Information received since the Federal Open Market Committee met in September indicates that the labor market has continued to strengthen and that economic activity has been rising at a strong rate. Job gains have been strong, on average, in recent months, and the unemployment rate has declined. Household spending has continued to grow strongly, while growth of business fixed investment has moderated from its rapid pace earlier in the year. On a 12-month basis, both overall inflation and inflation for items other than food and energy remain near 2 percent. Indicators of longer-term inflation expectations are little changed, on balance.

There was no mention of the deterioration in data with policymakers describing household spending growth as strong even though core retail sales stagnated in September. This unambiguously positive outlook is a signal of the central bank’s commitment to raising interest rates. There’s no doubt that the Fed will hike in December, especially if stocks maintain their current recovery.

The T10 Bond Rate went higher.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee expects that further gradual increases in the target range for the federal funds rate will be consistent with sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective over the medium term. Risks to the economic outlook appear roughly balanced.

In view of realized and expected labor market conditions and inflation, the Committee decided to maintain the target range for the federal funds rate at 2 to 2-1/4 percent.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its maximum employment objective and its symmetric 2 percent inflation objective. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

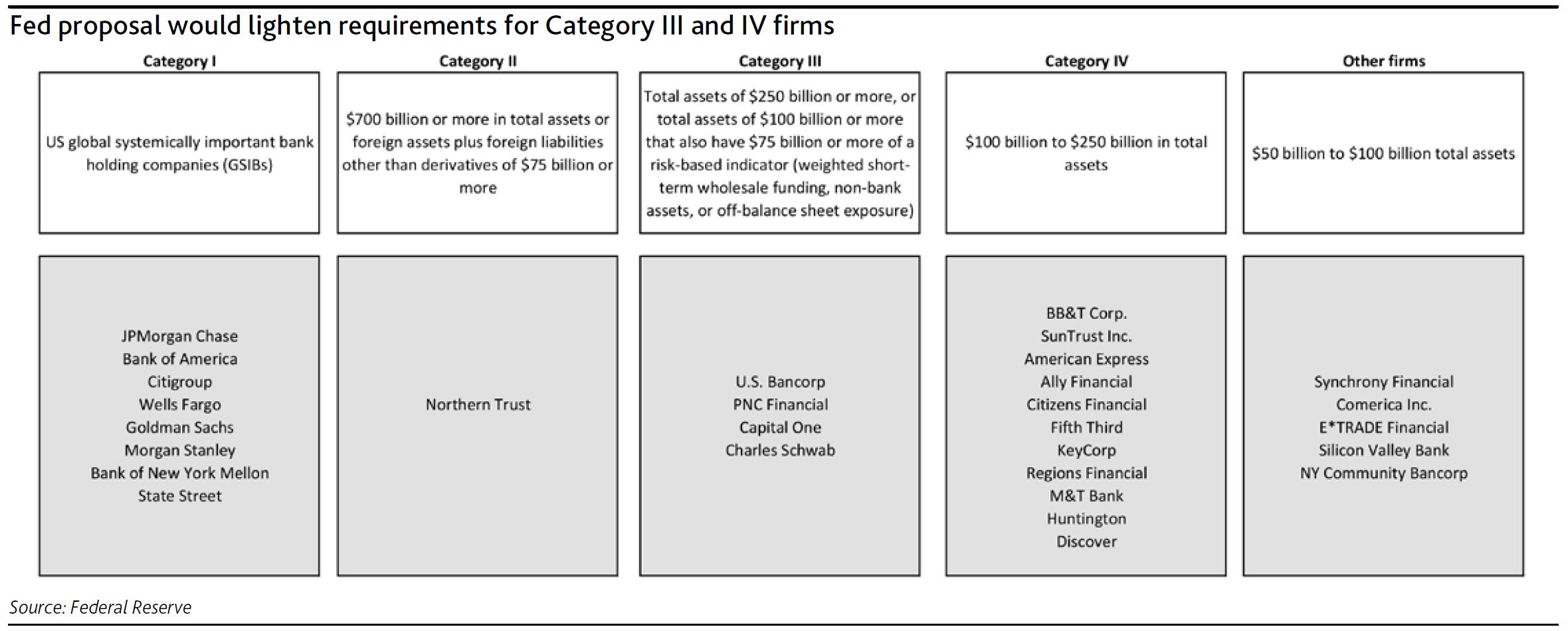

Moody’s says that relaxed regulatory oversight for the largest US regional banks would be credit negative.

