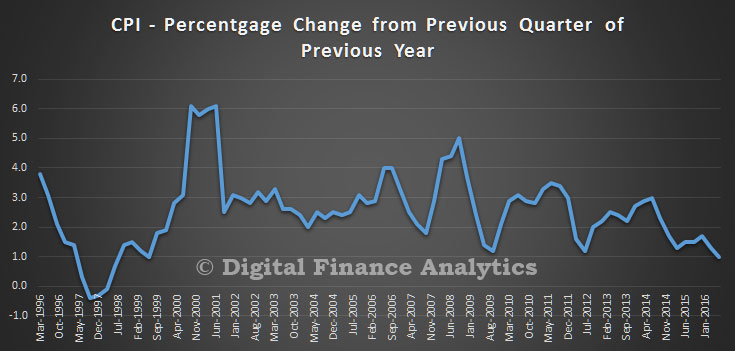

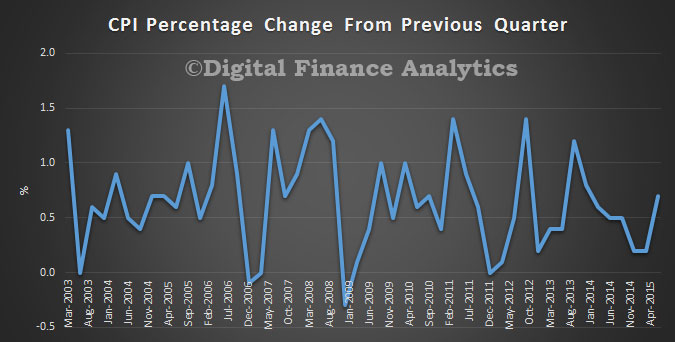

The Consumer Price Index (CPI) rose 0.5 per cent in the December quarter 2016, according to the latest Australian Bureau of Statistics (ABS) figures.

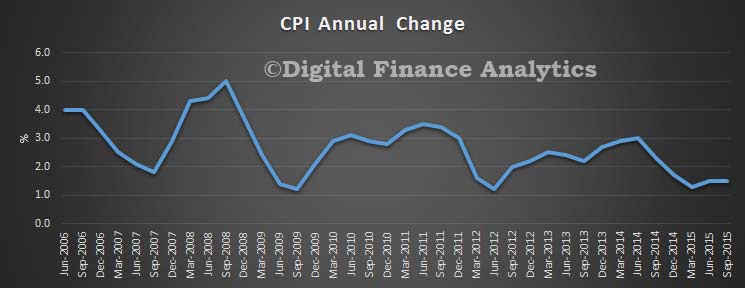

This follows a rise of 0.7 per cent in the September quarter 2016. The CPI rose 1.5 per cent through the year to December quarter 2016.

This was below expectation, but is probably not sufficiently low to prompt the RBA to cut the cash rate further, given recent comments from the Governor, and rising trends in other countries, following the US election.

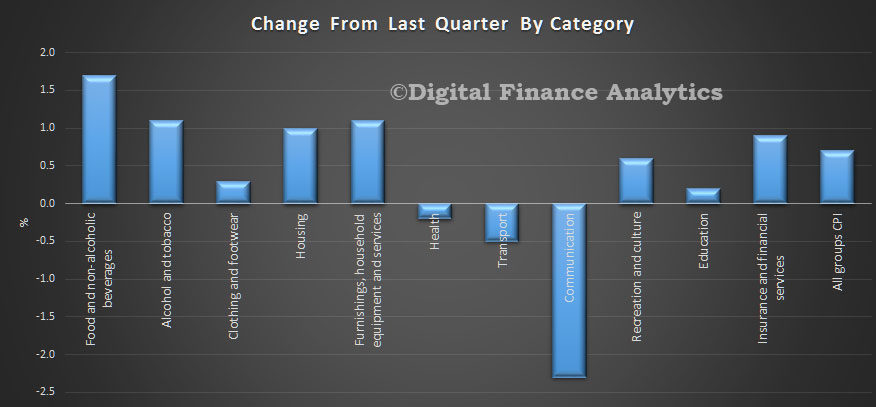

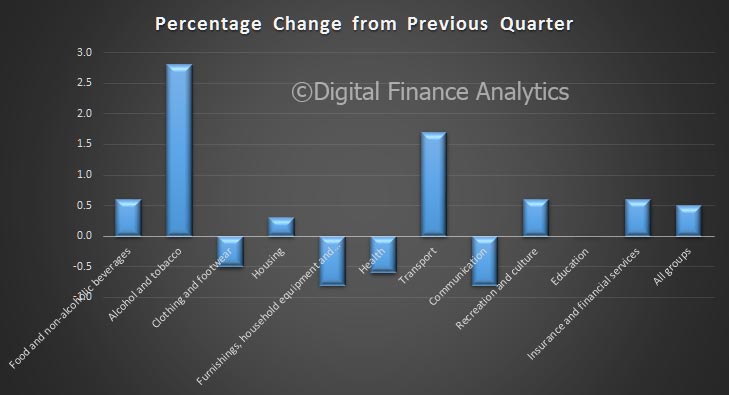

The most significant price rises this quarter are tobacco (+7.4 per cent), automotive fuel (+6.7 per cent) and restaurant meals (+1.1 per cent). These rises are partially offset by falls in furnishings, household equipment and services (-0.8 per cent) and communication (-0.8 per cent).

