We discuss the latest data from our household surveys.

CONTENTS 0:00 Start 0:31 Introduction 1:00 Overall Index 2:10 Property Segments 3:30 By States 4:20 By Age Bands 6:15 Wealth Segments 7:11 Job Security 7:56 Income 8:30 Costs Of Living 9:45 Savings 10:57 Debt 12:40 Net Worth 14:24 Other Indices 18:25 Conclusions 20:09 Outro

Go to the Walk The World Universe at https://walktheworld.com.au/

Digital Finance Analytics (DFA) Blog

Household Financial Confidence On The Improve [Podcast]

We discuss the latest data from our household surveys.

CONTENTS 0:00 Start 0:31 Introduction 1:00 Overall Index 2:10 Property Segments 3:30 By States 4:20 By Age Bands 6:15 Wealth Segments 7:11 Job Security 7:56 Income 8:30 Costs Of Living 9:45 Savings 10:57 Debt 12:40 Net Worth 14:24 Other Indices 18:25 Conclusions 20:09 Outro

Go to the Walk The World Universe at https://walktheworld.com.au/

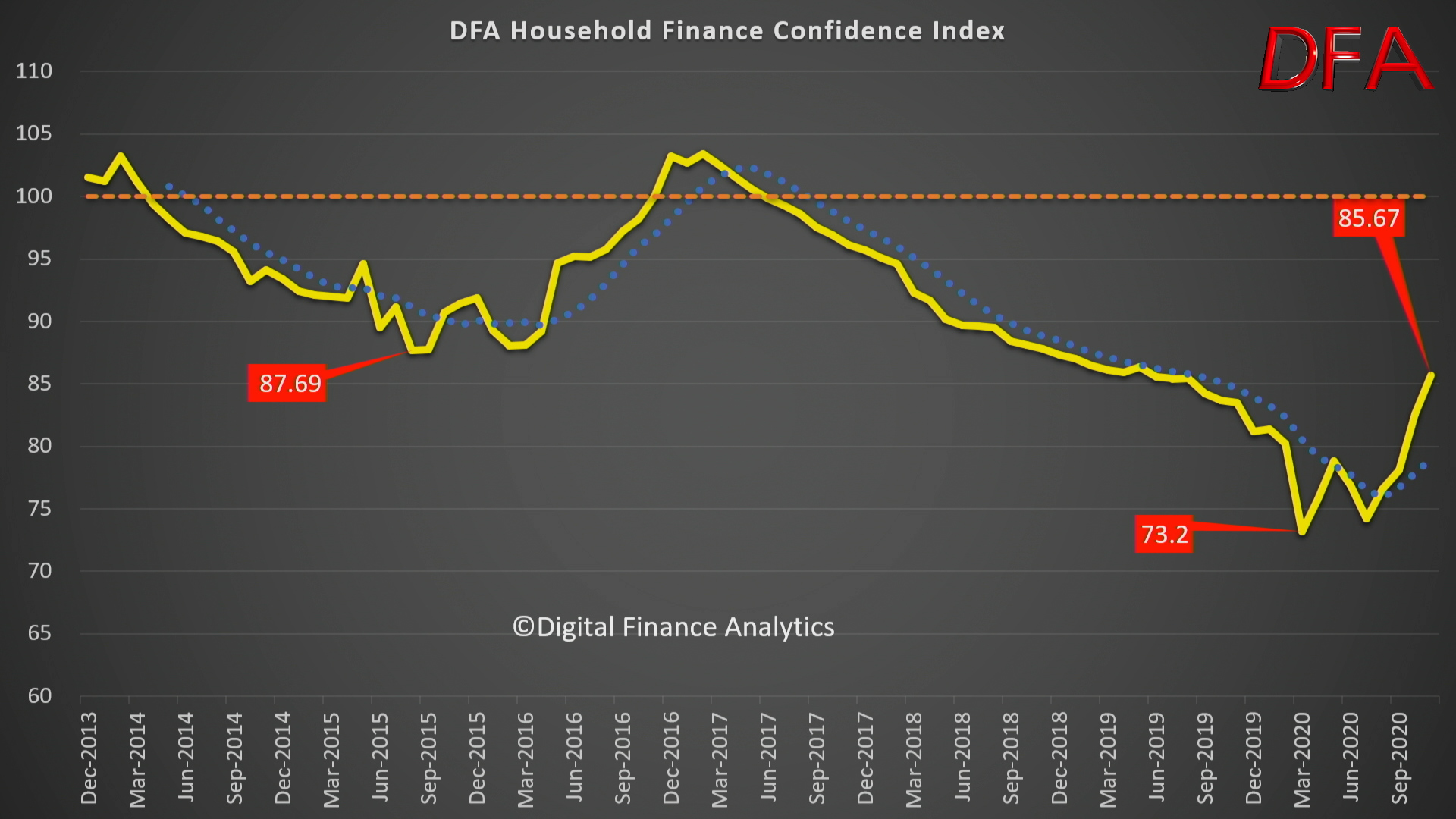

We have released the latest update to our Financial Confidence index, with data to 20th October 2020, later than usual, because we wanted to see if there was a post-budget bounce (as trumpeted by one index provider last week!).

We discussed the findings in our most recent live show:

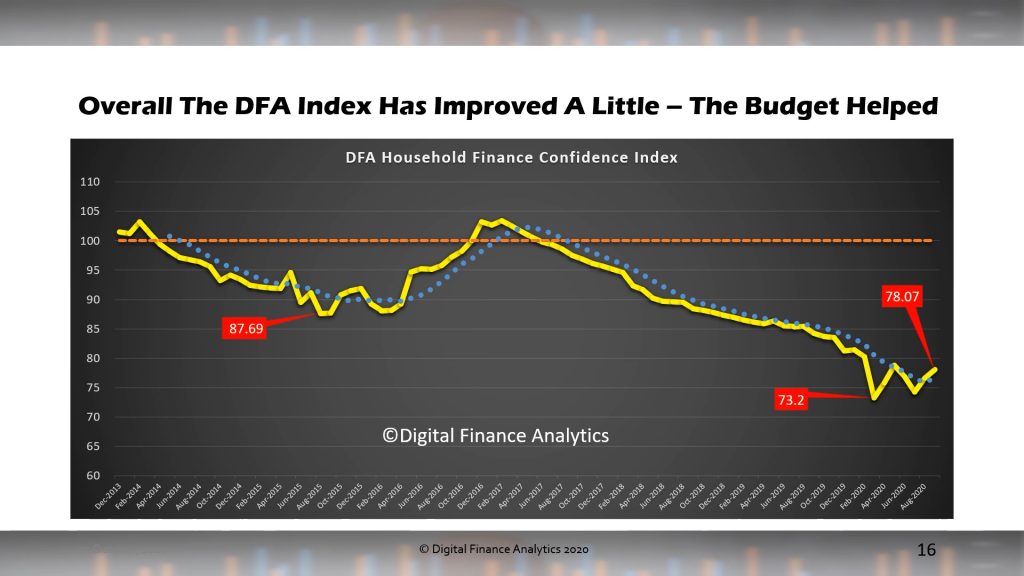

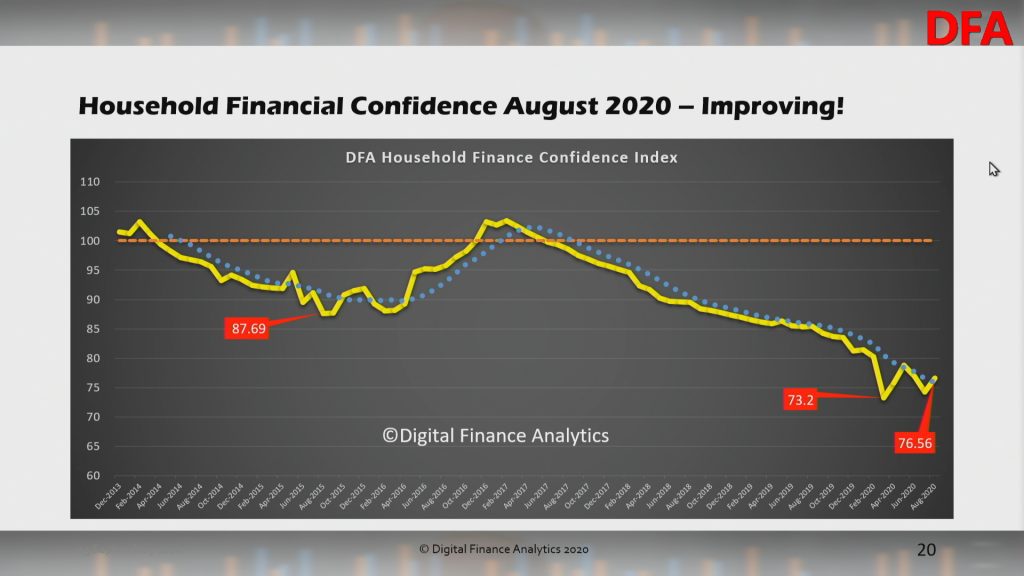

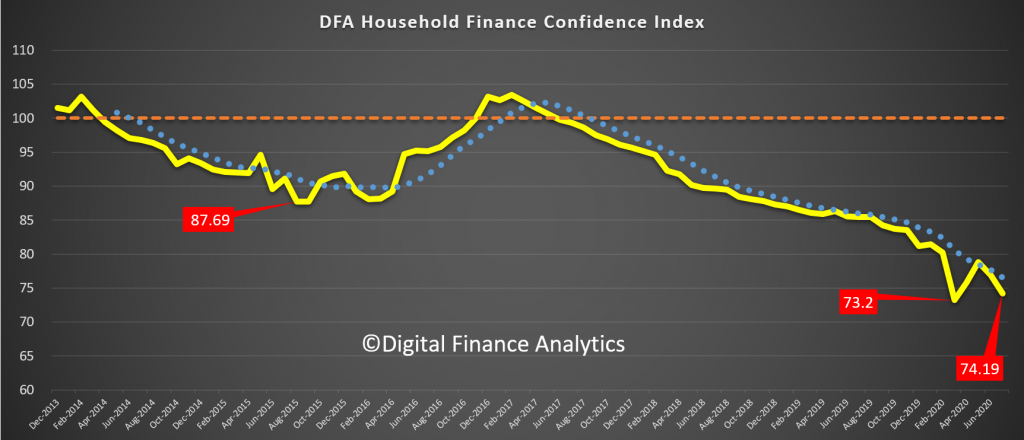

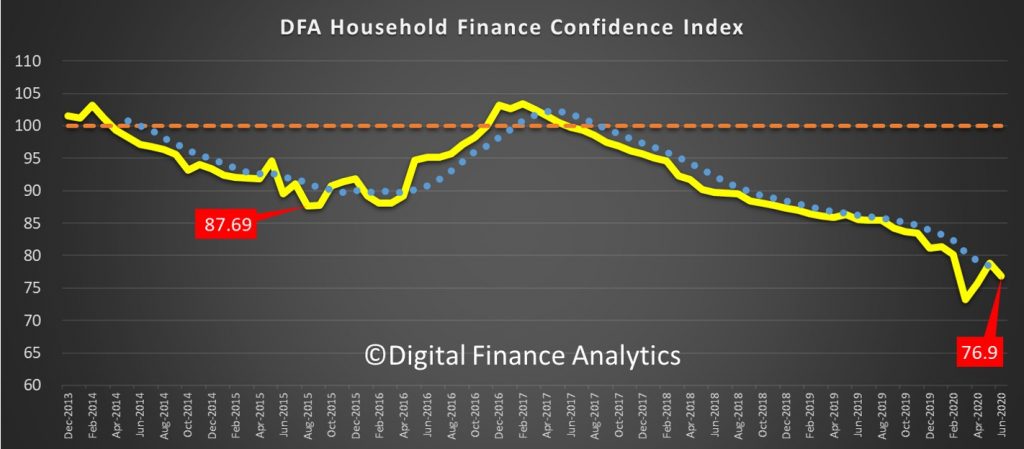

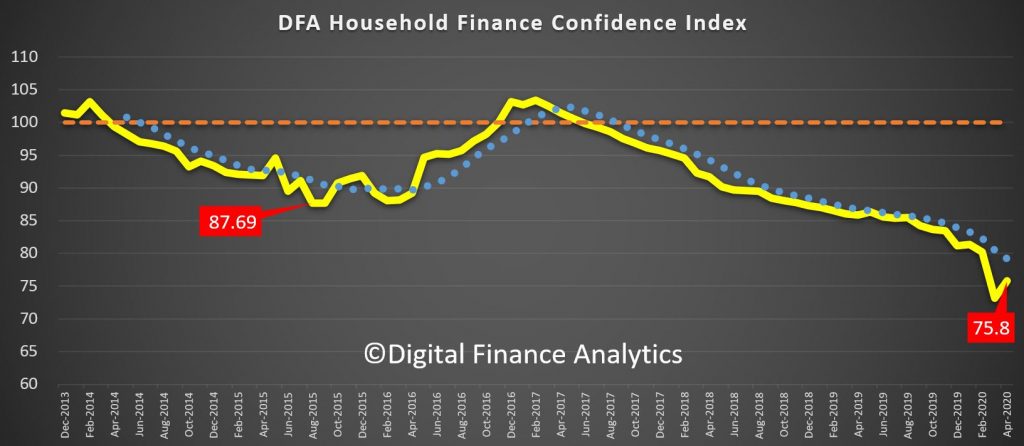

There was a slight recovery, but nothing which takes our index out of the “gloom” zone. The latest reading is 78.07 still well below the neutral setting.