On 31 October, the US Federal Reserve (Fed) proposed revisions to the prudential standards for the supervision of large US bank holding companies to implement the Economic Growth, Regulatory Relief, and Consumer Protection Act (the Act) that became law in May of this year. The proposal would apply less rigorous capital and liquidity standards to most large regional bank holding companies with less than $700 billion of consolidated assets or less than $75 billion of cross-jurisdictional activity, a credit-negative.

In particular, the Fed proposals would relax current supervisory requirements for banks with assets of more than $250 billion, which goes beyond the Act’s primary focus on banks below that threshold. However, the proposal is still consistent with the Act’s emphasis on regulation that increases in stringency with a firm’s risk profile, defining four categories of banks as described and named in Exhibit 1 (other firms are no longer subject to the Fed’s enhanced prudential standards under the Act).

The 11 firms in Category IV would be subject to significantly reduced regulatory requirements under the proposal, including public supervisory stress testing every two years instead of annually. These firms would also be permitted to exclude accumulated other comprehensive income (AOCI) from capital and would no longer be subject to the liquidity coverage ratio (LCR) or proposed net stable funding ratio (NFSR) rules. Internal liquidity stress-testing would be required quarterly rather than monthly.

The four firms in Category III would be subject to modestly reduced regulatory requirements under the proposal. They would no longer have to apply the advanced approaches (internal models-based) risk-based capital requirements but would remain subject to the standardized approach requirements. Like Category IV firms, they could elect to exclude AOCI from capital. However, they would still be subject to the annual public supervisory stress tests. Their LCR and NFSR requirements would be reduced to between 70% and 85% of full requirements.

The changes in capital and liquidity requirements for Category III and IV firms are likely to reduce their capital and liquidity buffers, a credit negative. Moreover, the reduced frequency of capital and liquidity stress testing could lead to more relaxed oversight and afford banks greater leeway in managing their capital and liquidity, as well as reduce transparency and comparability, since fewer firms will participate in the public supervisory stress test.

Category I and II firms would not see any changes to their capital or liquidity requirements. The proposals do not address the US operations of foreign banking organizations, but a proposal on their supervision will likely be forthcoming.

The Federal Reserve released the minutes relating to the 26th September decision to lift rates. The impression from the more detailed disclosures is that more hikes are likely, and perhaps quicker than originally expected. Members agreed to remove the sentence indicating that “the stance of monetary policy remains accommodative.”

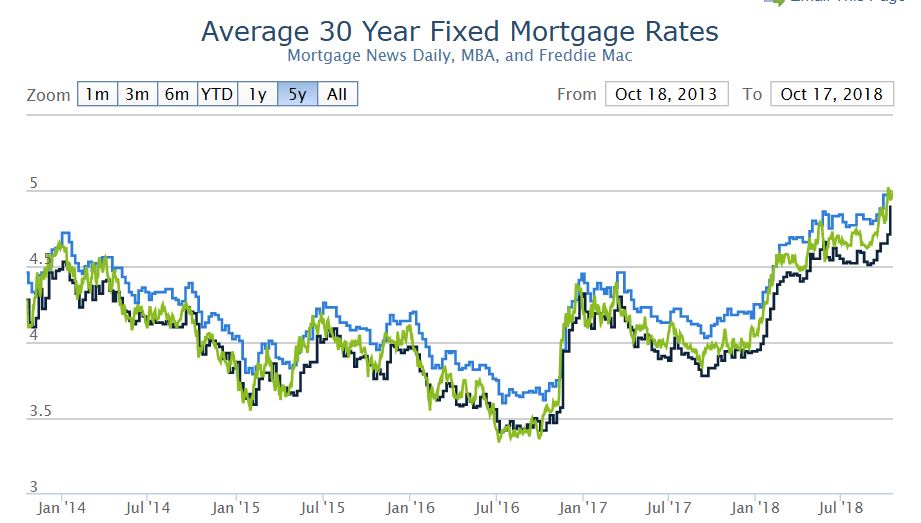

US Mortgage Rates continue higher.

This is what the FED said:

In their discussion of monetary policy for the period ahead, members judged that information received since the Committee met in August indicated that the labor market had continued to strengthen and that economic activity had been rising at a strong rate. Job gains had been strong, on average, in recent months, and the unemployment rate had stayed low. Household spending and business fixed investment had grown strongly. On a 12-month basis, both overall inflation and inflation for

items other than food and energy remained near 2 percent.

Indicators of longer-term inflation expectations were little changed on balance.

Members viewed the recent data as consistent with an economy that was evolving about as they had expected. Consequently, members expected that further gradual increases in the target range for the federal funds rate would be consistent with sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective over the medium term. Members continued to judge that the risks to the economic outlook remained roughly balanced.

