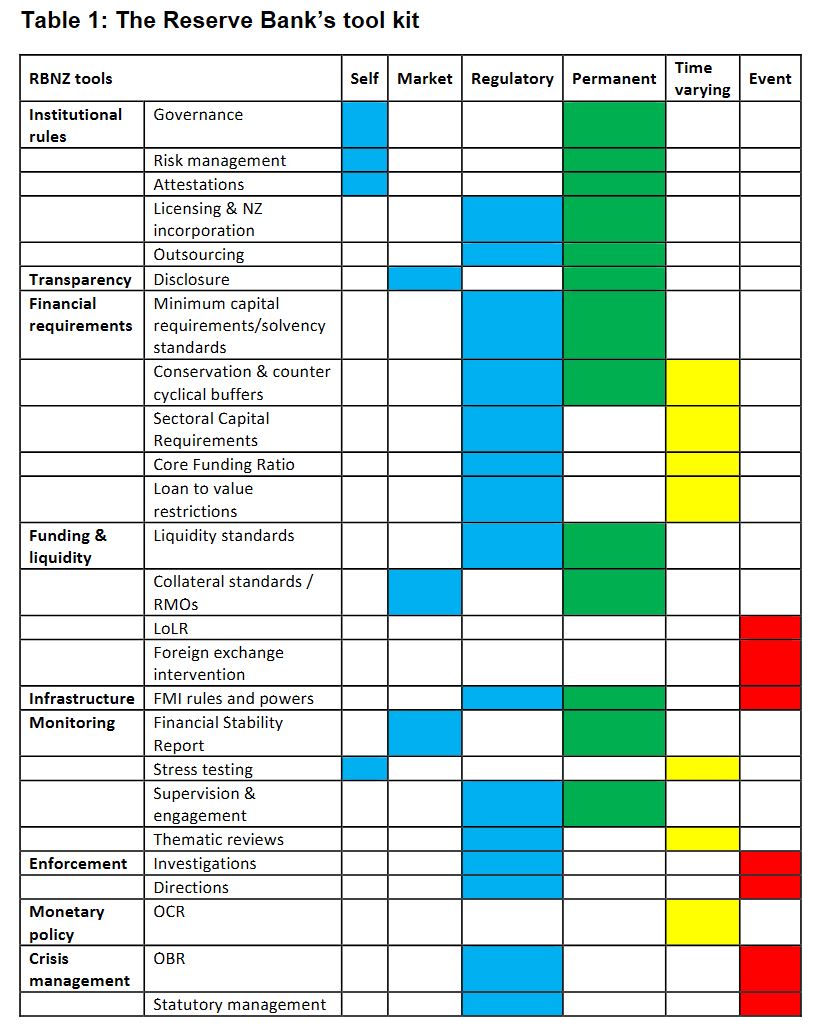

The Reserve Bank is tasked with ensuring the banking system is both sound and efficient. To achieve our task we have a range of tools (see Table 1). The most important tool in our kit is ensuring banks hold sufficient capital (equity) to be able to absorb unanticipated events. The level of capital reflects the bank owners’ commitment – or skin in the game – to ensure they can operate in all business conditions, bringing public confidence.

Given its importance, we have been undertaking a review of the optimal level of capital for the New Zealand system. We conclude that more capital is better. We are sharing our work with the banking sector and public, and expect to hear one side of the story loud and clear, that capital costs banks. We need to hear a broader perspective than that, to best reflect New Zealand’s risk appetite.

What have we done in practice?

The Reserve Bank needs to ensure there is sufficient capital in the banking “system” to match the public’s “risk tolerance”. This is because it is the New Zealand public – both current and future citizens – who would bear the social brunt of a banking mess.

We know one thing for sure, the public’s risk tolerance will be less than bank owners’ risk tolerance. How do we know this? Surely the more capital a bank has the safer it is and the more it can lend. Why don’t banks hold as much capital as they can?

