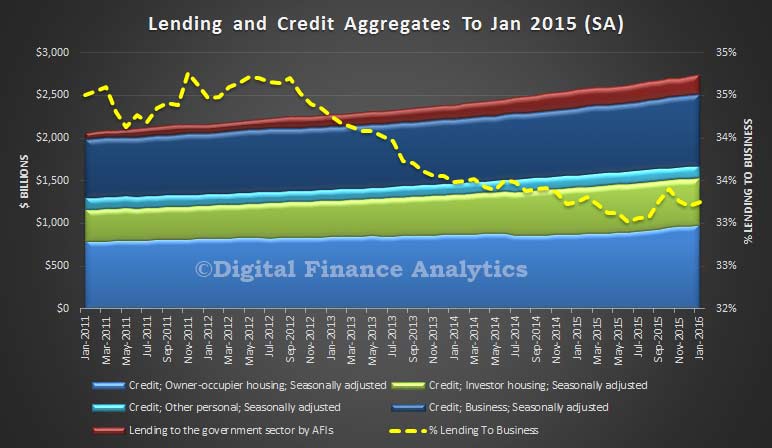

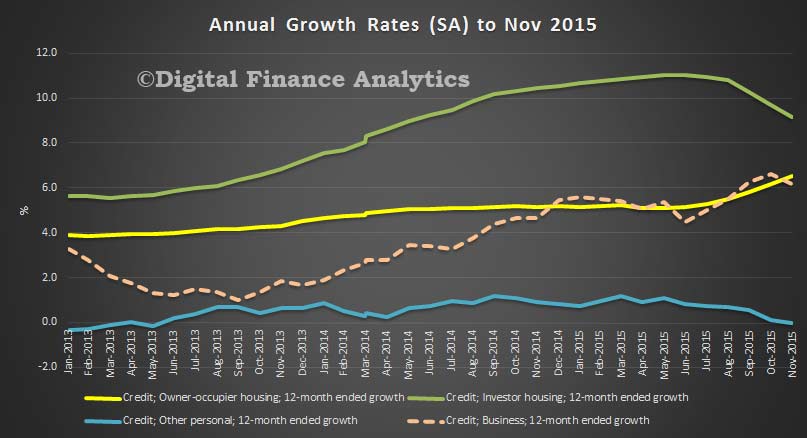

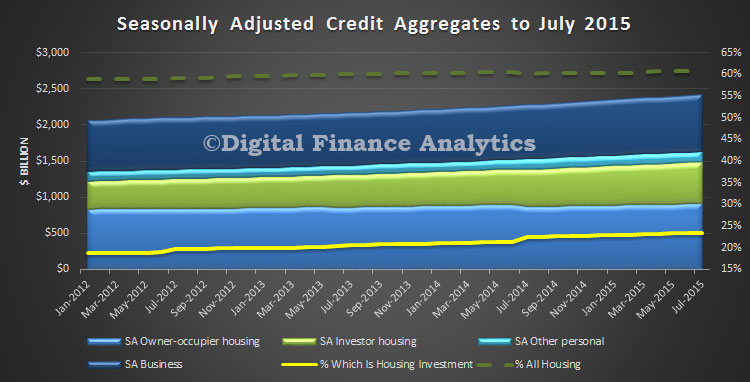

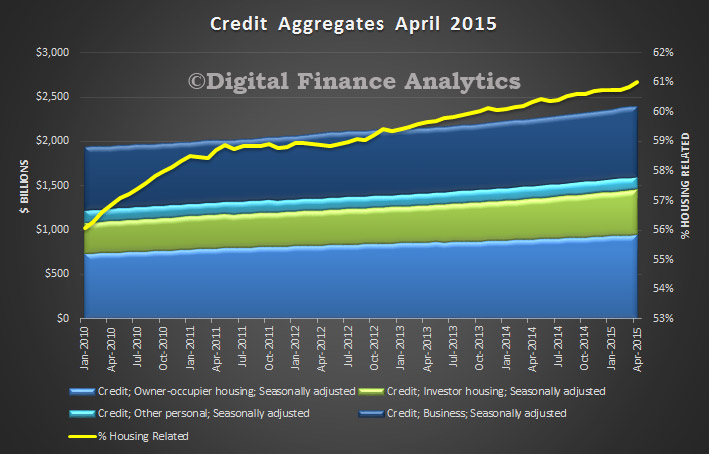

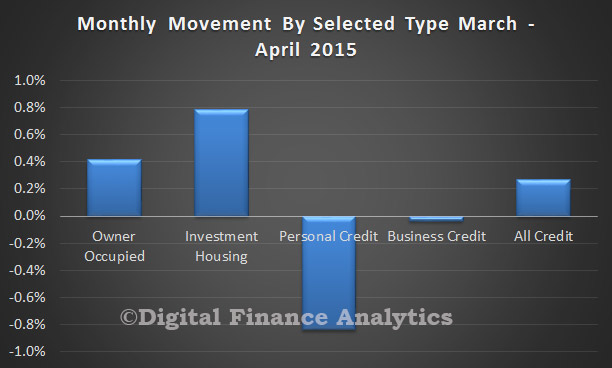

The RBA released their credit aggregates to end March today. Housing lending grew 0.5% in March and reflects an annual rate of 7.2% – well above inflation! Business credit grew by 0.3% or $2.6 billion (annualised 6.5%) and personal credit fell 0.3% or $0.6 billion, and represents an annualised fall of 1%. We are still not seeing real relative growth in the important business investment sector.