After assessing current conditions and the outlook for economic activity, the labor market, and inflation, members voted to raise the target range for the federal funds rate to 2 to 2¼ percent. Members agreed that the timing

and size of future adjustments to the target range for the federal funds rate would depend on their assessment of realized and expected economic conditions relative to the Committee’s maximum-employment objective and symmetric 2 percent inflation objective. They reiterated that this assessment would take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

With regard to the postmeeting statement, members agreed to remove the sentence indicating that “the stance of monetary policy remains accommodative.” Members made various points regarding the removal of the sentence from the statement. These points included that the characterization of the stance of policy as “accommodative” had provided useful forward guidance in the early stages of the policy normalization process, that this characterization was no longer providing meaningful information in light of uncertainty surrounding the level of the neutral policy rate, that it was appropriate to remove the characterization of the stance from the Committee’s statement before the target range for the federal funds rate moved closer to the range of estimates of the neutral policy rate, and that the Committee’s earlier communications had helped prepare the public for this change.

In choppy trading in the US on Wednesday, it appears the markets are coming to accept higher rates ahead. The Dow Jones Industrial Average fell 91.74 points, or 0.36 percent, to 25,706.68.

The Fear Index eased a little to 17.40, down 1.25%, but volatility still stalks the halls.

The S&P 500 lost 0.71 points, or 0.03 percent, to 2,809.21.

The Nasdaq Composite dropped 2.79 points, or 0.04 percent, to 7,642.70.

The 10-Year Bond rate continued higher ending at 3.207, up 0.88%.

The Fed moved as expected, and continues to highlight more upward movements in the months ahead – in fact their language is arguably more bullish now. The target range for the federal funds rate is now 2 to 2-1/4 percent.

Information received since the Federal Open Market Committee met in August indicates that the labor market has continued to strengthen and that economic activity has been rising at a strong rate. Job gains have been strong, on average, in recent months, and the unemployment rate has stayed low. Household spending and business fixed investment have grown strongly. On a 12-month basis, both overall inflation and inflation for items other than food and energy remain near 2 percent. Indicators of longer-term inflation expectations are little changed, on balance.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee expects that further gradual increases in the target range for the federal funds rate will be consistent with sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective over the medium term. Risks to the economic outlook appear roughly balanced.

In view of realized and expected labor market conditions and inflation, the Committee decided to raise the target range for the federal funds rate to 2 to 2-1/4 percent.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its maximum employment objective and its symmetric 2 percent inflation objective. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

Voting for the FOMC monetary policy action were: Jerome H. Powell, Chairman; John C. Williams, Vice Chairman; Thomas I. Barkin; Raphael W. Bostic; Lael Brainard; Richard H. Clarida; Esther L. George; Loretta J. Mester; and Randal K. Quarles.

Today we consider whether the shape of the yield curve is a good indicator of a future recession in the US.

To answer that question, let’s look at the longer term trends, using data from one of our favourite data sources FRED. FRED is the St. Louis Fed datasets, which contains a wide range of useful indices.

Here is plot of the 10 year rates since 1980. The shaded areas are US recessions, when the economy shrank (generally seen as a negative indicator), certainly unemployment rose as is clearly evident as a direct result of the recession.

But now let’s look at the 10-year rate from the 1980’s, and overlay the 3-month rate also. In the video we follow the inflection points, and here is the thing. Prior to each of the last three US recessions, the short-term rate overtook the long term rate in a classic inversion of the yield curve. And we see recessions follow.

The logic behind the inverted yield curve as a recession indicator is simple: if long-term yields are lower than short-term yields, the market’s view is that growth will slow in the coming years. More often than not, that view has been right.

From this, we can say there is clear evidence that once the yield curve does reverse, a recession will likely follow. But what does that tell us about the current situation? Well currently short term rates have been rising sharply, more so than long term rates, as the Fed draws in their QE horns. If that trend continues, the yield curve will go negative, and in that case a US recession is highly likely. And on current trajectory that could happen within a couple of years.

However, beware, because there were cases when the US yield curve inverted but a recession did not follow. For example, in the late 1980s, the yield curve inverted and then steepened again, before inverting again later on before a recession hit. The curve also inverted very briefly in the late 1990s, too, and again in 2005-2006. However, the trends to my mind do signal a recession, but the timing does vary. Sometimes it happens in just a few months, in other cases it’s taken a year or two. But it does look like a yield inversion is an important signal to watch for, worth bearing in mind when people are taking about all the reasons why the stock market in the US should go higher still.

In a release late last week, the FED said that as part of its annual examination of the capital planning practices of the nation’s largest banks, the Federal Reserve Board did not object to the capital plans of 34 firms but objected to the capital plan from DB USA Corporation due to qualitative concerns.