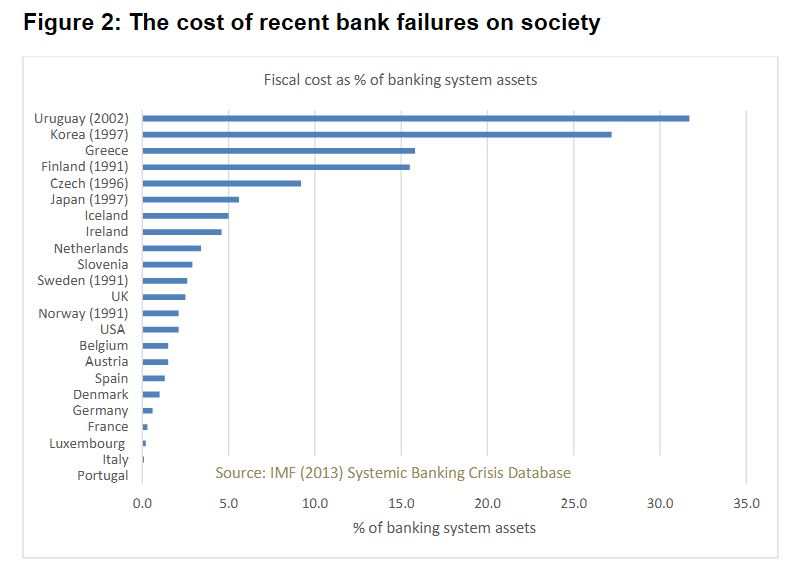

First, there is cost associated with holding capital, being what the capital could earn if it was invested elsewhere. Second, bank owners can earn a greater return on their investment by using less of their own money and borrowing more – leverage. And, the most a bank owner can lose is their capital. The wider public loses a lot more (see Figure 2).

Hence, we need to impose capital standards on banks that matches the public’s risk tolerance. We have been reassessing the capital level in the banking sector that minimises the cost to society of a bank failure, while ensuring the banking system remains profitable.