The most significant price rises this quarter are tobacco (+7.4 per cent), automotive fuel (+6.7 per cent) and restaurant meals (+1.1 per cent). These rises are partially offset by falls in furnishings, household equipment and services (-0.8 per cent) and communication (-0.8 per cent).

Vegetables rose 2.5 per cent in the December quarter 2016. Adverse weather conditions in major growing areas over previous periods continue to impact supply for particular vegetables (potatoes, capsicums, broccoli and cauliflower). Offsetting these rises are price falls for salad vegetables, tomatoes, lettuce and celery.

Vegetable prices have risen 12.5 per cent through the year to December quarter 2016.

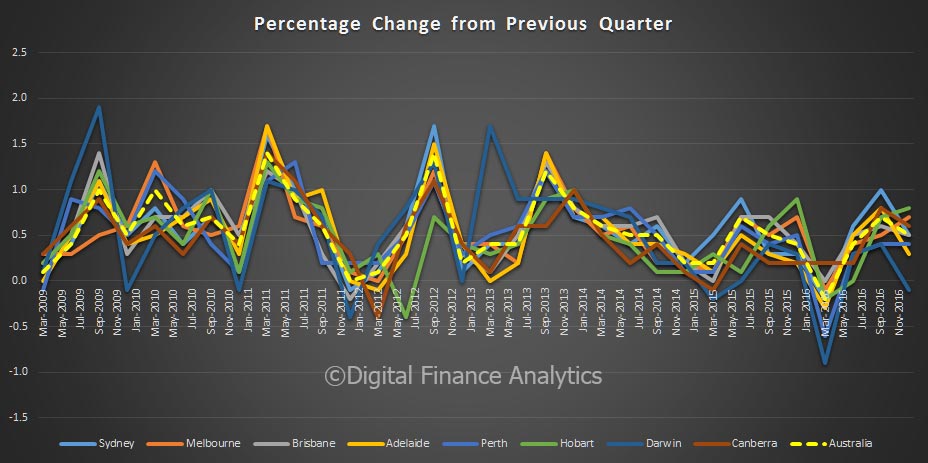

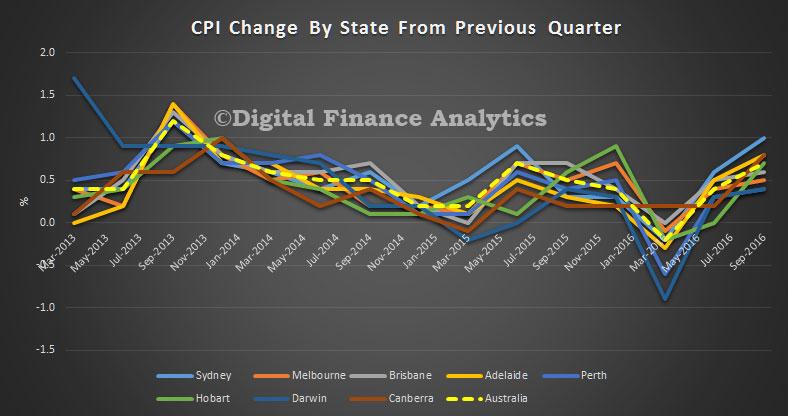

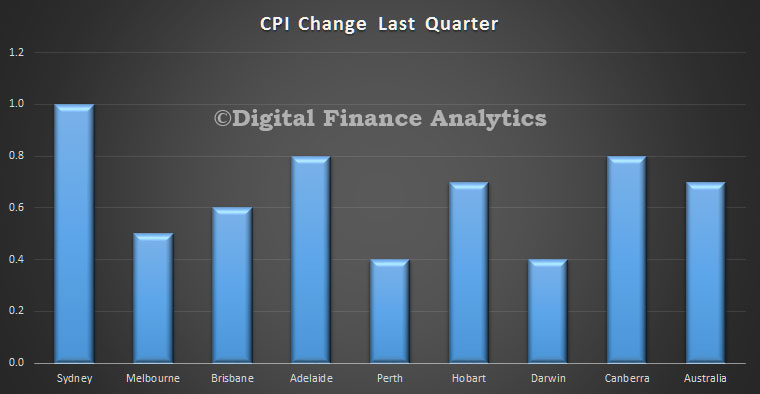

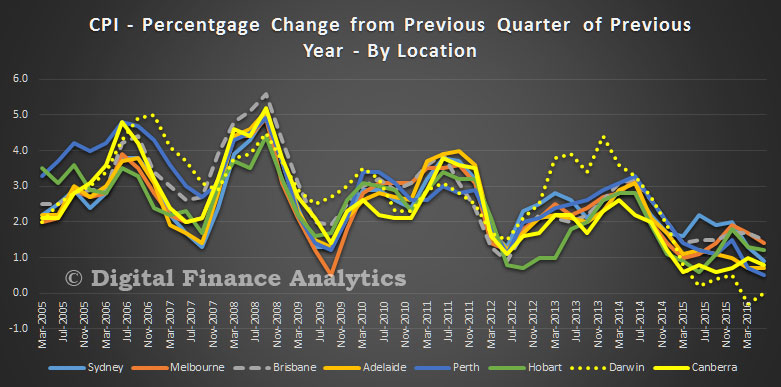

CPI fell in Darwin, and was highest in Hobart in the quarter.