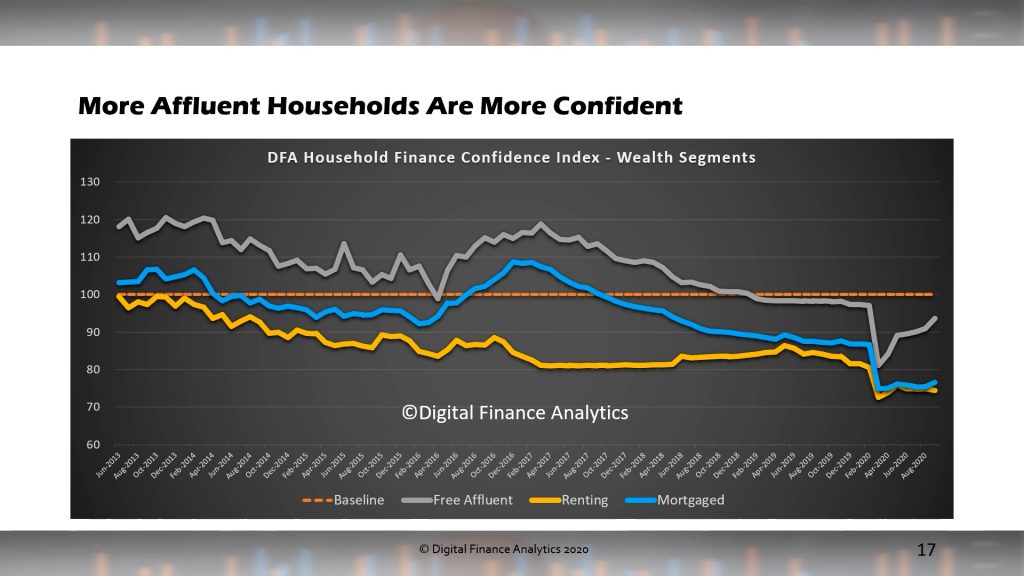

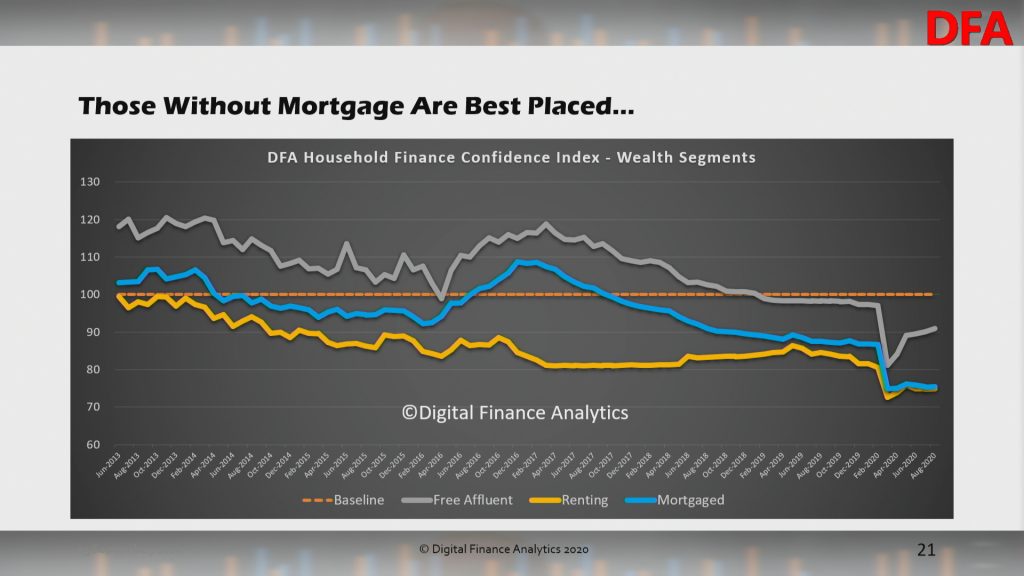

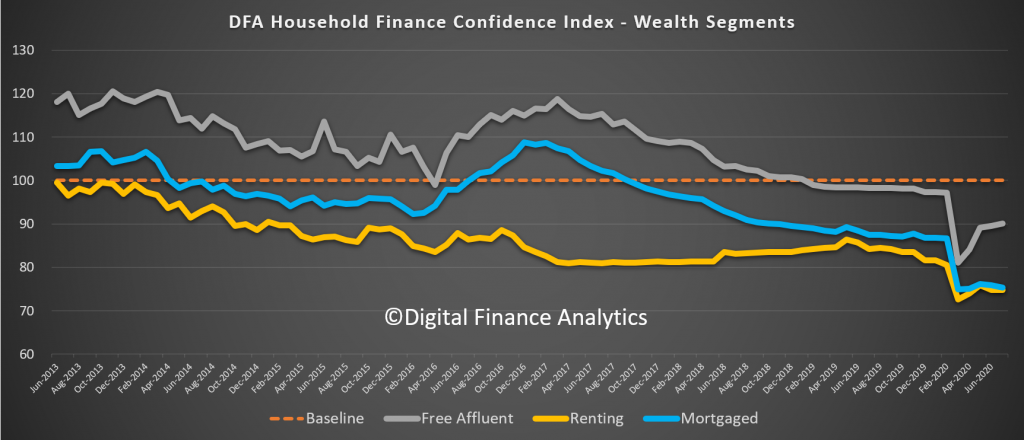

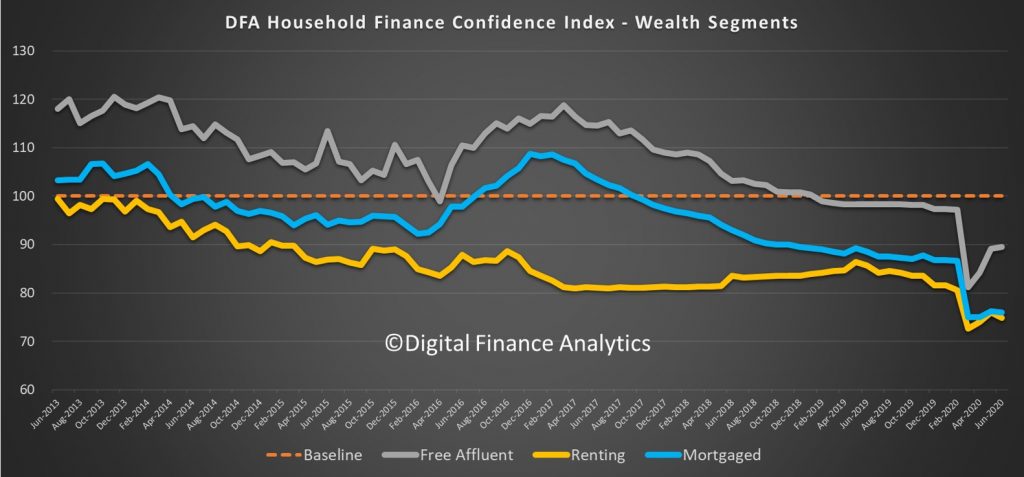

By our affluence segmentation, those mortgage free, and holding market investments improved as markets improved, while those with mortgages and those renting saw little change.

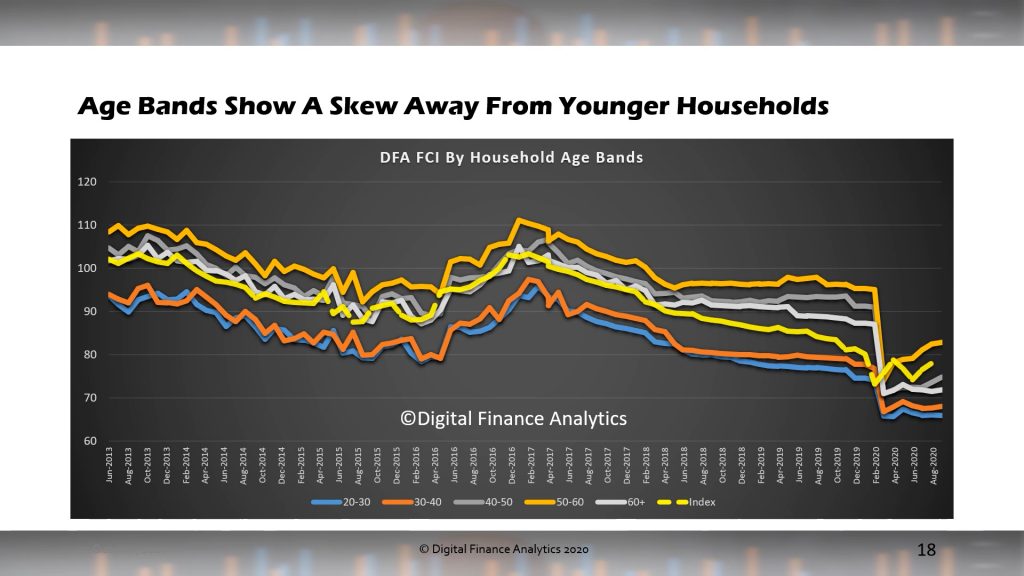

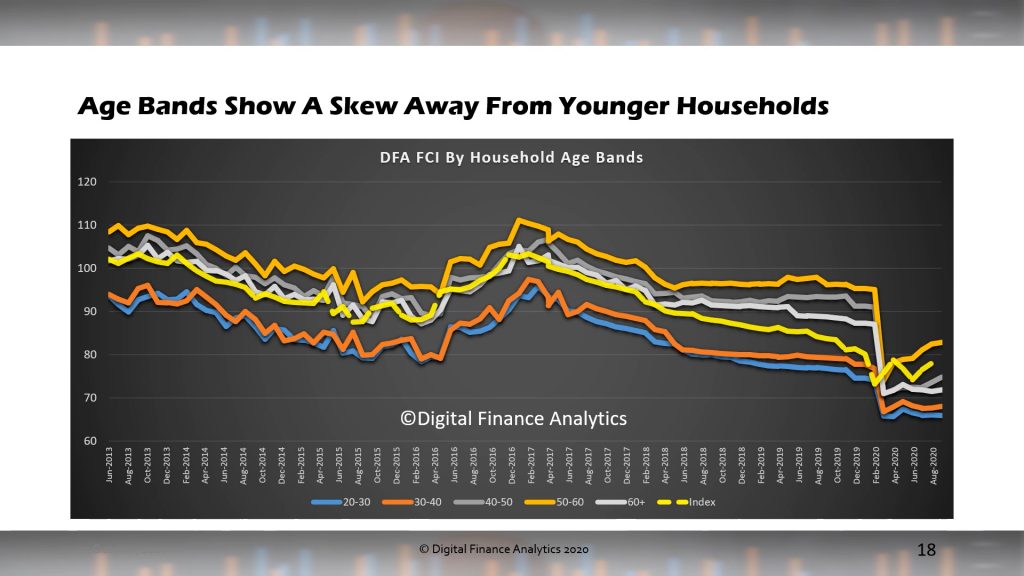

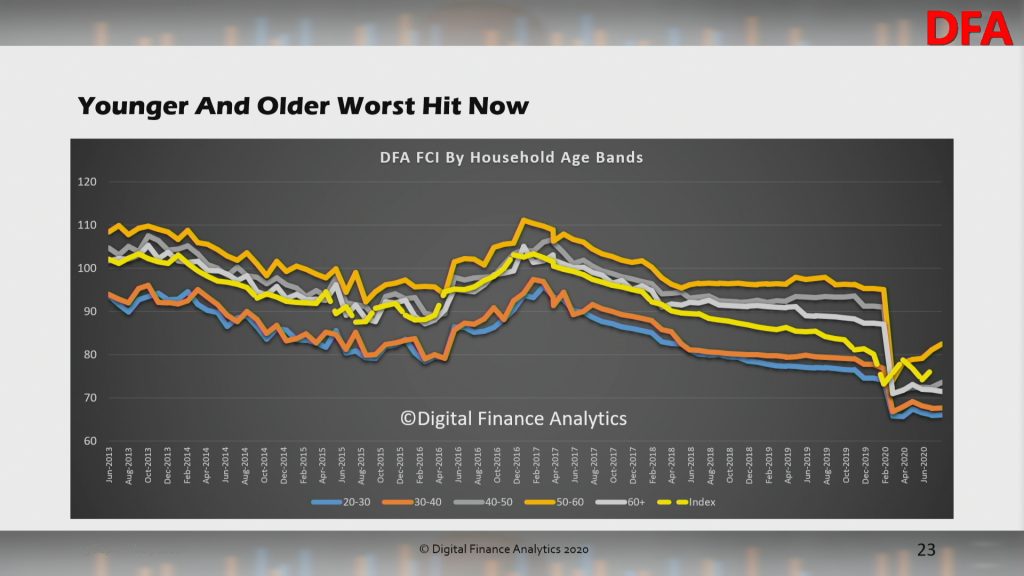

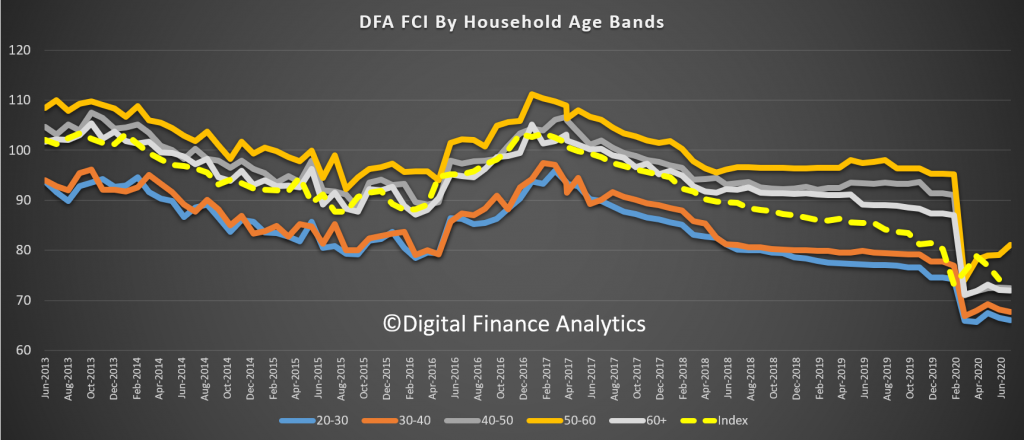

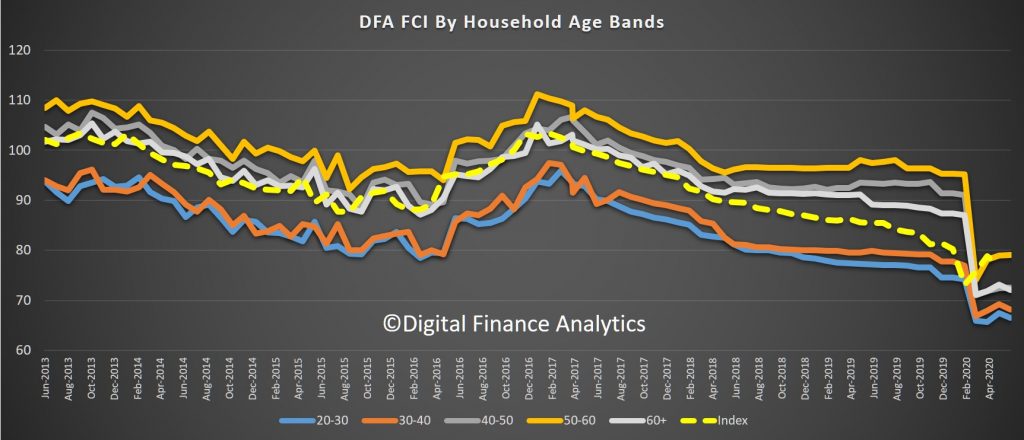

Across the age groups, younger households were least confident, reflecting fragmented jobs and incomes, and high leverage. Older households, especially those mortgage free were more positive, but older groups, reliant on bank savings also remain in gloom territory.