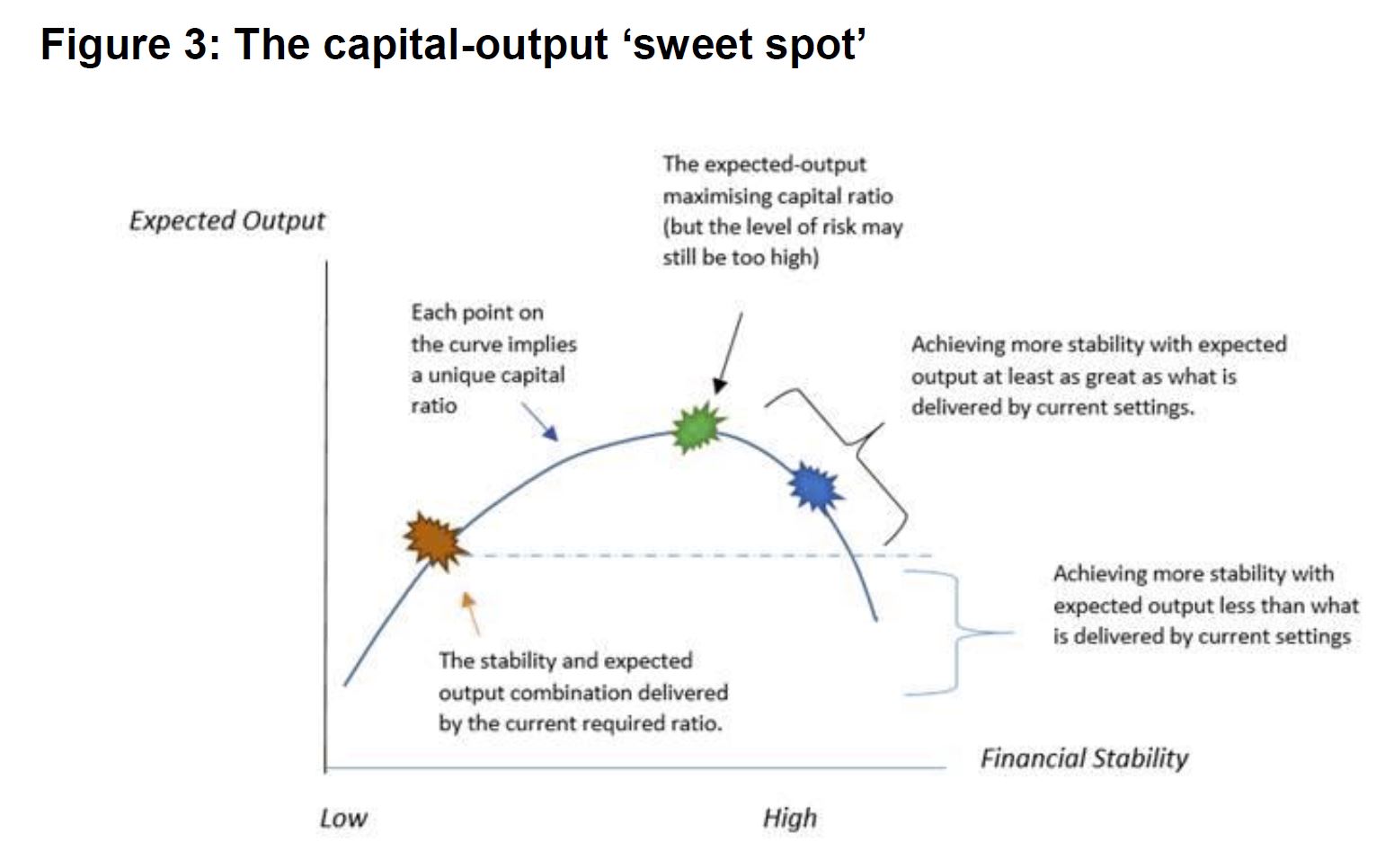

The stylised diagram in Figure 3 highlights where we have got to. Our assessment is that we can improve the soundness of the New Zealand banking system with additional capital with no trade-off to efficiency.

In making this assessment, our recent work makes the explicit assumption that New Zealand is not prepared to tolerate a system-wide banking crisis more than once every 200 years. We have calibrated our ‘sweet spot’ thinking about economic ‘output’ and financial stability benefits.

How did we arrive at this position?

Current levels of capital are based on international standards, and are not optimal for any one country. The standards are also a minimum. There is a clear expectation that individual countries tailor the standards to their financial system’s needs.

Banks also hold more capital than their regulatory minimums, to achieve a credit rating to do business. The ratings agencies are fallible however, given they operate with as much ‘art’ as ‘science’.

Bank failures also happen more often and be more devastating than bank owners – and credit ratings agencies – tend to remember. The costs are spread across the public and through time.

Many large banks are foreign owned – especially in New Zealand. Their ‘parents’ are subject to capital requirements in their home and host country. This creates continuous tension as to who gets the lion’s share of capital and failure management support. It would be naïve to expect a foreign taxpayer to bail out a domestic banking crisis.

Hence, New Zealand needs to assess its own risk tolerance, and decide who pays to clean up any mess and the scale of that mess.

A word of caution. Output or GDP are glib proxies for economic wellbeing – the end goal of our economic policy purpose. When confronted with widespread unemployment, falling wages, collapsing house prices, and many other manifestations of a banking crisis, wellbeing is threatened. Much recent literature suggests a loss of confidence is one cause of societal ills such as poor mental and physical health, and a loss of social cohesion. If we believe we can tolerate bank system failures more frequently than once-every-200 years, then this must be an explicit decision made with full understanding of the consequences.

The Australian Prudential Regulation Authority (APRA) has released its response to submissions on the introduction of a leverage ratio requirement for authorised deposit-taking institutions (ADIs).

APRA also announced that it is proposing to align the implementation of a range of revisions to the capital framework for ADIs, including the proposed leverage ratio, with the timeline set out in the Basel III framework.

The leverage ratio, which measures the proportion of an ADI’s assets that is funded through equity (capital) rather than debt, is designed to supplement risk-based capital requirements by providing stakeholders with an alternative perspective on ADIs’ capital strength.

APRA released proposals in February 2018 to incorporate a minimum leverage ratio within the ADI prudential framework. Most submissions broadly supported the introduction of a minimum leverage ratio, but raised concerns about the calibration of the minimum requirement and calculation methodology. In response, APRA has proposed to:

set the minimum requirement for ADIs using the internal ratings-based approach (IRB ADIs) to determining capital adequacy at 3.5 per cent, rather than 4 per cent;

keep the leverage ratio for ADIs that use the standardised approach to determine capital adequacy (standardised ADIs) at 3 per cent;

allow standardised ADIs to use Australian accounting standards, rather than the more complex Basel III methodology, to calculate certain parts of the ratio; and

require IRB ADIs to largely follow the Basel III methodology to calculate their leverage ratios.

ADIs’ leverage ratio requirements are outlined in the draft amended Prudential Standard APS 110 Capital Adequacy; APRA is also introducing a new reporting standard, ARS 110.1 Leverage Ratio. APRA is seeking industry feedback on the draft standards and invites interested parties to provide submissions by 22 February 2019.

Small ADIs that qualify for the simplified prudential framework – which is intended to introduce more proportionate and tailored prudential requirements for smaller and less complex ADIs – will be exempt from the leverage ratio requirements, but will still be required to report to APRA under ARS 110.1. Although still consulting on its final design, APRA is considering an eligibility threshold for the simplified framework of $15 billion in total assets, which will be complemented by other qualitative measures.