Due in part to recent changes to the tax law that negatively affected capital levels, two firms will maintain their capital distributions at the levels they paid in recent years. Separately, one firm will be required to take certain steps regarding the management and analysis of its counterparty exposures under stress.

The Comprehensive Capital Analysis and Review, or CCAR, in its eighth year, evaluates the capital planning processes and capital adequacy of the largest U.S.-based bank holding companies, including the firms’ planned capital actions, such as dividend payments and share buybacks. Strong capital levels act as a cushion to absorb losses and help ensure that banking organizations have the ability to lend to households and businesses even in times of stress.

“Even with one-time challenges posed by changes to the tax law, the CCAR results demonstrate that the largest banks have strong capital levels, and after making their approved capital distributions, would retain their ability to lend even in a severe recession,” said Vice Chairman Randal K. Quarles.

When evaluating a firm’s capital plan, the Board considers both quantitative and qualitative factors. Quantitative factors include a firm’s projected capital ratios under a hypothetical scenario of severe economic and financial market stress. Qualitative factors include the strength of the firm’s capital planning process, which incorporates risk management, internal controls, and governance practices that support the process.

This year, 18 of the largest and most complex banks were subject to both the quantitative and qualitative assessments. The 17 other firms in CCAR were subject only to the quantitative assessment. The Board may object to a capital plan based on quantitative or qualitative concerns.

The Board objected to the capital plan from DB USA Corporation due to qualitative concerns. Those concerns include material weaknesses in the firm’s data capabilities and controls supporting its capital planning process, as well as weaknesses in its approaches and assumptions used to forecast revenues and losses under stress.

The Board issued a conditional non-objection to the capital plans of both Goldman Sachs and Morgan Stanley and both firms will maintain their capital distributions at the levels they paid in recent years, which will allow them to build capital over the next year. Each firm’s capital ratios, under the capital plans they originally submitted and with the one-time capital reduction from the tax law changes, fell below required levels when subjected to the hypothetical scenario. This one-time reduction does not reflect a firm’s performance under stress and firms can expect higher post-tax earnings going forward.

The Board also issued a conditional non-objection for the capital plan from State Street Corporation. The stress test revealed counterparty exposures that produced large losses under the hypothetical scenario, which assumes the default of a firm’s largest counterparty under stress. The firm will be required to take certain steps regarding the management and analysis of its counterparty exposures under stress.

The Federal Reserve did not object to the capital plans of Ally Financial, Inc.; American Express Company; BB&T Corporation; BBVA Compass Bancshares, Inc.; BMO Financial Corp.; BNP Paribas USA; Bank of America Corporation; The Bank of New York Mellon Corporation; Barclays US LLC.; Capital One Financial Corporation; Citigroup, Inc.; Citizens Financial Group; Credit Suisse Holdings (USA); Discover Financial Services; Fifth Third Bancorp; HSBC North America Holdings, Inc.; Huntington Bancshares, Inc.; JP Morgan Chase & Co.; Keycorp; M&T Bank Corporation; MUFG Americas Holdings Corporation; Northern Trust Corp.; The PNC Financial Services Group, Inc.; RBC USA Holdco Corporation; Regions Financial Corporation; Santander Holdings USA, Inc.; SunTrust Banks, Inc.; TD Group US Holdings LLC; U.S. Bancorp; UBS Americas Holdings LLC; and Wells Fargo & Company.