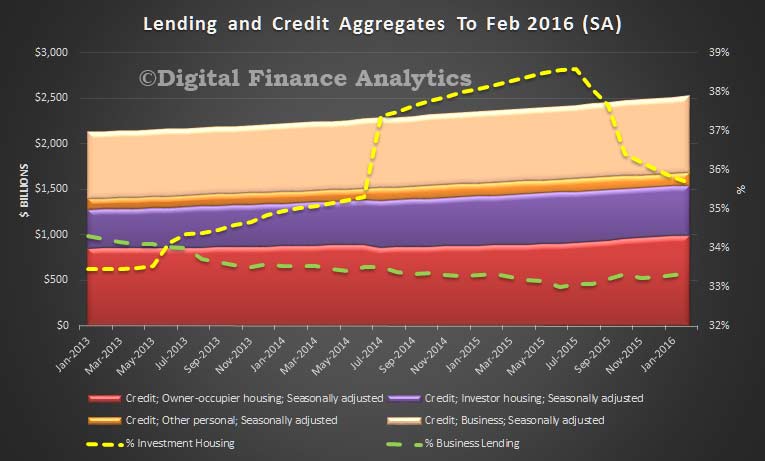

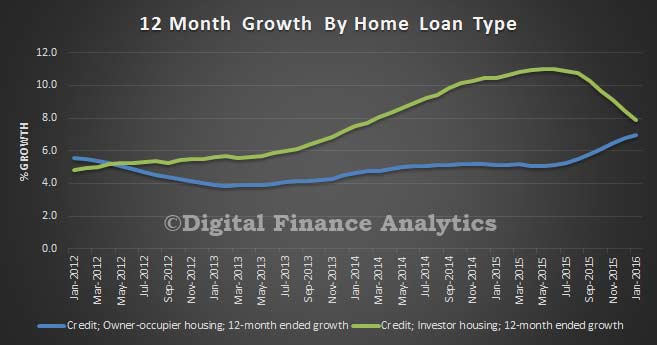

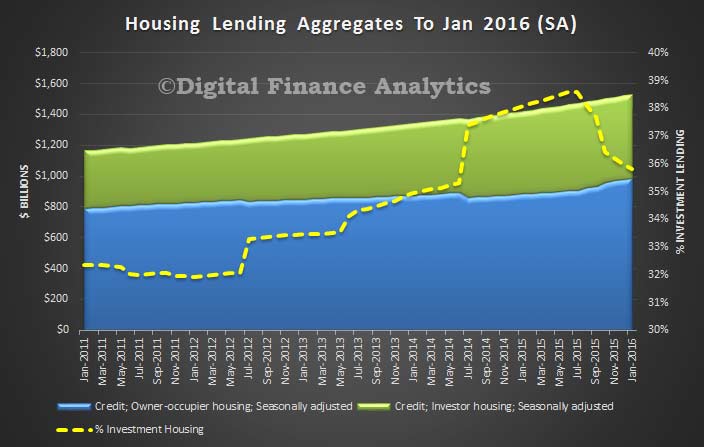

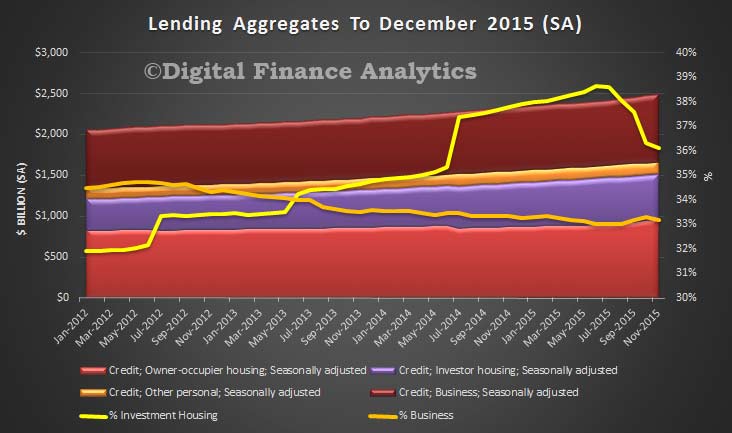

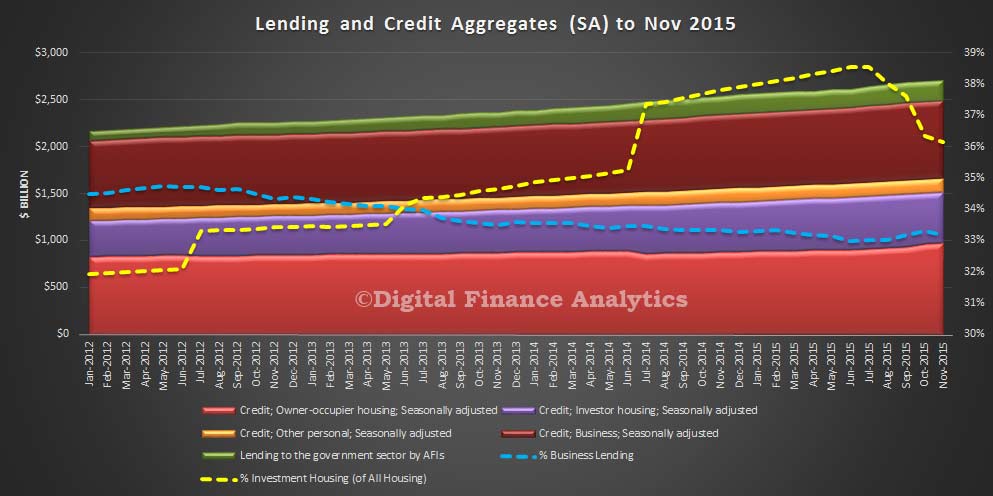

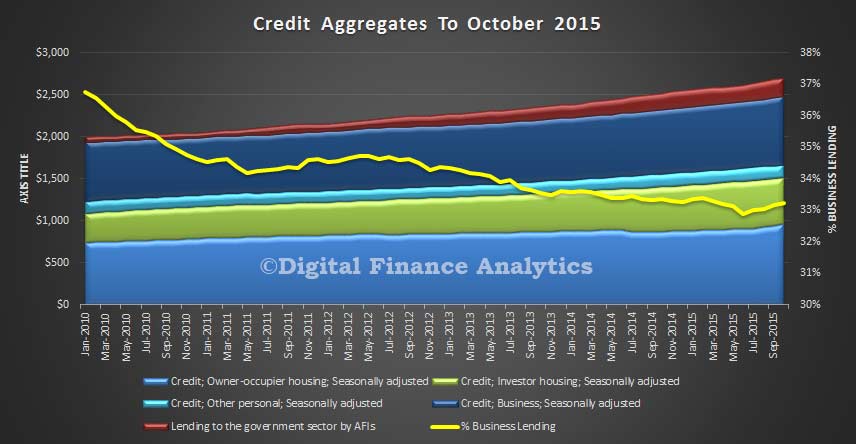

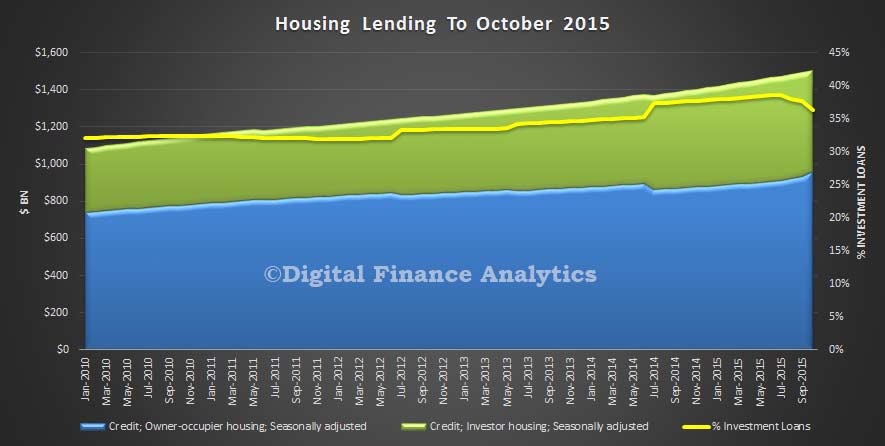

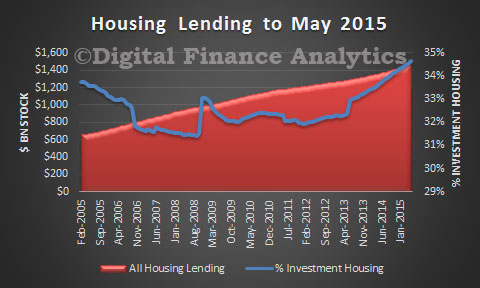

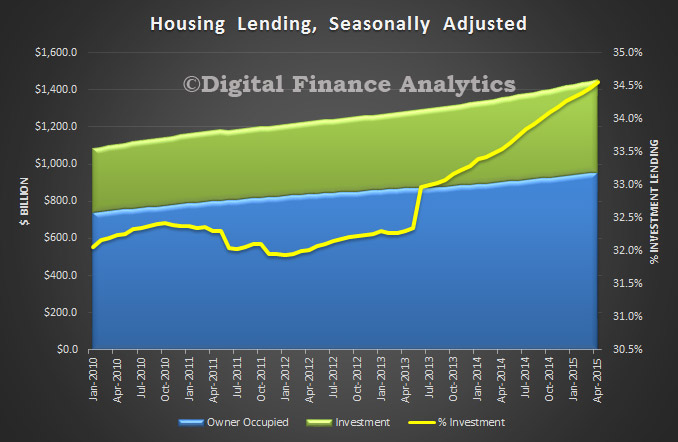

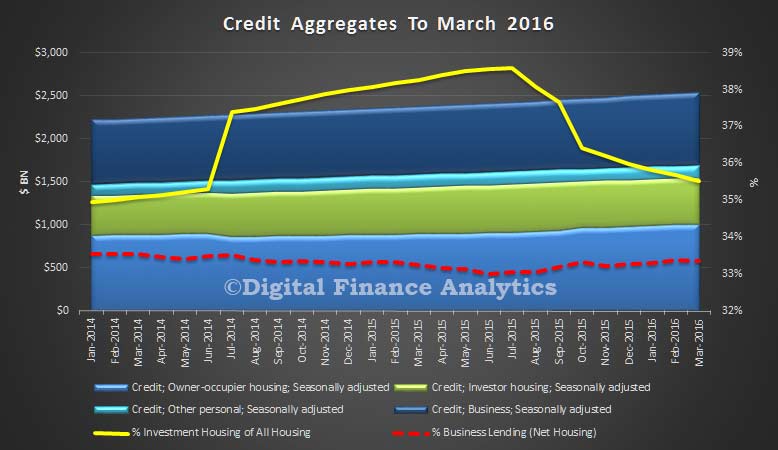

So, housing momentum is driving banks lending books. Seasonally adjusted lending for owner occupation grew 0.76%, or $7.5 billion, whilst lending for investment homes grew just 0.08%. Total growth was 0.5% or $7.7 billion to a new record of $1,547.6 billion. One third of loans are for investment purposes, though there is still some movement and reclassification. The RBA says:

So, housing momentum is driving banks lending books. Seasonally adjusted lending for owner occupation grew 0.76%, or $7.5 billion, whilst lending for investment homes grew just 0.08%. Total growth was 0.5% or $7.7 billion to a new record of $1,547.6 billion. One third of loans are for investment purposes, though there is still some movement and reclassification. The RBA says:

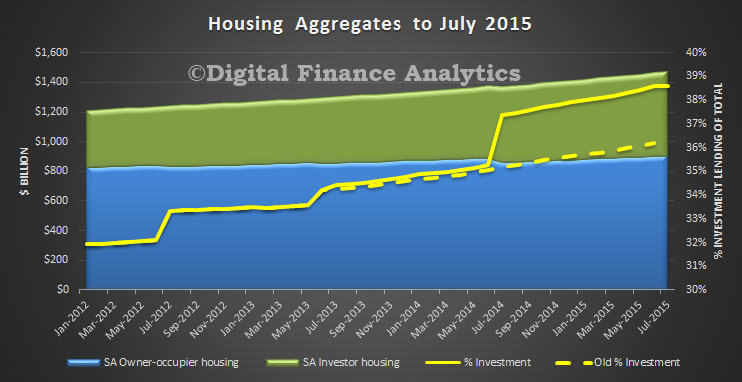

Following the introduction of an interest rate differential between housing loans to investors and owner-occupiers in mid-2015, a number of borrowers have changed the purpose of their existing loan; the net value of switching of loan purpose from investor to owner-occupier is estimated to have been $39 billion over the period of July 2015 to March 2016 of which $1.5 billion occurred in March. These changes are reflected in the level of owner-occupier and investor credit outstanding. However, growth rates for these series have been adjusted to remove the effect of loan purpose changes.

Such strong growth in home lending will make the RBA pause for thought before they cut the cash rate again – household debt continues to sky rocket, at a time when incomes are static. Not a good formula for enduring financial stability. Cutting rates will have little impact on personal credit (which is still falling) or business borrowing (driven more by confidence and future prospective growth). This should temper the knee-jerk calls for a cut following the lower than expected inflation number earlier in the week.

We will post separately on the APRA numbers, also released today.