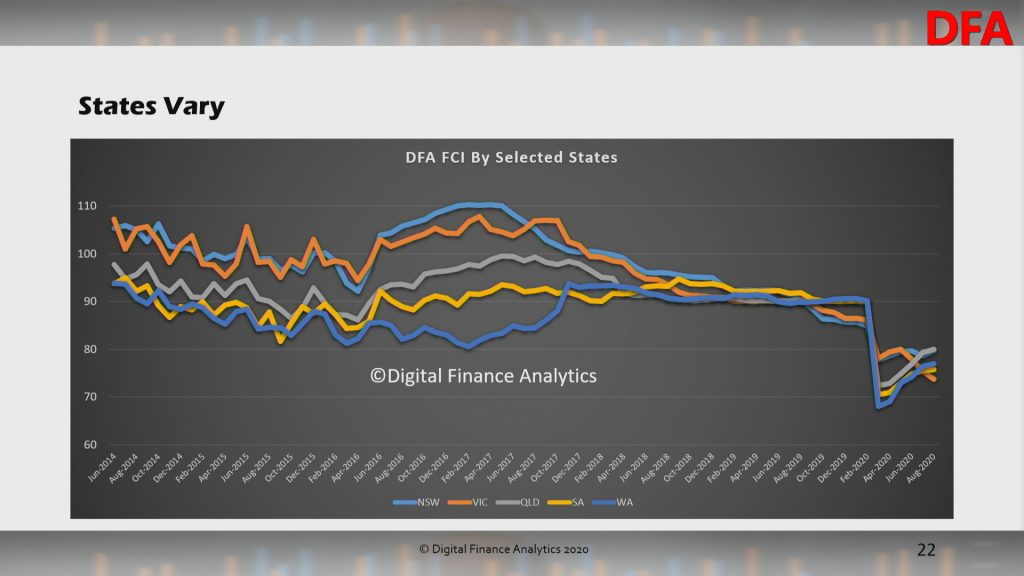

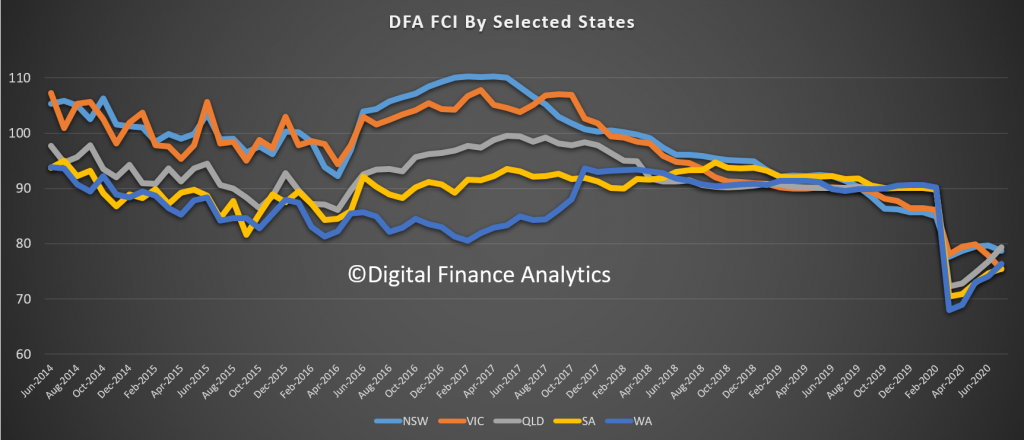

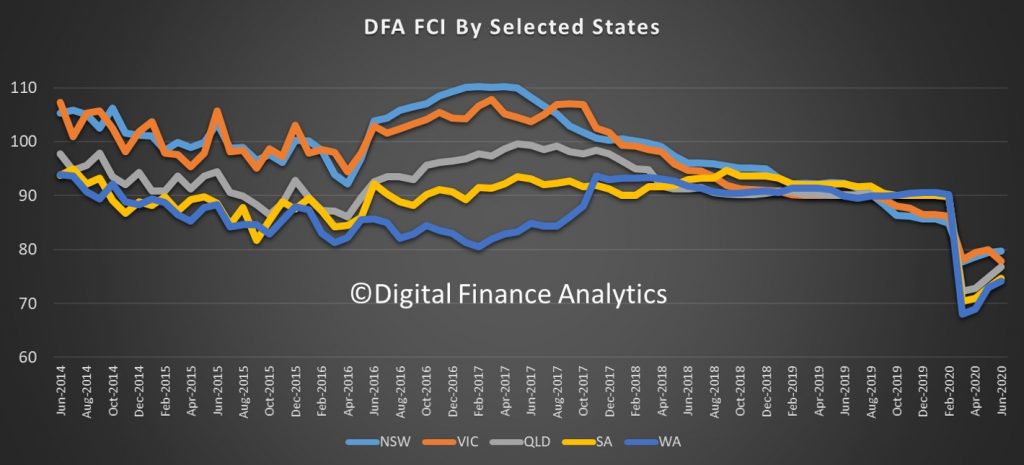

Across the states, Victoria showed a further slide (this may change if the lock-down is relaxed as anticipated), whereas WA continues to move higher, as the local economy recovers.

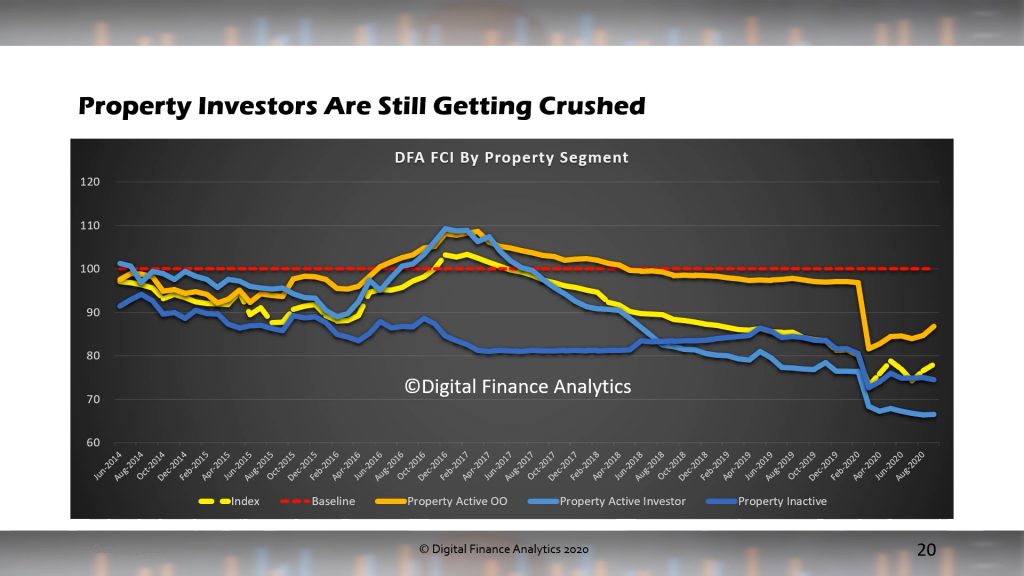

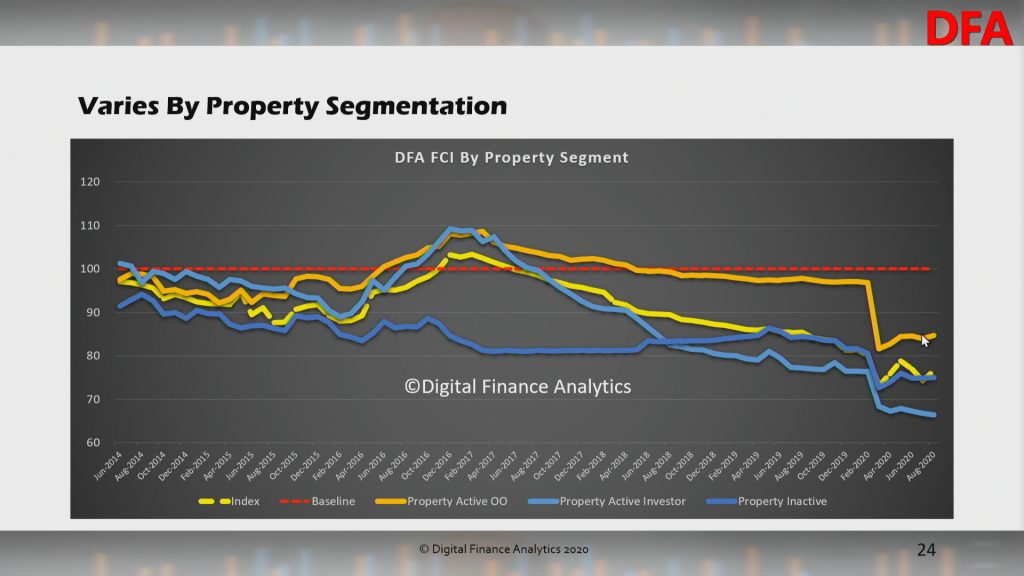

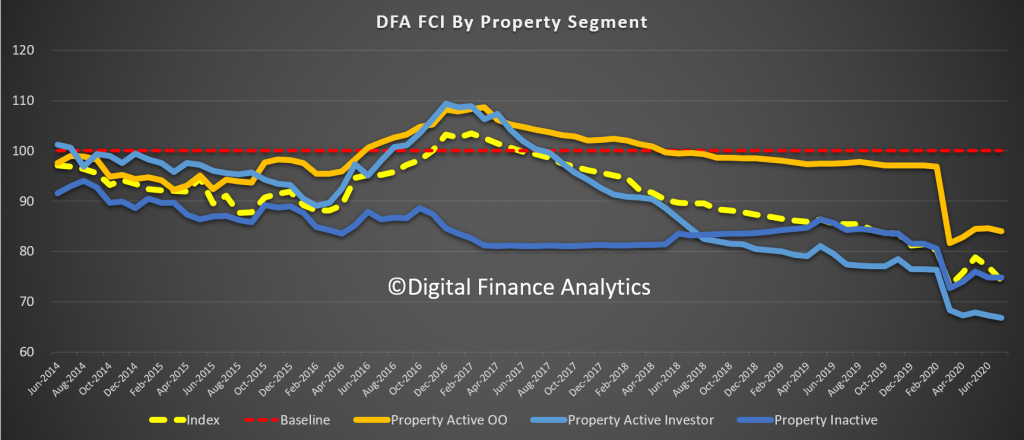

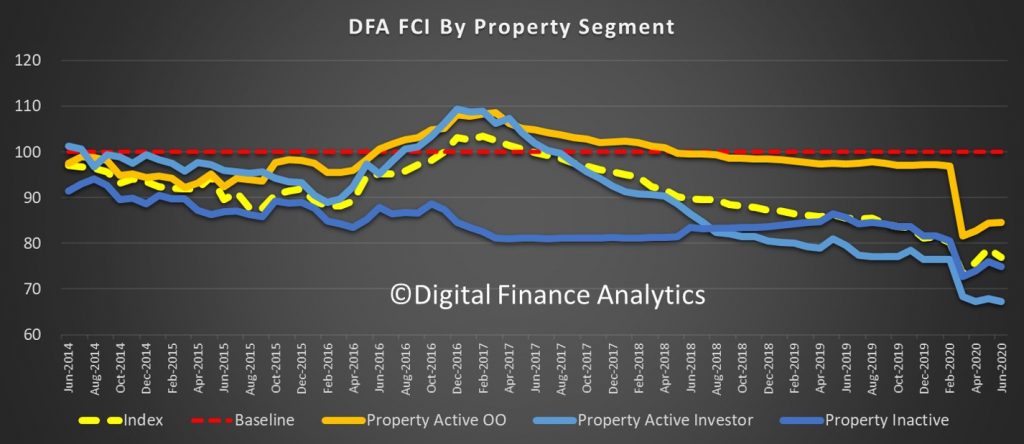

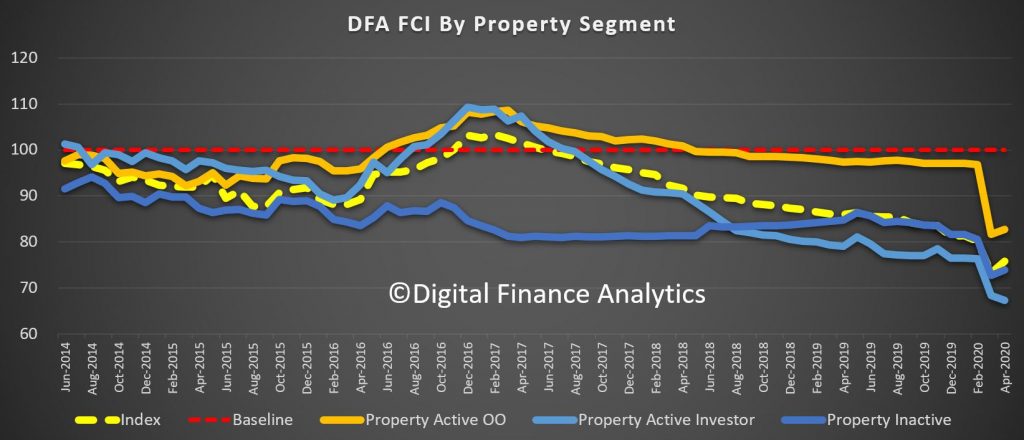

Across the property segments, property investors continue to languish, thanks to lower rental returns, higher vacancy rates and limited capital growth. Owner occupied households benefited from lower rates, and refinance, while those renting benefited from higher availability and lower rents (though some are confronting risks of being forced to leave due to investors wanting to sell, or to give notice).

