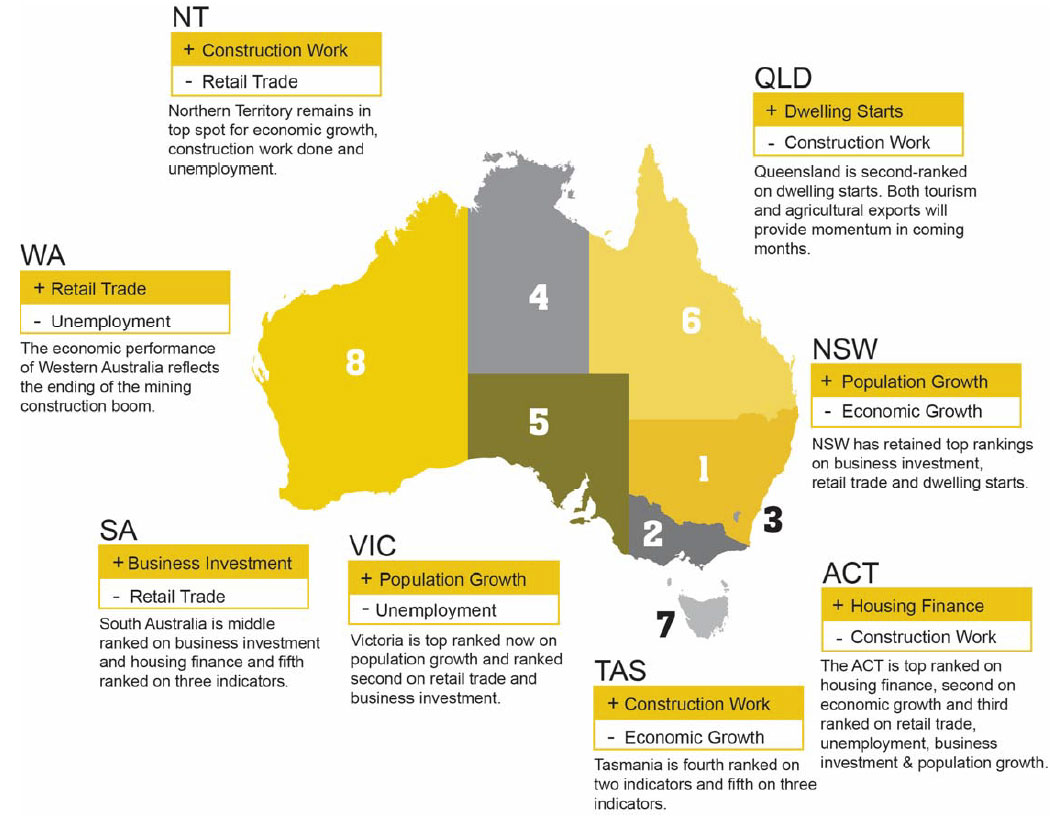

The latest CommSec State of The States report has been released. NSW has held on to the position as the best performing economy, supported by strong construction activity, whilst the economic performance of Western Australia reflects the ending of the mining construction boom.

The states performing better are associated strongly with rising residential construction, home prices and home loan volumes.

Each quarter CommSec attempts to find out by analysing eight key indicators: economic growth; retail spending; business investment; unemployment; construction work done; population growth; housing finance and dwelling commencements.

Just as the Reserve Bank uses long-term averages to determine the level of ‘normal’ interest rates; we have done the same with key economic indicators. For each state and territory, latest readings for the key indicators were compared with decade averages – that is, against the ‘normal’ performance.

The latest State of the States report also includes a section comparing annual growth rates for the eight key indicators across the states and territories as well as Australia as a whole. This enables another point of comparison – in terms of economic momentum.

NSW has retained its top rankings on business investment, retail trade, and dwelling starts. But NSW is now is second spot on unemployment, construction work, population growth and housing finance. NSW is in third spot on economic growth.

Victoria remains in second spot on the economic performance rankings. Victoria is top ranked now on population growth and ranked second on retail trade and business investment. Victoria is third ranked on construction work, housing finance and dwelling starts.

The ACT also has held on to its position as the third ranked economy. The ACT is top ranked on housing finance, second on economic growth and third ranked on retail trade, unemployment, business investment and population growth. Retail trade is up 5.1 per cent on a year ago.

The Northern Territory holds fourth position and remains in top spot for economic growth, construction work done and unemployment. However the Territory economy is losing momentum, ranked last on four indicators – population growth, business investment, housing finance and retail trade.

The South Australian economy is in fifth position. South Australia is middle ranked on business investment and housing finance and fifth ranked on three indicators.

Queensland is in sixth placeon the economic performance rankings. The economy is second-ranked on dwelling starts and population growth is lifting. Both tourism and agricultural exports will provide momentum in coming months and higher coal prices are encouraging.

Tasmania has improved from eighth position to seventh on the rankings. Tasmania is fourth ranked on two indicators and fifth on three indicators. Annual growth on home lending is strongest in the nation at 10.3 per cent.

The economic performance of Western Australia reflects the ending of the mining construction boom. But income levels will lift in line with record mining export volumes and the recent improvement in resource prices.