APRA is now proposing that revisions to the capital framework, initially outlined in February 2018, will come into effect from 1 January 2022, the internationally agreed implementation date set by the Basel Committee on Banking Supervision. APRA had originally proposed an implementation date of 1 January 2021, but is proposing to revise this based on industry concerns about the business impact of moving ahead of international competitors.

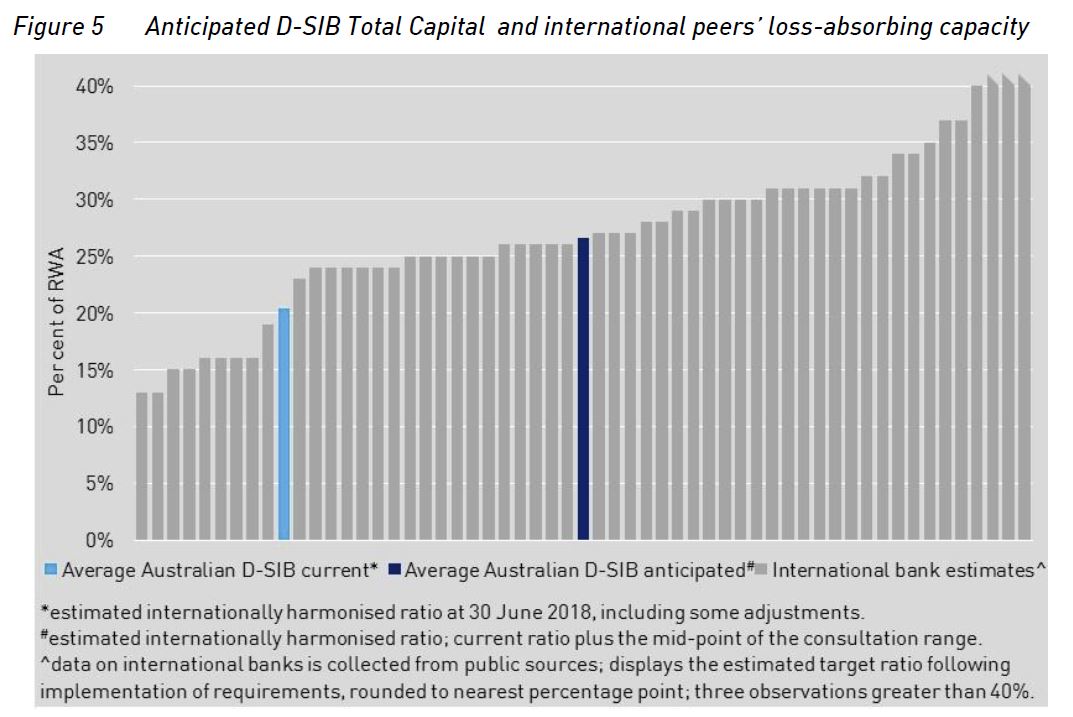

It shows that currently major Australian banks are at the lower end of Total Capital compared with international peers. As a result of proposed changes, major banks (Domestic systemically important banks in Australia, D-SIBs) will see their funding costs rise – incrementally over four years – by up to five basis points based on current pricing. This is intended to build in more financial resilience by lifting the capital requirements, centred on tier 2. Other banks may also be impacted to an extent.

If the D-SIBs were to maintain an additional four to five percentage points of Total Capital they would have ratios more in line with their international peers. But not in the top 25%, and the banks overseas are also lifting capital higher… so some tail chasing here! Is this “unquestionably strong”?

Under the proposals, each D-SIB would be required to maintain additional loss absorbency of between four and five percentage points of RWA. It is anticipated that each D-SIB’s Total Capital requirement would be adjusted by the same amount.

By way of background, the Australian Government’s 2014 Financial System Inquiry (FSI) recommended APRA implement a framework for loss absorbing and recapitalisation capacity in line with emerging international practice, sufficient to facilitate the orderly resolution of Australian ADIs and minimise taxpayer support (FSI Rec 3). The Government supported this recommendation in its response to the FSI.

APRA’s role is not to eliminate failure altogether, but to reduce its probability and impact. This role is set out in APRA’s statutory objectives under the Australian Prudential Regulation Authority Act 1998 and the Banking Act 1959, which require APRA to protect depositors and pursue financial system stability. In performing its functions, APRA will balance those objectives with the need for efficiency, competition, contestability and competitive neutrality in the financial system.