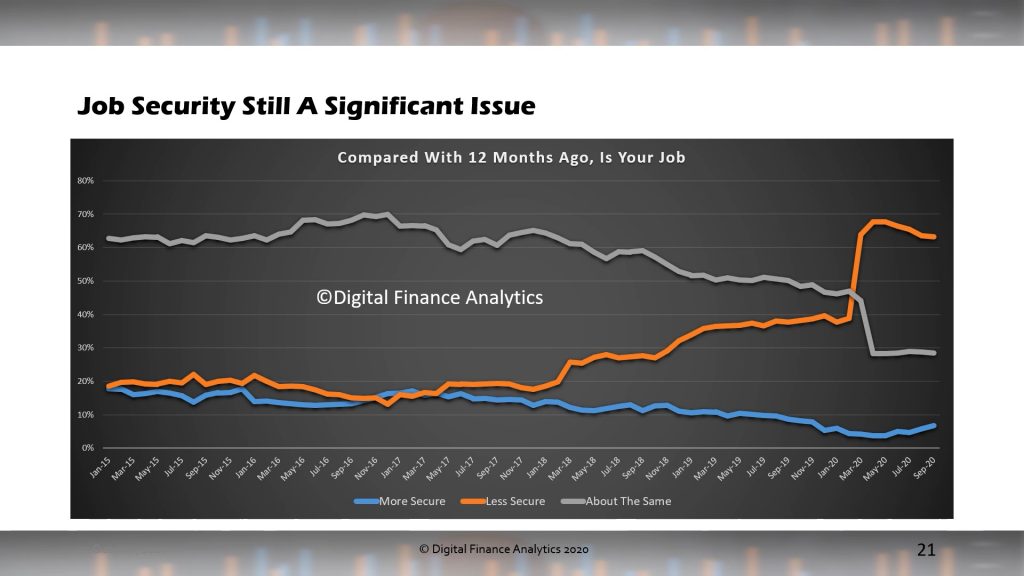

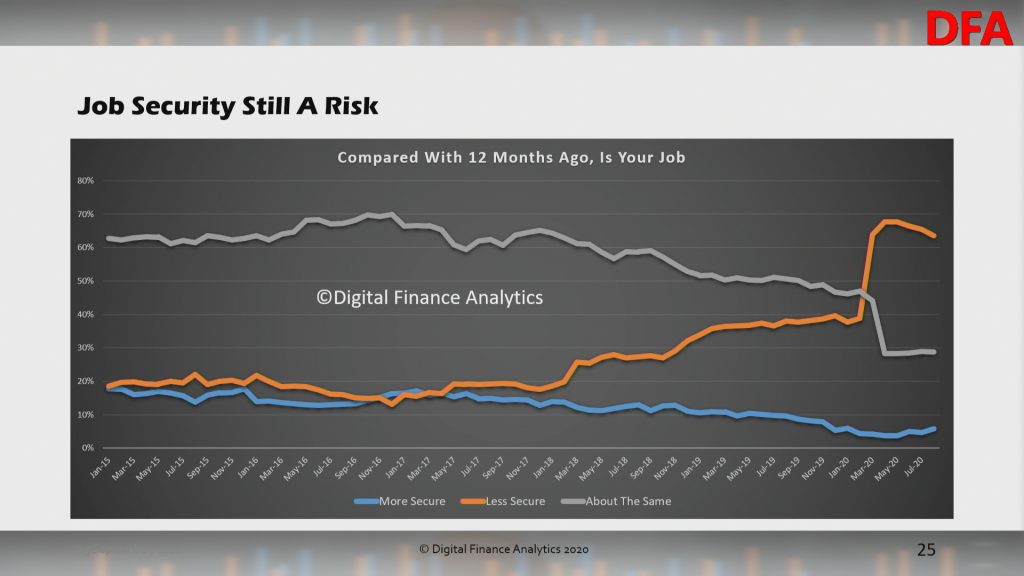

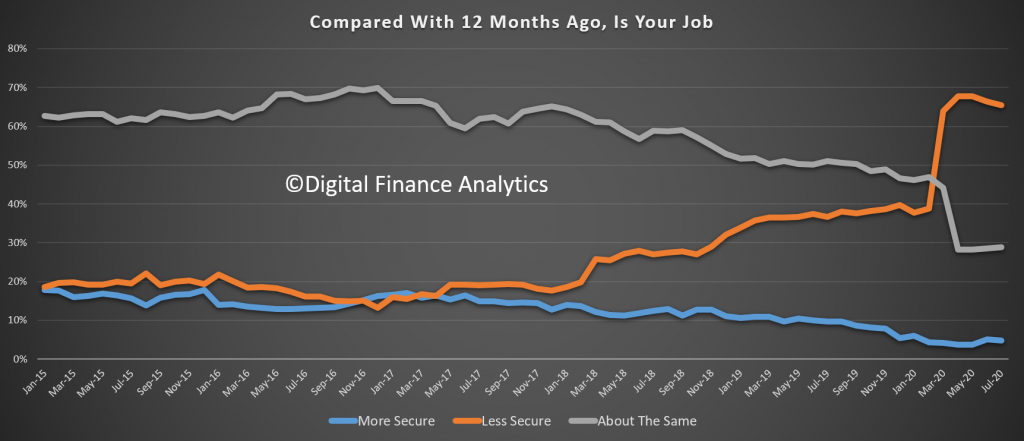

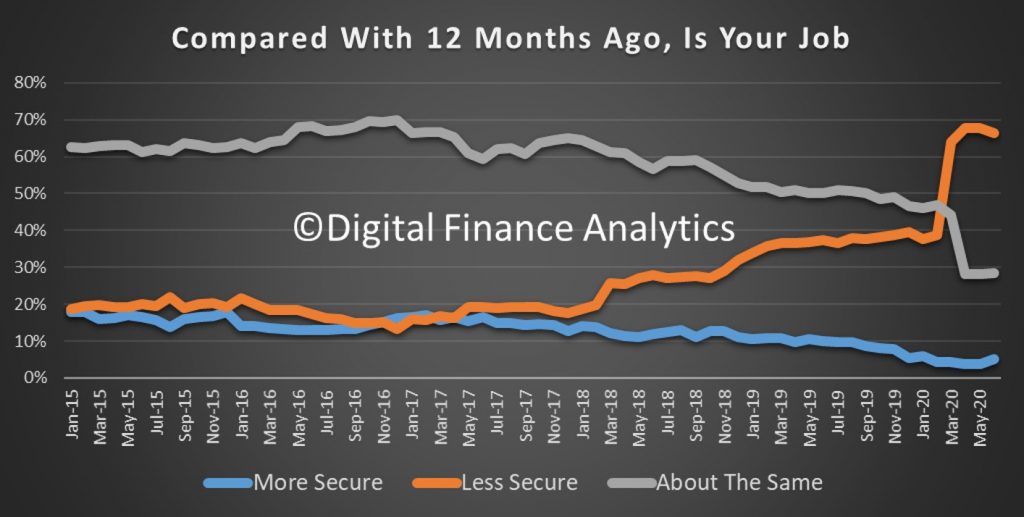

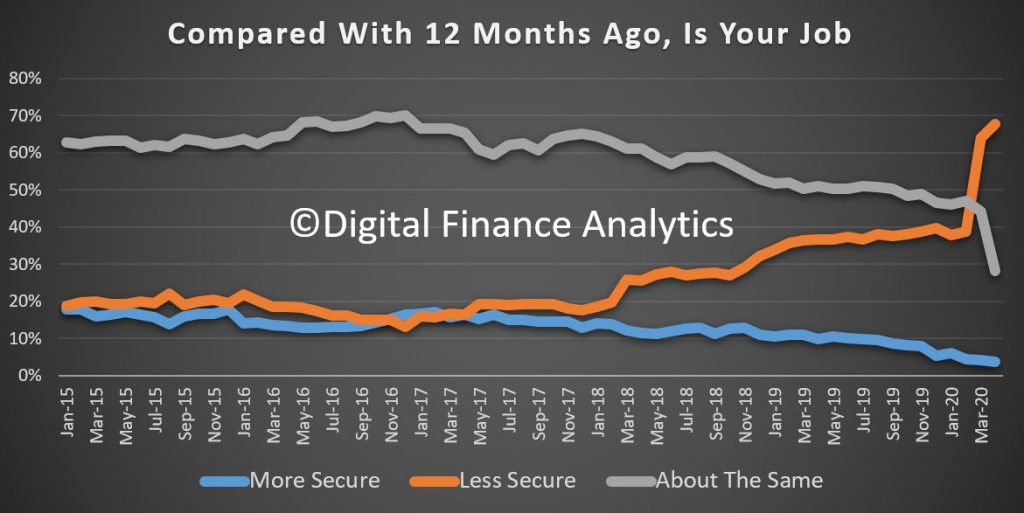

Across the components of the index, job security remains a significant issue with more than 60% of households less secure than a year ago. Many are working less hours, while structural unemployment continues to rise. Many SMEs are also cutting.