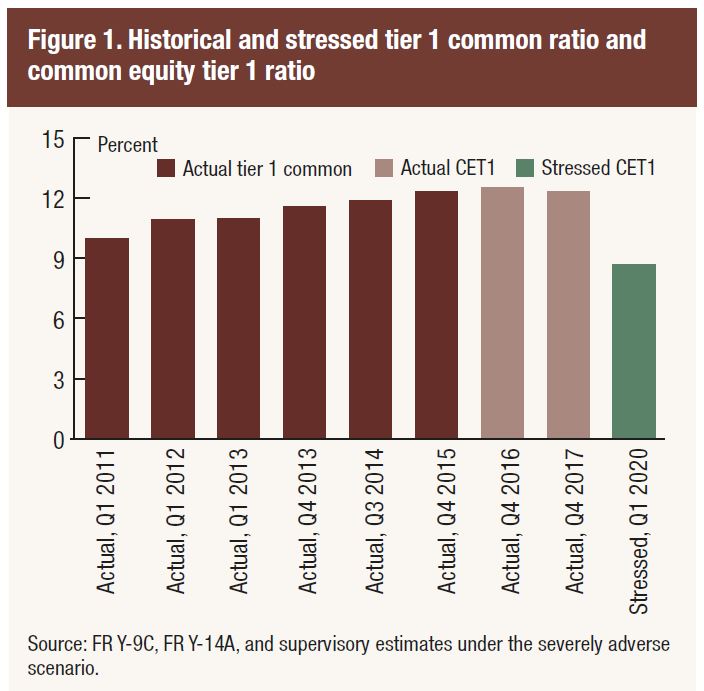

U.S. firms have substantially increased their capital since the first round of stress tests led by the Federal Reserve in 2009. The common equity capital ratio–which compares high-quality capital to risk-weighted assets–of the 35 bank holding companies in the 2018 CCAR has more than doubled from 5.2 percent in the first quarter of 2009 to 12.3 percent in the fourth quarter of 2017. This reflects an increase of more than $800 billion in common equity capital to more than $1.2 trillion during the same period.

The 2018 results from the Federal Reserve bank stress testing are out, and as normal they include the results for all 35 named institutions, a laudable degree of transparency compared with the Australian version!

The Fed says that all 35 Banks will be fine, even if stocks crash by 65%, the volatility index reaches 60, home prices fall 30% and commercial real estate drops 40% all at the same time.

They say that in the aggregate, the 35 firms would experience substantial losses under both the adverse and the severely adverse scenarios but could continue lending to businesses and households, due to the substantial accretion of capital since the financial crisis. So that’s alright then…

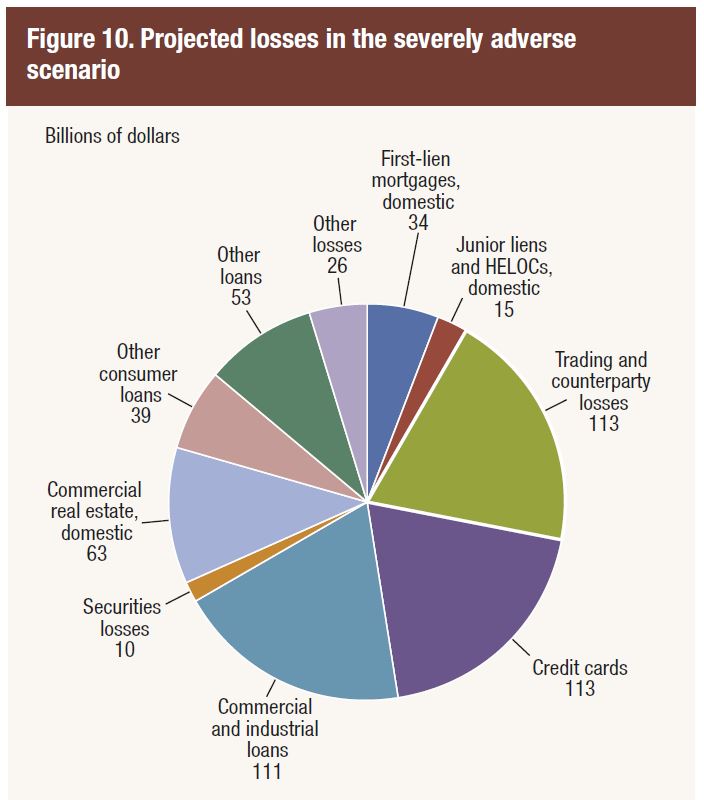

Aggregate losses at the 35 firms under the severely adverse scenario are projected to be US$578 billion and the net income before taxes is projected to be −US$139 billion.

The aggregate Common Equity Tier 1 (CET1) capital ratio would fall from an actual 12.3 percent in the fourth quarter of 2017 to its minimum of 7.9 percent over the planning horizon. Since 2009, the 35 firms have added about $800 billion in common equity capital.

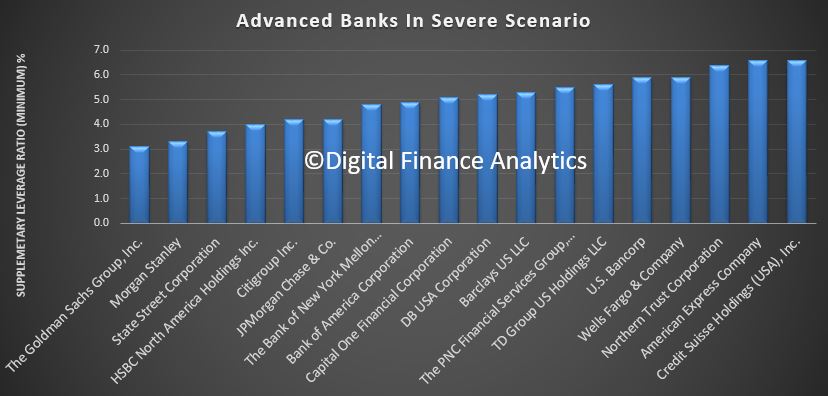

Goldman Sachs ended up with a Tier 1 minimum supplementary leverage ratio (SLR) of 3.1, just exceeding the required 3.0 minimum the Fed set for its annual capital plan, the lowest among participating banks. However, Morgan Stanley was next, at 3.3, then State Street at 3.7. The others were above 4.