Disorderly failures are inconsistent with APRA’s objectives, as they are highly disruptive to depositors and have an adverse impact on financial system stability. Australia has not experienced a disorderly ADI failure in recent history, though the failure of HIH Insurance Limited (HIH) in 2001 provides an example of the adverse consequences of a disorderly failure of an APRA-regulated institution. In that instance, policyholders were severely affected and essential insurance services to the broader community became unavailable for a period of time.

Conversely, orderly resolution of an ADI would occur when a problem is identified and escalated early enough to allow APRA and other financial regulators to manage and respond in a manner that protects the interests of depositors, stabilises the ADI’s critical functions and promotes financial stability. Achieving an orderly resolution does not necessarily mean a crisis is averted, rather the manner in which an ADI’s failure is managed would result in better outcomes given the circumstances.

APRA’s statutory powers were recently strengthened by the passage of the Financial Sector Legislation Amendment (Crisis Resolution Powers and Other Measures) Act 2018.

The effectiveness of resolution planning will be a focus for APRA over the coming years. APRA is in the process of developing a formalised framework for resolution planning and will consult further on this in 2019.

The proposals in this discussion paper focus on the availability of financial resources to support orderly resolution.

These proposals would ensure ADIs have adequate financial resources available to support orderly resolution in the highly unlikely event of failure. This will be achieved by adjusting, where appropriate, an ADI’s Total Capital requirement.

These proposals are distinct from APRA’s work on ensuring ADI capital levels are ‘unquestionably strong’, which relates to the ongoing resilience of institutions and is in response to a separate FSI recommendation (FSI Rec 1).

APRA is proposing an approach on loss-absorbing capacity that is simple, flexible and designed with the distinctive features of the Australian financial system in mind, and has been developed in collaboration with the other members of the Council of Financial Regulators. The key features of the proposals include:

for the four major banks – increasing Total Capital requirements by four to five percentage points of risk-weighted assets

for other ADIs – likely no adjustment, although a small number may be required to maintain additional Total Capital depending on the outcome of resolution planning, which would inform the appropriate amount of additional loss absorbency required to achieve orderly resolution. This assessment would occur on an institution-by-institution basis.

Tier 2 capital instruments are designed to convert to ordinary shares or be written off at the point of non-viability, which means they will be available to absorb losses and can be used to facilitate resolution actions. Tier 2 capital instruments have been a feature of ADI capital structures in various forms since being introduced as part of the 1988 Basel Accord. These instruments have been used as part of resolution actions in other jurisdictions, supporting orderly outcomes.

It is also important that holders of instruments which are intended to be converted or written off in resolution understand the distinctive risks of these investments. In the context of AT1 instruments, APRA has noted that it is inadvisable for investors to view such instruments as higher-yielding fixed-interest investments, without understanding the loss-absorbing role they play in a resolution.15 In the case of the Australian ADIs’ Tier 2 capital instruments, these are mostly issued to institutional investors, who are likely to understand the risks involved.

As ADIs will be able to use any form of capital to meet increased Total Capital requirements, APRA anticipates the bulk of additional capital raised will be in the form of Tier 2 capital. The proposed changes are expected to marginally increase each major bank’s cost of funding – incrementally over four years – by up to five basis points based on current pricing. This is not expected to have an immediate or material effect on lending rates.

APRA proposes that the increased requirements will take full effect from 2023, following relevant ADIs being notified of adjustments to Total Capital requirements from 2019.

In addition to the proposals outlined in this discussion paper, APRA intends to consult on a framework for recovery and resolution in 2019, which will include further details on resolution planning.

APRA Chairman Wayne Byres said one of APRA’s core functions as Australia’s prudential regulator is to plan for, and if required, execute the orderly resolution of the financial institutions it regulates.

“The resilience of the Australian banking system continues to improve, underpinned by the build-up of capital over the last decade.

“However, no matter how resilient financial institutions are, the possibility of failure cannot be entirely removed. Therefore, in addition to strengthening the resilience of the financial system, it is prudent to plan for the unlikely event of failure.

“The events of the global financial crisis demonstrated the impact that failures can have on the broader financial system and the subsequent social and economic consequences.

“The aim of these proposals and resolution planning more broadly is to ensure that the failure of a financial institutions can be resolved in an orderly fashion, which protects the interests of beneficiaries and minimises disruption to the financial system,” Mr Byres said.