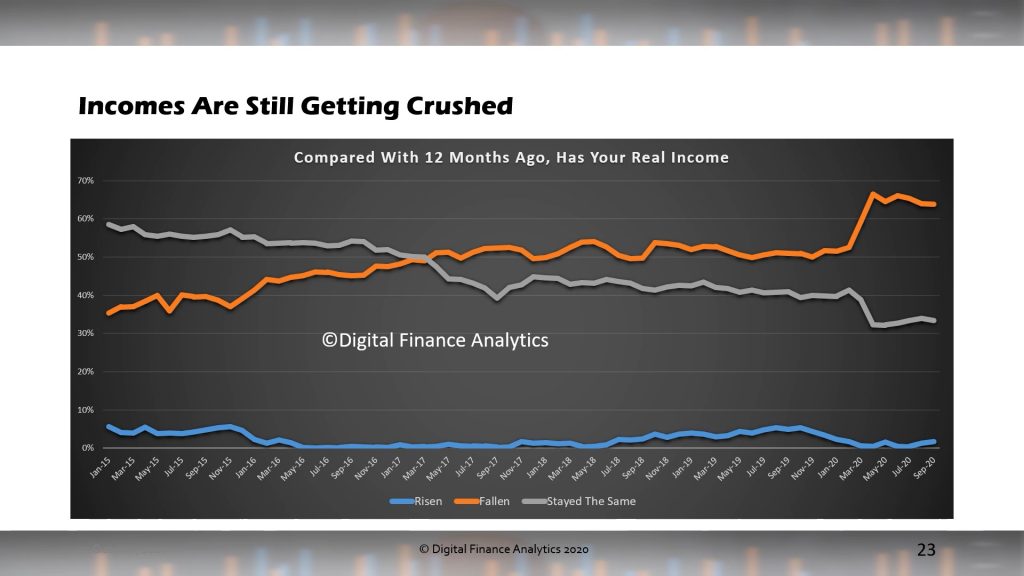

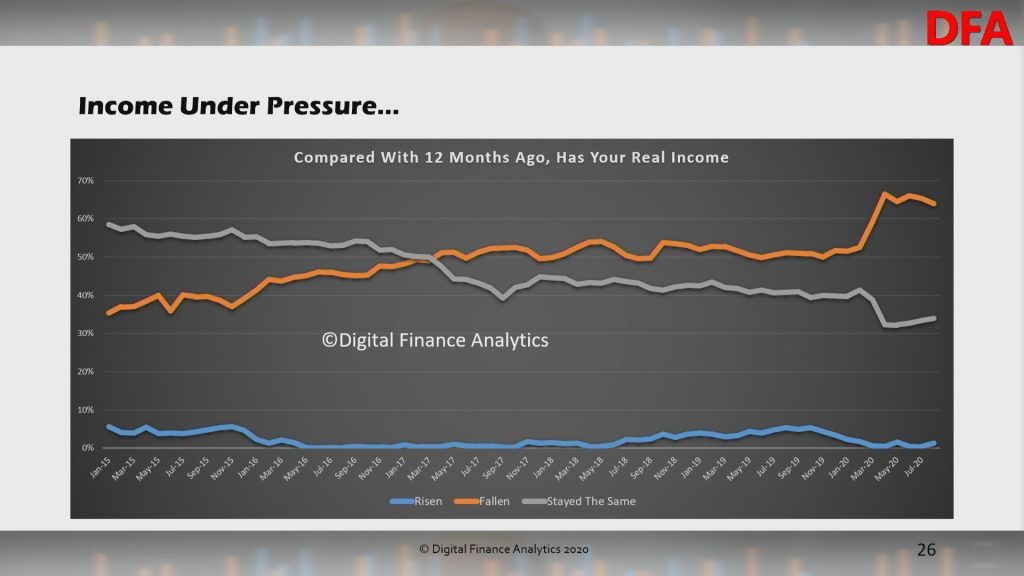

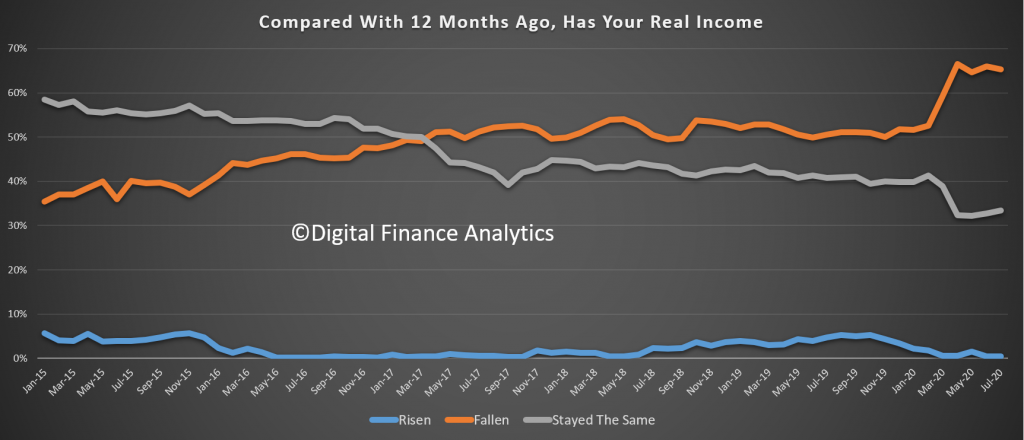

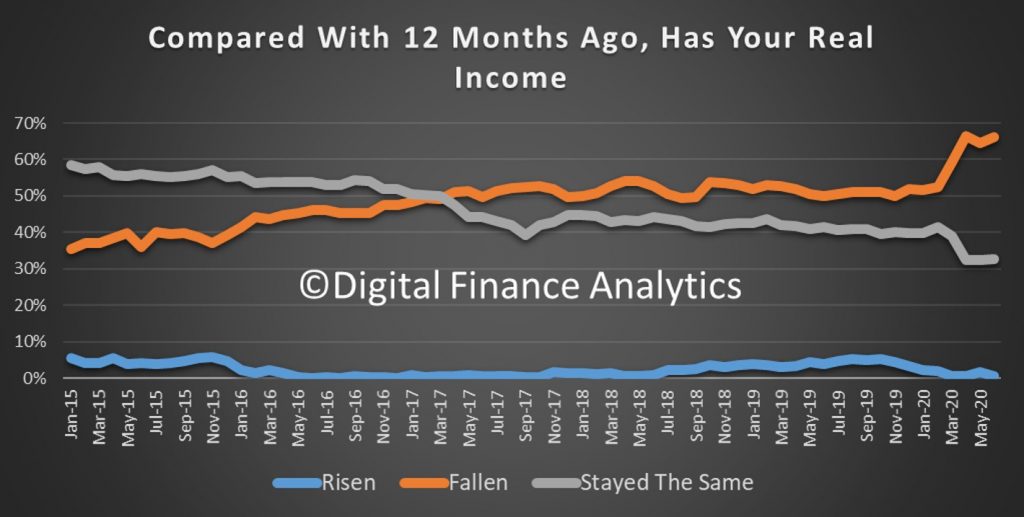

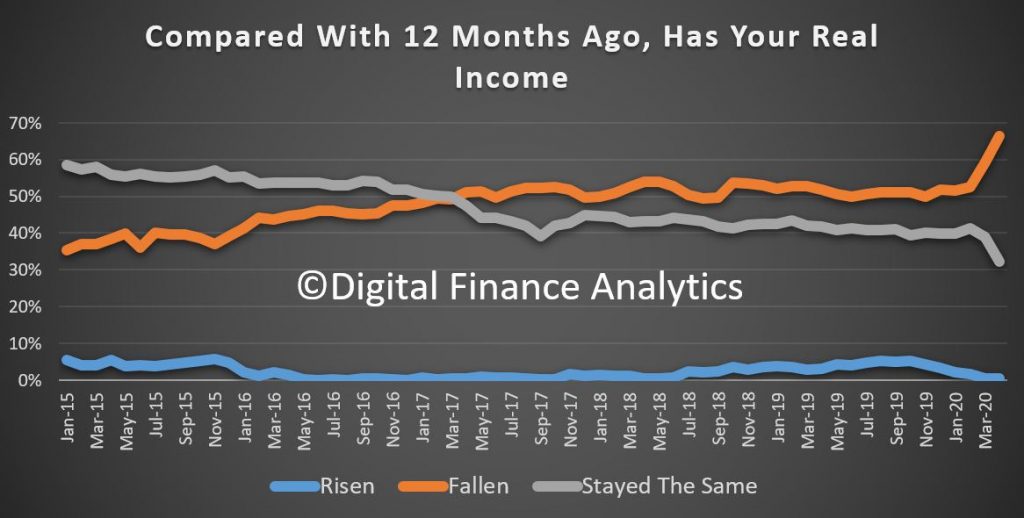

Incomes remain under pressure, thanks to less hours worked, and lower pay rates. Reductions to JobKeeper and JobSeeker are also hitting some now.

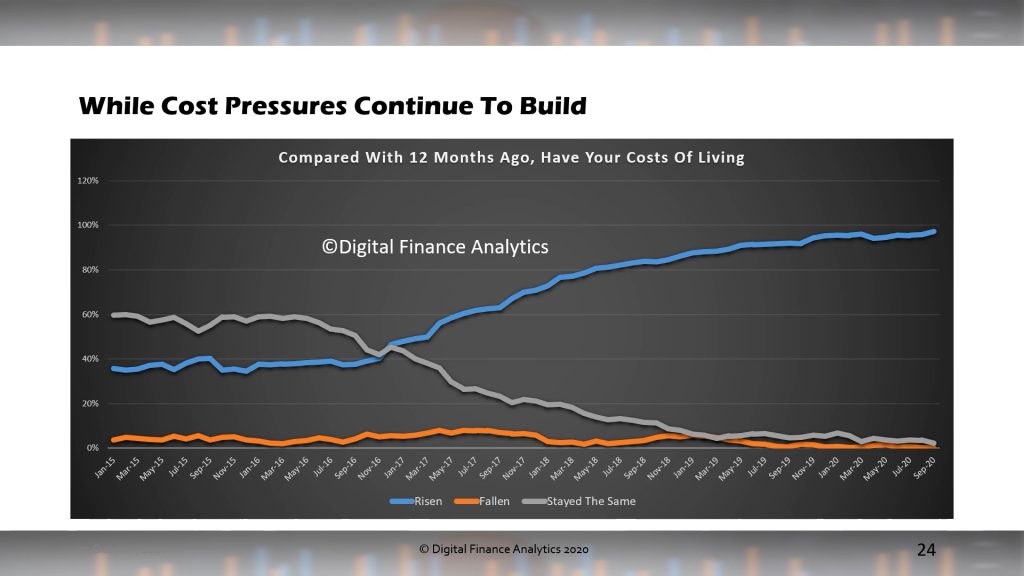

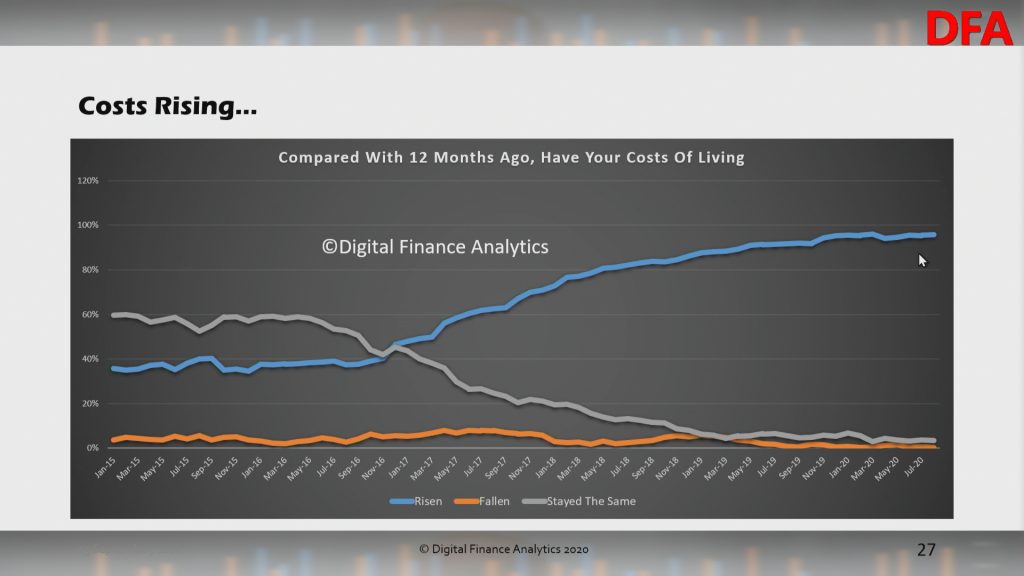

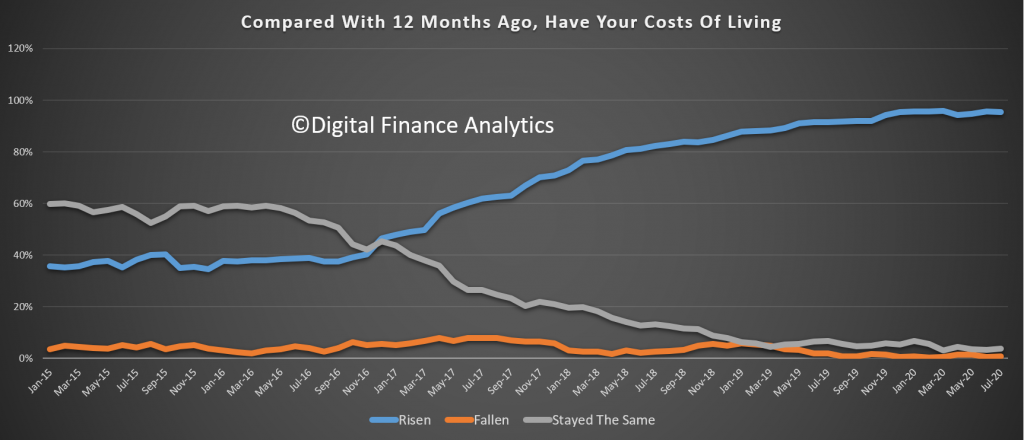

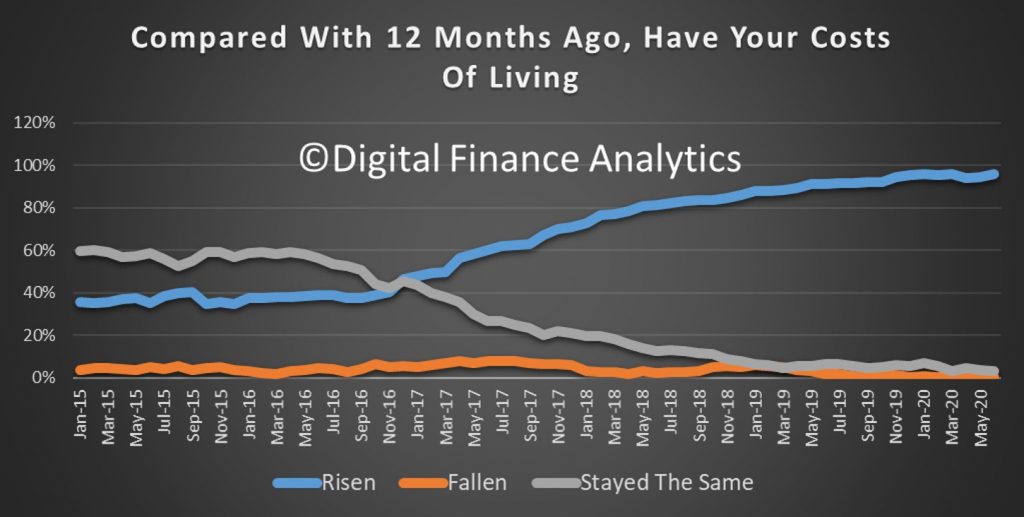

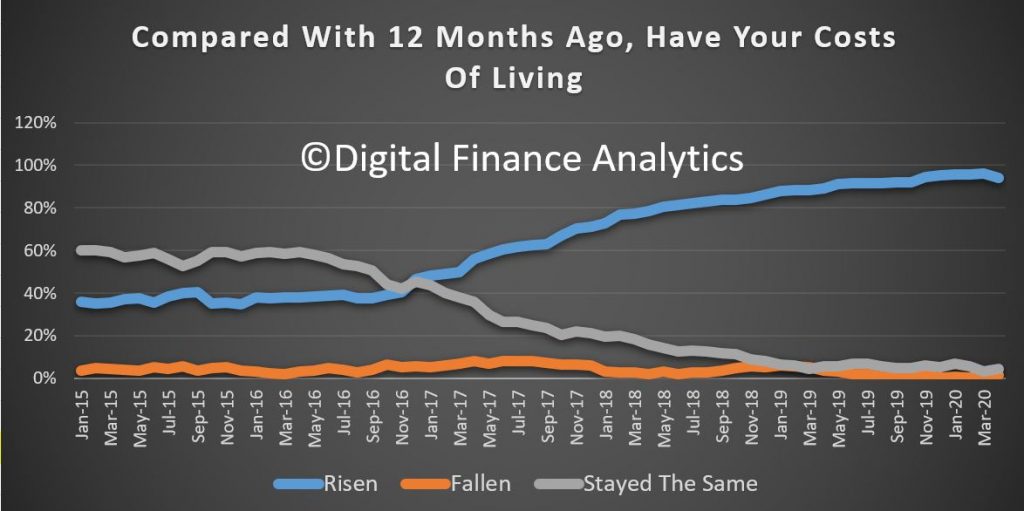

Costs pressures are still clearly in play, with most households seeing costs across multiple categories continuing to rise. Everyday costs at the supermarket appear to be rising faster than the official cpi.