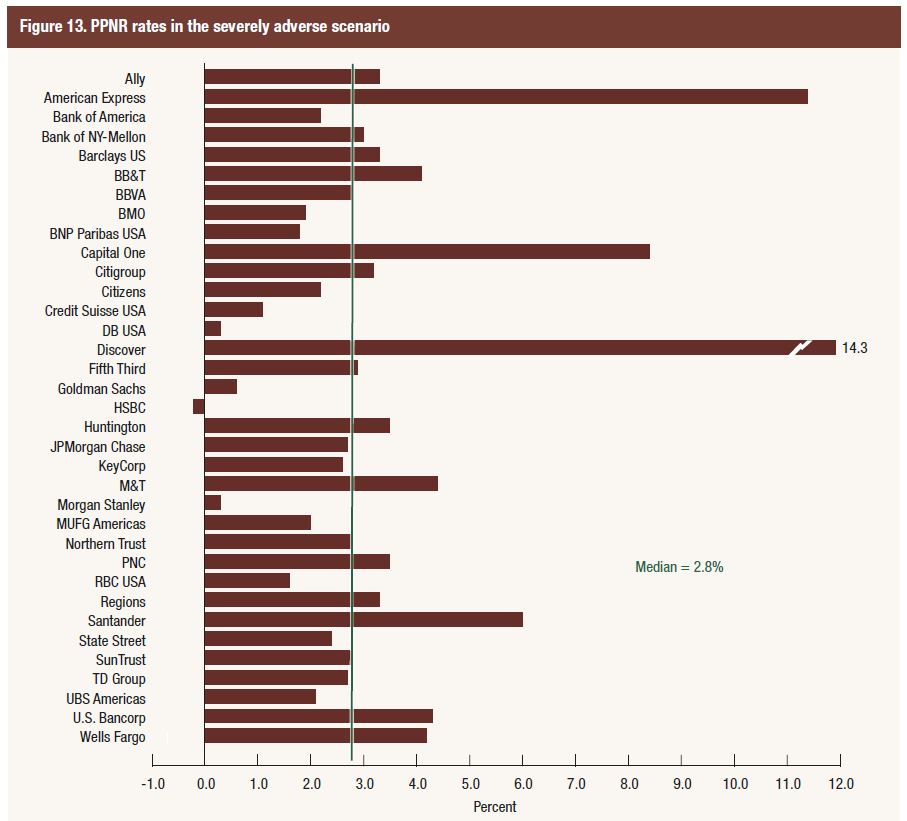

Projected aggregate pre-provision net revenue (PPNR) is $492 billion, and net income before taxes is projected to be −$139 billion.

Some US outposts of European banks are most at risk in this analysis, together with some of the big investment banks.

Some observations.

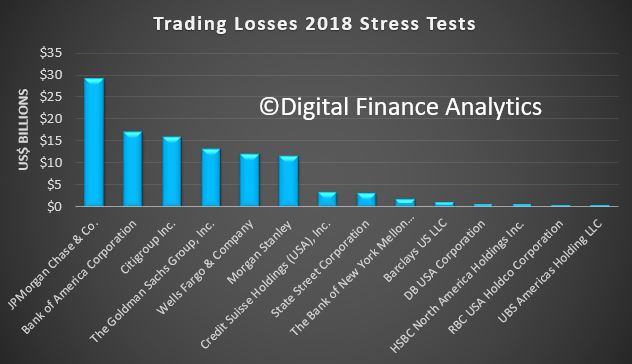

First, losses from trading and counter-party losses were estimated at $133 billion, stemming from 9 institutions, including $17.3 billion from Bank of America Corporation, $16.3 billion from Citigroup, $13.3 billion from Goldman Sachs, $29.4 billion from JP Morgan $29.4 billion, Morgan Stanley $11.7 billion and $12.2 billion from Wells Fargo.

These estimate of losses are calibrated based on historical performance, but given the massive size of the derivatives market, this is just a best guess. We discussed the size and shape of the derivatives market recently in the $37 trillion dollar black hole.

Second, its hard to estimate the potential impact of contagion and freezing of the markets as happened into 2007, as each bank is modelled separately. This begs the question as to whether the system level modelling is robust enough. Especially if one major counter-party fell over during a crisis. 2007 showed the problem when trust across the markets falls, and margins widen significantly.

Third the assumptions are that things will revert to normal conditions in a few years – suggesting this is a “blip type crises.” Some of the smaller banks may have performed better in the tests than they would in the real world.

But the bottom line, according to the FED is that the banks can stand on their own two feet in the mother of all crises, so not excuse for any bail-out then… We will see.

That said, the analysis is the most comprehensive in the world. Its worth reading the detail.

The Federal Reserve has established frameworks and programs for the supervision of its largest and most complex financial institutions to achieve its supervisory objectives, incorporating the lessons learned from the 2007 to 2009 financial crisis and in the period since. As part of these supervisory frameworks and programs, the Federal Reserve assesses whether bank holding companies BHCs with $100 billion or more in total consolidated assets are sufficiently capitalized to absorb losses during stressful conditions, while meeting obligations to creditors and counterparties and continuing to be able to lend to households and businesses.

This annual assessment includes two related programs:

Dodd-Frank Act supervisory stress testing is a forward-looking quantitative evaluation of the impact of stressful economic and financial market conditions on firms’ capital.

The Comprehensive Capital Analysis and Review (CCAR) consists of a quantitative assessment for all firms, and a qualitative assessment for firms

that are LISCC or large and complex firms.

For this year’s stress test cycle (DFAST 2018), which began January 1, 2018, the Federal Reserve conducted supervisory stress tests of 35 firms.