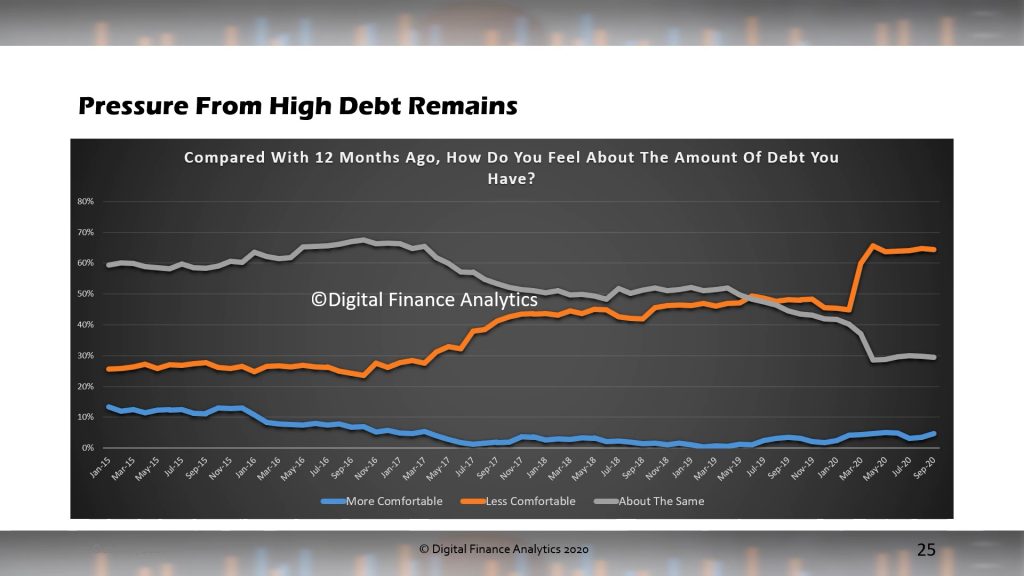

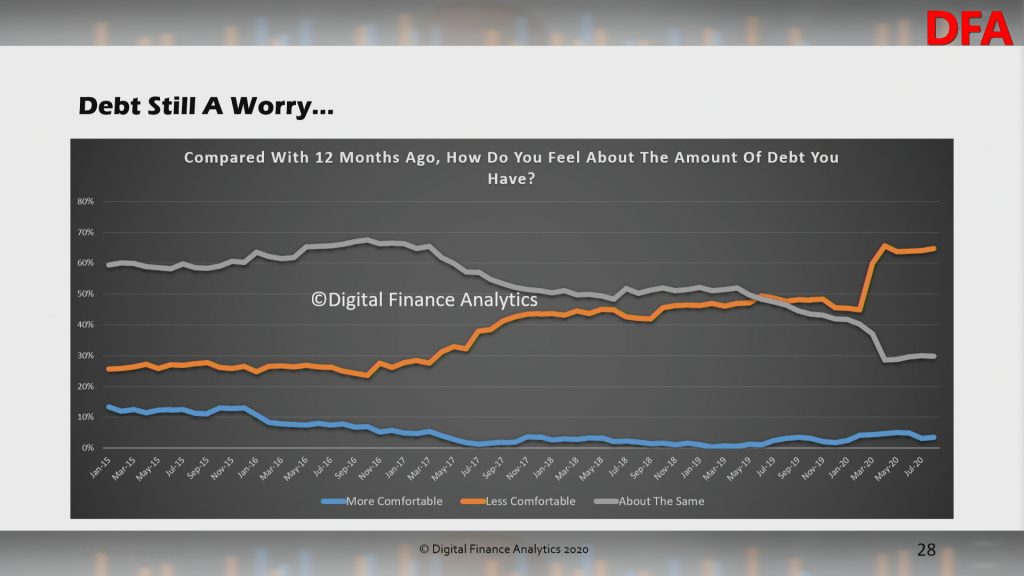

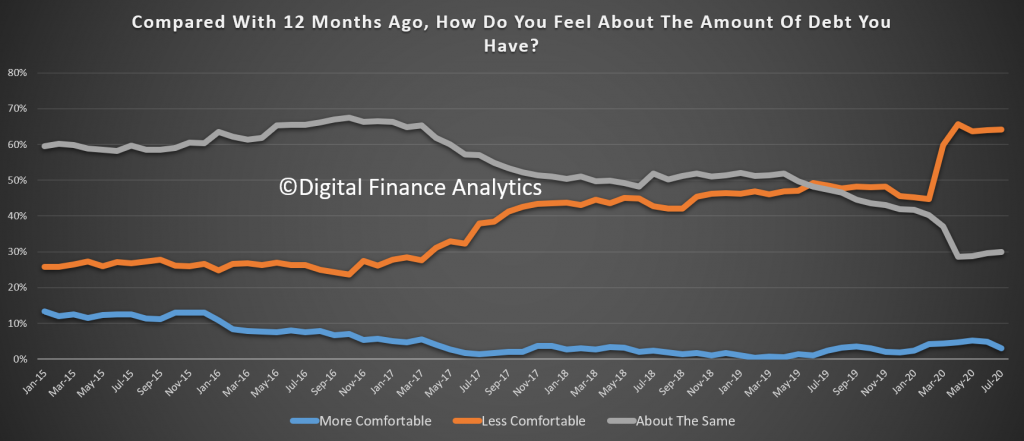

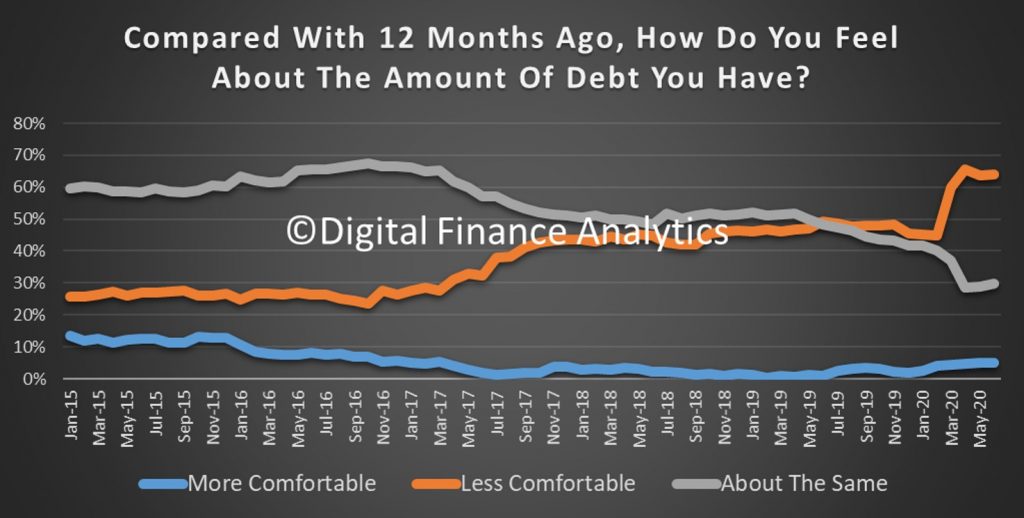

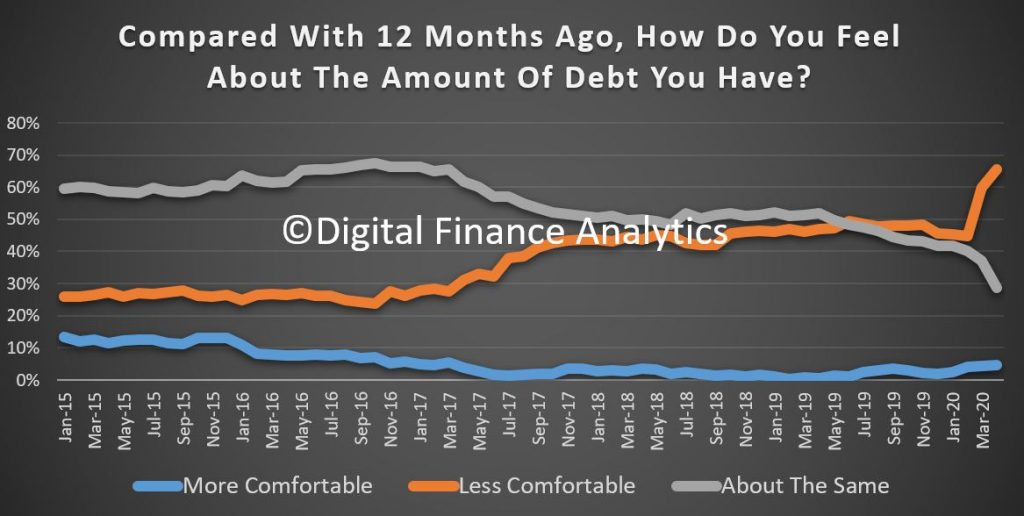

Those households with debt (not all are borrowing) are more concerned, especially those who were on principal and interest repayment holidays which are now ending. We continue to see expansion of credit (and Buy-Now-Pay-Later facilities) to those already in significant debt.

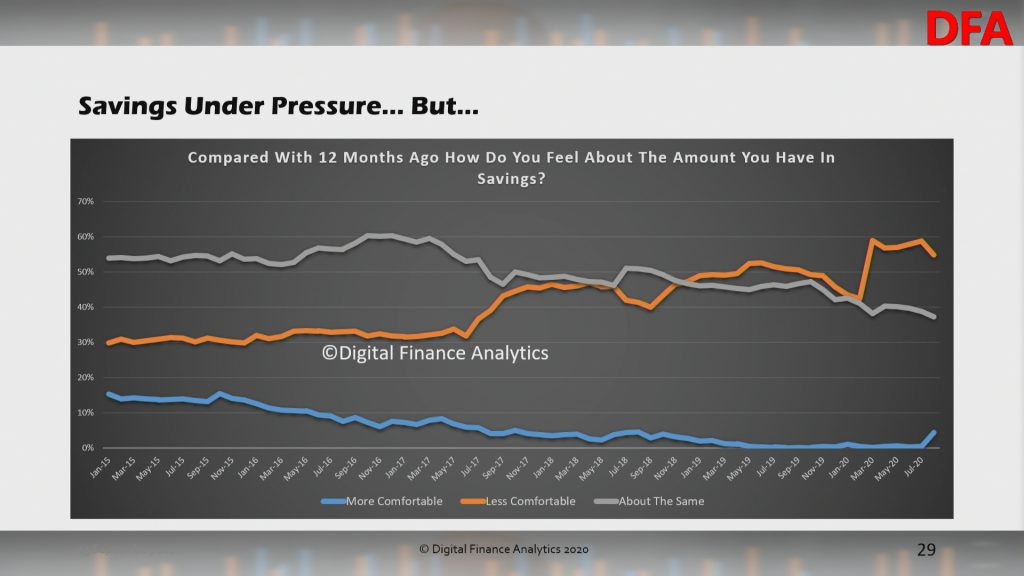

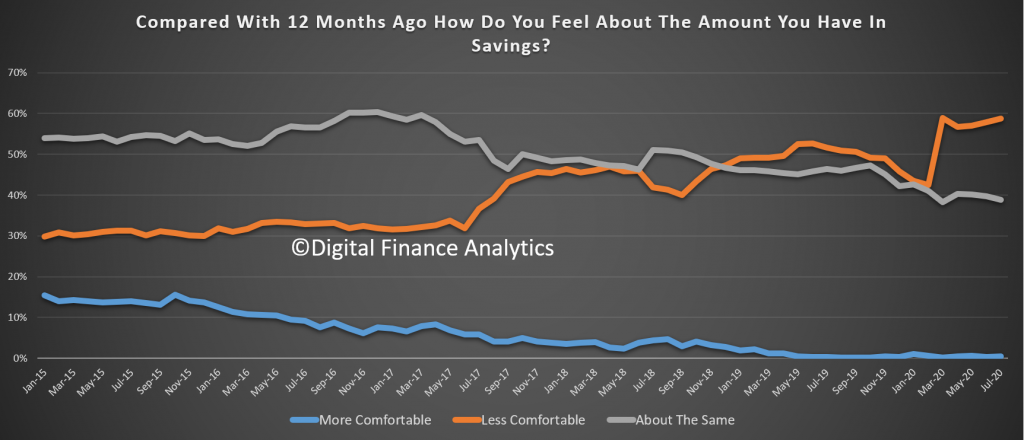

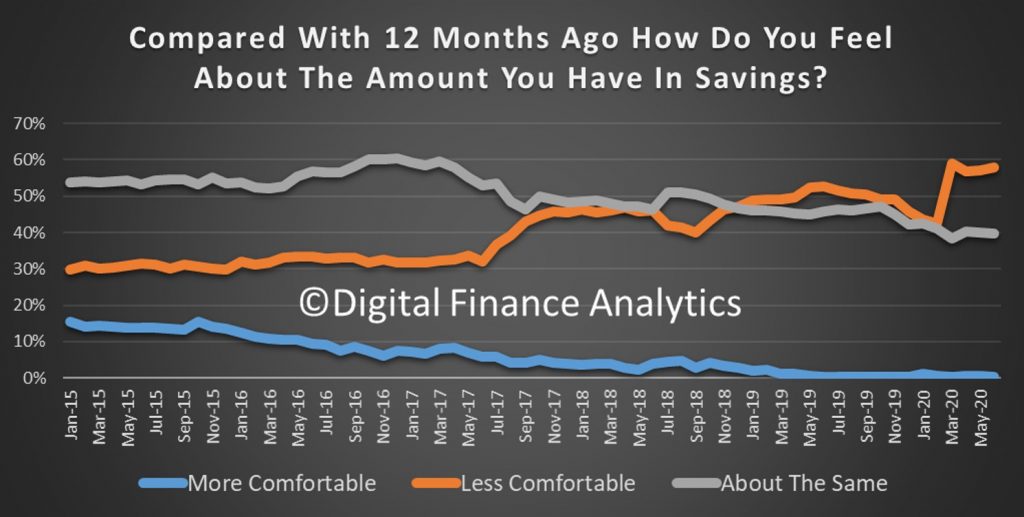

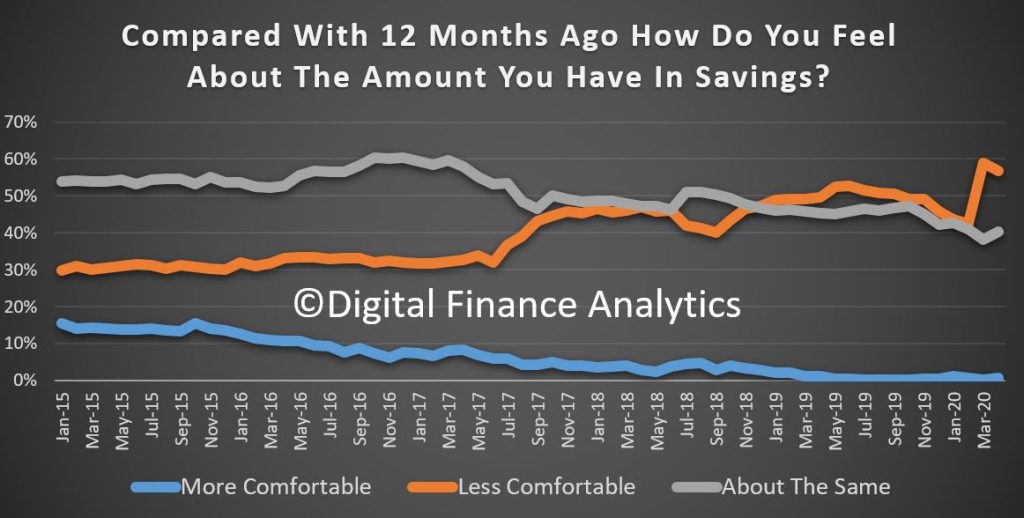

Savings are under pressure, especially with the continued crushing of deposit rates (thanks RBA…!). Those with savings in the banks have see rates drive towards zero in recent times. As a result more households are having to dip into capital, or moving to higher-risk investments. This largely silent group is drowned out by the clamour from the mortgaged sector and property bulls.

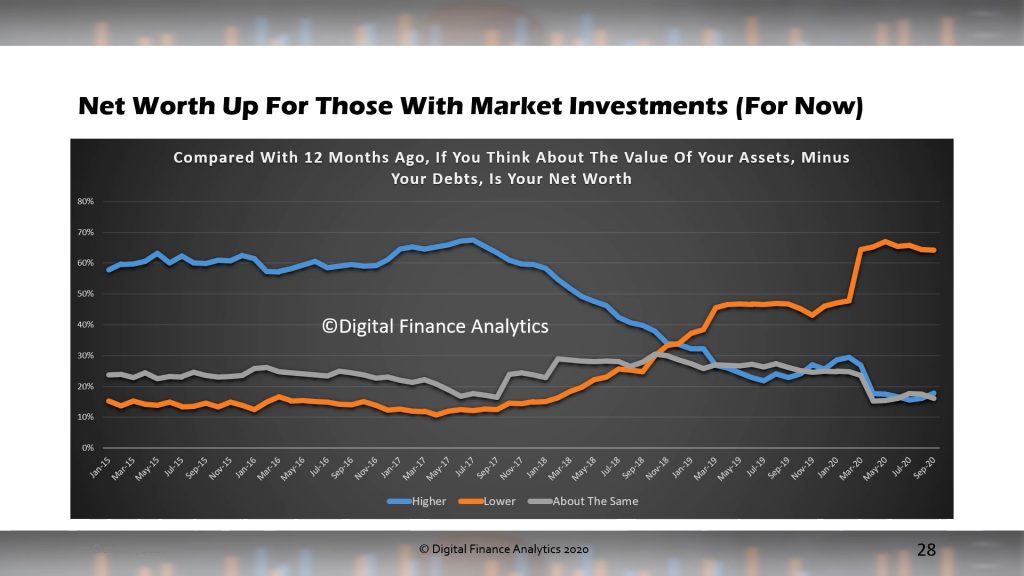

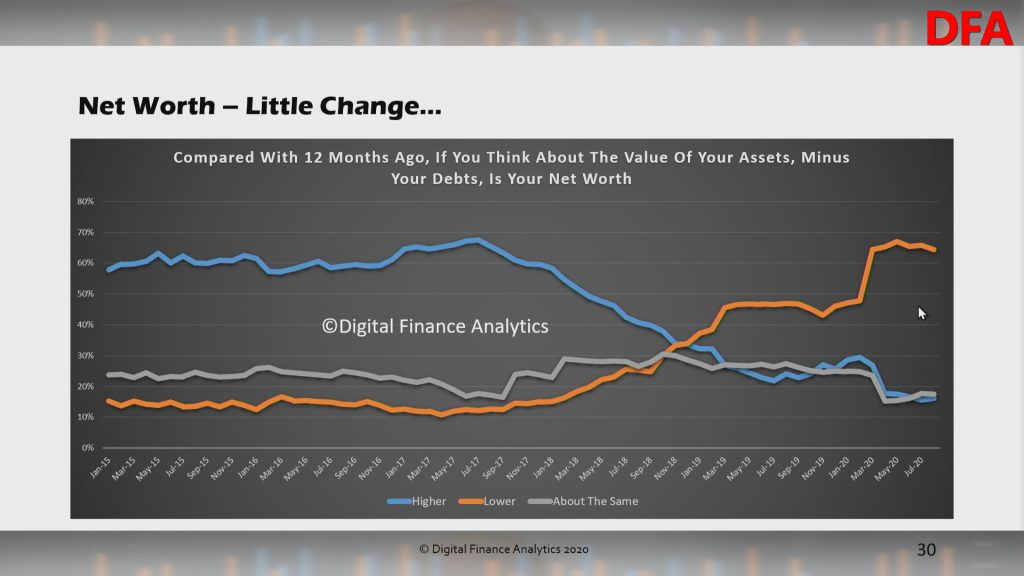

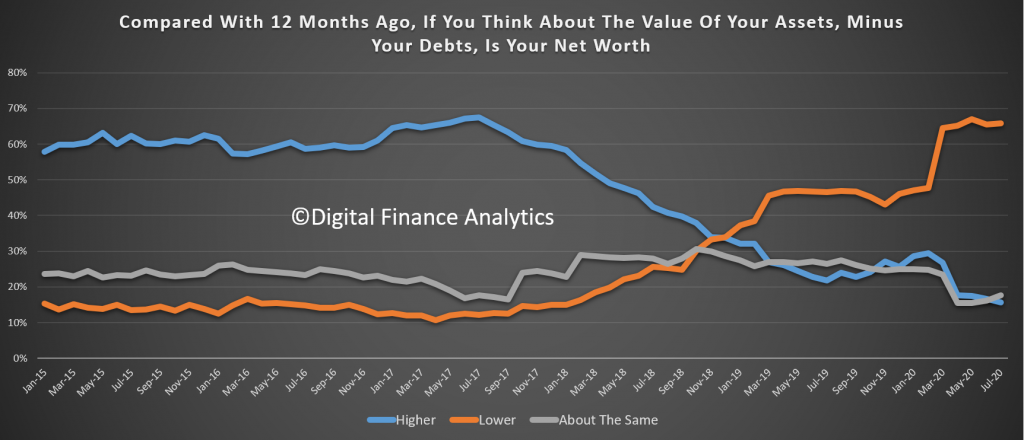

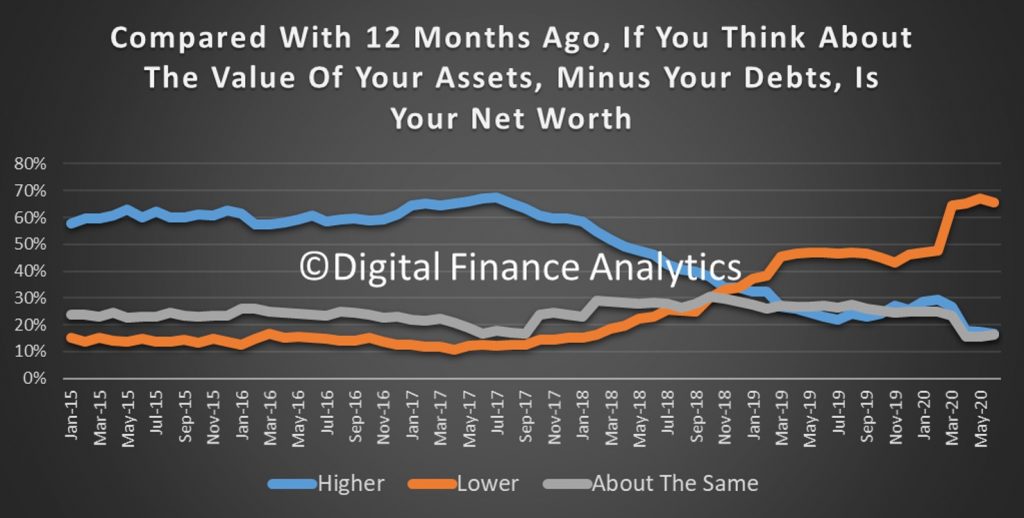

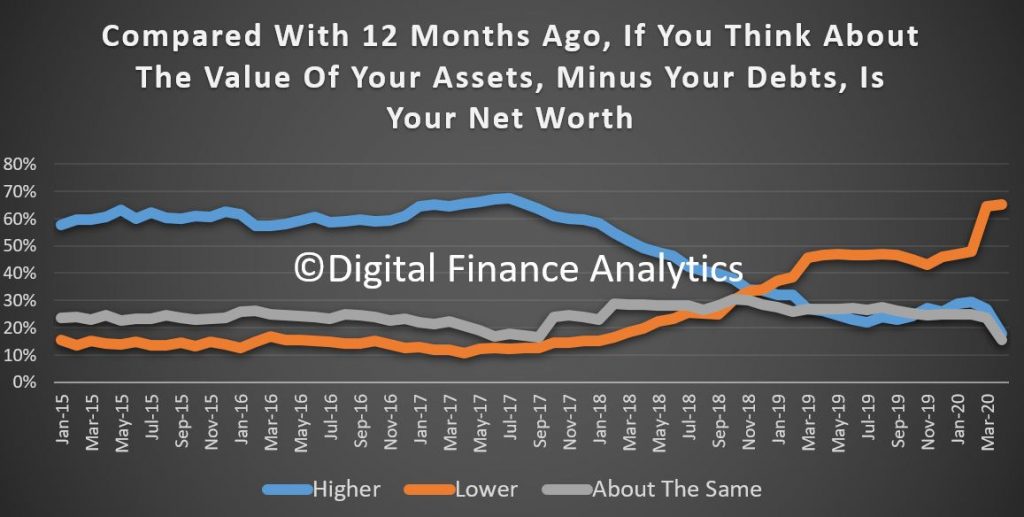

Finally, net worth has improved for those with market investments, for now, though 65% of households are still sitting on lower net worth than a year ago.

Given the current and expected monetary policy settings, we expect to see continued weakness in the index, until such time as employment and income growth accelerates. This is some way away yet.

We have released the latest edition of confidence measures based on our surveys. You can watch our live stream replay where we discuss the results in detail.

The overall index recovered a little in August, but remains well below the 100 neutral setting at 76.56.

Within the cohorts, more affluent and mortgage free households are best placed, thanks to continued strength in stock markets. Those with mortgages and those renting, not so much. The massive levels of Government support, plus repayment holidays also helped, together with significant superannuation withdrawals.

The state variations are striking, with a further fall in Melbourne in response to the latest lock-downs, while WA is looking stronger.

Across the age groups, younger and older households are more exposed, while late middle aged households, who have more financial resources, and less mortgage debt, are more positive.

Across the property segments, owner occupied property holders are more positive relatively speaking, thanks to lower mortgage rates – this despite higher mortgage stress. However, property investors continue to wrestle with poor returns, limited capital growth, and pressure to commence repayments on mortgage balances. Many are still considering disposing of property in the months ahead. Renters are caught with more limited income, despite rents slipping in some areas. There is also concern in this cohort about the status of deferred rentals down the track.

Within the moving parts of the index, job security remains a significant issue, though there was a slight easing in some areas, while in Melbourne things have degraded significantly. Many self-employed households are under severe pressure, with up to one in three concerned about the future of their business.

Income pressures remain to the fore, despite JobKeeper and JobSeeker. Some households have received higher incomes, though these will be reducing in September. Others have received no support despite income compression. The majority suggest real incomes have declined in the past year.

Costs of living continue to run above the official CPI figures. Food staples appears to be rising quite fast, despite lower spending by some households on transport and petrol. School fees and health care costs also figure.

Households are under considerable debt pressure despite the current repayment holidays. Given income pressures, meeting future debt commitments registered as a significant risk. This is consistent with high levels of mortgage and rental stress.

On the other hand, those receiving additional support, pulling money from superannuation, or repayment holidays are saving hard, as a hedge against future uncertainty. That said, many Australians reliant on income from bank savings continue to see their ability to service debt crushed by close to zero returns on deposits. Buy Now Pay Later facilities are in vogue to spread the costs of purchases, and as a way to manage cash flow. About 20% of users end up paying late costs, making this “free” credit expensive.

Finally, net worth remained relatively static as the elements in the index shifted. There is considerable confusion in the minds of many households who hold property, given the mixed data available about the property market. Many still believe the Government will stop home prices falling. Nevertheless, households remain cautious ahead of the impending cuts in support, and this does not bode well for greater consumption ahead. The major pain point is small businesses, may of whom have not been able to benefit from JobKeeper. This should be a focus for the Government in the upcoming budget.

The latest edition of our Financial Confidence Index, just released, reveals further weakness as COVID shut downs and constraints bite in VIC and NSW.

We discussed this on our recent live stream event.