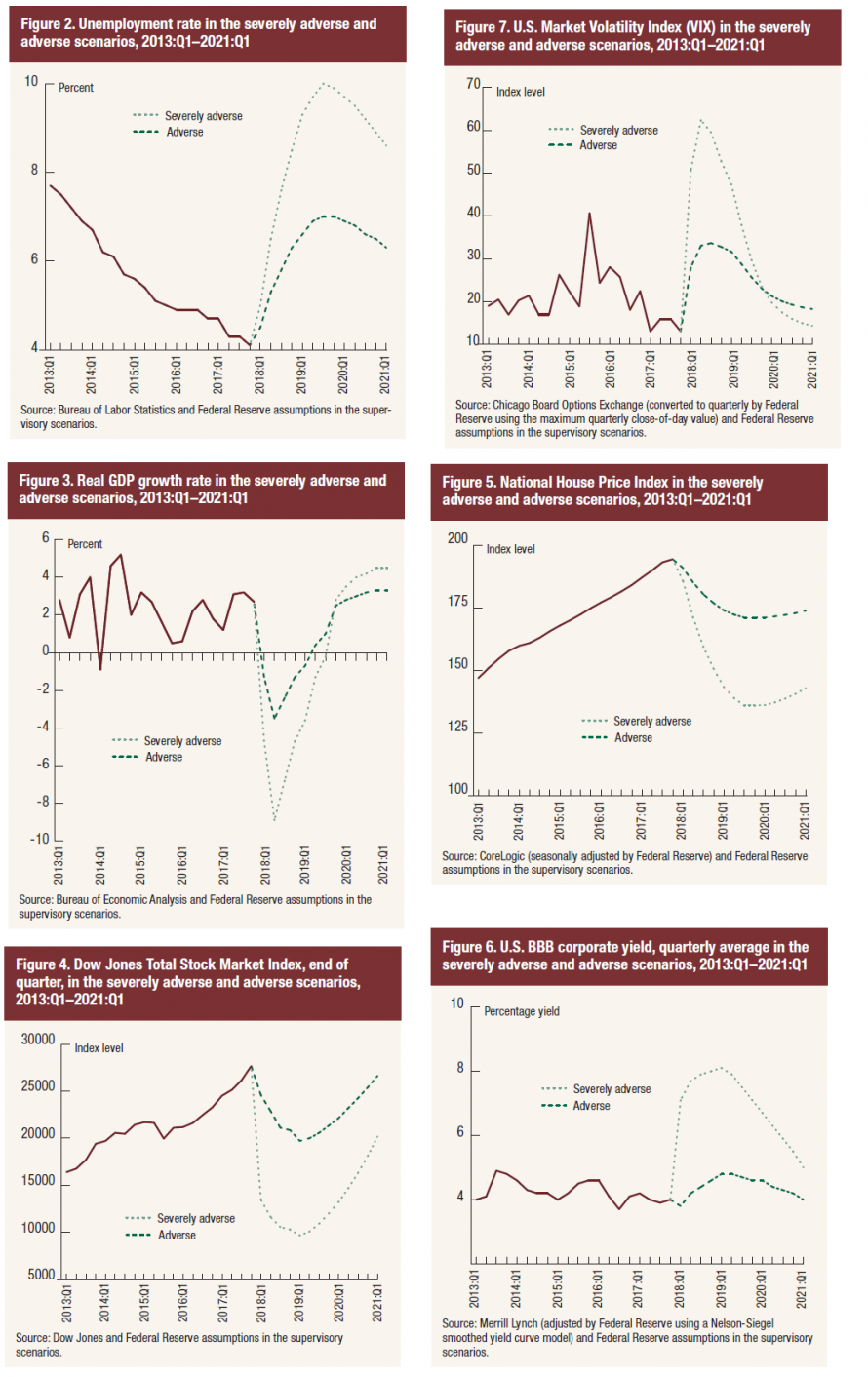

The adverse and severely adverse supervisory scenarios used in DFAST 2018 feature U.S. and global recessions. In particular, the severely adverse scenario is characterized by a severe global recession in which the U.S. unemployment rate rises by almost 6 percentage points to 10 percent, accompanied by a global aversion to long-term fixed-income assets. The

adverse scenario features a moderate recession in the United States, as well as weakening economic activity across all countries included in the scenario.

In conducting its supervisory stress tests, the Federal Reserve calculated its projections of each firm’s balance sheet, risk-weighted assets (RWAs), net income, and resulting regulatory capital ratios under these scenarios using data on firms’ financial conditions and risk characteristics provided by the firms and a set of models developed or selected by the Federal Reserve. For DFAST 2018, the Federal Reserve updated the calculation of projected capital to reflect changes in the tax code associated with the passage of the Tax Cuts and Jobs Act (TCJA) in December 2017. As in past years, the Federal Reserve also enhanced some of the supervisory models to incorporate new data, where available, and to improve model stability and performance. The enhanced models generally exhibit an increased sensitivity to economic conditions compared to past years’ models.

The results of the DFAST 2018 projections suggest that, in the aggregate, the 35 firms would experience substantial losses under both the adverse and the severely adverse scenarios but could continue lending to businesses and households, due to the substantial accretion of capital since the financial crisis. Over the nine quarters of the planning horizon, which for DFAST 2018 begins in the first quarter of 2018 and ends in the first quarter of 2020, aggregate losses at the 35 firms under the severely adverse scenario are projected to be $578 billion. This includes losses across loan portfolios, losses from credit impairment on securities held in the firms’ investment portfolios, trading and counterparty credit losses from a global market shock, and other losses.

Projected aggregate pre-provision net revenue (PPNR) is $492 billion, and net income before taxes is projected to be −$139 billion. In the severely adverse scenario, the aggregate Common Equity Tier 1 (CET1) capital ratio would fall from an actual 12.3 percent in the fourth quarter of 2017 to its minimum of 7.9 percent over the planning horizon. The aggregate CET1 ratio is projected to rise to 8.7 percent by the end of the planning horizon.

In the adverse scenario, aggregate projected losses, PPNR, and net income before taxes are $333 billion, $467 billion, and $125 billion, respectively. The aggregate CET1 capital ratio under the adverse scenario would fall to its minimum of 10.9 percent over the planning horizon.

US Mortgage rates didn’t move much today. That keeps them in line with some of the highest levels in nearly 7 years, though the same could be said for a majority of the days since mid-April.

Higher rates will spill over into the capital markets too. The DOW fell.

Information received since the Federal Open Market Committee met in May indicates that the labor market has continued to strengthen and that economic activity has been rising at a solid rate. Job gains have been strong, on average, in recent months, and the unemployment rate has declined. Recent data suggest that growth of household spending has picked up, while business fixed investment has continued to grow strongly. On a 12-month basis, both overall inflation and inflation for items other than food and energy have moved close to 2 percent. Indicators of longer-term inflation expectations are little changed, on balance.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee expects that further gradual increases in the target range for the federal funds rate will be consistent with sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective over the medium term. Risks to the economic outlook appear roughly balanced.

In view of realized and expected labor market conditions and inflation, the Committee decided to raise the target range for the federal funds rate to 1-3/4 to 2 percent. The stance of monetary policy remains accommodative, thereby supporting strong labor market conditions and a sustained return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its maximum employment objective and its symmetric 2 percent inflation objective. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

Voting for the FOMC monetary policy action were Jerome H. Powell, Chairman; William C. Dudley, Vice Chairman; Thomas I. Barkin; Raphael W. Bostic; Lael Brainard; Loretta J. Mester; Randal K. Quarles; and John C. Williams.