We had been tracking some positive movements after the March fall, but in July we dropped back to 74.19, well below the 100 neutral setting. This is based on data from our rolling 52,000 household surveys, and examines their expectations on jobs, income, costs, savings, loans and net worth. The data is collected at a post code level.

In the past month households without mortgages but holding stocks have done better than those with a mortgage or those renting without market exposure. This highlights an important division between some households and others in terms of their finances.

Across the states, VIC and NSW are pulling the FCI down, while smaller (now more isolated) states are doing a little better. The lock down in VIC is having a significant negative impact.

All property segments eased back, although property investors continue to be most negative, fretting about falling capital values and lower rental returns. JobKeeper and JobSeeker are wired into many households budgets now and as support eases, more are concerned about what is ahead.

Age band analysis reveals that those younger and older remain more concerned, while those in the middle bands, with lower mortgage commitments and more market exposure are more positive, though easing down.

Looking at the elements of the survey, job prospects continue to worry though there is a slight fall from nearly 70% of households who see employment as less secure. This is being driven by what I call structural unemployment, and middle management jobs in large corporations across the country fact the axe. I discussed this on ABC RN yesterday

Incomes remain under severe pressure, despite JobKeeper and JobSeeker. As these are scaled back, pressures are likely to intensify.

Costs of living continue to accelerate, with households observing the rising costs of basic essentials at the supermarkets. While traveling less is common thanks to restrictions, net-net most are feeling the pinch.

Debts are a worry for more households, especially mortgage debt. Where people are in receipt of Government support, and even superannuation draw downs, around half are looking to pay debt down. Lower interest rates on mortgages are helping some but we see evidence of higher LVR loans and households with income pressures finding it more difficult to refinance to lower cost alternatives.

The collapse of interest rates on bank deposits continues to bite, with more switching from term deposits. Some are choosing to place funds into the financial markets, or buying gold etc. instead. But this does not necessarily assist with income flow, especially as dividends are also under pressure ahead.

Finally, net worth continues to be supported by financial market rises, while property falls have been slight so far. That said, the proportion saying their net worth is lower remains significant.

If Government support is unwound before the economy picks up, our view is household financial confidence will continue to suffer; not good for investment, spending or overall economic growth.

The latest results from our household surveys reveals that after a small recovery last month, confidence has deteriorated again. This is data to mid July, and includes the recent impact of renewed lock-downs in some areas. Indeed, significantly the Melbourne lock-down, and the broader concerns about COVID are responsible for the latest falls. No V-shaped recovery here.

We discussed this at length during our live stream yesterday.

The DFA survey asks households to compare their financial status compared to a year ago across multiple dimensions, including income, costs, jobs, debt savings and net worth. We are also able to cut the data across multiple dimensions. For example, across our wealth segments, those with no mortgage, but holding mortgage free property and shares etc. are a little more confident, thanks to the financial market rebound. But those with mortgages, and those renting are both feeling the pressure.

Across the states, the pain is more extreme in VIC, and NSW, while the smaller states are moving higher, though still remain well below the neutral 100 average.

Across our property segments, property investors continue to slide, thanks to lower rental returns, higher vacancy rates, and little expect capital gain. No surprise then that more investors are seriously weighing up selling before further markets falls. Owner occupied property holders have benefited from lower interest rates as the surge of refinancing to lower mortgage rates continues. Renters are under pressure, because despite lower rentals for some, there are pressures relating to rental holidays (deferrals?).

Across the age bands, those younger and older are seeing more pressure, whereas those in middle-aged bands improved slightly, because these cohorts have accumulated more assets and equity, and have relatively less debt. Older households are experiencing a real income drought thanks to lower returns on deposits, and lower expected dividends. More younger households are unemployed and job prospects are faltering.

Across the elements which drives the survey, job security remains a major concern. There was a small drop in those feeling less secure, as some jobs came back, but over 68% of households remain concerned – which suggests they will be cautious ahead.

Income pressures have increased, with jobs evaporating, and less hours worked. This is the highest reading since we started running the survey.

The question of costs continues, with many reporting increased costs of living way above the official cpi. This despite the increased working from home. Higher power costs from more home use was a stand out. The need to commence paying for childcare also hit home.

Debt remains a burden for those with mortgages and for households with other unsecured debts. More than 60% of borrowing households are worried abut their ability to service their loans. Many are seeking refinancing, or to use debt consolidation to try to reduce payments. And as we reported previously mortgage stress is as high as ever its been. We think defaults will follow, despite lenders’ repayment holidays.

Savings remain under pressure (although some on JobKeeper received more income than normal and have saved some of the funds, and superannuation withdrawals are also being horded by many to accessed the scheme). The pressure comes from needing to tap into savings for living expenses, and lower returns from deposits. More than 3 million households do rely in income from deposit accounts, and rates are close to zero now.

Finally, net worth has declined for more than 60% of households, thanks to lower property prices, though offset by higher stock prices. Forward expectations are also weaker, as more property price falls rises. Any market correction would also add more fuel to the fire.

So standing back, it is clear the household sector continues to be trapped in a web of concerns, and as a result their willingness to spend is likely to be crimped. Not good for future GDP. Until COVID is controlled, we have to expect confidence to continue to languish. This has some way to travel. Expect saw-tooth patterns of growth for the next couple of years.

We update our models to take account of the latest data, look at the news about JobSeeker and JobKeeper, and discuss the RBA’s comments. Plus we will have our postcode data online and also look at the latest financial confidence outcomes. Ask a question live via the YouTube chat.

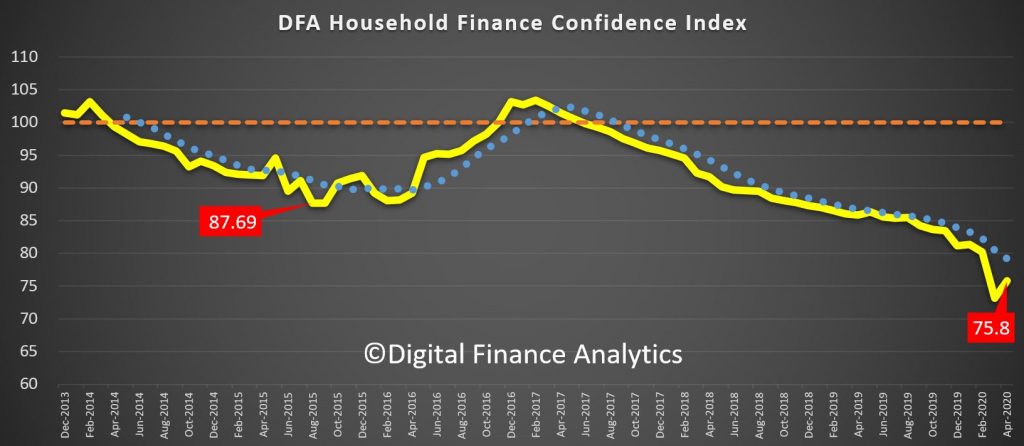

Our latest household financial confidence index improved a little in April, up from 73.2 in March to 75.8 in April. That said, it is still well below the 100 which is a neutral setting, meaning that households are extremely cautious about their finances.

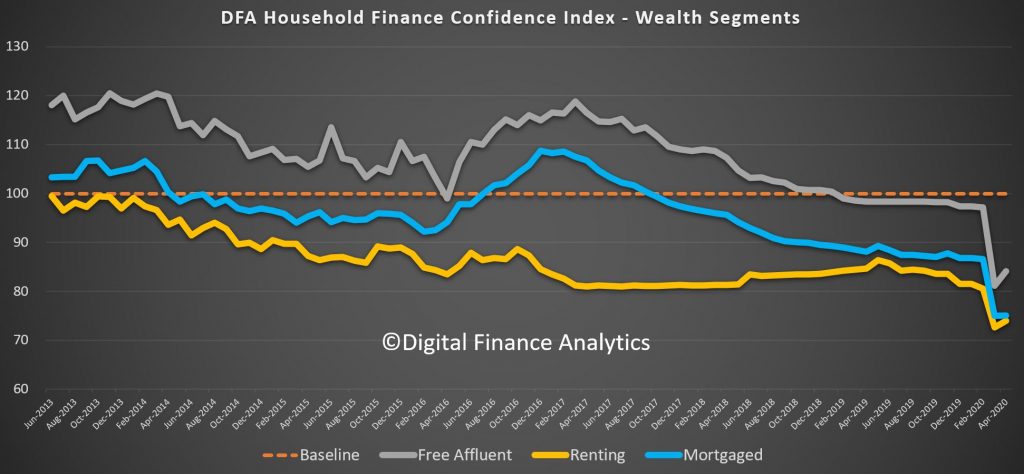

Across our wealth segments, those free affluent households recovered the most mainly thanks to the recovery in stock markets over the past month. Those renting are benefiting from falling rents (though many have income shocks to deal with) while those with a mortgage showed little evidence of a recovery in confidence, thanks to rising debt concerns.

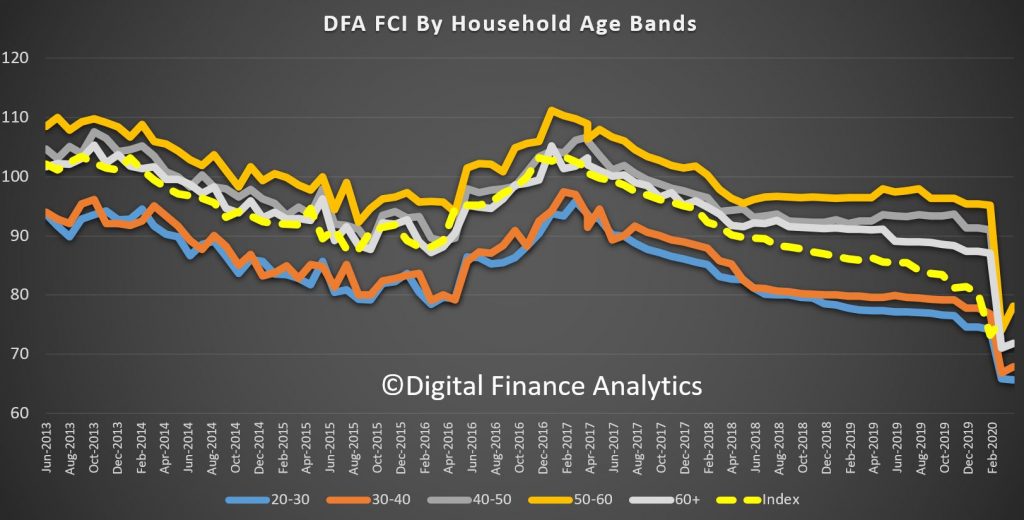

Across the age bands, those aged 50-60 showed the strongest bounce, while those aged 20-30 reported a further fall – not least because younger households tend to be more exposed to zero hour contracts, and part time employment not supported by JobKeeper.

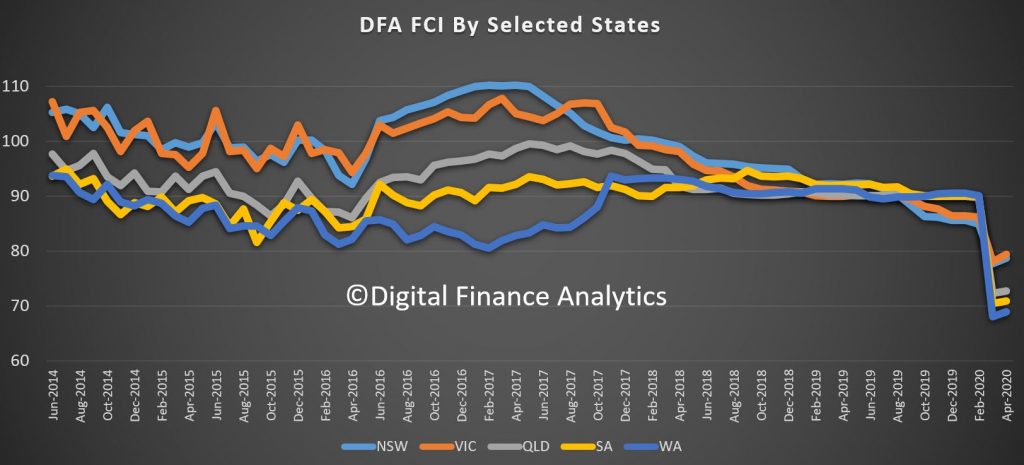

The recovery in confidence was evident across all the states, with NSW and VIC on average more positive relatively speaking than SA and WA.

Across our property segmentation, owner occupied households improved, as did those not holding property, but property investors fell again, thanks to less support from banks in terms of mortgage repayment holidays and falling rents and occupancy. Around 8% of property investors are seriously looking to sell their property if they can. More on that in a future post.

The true state of play is best shown when we look at the moving parts of the index. 67% of households now feel less secure regarding their job prospects than a year ago, a rise of 28% from last month.

There was a 14% rise in those feeling less comfortable with their savings, to 56% of households. There was a clear intent to try to save more in the months ahead, given current economic uncertainties.

65% of households are less comfortable with their ability to service debt, a rise of more than 20% of households, this despite falling interest rates and bank support schemes. Around $160 billion of loans received some leniency from the banks, but that is a small share of the $1.7 trillion mortgage sector and the $280 billion SME sector.

Income pressures are mounting, with 14% saying their incomes had fallen – to 66% of households, while under 1% saw any rise in income – including some who will benefit from higher incomes under JobKeeper than they would normally receive.

Costs of living continue to drive higher – despite the fall in oil prices – with many households incurring greater costs because they are spending more time at home. 94% said their costs were higher than a year ago.

Finally, household net worth was lower for 65% of households, reflecting stock market and property price adjustments, and rising debt levels. There was a drop of 11% in households claiming net worth had risen over the past year to 18%.

So we think the longer terms impacts on households are yet to be fully understood. Certainly, our data suggests households will be cautious, as income pressures, costs of living and rising debts bite. If home prices slide further as we expect they will, then household net worth will put a further brake on the wealth effect and will also adversely impact many households. This does not suggest a V shaped recovery to me.

Blog")